In Seinfeld lore, the Soup Nazi was notorious for denying soup to those who didn’t follow a strict regimen and express proper reverence when ordering his amazing soup. Even a minor infraction would elicit a fierce “no soup for you!”

In a recent conversation with a friend who went to Wall Street when I did (100 years ago), he correctly observed that macro forecasts had become incredibly difficult since a simple presidential tweet or Fed president gaff could exact enormous swings in the markets.

Frequently, these swings are sharp rallies such as yesterday’s — occasionally sharp plunges. Rarely do they represent an important shift in the economic landscape. But algorithms’ swelling importance means the repercussions can be way out of line with the new “information” and markets reverse the following day — as will be the case today.

There’s an important lesson to be drawn from this frequent detachment from fundamentals: don’t put all your eggs in the fundamental basket. Sometimes, as has been the case lately, they do a very poor job of providing direction.

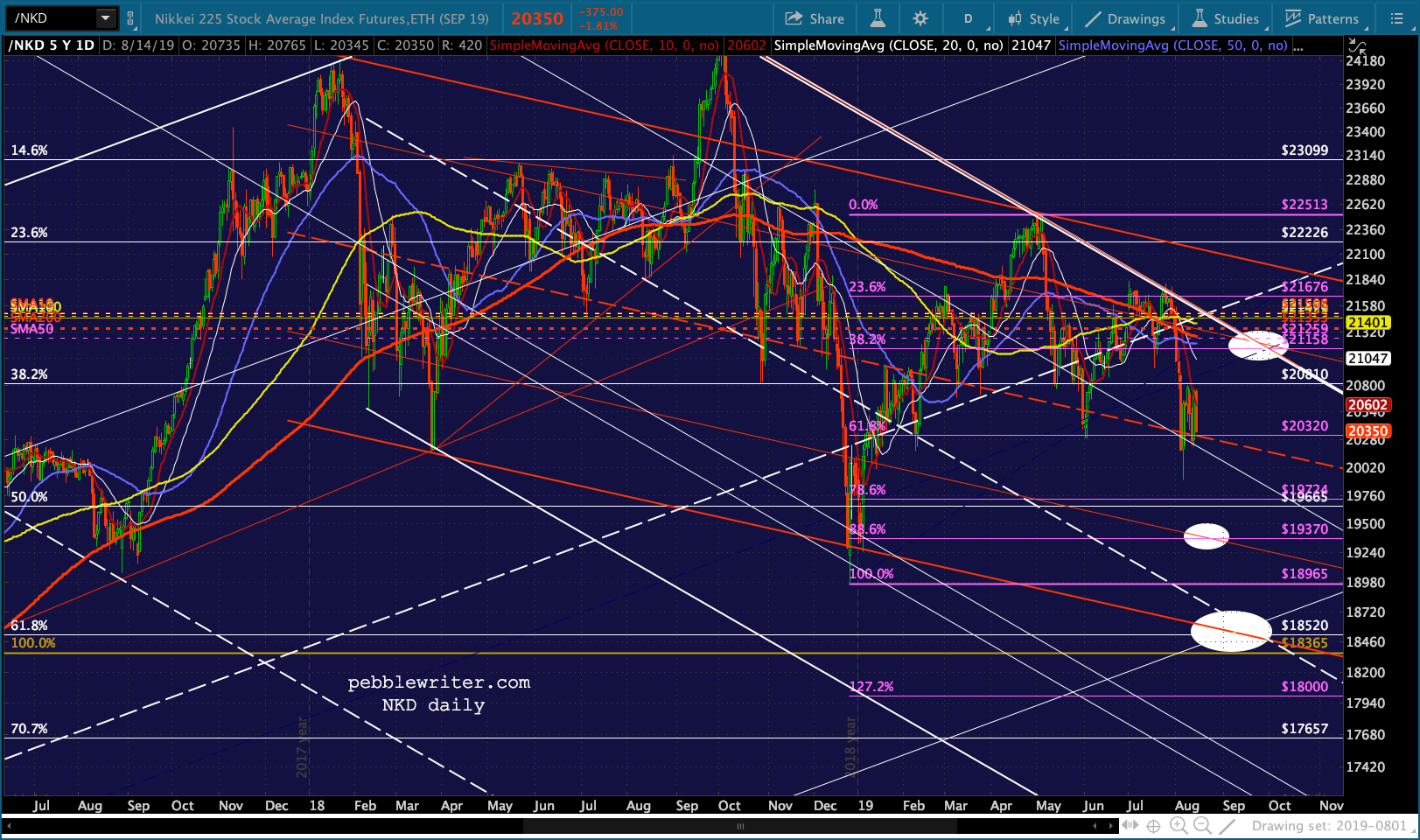

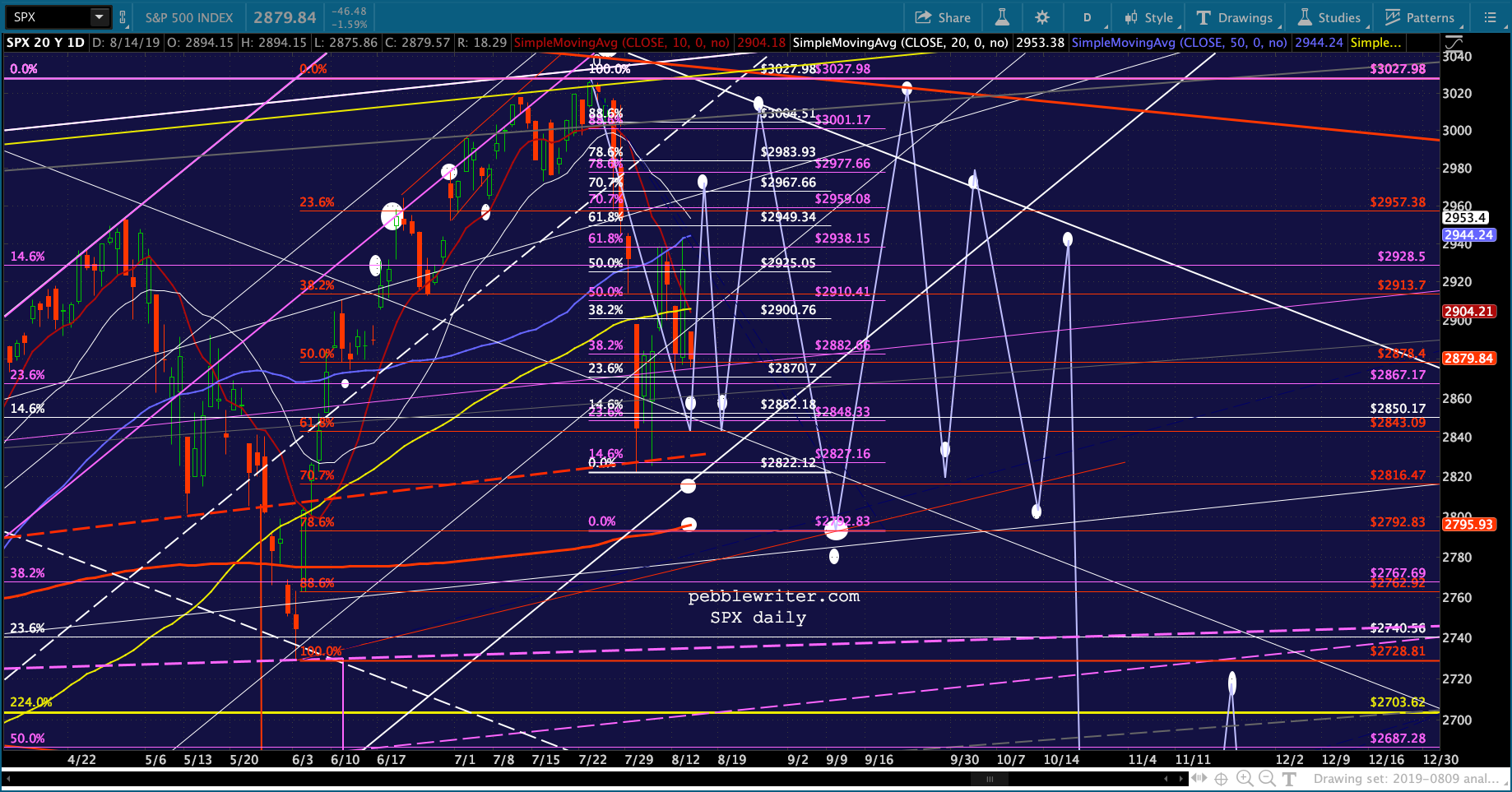

Technical analysis and chart patterns, on the other hand, have done a masterful job of accurately forecasting turning points. The latest example: forecasting the recent top (within 0.6% of the forecast peak) and the subsequent selloff weeks in advance [see: Analog Watch, July 15.]

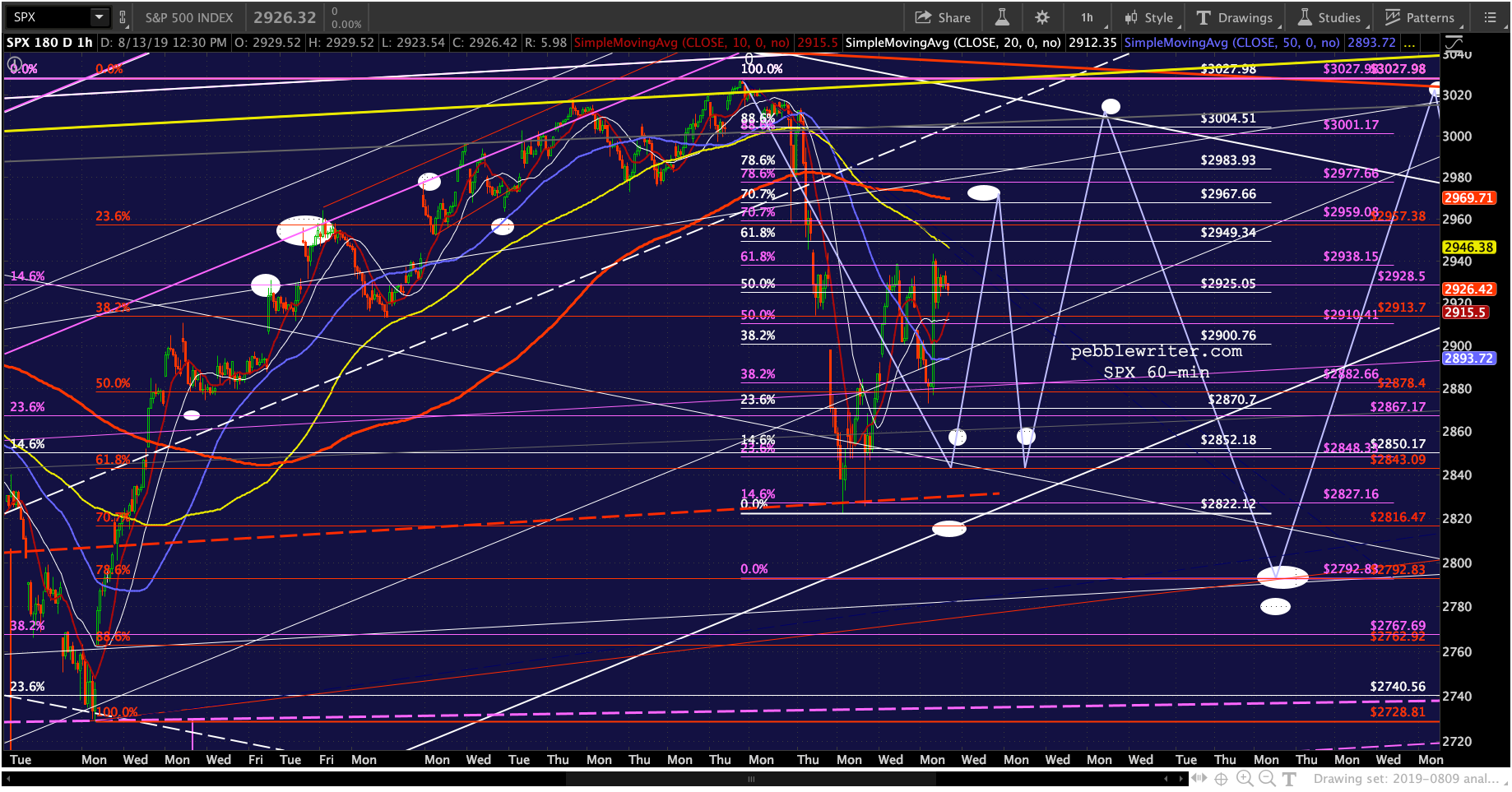

Today’s reversal will hopefully confirm the accuracy of this analog posted a month ago. If confirmed, it forecasts another 20+ large (think 10%) swings over the next 9 months. Ideally, we’ll hit ES 2817 or even 2793 by the end of the day. SPX will shed over 100 points at its lows. Today’s minor infraction, of course, is that the 2s10s has officially inverted. Will investors care? Should they?

Today’s minor infraction, of course, is that the 2s10s has officially inverted. Will investors care? Should they?

The last time this happened was May 2, 2007. Stocks yawned, as it was one of a series of inversions that began in December 2005. Following that initial inversion, SPX shrugged it off and continued rallying in fits and starts for another 5 1/2 months when it dipped all of 8% into mid-June 2006 before rallying 29% to the Oct 2007 top. As we’ve discussed many times, it’s not inversions that trigger a correction/crash. It’s the sharp unwinding of an inversion. When 2s10s spiked higher — the result of the 2Y plunging faster than the 10Y — the Great Financial Crisis had arrived.

As we’ve discussed many times, it’s not inversions that trigger a correction/crash. It’s the sharp unwinding of an inversion. When 2s10s spiked higher — the result of the 2Y plunging faster than the 10Y — the Great Financial Crisis had arrived.

Following that last inversion in May 2007, SPX barely paused on its way from 1313 to a new high at 1576. But, once the 2s10s topped 20 bps, SPX quickly ran out of upside. There are both similarities and differences between now and then. For instance, when 2s10s began spiking higher, the 10Y was around 4.8% and the 2Y was around 4.6%. There was plenty of room for rates to decline.

There are both similarities and differences between now and then. For instance, when 2s10s began spiking higher, the 10Y was around 4.8% and the 2Y was around 4.6%. There was plenty of room for rates to decline.

With the 2Y and 10Y currently at 1.6%, it’s a very different backdrop which presents very different challenges to central bankers.

continued for members…

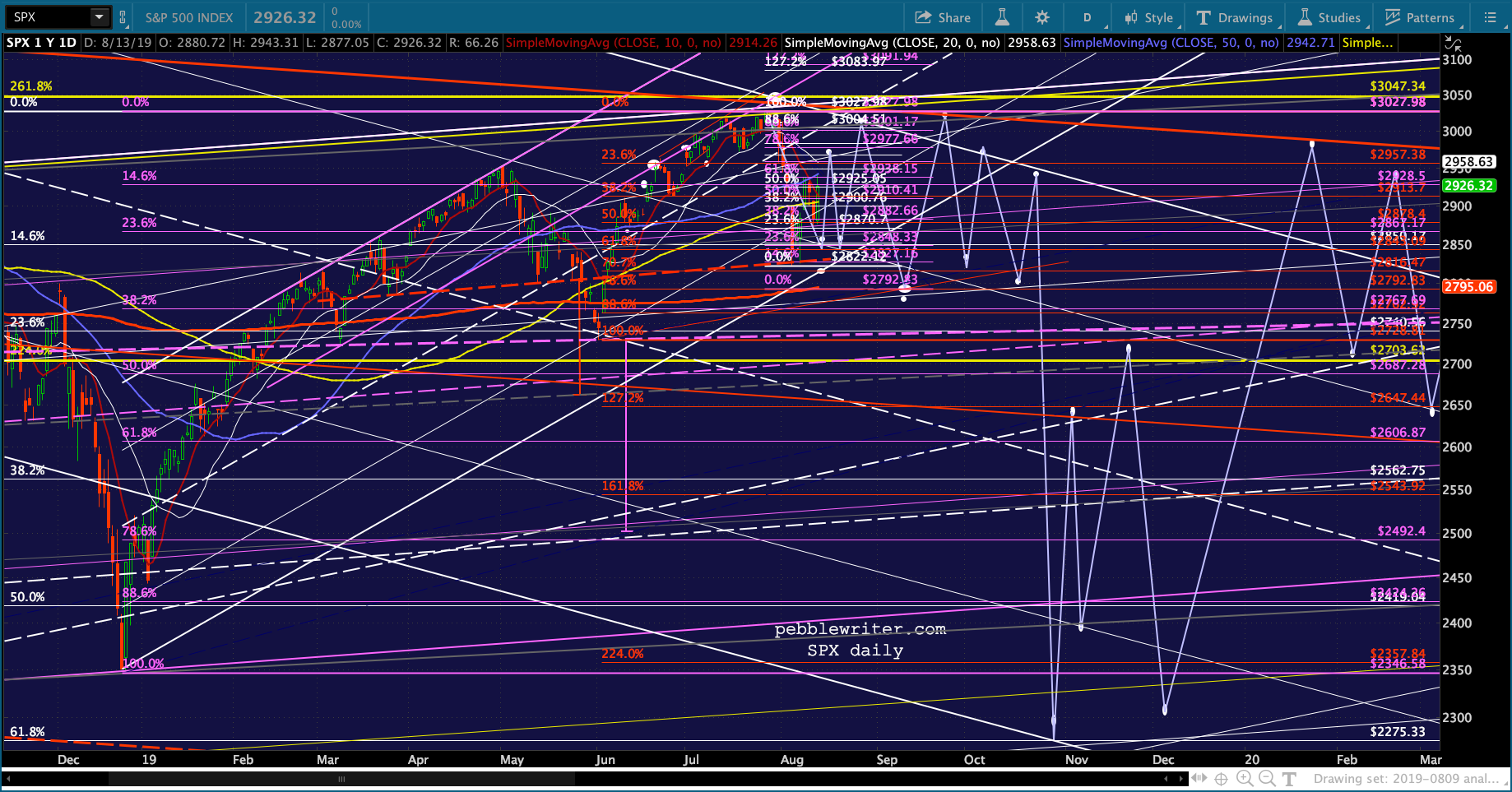

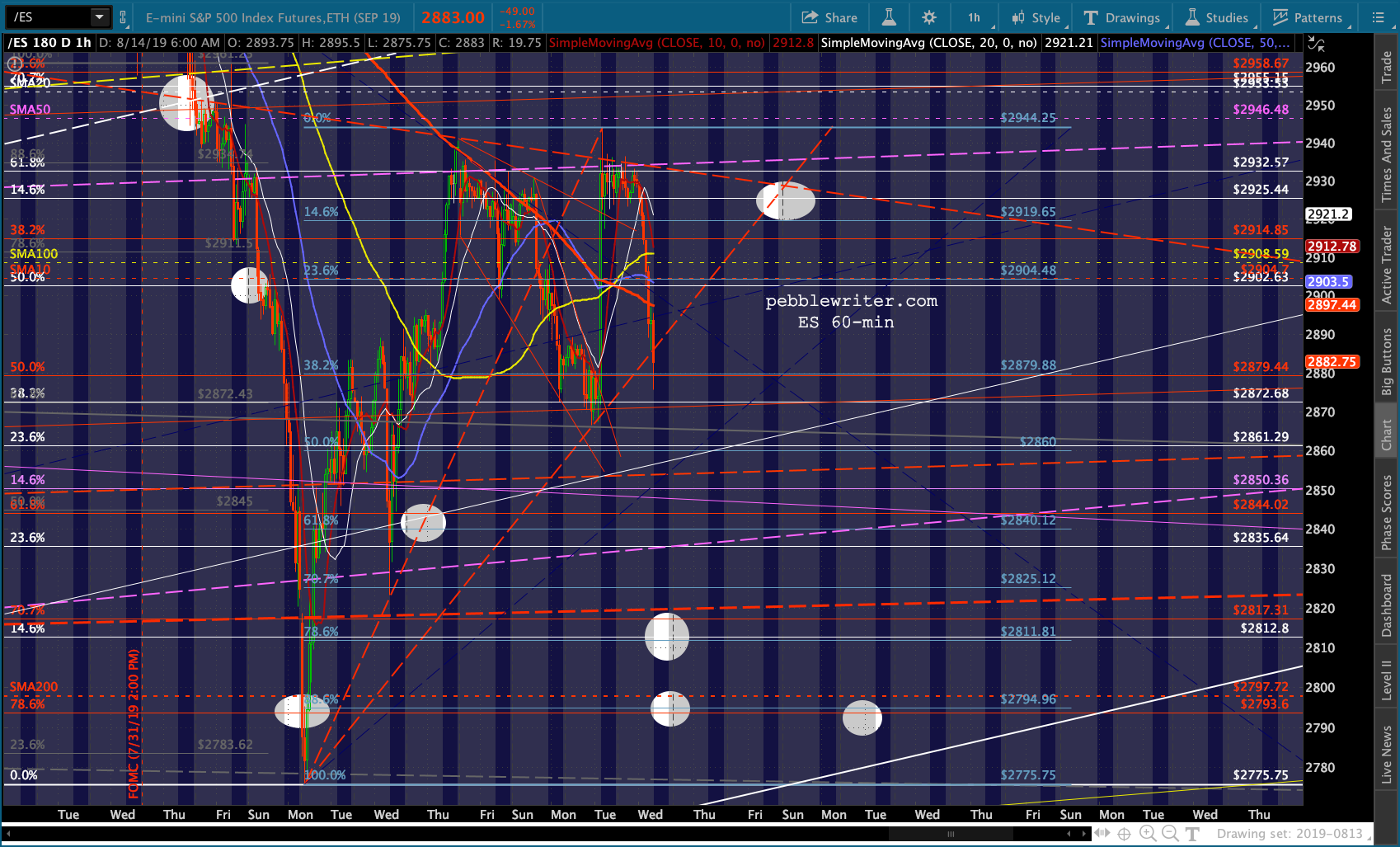

SPX is about 110 points from my favorite target for today: the .707 Fib at 2816.47. It would make today the cycle low, which would satisfy our analog. And, it would tag the white channel bottom, setting up a technical bounce into Aug 27.

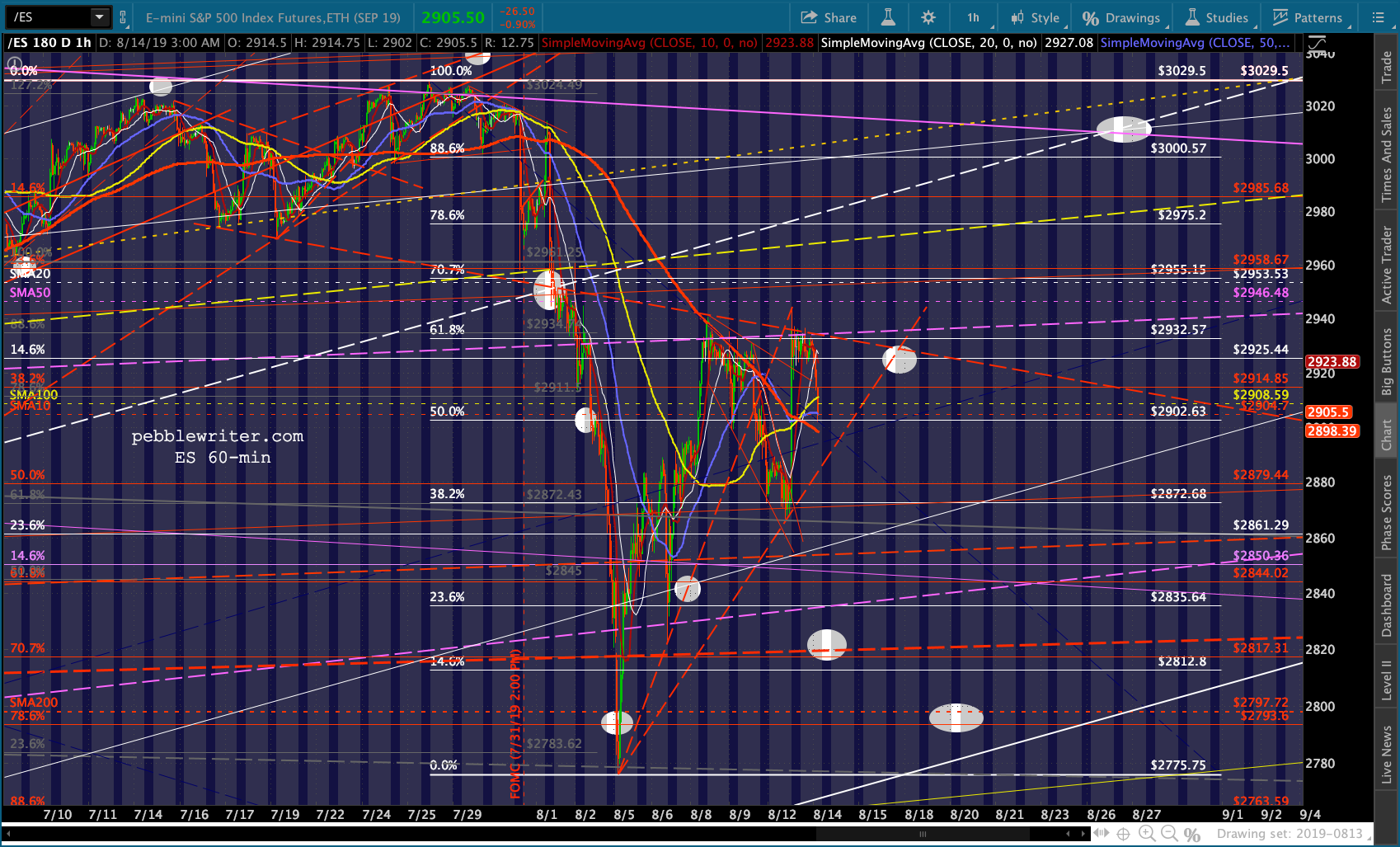

As we discussed then, we obviously don’t require a new low. The August low, especially in ES, was already lower than the analog suggested. But, it would be nice. With ES already off 26 points, we’re about 1/3 of the way there. The key will be breaking below the red fan line from the August 5 lows. Just eyeballing it, SPX 2817 would align with ES 2822ish.

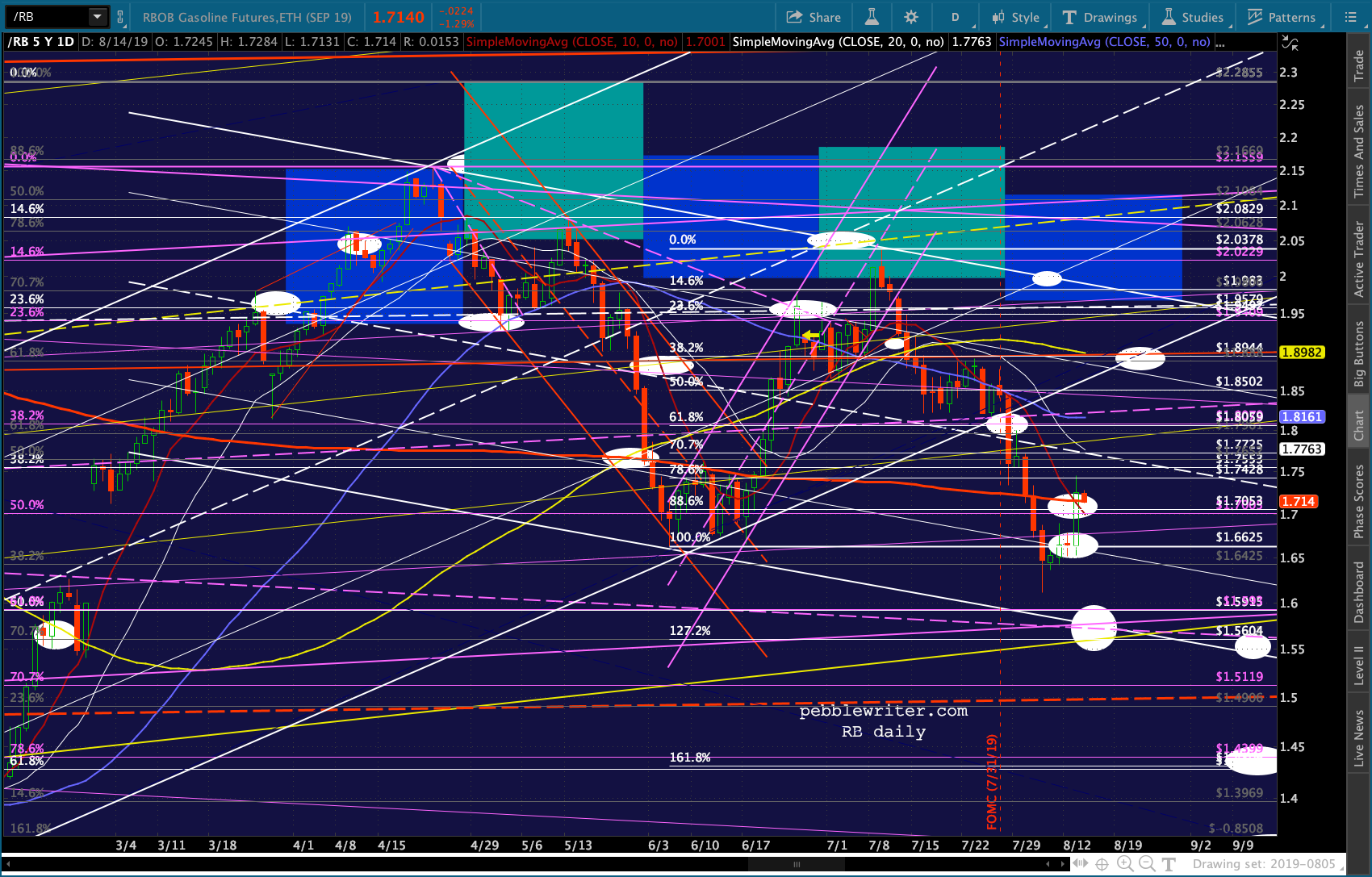

With ES already off 26 points, we’re about 1/3 of the way there. The key will be breaking below the red fan line from the August 5 lows. Just eyeballing it, SPX 2817 would align with ES 2822ish.  We’d just need CL, USDJPY and VIX to cooperate — at least 2 of the 3.

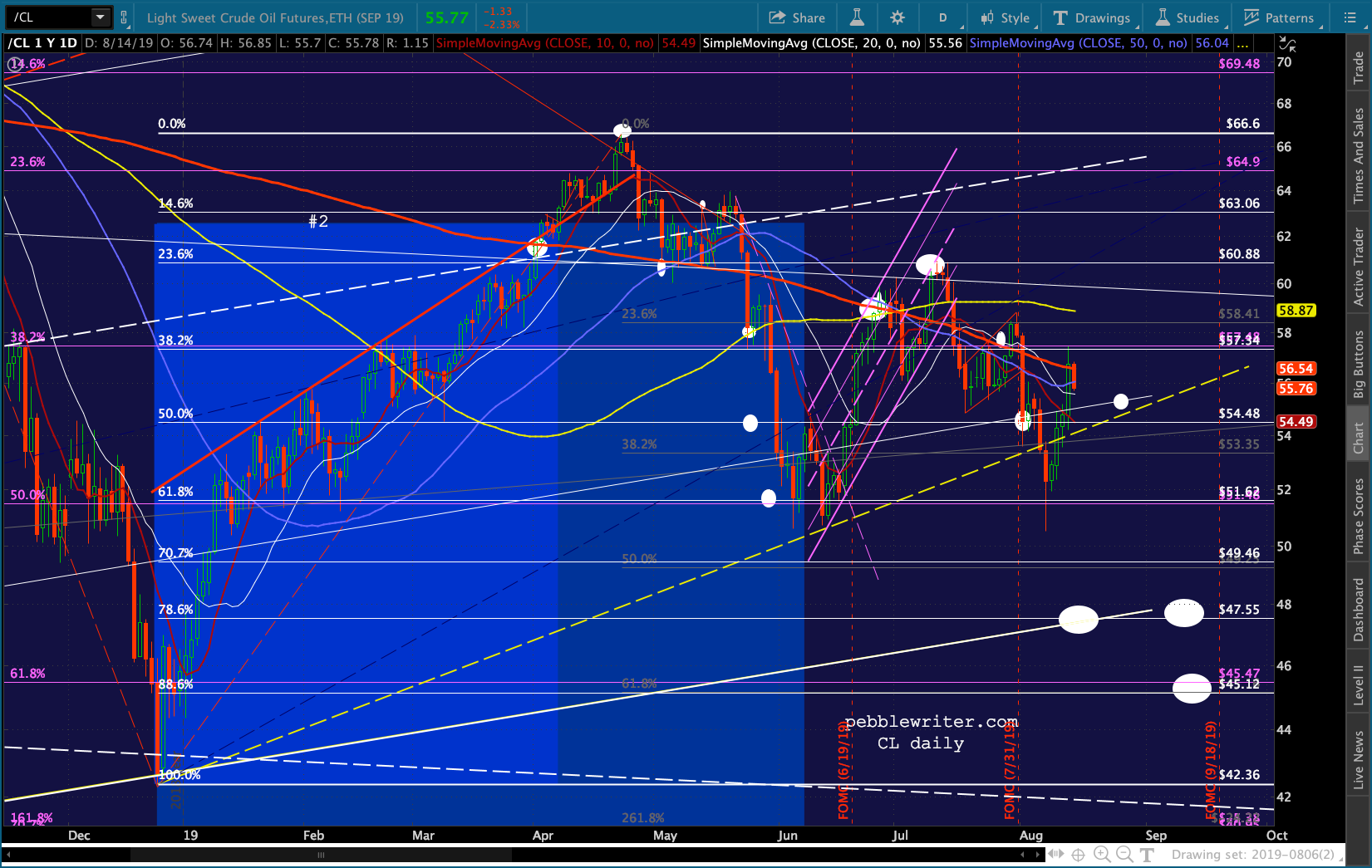

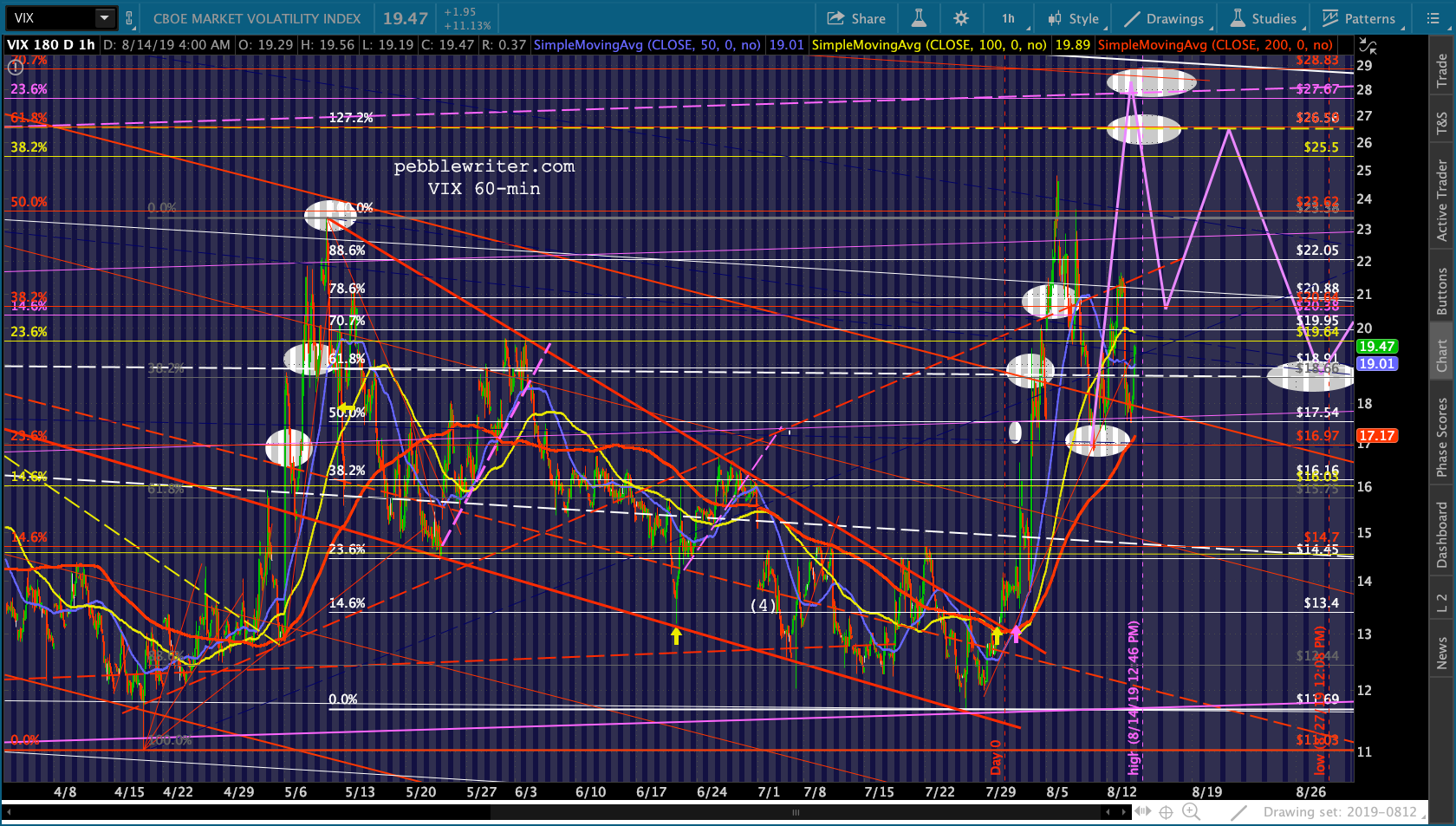

We’d just need CL, USDJPY and VIX to cooperate — at least 2 of the 3.

CL has reversed at its SMA200. USDJPY is reversing at its SMA10.

USDJPY is reversing at its SMA10.  And, VIX backtested the red channel again.

And, VIX backtested the red channel again.  The rest of today’s charts…

The rest of today’s charts…

UPDATE: 9:45 AM

UPDATE: 9:45 AM

ES has broken below the red TL. Now that the cash market is open, it appears SPX 2816 would be closer to ES 2815. There’s a Fib nearby: the .786 at 2811.81. If SPX were to dip below its .707, it obviously has potential to its SMA200 at 2795 (ES’ .886 at 2793.60.)

If SPX were to dip below its .707, it obviously has potential to its SMA200 at 2795 (ES’ .886 at 2793.60.) This scenario is every bit as likely, IMO. But, it would mean SPX has broken below its channel bottom. Not sure if TPTB would want to risk it just yet.

This scenario is every bit as likely, IMO. But, it would mean SPX has broken below its channel bottom. Not sure if TPTB would want to risk it just yet.

My favorite scenario, BTW, is that this morning’s EIA inventory report sends CL down to 47.55 and VIX up to 28-29ish with USDJPY testing either 104.74 or 101.23.

Some of you might remember that we often bottom out around 3:34PM on these big down days. Worth keeping an eye on…

UPDATE: 3:55 PM

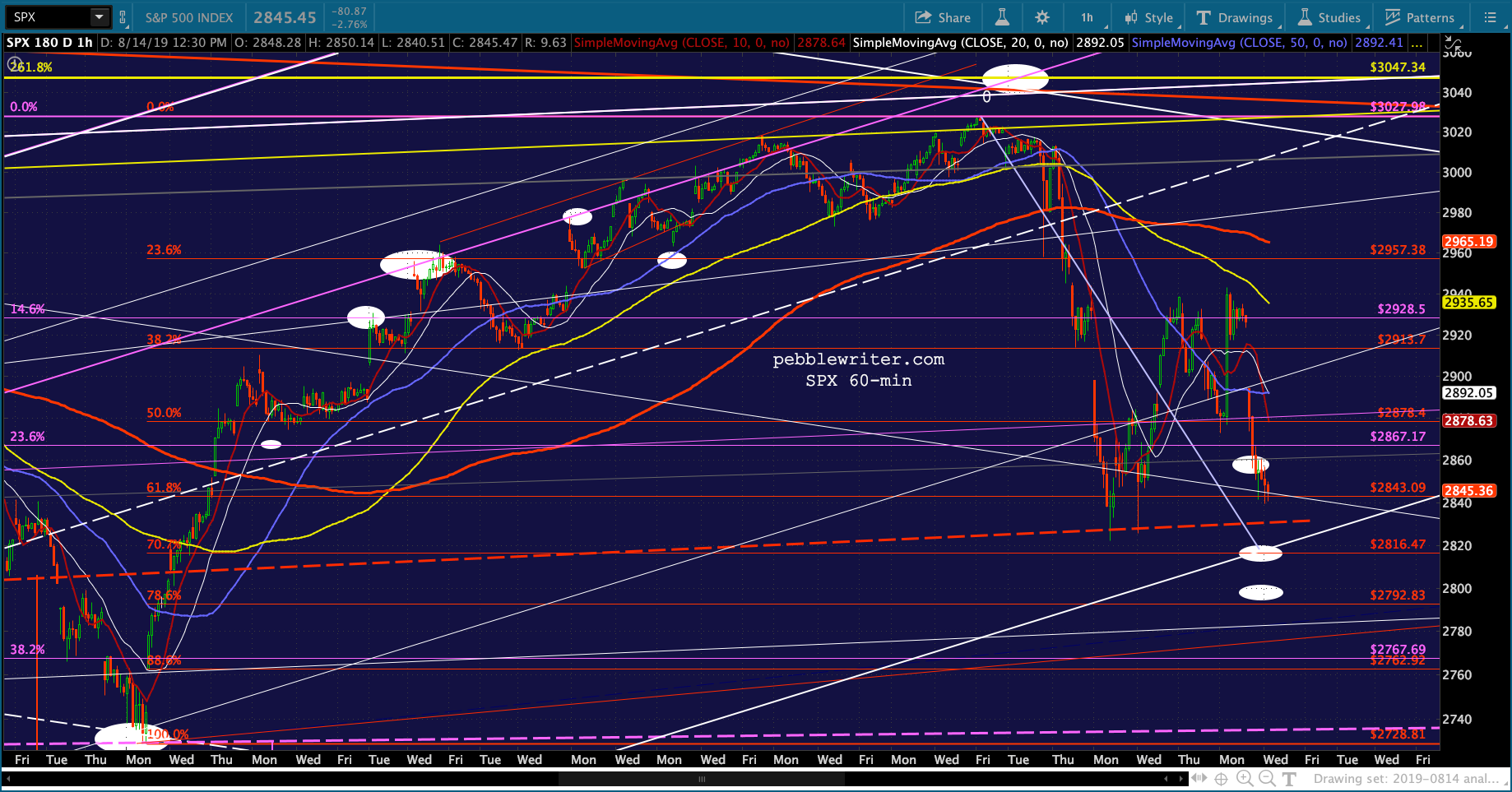

Just a few minutes left, and no clarity on whether this is the low or we might get one final flush. In any case, we’re pretty darned close to 2816.47, within spitting distance of 2800. No guarantee we won’t get another leg down now or in the morning. I would be very cautious if holding a short position overnight. I believe we’re still likely to see 2816 or the SMA200, now at 2795.73. But, I wouldn’t bet the farm on it.

I would be very cautious if holding a short position overnight. I believe we’re still likely to see 2816 or the SMA200, now at 2795.73. But, I wouldn’t bet the farm on it.

Comments

2 responses to “No Soup for You!”

You’ve got this analog oiled well! Running smooth.

Thanks Jamie. I’m trying!