Anyone who studies factors is well aware of the impact the yen carry trade, VIX and oil prices have had on equities. While VIX did a spectacular job of igniting algos once USDJPY ran out of upside, it blew up spectacularly in January and February.

Since then, oil (taking turns with VIX and USDJPY) has kept stocks on a steady course. Remember, when Crude Light (CL) bottomed on Feb 11, 2016, SPX did too — remaining above the critically important 1.272 Fib extension and establishing a rising channel that remains in force over two years later.

Since then, oil (taking turns with VIX and USDJPY) has kept stocks on a steady course. Remember, when Crude Light (CL) bottomed on Feb 11, 2016, SPX did too — remaining above the critically important 1.272 Fib extension and establishing a rising channel that remains in force over two years later.  And, when SPX reached overhead resistance at the 2.24 extension, CL came the rescue once again – breaking out of the rising channel that had been in place since June of 2016 and even popping above its .618 Fib for good measure.

And, when SPX reached overhead resistance at the 2.24 extension, CL came the rescue once again – breaking out of the rising channel that had been in place since June of 2016 and even popping above its .618 Fib for good measure. A close-up shows that CL broke out of a secondary, steeply rising channel (in white) on Jan 3…

A close-up shows that CL broke out of a secondary, steeply rising channel (in white) on Jan 3… …the exact same day that SPX needed help breaking above its 2.24 as well as a sharply rising trend line (below, in yellow.)

…the exact same day that SPX needed help breaking above its 2.24 as well as a sharply rising trend line (below, in yellow.) In the world of chart patterns, there aren’t many developments that are more bullish than a breakout of an already steeply rising channel. The algos were positively giddy.

In the world of chart patterns, there aren’t many developments that are more bullish than a breakout of an already steeply rising channel. The algos were positively giddy.

They were less thrilled, however, when CL dropped back through its .618 and the top of the purple channel — contributing to SPX’s sharpest sell off in years.

It was no coincidence that CL bottomed out on Feb 9, the same day that SPX backtested its 200-day moving average. Nor was it a coincidence that SPX managed to regain its 2.24 on the same day that CL climbed back above its purple channel top.

Since then, CL has continued to bounce along the top of the purple channel — popping higher every time SPX needs a boost, and dropping back down when SPX needs a breather. This game could go on indefinitely, except that changes in oil (and gas) prices have consequences. As we’ve discussed many times, they are usually the biggest determinant of changes in the monthly and annual CPI data.

This game could go on indefinitely, except that changes in oil (and gas) prices have consequences. As we’ve discussed many times, they are usually the biggest determinant of changes in the monthly and annual CPI data.

When CPI shows big increases, it can send the bond market into convulsions over the prospect of higher interest rates. When CPI falls flat, yields fall and the dollar takes a hit.

Understanding this dynamic has helped us immeasurably in forecasting oil and gas price moves — considerably more than the fundamentals have.

But, we’ve arrived at a level where keeping CPI in a desirable range will necessarily conflict with keeping stocks on the rise. And, sooner or later, the algos might just figure out that all these little breakouts and bounces produce no actual follow through.

If stocks are to fly any higher, either further oil and gas price increases will result in undesirable inflation or the algos will need to find themselves a new pilot.

continued for members…

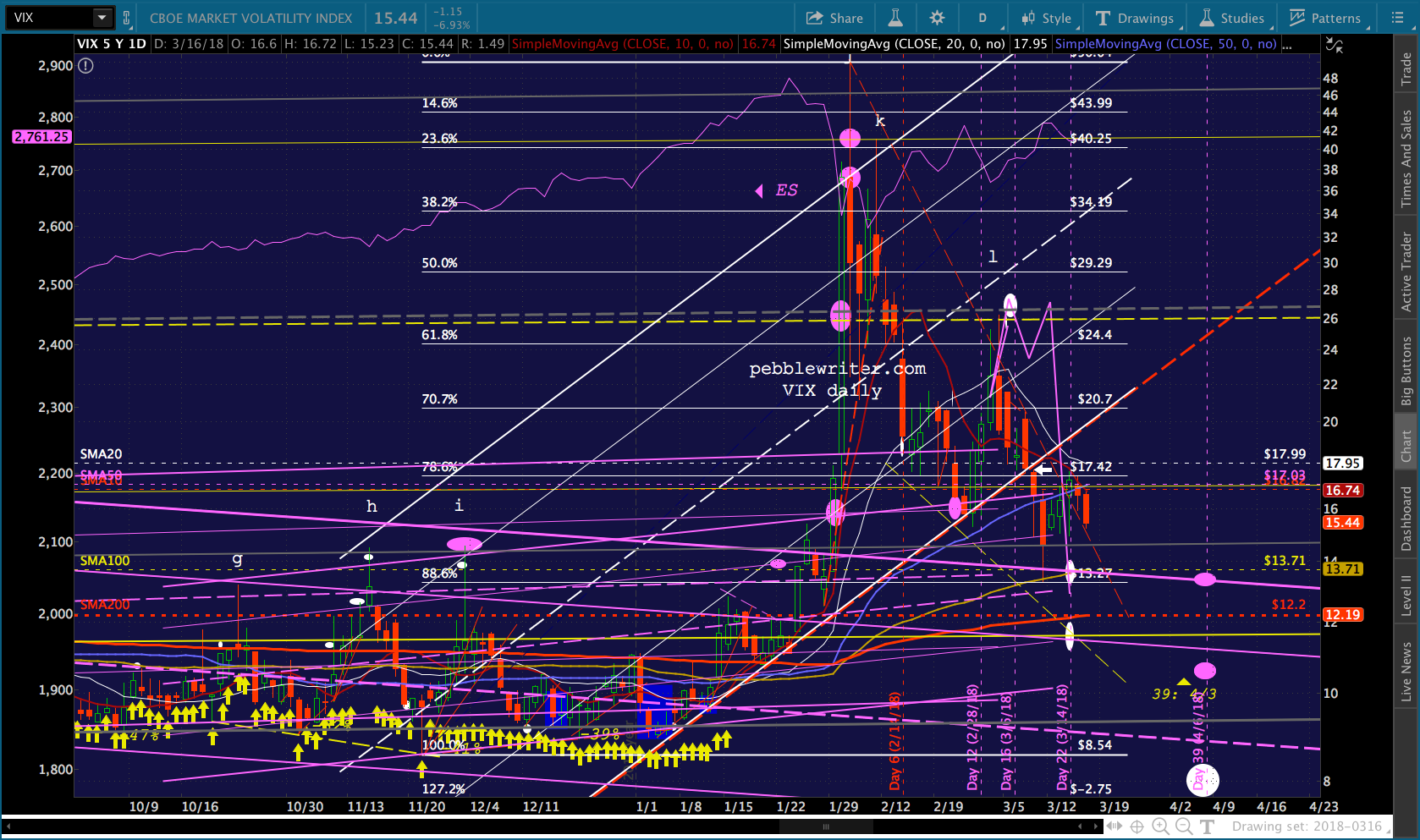

VIX isn’t out of the running, of course. It still hasn’t reached its .886 at 13.27. And, there’s nothing to keep it from returning to the folds of the falling purple channel which it backtested and bounced off of on Mar 9. It played this game pretty well for over a year. With Larry Kudlow (sigh…) in charge of propping up “King Dollar” we might see USDJPY regain some of its mojo. It’s been playing cat and mouse with the red TL from Jan 7. But, a backtest of the broken white channel up around 110.50 would certainly give stocks a leg up.

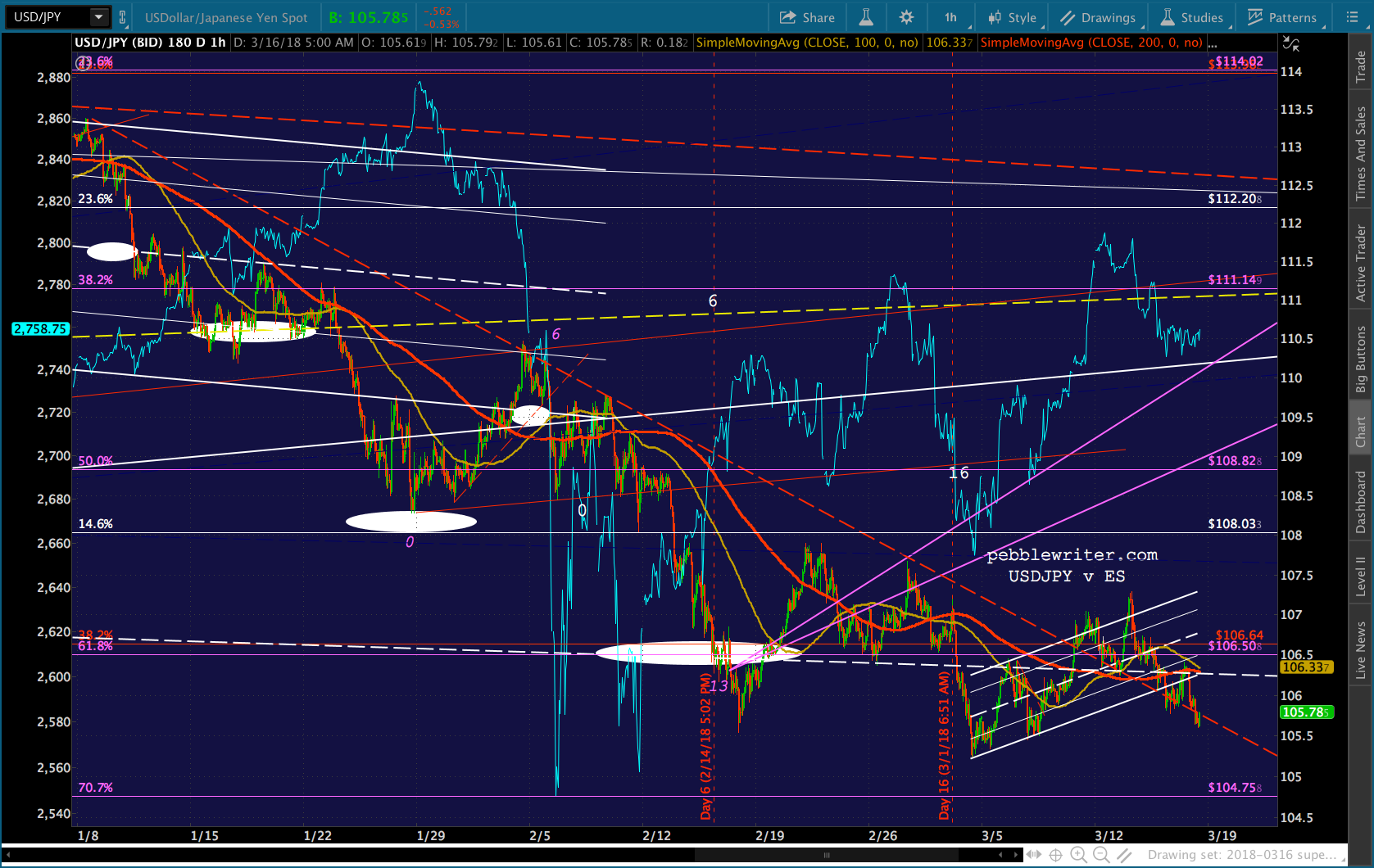

With Larry Kudlow (sigh…) in charge of propping up “King Dollar” we might see USDJPY regain some of its mojo. It’s been playing cat and mouse with the red TL from Jan 7. But, a backtest of the broken white channel up around 110.50 would certainly give stocks a leg up. The bigger picture shows things going downhill since late January. USDJPY is ripe for a recovery if it can every hold the white channel midline.

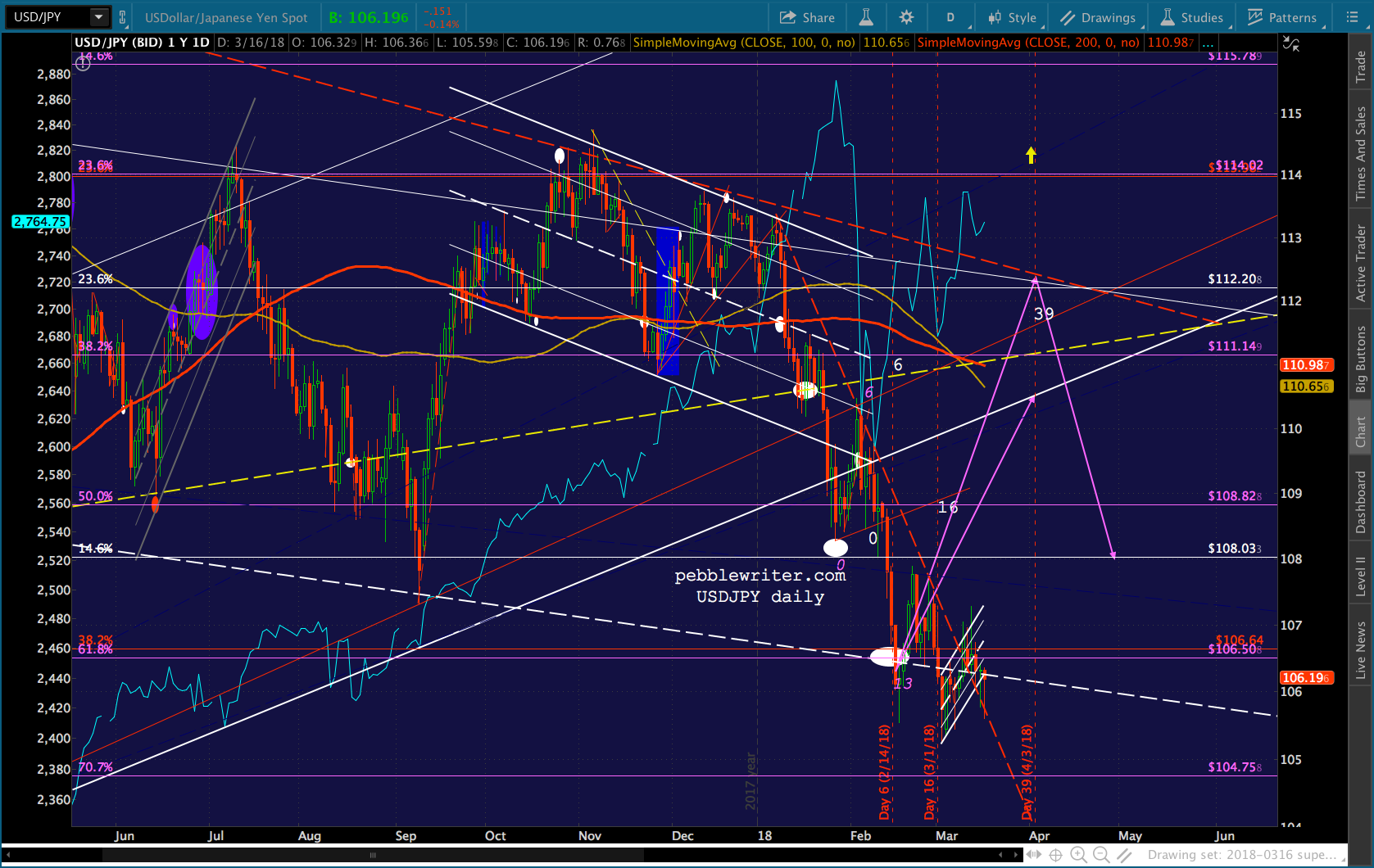

The bigger picture shows things going downhill since late January. USDJPY is ripe for a recovery if it can every hold the white channel midline. While I’ve been writing, CL has bounced up to the white channel midline and a TL off the recent highs. Could be time for a retreat to the purple channel top at 60.25 or potentially the white channel bottom (55.24 or 58.70) by Mar 20. Keep a very close eye out for signs of a reversal.

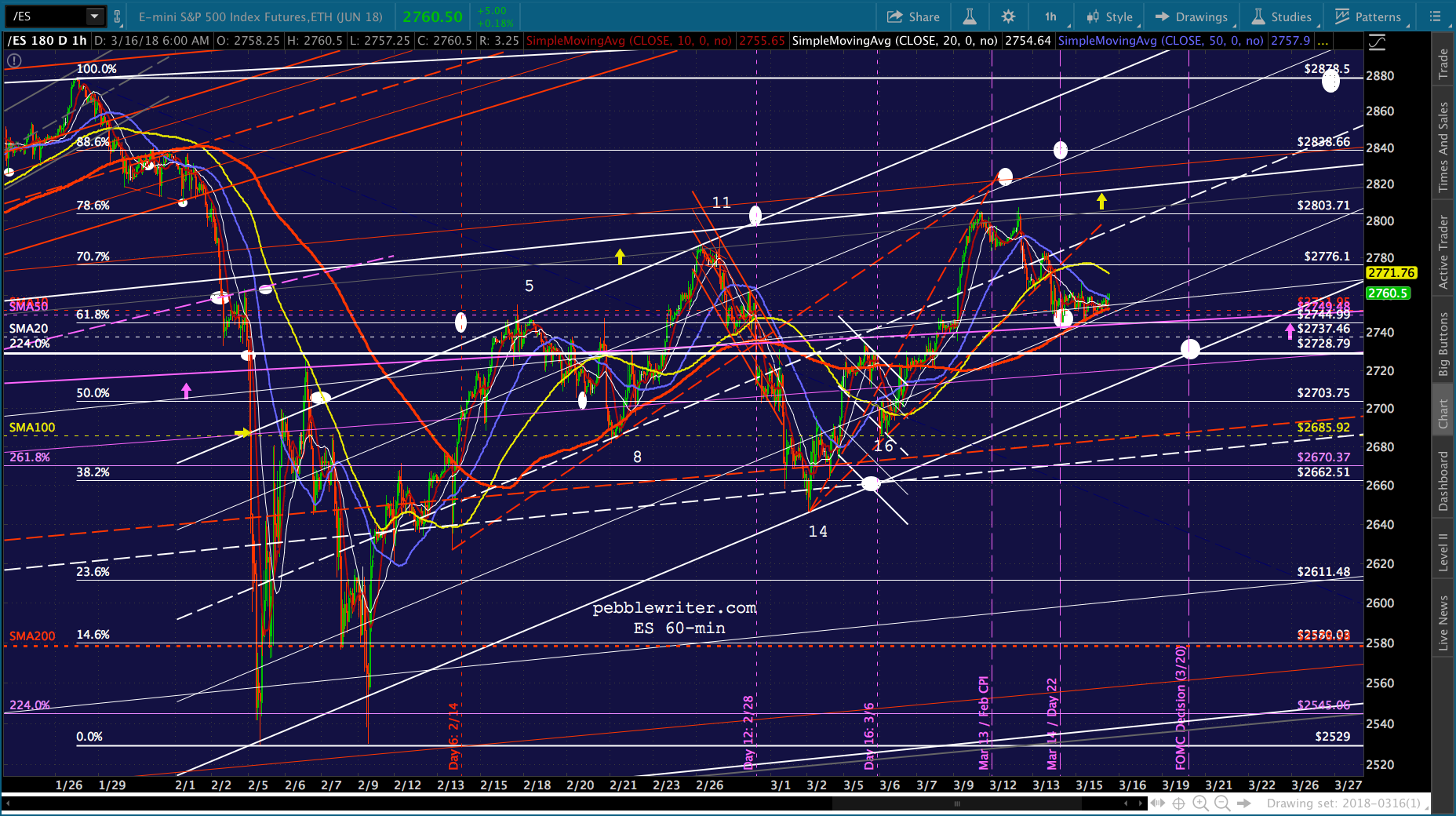

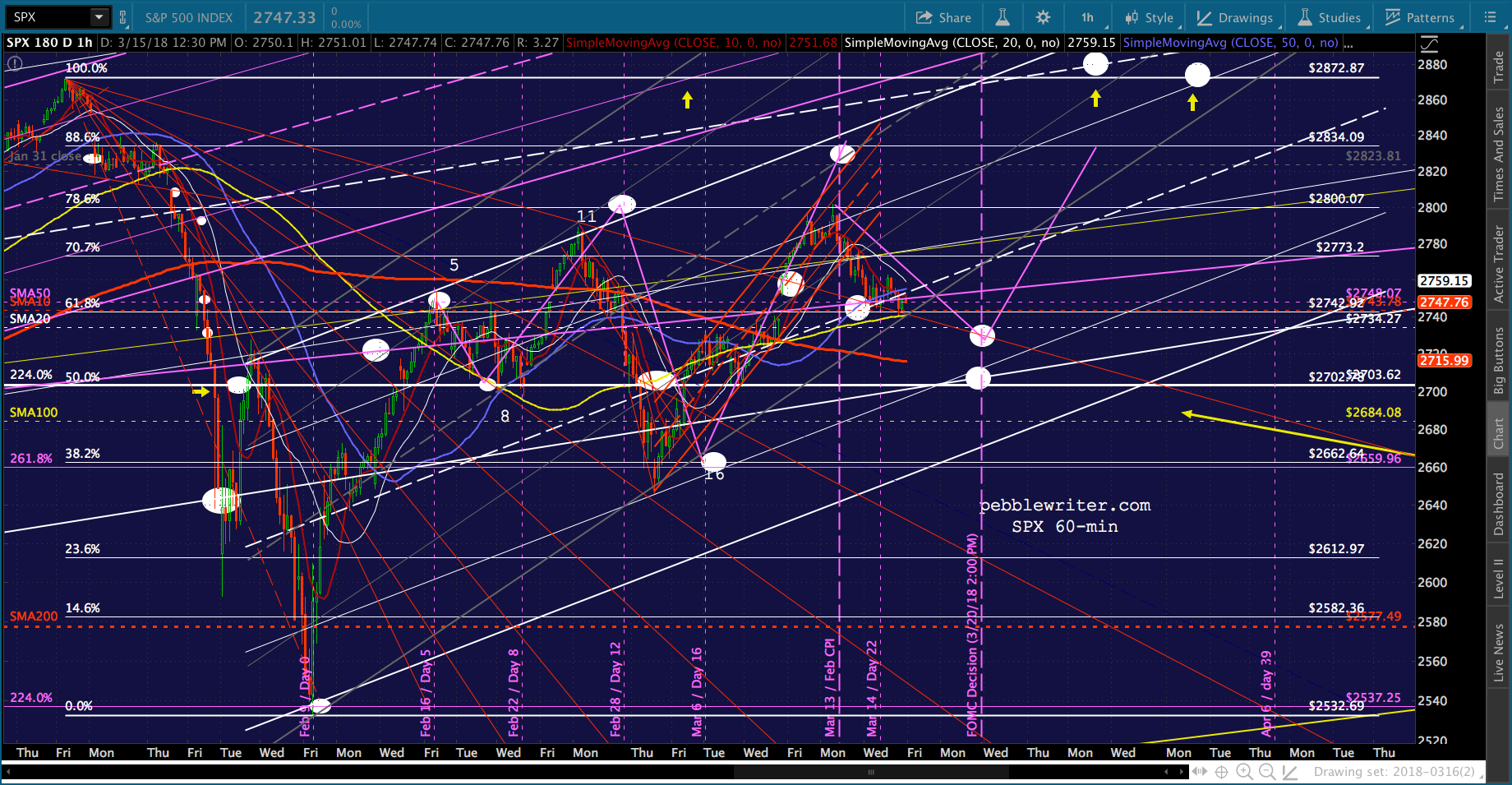

While I’ve been writing, CL has bounced up to the white channel midline and a TL off the recent highs. Could be time for a retreat to the purple channel top at 60.25 or potentially the white channel bottom (55.24 or 58.70) by Mar 20. Keep a very close eye out for signs of a reversal. A reminder, the 10Y2Y chart shows a dip ahead, as does our analog. The charts show potential downside to ES 2728 or SPX 2703 — though the analog suggests it’ll be on the milder side.

A reminder, the 10Y2Y chart shows a dip ahead, as does our analog. The charts show potential downside to ES 2728 or SPX 2703 — though the analog suggests it’ll be on the milder side.

GLTA.

GLTA.