For those looking for inflation to top out, today’s PPI report of 0.4% versus 0.2% consensus was a disappointment.

After ramping sharply overnight, futures are now trying to hold on to meager gains. Meanwhile, the yen has plunged to levels not seen since 1998. If USDJPY tops 147.65, the previous high was back in 1990. The BoJ’s commitment to the yen carry trade is astounding. Talk about “all in…”

Meanwhile, the yen has plunged to levels not seen since 1998. If USDJPY tops 147.65, the previous high was back in 1990. The BoJ’s commitment to the yen carry trade is astounding. Talk about “all in…” Don’t wander too far from your computer. Fed minutes are due out at 2pm ET today and CPI comes out tomorrow morning.

Don’t wander too far from your computer. Fed minutes are due out at 2pm ET today and CPI comes out tomorrow morning.

continued for members…

An assortment of charts I’m watching closely…

SPX and ES are slipping toward their Feb 2020 highs – shown here on a clean SPY chart.

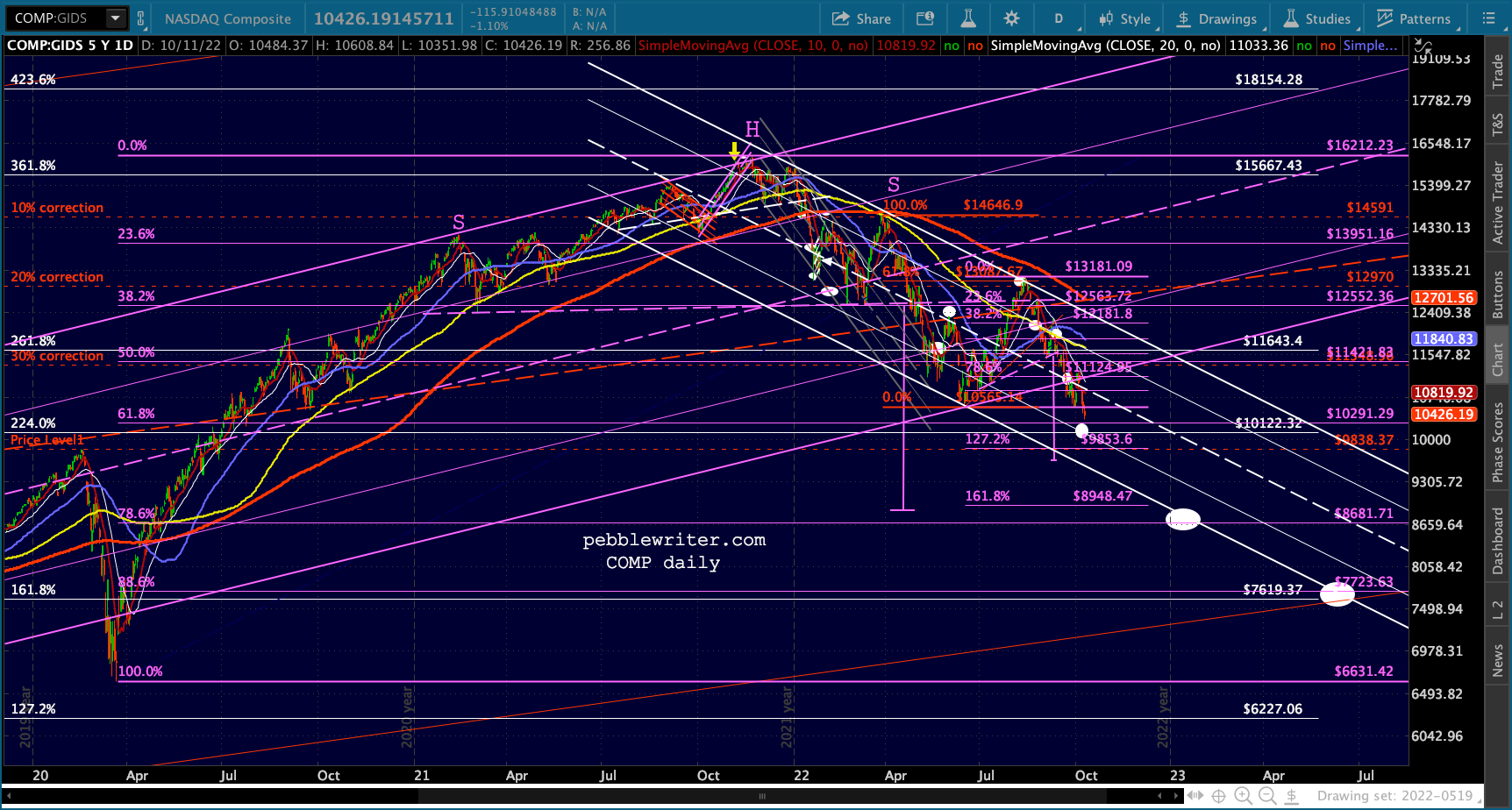

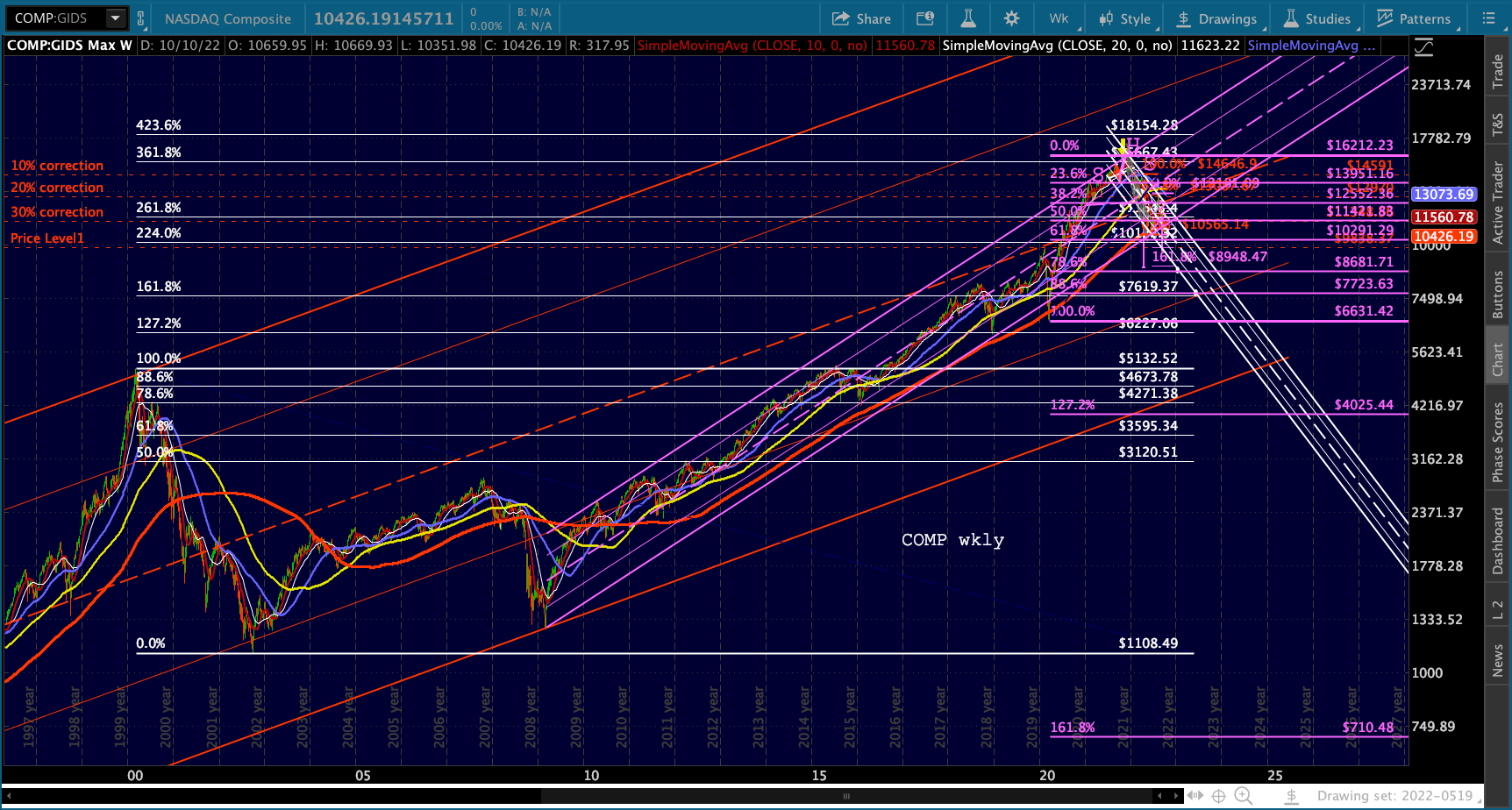

COMP is coming up on its .618, with its 2.24 and Feb 2020 highs just below.

COMP is coming up on its .618, with its 2.24 and Feb 2020 highs just below. Remember, it has already broken down from its purple channel from 2009. So, if the 2020 highs give way, it’s probably headed for the purple .786 by the end of the year or even the purple .886 next summer.

Remember, it has already broken down from its purple channel from 2009. So, if the 2020 highs give way, it’s probably headed for the purple .786 by the end of the year or even the purple .886 next summer. And, XLU is almost to the point where its cycle indicates should be a low. Note that this is the first time in 2 years that it has failed to make a higher low.

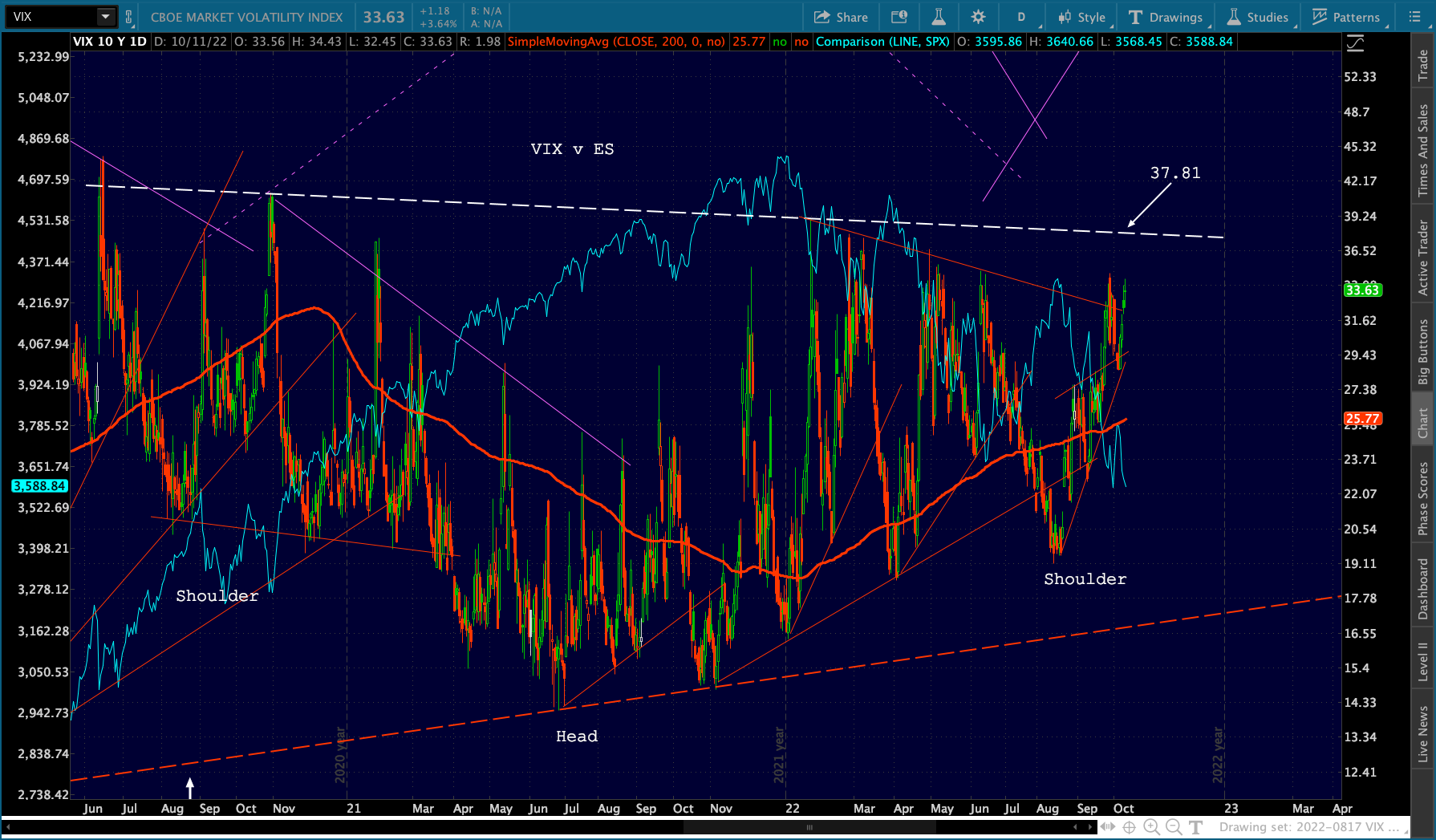

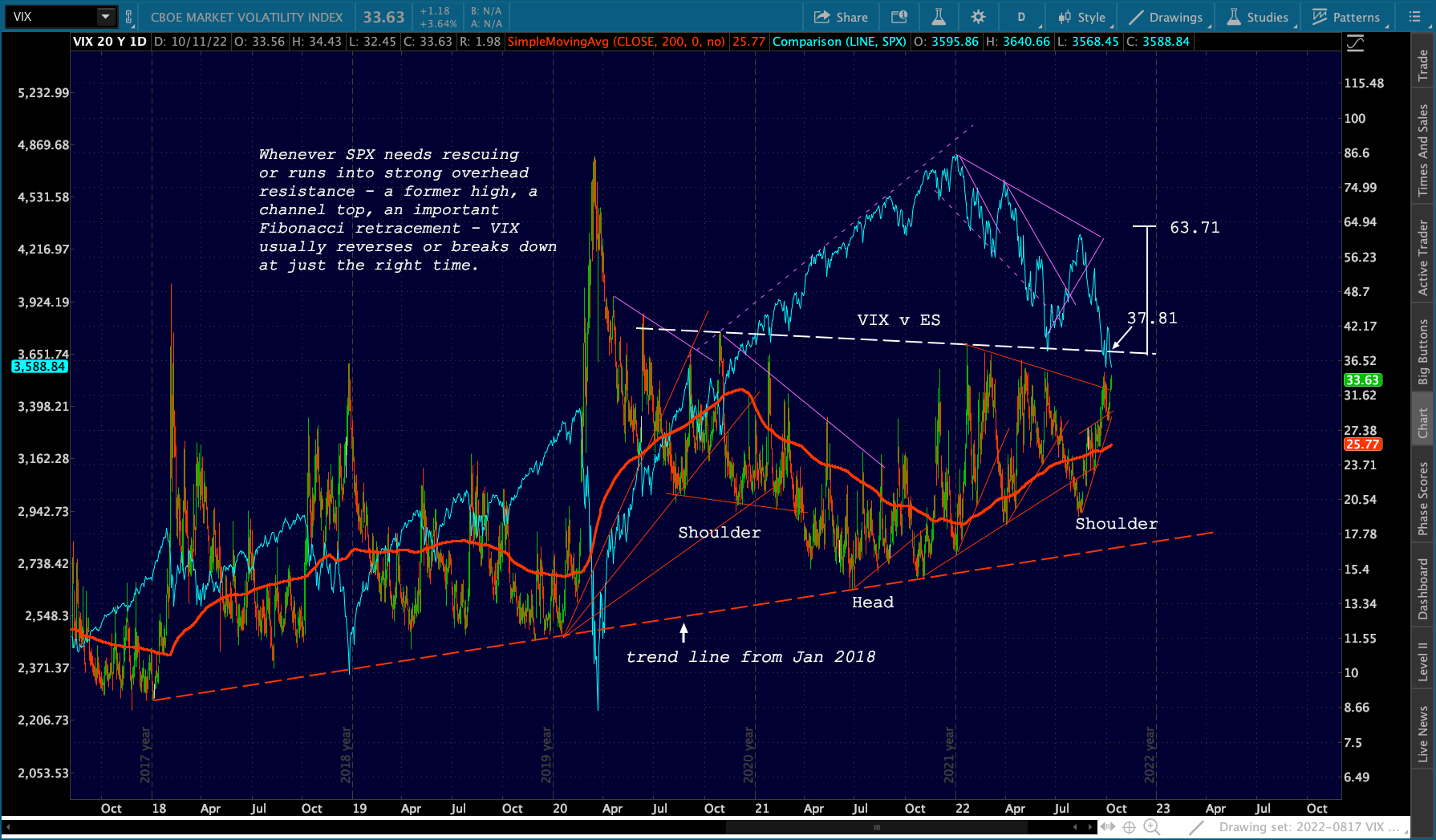

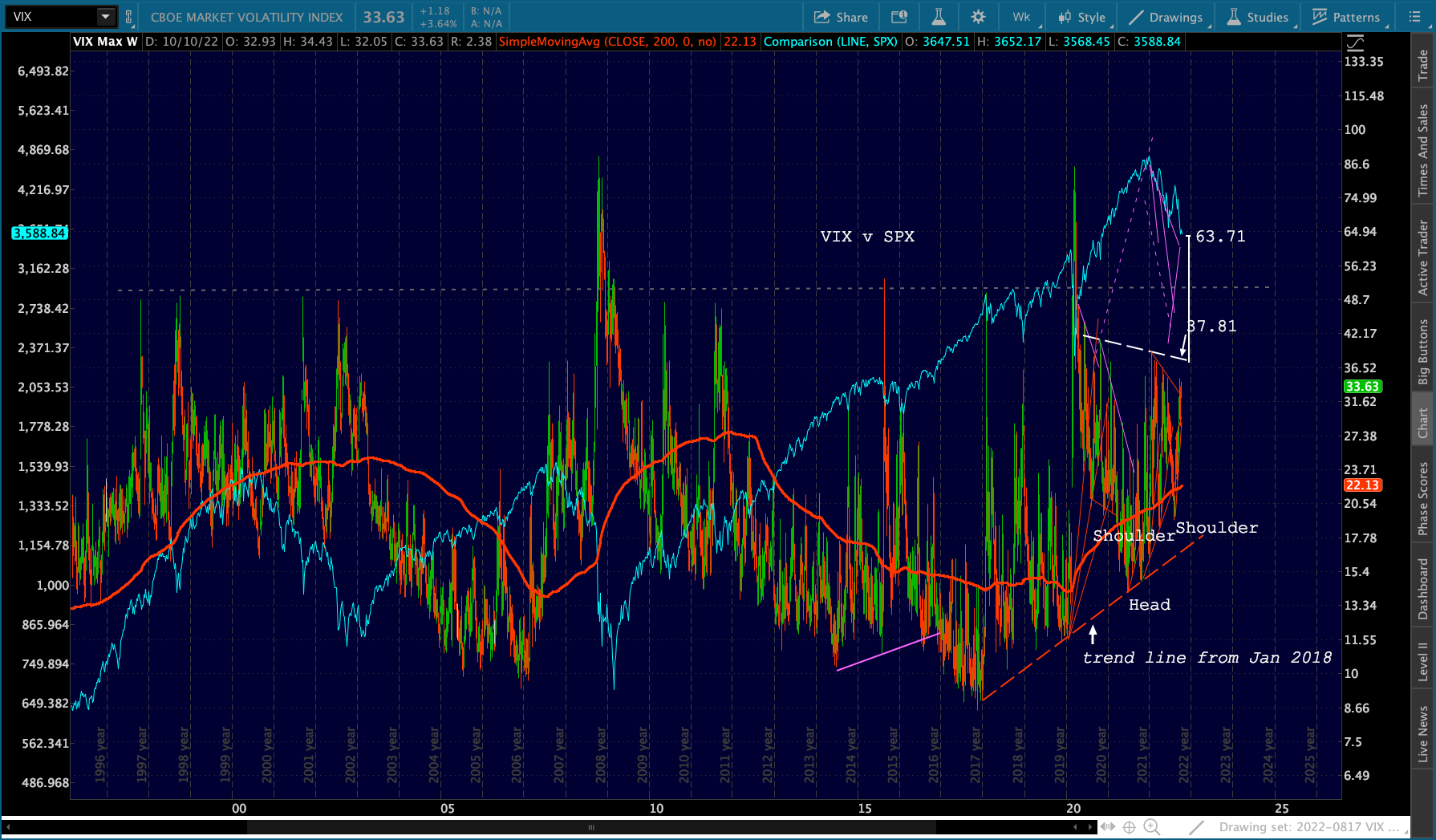

And, XLU is almost to the point where its cycle indicates should be a low. Note that this is the first time in 2 years that it has failed to make a higher low. Then there’s VIX. After finally breaking above and backtesting the red TL from March, VIX can set its sights on the neckline at 37.81. Needless to say, a rise above the neckline would target levels not seen since the pandemic and the GFC.

Then there’s VIX. After finally breaking above and backtesting the red TL from March, VIX can set its sights on the neckline at 37.81. Needless to say, a rise above the neckline would target levels not seen since the pandemic and the GFC.

For this reason, I suspect we’re close to an interim bottom and that it should occur as soon as tomorrow but sometime in the next two weeks.

For this reason, I suspect we’re close to an interim bottom and that it should occur as soon as tomorrow but sometime in the next two weeks.

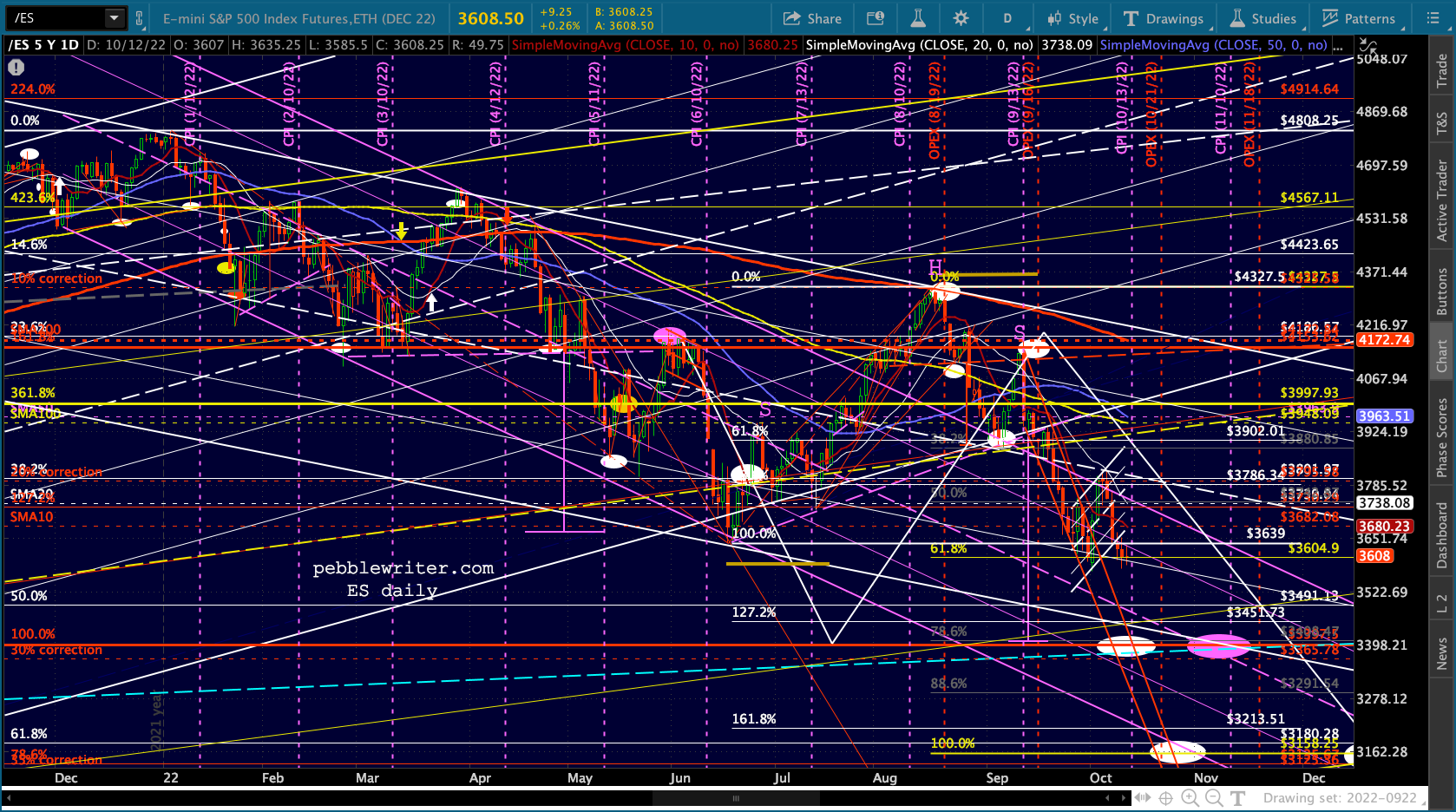

It’s clear that stocks’ biggest moves have come in the wake of CPI reports all year. With a few exceptions, ES rallies into the CPI report and sells off afterwards. There were two instances where ES declined into the report – March and May. In both cases, ES made a lower low before rebounding. I suspect the same will happen this week. If I were behind the curtain pushing the buttons, I would let markets sell off after the Fed’s minutes come out this afternoon and into the after hours as VIX climbs to 37.80, tagging 3400 after the CPI report, rebounding after tomorrow’s open so that SPX gets a chance to tag 4000ish.

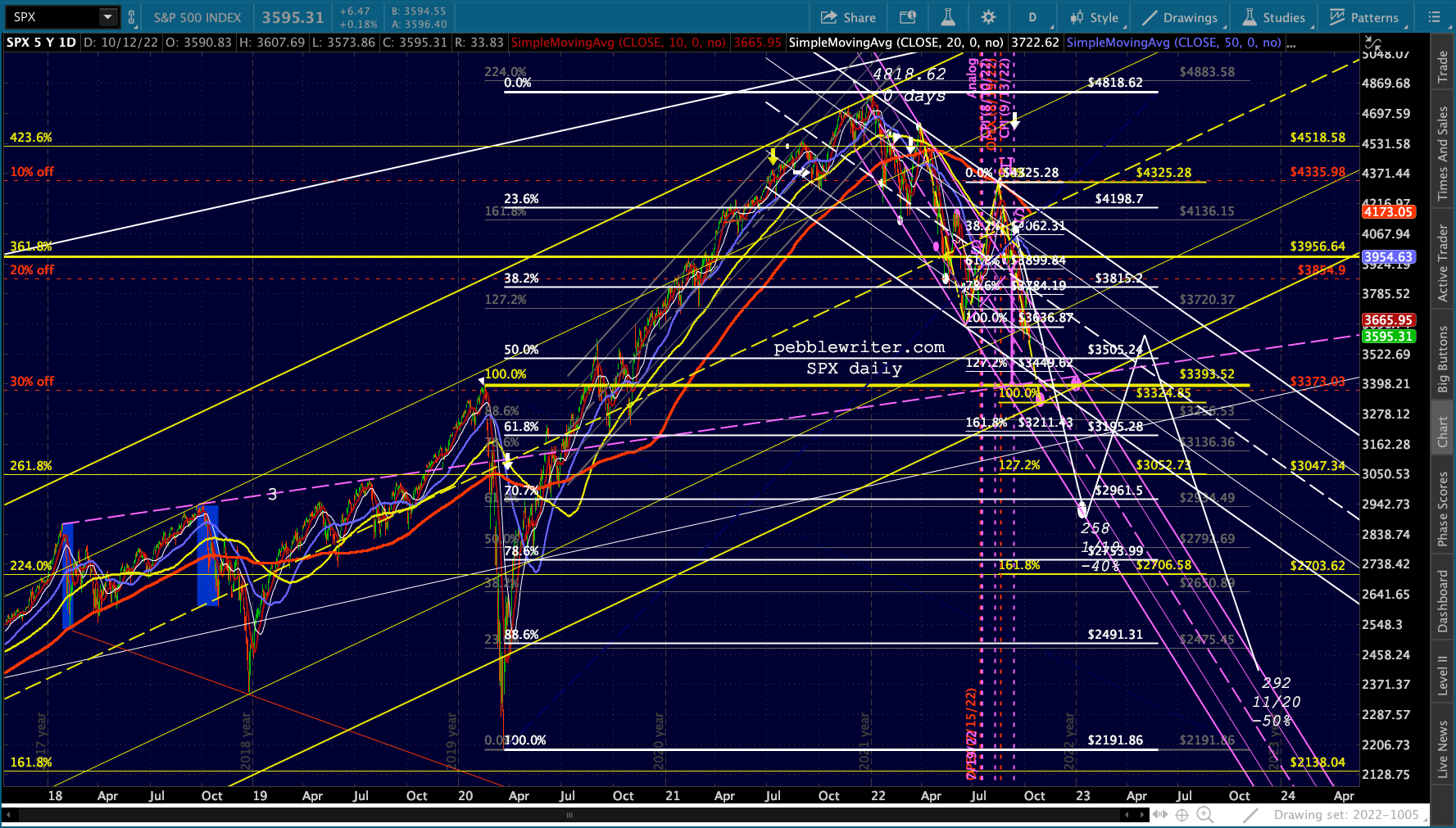

If I were behind the curtain pushing the buttons, I would let markets sell off after the Fed’s minutes come out this afternoon and into the after hours as VIX climbs to 37.80, tagging 3400 after the CPI report, rebounding after tomorrow’s open so that SPX gets a chance to tag 4000ish. Note that SPX’s 30% off mark at 3373 is right next to its Feb 2020 high of 3393 and only slightly above the C=A target of 3324 – which intersects the yellow channel bottom around the end of the month. The channel bottom intersects 3393 closer to the end of the year.

Note that SPX’s 30% off mark at 3373 is right next to its Feb 2020 high of 3393 and only slightly above the C=A target of 3324 – which intersects the yellow channel bottom around the end of the month. The channel bottom intersects 3393 closer to the end of the year.

The 30% mark would also give SPX a chance to get back in sync with the 2000 top. As we posted back in March [see: Should We Fear a Yield Curve Inversion?]

UPDATE: 3:15 PM

UPDATE: 3:15 PM

The minutes didn’t reveal anything we hadn’t already heard. Highlights:

“Some participants noted rising labor tensions, a new round of global energy price increases, further disruptions in supply chains, and a larger-than-expected pass-through of wage increases into price increases as potential shocks that, if they materialized, could compound an already challenging inflation problem.”

“Many participants emphasized that the cost of taking too little action to bring down inflation likely outweighed the cost of taking too much action.”

“Participants saw supply bottlenecks as likely continuing for a while longer, and a couple commented that constraints on production were increasingly taking the form of labor shortages rather than parts shortages. Participants judged that a softening in the labor market would be needed to ease upward pressures on wages and prices.”

Futures are still flat.