So far, the futures are ignoring another round of abysmal economic data:

- 5.25 million more unemployed, raising total filings to 22 million

- unemployment rate to 17%+, far exceeding the GFC’s 10%

- housing starts drop 22.3%, the most since 1984

- Philly Fed plunges to -56.6, the lowest since 1980 and worse than the GFC

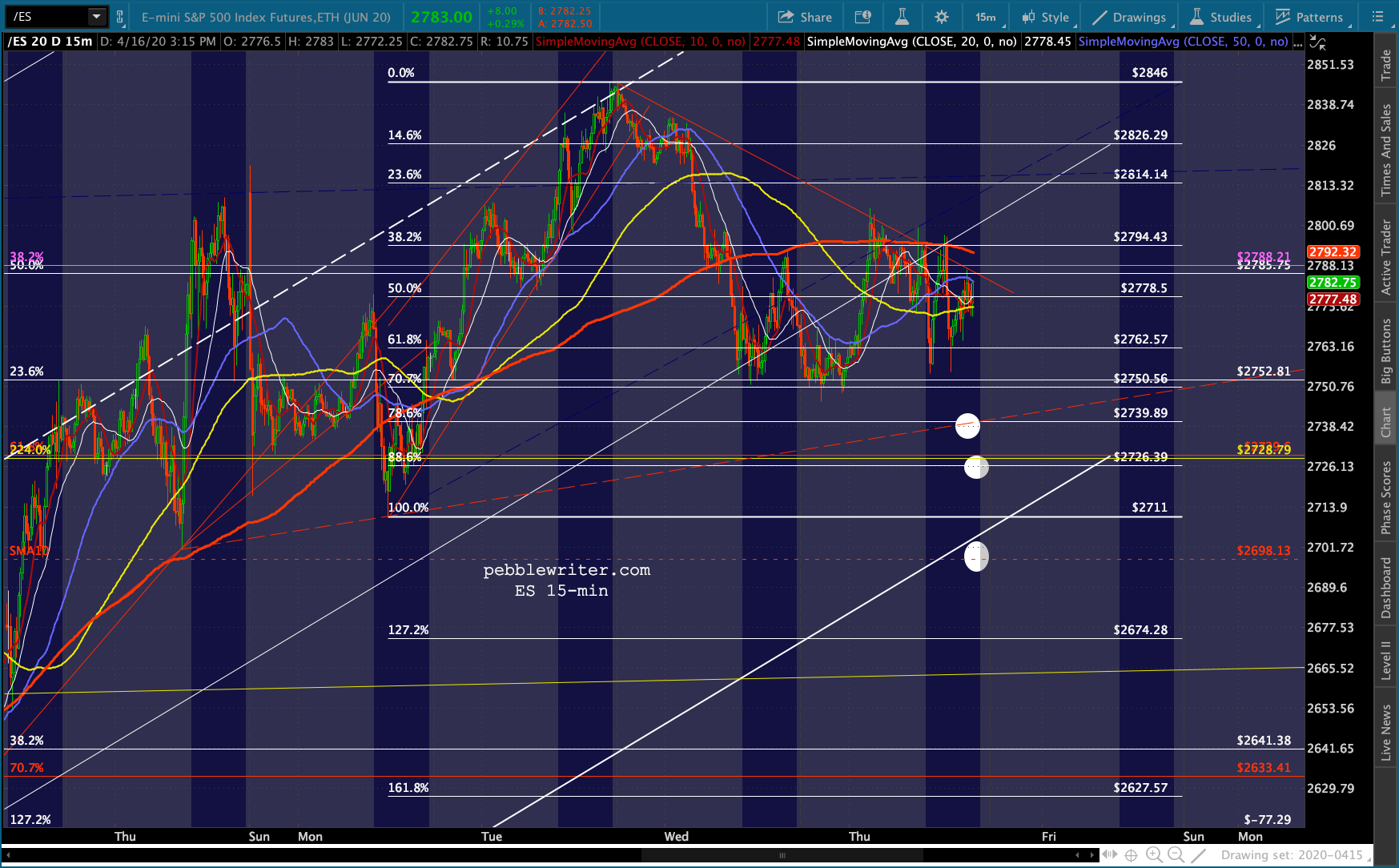

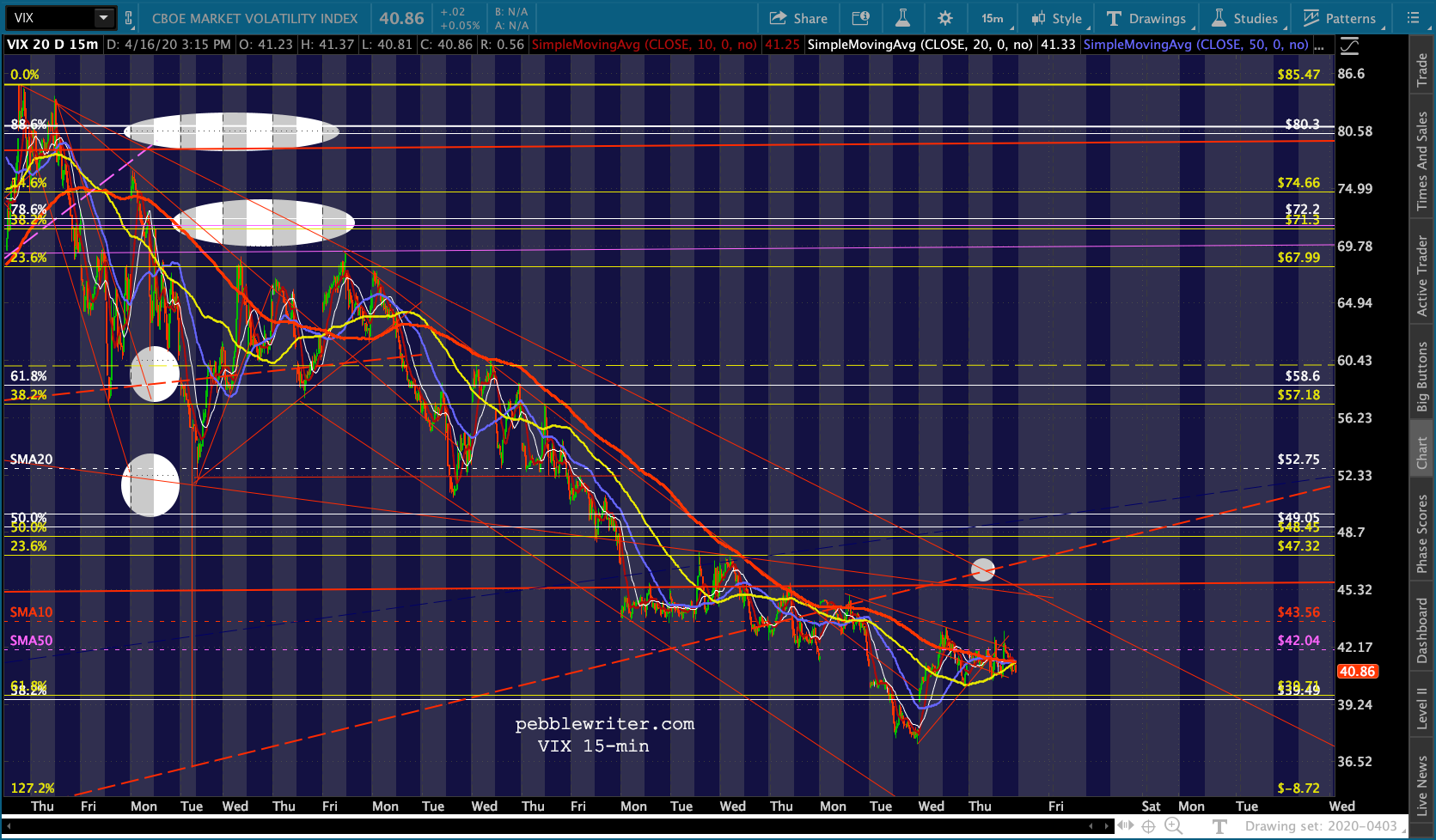

Instead of plunging, ES is up nearly 20 points as the algos are more concerned with VIX’s breakdown. Nothing new here, of course…but can it last past the open?

Nothing new here, of course…but can it last past the open?  Not if yesterday’s close by DJIA and COMP are any indication. The Dow passed up an opportunity to break out above its 2.24 extension…

Not if yesterday’s close by DJIA and COMP are any indication. The Dow passed up an opportunity to break out above its 2.24 extension… …and COMP pulled back and closed below its SMA200.

…and COMP pulled back and closed below its SMA200.  Not exactly the behavior of a market intent on higher highs… Meanwhile, global COVID-19 cases reached 2mm yesterday – up from 1mm on April 2. The US now accounts for over 30% of all cases and moved up from 44th to 43rd in testing per capital in the world.

Not exactly the behavior of a market intent on higher highs… Meanwhile, global COVID-19 cases reached 2mm yesterday – up from 1mm on April 2. The US now accounts for over 30% of all cases and moved up from 44th to 43rd in testing per capital in the world.

continued for members…

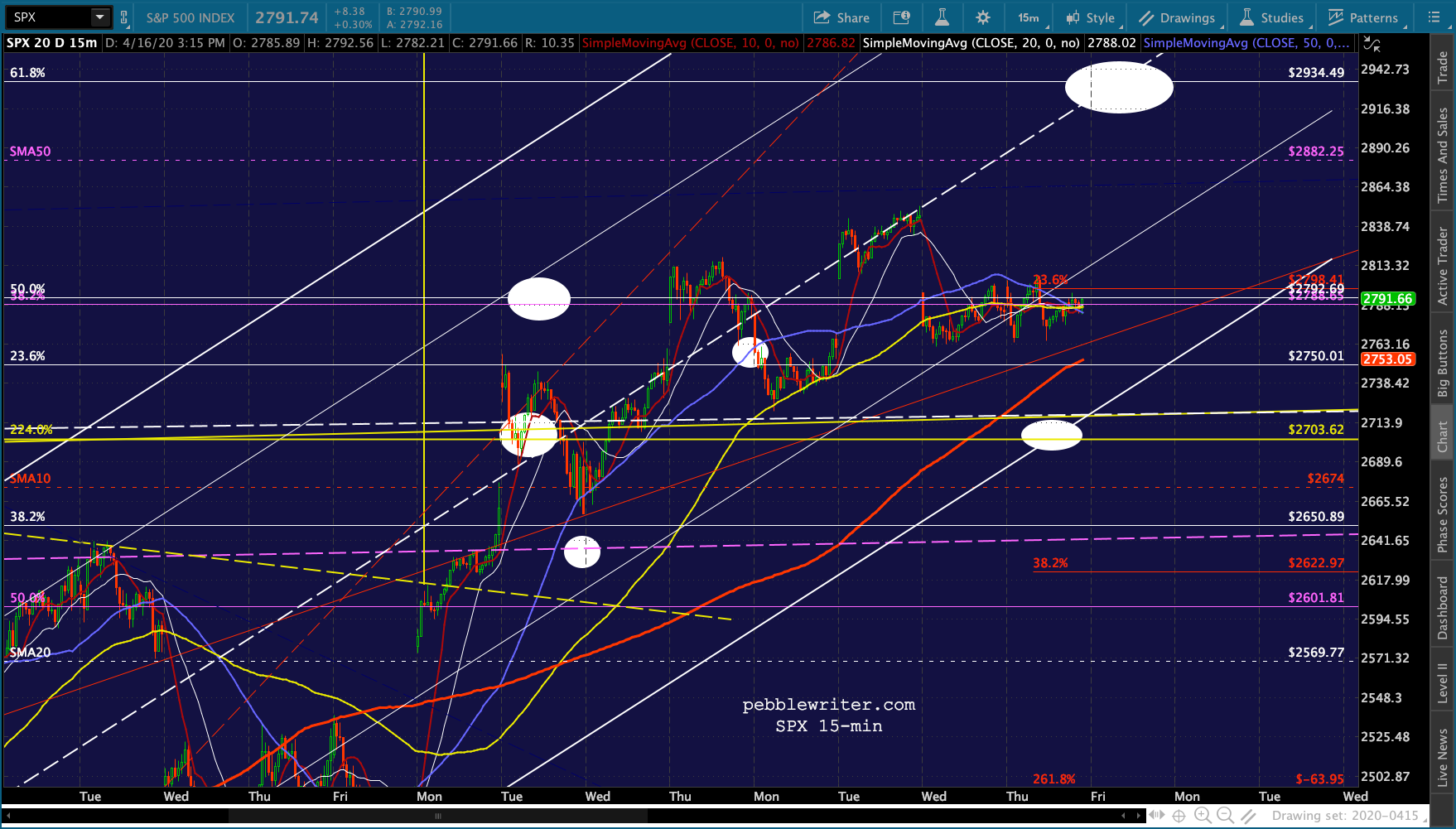

The breakout would be pretty easy to spot – likewise the breakdown.

SPX’s version offers a nice downside target at the 2.24 at 2703 – meaning any downside could be pushed off until tomorrow morning.

SPX’s version offers a nice downside target at the 2.24 at 2703 – meaning any downside could be pushed off until tomorrow morning.

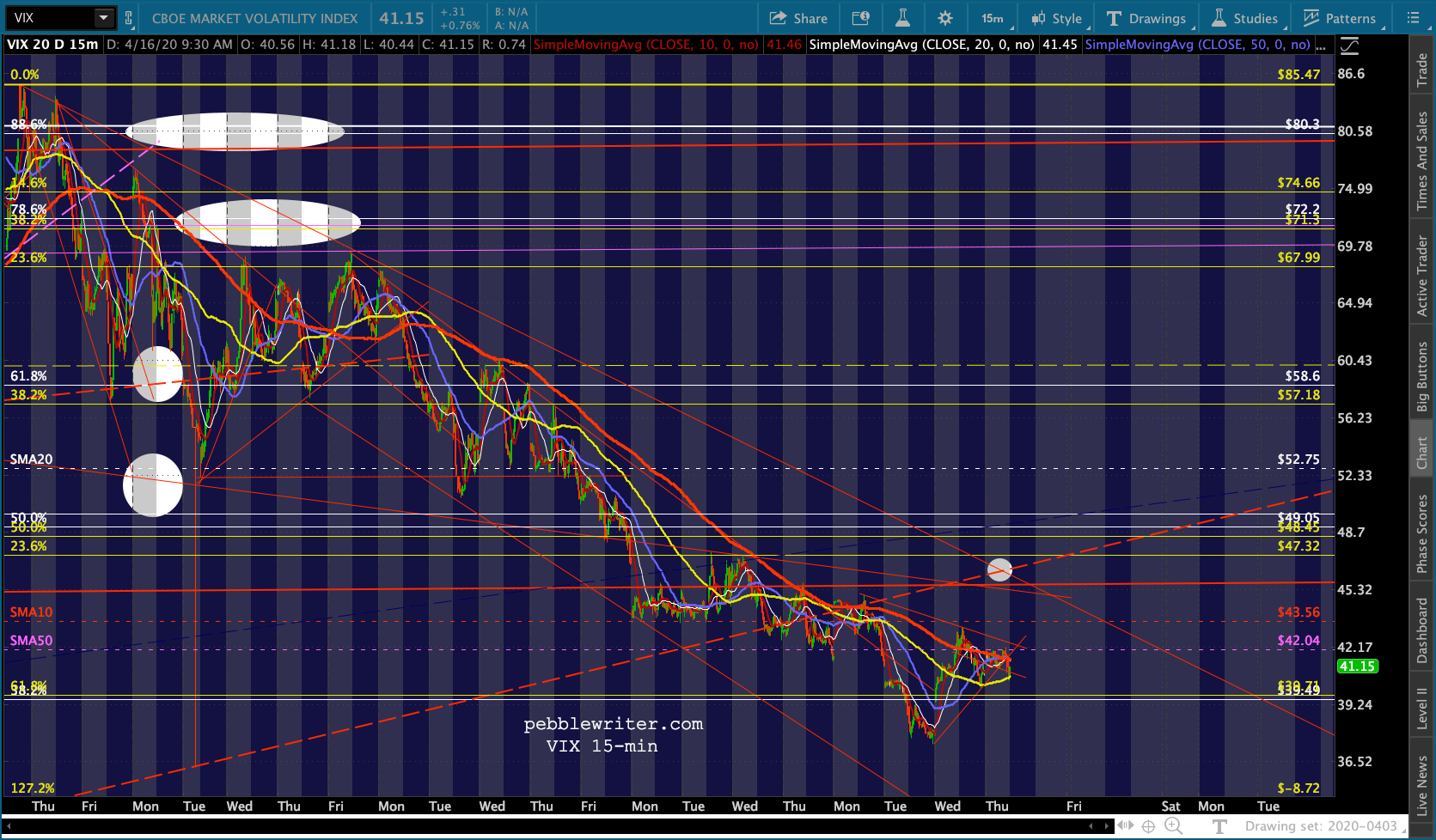

I’m still looking for VIX to backtest the SMA10 or the marked intersection.

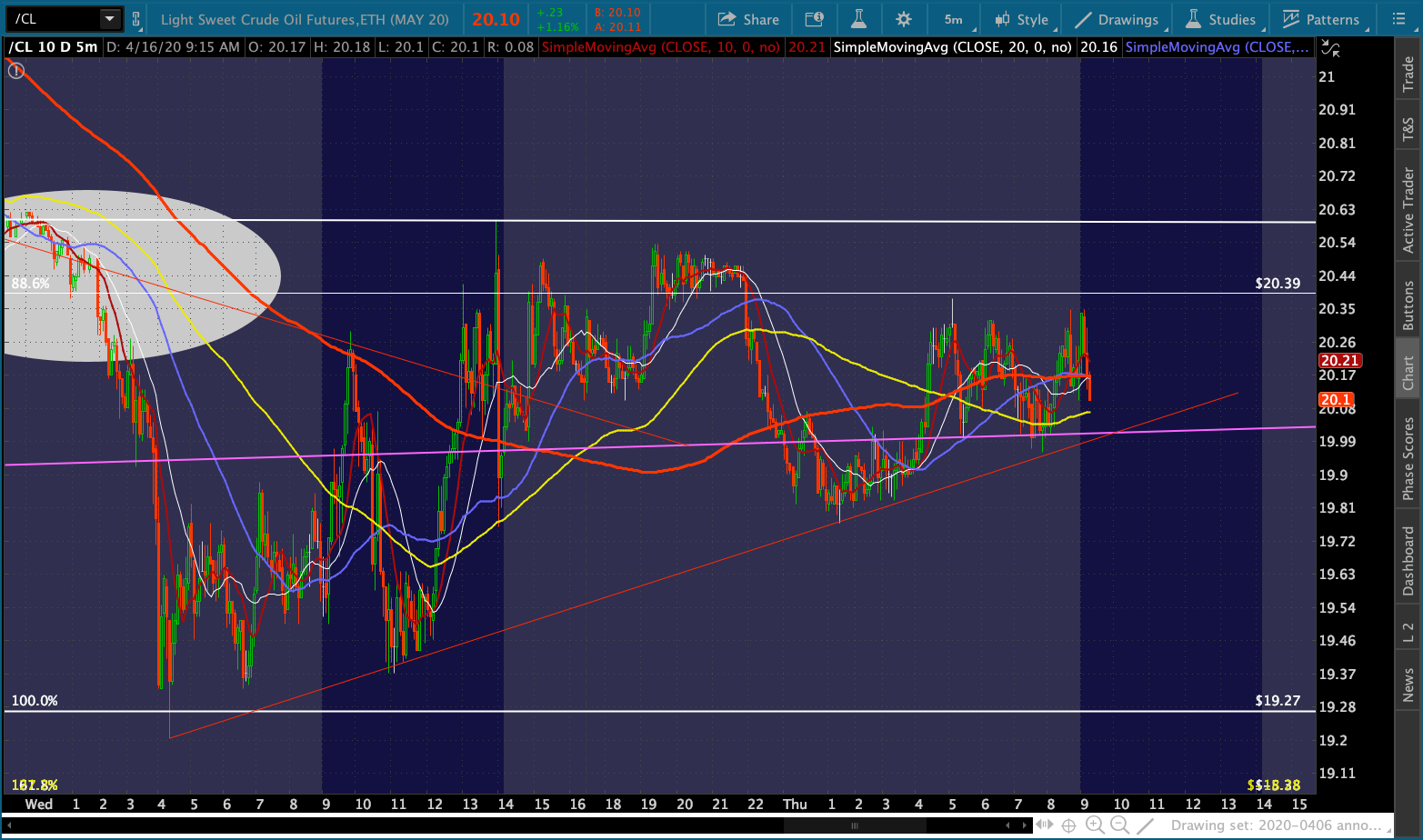

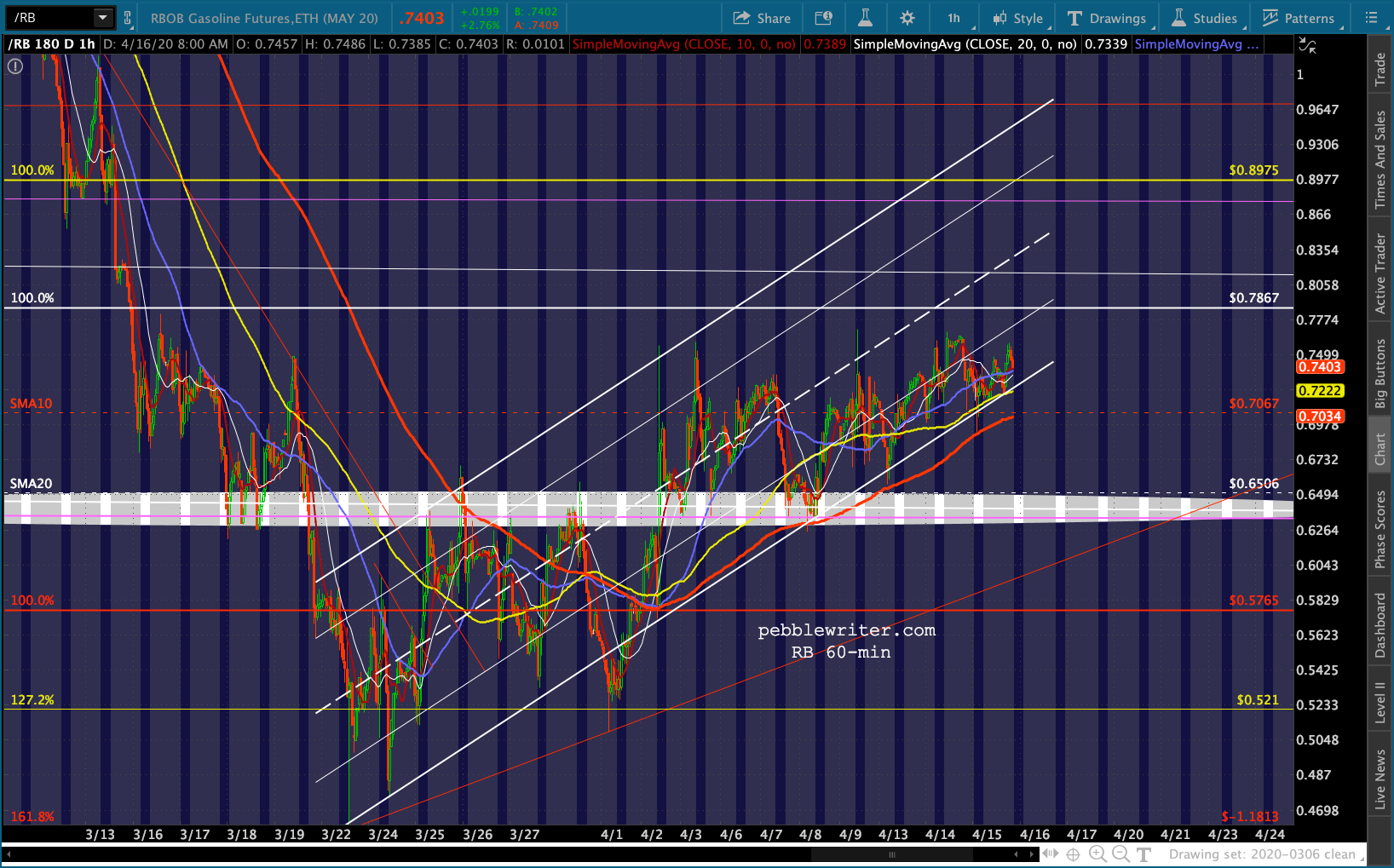

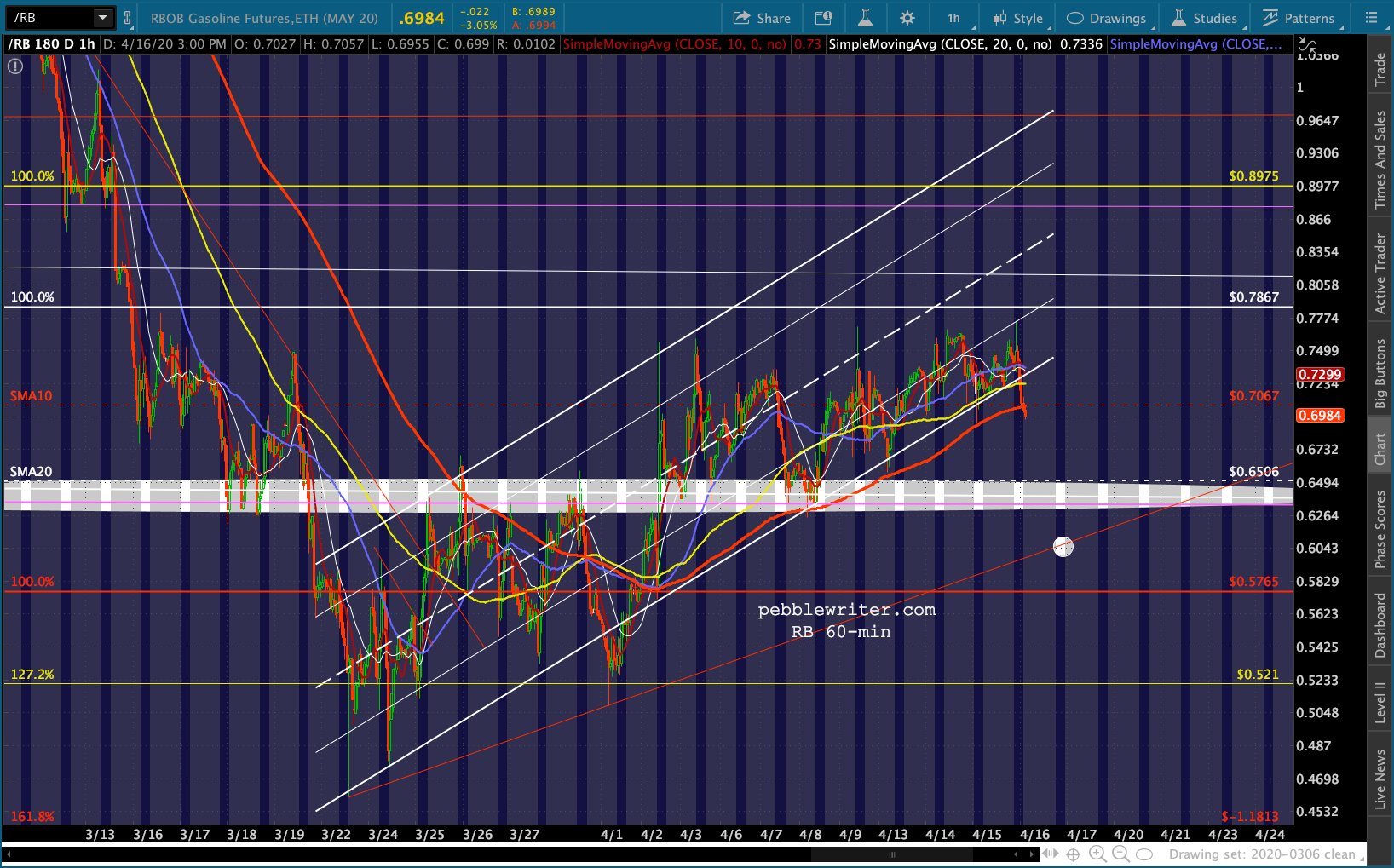

I’m still looking for VIX to backtest the SMA10 or the marked intersection. CL and RB have managed to string together a series of bounces, satisfying the algos that they’re on the mend. But, it’s still not very reassuring.

CL and RB have managed to string together a series of bounces, satisfying the algos that they’re on the mend. But, it’s still not very reassuring.

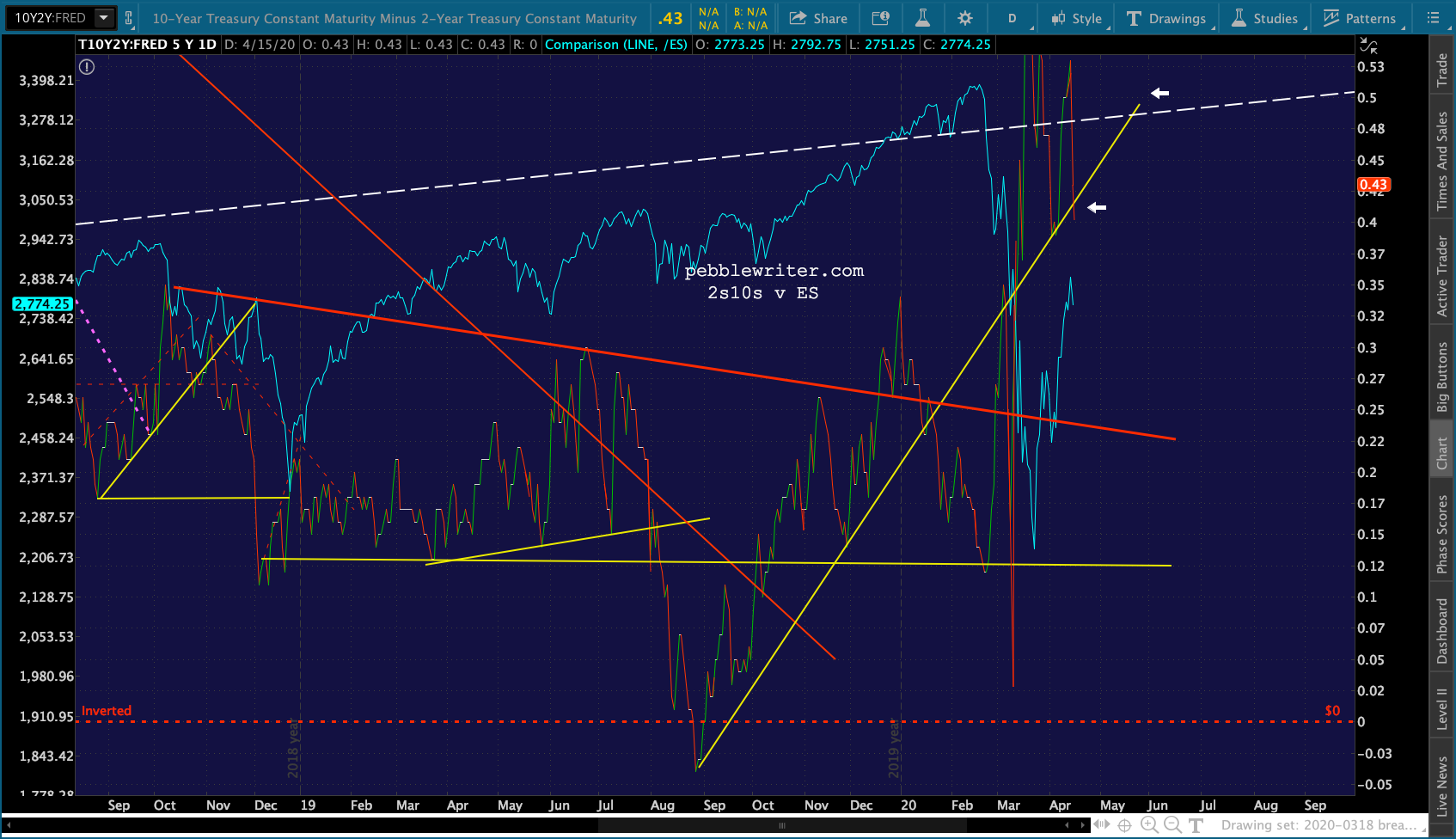

The 2s10s is looking bearish…at least for the moment, dipping below the red TL…

The 2s10s is looking bearish…at least for the moment, dipping below the red TL…

…on a decline in 10Y yields…

…on a decline in 10Y yields… …and a higher low on the 2Y.

…and a higher low on the 2Y.

Note that ZN has pushed above its 1.272 again…

Note that ZN has pushed above its 1.272 again… …as TNX continues to threaten a breakdown.

…as TNX continues to threaten a breakdown. The USDJPY is actually breaking down slightly – hardly supportive of stocks.

The USDJPY is actually breaking down slightly – hardly supportive of stocks.

UPDATE: 3:30 PM

UPDATE: 3:30 PM

Markets spent the entire day trying to decide whether or not to break down or out.

For the past hour, CL and RB seemed intent on driving stocks lower…

For the past hour, CL and RB seemed intent on driving stocks lower…

…but USDJPY and VIX weren’t interested.

…but USDJPY and VIX weren’t interested.

Thus, we’re right where we started – a 15-pt gain that offers little insight as to what happens next.

Thus, we’re right where we started – a 15-pt gain that offers little insight as to what happens next.

We’ll get the Conference Board Leading Economic Indicators at 10AM tomorrow. They’ll be the first to reflect March and the impact of the coronavirus, but it’s hard to imagine they’ll be any more negative than this morning’s data.

Trump is supposedly going to announce his plans to reopen the country and a $2 trillion infrastructure plan at 6PM this evening. While some states might be thrilled, I don’t imagine it will go over well with at least half the country.

Stay tuned.