You didn’t have to read any further than the title of Freddie Mac’s latest quarterly market report to understand what’s happening in the housing market:

It made me wonder just how important lower rates have been to price appreciation. And, given the Fed’s purported insouciance toward rising rates, how alarmed should we be that rates are spiking higher?

It made me wonder just how important lower rates have been to price appreciation. And, given the Fed’s purported insouciance toward rising rates, how alarmed should we be that rates are spiking higher?

Home buyers usually base purchase decisions on what they can afford (or what they can qualify for), and affordability comes down to purchase price and interest rates. So, it’s a fairly simple process to assess the effect of one on the other.

The National Association of Realtors (NAR) reported that January 2021’s median sales price for existing homes was $303,900 — 14.1% higher than in January 2020 ($266,300) and 21.9% higher than in January 2019 ($249,400.) If you owned a home during this time, congratulations!

If you don’t mind looking a gift horse in the mouth, you might be wondering why prices increased so much. As it turns out, a great deal of the appreciation was due to the historic drop in interest rates.

If you don’t mind looking a gift horse in the mouth, you might be wondering why prices increased so much. As it turns out, a great deal of the appreciation was due to the historic drop in interest rates.

![]() Let’s take a peek under the hood.

Let’s take a peek under the hood.

Freddie Mac reported that the average interest rate on a 30-year fixed conventional mortgage in late January 2021 was 2.73%. Assuming taxes and insurance at the nationwide average and a 20% down payment, the monthly payment (PITI) for a $303,900 home would have been $1,347. A buyer would have needed an annual income of about $57,730 to qualify.

Since median household income in the US is currently about $78,500, the median home price of $303,900 seems reasonable. [Of course, housing is not affordable in many cities — particularly in larger cities and on both coasts.]

Since median household income in the US is currently about $78,500, the median home price of $303,900 seems reasonable. [Of course, housing is not affordable in many cities — particularly in larger cities and on both coasts.]

One year ago, in January 2020, with rates at 3.51% and an income of $57,730, you could have purchased a $275,227 home. And, in January 2019 with rates at 4.46%, you could have purchased a $245,370 home. In other words, the drop in mortgage rates alone accounts for a 23.9% increase in value.  Remember, the NAR reported an increase in the median sales price between January 2019 and January 2021 of 21.9%. So, all else being equal, the increase in value for the median existing home was entirely attributable to the drop in interest rates.

Remember, the NAR reported an increase in the median sales price between January 2019 and January 2021 of 21.9%. So, all else being equal, the increase in value for the median existing home was entirely attributable to the drop in interest rates.

Imagine the effect of all that wealth created out of thin air, and it becomes easier to understand the Fed’s motivation in driving rates to all-time lows.

![]() Of couse, the drop we’ve seen over the past 10 years is nothing compared to the drop over the past 40 years.

Of couse, the drop we’ve seen over the past 10 years is nothing compared to the drop over the past 40 years. Thank you, Fed. All’s well that ends well, right?

Thank you, Fed. All’s well that ends well, right?

Not so fast. If falling rates can result in a sharp increase in value, what about rising rates? As interest rates rise, the income required to qualify for a loan increases. This wouldn’t matter much if your income were stable and you planned on owning your home for, say, the rest of your life.

But, what if you want or need to sell your home in the next few years in the midst of a rising rate environment? If rates were increasing, the average buyer might be less willing or able to pay your asking price. You could hope that your buyer’s income rose enough over the years to compensate for the increase in payment.

But, “hope” isn’t really a strategy, is it? So, let’s do the numbers. Let’s assume rates rise over the next year to where they were one year ago, and that rates two years from now revert back to where they were two years ago.

But, “hope” isn’t really a strategy, is it? So, let’s do the numbers. Let’s assume rates rise over the next year to where they were one year ago, and that rates two years from now revert back to where they were two years ago.

Remember, the Fed’s policy of lowering rates to historic lows would have enriched you by $72,000 over the past two years – not bad, considering you made a down payment of only $61,000 and were able to write off the bulk of your monthly payments.

An increase, on the other hand, to 3.51% by 2022 would reduce the value of your $303,900 home to $275,227 – a 9.4% drop. If you were to sell at that price, you would net only $15,593 after paying a 6% commission and paying off your $243,120 mortgage. In other words, you would have lost 74% of your original down payment.

An increase to 4.46% by 2023 would further slash the value of your home to $245,370 – a 19.3% haircut from its original $303,900 value. After commissions and settling up with the bank, you would owe $12,472. Including the $60,780 down payment, you would have lost a total of $73,252 – 121% of your initial investment. Ouch.

Someone gleefully signing up for a $567,000 mortgage at a rate of 2.73% on a $709,500 house (the average) in Los Angeles because the $2,900 house payment is even lower than their rent payment would do well to consider the repercussions of rising rates.

Someone gleefully signing up for a $567,000 mortgage at a rate of 2.73% on a $709,500 house (the average) in Los Angeles because the $2,900 house payment is even lower than their rent payment would do well to consider the repercussions of rising rates.

If rates simply reverted to 2019’s 4.46% when they sold, they’d need to write a $29,000 check at closing – a bitter pill after waving goodbye to their $142,000 down payment.

Is such an outcome in the cards? I doubt it. As we’ve discussed countless times over the years, the Fed needs higher interest rates and inflation like a fish needs a bicycle. While inflation is set to spike much higher over the next 4-6 weeks due to sharply higher oil/gas prices…

…I have little doubt that oil/gas prices have already begun their collapse. It’s one of the very effective ways central bankers have been able to quickly bring inflation back under control in the past. Yes, we’ve seen this movie before.

…I have little doubt that oil/gas prices have already begun their collapse. It’s one of the very effective ways central bankers have been able to quickly bring inflation back under control in the past. Yes, we’ve seen this movie before.

Jay Powell insists the Fed’s not worried about higher inflation and higher interest rates. That makes them either liars or fools. And, I sure don’t take them for fools.

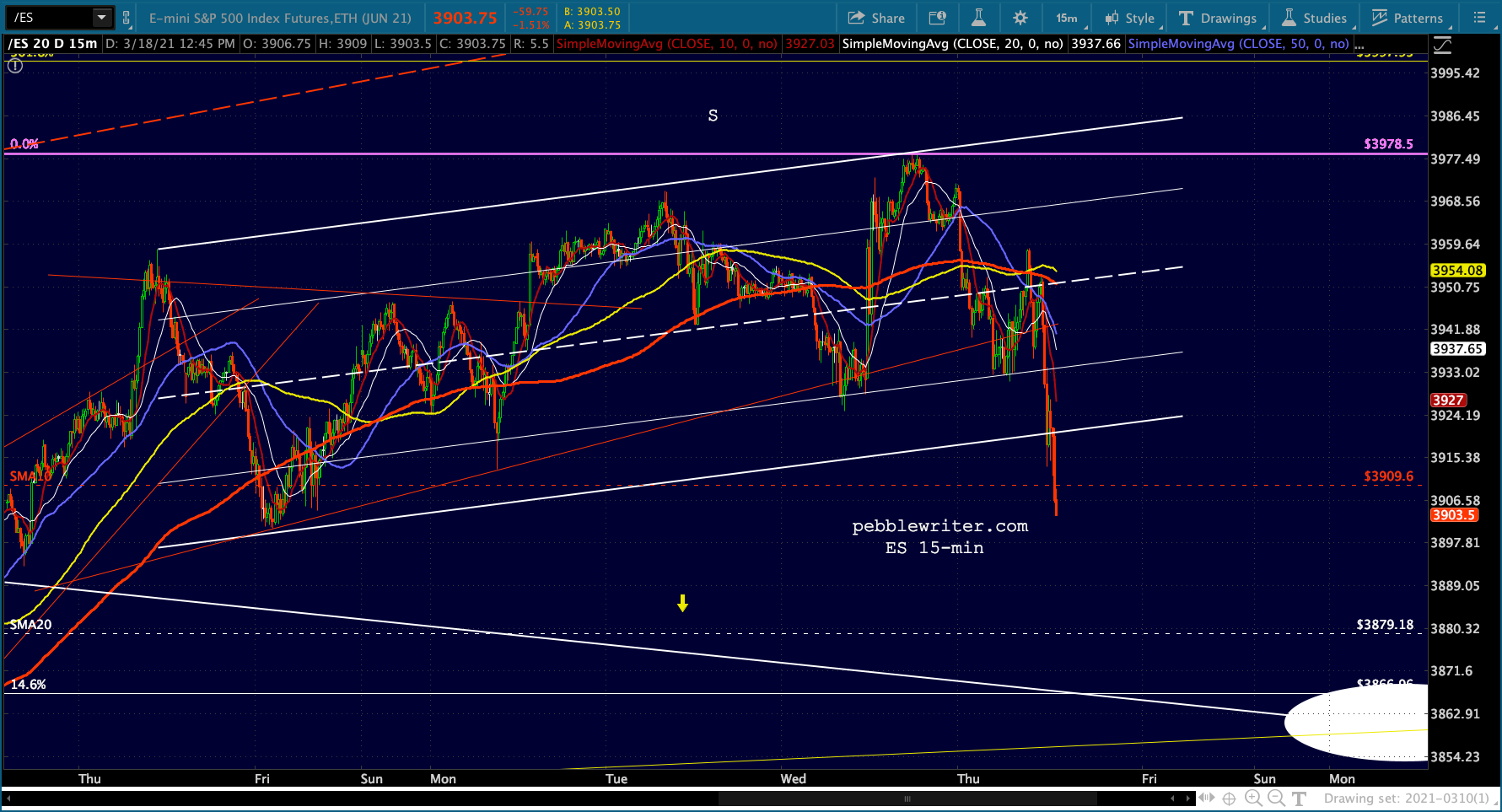

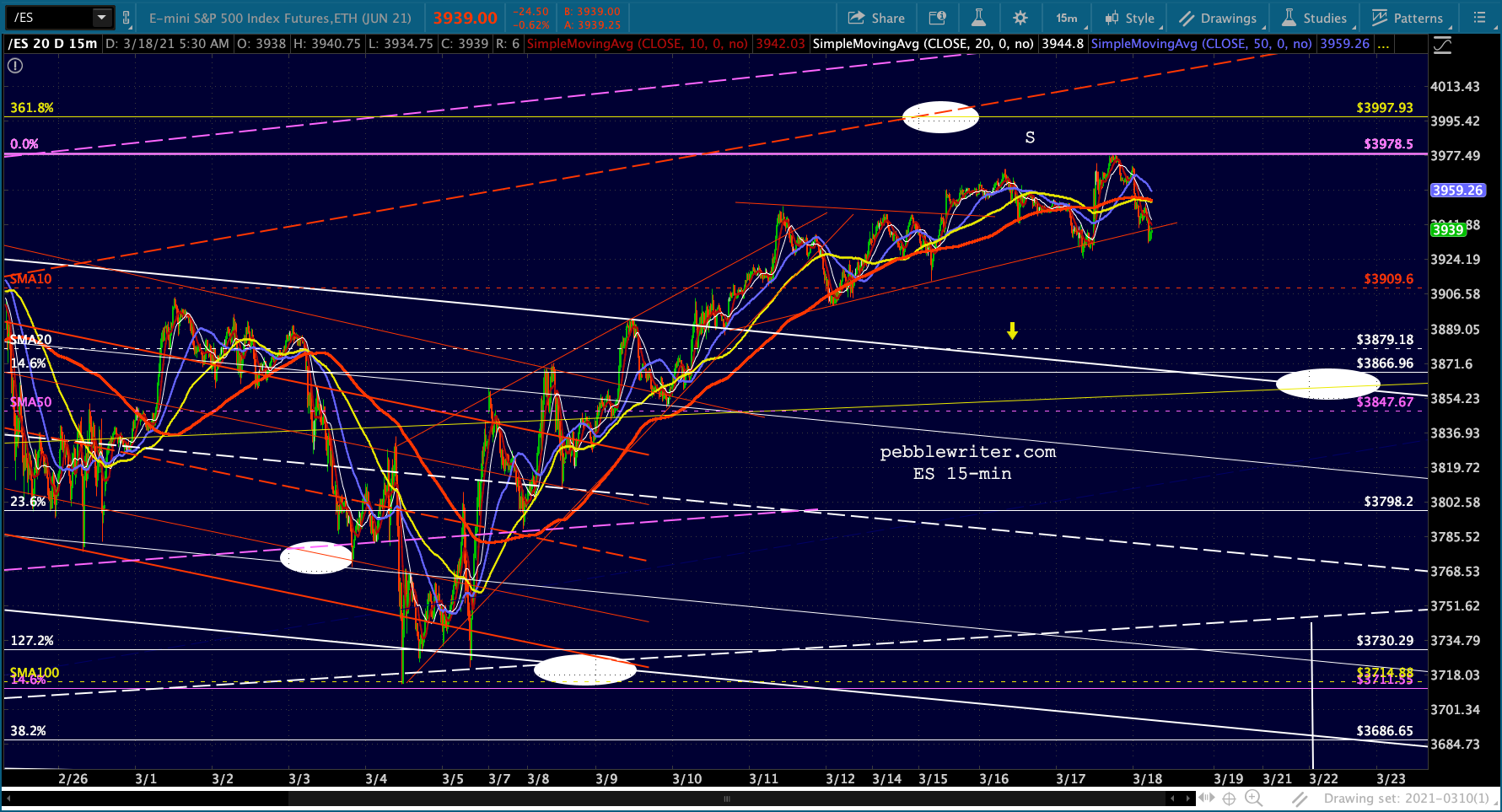

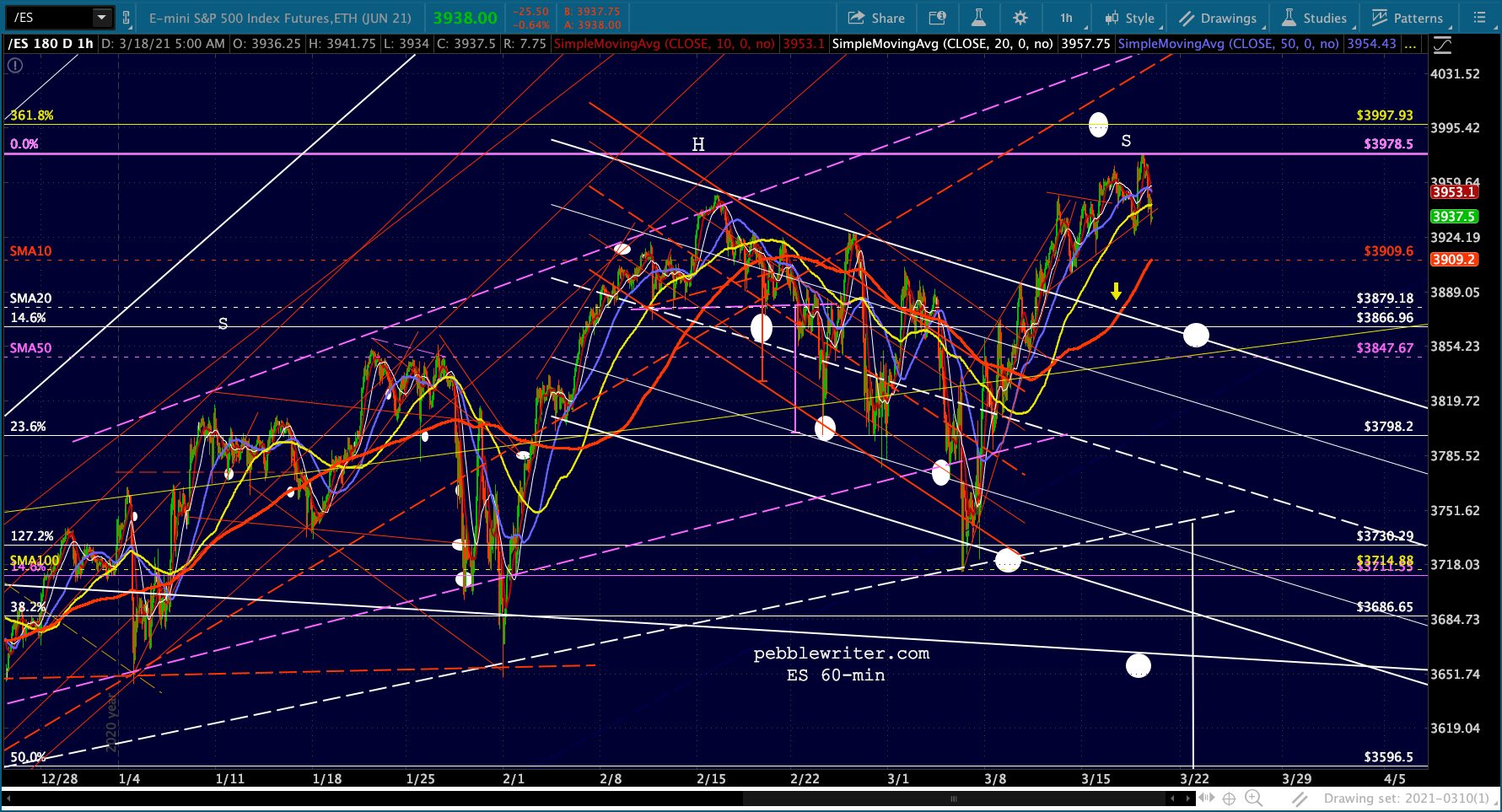

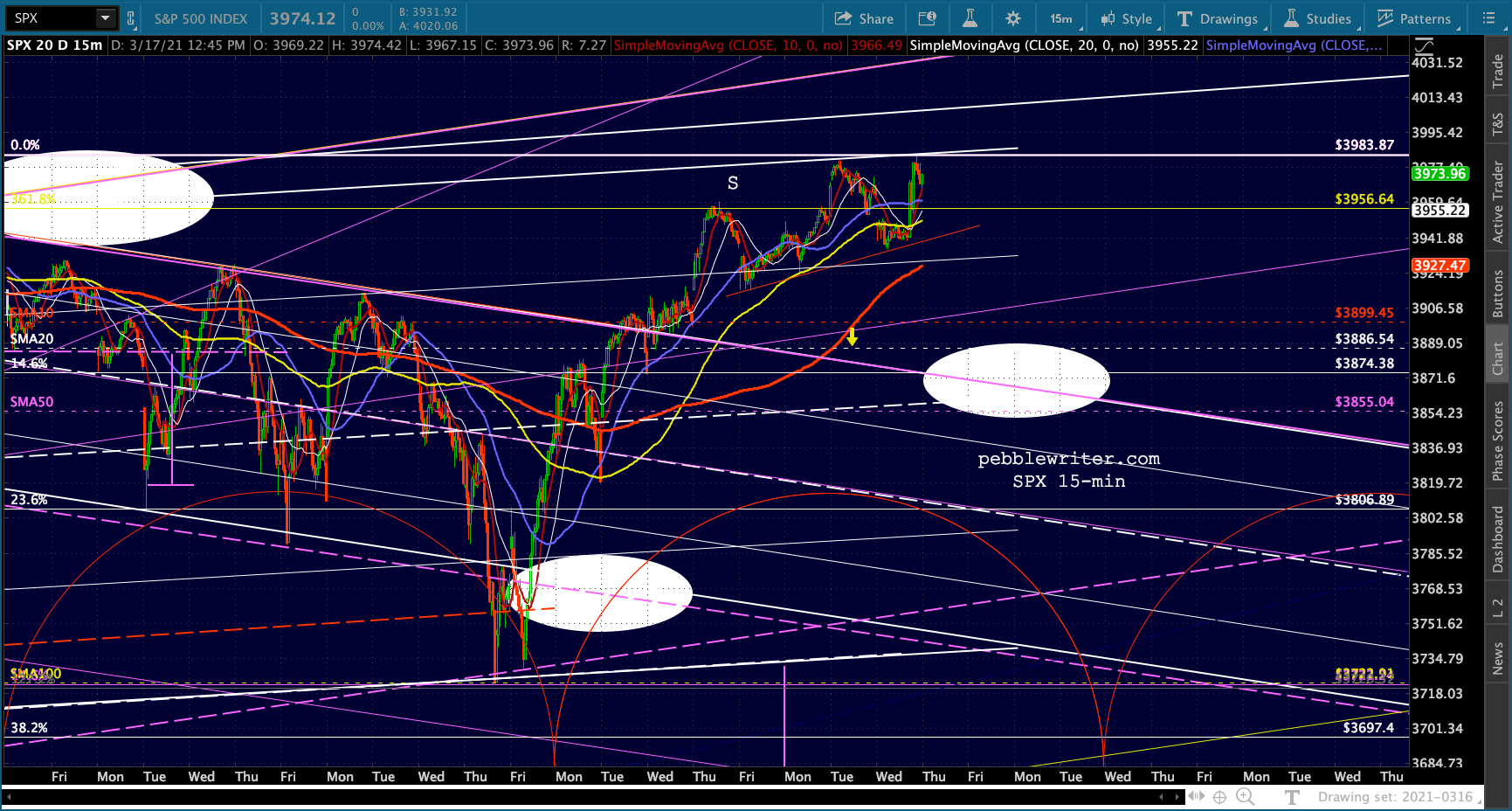

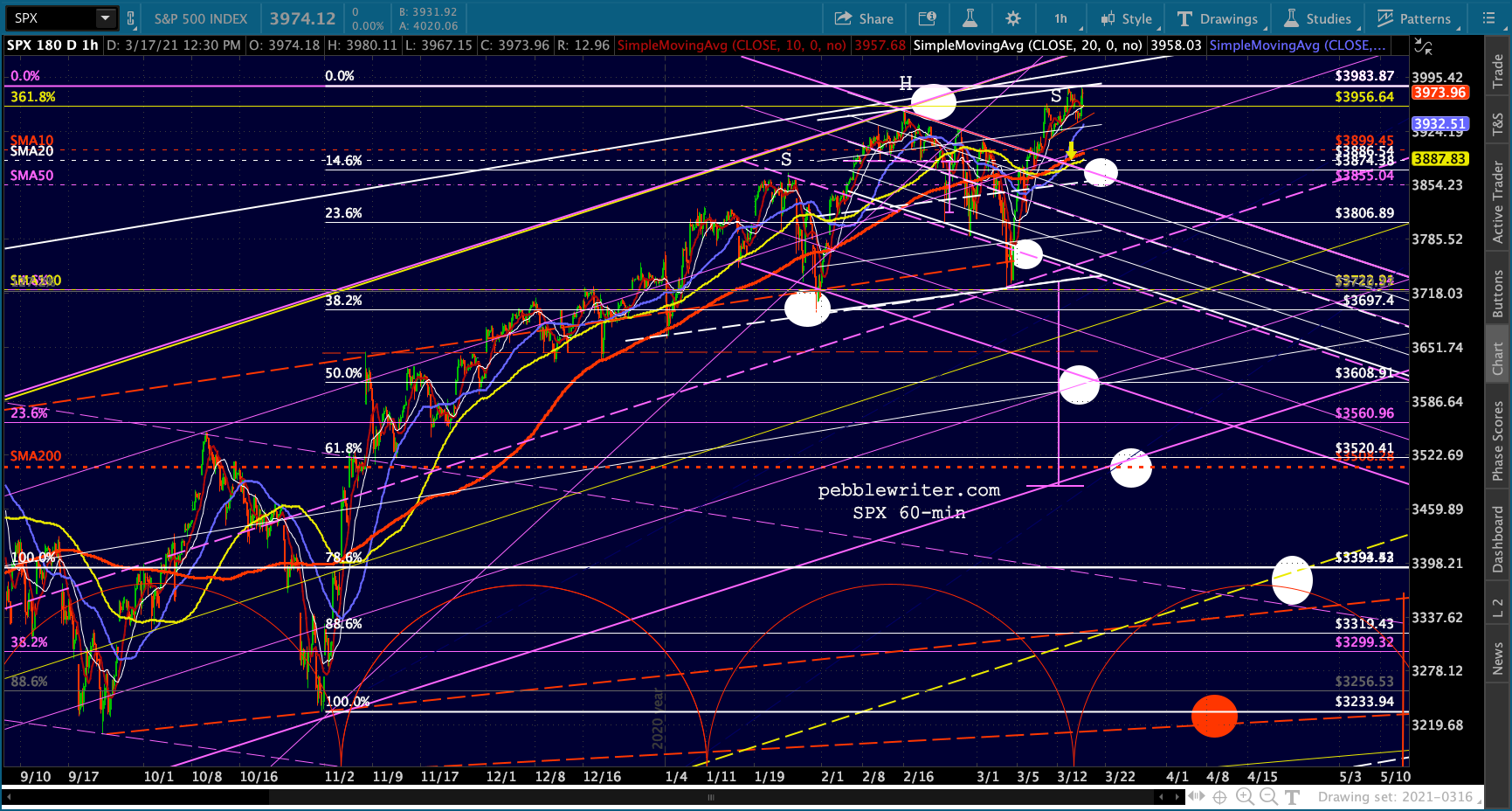

continued for members…Futures have had a while to think about the Fed’s stance, and aren’t feeling that bullish at the moment. ES seems almost certain to break below its rising red TL and backtest at least the SMA10 at 3909 and probably the broken white channel at 3866ish.

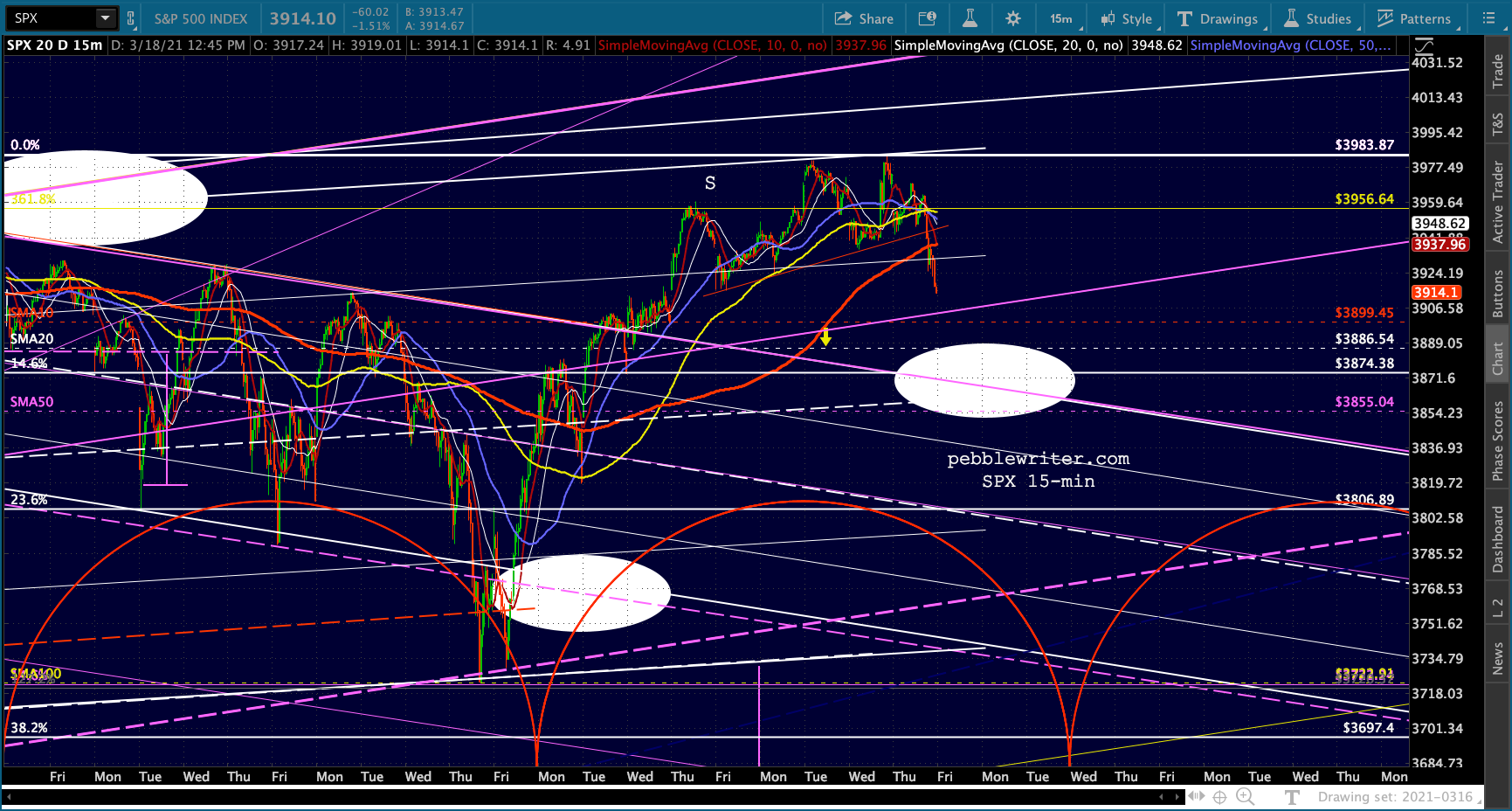

Neither ES nor SPX officially busted their H&S Patterns yesterday – though SPX came very close.

Neither ES nor SPX officially busted their H&S Patterns yesterday – though SPX came very close.

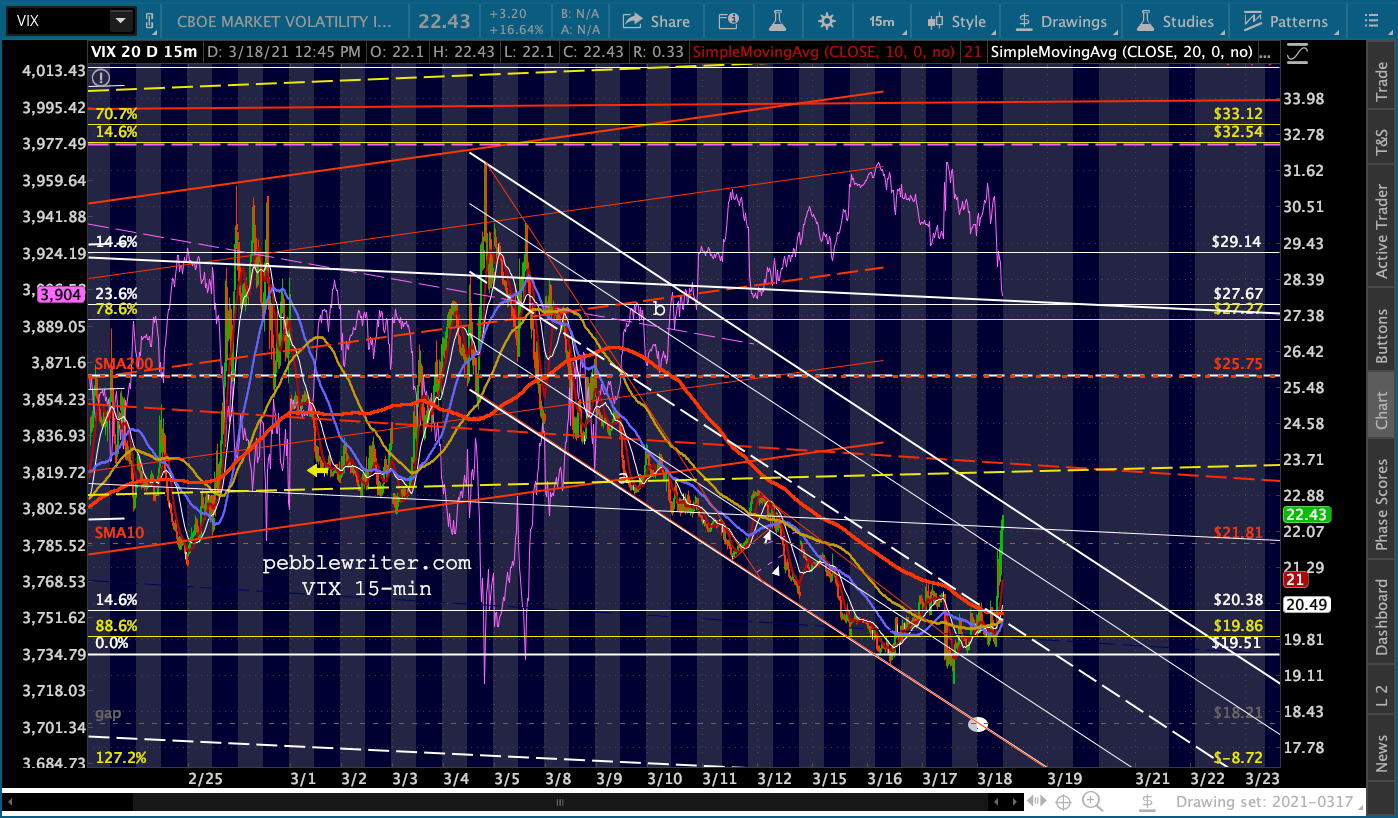

VIX will likely continue to play an important role. Today is the day the falling white channel intersects the gap at 18.21.

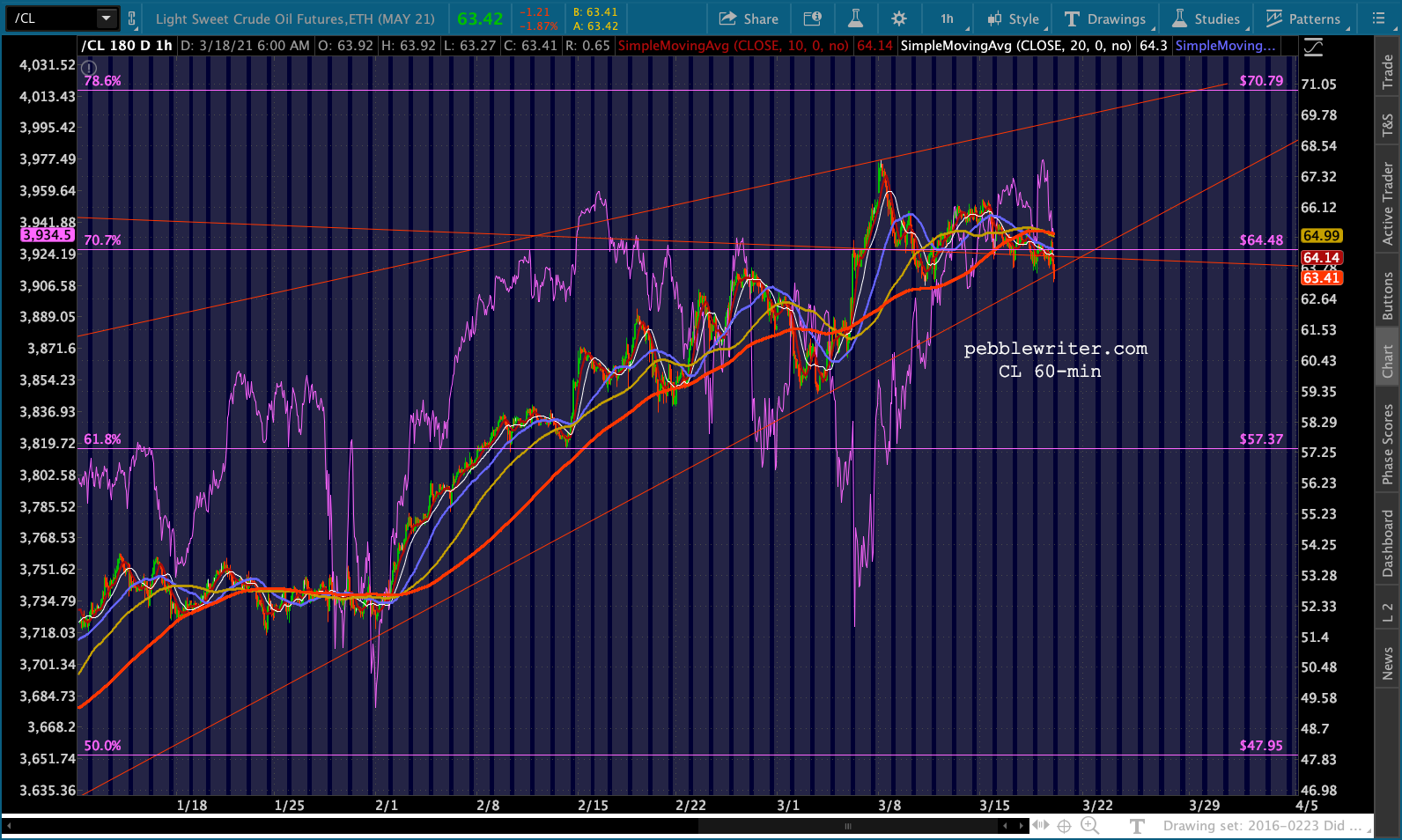

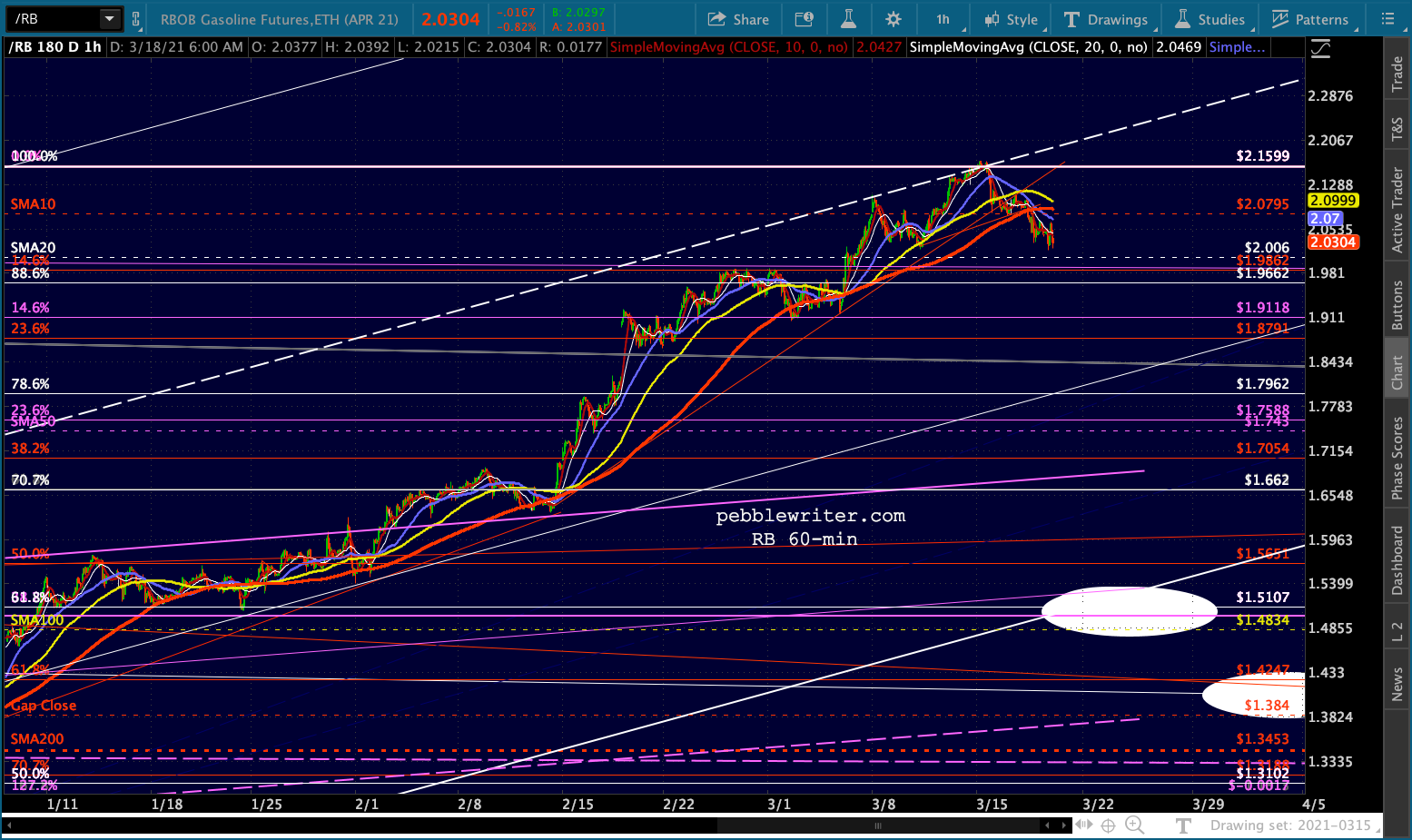

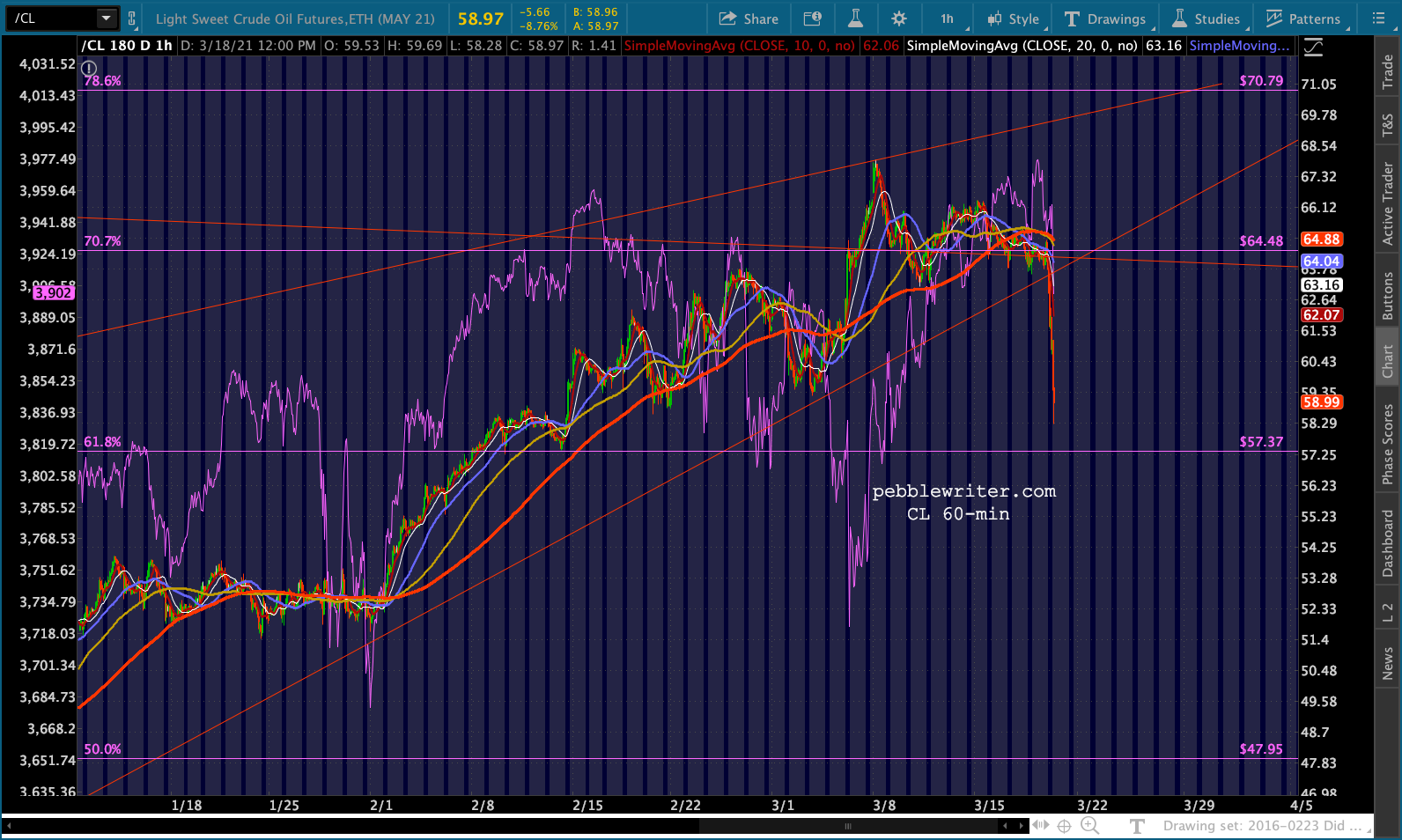

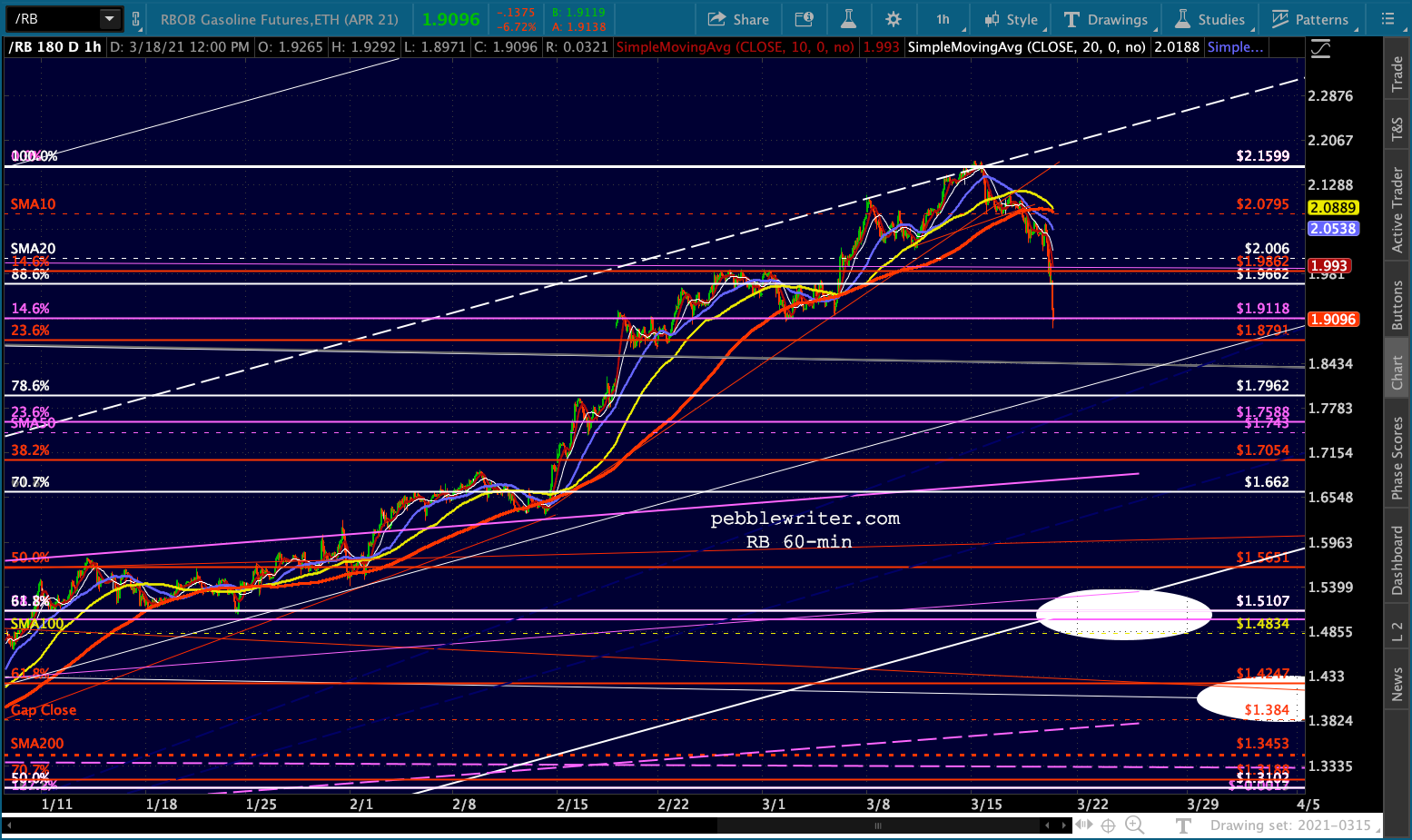

VIX will likely continue to play an important role. Today is the day the falling white channel intersects the gap at 18.21.  Note that CL and RB’s breakdowns are officially underway.

Note that CL and RB’s breakdowns are officially underway.

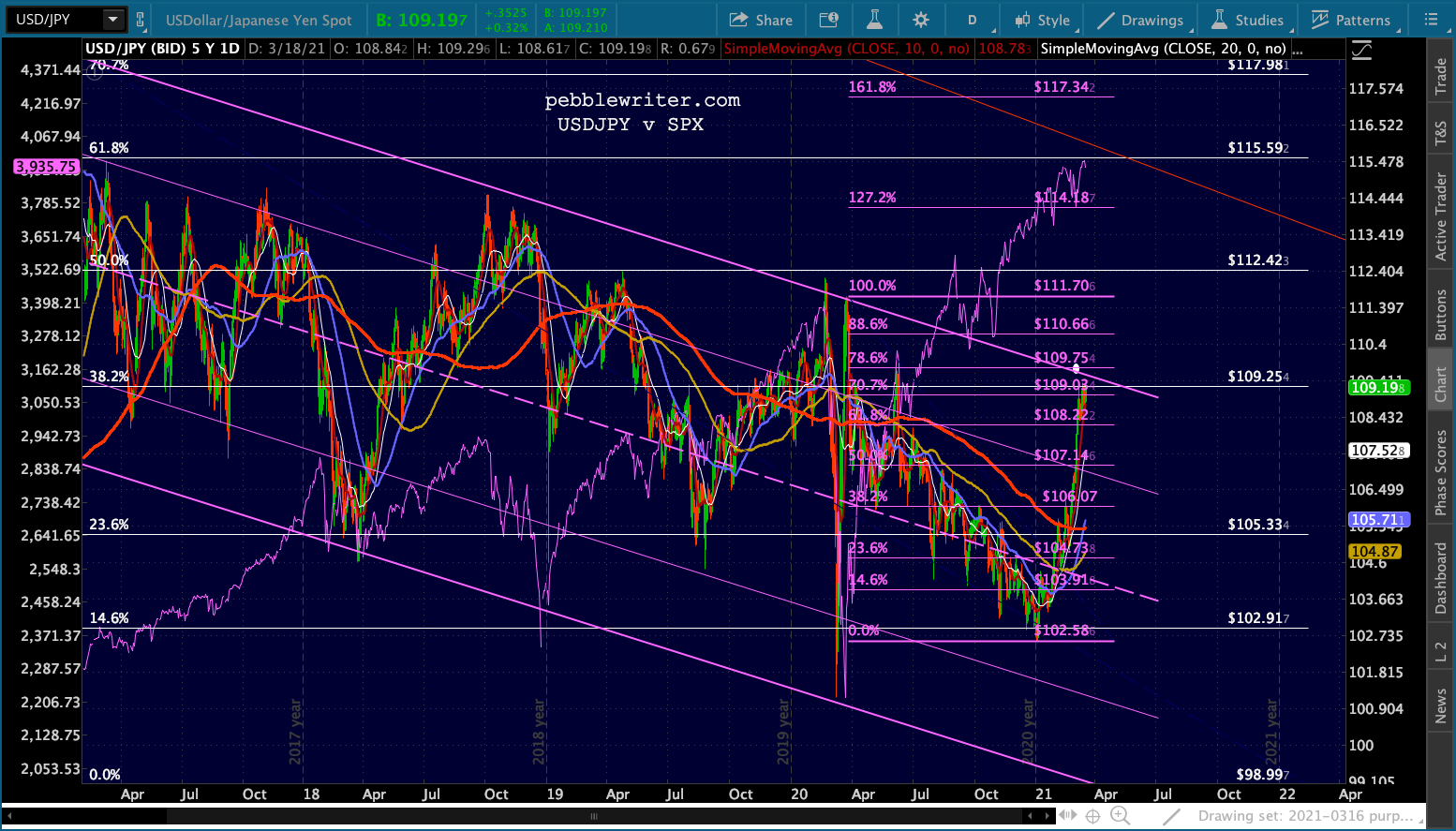

And, USDJPY is still poised to pick up the slack if stocks are rocked by the declines in oil/gas.

And, USDJPY is still poised to pick up the slack if stocks are rocked by the declines in oil/gas.

If we zoom out a little, we can see where a breakout might go. The Fib pattern below was instrumental in helping us identify critical turning points back in 2015 (remember the yellow .618 Fib at 120.11?)

If we zoom out a little, we can see where a breakout might go. The Fib pattern below was instrumental in helping us identify critical turning points back in 2015 (remember the yellow .618 Fib at 120.11?)

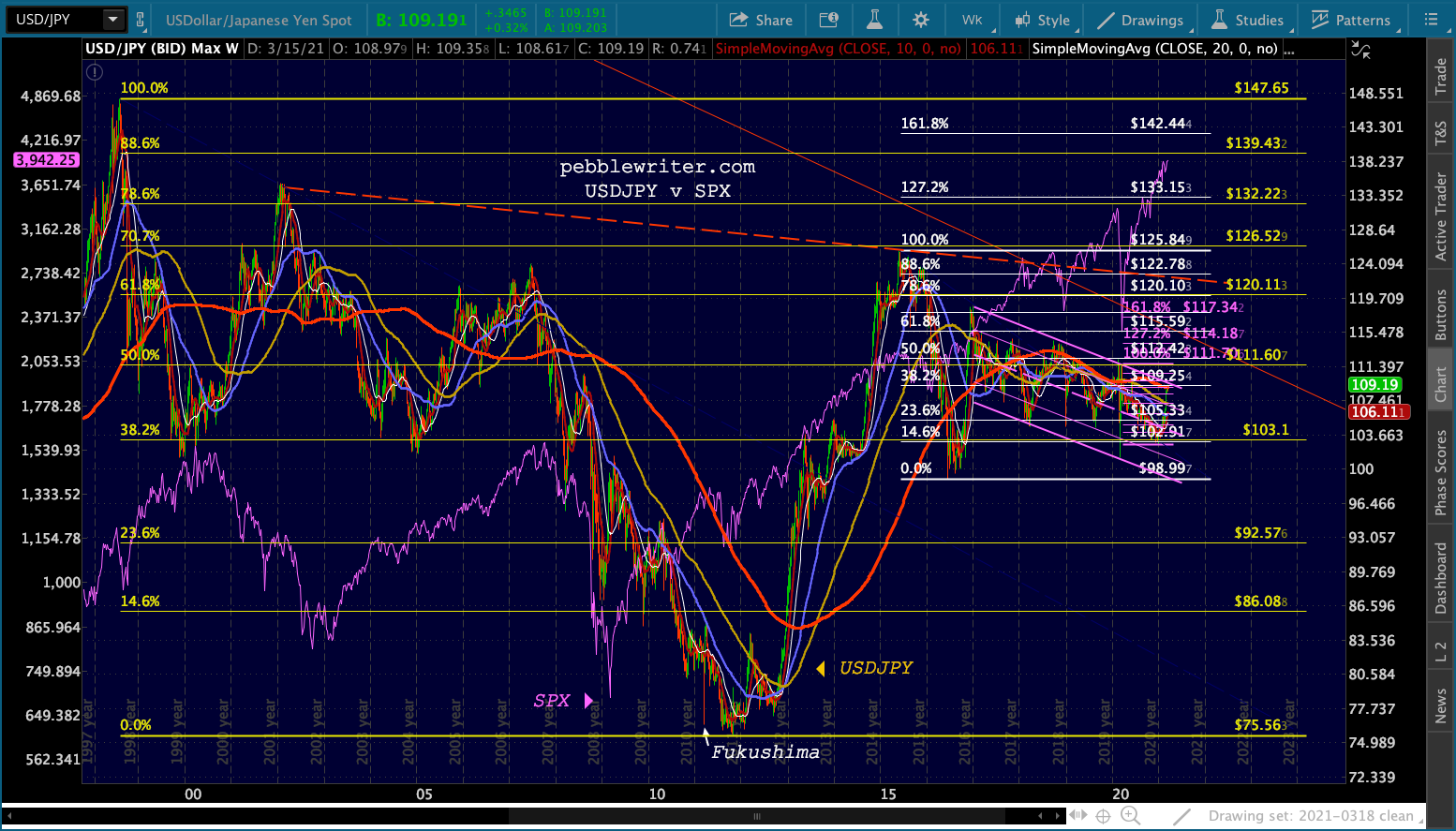

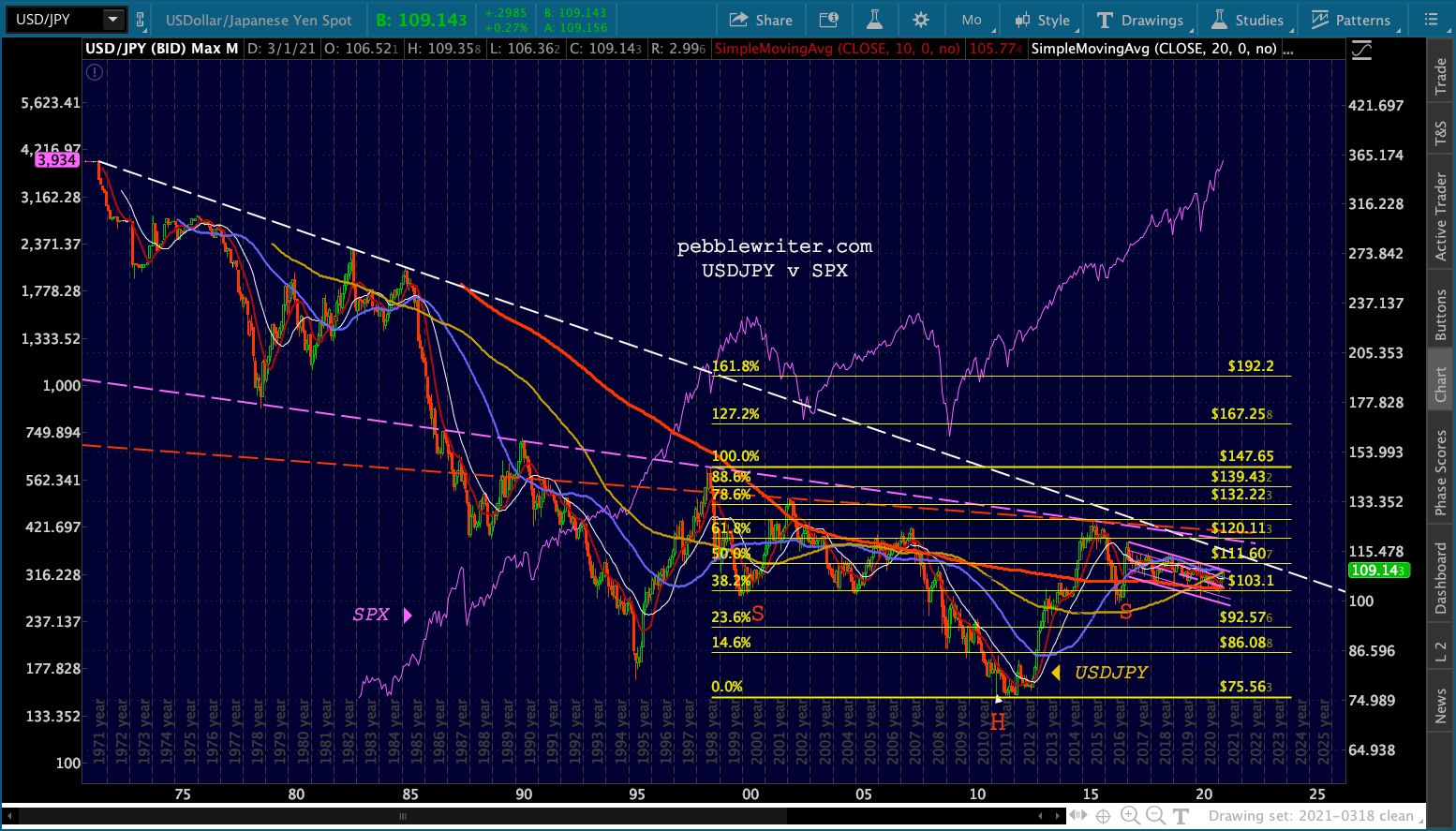

My eye is immediately drawn, however, to the dashed red TL and the Inverted H&S Pattern it suggests. I might be tempted to leave it at this and focus on the potential for that pattern to complete at 120.11ish. But, if we zoom out a little more, we can see a much more interesting TL – shown below in purple and an extemely interesting TL – shown in white. I’ll flesh these out in a separate post – hopefully later today.

But, if we zoom out a little more, we can see a much more interesting TL – shown below in purple and an extemely interesting TL – shown in white. I’ll flesh these out in a separate post – hopefully later today.

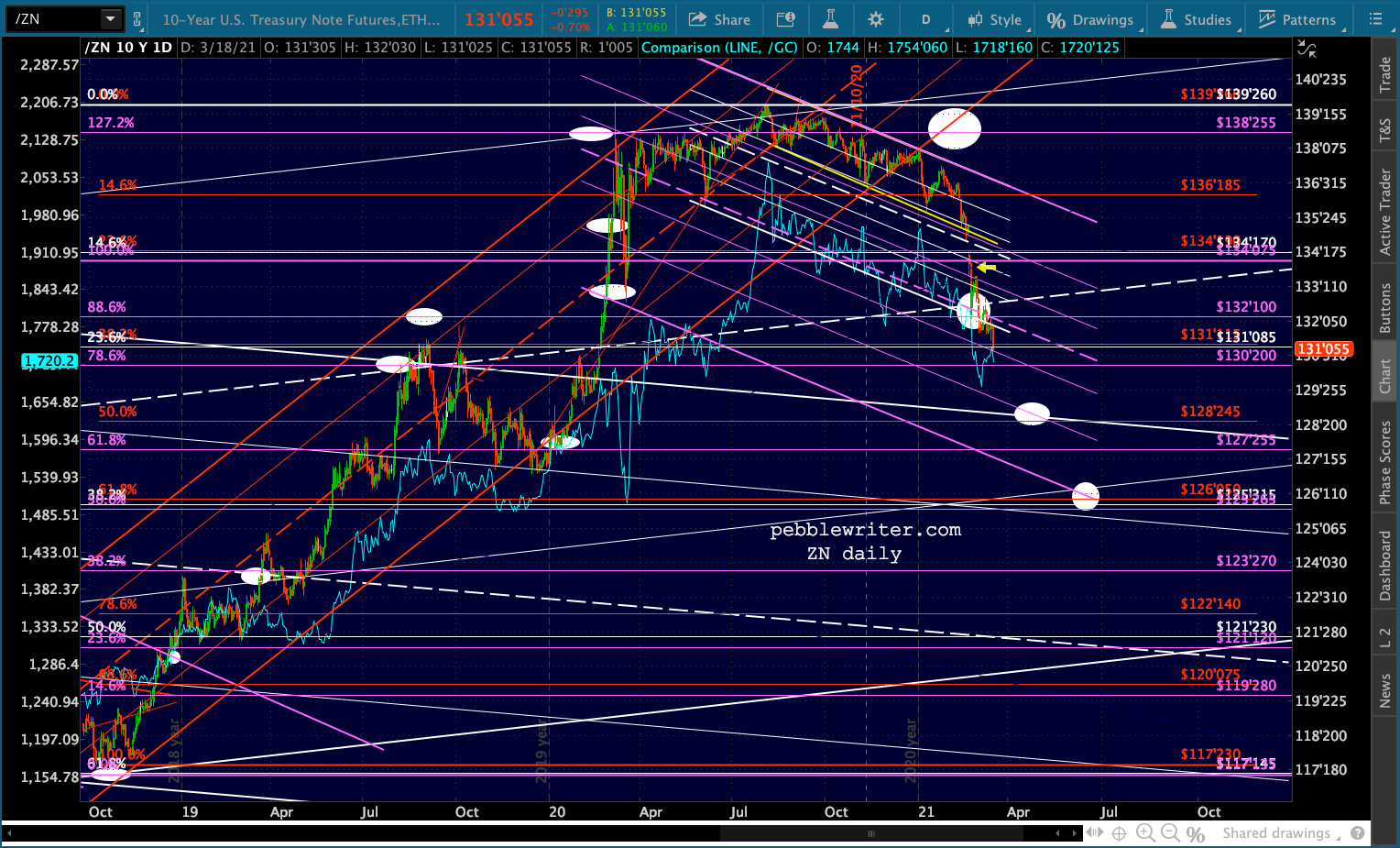

The last chart I’d suggest folks focus on today is the 10Y, which is fast approaching the broken channel backtest at 128’245.

The last chart I’d suggest folks focus on today is the 10Y, which is fast approaching the broken channel backtest at 128’245. More later…

More later…

UPDATE: 3:45 PM

The chickens…

…are coming home to roost.

…are coming home to roost.