Once in a while, the normally pro-status quo Wall Street Journal surprises me and publishes an article questioning the underlying health of the market.

In BOJ Helps Tokyo Stocks to Soar, it published an internal study indicating that 97% of the days the Bank of Japan invested money in stocks were days that the market either opened lower, or reversed to close lower after initially opening higher. As we noted at the time [see: The Yen Carry Trade Explained], this practice, alone, was responsible for most of equities’ gains between 2011 and 2015.

In yesterday’s Central Banks Embrace Risk in Era of Low Rates, the authors cite a study by Invesco Ltd revealing that 80% of central banks plan to expand their purchases of equities in the coming year.

The bankers’ rationale is that rates are too low in order for them to earn reasonable returns on their excess funds. To those of us who study equity prices day in and day out, that explanation is plainly disingenuous.

As we’ve noted countless times in the past, central banks are increasingly in the business of both directly and indirectly propping up and driving stock prices higher. It has been obvious since late 2008, and has never been more obvious than in the past several several months.

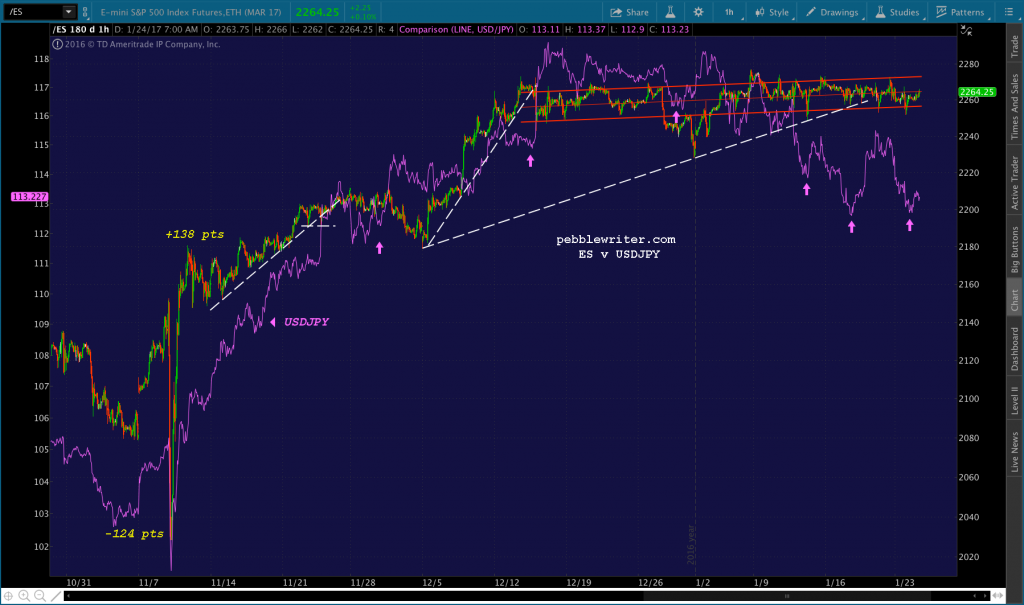

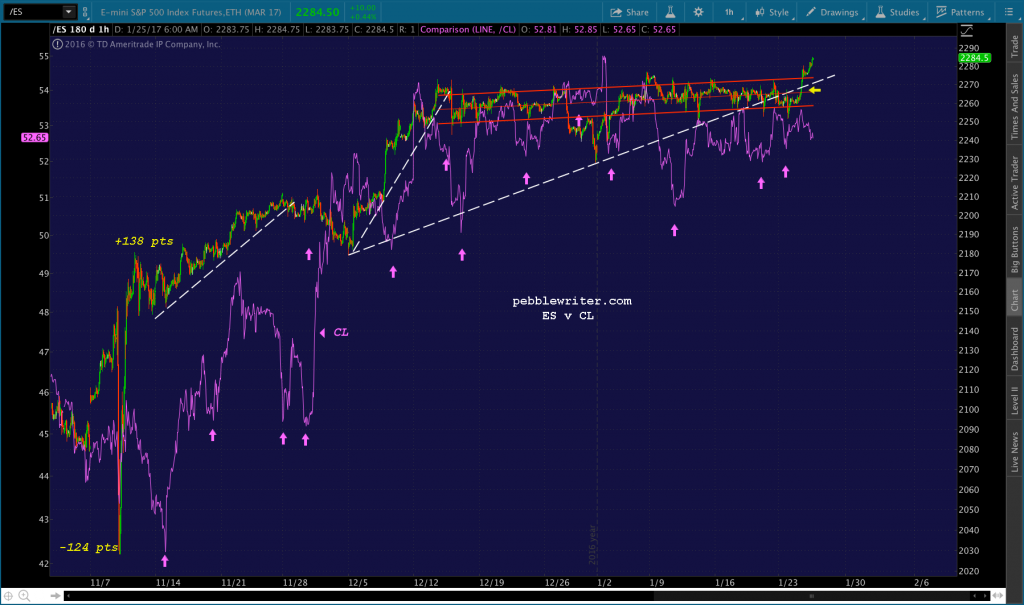

The sudden 138-pt rebound off the 124-pt election night plunge has been credited to a sudden appreciation for all things Trump. And, maybe the man’s policies will ultimately be good for business. However, the charts clearly show that the bulk of the gains came from a sharp spike in USDJPY, an unprecedented takedown of VIX futures and timely pops in the price of CL.

The 17% rally in USDJPY (yen devaluation) between Nov 8 and Dec 15 was punctuated by many smaller spikes (purple arrows) that were timed to support ES every time it threatened to break trend (dashed lines.) These spikes have continued, in maintenance mode, even though USDJPY has topped out.

If anything, VIX’s role has been even more critical to maintaining a rally. Once a reliable indicator of risk in the markets, VIX is now just another tool used by central banks to rescue stocks and build on rallies [see: VIX, Just Another Tool.]

On election night, while ES was plunging 5.7%, VIX fell precipitously. It shed 38% in less than 24 hours, and 53% by Dec 21. Most importantly, it broke down from a rising channel that had established by the last time VIX was beat up (in order to save stocks following the Brexit vote.)

As I write this, VIX is currently off 3.4% in order to maintain stocks in the green after the latest round of decidedly negative economic news (Dec home sales off 2.8%, even after seasonal adjustment and the usual NAR spin.)

As has occurred repeatedly over the past six weeks, we’re left to wonder whether a a channel dating back to 2014 will break down. But, it’s the little hits that VIX takes all day, and especially overnight, that drive the algos which drive the “markets.”

As I wrote yesterday, it’s very difficult to get much downside going if all it takes to prevent it is some 23-year old MIT grad, sitting in a windowless room somewhere, mashing on the SHORT VIX button over and over again until prices stabilize.

The last tool responsible for post-election rally is the price of oil. I know it seems counterintuitive, as higher oil prices bust budgets for consumers and businesses alike. They are also already contributing to higher inflation — which is a factor in driving interest rates higher during a period when all-time low interest rates have been instrumental in inflating asset prices in the first place.

But, rising oil prices proved vital to stocks’ recovery in early 2016. And, they continue to provide important support at key points in time. Today, for instance, they are up 1.25%, working in conjunction with VIX shorting to drive SPX higher.

An unbridled rally in USDJPY or plunge in VIX has little immediate impact on most consumers or businesses. But, since inflation is currently a real threat to bull markets, using oil to drive markets higher requires a deft hand.

More often than not, CL spikes when markets are opening or when intraday resistance is met. As soon as the save/assist is accomplished, it frequently returns to whatever the prevailing trend was. The return trip almost always occurs in the low-volume after hours, when prices are more easily propped up.

It’s usually a safe bet that when SPX is rallying on USDJPY strength or VIX-bashing, CL will be resetting for the next time it’s needed. Again, remaining at higher levels has real and negative repercussions that would ultimately inhibit an ongoing rally — unless it’s one which is built on a reflation theme.

And, that’s where the rubber meets the road, isn’t it?

Official government sources report low unemployment, robust job growth, rising asset prices, etc. And, corporate buybacks and historically low interest rates enable most companies to report steadily increasing EPS.

Yet, real income still languishes below 2000 levels, even for the top 5%.

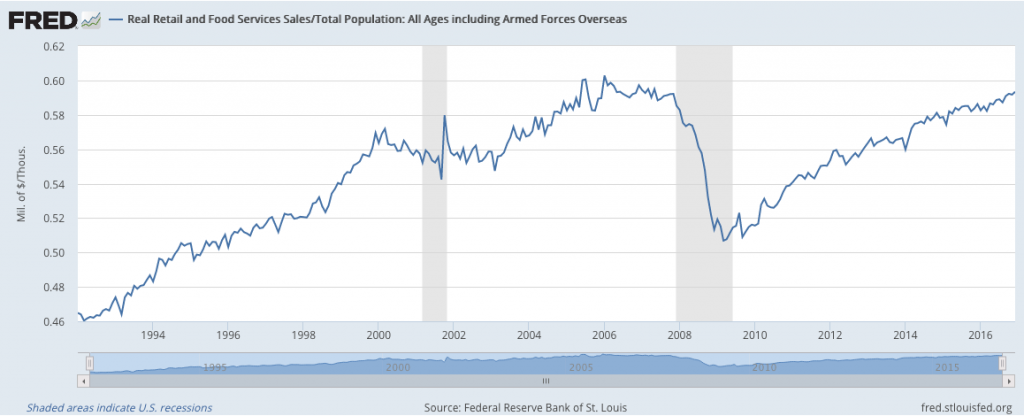

Real per-capita retail sales, even using the government’s questionable inflation data, has yet to reach 2006 levels.

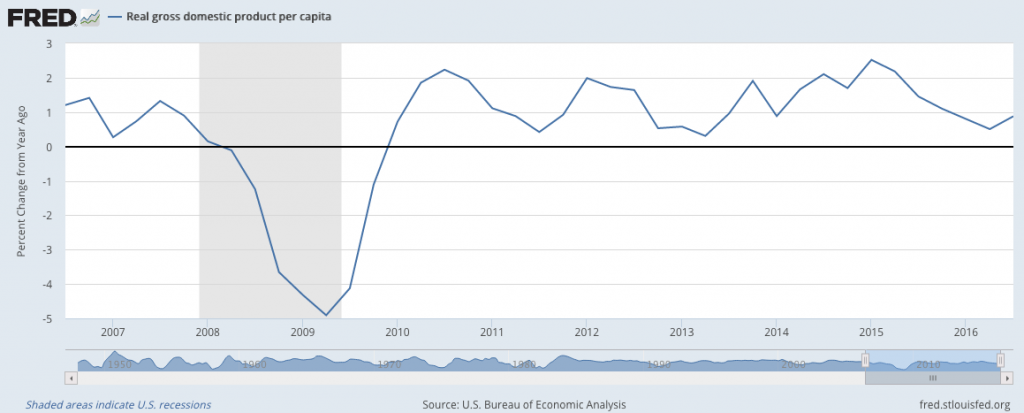

And, real per-capital GDP growth has retreated back below 1%.

Comparing real household income to our ever-expanding debt, and it’s pretty clear we will run into a severe imbalance between income and debt service — especially if Trump follows through on his promise to lower taxes.

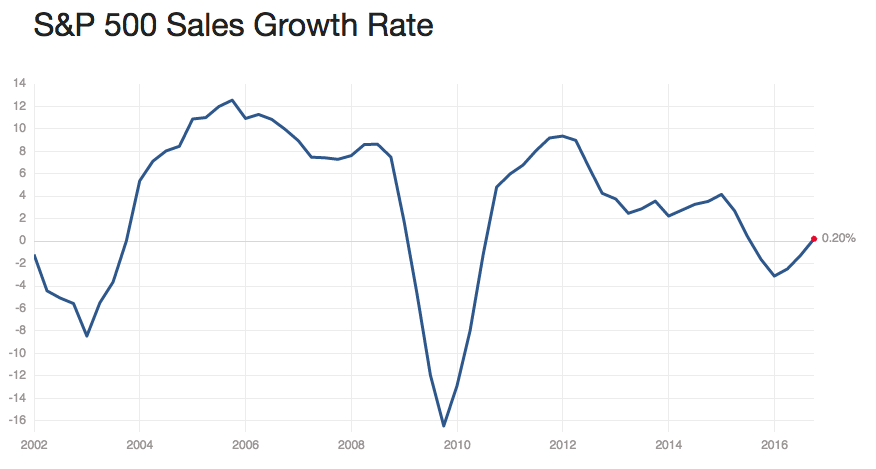

Contrast the above with lethargic corporate revenue growth…

…and, it’s more than a bit alarming that PE ratios are higher than at any time in US history except for just prior to the 1929 and 2000 crashes (we recently topped the 2007 figure.)

Are stock prices sustainable in the face of all the above?

Since I began writing this article at 4am this morning, S&P 500 futures have gained nearly 1% and SPX, itself, just set a new all-time high. Why? VIX is currently off by 4.25%, USDJPY has gained over 1% and CL added 1.7%.

I sat next to a writer/producer friend at our daughters’ basketball game last night. He asked me about the market, and I replied that its recent behavior is more closely related to his business than mine.

A narrative was formed, back in 2008, that enough easy money would paper over the unraveling precipitated by the Great Financial Crisis. For the most part, it worked pretty well. When low interest rates didn’t work, The Powers That Be moved on to zero interest rates and, finally, on to negative interest rates.

They allowed banks and other financials to extend and pretend — shifting focus from enormous balance sheet problems that, in many cases, still exist both here and abroad. They let many of the same players who created the GFC not only continue in business, but looked the other way as old bubbles were re-inflated and new ones were formed.

Central bankers are praying that the narrative will take — that investors will ignore such charts as those above and focus, instead, on the bright, shiny new administration and its promise for the future. If only asset values can climb high enough, so the story line goes, there’s bound to be a trickle down effect that will benefit all — or, at least, allow the bankers to get out whole.

Or, maybe, they have no other cards to play besides depressing the yen and VIX and inflating oil prices. Perhaps, in the confusion, folks won’t notice the yawning gap between nominal and real rates of return that will surely decimate their pensions and imperil their children’s futures.

We’ll review, tomorrow, what options central bankers have. What would it take to keep all the plates spinning? What does it mean for those of us trying to anticipate and capitalize on price trends?

Stay tuned.