It was only 3 weeks ago, July 16. In that day’s post [see: On the Brink] we noted that the equity meltup was at risk from the bond market.

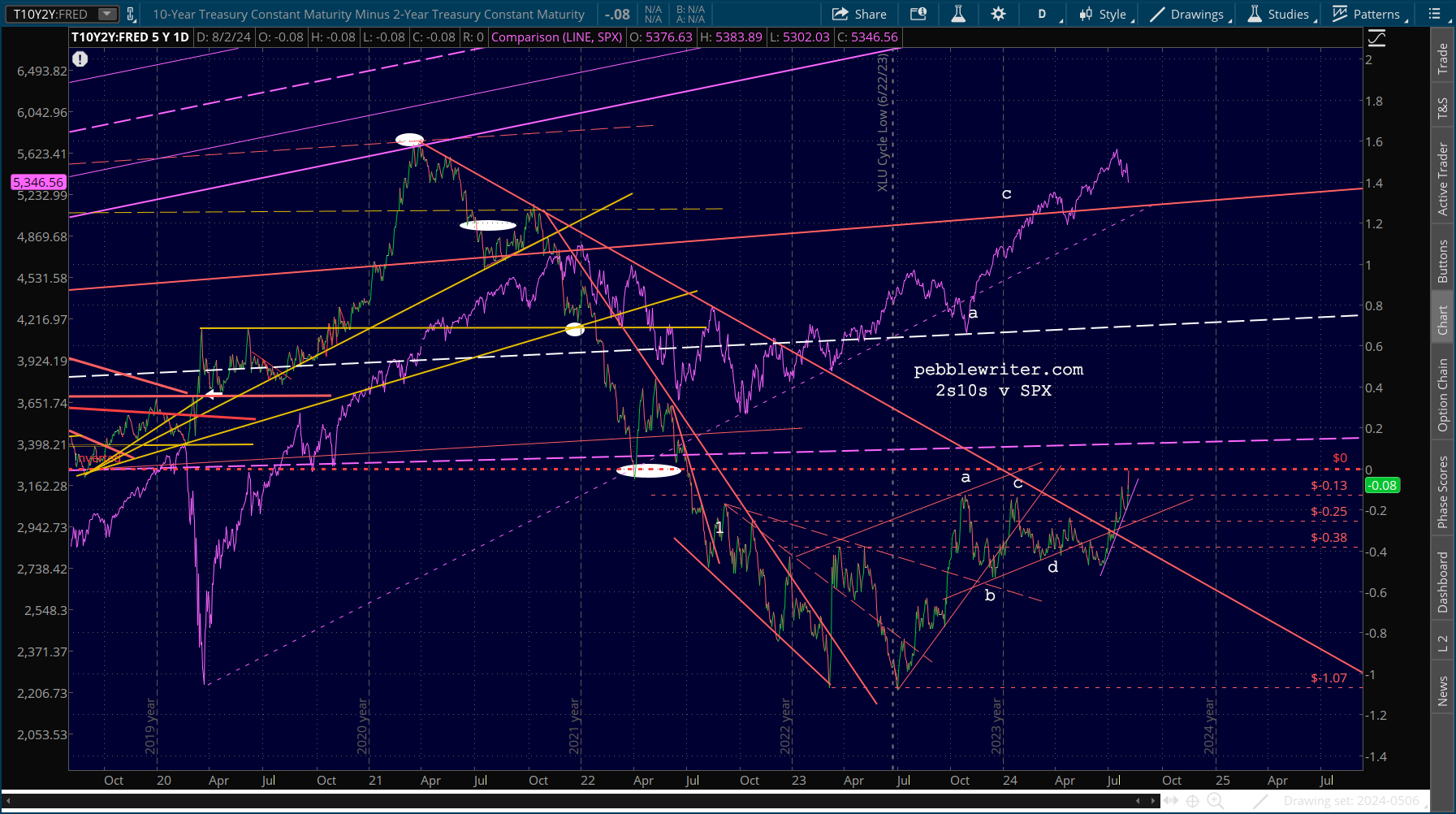

A rather worrisome development in the bond market is threatening equities’ meltup. We’ve discussed this many, many times in the past. A breakdown in the 2s10s leads to corrections, while a breakout leads to crashes.

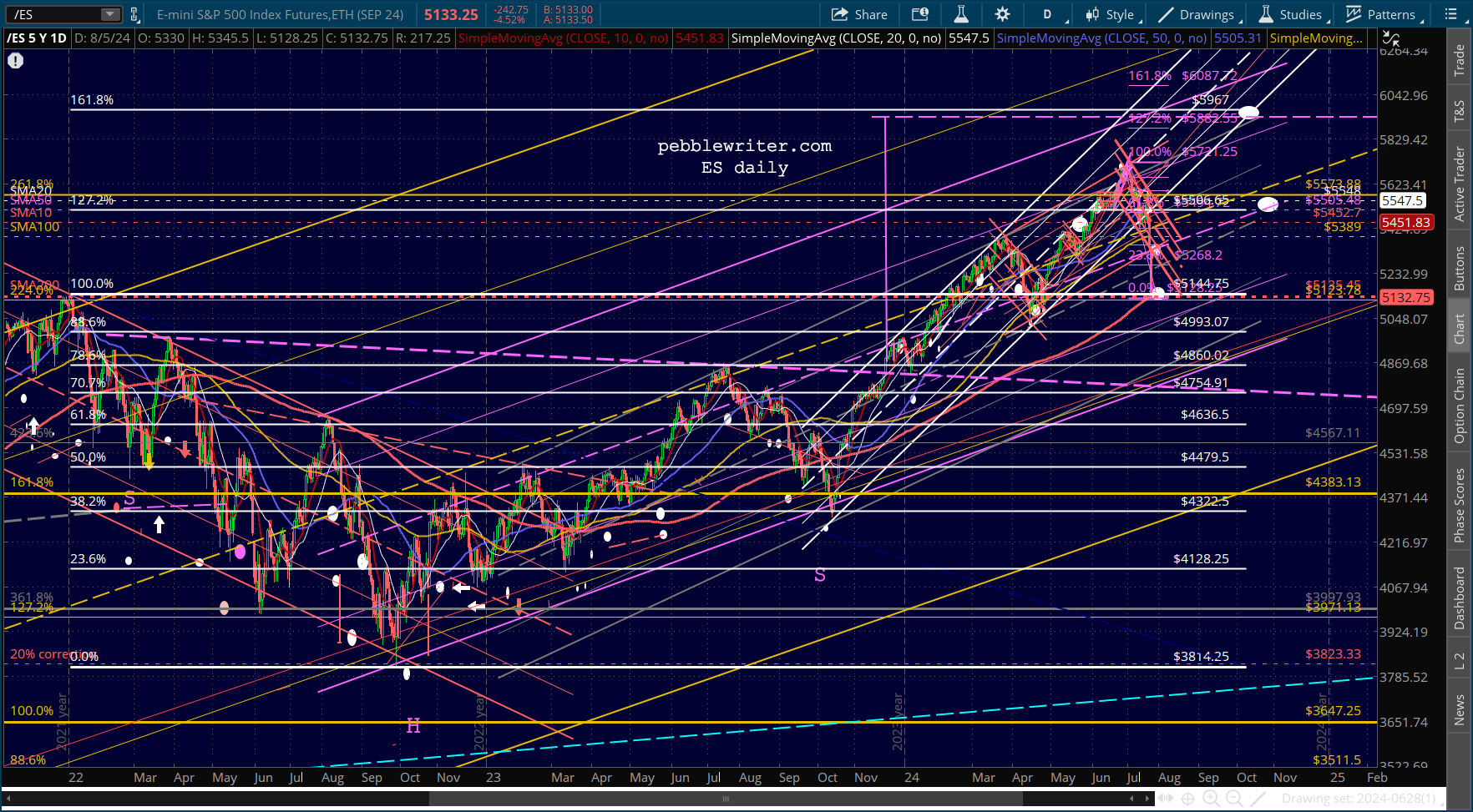

It’s always a bit unnerving to publicly utter the “c” word in the midst of a market meltup. At the open that day, S&P 500 was up over 19% ytd. In fact, it closed at an all-time high that day.

In hindsight, with SPX 10% now lower (Nikkei futures off 28%) and futures nailing our next downside target, it seems pretty obvious. Don’t look now, but the bond market is on the brink yet again – an even more important brink. And, the yen carry trade is fast unwinding.

Don’t look now, but the bond market is on the brink yet again – an even more important brink. And, the yen carry trade is fast unwinding.

continued for members…

The 2s10s have broken out and are on the brink of turning positive for the first time since July 2022. And, stocks are doing what they seem to always do under such circumstances: crashing.

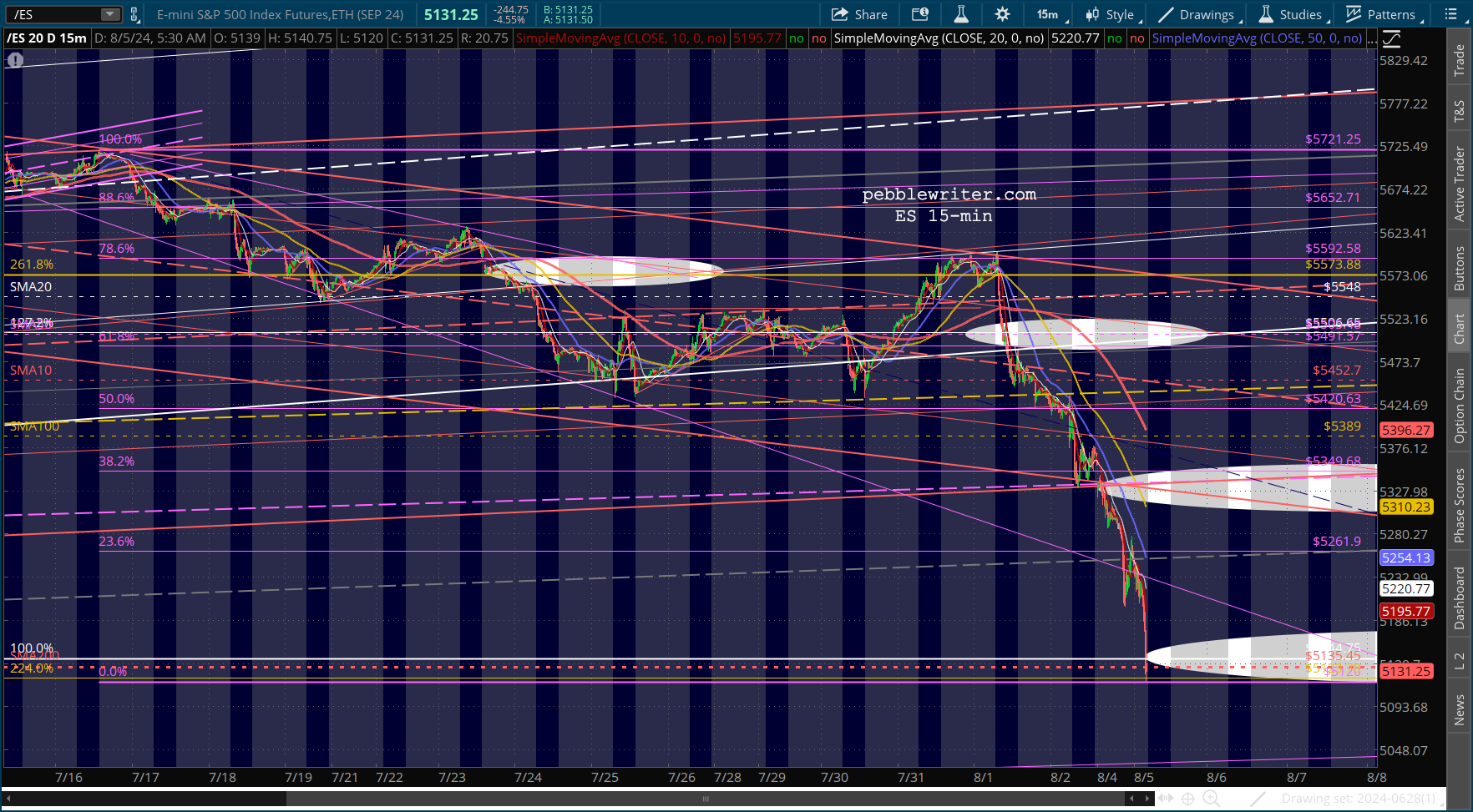

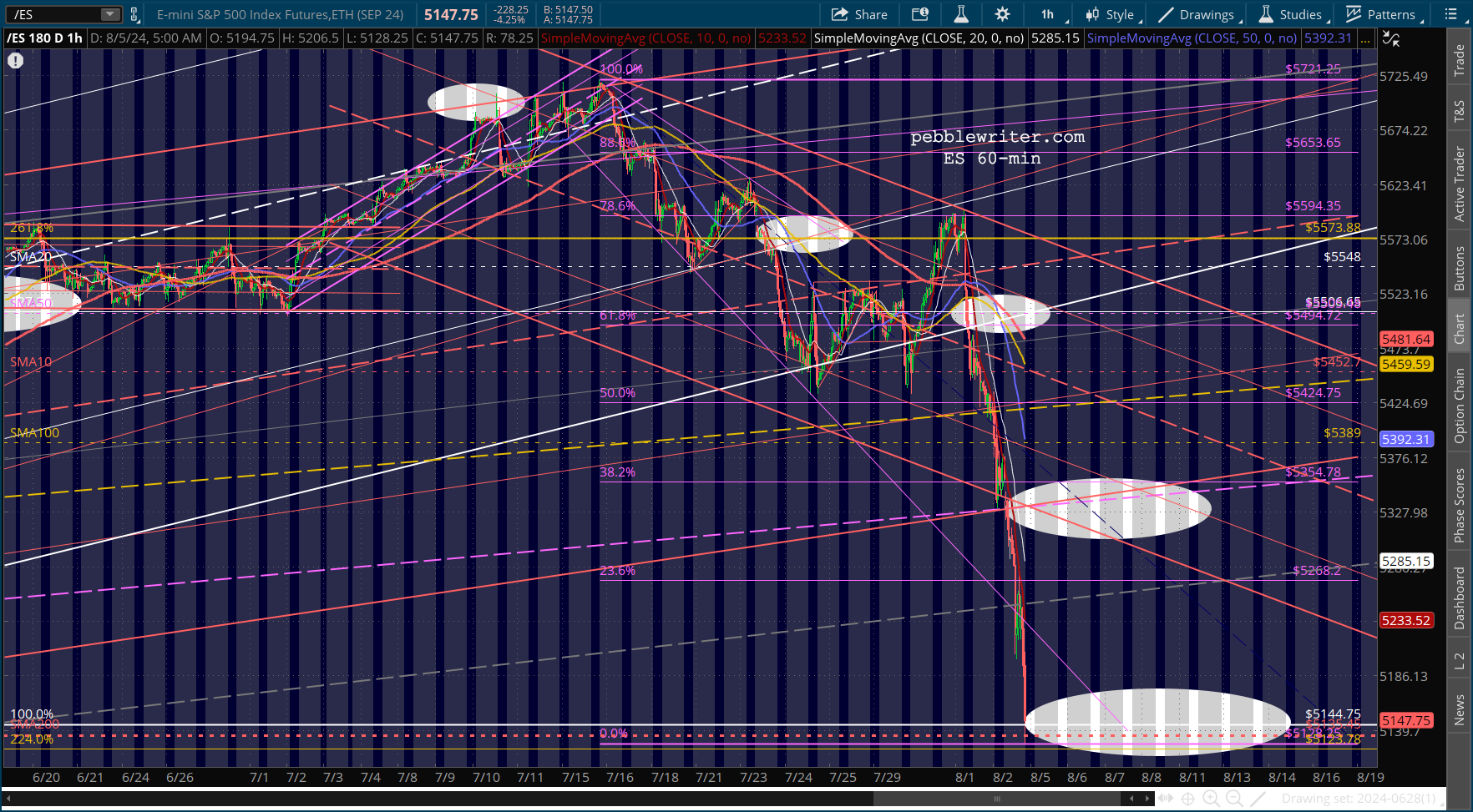

Futures were off as much as 260 points earlier and should attempt a bounce at the SMA200. Remember, this is not the same level as SPX’s SMA200, which is much lower at 5007.

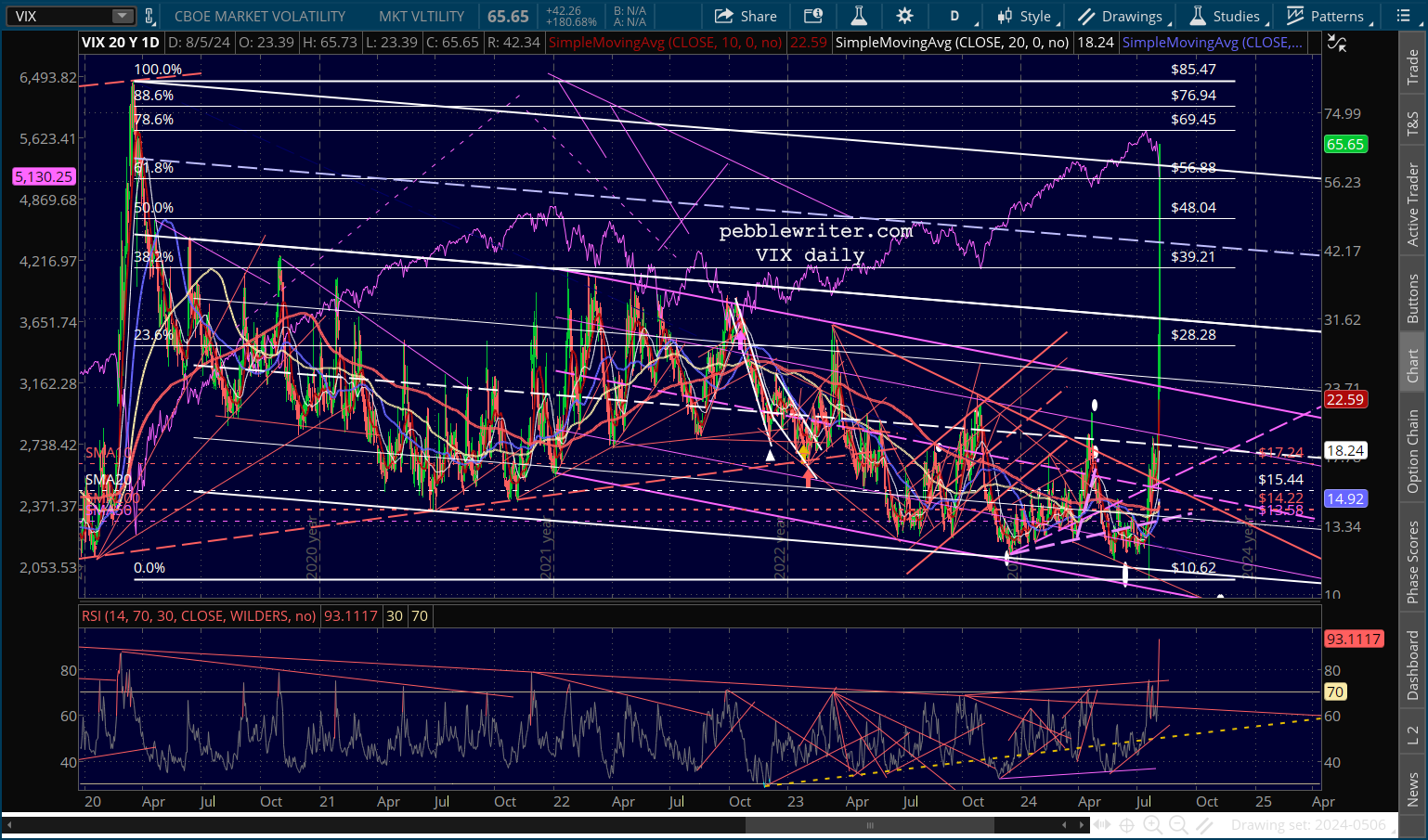

VIX has reached the highest level since the Mar 2020 lows and is massively overbought.

VIX has reached the highest level since the Mar 2020 lows and is massively overbought.

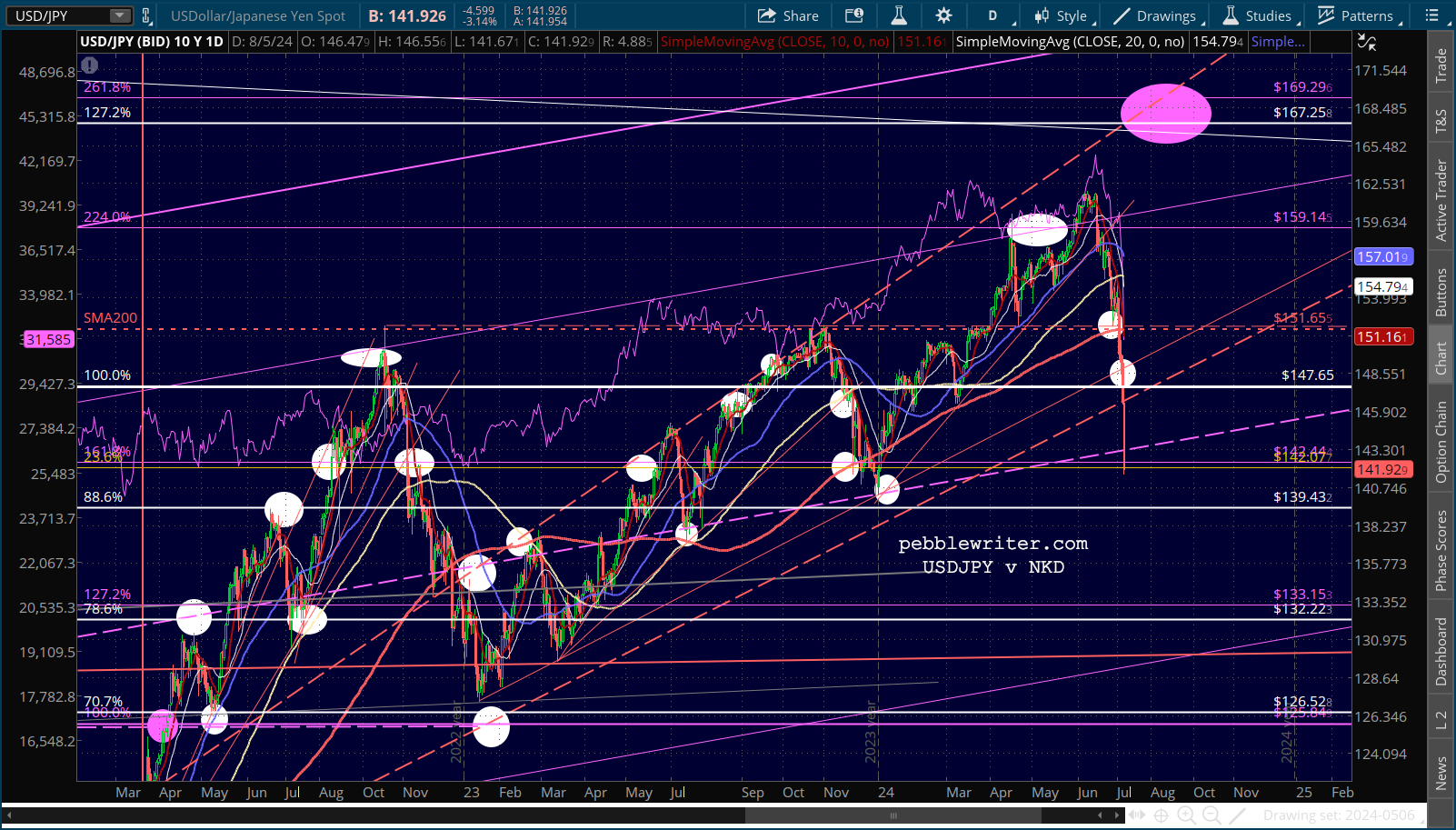

Central bankers are working to control the carnage, with most of the damage being in the USDJPY.

Central bankers are working to control the carnage, with most of the damage being in the USDJPY.

The Nikkei itself was down as much as 12% overnight.

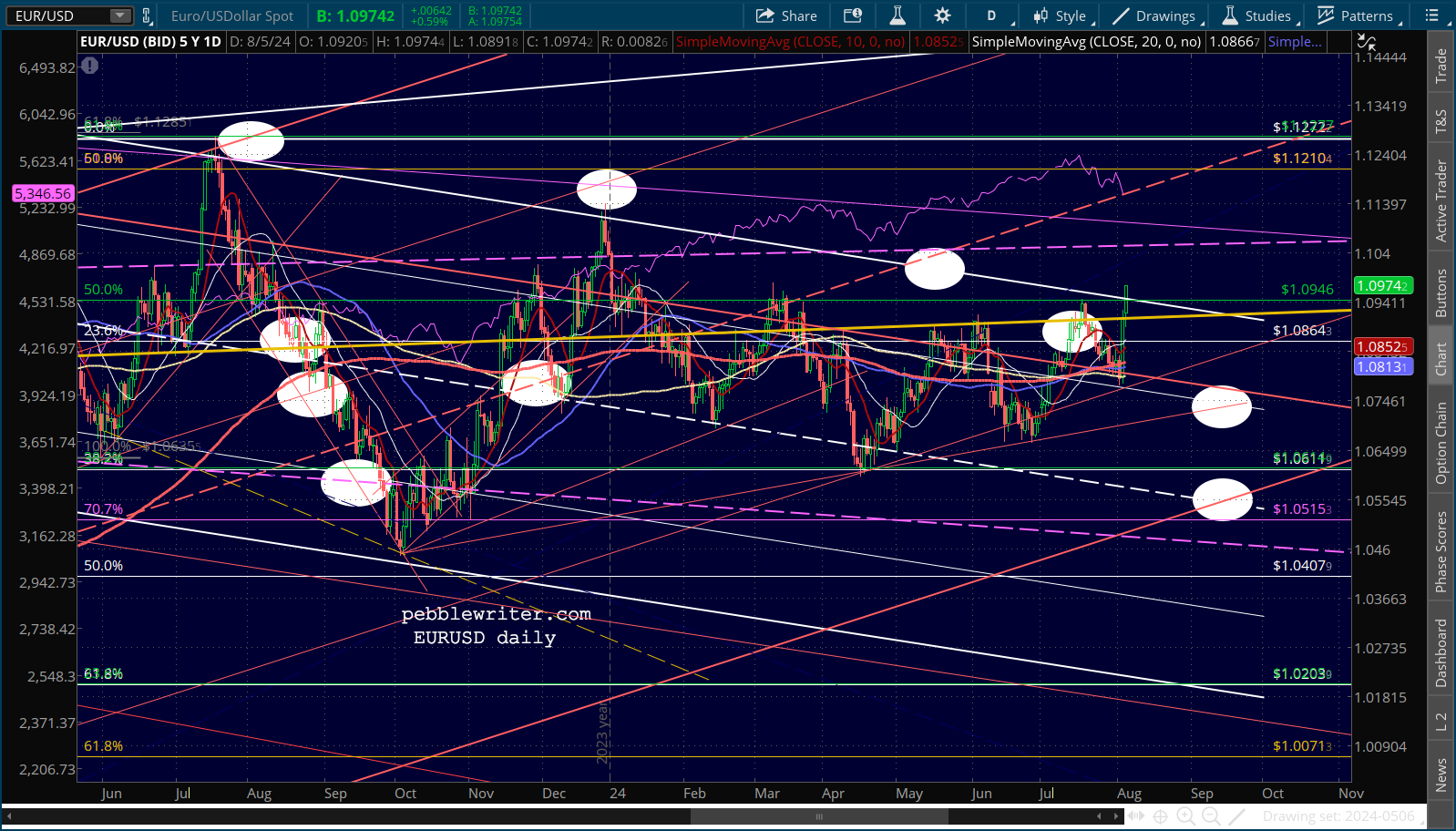

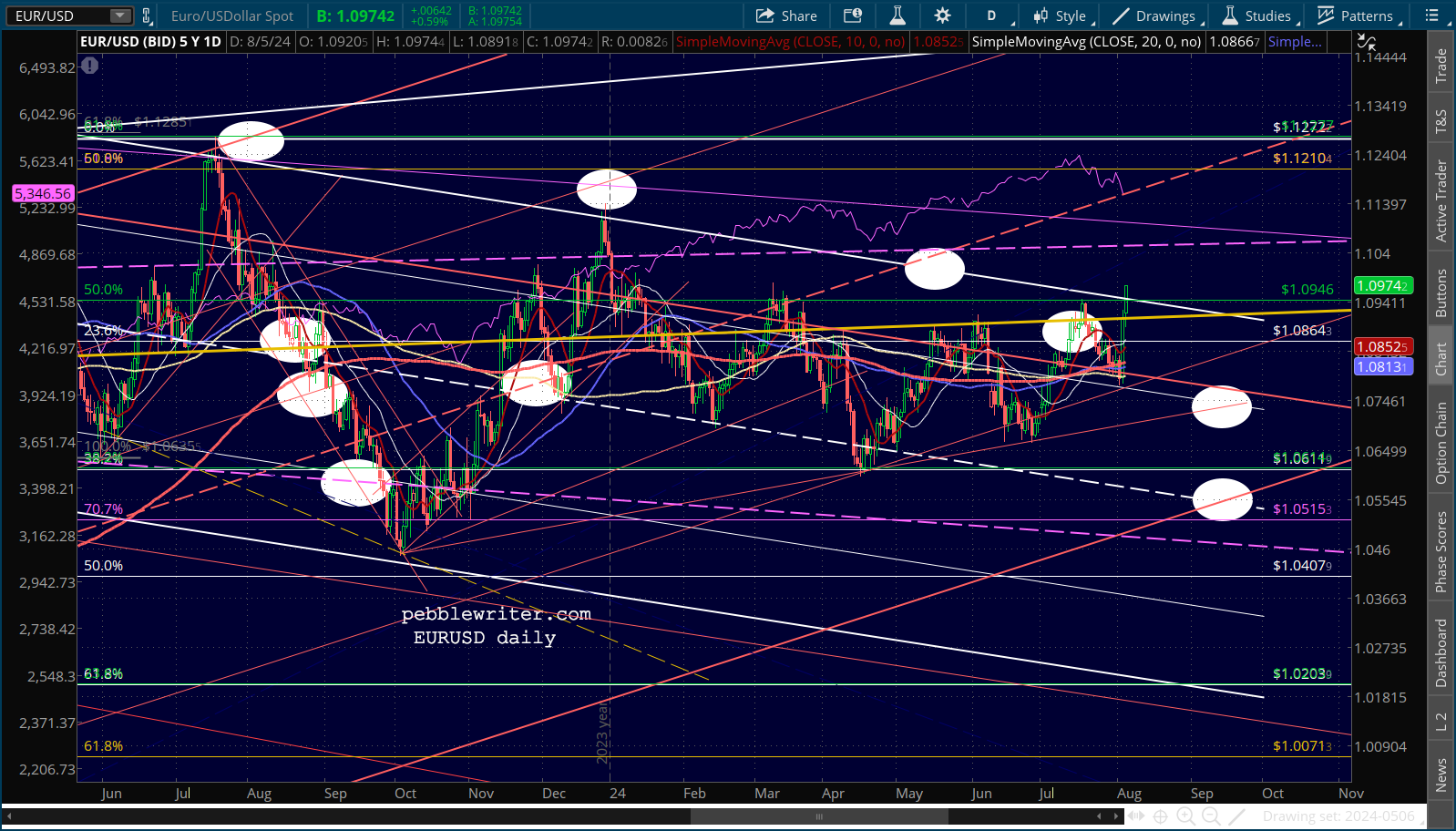

The Nikkei itself was down as much as 12% overnight. The DXY is off almost 1% – a very large move.

The DXY is off almost 1% – a very large move.

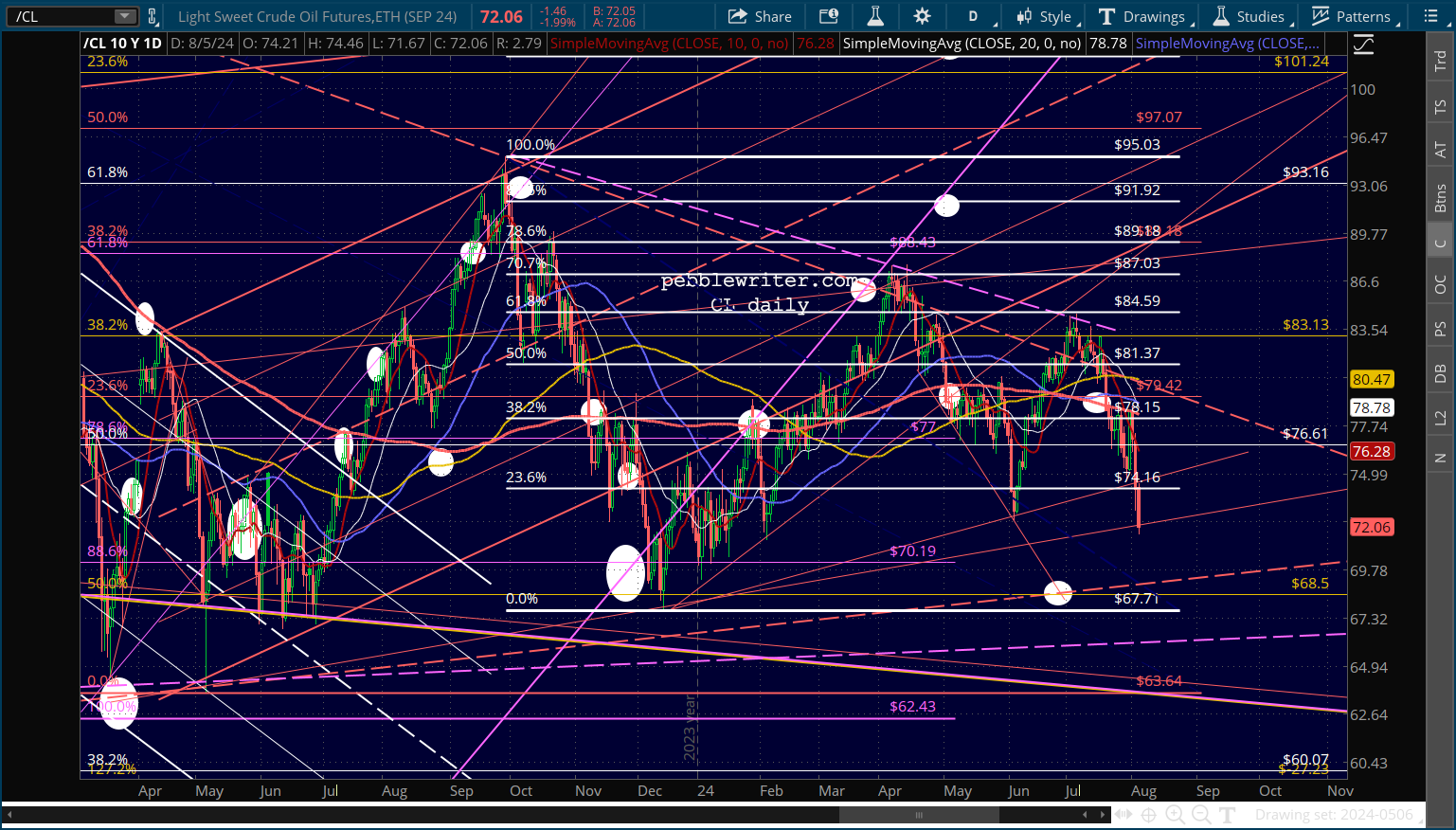

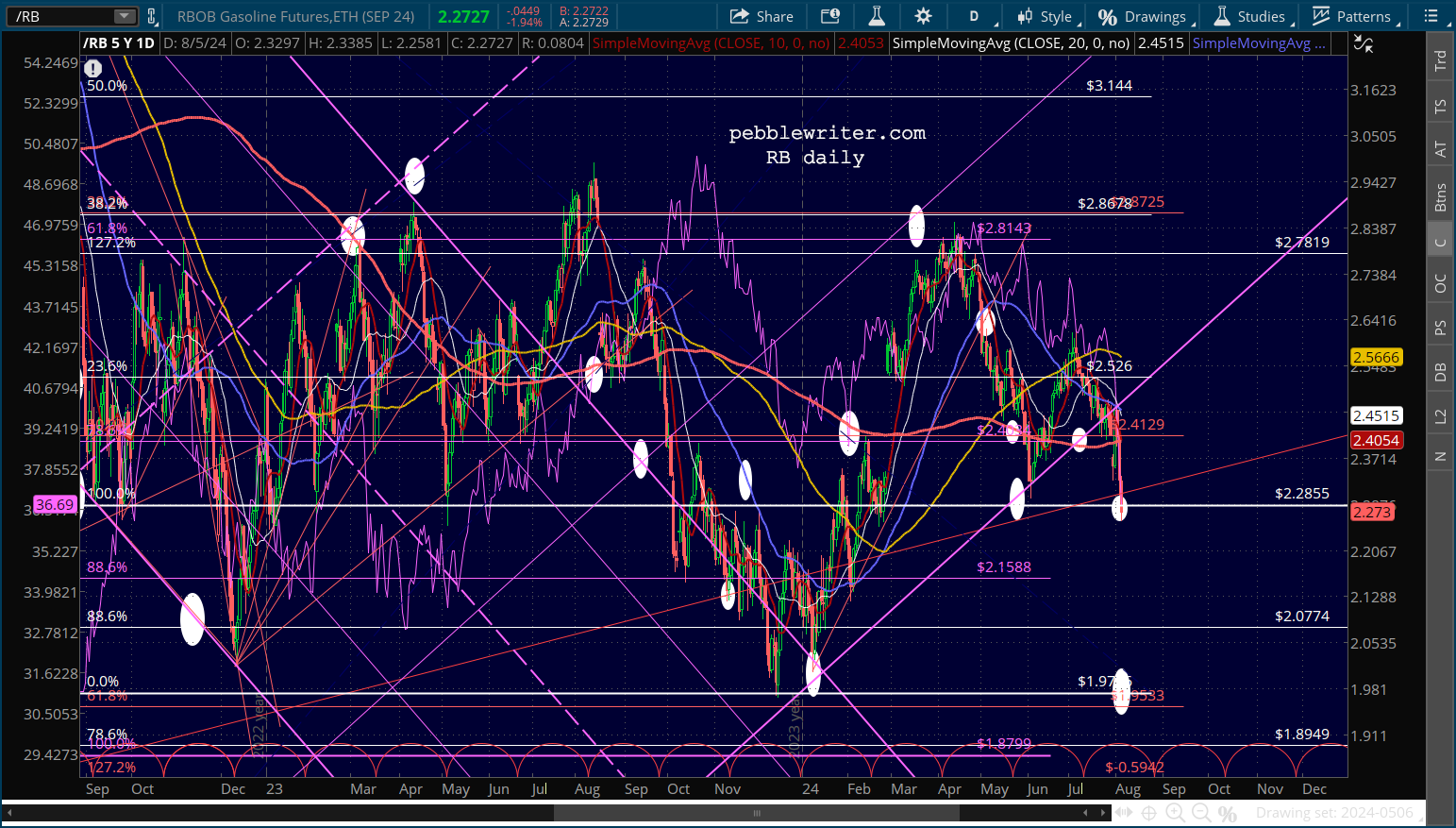

Oil and gas are also tumbling, with CL tagging the TL from May 2023 and RB tagging our 2.28 target.

Oil and gas are also tumbling, with CL tagging the TL from May 2023 and RB tagging our 2.28 target.

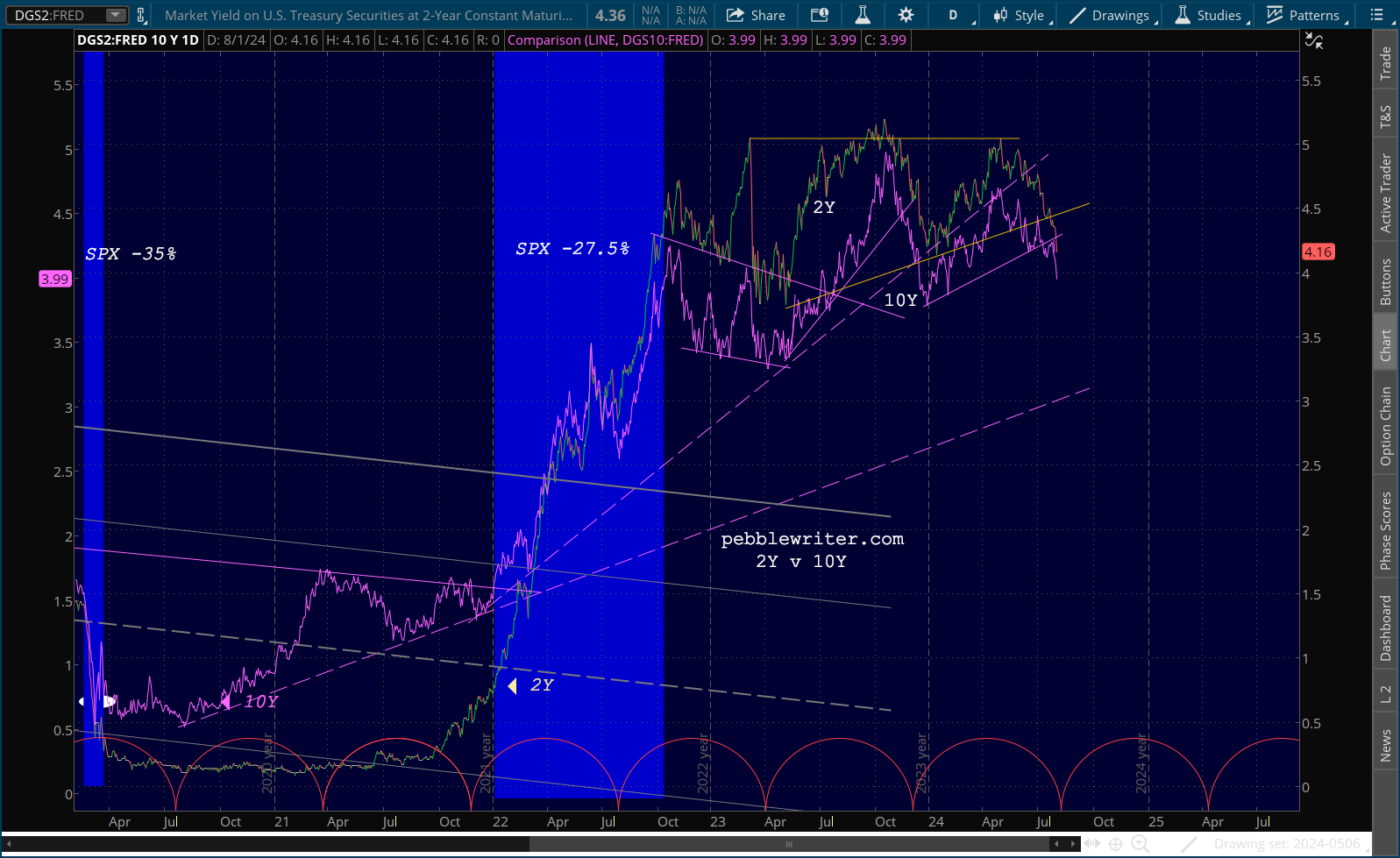

This is contributing to the fear-driven crash in the 10Y. Unfortunately for equity bulls, the 2Y has fallen even further, putting the 2s10s on the brink of un-inverting.

This is contributing to the fear-driven crash in the 10Y. Unfortunately for equity bulls, the 2Y has fallen even further, putting the 2s10s on the brink of un-inverting.

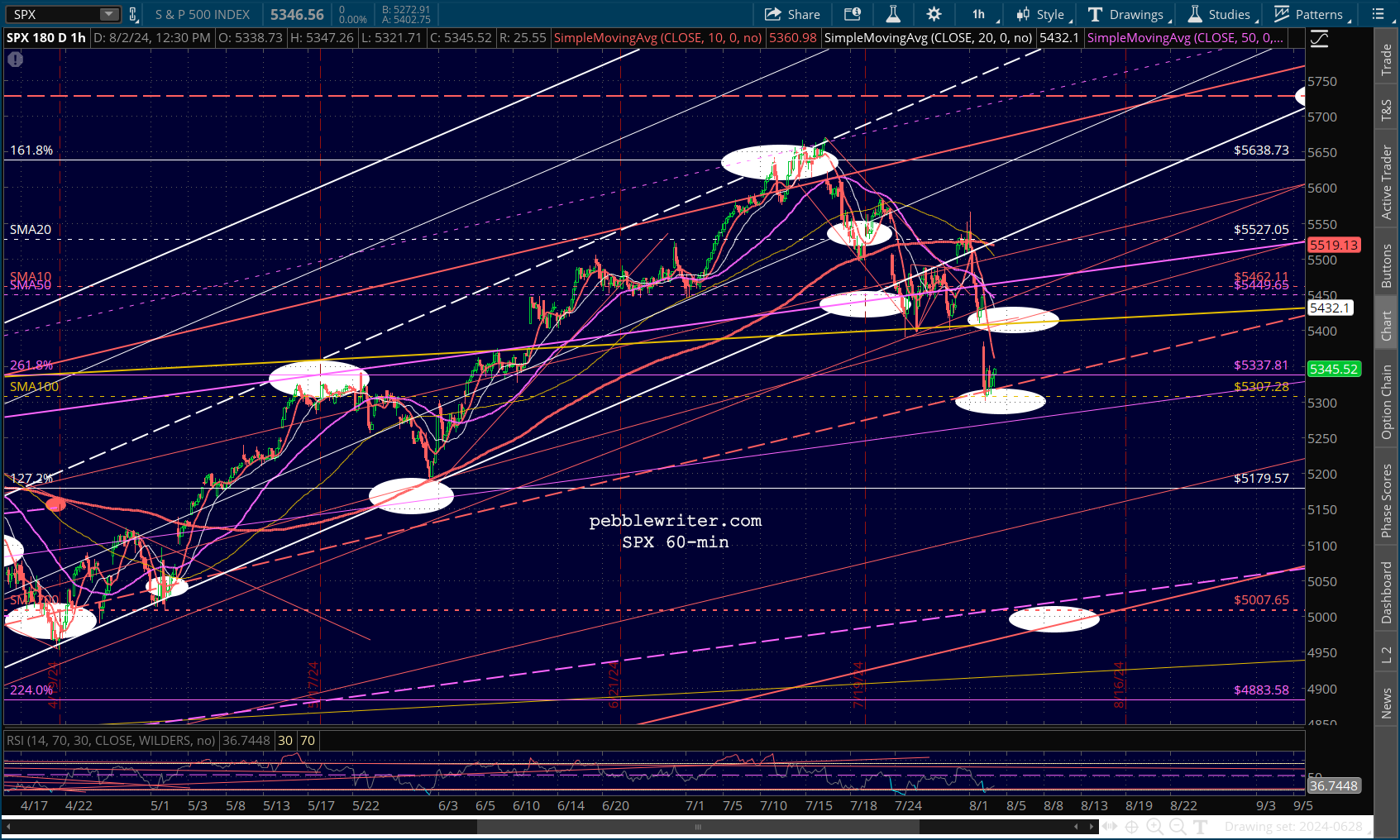

If the 2s10s pops above zero, SPX might test its own SMA200 as well.

If the 2s10s pops above zero, SPX might test its own SMA200 as well.

Stay tuned…

* * *

As a reminder, I will likely be unable to post tomorrow (and potentially Wednesday.)