While we’re all waiting for our heroes on Capitol Hill to ride in on white horses…

FRIDAY

Friday’s market proved, once again, the power of harmonics. While I, and seemingly everyone else, was watching the 200-day moving average (1284.27) for a bounce, it was a Gartley pattern and a fan line that proved the more accurate forecasting tool.

Here are the two Gartley’s I was watching:

Pretty well drawn, except for the false start back at the end of June. The .786 retrace completion, or D point, is at 1279.13.

From the other apparent starting point, D is at 1282.90. The actual low for the day was 1282.86.

Normally, I look for a bounce of .618 of the DC leg from a Gartley pattern. This would indicate an upside with potential to 1321.84.

And, the fan line? Take a gander at the yellow dashed-line. It starts at the Nov 30 low and tags the Jun 15, 16, 24 and 27 lows.

Here’s a close up:

I normally consider Gartley targets pretty reliable. But, under the circumstances, I gotta say it’s anyone’s guess how far and how fast the next couple of days go. I believe we’re still under the influence of the 2007 pattern, but this debt ceiling matter will clearly determine the direction and magnitude of at least the next few days.

LOOKING FORWARD

If we get positive news on the debt ceiling, look for a relief rally that’s proportional to the perceived quality of the news. I expect it to be a crock, providing no real cost savings or revenue increases. But, that doesn’t matter. What really matters is how well TPTB sell the deal as the key to our salvation.

It appears as though S&P; has folded in the face of what was probably unbelievable pressure from the government. So, we’ll get a slap on the wrist rather than actual downgrade. Moody’s and Fitch will probably fall in line.

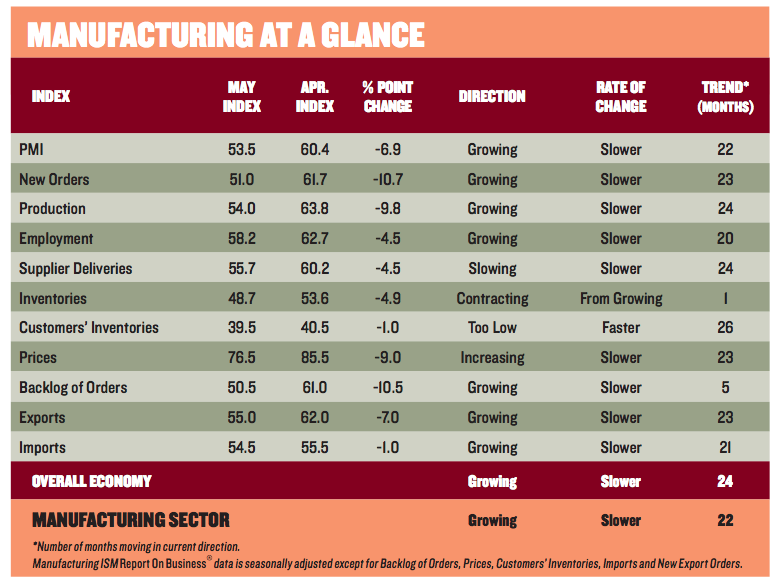

It’ll be interesting to see how the economic data shakes out. ISM is scheduled to report at 10 AM. The last two times they reported negative news, the market tanked. On May 2, they reported the April PMI at 60.4, down from March’s 61.2. It confirmed the downtrend that started with the previous month’s report. May 2, of course, marked the top of the current pattern and the start of a 112-point decline in stocks.

On June 1, ISM reported a PMI of 53.5, well below the previous month’s 60.4. The 31-point decline was the worst of 2011. I have no secret source inside ISM, but I have gone back and read the last few reports.

The only “good news” the past two months has been the pickup in activity due to inventory buildup. You could look at this as positive and represents increasing demand. Or, you could look at it as a sign that purchasers jumped the gun, mistakenly believing demand would return. I’ve included the breakdown from the past two reports below FYI.

Also, here’s a look at the global picture. It appears there’s a pretty good chance of a decline below the neutral reading of 50.

LOOKING BACK

Last, I’ve spent most of the weekend in the Wayback Machine, considering what really happened in the Great Depression that isn’t widely known these days. Maybe I learned this back in college and have forgotten it, but I found it interesting that a real estate crash preceded the Great Depression. Really.

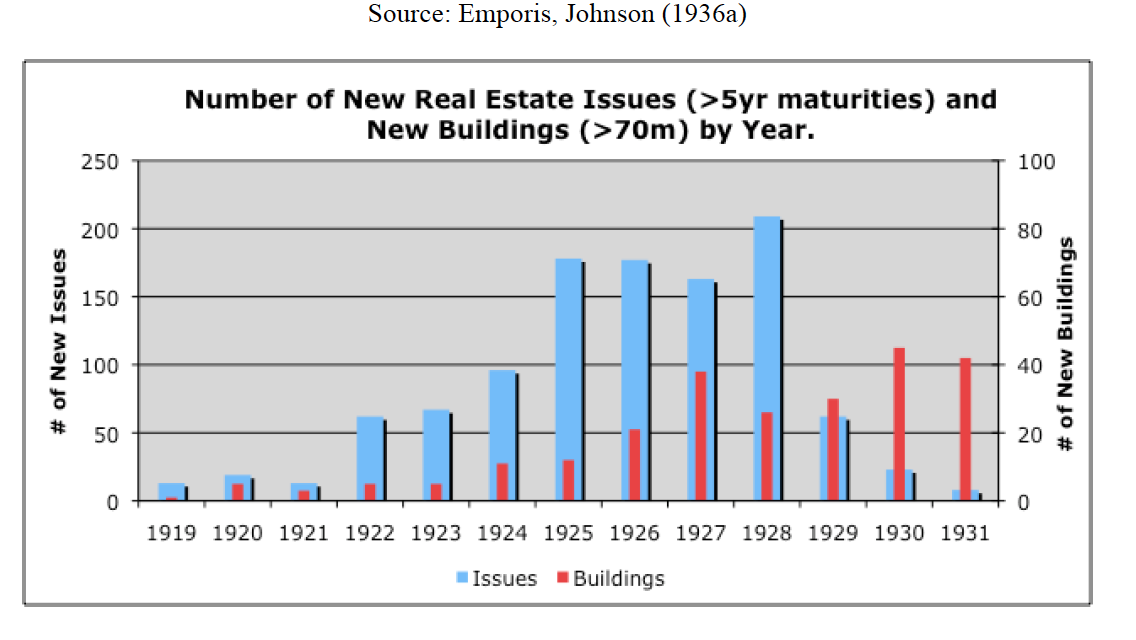

In “Securitization in the 1920’s“, William Goetzmann and Frank Newman of Yale describe a real estate market run amok, much like the early 2000s. In New York, for instance, more skyscrapers were built (235) than in any 10-year period ever. Many were financed with bonds, offered in denominations as low as $100 and offering interest rates of 4-7%. Interestingly, the coupon payments were often paid in gold — as it was considered an excellent inflation hedge at the time.

Annual issuance grew from about $58 million in 1919 to $696 million in 1925, representing 23% of total corporate debt nationwide. The market peaked in 1928, falling over 75% by 1933.

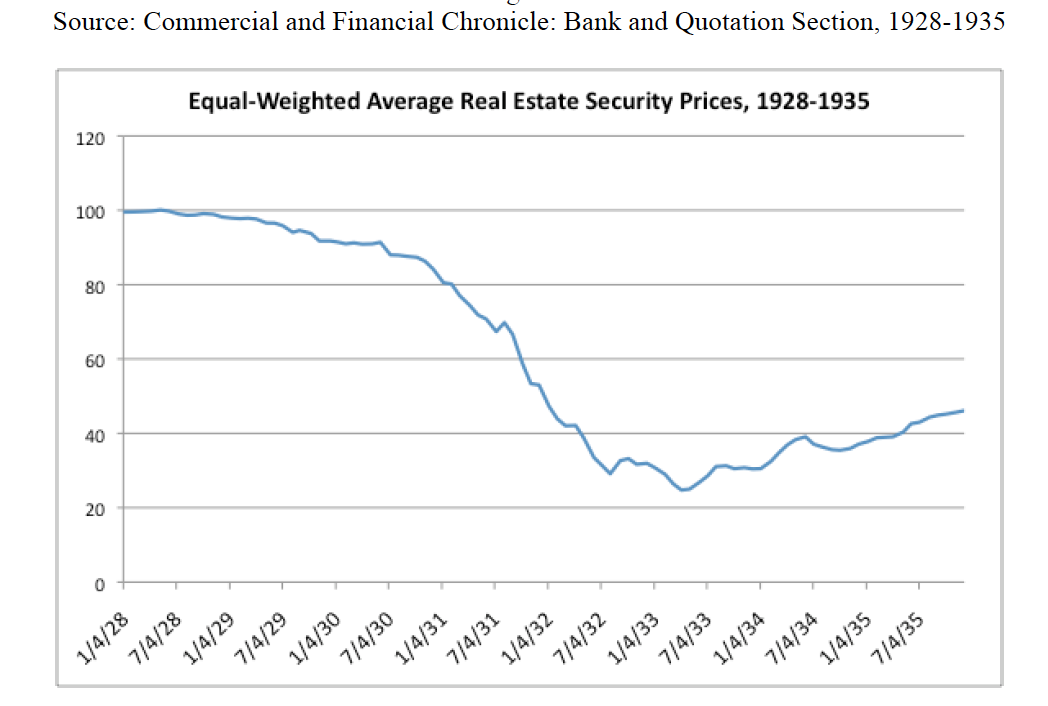

The stock market tanked after the crack in the real estate securities market, as is clearly demonstrated by the following graph:

If I get really ambitious, I’ll put together a comparison of like spreads for the past 10 years. But, I think I know what it will look like.

Sure makes me wonder about that uptick in subprime loan delinquency rates in the first quarter…

Additional ISM data:

Comments

5 responses to “Random Thoughts While Awaiting Certain Doom”

Hey George, Looking at the Chicago July report, pretty negative from a trend standpoint. Barometer, Production, New Orders, Employment, Deliveries, Cap Equip all lower than June. Only Prices, Inventories, and Backlogs up. Chicago has been a bright spot, for sure. But, NY and Boston looking troublesome. Seen the Global numbers? Fell to 52.3 from 53 in June; graph looking like it'll cross below 50 in July.

Both valid points.

Thanks

As far as making it all the way to 1321, I'm not at all certain. Under normal circumstances, I'd expect it. But, these are not normal, right?

I think there's two components to the debt deal — that it happens at all, and the quality/quantity of cutbacks. It seems like it is pretty certain, so I'm wondering if the 20 point pop here is the market's lack of enthusiasm for the limited LT impact. If that's the case, 1321 may not be reachable at all — especially if we get weak econ numbers this week.

Like your work.

Just to be clear………you are looking for a move to 1321, then resume the drop?

Thanks

Chicago PMI seems to lead the ISM manufacturing. It is down, though still positive. I think at best ISM will be below expectation as the consensus is about the same as last month.