Following a strong March where consumers ramped up purchases in advance of tariff-induced price hikes, retail sales plunged in April to 0.1%, well below expectations of 0.4%. Combined with UNH’s 10%+ downdraft following news of a criminal probe, futures are off moderately this morning.

Even Walmart is warning of a weakening consumer and risks posed by prices elevated by Trump’s tariffs.

Even Walmart is warning of a weakening consumer and risks posed by prices elevated by Trump’s tariffs.

“The higher tariffs will result in higher prices,” CEO Doug McMillon.

continued for members…

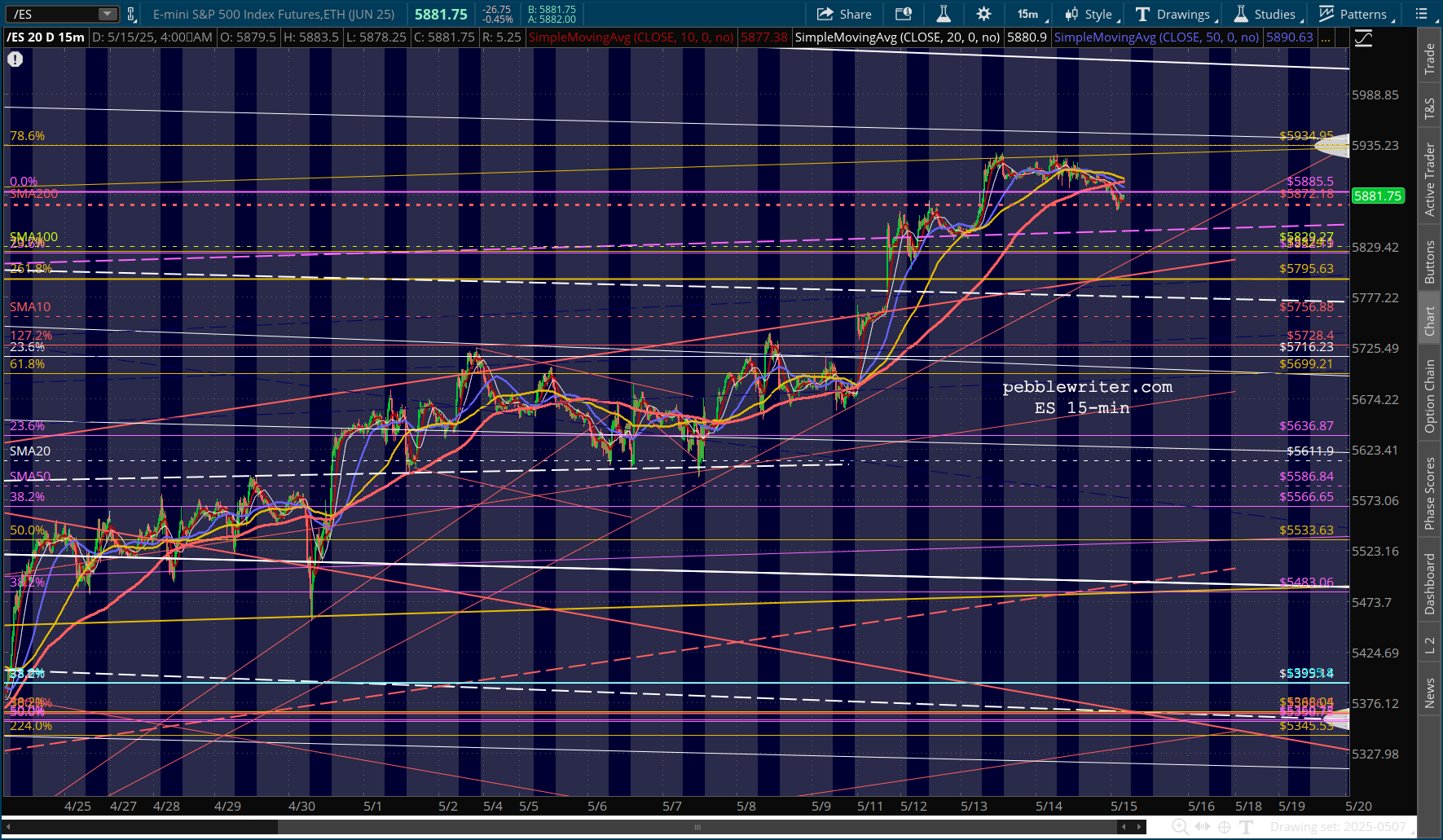

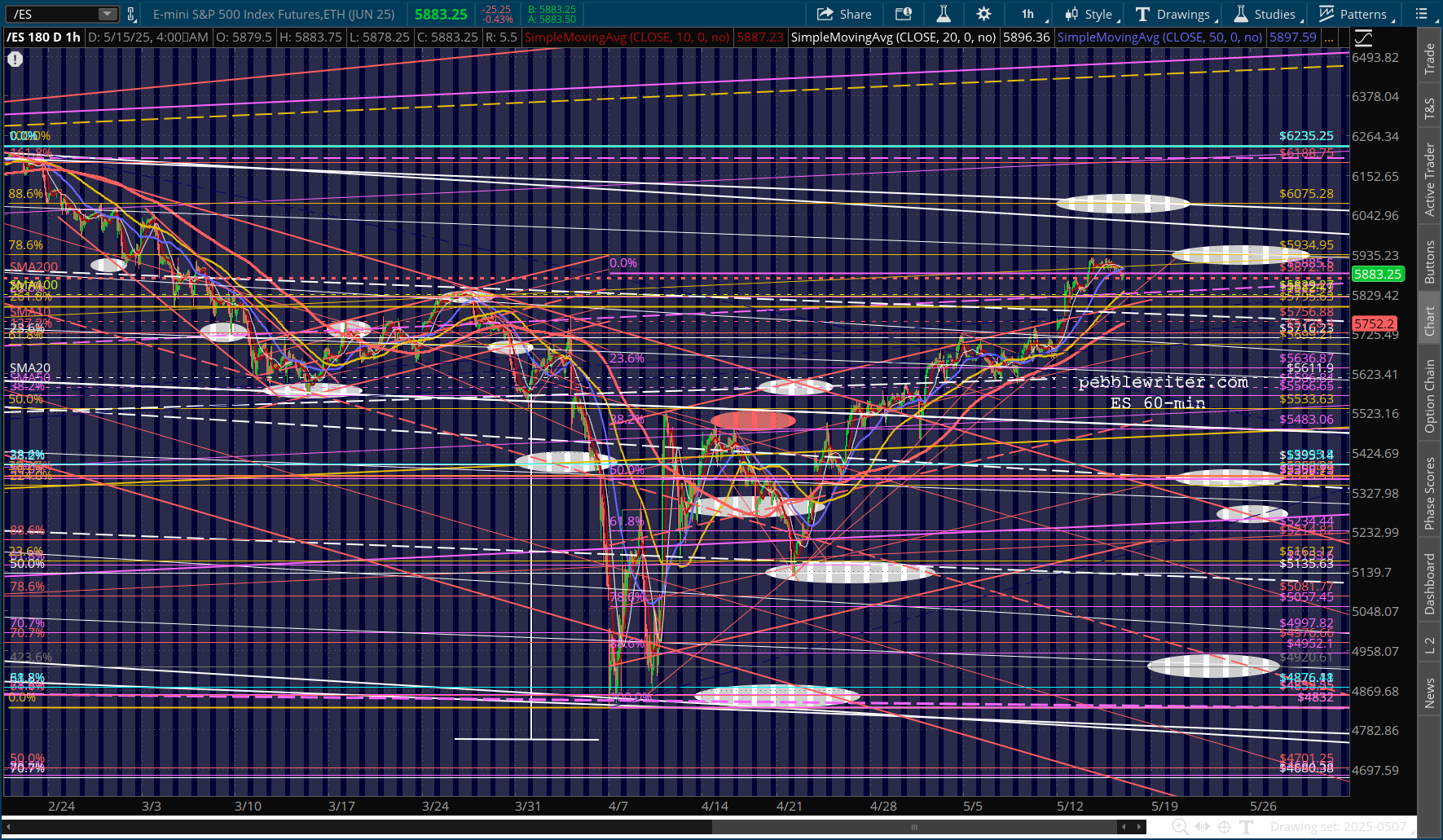

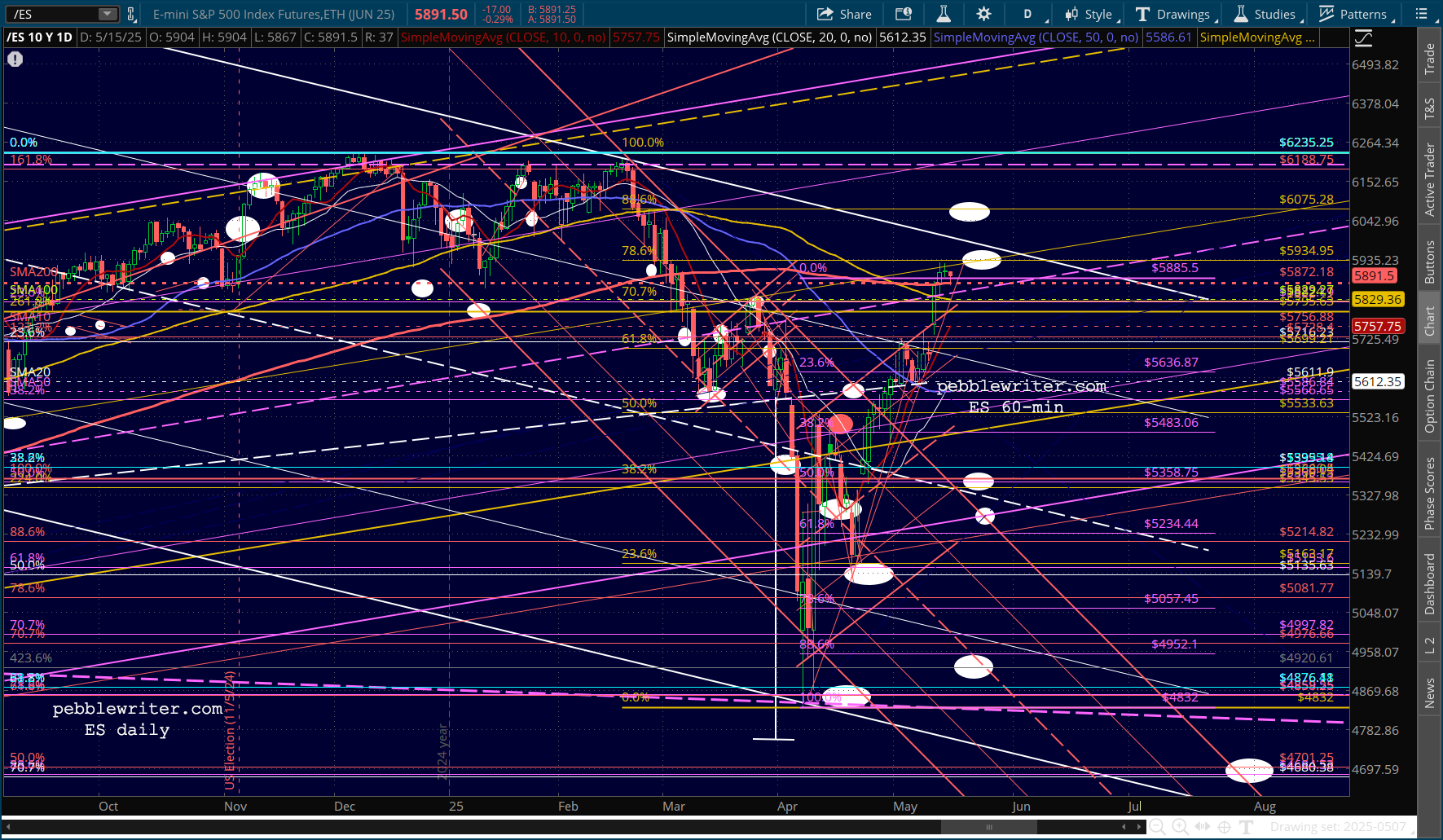

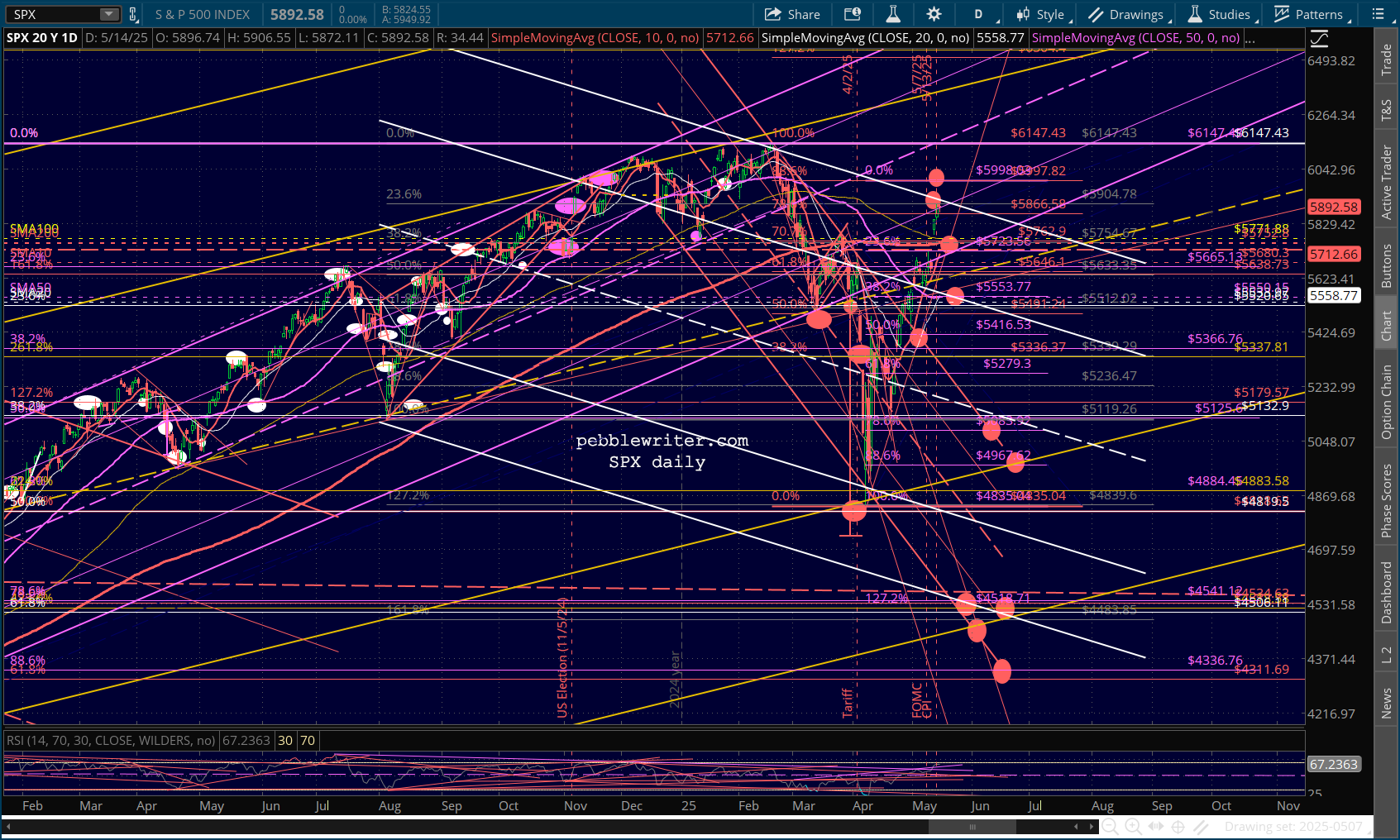

ES has backtested its SMA200 as expected. SPX’s is much further away at 5739, 150 points below yesterday’s close. This sets up a very confusing picture for chartists. It increases the likelihood of a longer topping process rather than an imminent sharp decline.

This corresponds with a number of charts which suggest we could be well into June or even later before any significant drops. Obviously, there is still a chance that the tariff situation will come apart at the seems (e.g. China announcing that no progress has been made.)

There’s also a very good chance that the inflation which tariffs will cause is completely downplayed by the Trump administration. We’ve seen it already. It will be interesting to watch non-governmental sources of economic info such as tomorrow’s University of Michigan Consumer Sentiment print.

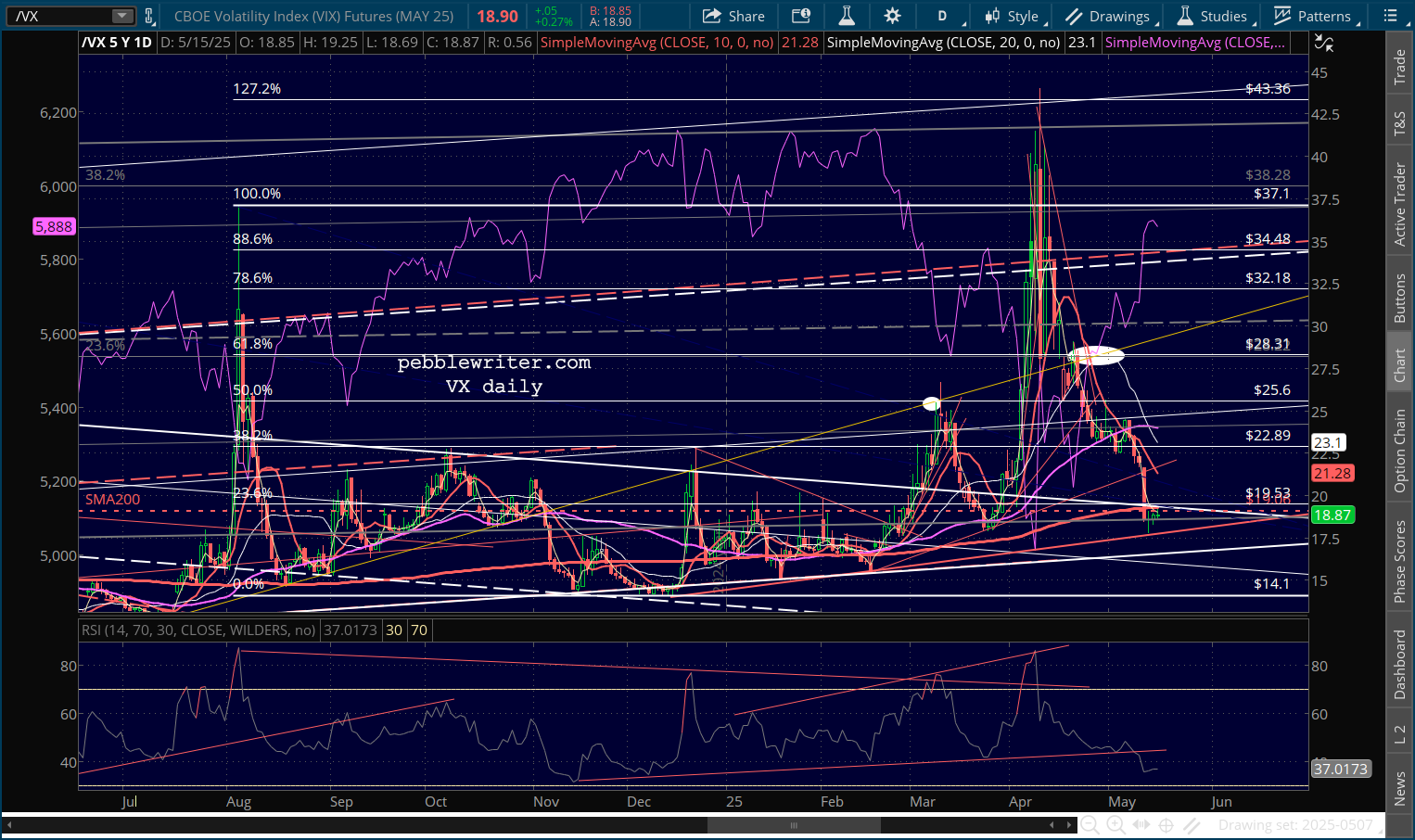

VX caught a bid on its red TL but its RSI is not confirming a bounce just yet.

VX caught a bid on its red TL but its RSI is not confirming a bounce just yet.

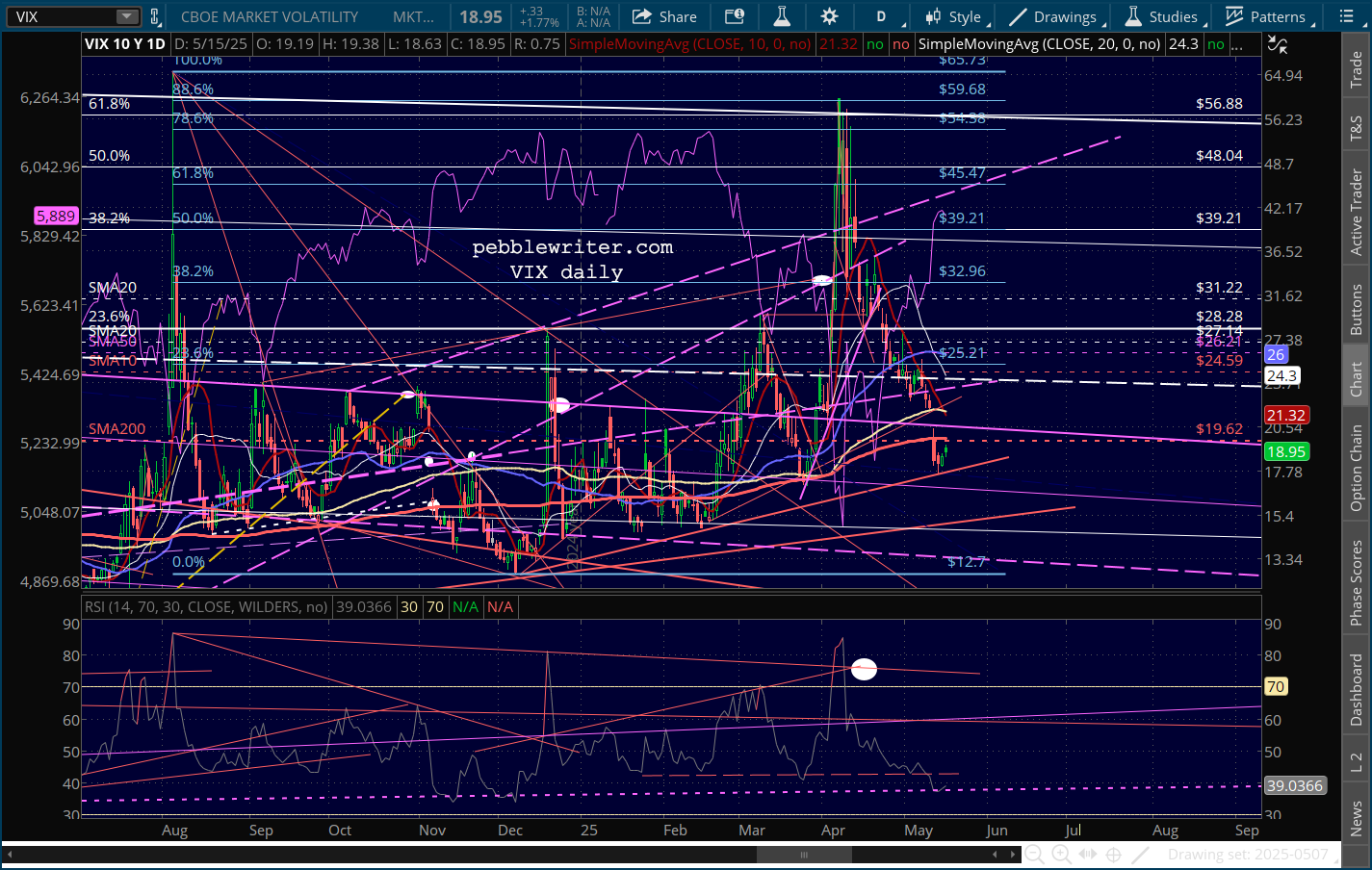

VIX, on the other hand, has bounced on TL support in both the index and its RSI.

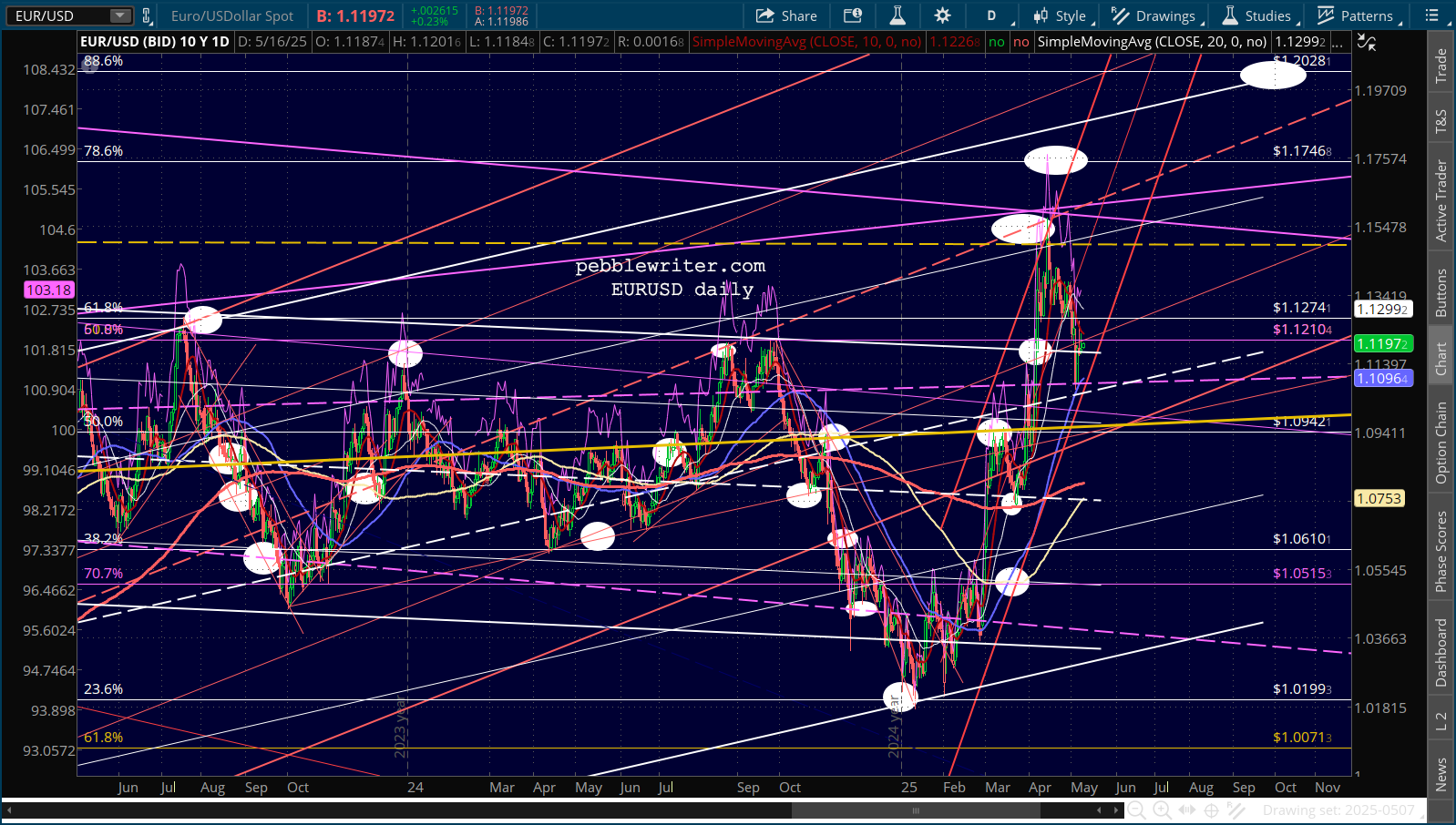

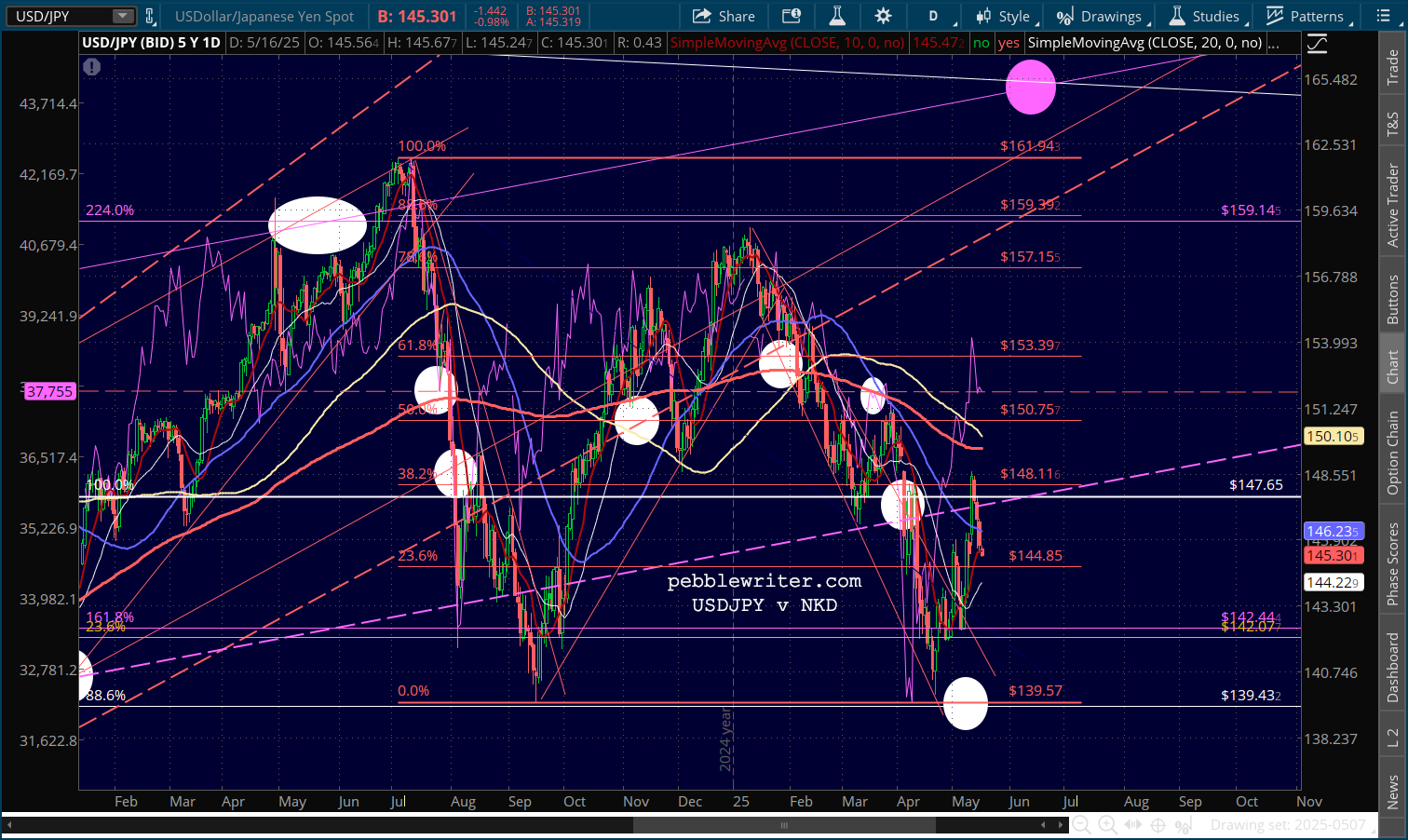

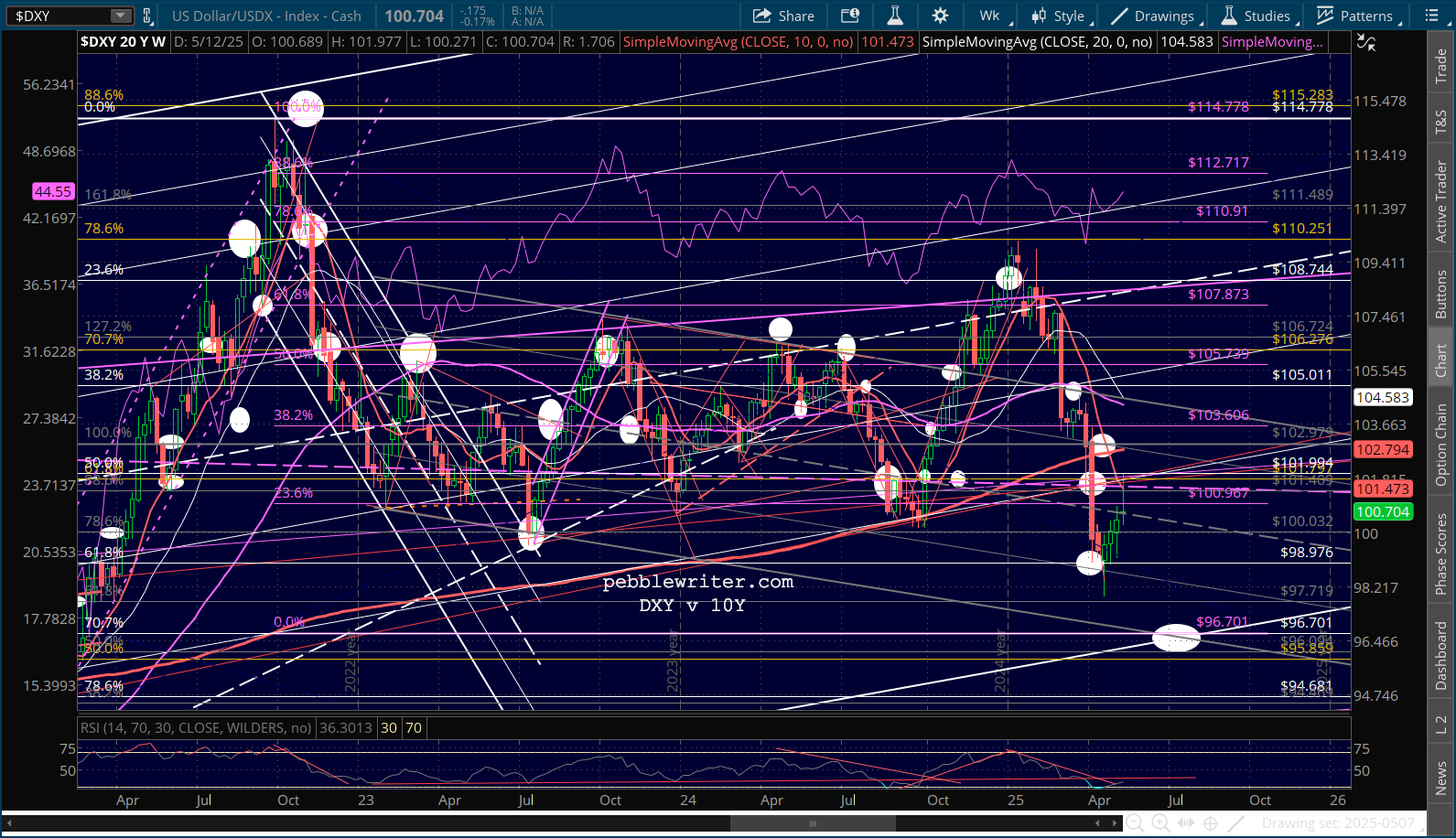

VIX, on the other hand, has bounced on TL support in both the index and its RSI. Currencies still suggest a weakening dollar…

Currencies still suggest a weakening dollar…

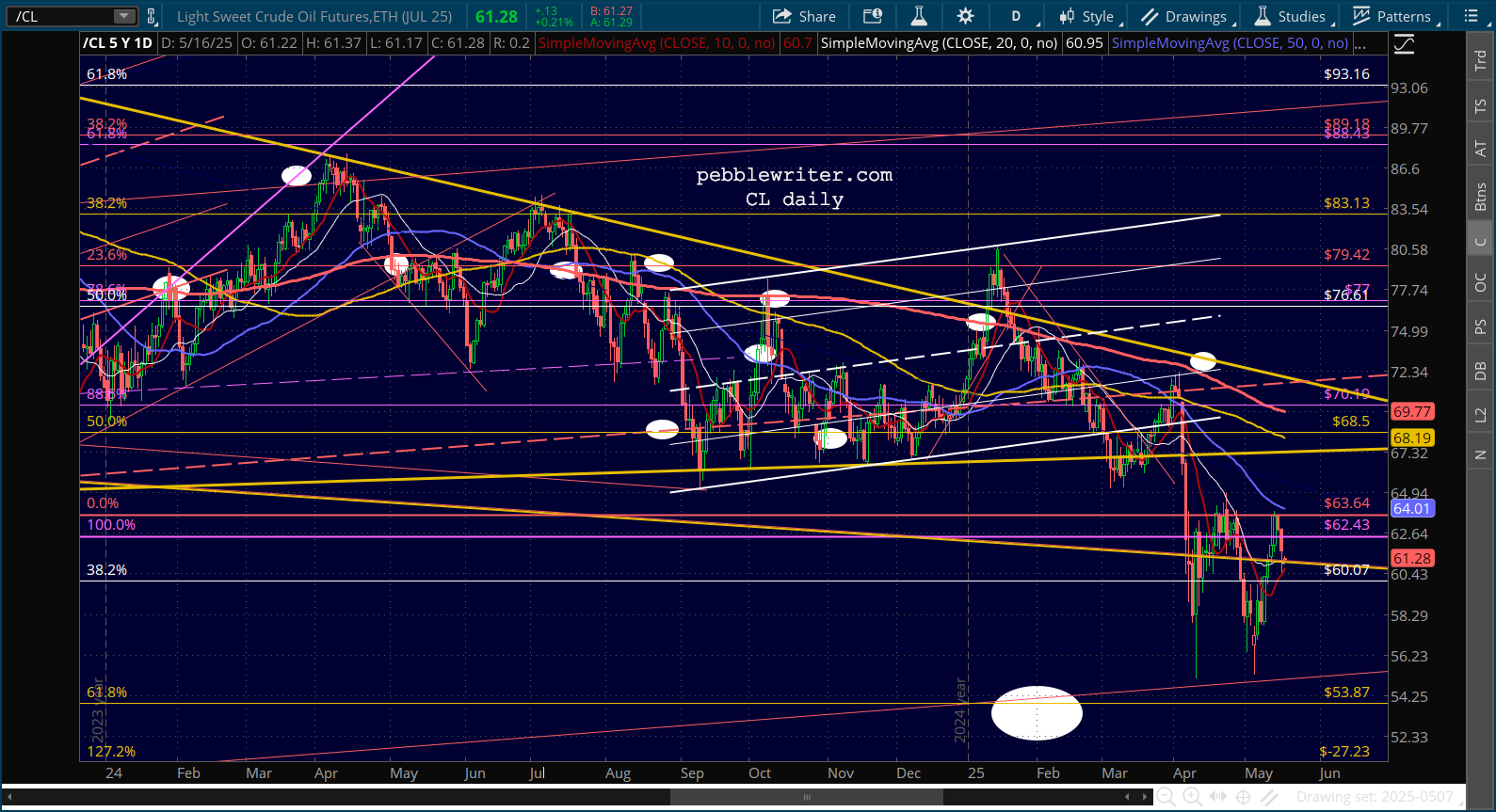

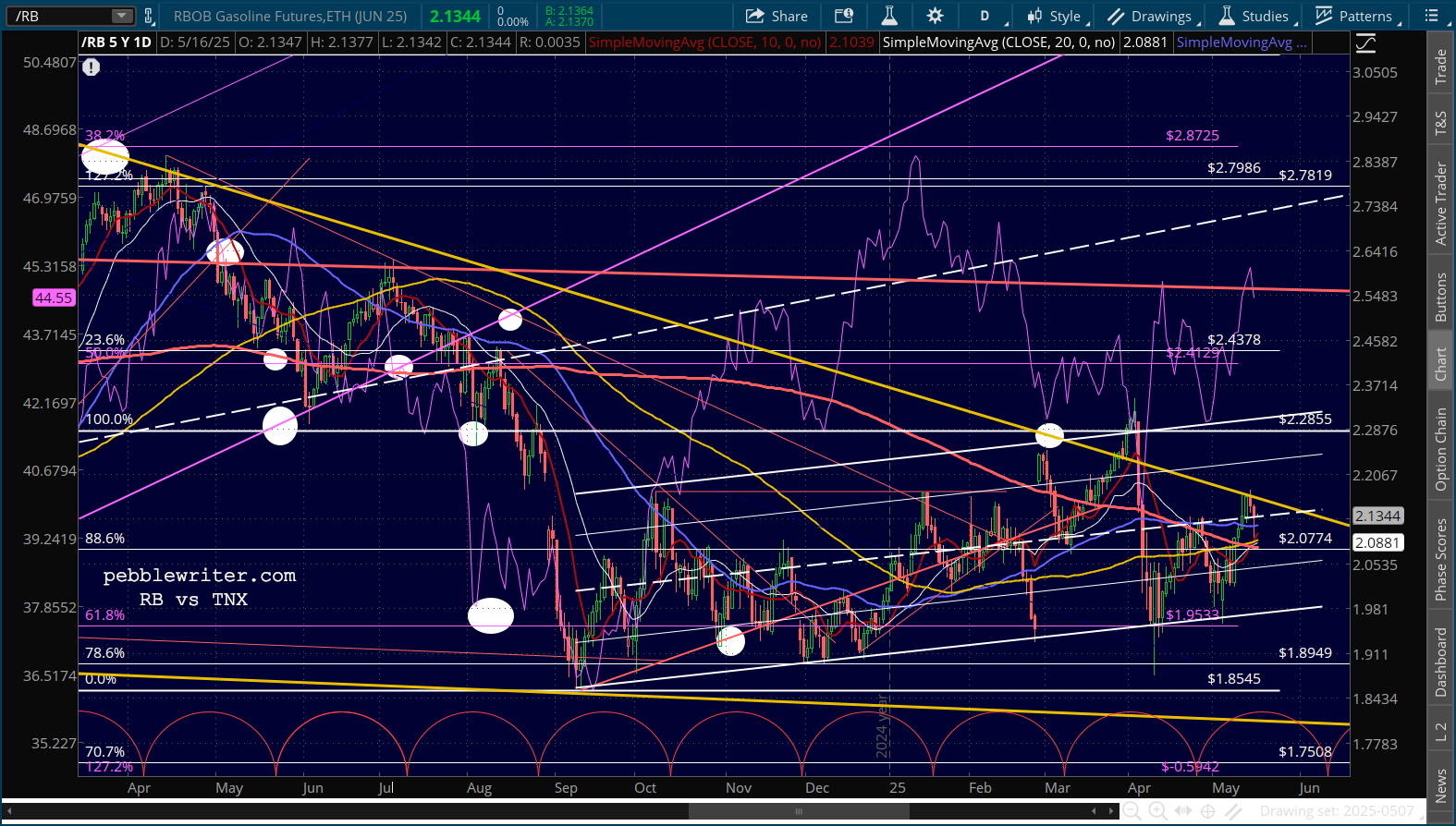

…while CL and RB remain under control, likely because the Saudis are in the process of wooing Trump.

…while CL and RB remain under control, likely because the Saudis are in the process of wooing Trump.

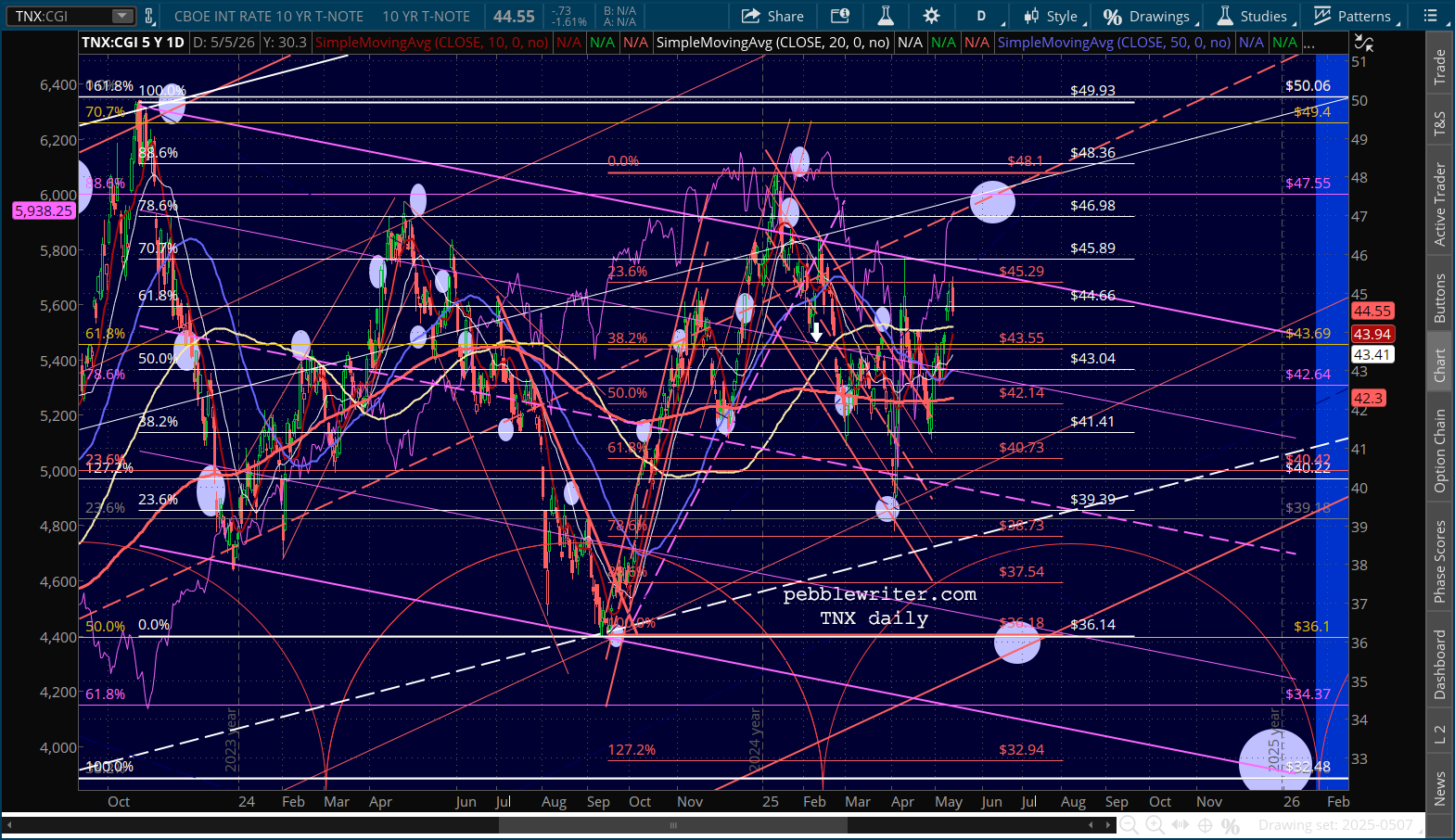

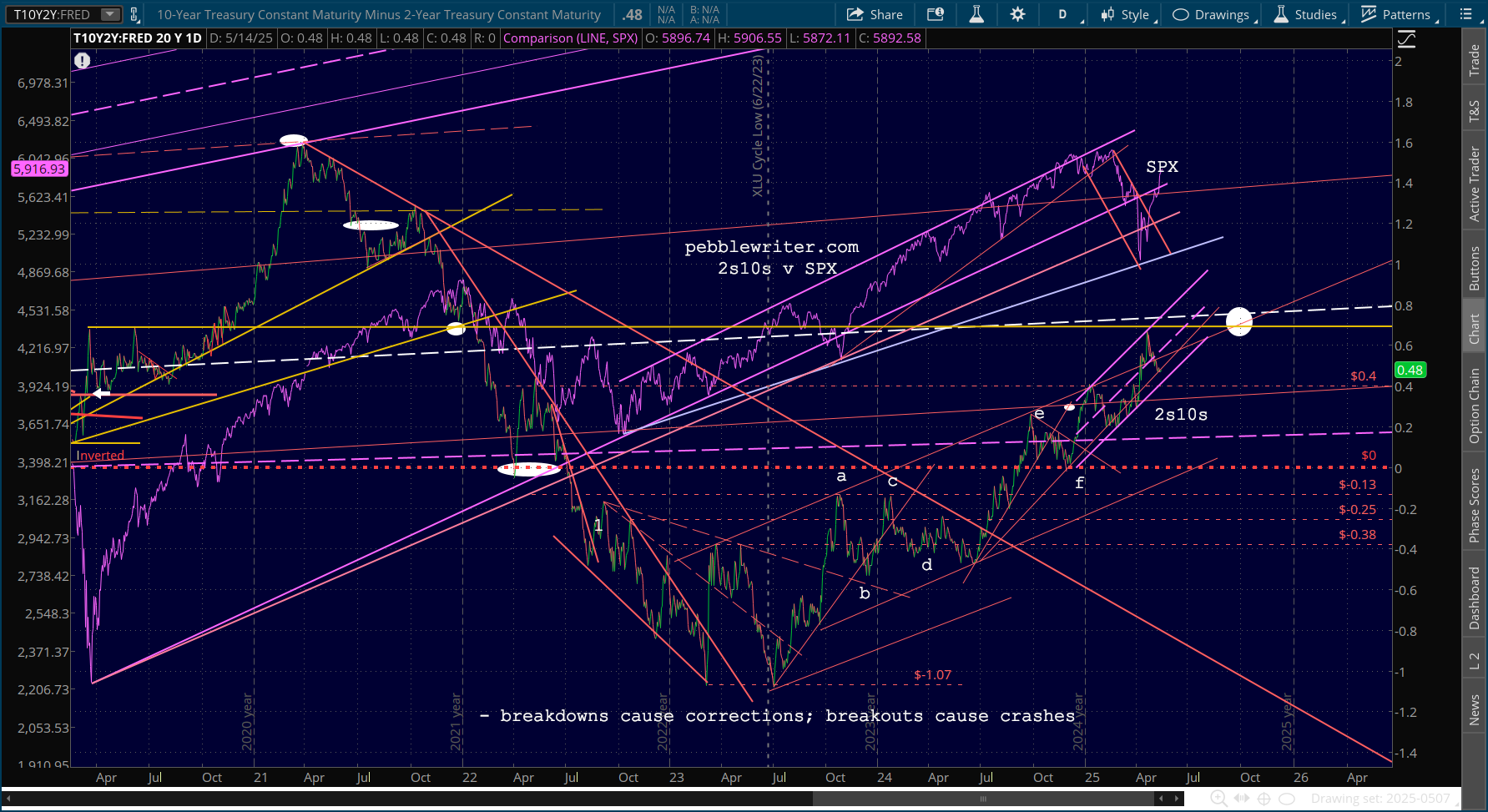

So, TNX has plenty of reason to decline.

So, TNX has plenty of reason to decline.

At some point, I expect it to gather speed to the downside. But, the degree of inflation we experience will no doubt play a significant role.

GLTA

GLTA