December CPI came in at 2.9%, in line with expectations and lower than many had feared. Core CPI was 3.2%, down from the outlook of 3.3%.

Futures, already in the green after strong earnings from key banks, soared in a relief rally. Though not out of the woods, if stocks can hold current levels it would do serious damage to the bears’ case.

Though December’s CPI has helped stocks, January’s has the potential to do more damage as it tops 3%.

Though December’s CPI has helped stocks, January’s has the potential to do more damage as it tops 3%.

continued for members…

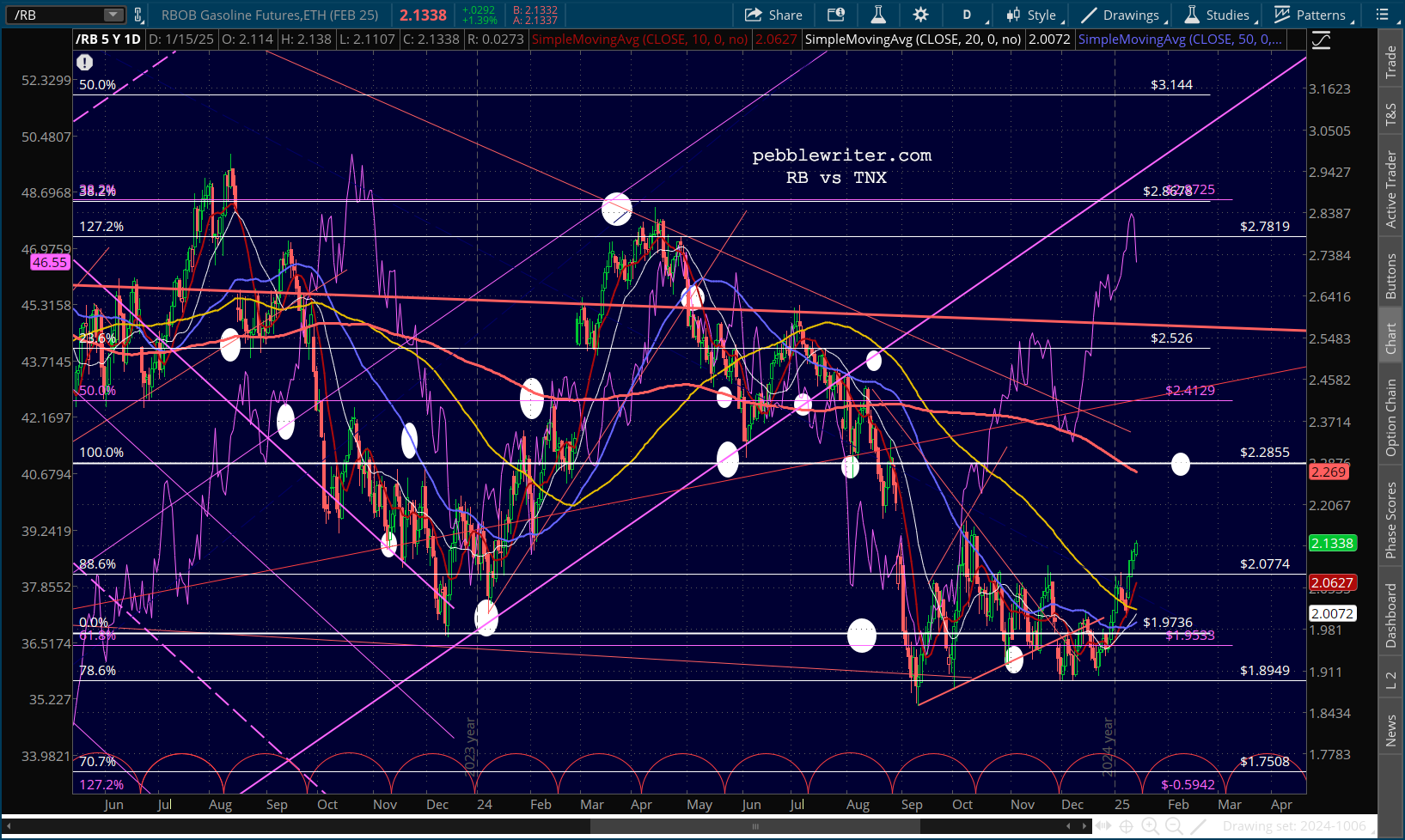

As of right now, the 10Y has reversed back below the breakout seen the past two sessions. The key is 4.698 – which might be difficult to hold if oil and gas continue to rise.

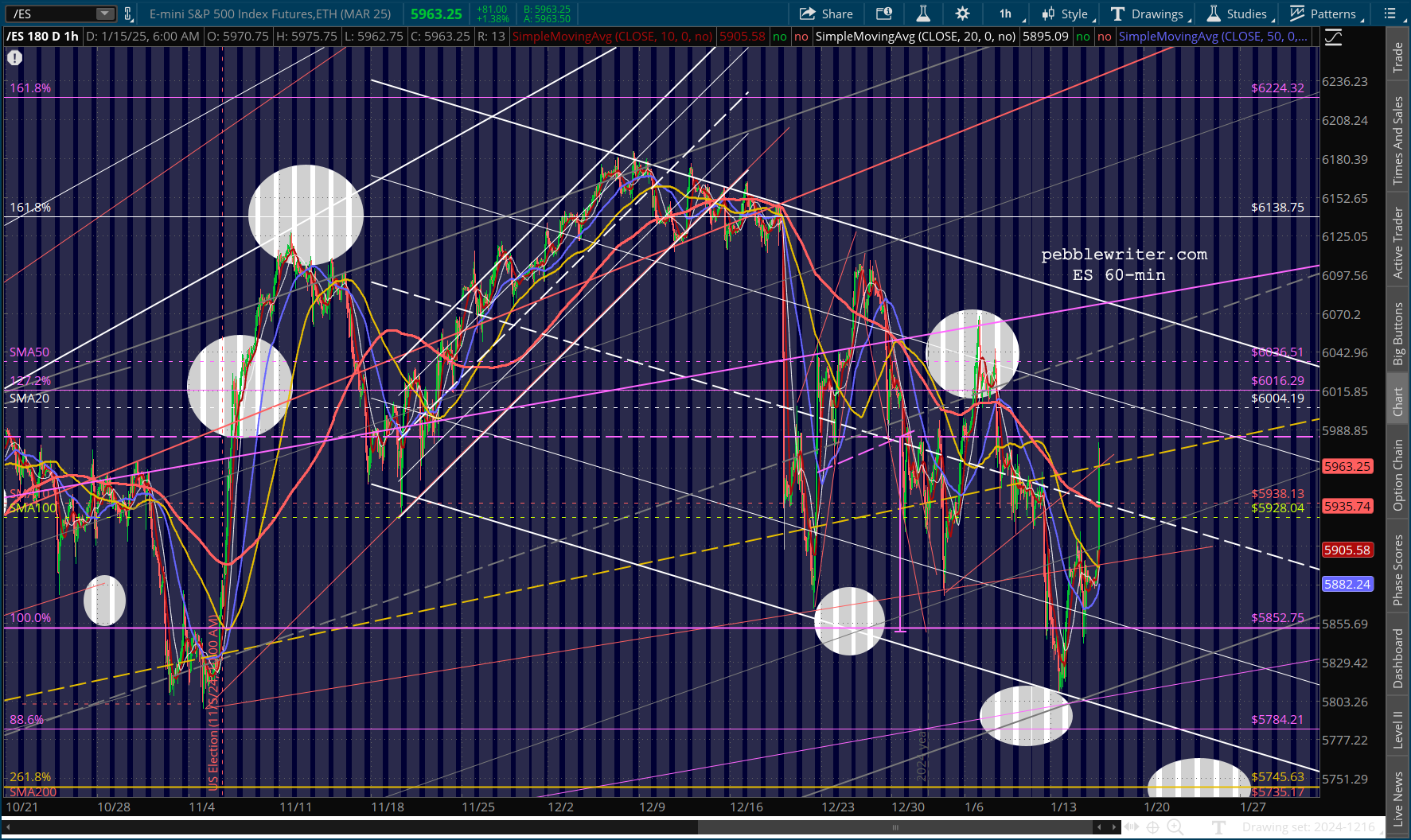

Futures will open above their SMA10 but below the SMA20.

Futures will open above their SMA10 but below the SMA20.

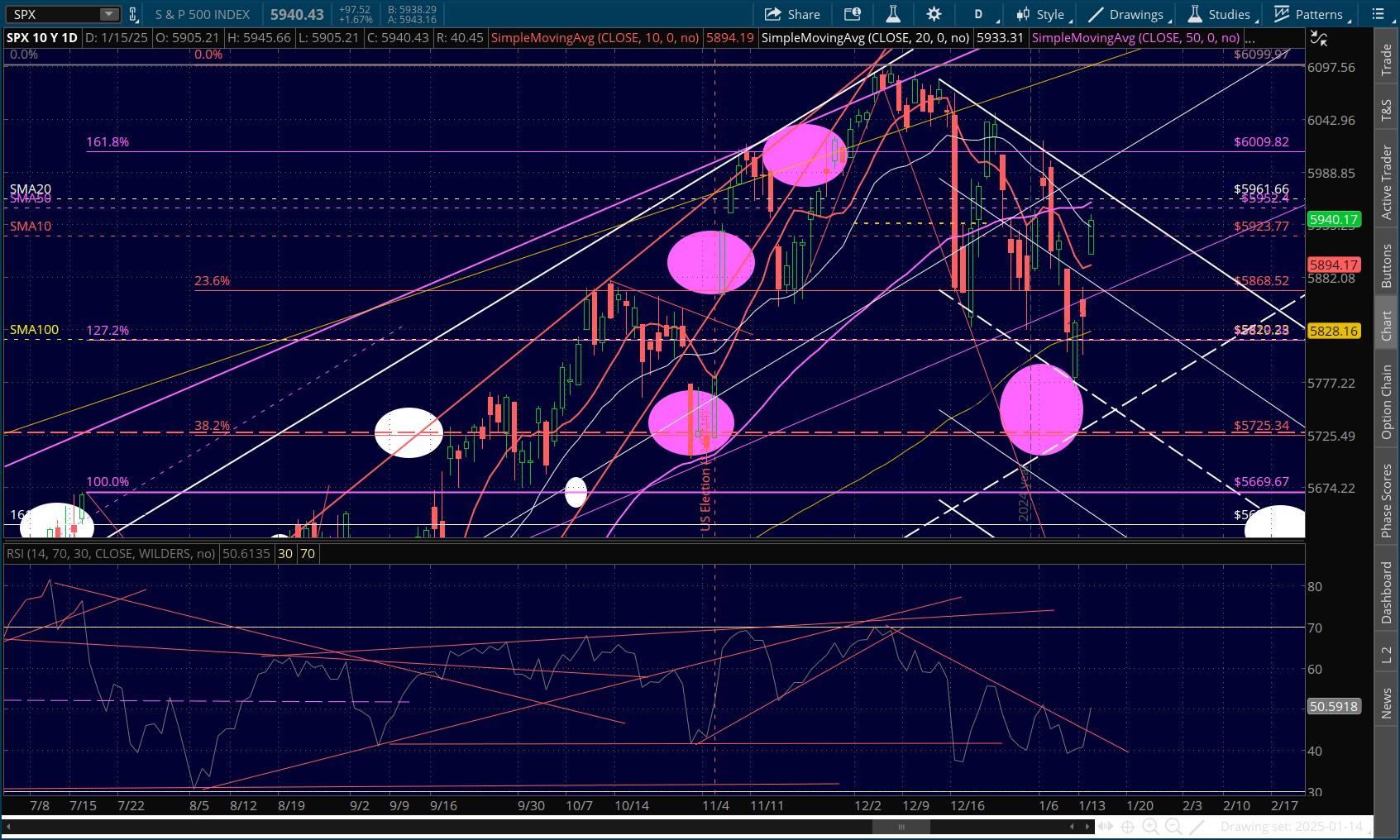

If today’s session doesn’t fall apart, it at the very least pushes the downside targets out into Feb and Mar. For SPX to get back on a bullish track, however, it would need to push above its SMA50.

If today’s session doesn’t fall apart, it at the very least pushes the downside targets out into Feb and Mar. For SPX to get back on a bullish track, however, it would need to push above its SMA50.

Note that VIX has not broken down, usually required for stocks to break out.

Note that VIX has not broken down, usually required for stocks to break out. Though the DXY is off 0.47%, its chart is still bullish. Even though the 10Y is currently 10 bps lower…

Though the DXY is off 0.47%, its chart is still bullish. Even though the 10Y is currently 10 bps lower…

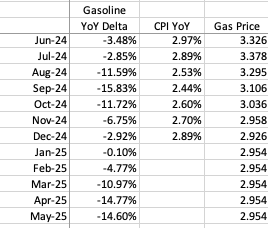

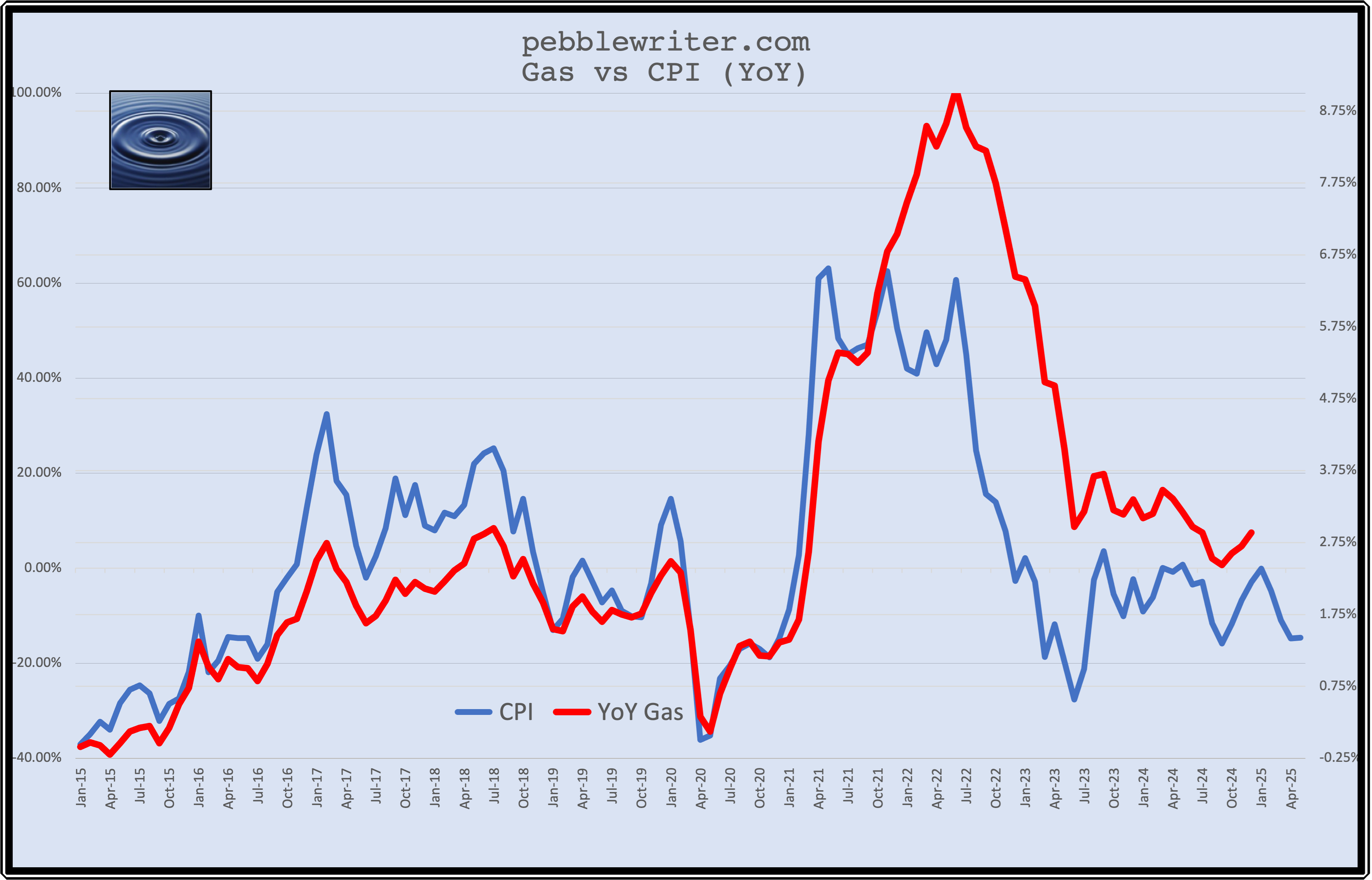

…oil and gas continue to rise. The January CPI print therefore remains problematic.

…oil and gas continue to rise. The January CPI print therefore remains problematic.

So the period following Feb 12, when Jan CPI is released, becomes more difficult. If stocks can get past that CPI print without dropping through the SMA200, then the YoY gas factor turns positive. Assuming gas prices can hold current levels, we would start to see a negative YoY change…

So the period following Feb 12, when Jan CPI is released, becomes more difficult. If stocks can get past that CPI print without dropping through the SMA200, then the YoY gas factor turns positive. Assuming gas prices can hold current levels, we would start to see a negative YoY change…

…that should mitigate sticky prices in other inflation categories.

…that should mitigate sticky prices in other inflation categories.

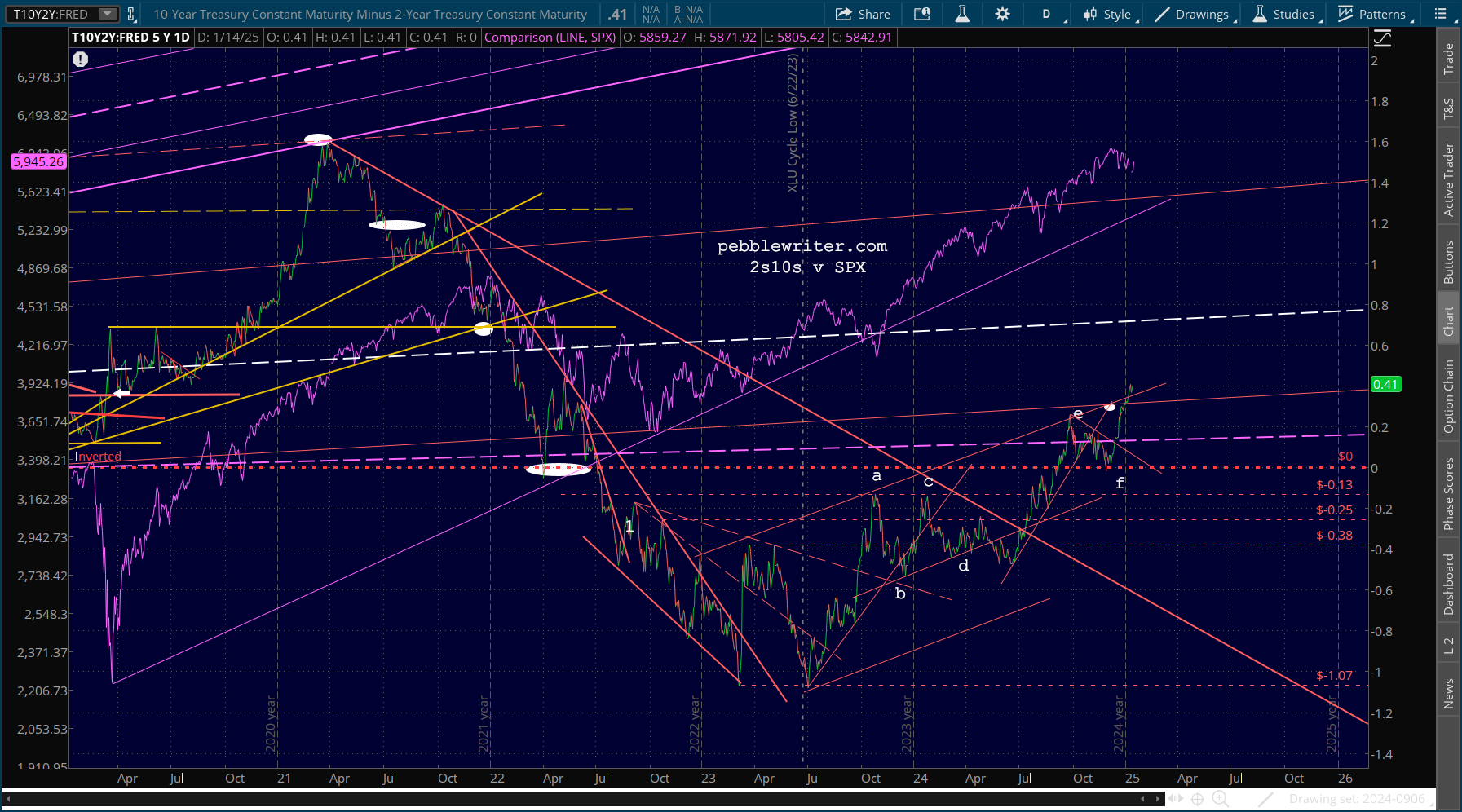

It’s important to note that the 2s10s is still above 40 bps, seemingly breaking out – which would be a huge negative for stocks.

It’s important to note that the 2s10s is still above 40 bps, seemingly breaking out – which would be a huge negative for stocks.