Stocks are off slightly on the huge jobs miss (+235K versus +800K consensus, +1,053 prior), raising the question of whether even this much bad news can be good news for stocks. In this “heads bulls win, tails bears lose” market, the Fed remains the ultimate arbiter of market direction – based not only on the massive infusions of liquidity and interest rate suppression, but the deliberate and calculated trampling of volatility at critical levels of support/resistance.

In this “heads bulls win, tails bears lose” market, the Fed remains the ultimate arbiter of market direction – based not only on the massive infusions of liquidity and interest rate suppression, but the deliberate and calculated trampling of volatility at critical levels of support/resistance.

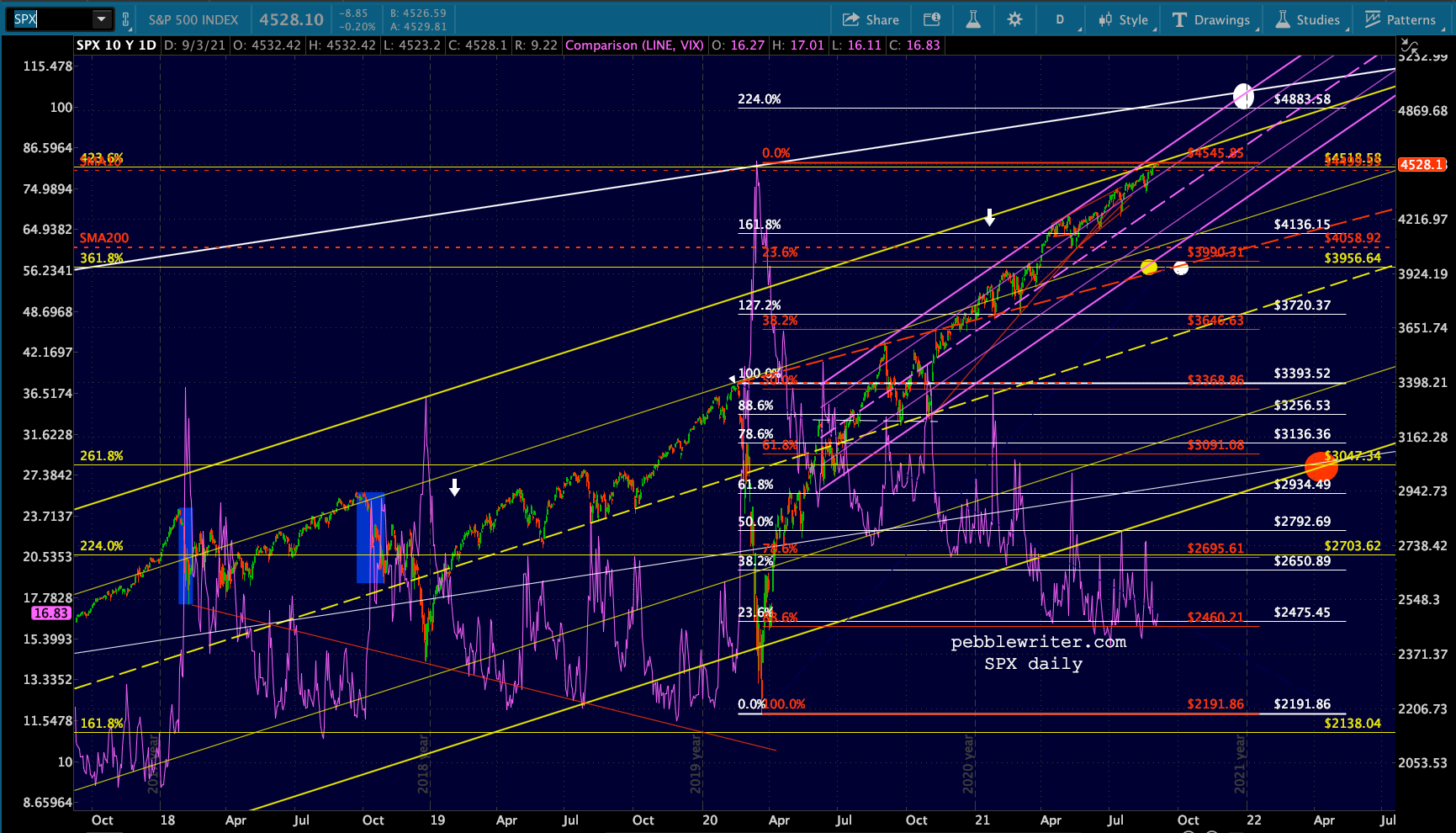

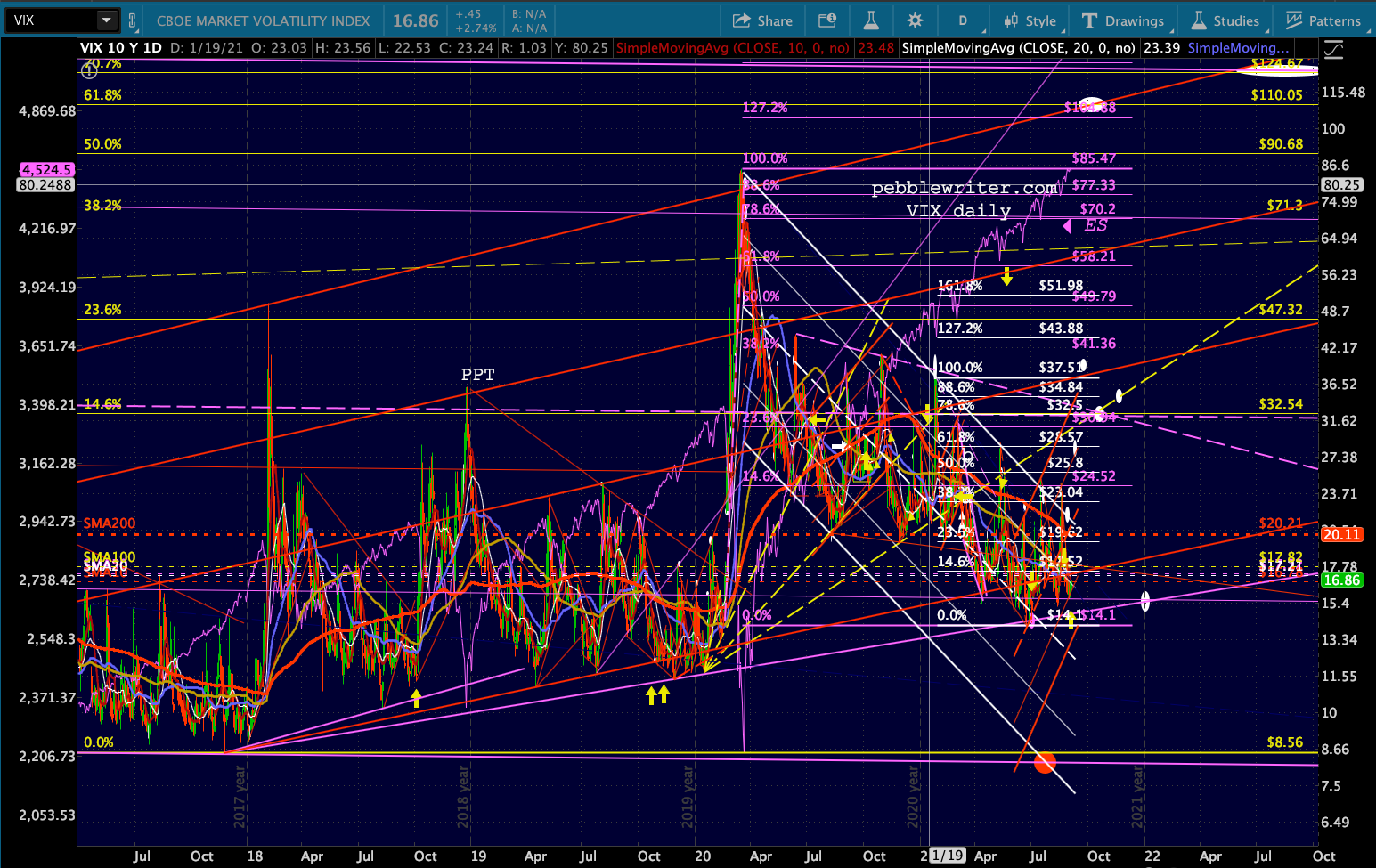

Every few months, we roll out this chart which clearly shows the relationship between key breakouts in SPX versus breakdowns in VIX. Despite many sharp spikes higher, VIX has been threatening to break below the dashed purple trend line for the past three years.

It seems like a good time to take a look at the big picture.

It seems like a good time to take a look at the big picture.

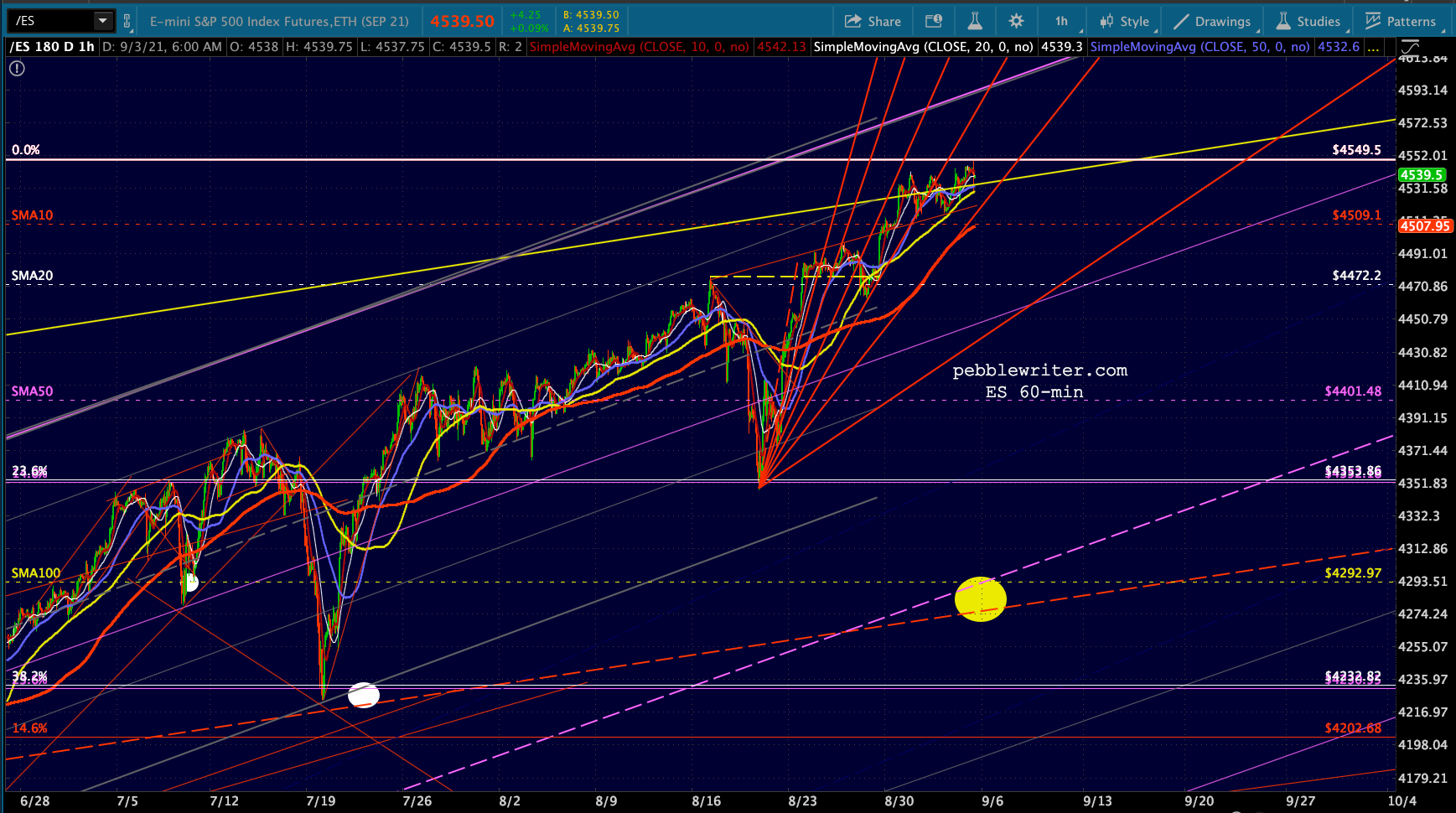

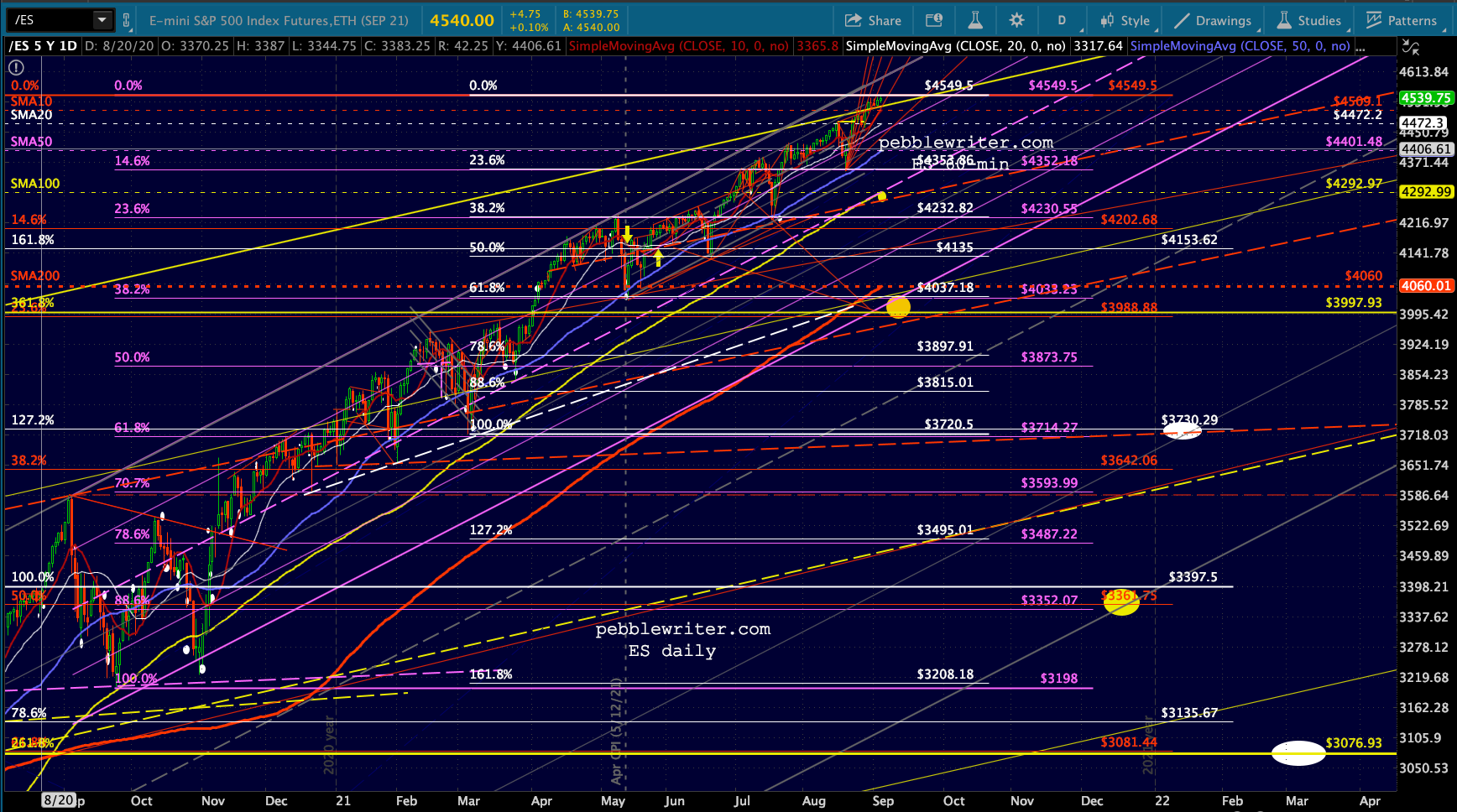

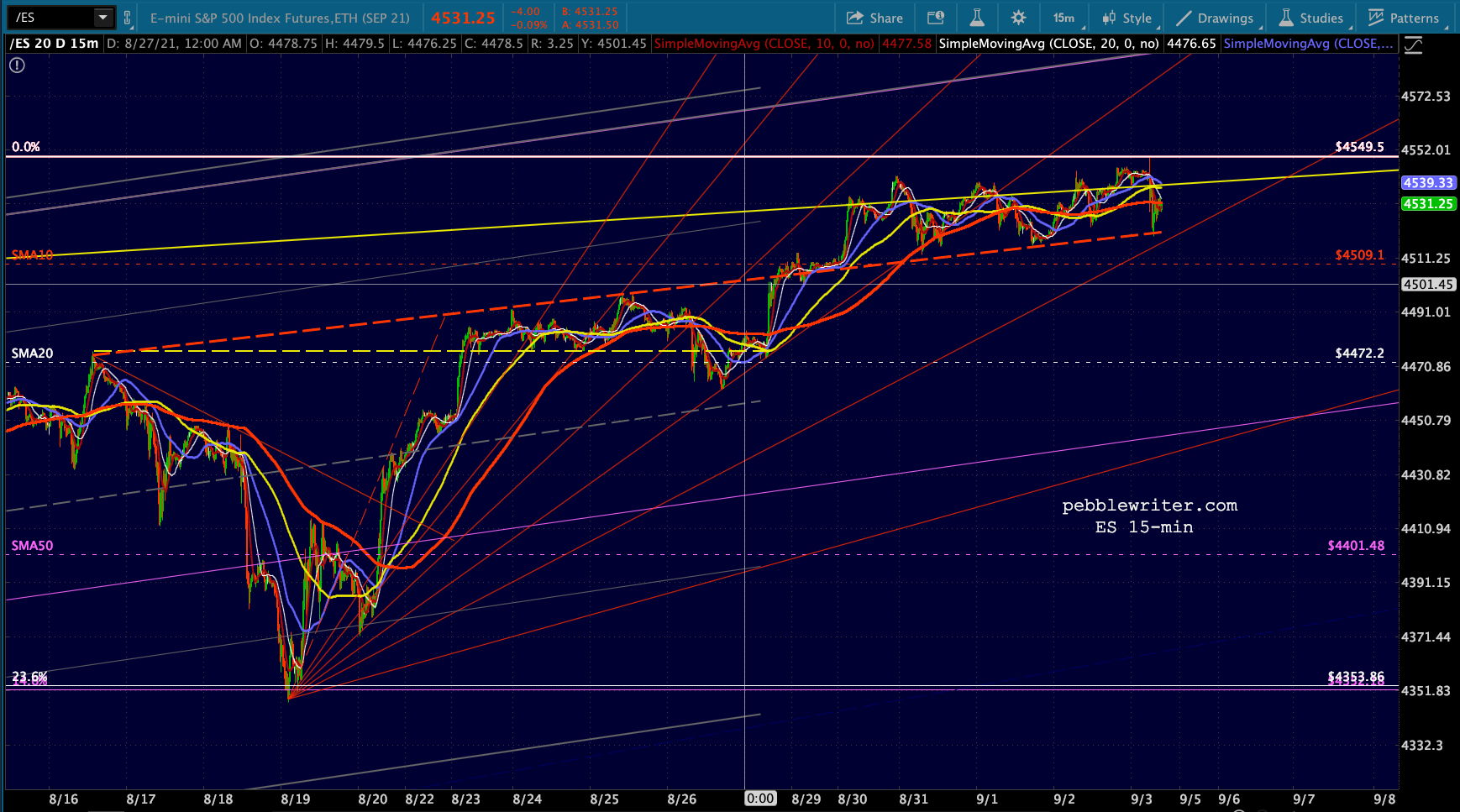

continued for members…First, a quick look at where we are in ES and SPX…

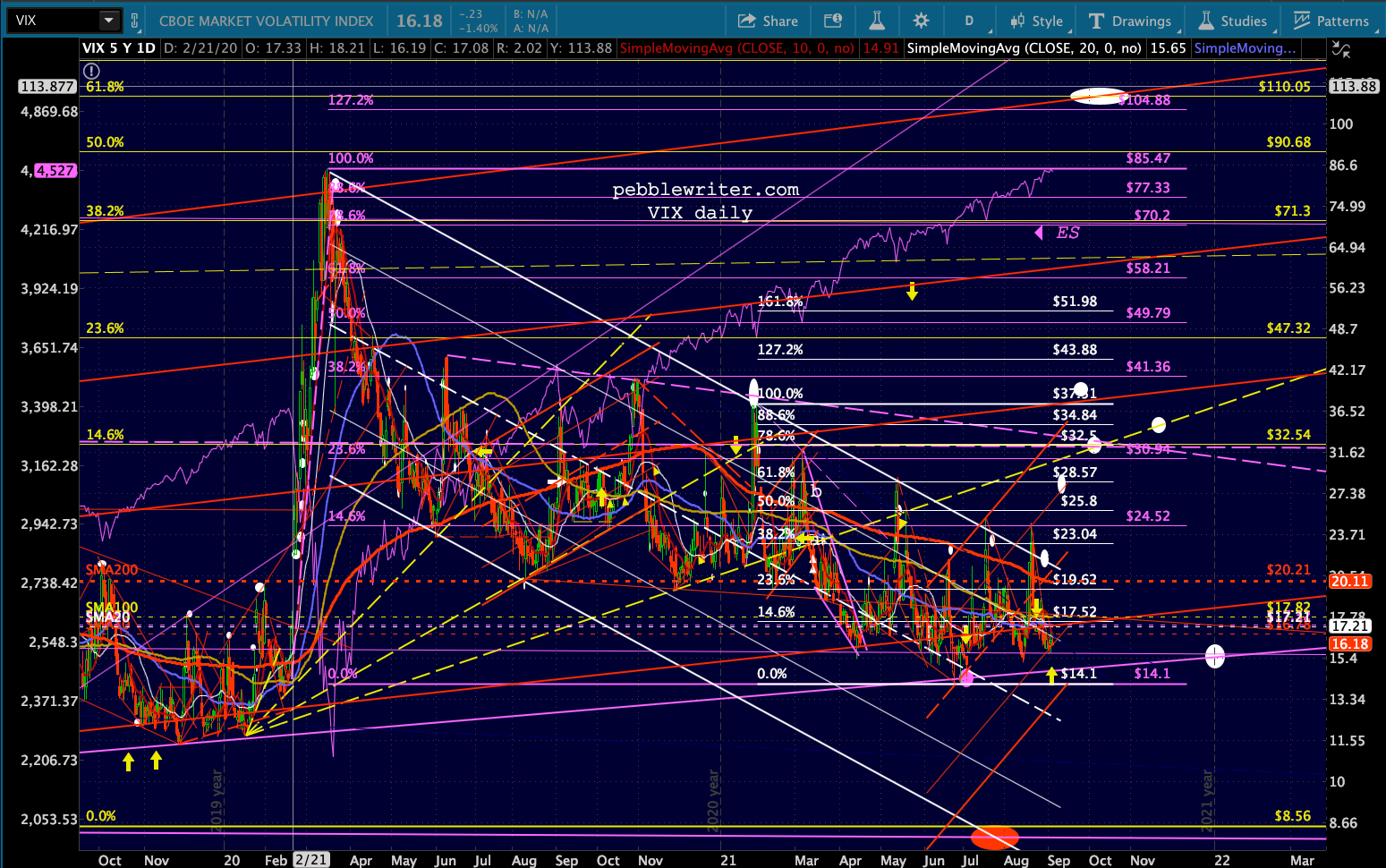

…and VIX.

…and VIX.

The proposition is fairly simple. For SPX to keep rising, we would need VIX to begin to chip away at its TL from Oct 2018.

The proposition is fairly simple. For SPX to keep rising, we would need VIX to begin to chip away at its TL from Oct 2018.

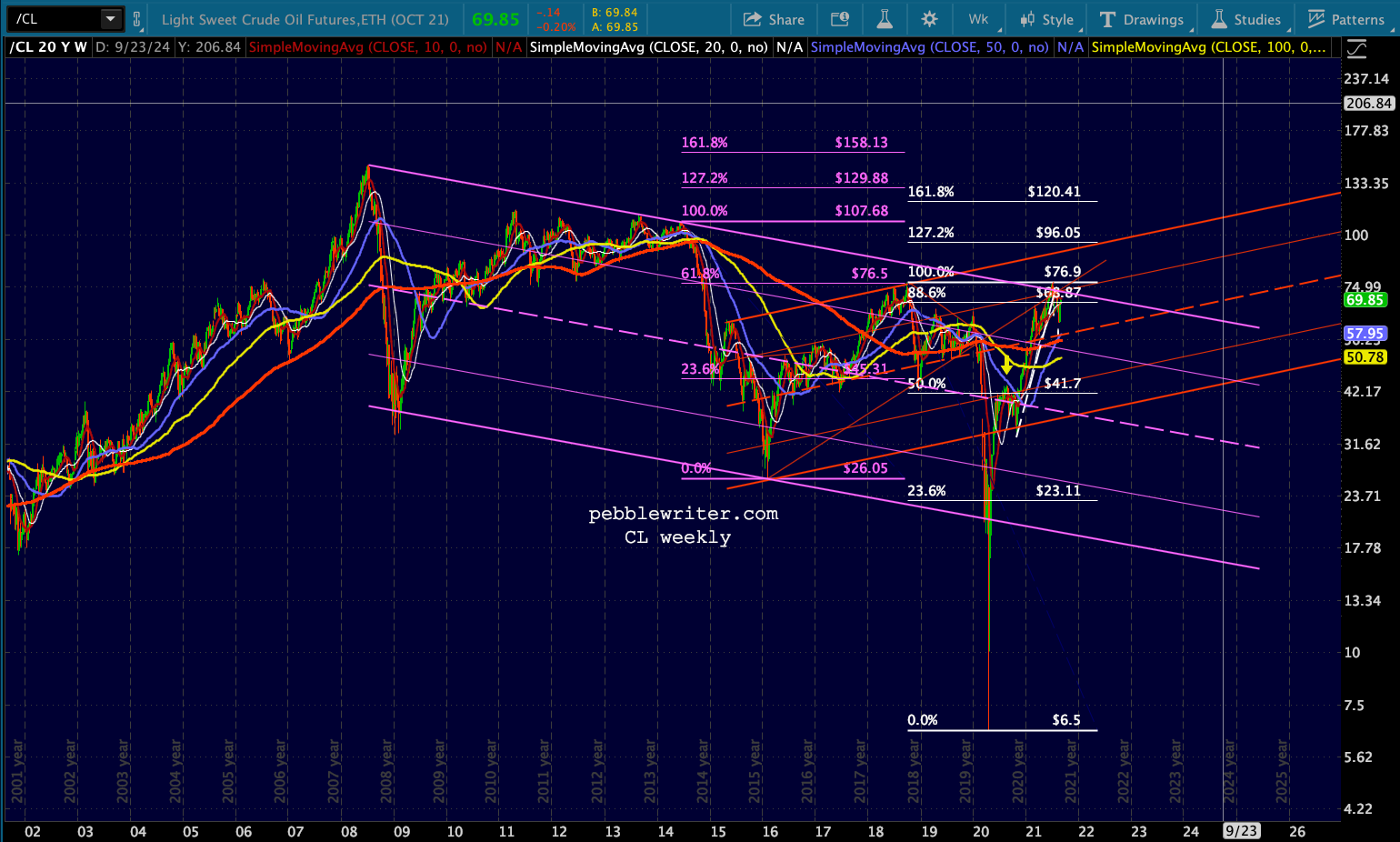

But, we would want to see other factors contribute. CL, for instance, recently reversed at the top of a TL/channel dating back to 2008. Since then, however, it has ignored the chance to drop to/through its SMA200 and broke back above a TL from February. Bears would benefit from a drop to/through the SMA200. Bulls need it to hold here or, ideally, break above the purple channel top.

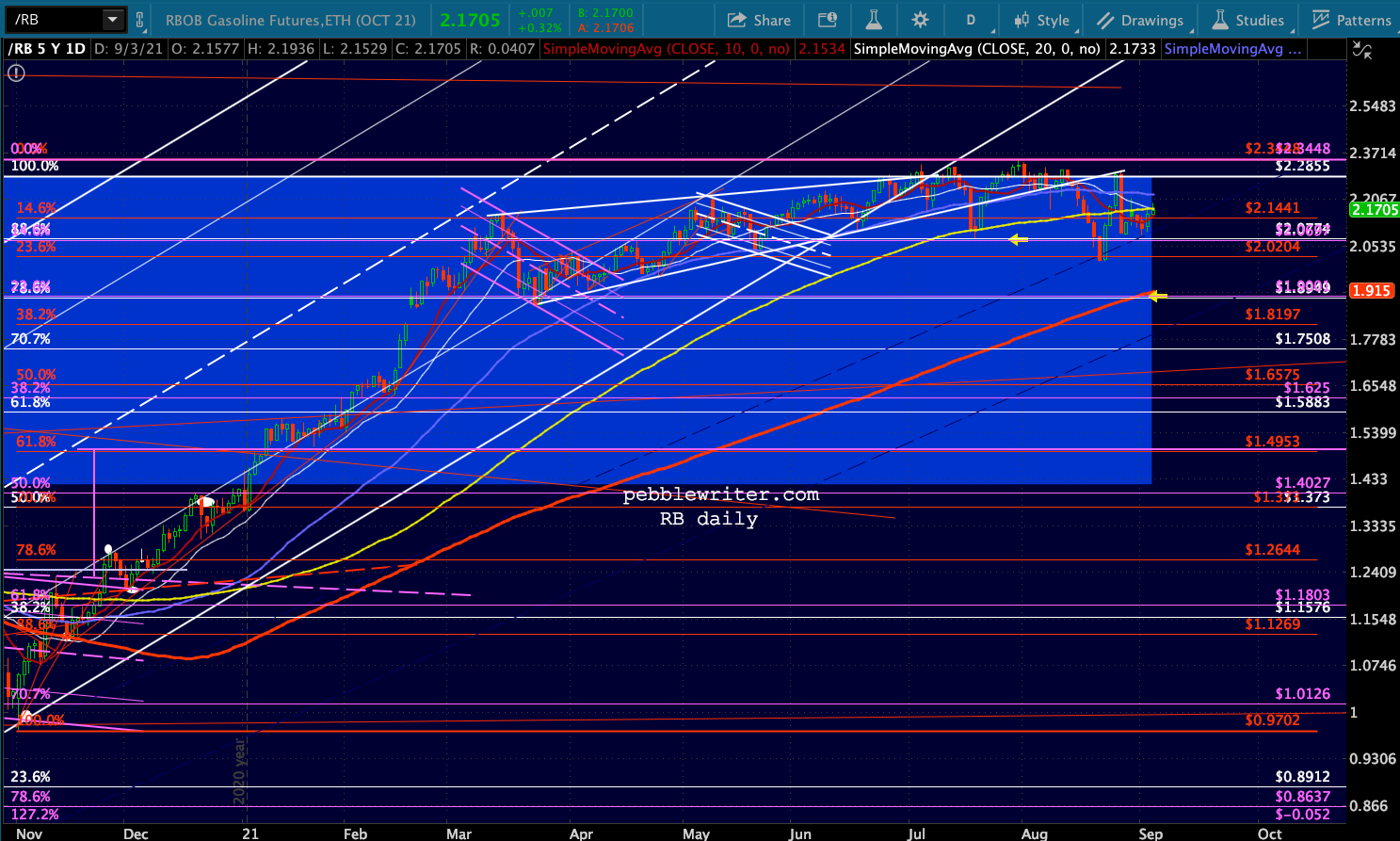

Since then, however, it has ignored the chance to drop to/through its SMA200 and broke back above a TL from February. Bears would benefit from a drop to/through the SMA200. Bulls need it to hold here or, ideally, break above the purple channel top. But, what about inflation? For that, we turn to the RBOB chart. RB recently tested its May 2018 highs…

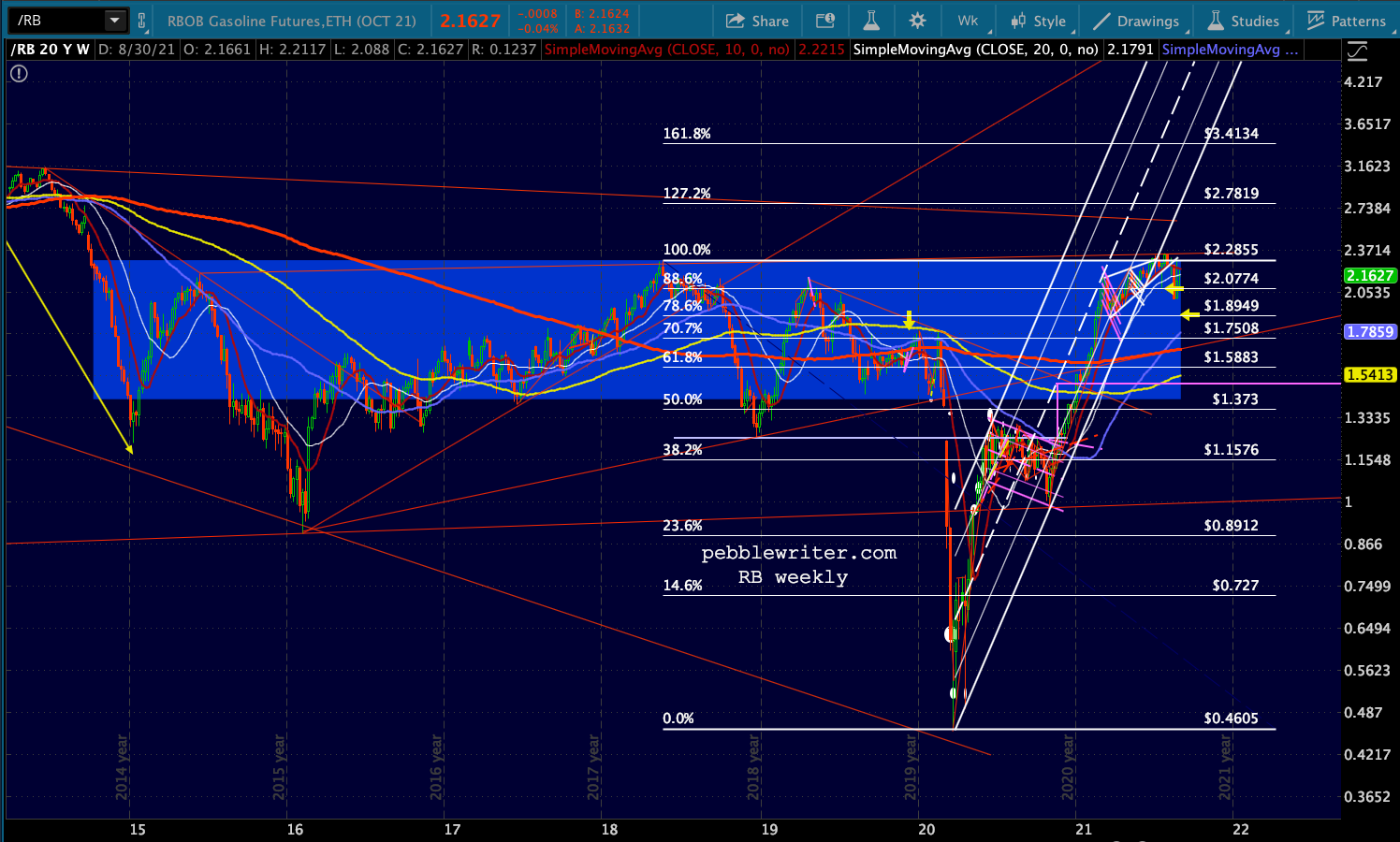

But, what about inflation? For that, we turn to the RBOB chart. RB recently tested its May 2018 highs… …which were slightly higher than its May 2018 highs.

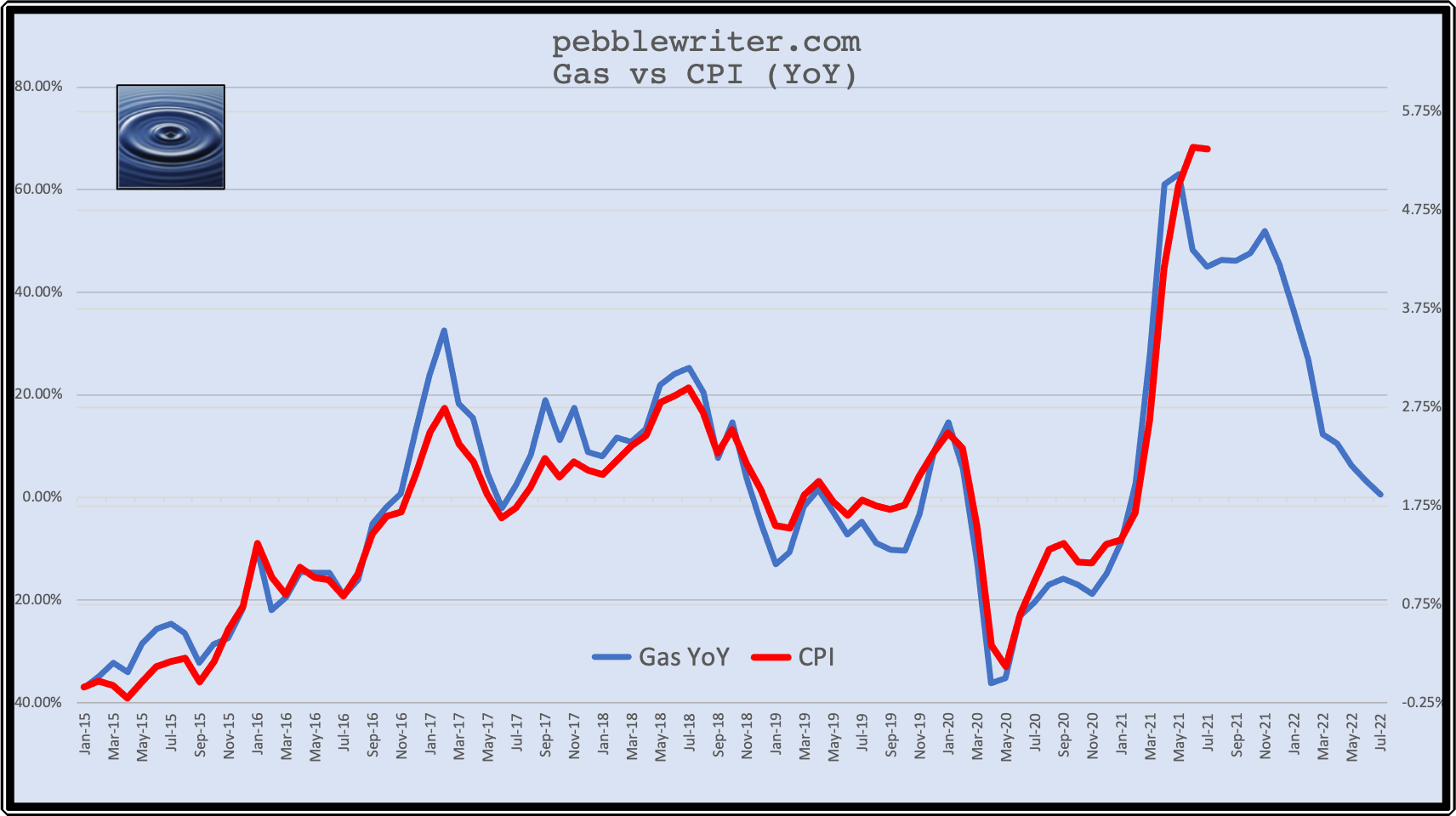

…which were slightly higher than its May 2018 highs. As we’ve pointed out countless times, YoY changes in RB have been very highly correlated with CPI over the years. Back in December 2020 [see: Don’t Ignore Inflation] we discussed how the coming spike in the YoY increase in oil/gas prices would result in much higher CPI.

As we’ve pointed out countless times, YoY changes in RB have been very highly correlated with CPI over the years. Back in December 2020 [see: Don’t Ignore Inflation] we discussed how the coming spike in the YoY increase in oil/gas prices would result in much higher CPI.

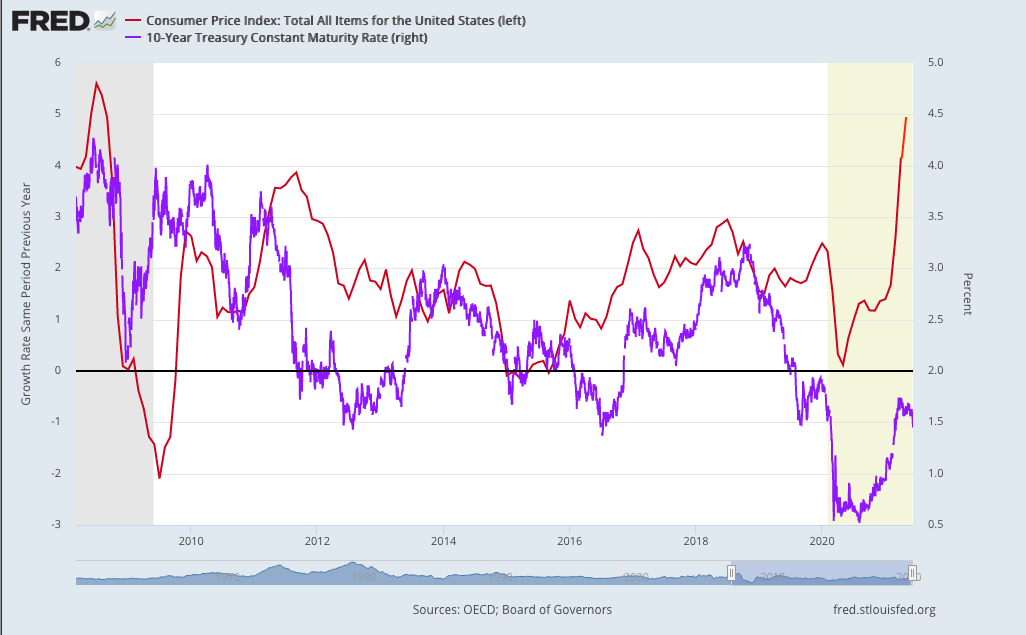

My belief at the time was that the Fed would step in and moderate the rise in oil/gas prices lest the YoY comparisons to the Mar-May 2020 crash price levels result in a sharp rise in CPI and, in turn, interest rates. Although I was right about inflation, I was completely wrong about interest rates. Contrary to my expectations, the Fed never blinked. With $120 billion per month at its disposal, the Fed was able to suppress interest rates to the point where spiraling inflation simply didn’t matter.

Although I was right about inflation, I was completely wrong about interest rates. Contrary to my expectations, the Fed never blinked. With $120 billion per month at its disposal, the Fed was able to suppress interest rates to the point where spiraling inflation simply didn’t matter.

How long will the divergence between CPI and interest rates continue? If gas prices were to remain at August levels going forward, the YoY increase would, by definition, eventually drop down to zero by August of next year.

How long will the divergence between CPI and interest rates continue? If gas prices were to remain at August levels going forward, the YoY increase would, by definition, eventually drop down to zero by August of next year.

In other words, the Fed could potentially have its market-supporting cake and eat it too by maintaining an elevated level of oil/gas prices. The few who haven’t already stopped bitching about inflation because there has been no impact on interest rates would have nothing to bitch about if inflation were to also drop back to, say, 2%.

In other words, the Fed could potentially have its market-supporting cake and eat it too by maintaining an elevated level of oil/gas prices. The few who haven’t already stopped bitching about inflation because there has been no impact on interest rates would have nothing to bitch about if inflation were to also drop back to, say, 2%. To be continued…

To be continued…