Inflationless growth. Sounds too good to be true, like “tastes great, less filling.”

Seasonally-adjusted CPI came in at 0.2% MoM and 2.2% YoY. Without seasonal adjustment, the MoM figure would have been 0.5% again. And, without the 7.7% YoY increase in energy prices, the annual number would have been below 2%.

Bottom line, the BLS threaded the needle on this report. The monthly figure (after adjusting, of course) was low enough to ease tensions over the acceleration in inflation seen over the past few months. But, the annual figure was high enough to ease tensions over an economic slowdown.

The biggest movers in the annual data were gasoline and fuel oil, at 12.6% and 20.7% respectively — reinforcing the fact that inflation is mostly about oil and gas. For once, the BLS’ data was almost in line with other official reports.

The biggest movers in the annual data were gasoline and fuel oil, at 12.6% and 20.7% respectively — reinforcing the fact that inflation is mostly about oil and gas. For once, the BLS’ data was almost in line with other official reports.

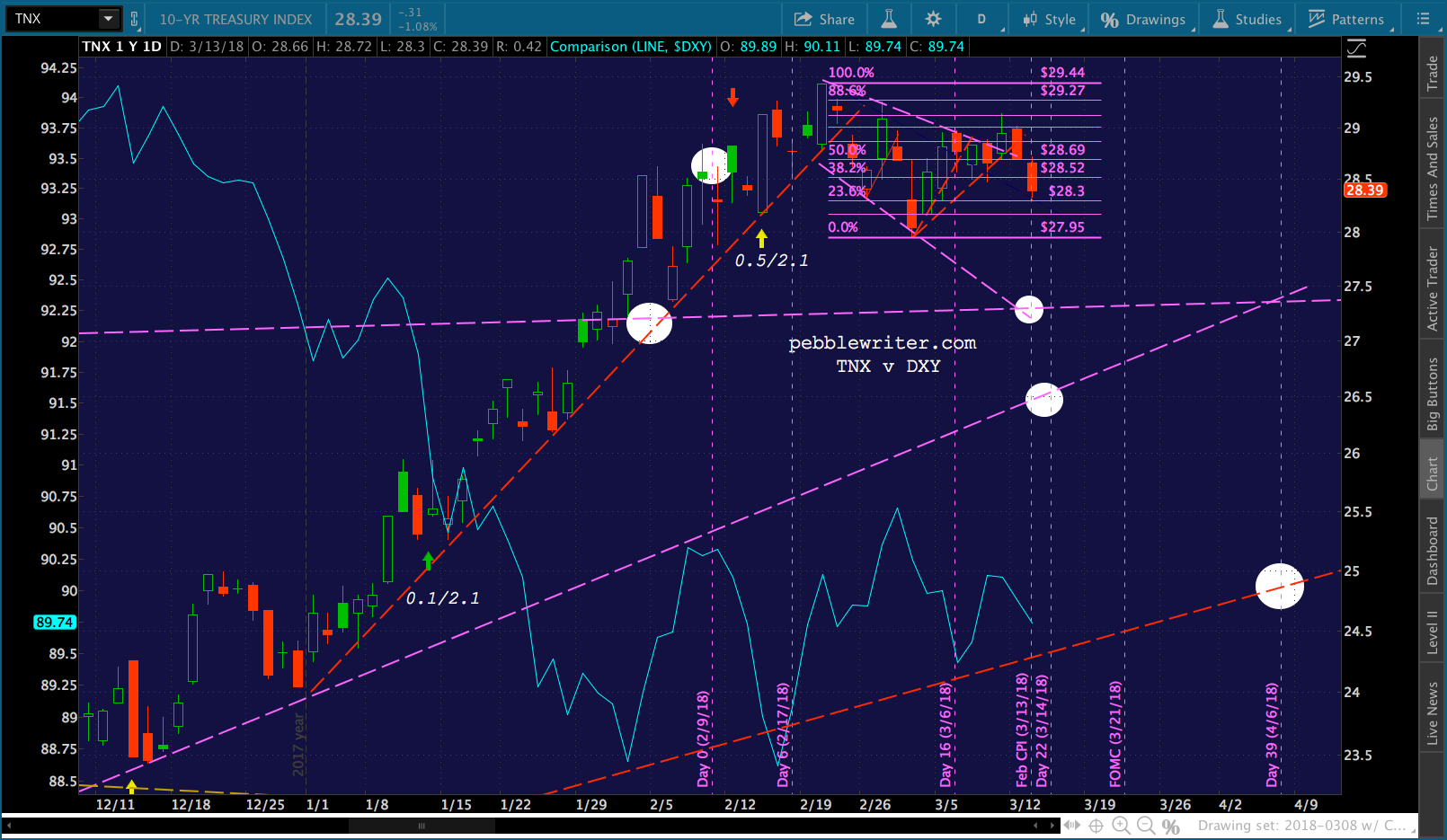

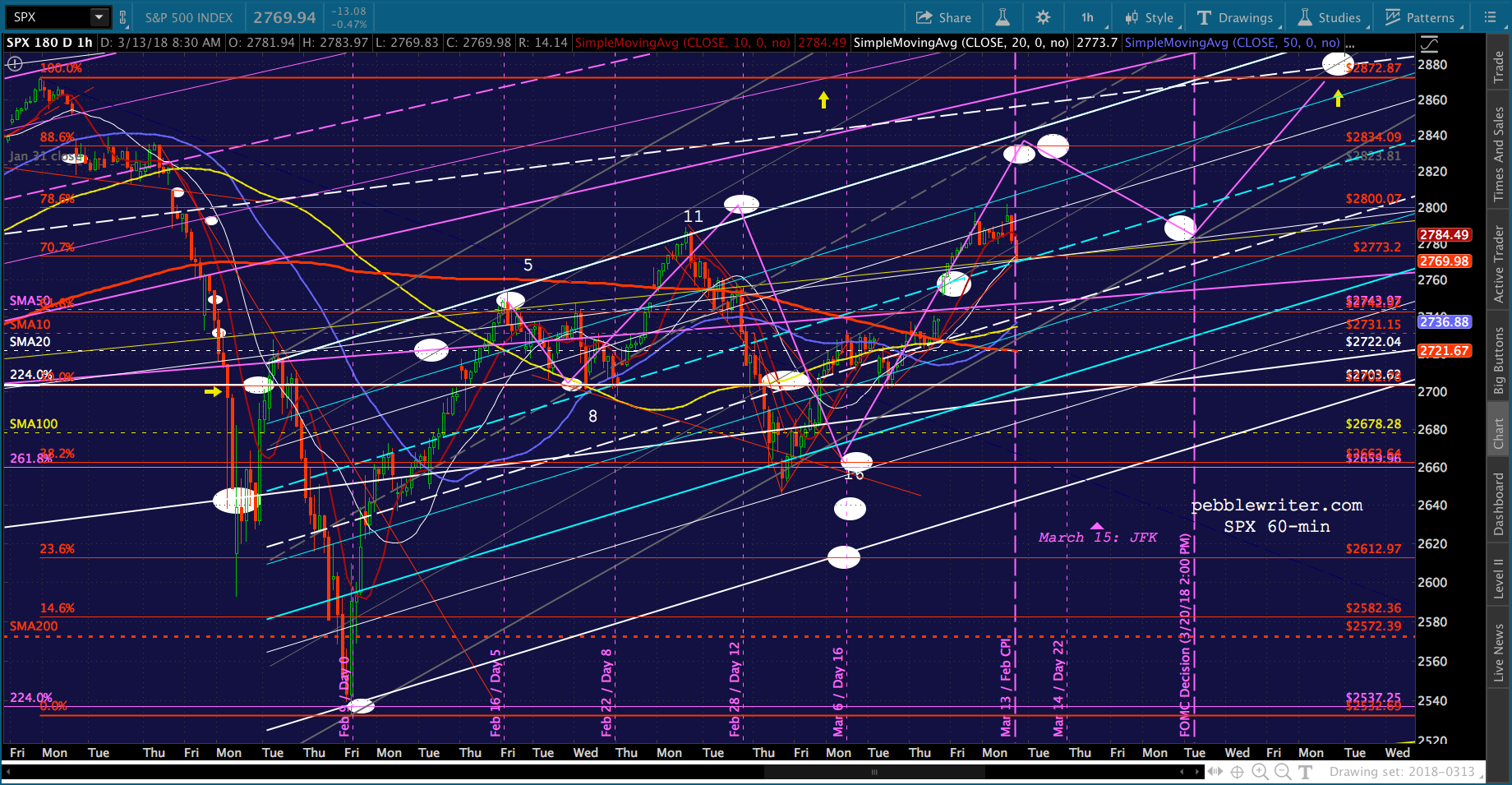

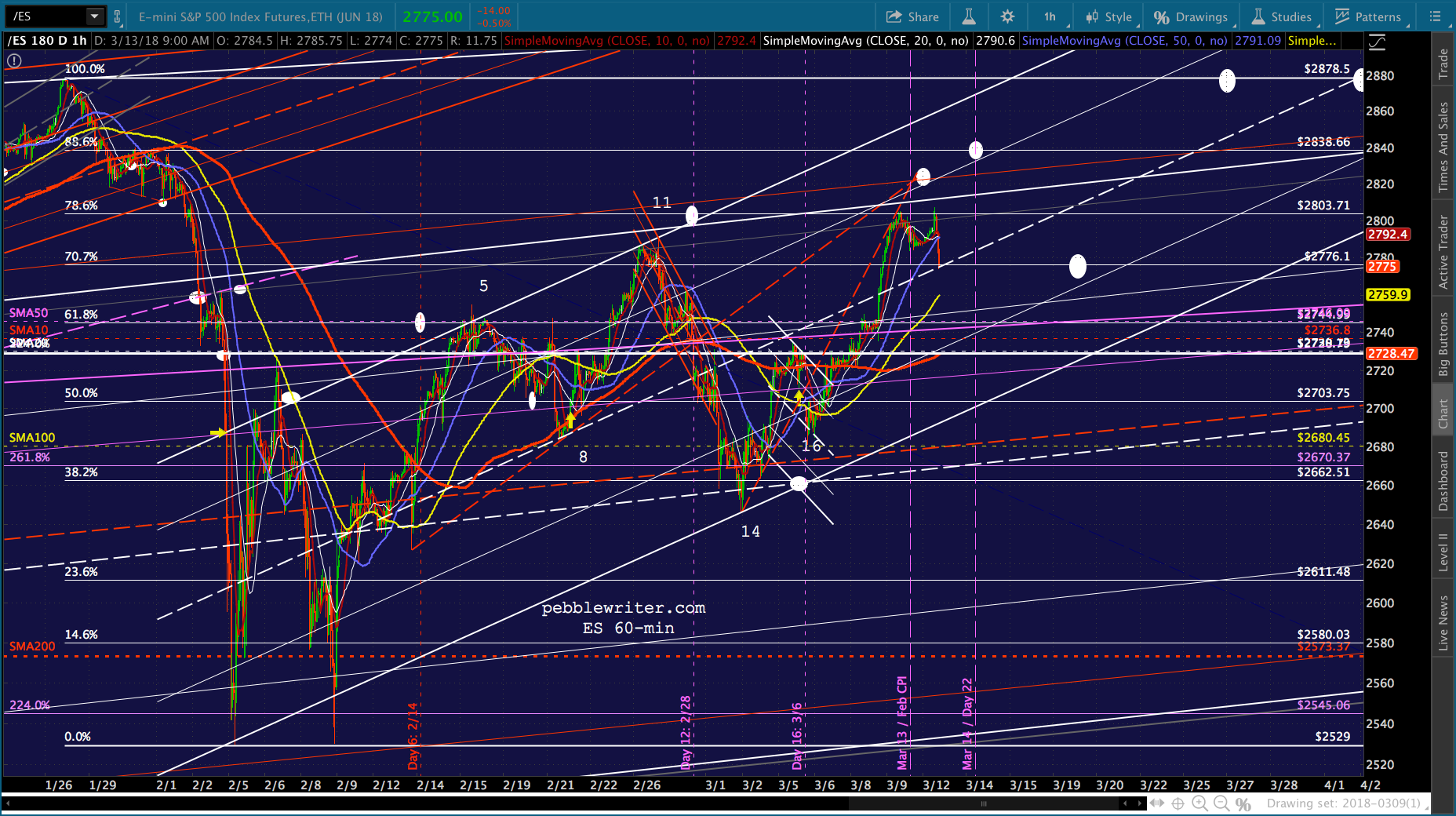

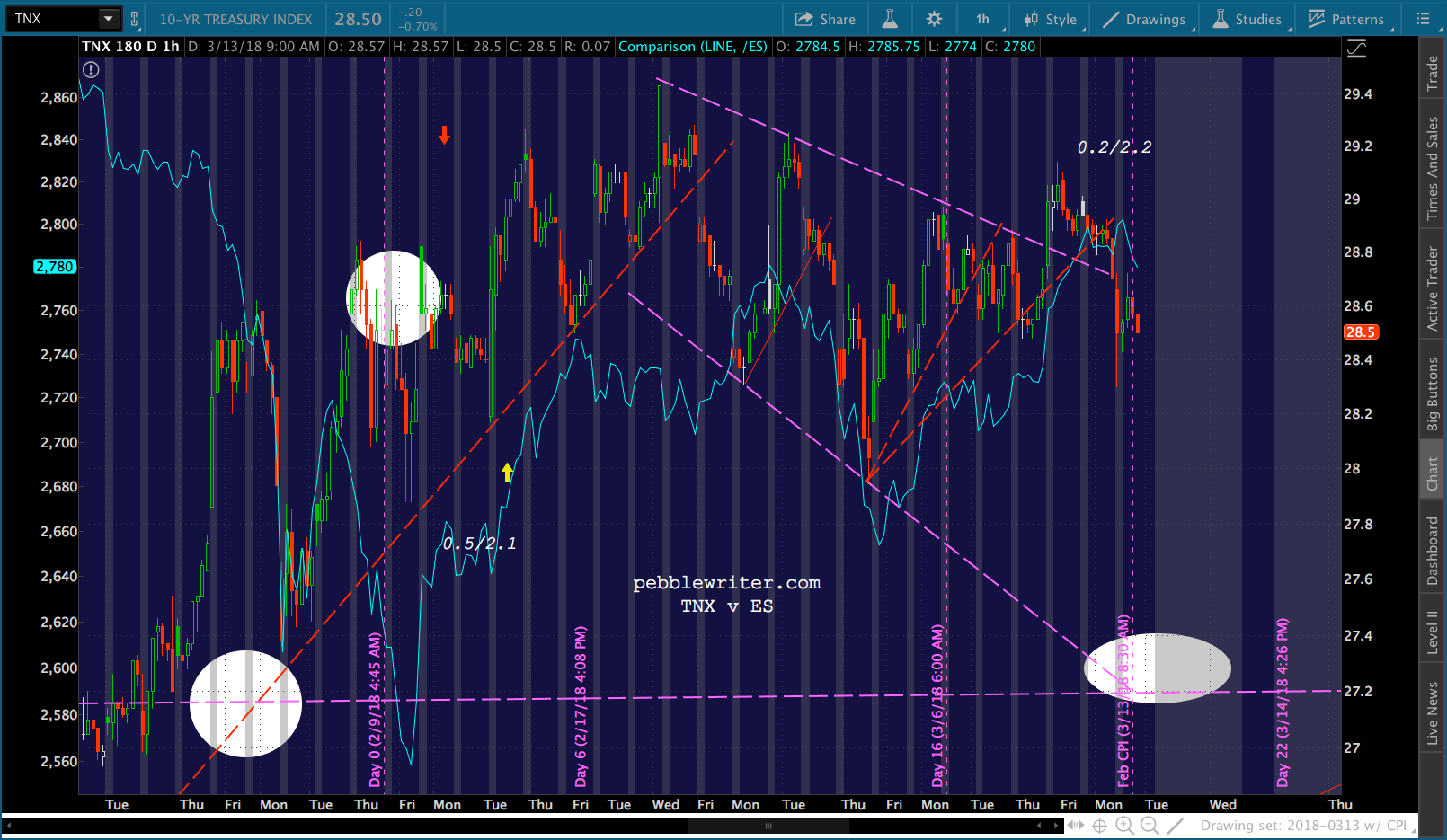

As expected, the bond market is relieved by the report. 10Y yields have dropped fairly sharply off recent (headfake) highs.

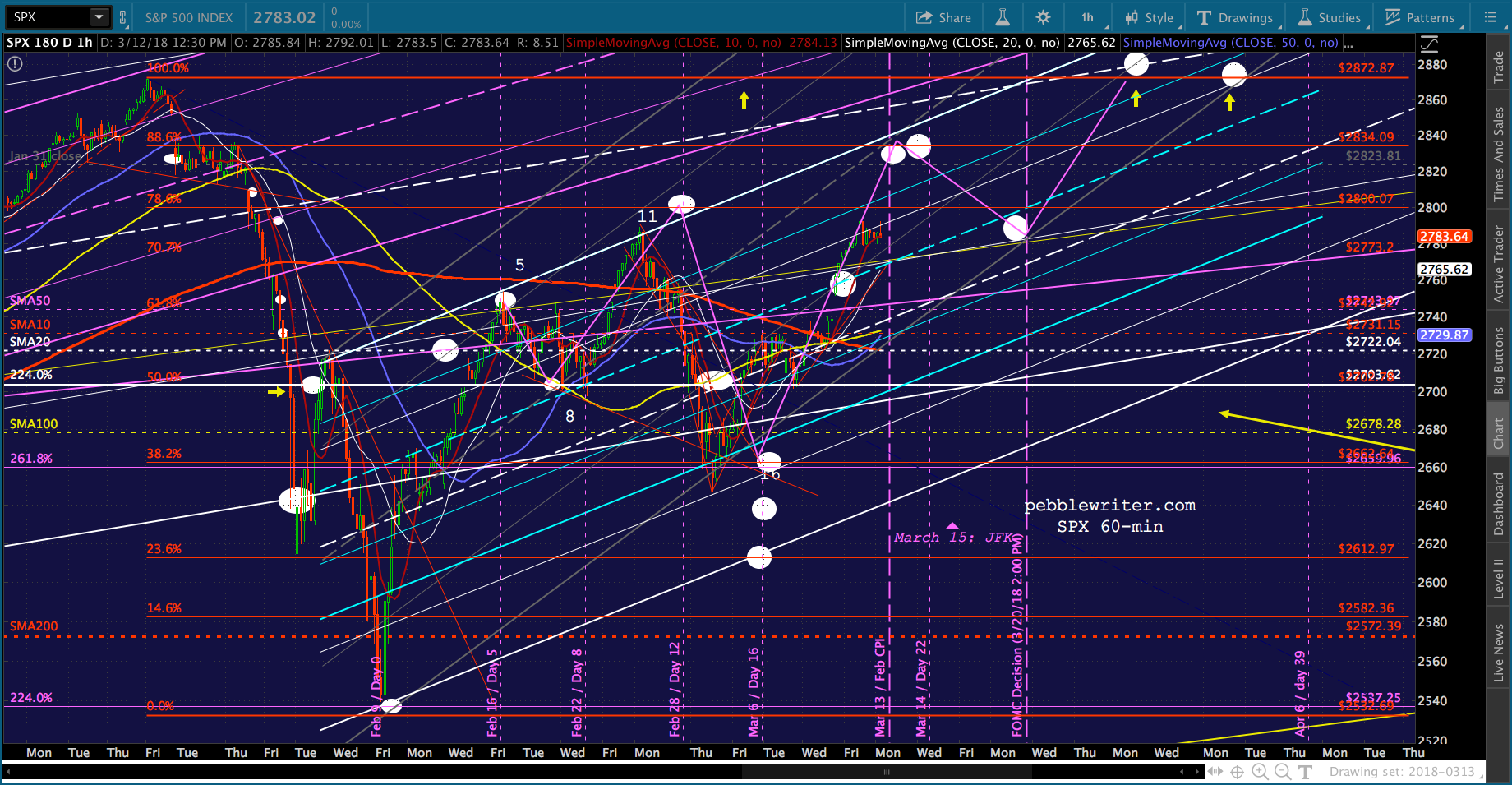

As expected, the bond market is relieved by the report. 10Y yields have dropped fairly sharply off recent (headfake) highs. Equities are responding favorably, with ES back over its .786 as SPX approaches its (2800.07.) Both are now within easy striking distance of our next upside targets — thanks largely to algos reaction to the yield drop, USDJPY’s breakout and VIX’s smack down.

Equities are responding favorably, with ES back over its .786 as SPX approaches its (2800.07.) Both are now within easy striking distance of our next upside targets — thanks largely to algos reaction to the yield drop, USDJPY’s breakout and VIX’s smack down.

It remains to be seen what they’ll think of the loss of Cohn and Tillerson.

It remains to be seen what they’ll think of the loss of Cohn and Tillerson.

continued for members…

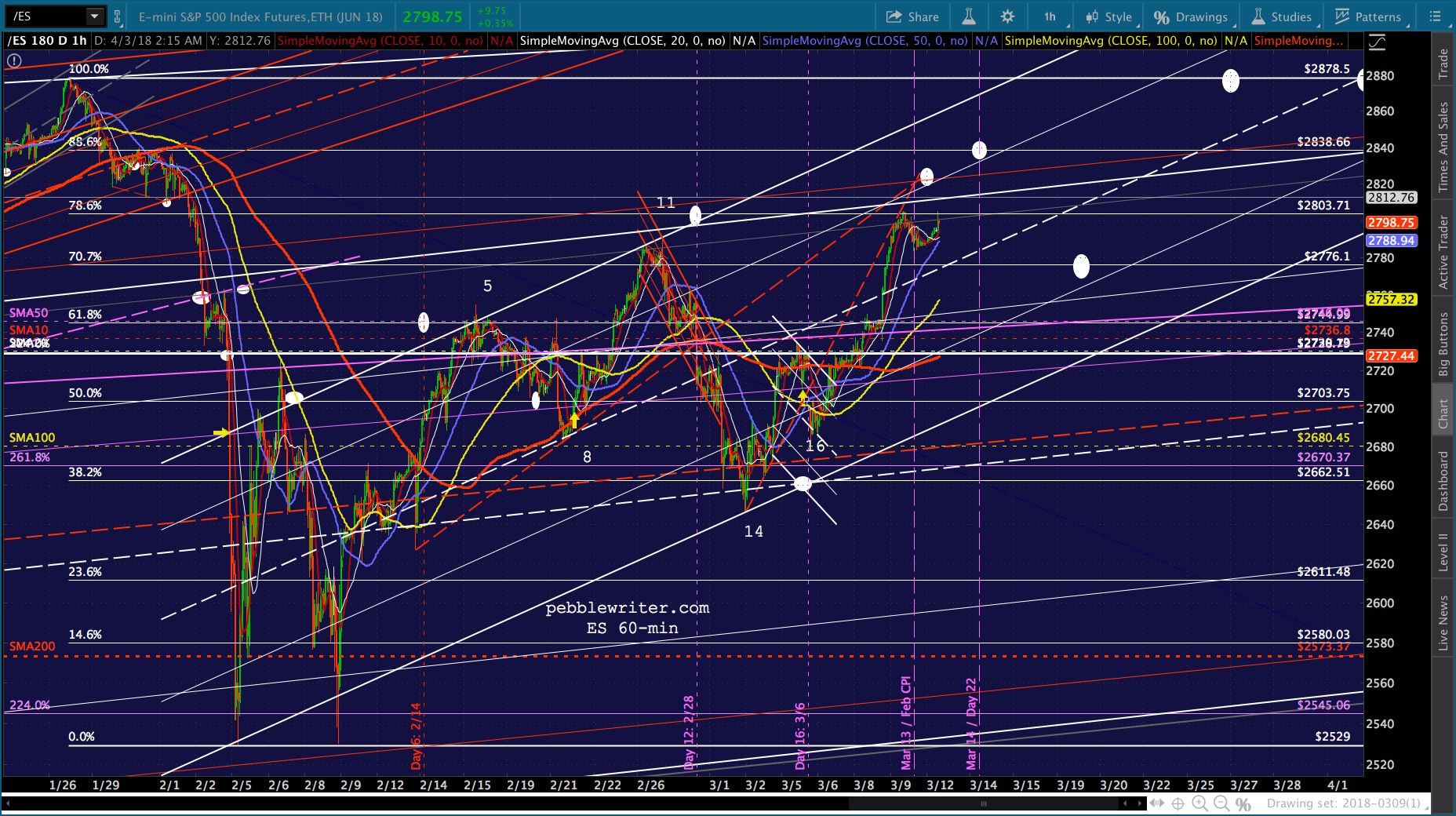

The bulls need ES to pop through its flatter white channel here.

If it gets over 2800.07, SPX faces token resistance until reaching the .886 at 2834.09. It’s unlikely to go straight there, though. Its usual course of action is to come close, then lay in wait until gapping through it some morning when the wind is blowing in the right direction.

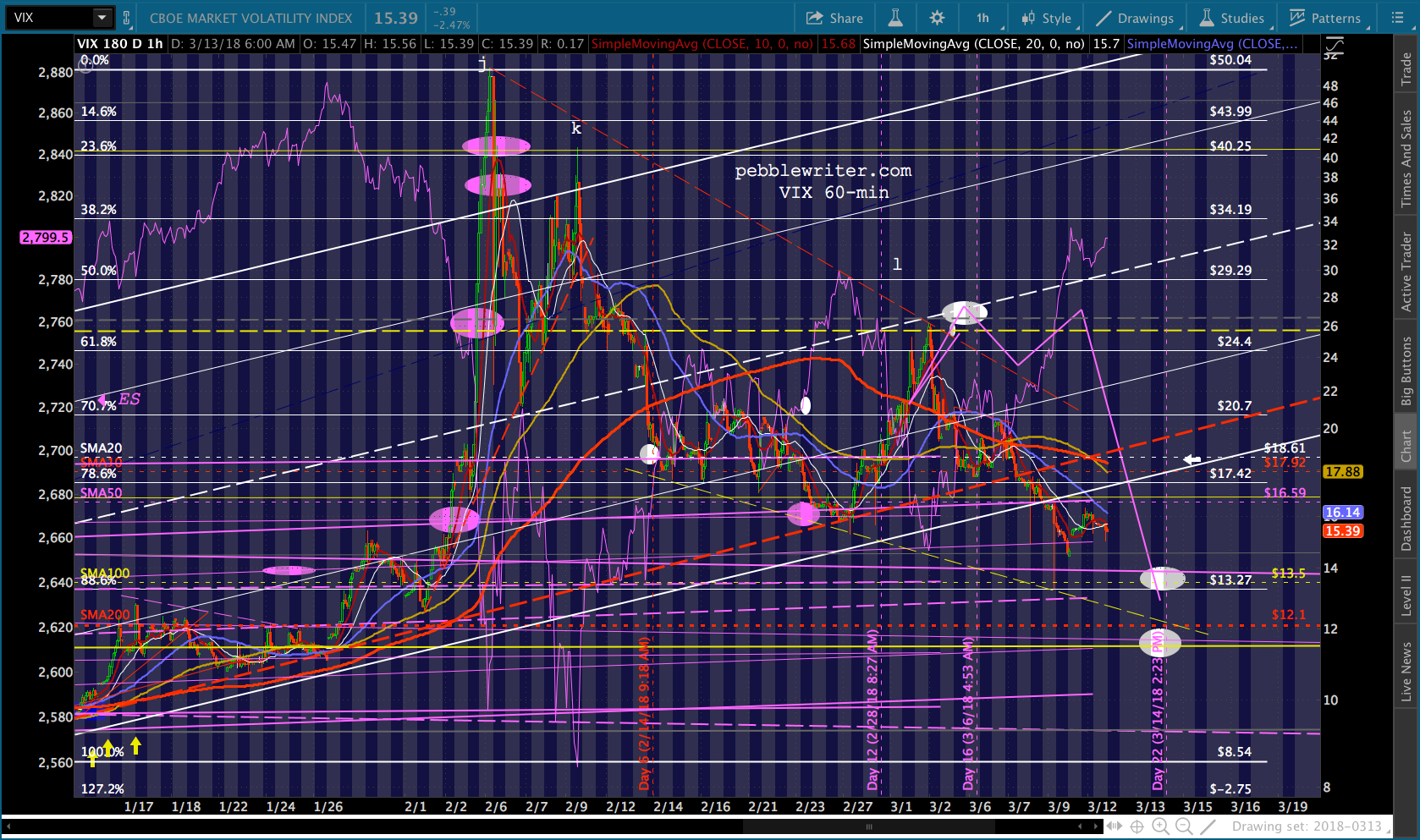

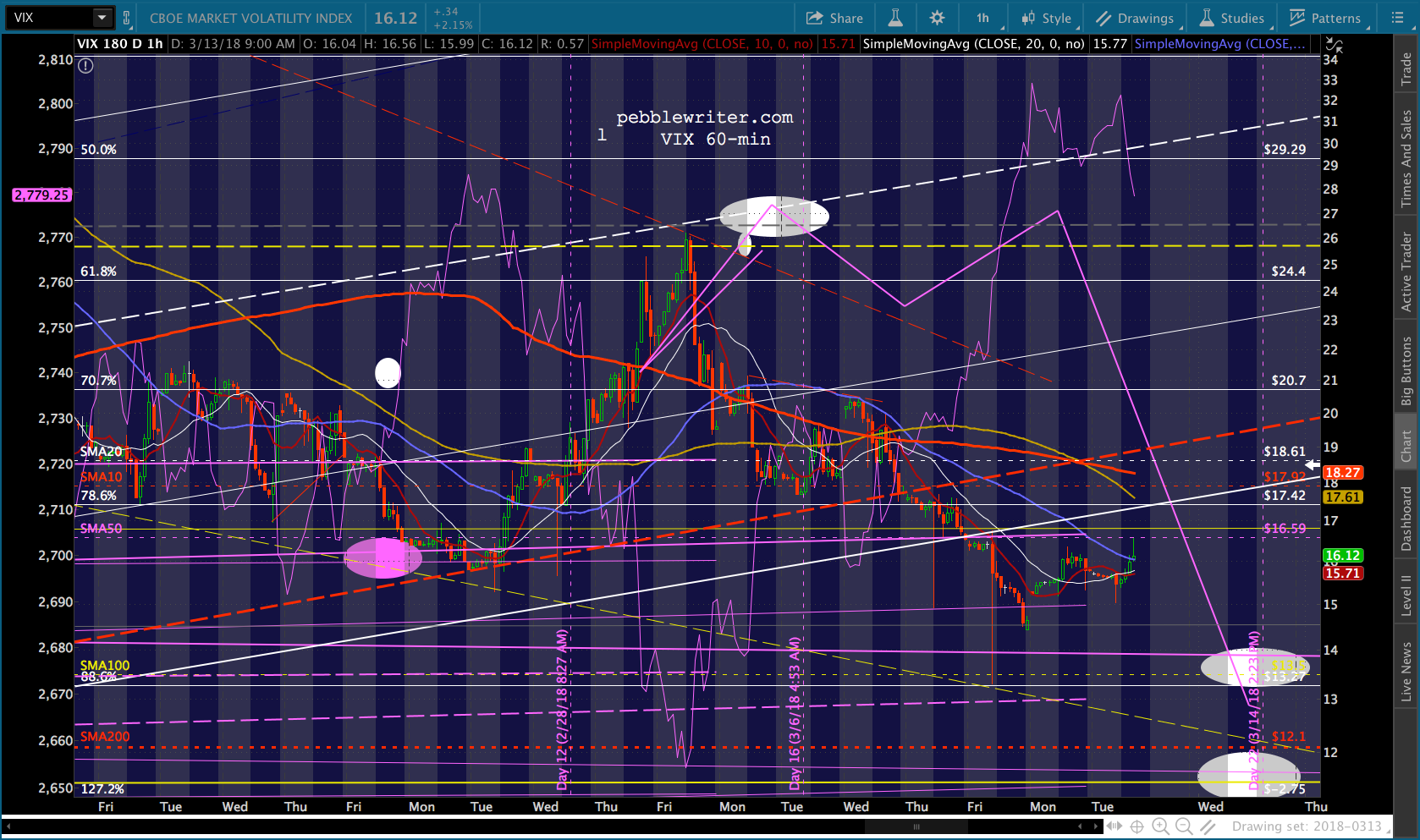

Note that VIX tagged the .886 retracement of its all-time low to the Feb highs (13.31 v 13.27) the other day. This would ordinarily mean a reversal higher, but there’s still a clear path to lower lows without any special gymnastics.

Note that VIX tagged the .886 retracement of its all-time low to the Feb highs (13.31 v 13.27) the other day. This would ordinarily mean a reversal higher, but there’s still a clear path to lower lows without any special gymnastics.

UPDATE: 11:00 AM

UPDATE: 11:00 AM

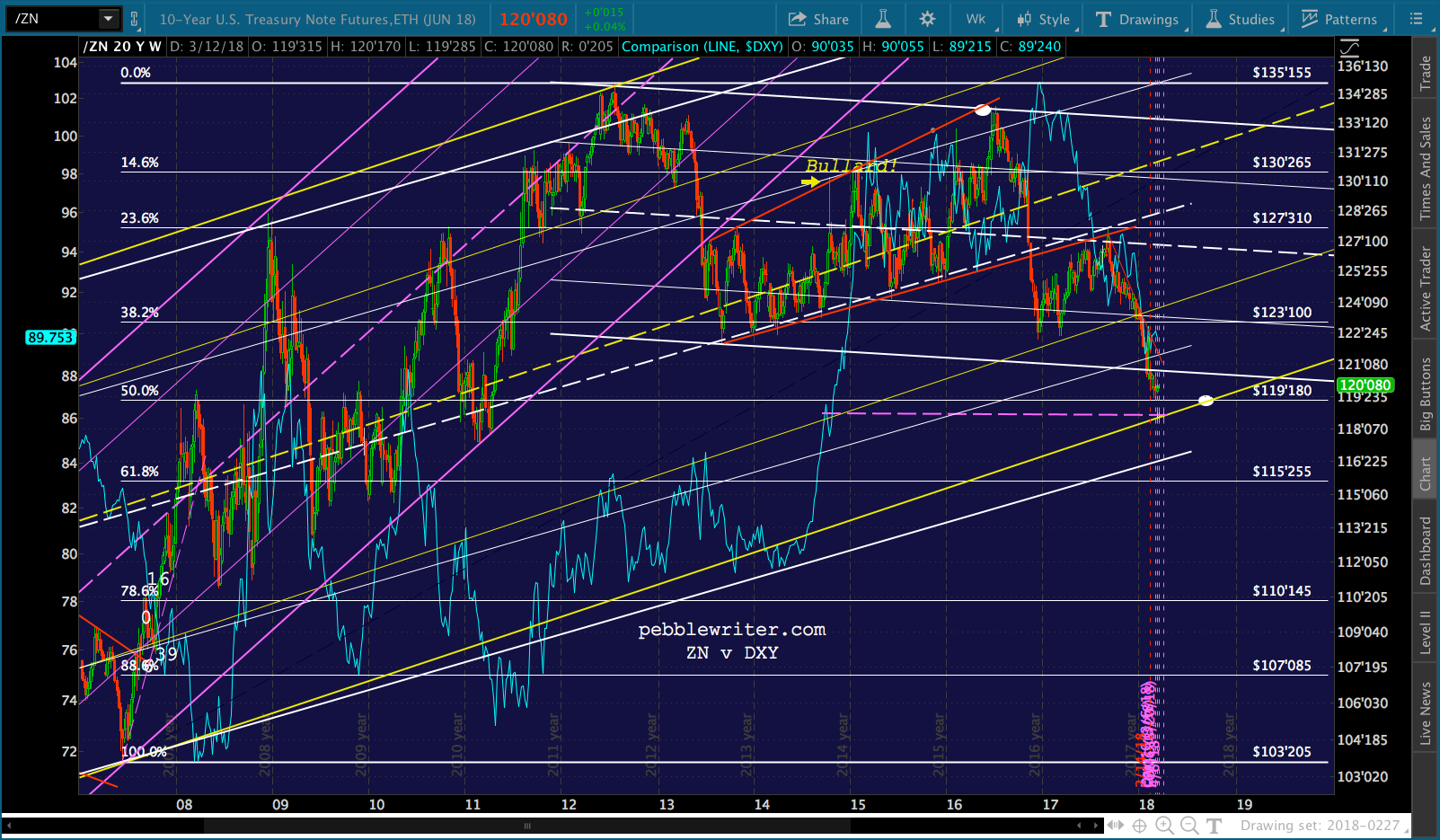

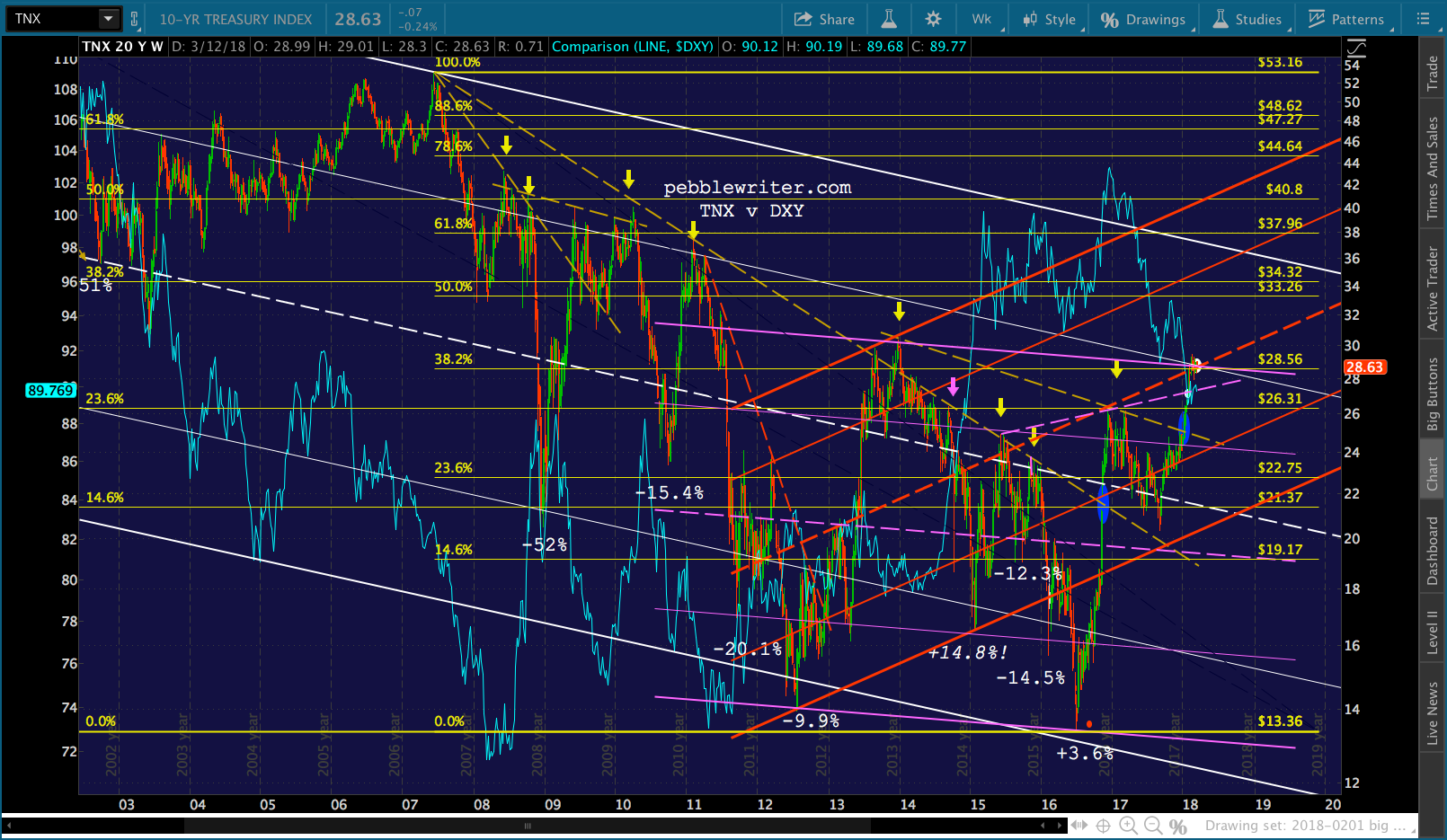

Tension remains in the battle between ZN reaching channel support and TNX retreating from a channel and Fib tag. ZN needs to tag the yellow channel bottom (though the white one would be more legit) at some point. The most logical point would be at the .500 Fib — but that intersection doesn’t occur until early October.

Obviously, it would dip down there at any time. But, it would likely need to occur on a day when stocks are being permitted a breather — as it would require rates (TNX) to pop higher. At this point, that would be undesirable. The next important resistance isn’t until 34.32, followed by 37.96.

Obviously, it would dip down there at any time. But, it would likely need to occur on a day when stocks are being permitted a breather — as it would require rates (TNX) to pop higher. At this point, that would be undesirable. The next important resistance isn’t until 34.32, followed by 37.96.  UPDATE: 12:10 PM

UPDATE: 12:10 PM

ES and SPX are backtesting their .707s and channel midlines — a good place for a bounce if they’re going higher…a good place for stops if they break down.

TNX bumped a little, but is settling lower.

TNX bumped a little, but is settling lower.  Remember, tomorrow is Day 22 – when VIX was supposed to collapse through support. It has already broken support, of course. But, there’s still room for more — reaching the actual .886, for instance, instead of merely coming close. We’ll be watching for signs of VIX breaking down. For now, all I see is higher lows and higher highs.

Remember, tomorrow is Day 22 – when VIX was supposed to collapse through support. It has already broken support, of course. But, there’s still room for more — reaching the actual .886, for instance, instead of merely coming close. We’ll be watching for signs of VIX breaking down. For now, all I see is higher lows and higher highs. UPDATE: 12:28 PM

UPDATE: 12:28 PM

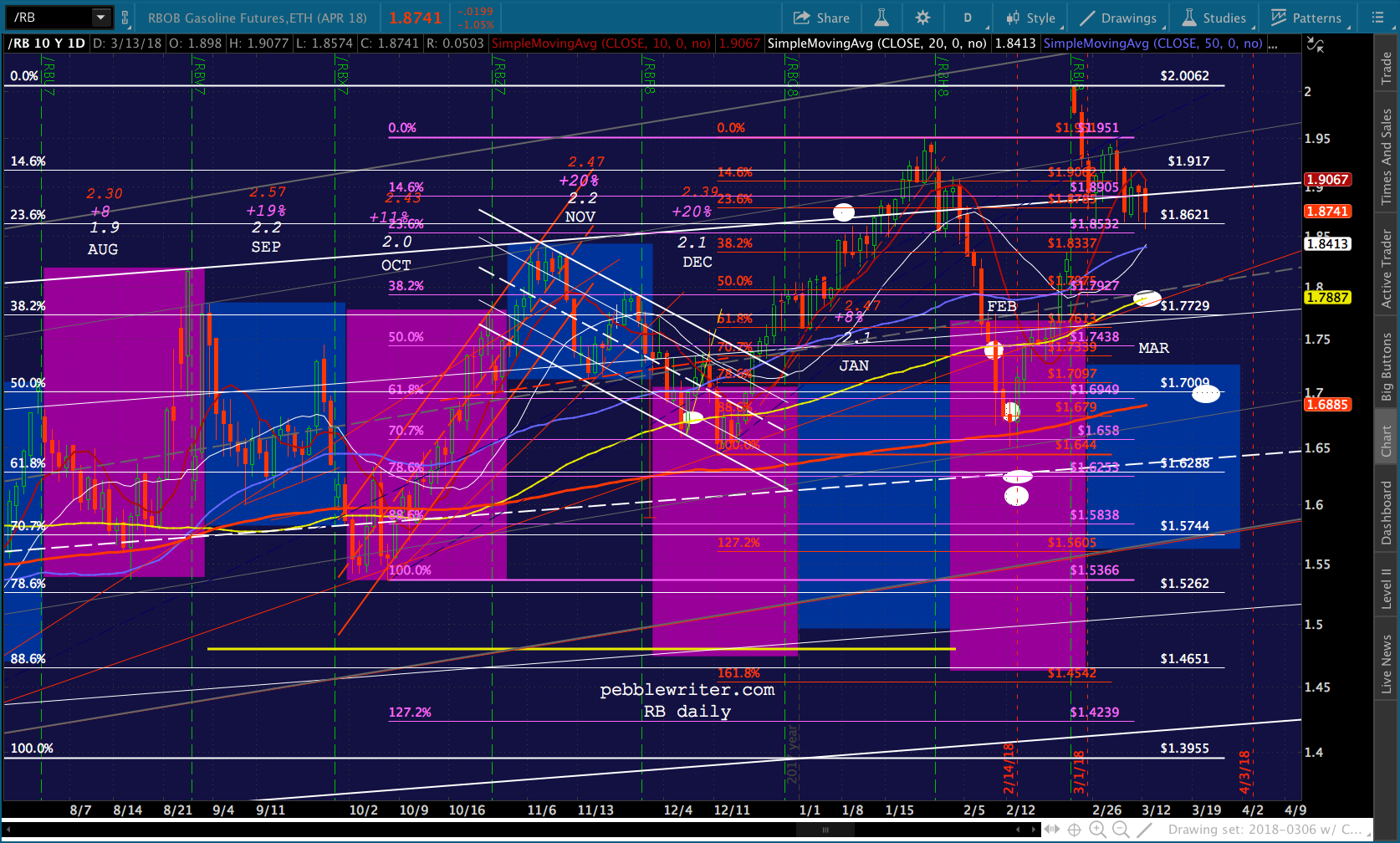

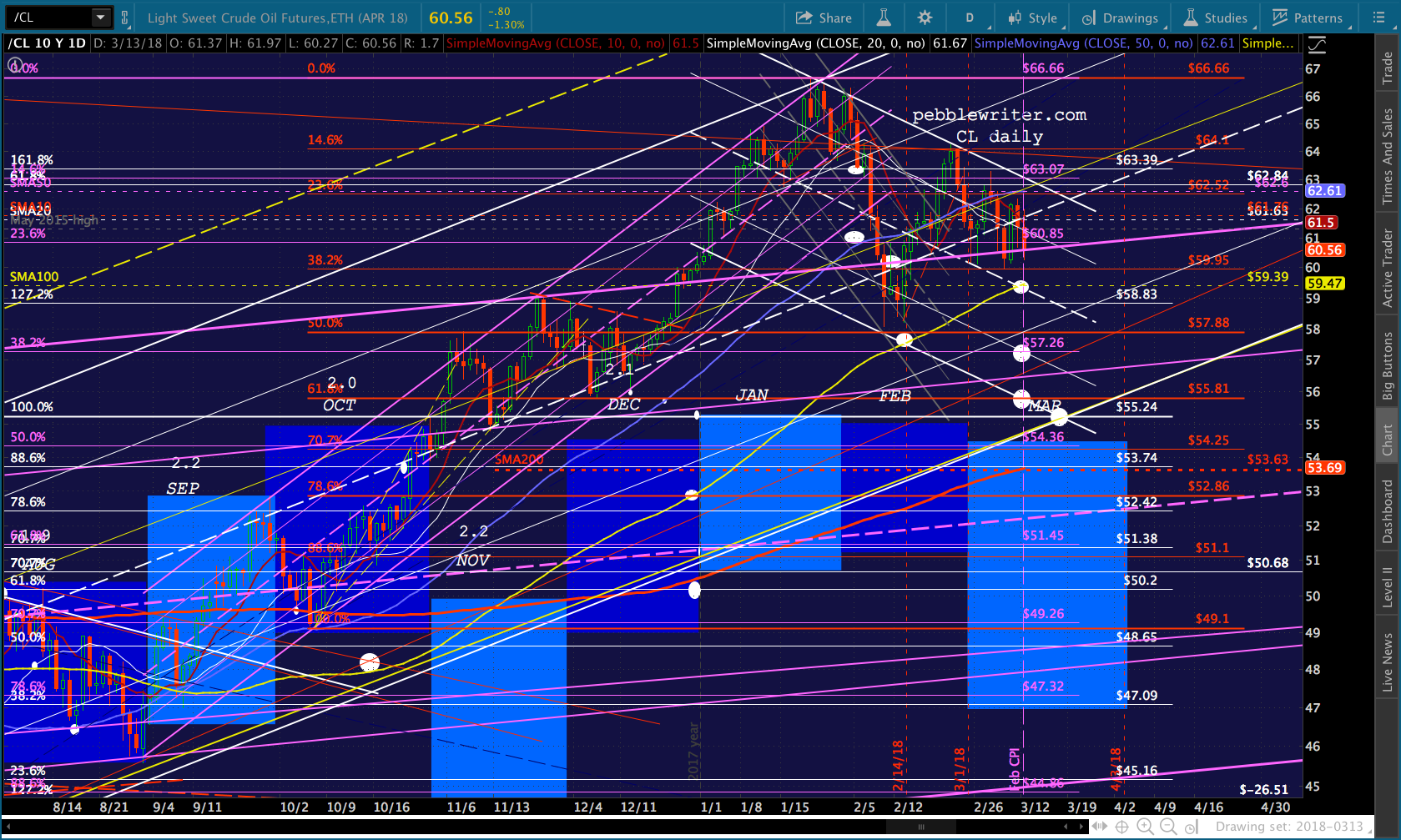

CL and RB continue to look vulnerable today. But, neither has officially given up on its channel “breakout.” It seems pretty apparent that each needs to sell off more if TPTB wish to repeat a desirable CPI number for March.

But, I suspect the selloffs won’t be significant until SPX/ES are ready for a meaningful retreat/backtest — perhaps after reaching (or nearing or backtesting) their .886 or Jan highs. If SPX/ES falter before then, look for CL and RB to lend support.

There’s about 15″ of snow on the ground and more coming down. The power keeps flickering, so I suspect power lines are coming down here and there. I’m going to sign off for now. If I don’t update later today, you’ll understand why.

There’s about 15″ of snow on the ground and more coming down. The power keeps flickering, so I suspect power lines are coming down here and there. I’m going to sign off for now. If I don’t update later today, you’ll understand why.

GLTA.