It’s not that Q2 hasn’t been kind to investors. The S&P 500 is still up 39% from its March 23 lows (40% for the Dow, 49% for COMP.) But, it’s impossible to ignore how stocks got here and wonder whether they’ll continue to dance with the forces that brought them. Moreover, what happens if the Fed decides it’s done enough for now and the music stops?

As we discussed yesterday, the bearish charts and downside indicators are piling up. And, of course, big rallies produce meaningful rebalancing that could offset the usual end-of-quarter algo-driven meltup. The next few days will be most interesting.

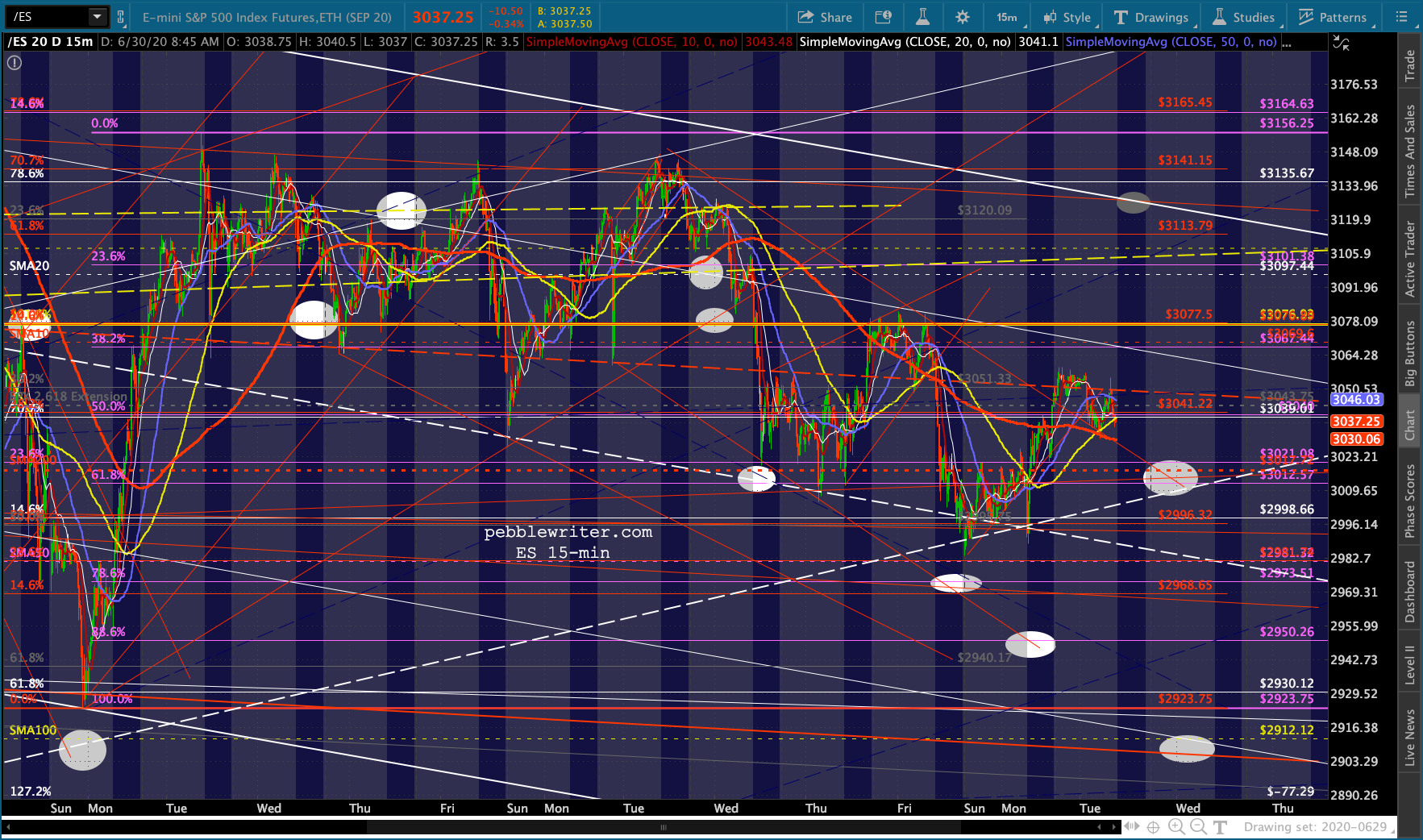

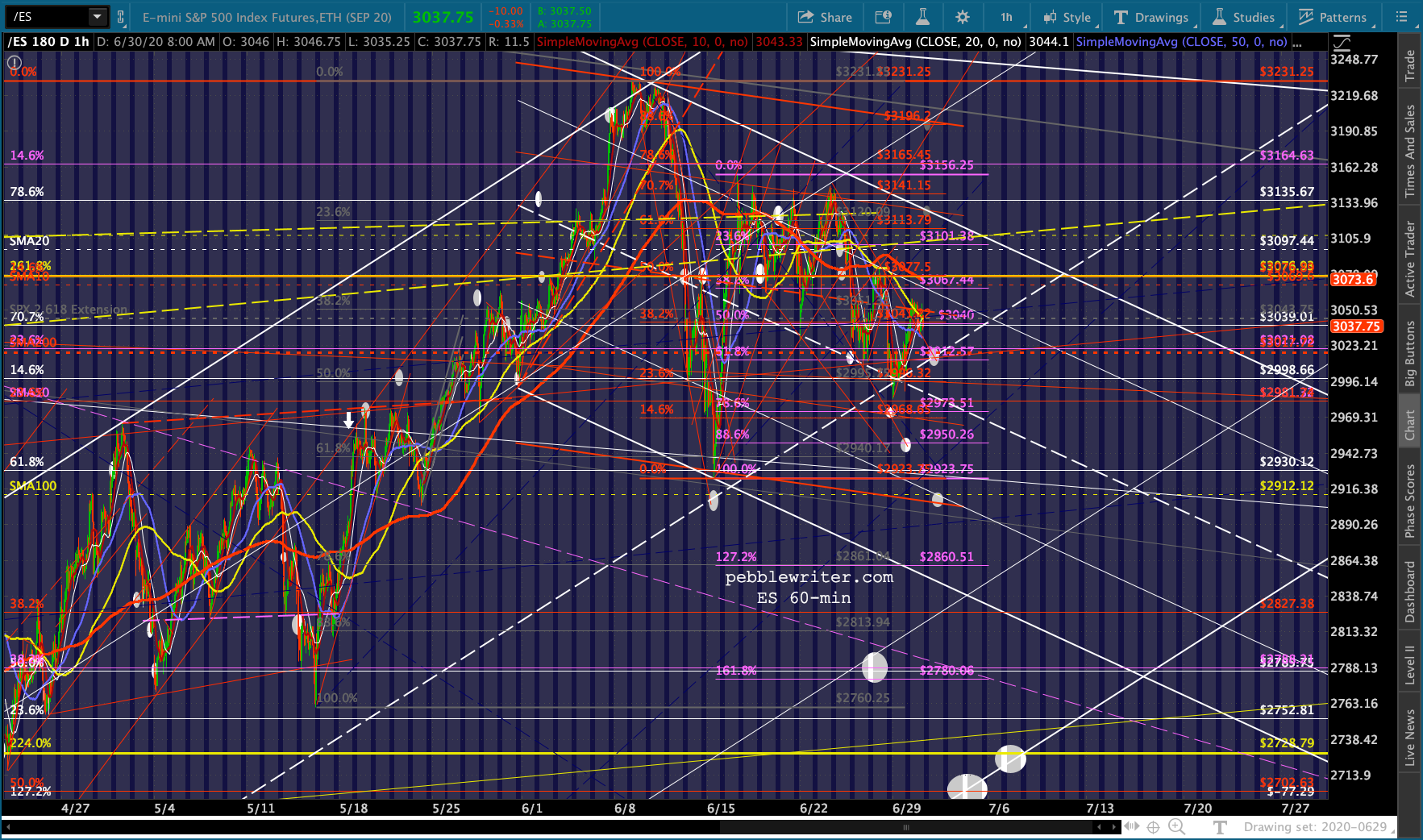

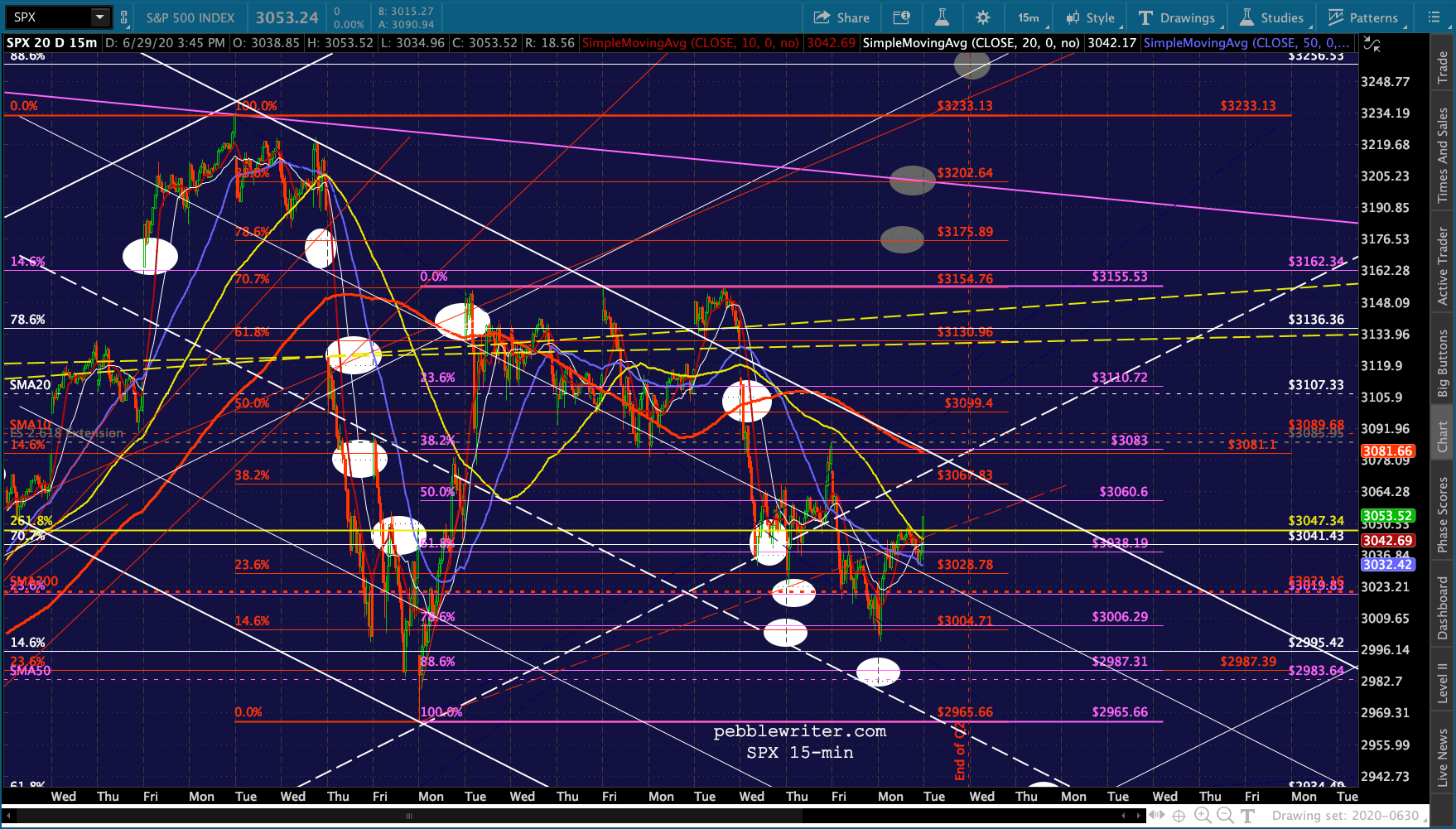

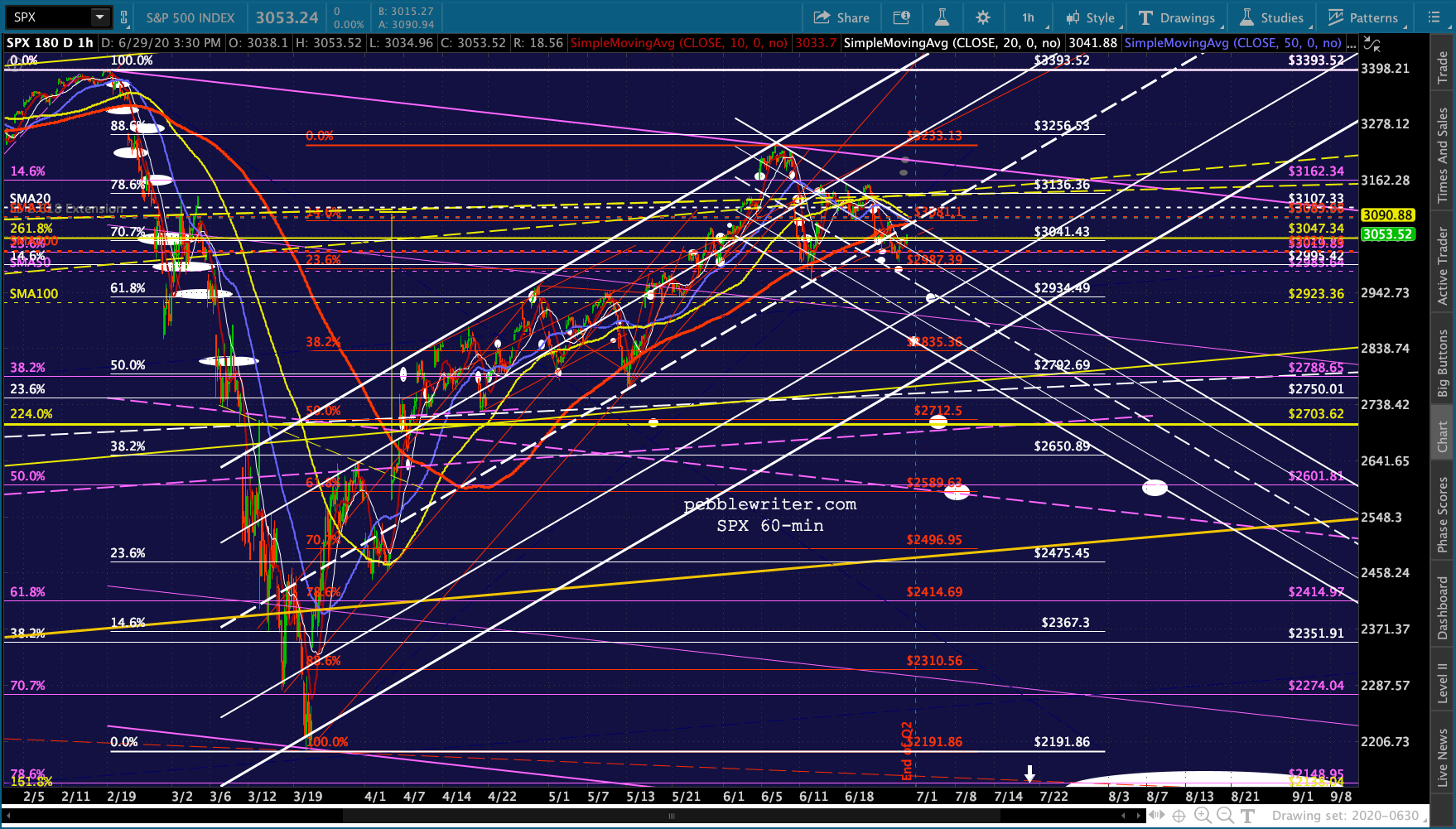

continued for members…Futures are off modestly despite efforts to prop them up one more session. Yesterday’s stick save preserved the white channel midline and put ES and SPX back above their SMA200s.

continued for members…Futures are off modestly despite efforts to prop them up one more session. Yesterday’s stick save preserved the white channel midline and put ES and SPX back above their SMA200s. But, they remain in falling channels with a bearish 10/20 cross. Unless prices can rally for another week or so (breaking out of the falling white channel) causing the rising SMA50 to cross above the SMA200, the outlook is still negative.

But, they remain in falling channels with a bearish 10/20 cross. Unless prices can rally for another week or so (breaking out of the falling white channel) causing the rising SMA50 to cross above the SMA200, the outlook is still negative.

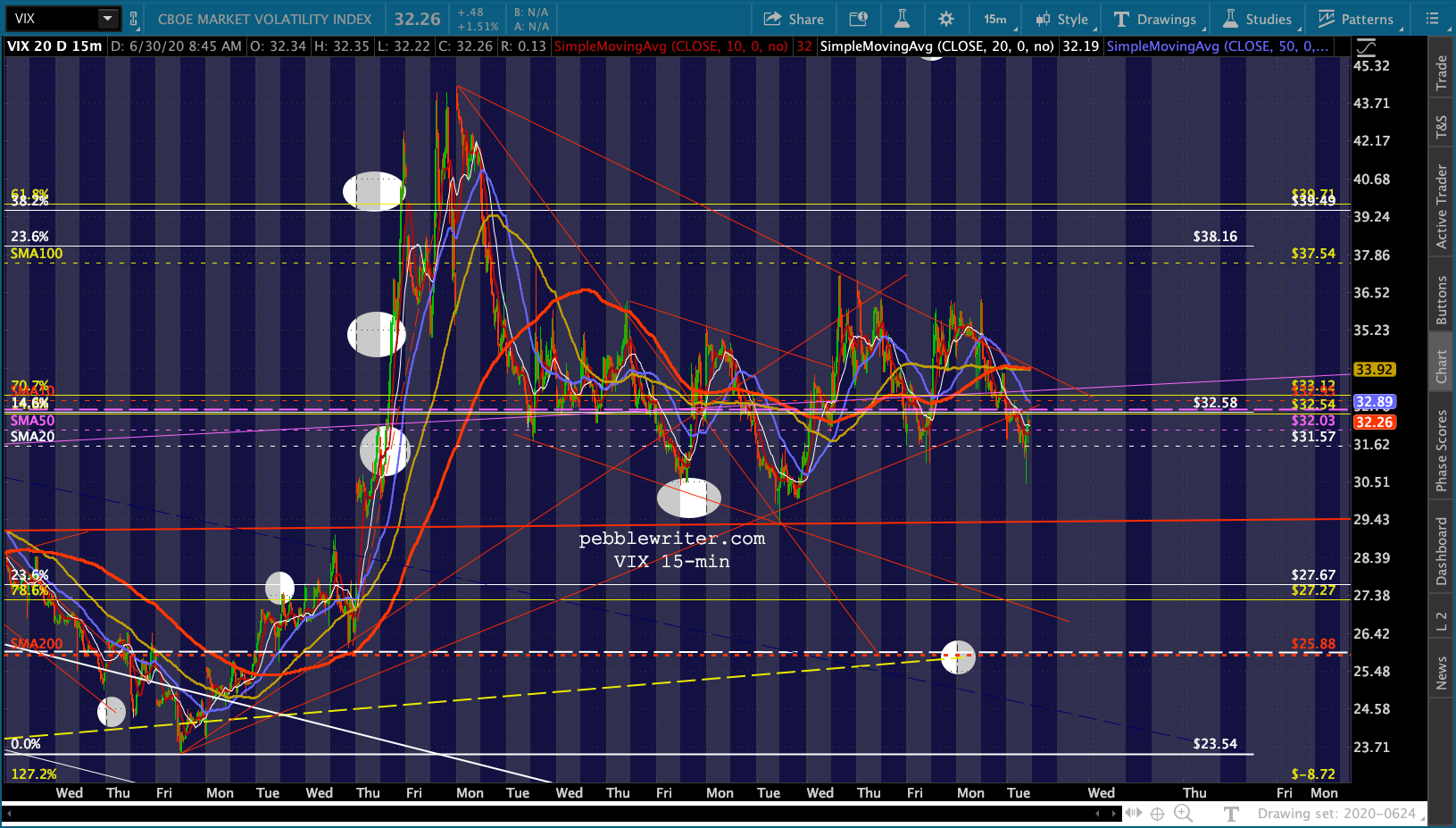

The other potential saviour remains VIX, which broke below and is backtesting its red TL, with the SMA200 and yellow TL still a potential magnet.

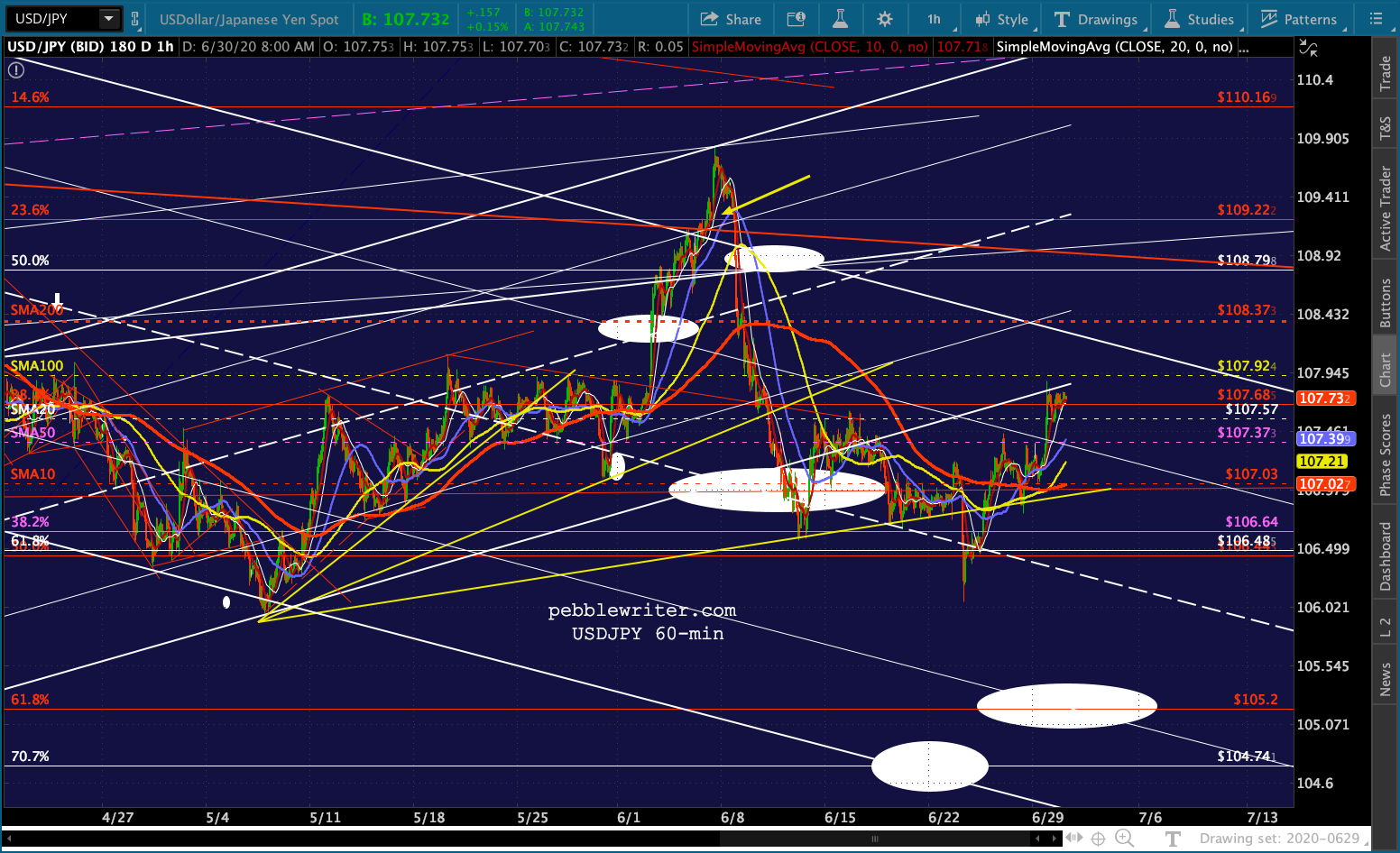

The other potential saviour remains VIX, which broke below and is backtesting its red TL, with the SMA200 and yellow TL still a potential magnet. USDJPY has done an excellent job of propping up stocks, but is still only backtesting the broken white channel. It would need to break back into it to have much of an impact going forward.

USDJPY has done an excellent job of propping up stocks, but is still only backtesting the broken white channel. It would need to break back into it to have much of an impact going forward.

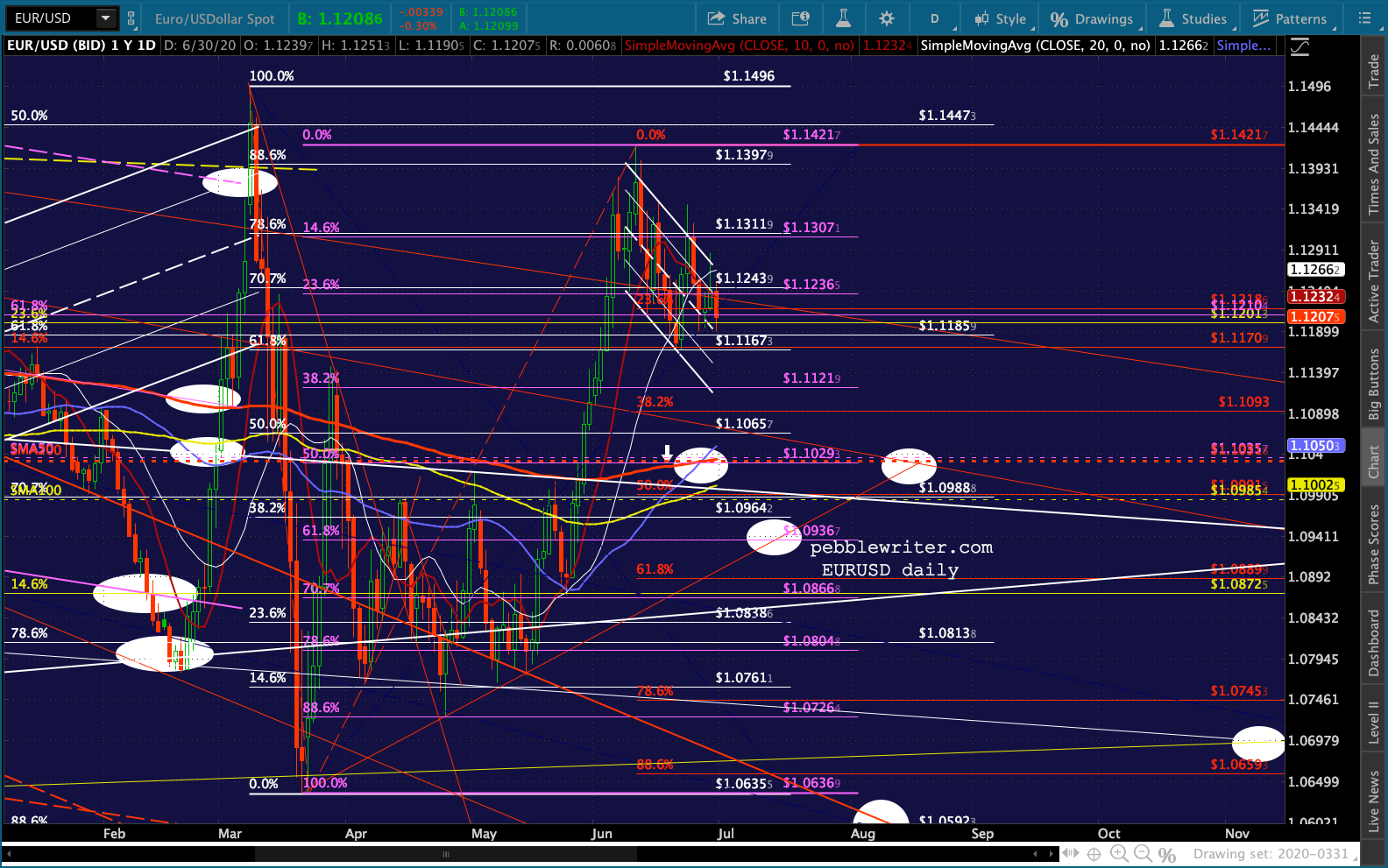

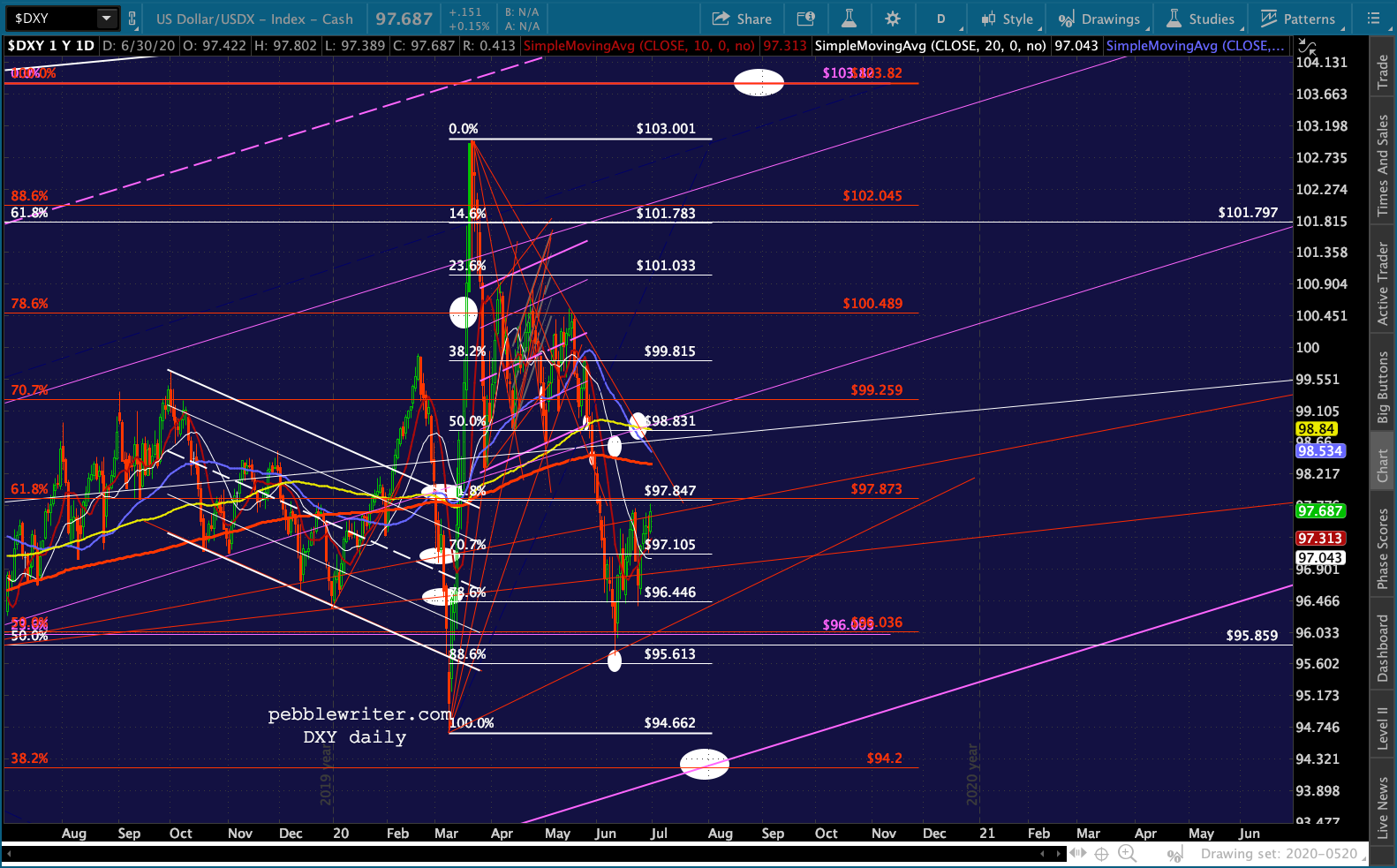

EURUSD continues to break down, which bodes well for a rising DXY. Depending on how far and how fast DXY rises, it can spell trouble for stocks.

EURUSD continues to break down, which bodes well for a rising DXY. Depending on how far and how fast DXY rises, it can spell trouble for stocks.

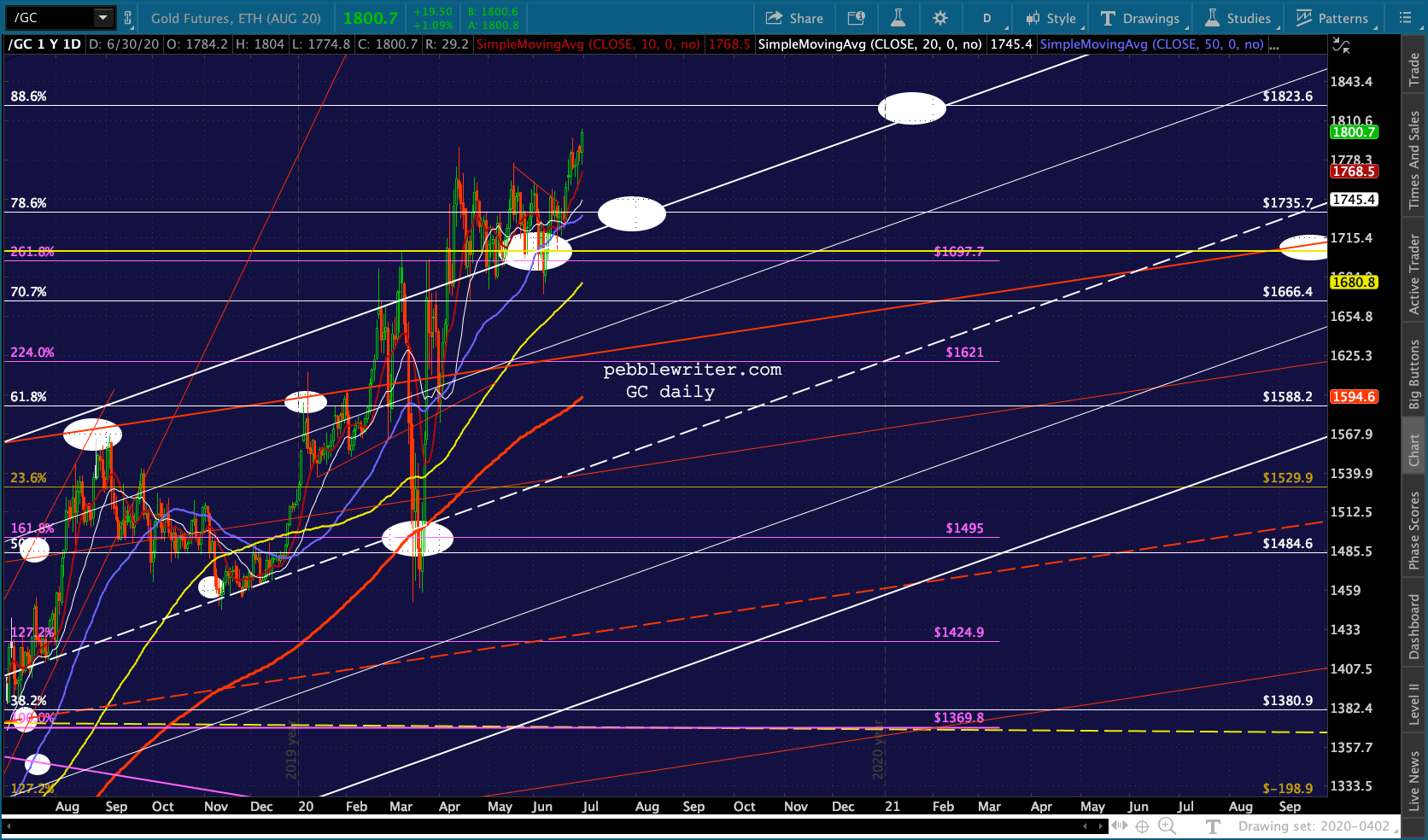

Gold is now only 23 away from our 1823.60 target.

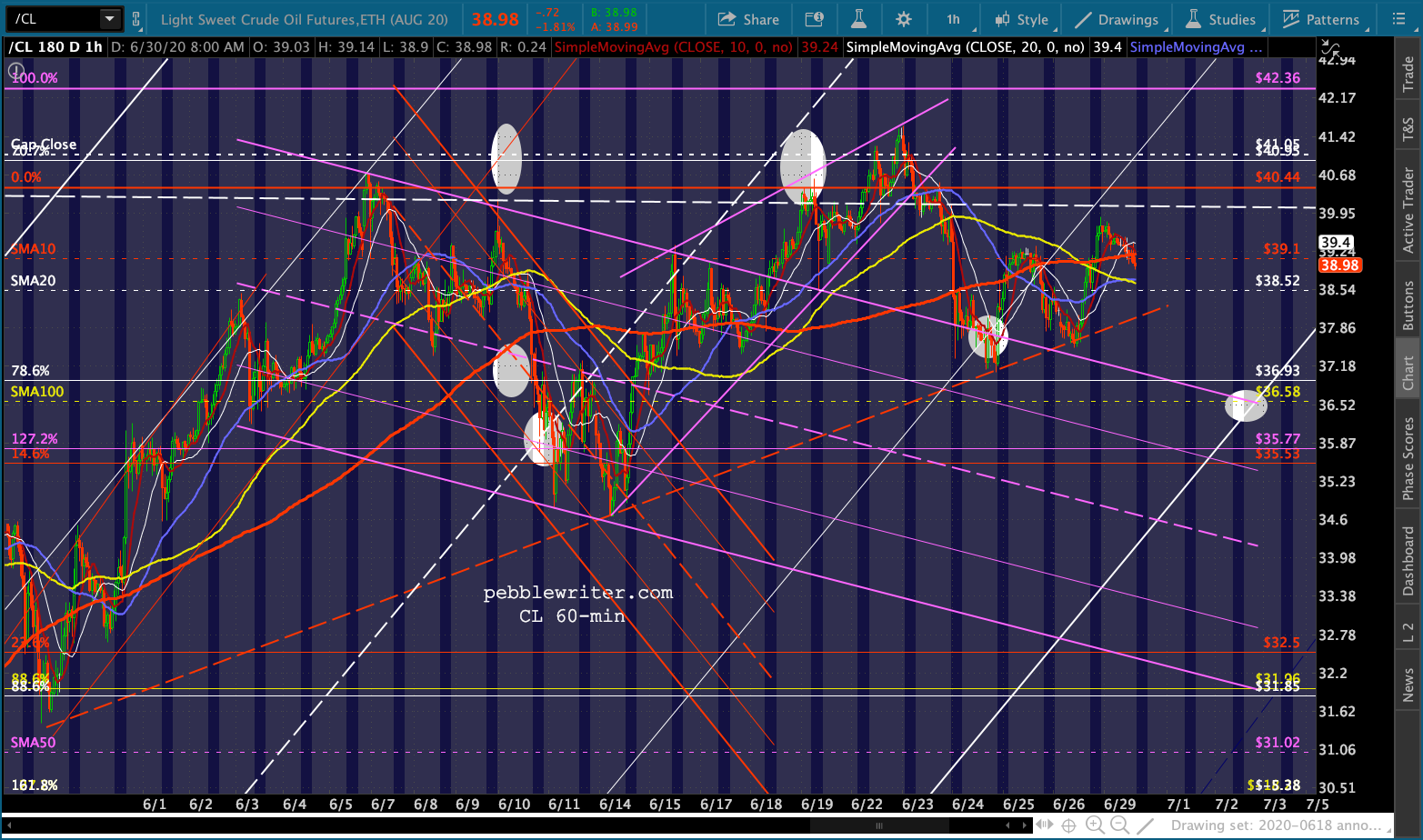

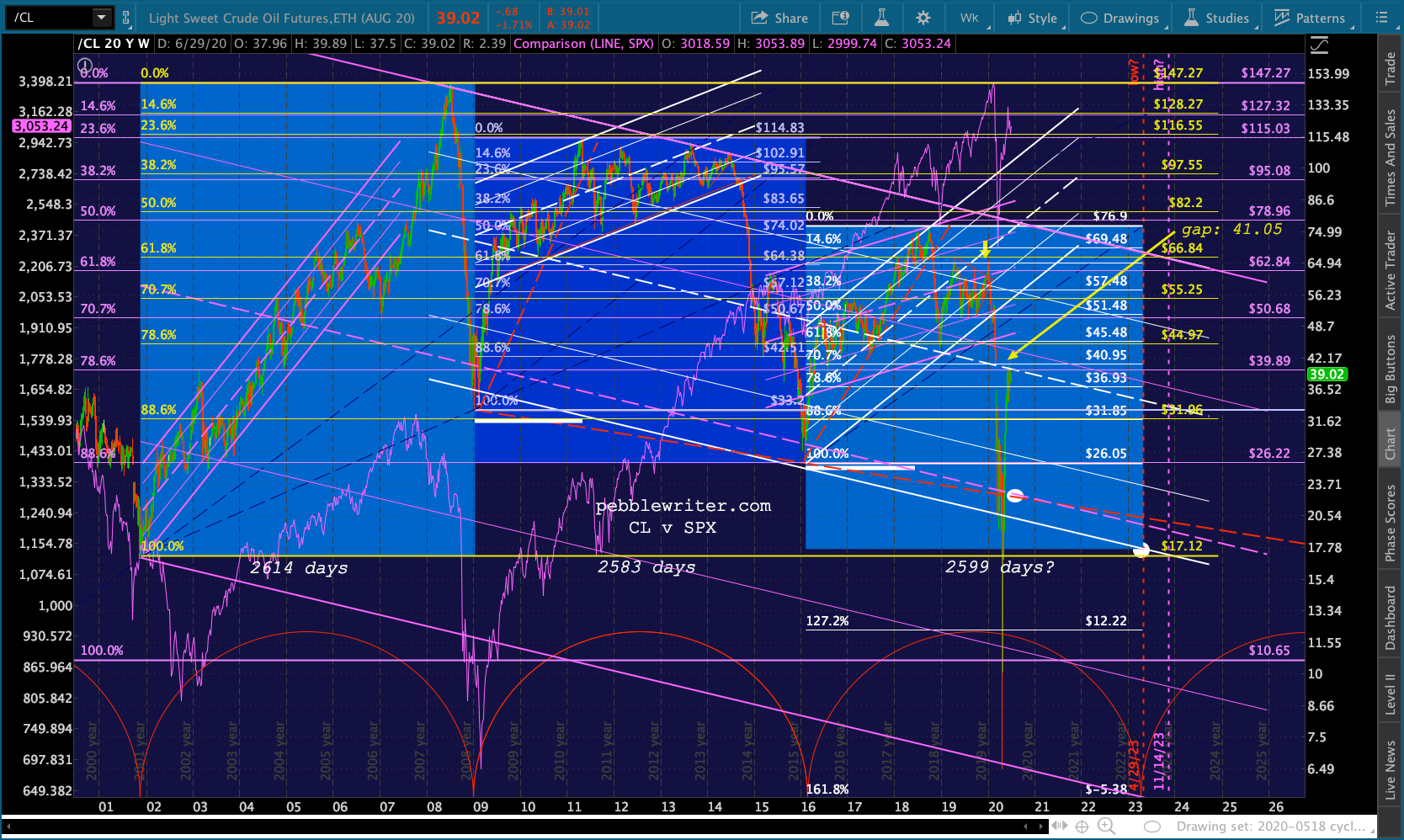

Gold is now only 23 away from our 1823.60 target. Oil and gas are both off this morning, though they’re holding trend.

Oil and gas are both off this morning, though they’re holding trend.

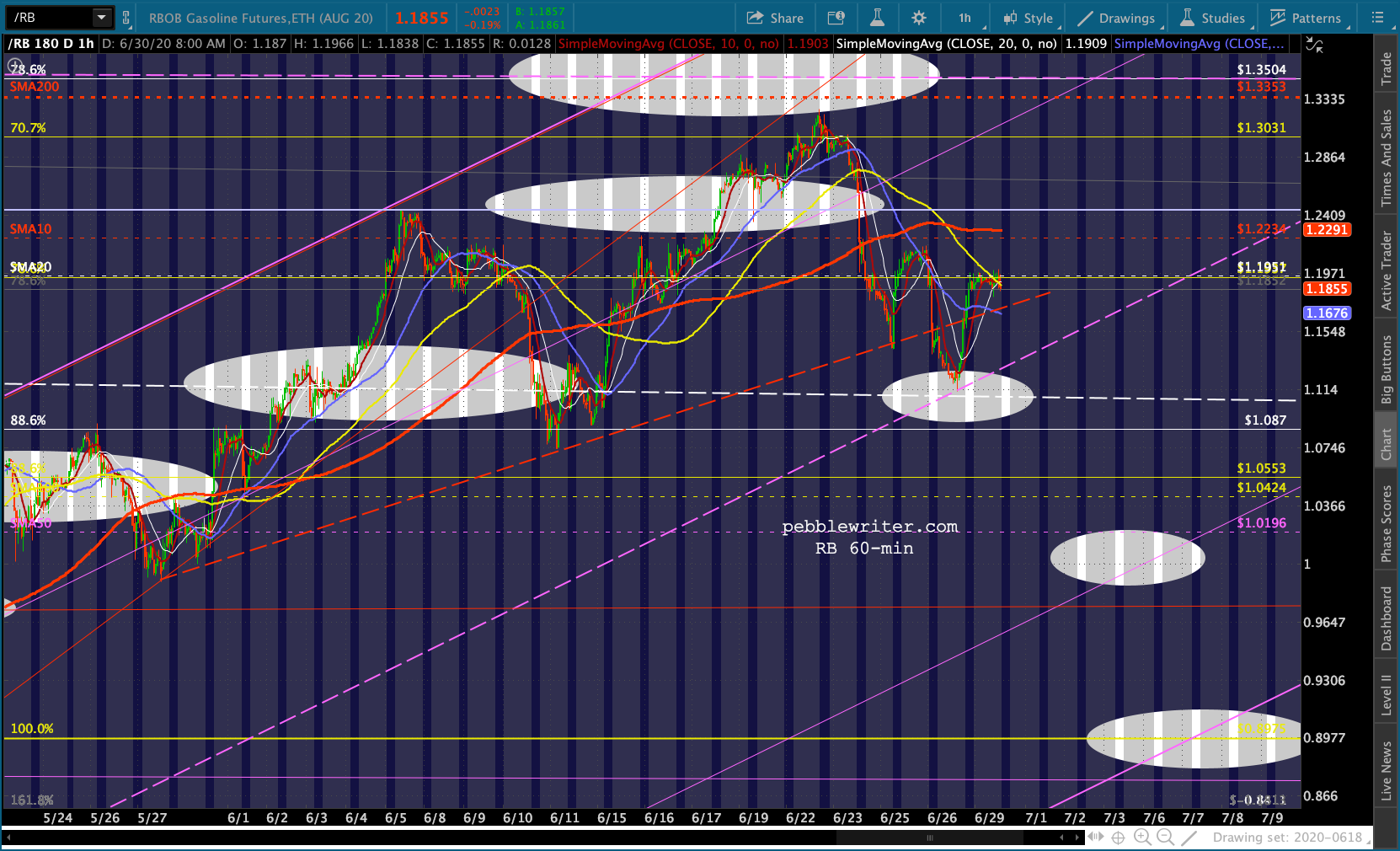

RB bounced off its purple midline and rebounded back above the red TL which broke down Friday.

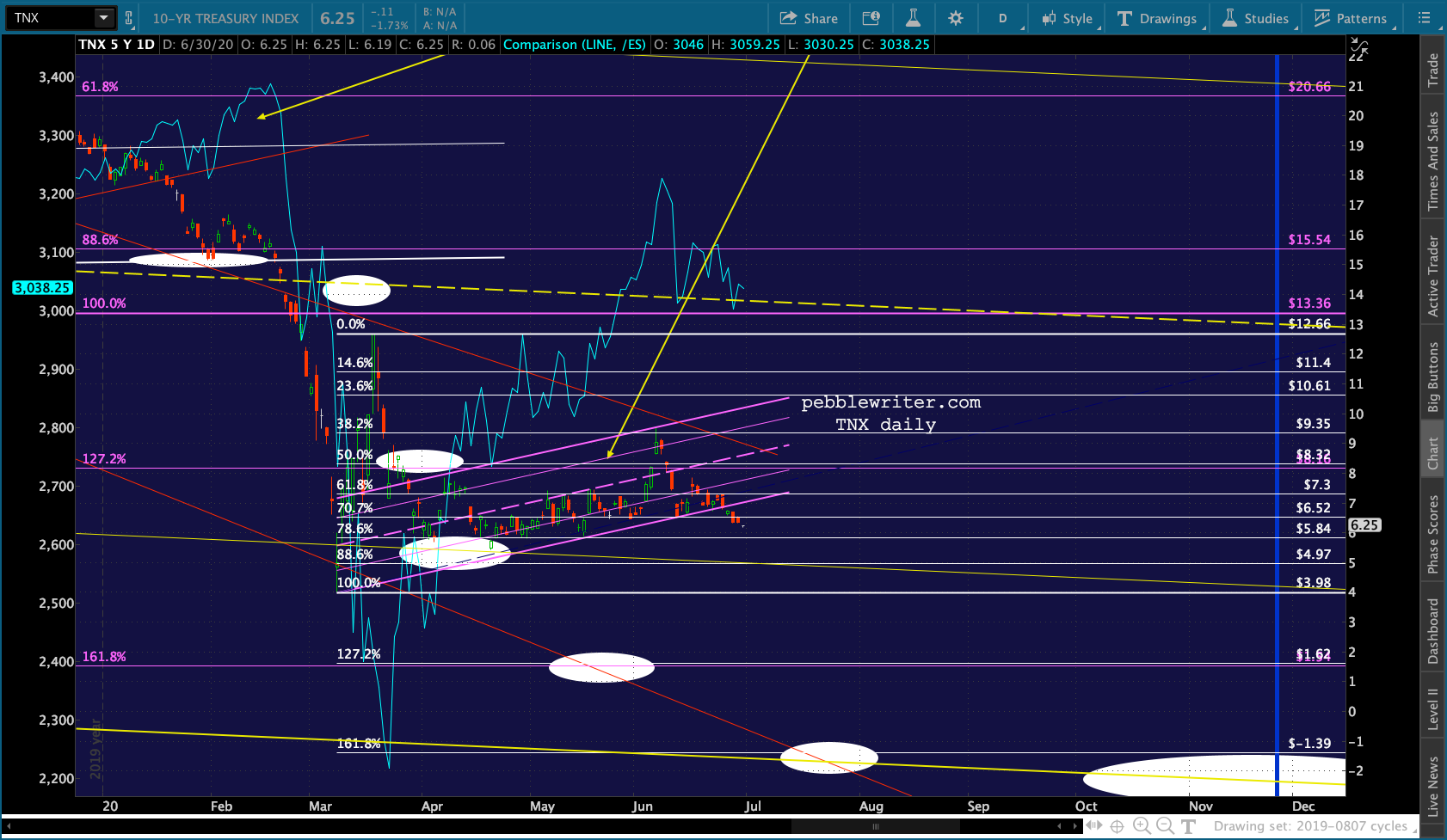

RB bounced off its purple midline and rebounded back above the red TL which broke down Friday. And, TNX continues to slump after breaking down last Thursday.

And, TNX continues to slump after breaking down last Thursday.

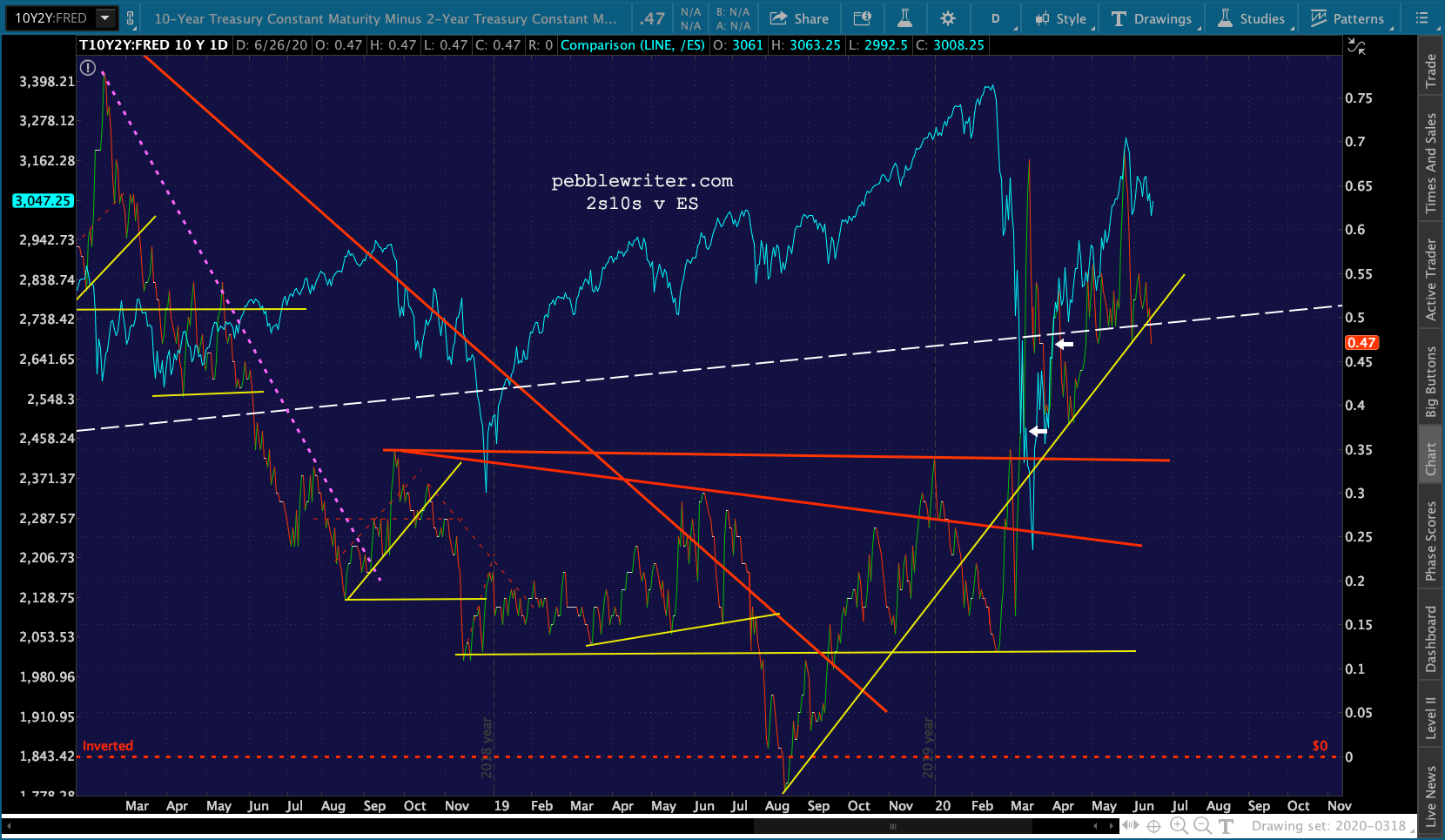

This has the potential to pressure the 2s10s lower – raising the risk of a breakdown, though it has thus far managed to bounce back each time.

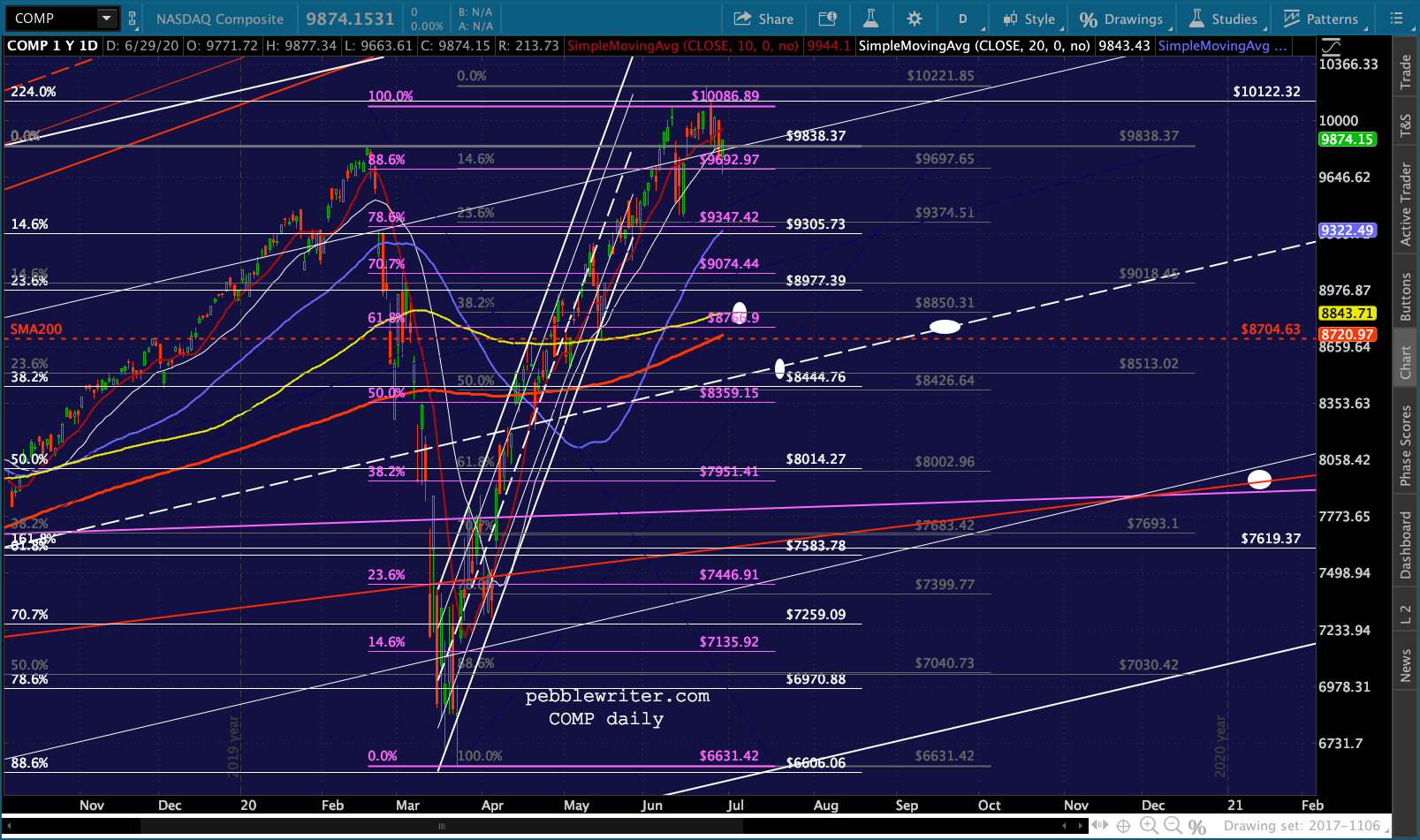

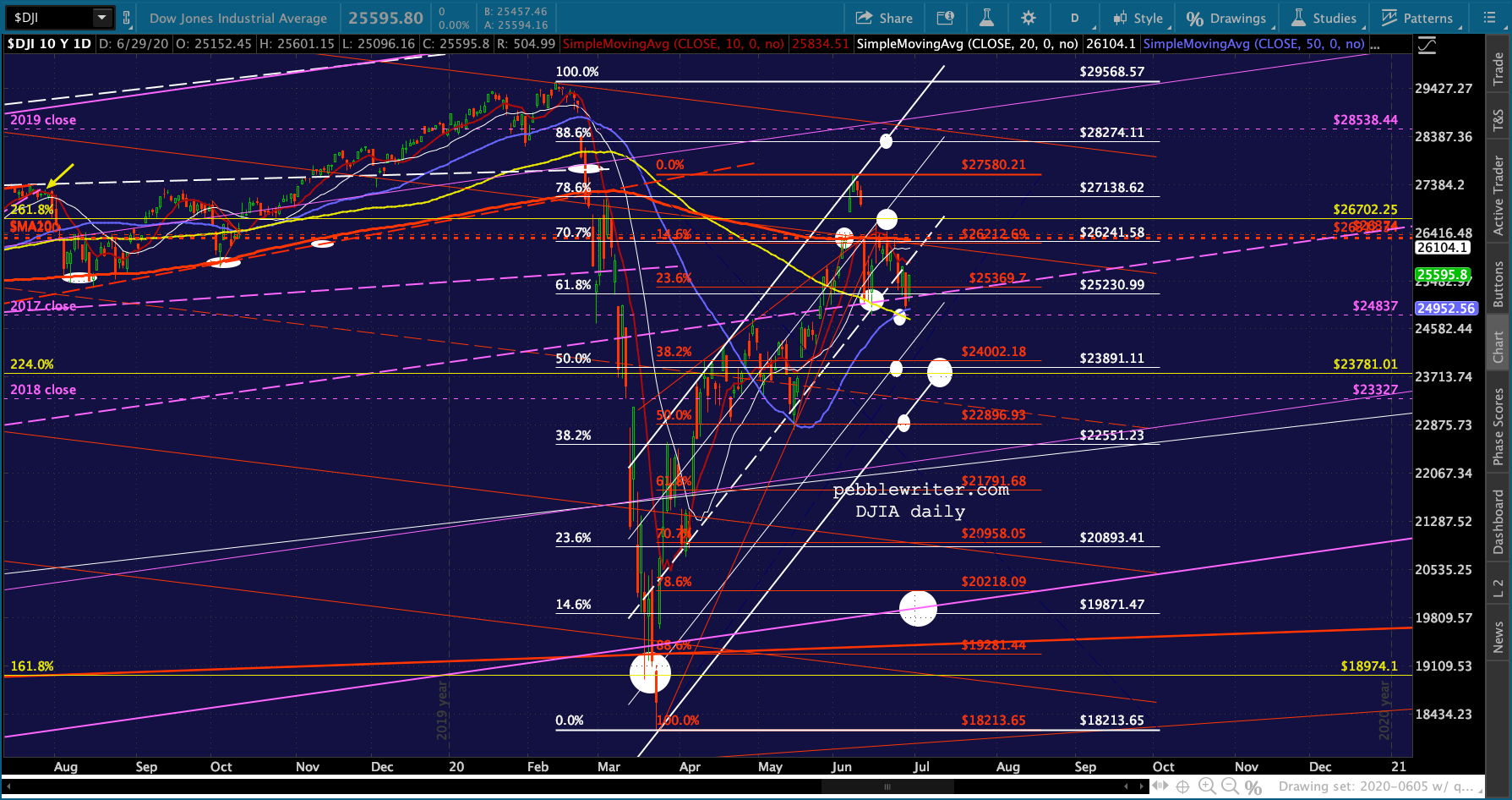

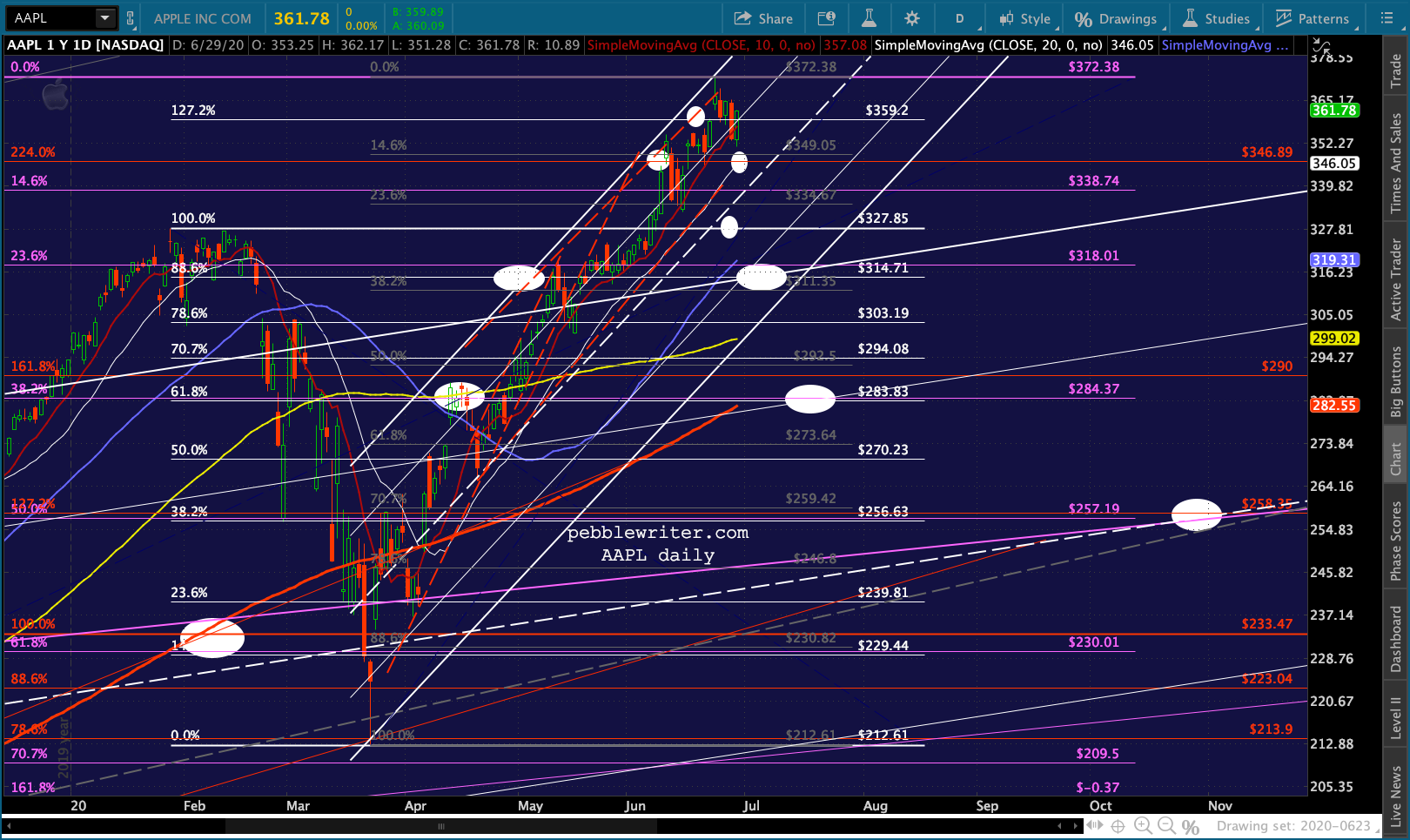

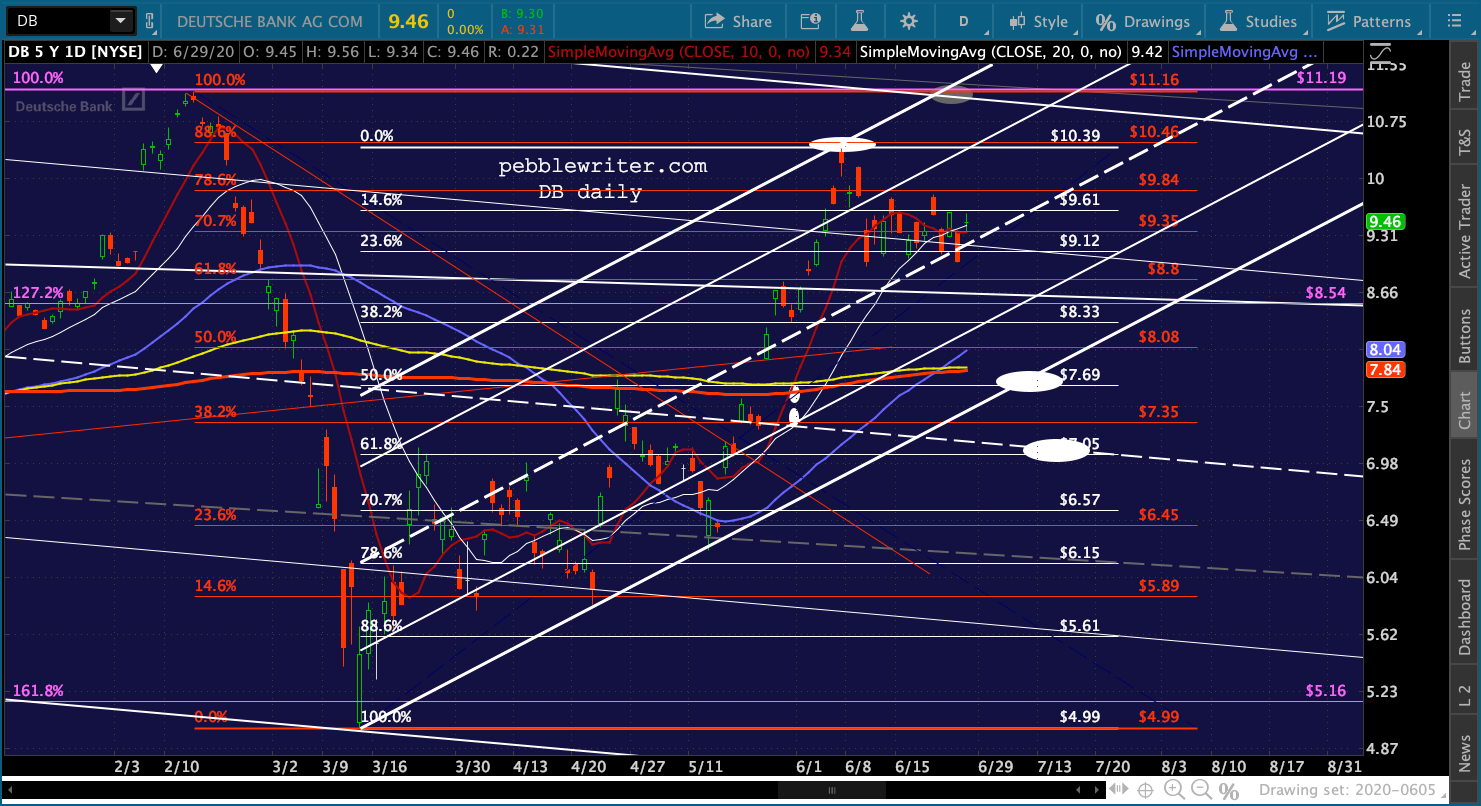

This has the potential to pressure the 2s10s lower – raising the risk of a breakdown, though it has thus far managed to bounce back each time. COMP and DJIA continue to look vulnerable here, as do individual stocks of interest including DB and AAPL.

COMP and DJIA continue to look vulnerable here, as do individual stocks of interest including DB and AAPL.

For those interested, Dr. Fauci et al will be testifying before the Senate Committee on Health Education Labor and Pensions. The testimony can be viewed HERE.

For those interested, Dr. Fauci et al will be testifying before the Senate Committee on Health Education Labor and Pensions. The testimony can be viewed HERE.

Powell and Mnuchin will testify before the House Committee on Financial Services at 12:30. The proceedings can be viewed HERE.

Unless something extraordinary happens, I’ll return to the bond market update begun on Friday. It has morphed into a quarter-end review of the big picture, something I think would be more interesting to most. As such, it is taking longer than expected.

Last, I plan on taking Monday July 6 off and will likely post very little or not at all on that day.