NOTE: New on the MEMBERSHIP>MY PROFILE page, a sign up area that will allow subscribers to be texted whenever a new post is added or added to [note: additions don’t seem to be generating additional texts — working on this]. I tested it last night, and it took only 3-4 minutes for a SMS text advising me of a new post to appear on my mobile. It doesn’t appear to handle non-US cell providers, so I’m looking for additional vendors that can accommodate those outside the states.

UPDATE: 1:15 PM

Be cautious with this smaller pattern, though. The 60-min chart shows a distinct possibility of a bounce at the neckline (as happened with the larger pattern.) Focus on the bold, yellow TL on the RSI below. I would suggest anyone considering piling on shorts protect themselves, as always, with tight stops.

UPDATE: 12:30 PM

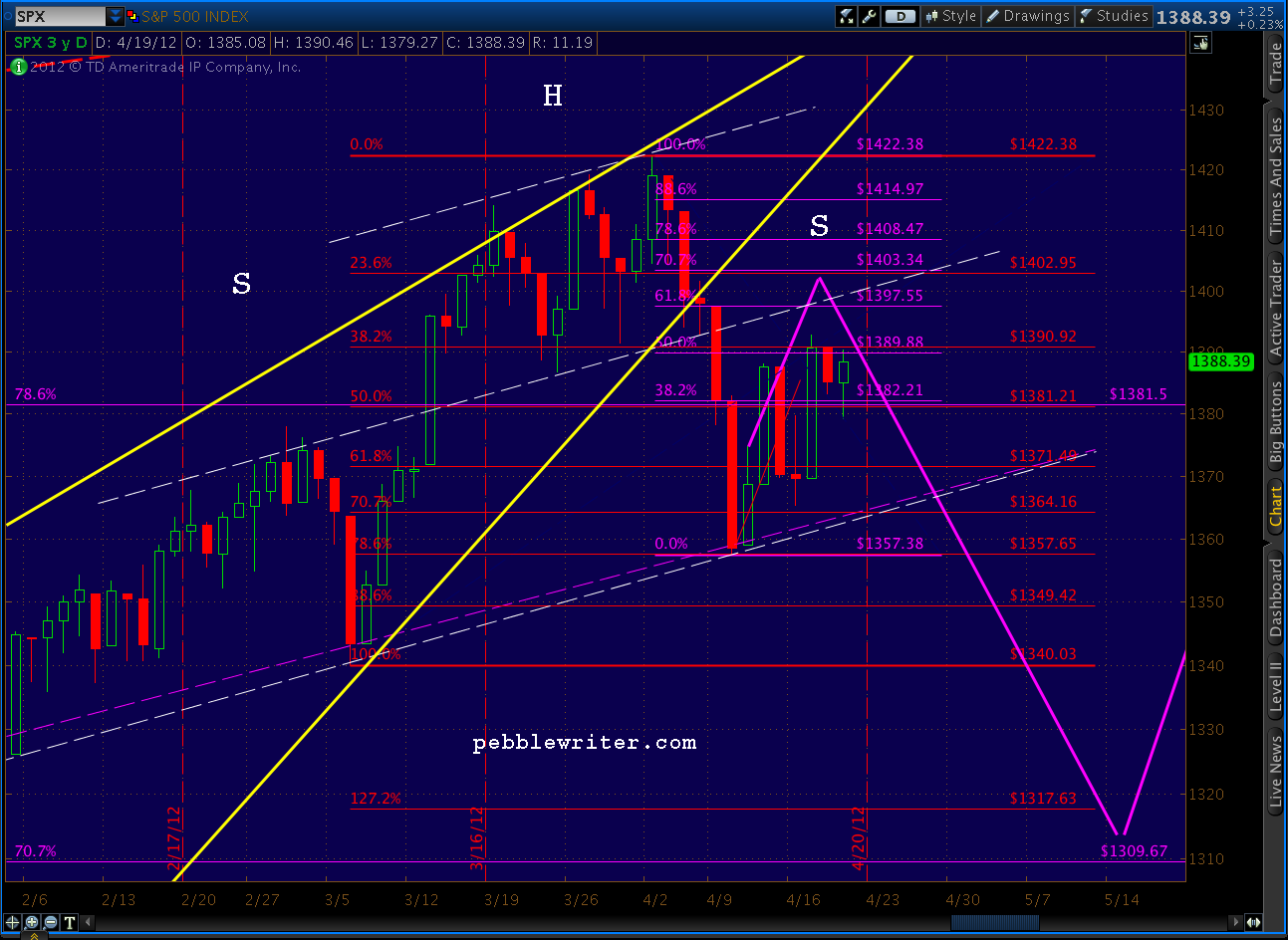

Over on the right shoulder of the Head & Shoulders pattern we’ve been watching is a… H&S pattern. It would complete somewhere just below 1394 and targets 1372 — the (wait for it…) neckline of the larger pattern.

Ever get the feeling the market is just toying with you? Seriously, though, this fits rather well with the RSI indicators, which as I posted earlier, support the idea of another test of the neckline.

If we get crazy positive non-farm payroll numbers in the morning, all bets are off. Barrons is reporting consensus estimates of 165,000 (below), while Briefing.com estimates 140K.

If we get crazy positive non-farm payroll numbers in the morning, all bets are off. Barrons is reporting consensus estimates of 165,000 (below), while Briefing.com estimates 140K.

UPDATE: 12:30 PM

Non-manufacturing ISM numbers confirm the economy’s slowdown. Recall that the recent national numbers for manufacturers inexplicably showed an improvement — in stark contrast to the regional numbers and most other economic indicators I watch.

The services sector (the larger share of the US economy) confirms what I suspect was a bad print a couple days ago. We see worsening in the overall index (from 56 to 53.5 and vs expectations of 56.5) and in the categories of business activity, new orders, employment and prices (the largest drop of all.)

ORIGINAL POST: 11:00 AM EST

The RSI channel we analyzed (in excruciating detail) yesterday is holding so far.

If we can break that last little fan line (k-4) things should accelerate a little to the downside, probably to test the k-5 line, which I believe will correlate with the H&S pattern neckline.

If we can break that last little fan line (k-4) things should accelerate a little to the downside, probably to test the k-5 line, which I believe will correlate with the H&S pattern neckline.

It seems like the market is waiting for a sign of some sort for any serious downside to develop — which will likely come from Europe, China or MENA. Why? If good economic news drives the market up, and bad economic news increases (even falsely) the odds of QE, then it stands to reason that only an exogenous shock — one over which the Fed has less control — will drive prices lower.

Having said that, the entire economic picture has the feel of a triangle pattern. We careen from good news to bad, euphoria to despair — all the while drawing closer to the (IMO) inevitable day of reckoning where the mountain of debt shakes just enough to unleash a major landslide.

We see a preview of the effects in places like Greece, Ireland, Portugal and increasingly Spain. Total debt to GDP is much too high in these countries, but the US tops them all. Official reports put acknowledged debt/GDP in the US at 101.5%. But, as this Zerohedge article points out, the contingent liabilities such as the NPV of unfunded pension and health care drive our true debt/GDP to well over 300%.