Once again, the FOMC will have the opportunity to demonstrate their priorities. Will they cut rates again, ostensibly in an effort to stave off a recession? Or will they keep their powder dry and risk a market meltdown?

Mohammed El Erian, in a wonderful moment of truthiness this morning on CNBC, argued that cutting rates is a bad idea. Referring to the ECB’s experience:

It is not only ineffective, it is actually harmful to the long-term stability of the economy. It is undermining the financial sector; it is undermining the provision of long-term protection services; it is allowing zombie firms to survive; and, it is contributing to resource misallocation. On top of that, we see an increase in the saving rate in Germany, because people are compensating for the low rates. I don’t understand why it is we’d want to follow the path of the ECB.

Of course, one person’s resource misallocation is another’s reasonably priced bull market. Like a insecure lover, the market desperately needs the Fed to continue showering it with compliments (the latest iteration of not-QE) lest it look in the mirror and discover the extra pounds and wrinkles which time has wrought.

Nothing has changed in our outlook from Monday. Unless the Fed manages a dovish surprise, which is highly unlikely, yesterday’s highs should stand for quite a while… … and volatility should spike much higher in the days ahead.

… and volatility should spike much higher in the days ahead. continued for members…We’ll want to see VIX pop through the cluster of moving averages, particularly the SMA200 at 15.6.

continued for members…We’ll want to see VIX pop through the cluster of moving averages, particularly the SMA200 at 15.6.

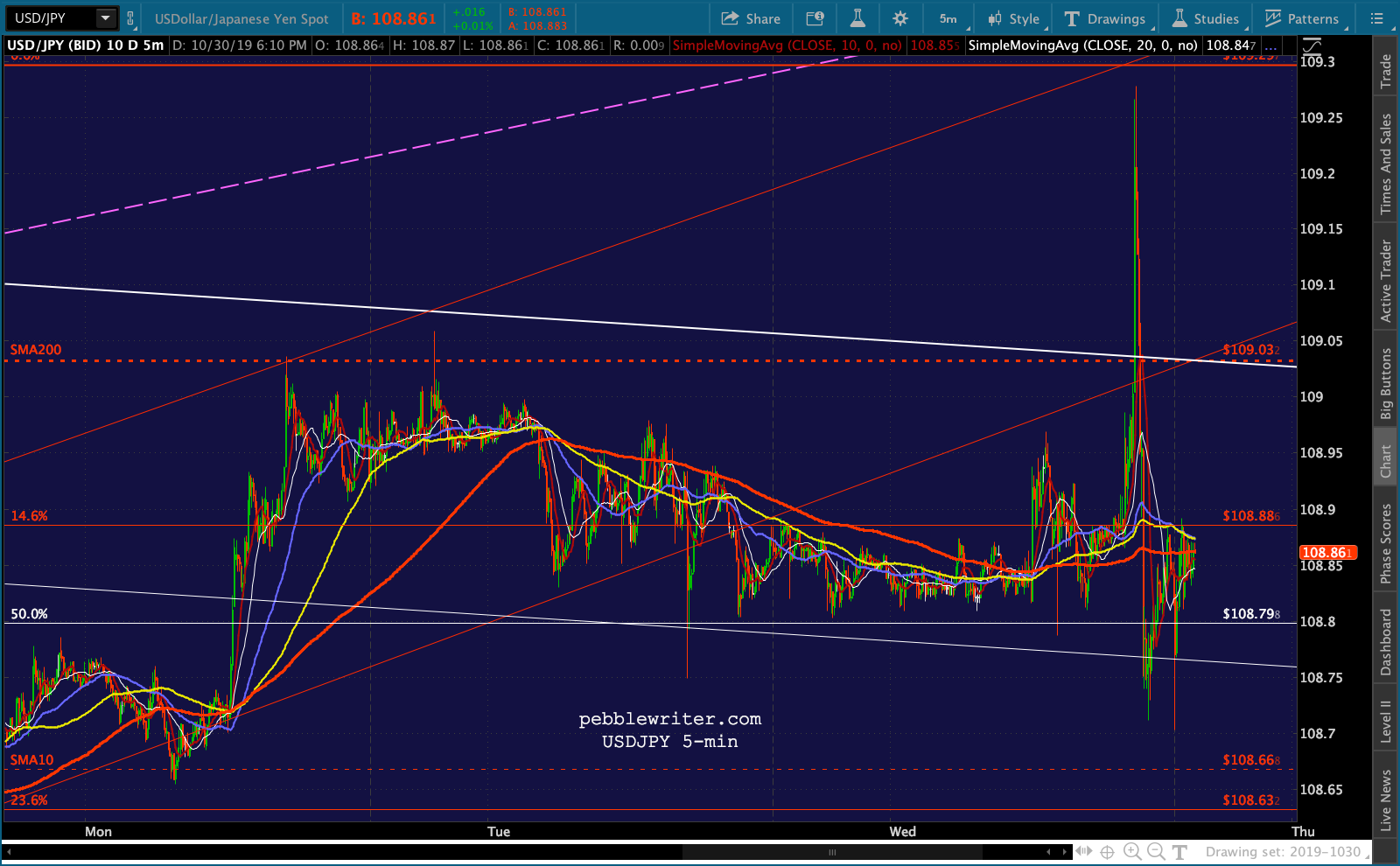

We’ll also want to see USDJPY ‘s latest breakout fall back to Earth.

We’ll also want to see USDJPY ‘s latest breakout fall back to Earth.  I always get nervous this time after year since the BoJ completely changed the market’s trajectory on Oct 31, 2014 — essentially extending the bull market another 7 months. SPX had just completed a Bat Pattern, reversing off the .886 Fib at 1996.

I always get nervous this time after year since the BoJ completely changed the market’s trajectory on Oct 31, 2014 — essentially extending the bull market another 7 months. SPX had just completed a Bat Pattern, reversing off the .886 Fib at 1996.

Two weeks earlier, SPX had backtested the 1.272 at 1823 thanks to Bullard’s on-air suggestion that QE3 would be a great idea. Had USDJPY reversed at the top of its long term channel, SPX would have tested the 1.272 again and failed. Plain and simple, it was a breakout which was enabled and then protected by coordinated central banker manipulation.

Plain and simple, it was a breakout which was enabled and then protected by coordinated central banker manipulation.

These are the chart patterns from back then. The case for a reversal off the top of the falling red channel was pretty strong. Instead, it broke out and sailed up past the white .886 and red .618 as CL cratered in order to accommodate what would otherwise have been an incredible rise in oil and gas prices in Japan — already reeling from the shutdown of nukes in the wake of Fukushima.

Instead, it broke out and sailed up past the white .886 and red .618 as CL cratered in order to accommodate what would otherwise have been an incredible rise in oil and gas prices in Japan — already reeling from the shutdown of nukes in the wake of Fukushima. More charts and discussion can be found in the Oct 31, 2014 post: Trick or Treat?

More charts and discussion can be found in the Oct 31, 2014 post: Trick or Treat?

I mention this because USDJPY has broken out somewhat, and the BoJ is very much a cornered, injured animal caught in an equity trap of its own making. If they pulled a similar move out of desperation, forget about a big decline for US equities.

Plus, we’ve seen five distinct instances of SPX failing to even tag its SMA200 since Aug 5, when the SMA200 was 100 points lower. The manipulators have been busy.

And, we’ll want to see CL at least test 50.52 again and, potentially, push lower to test the channel bottom or a lower Fib such as the .886 at 45.12. RB is on its own path, which is driven largely by inflation goal-setting.

RB is on its own path, which is driven largely by inflation goal-setting. And, we would want to see the 10Y fall, but be far outpaced by a tumbling 2Y — a flight to safety as stocks tumble rather than a response to the inflation picture.

And, we would want to see the 10Y fall, but be far outpaced by a tumbling 2Y — a flight to safety as stocks tumble rather than a response to the inflation picture.

ES and SPX have many potential downside targets should they start tumbling. Some of the more interesting ones are shown below.

ES and SPX have many potential downside targets should they start tumbling. Some of the more interesting ones are shown below.

Most of the recent FOMC meetings have signaled at least interim tops, with the downturn beginning the day of the announcement.

Most of the recent FOMC meetings have signaled at least interim tops, with the downturn beginning the day of the announcement.

And, though we don’t talk about it often, the Dow has failed to confirm SPX’s new highs and is bumping up against the top of a consolidating triangle. It continues to look particularly weak.

And, though we don’t talk about it often, the Dow has failed to confirm SPX’s new highs and is bumping up against the top of a consolidating triangle. It continues to look particularly weak. More later.

More later.

UPDATE: 2:15 PM

The FOMC voted for a 25 bps cut and hinted at holding at that level through the end of the year. Still 2 dissenters but Bullard not arguing for a larger cut this time – a slightly hawkish development.

So far, stocks have been bid with VIX slipping lower and CL and USDJPY bumping just high enough to keep stocks from slipping lower — a defensive posture IMO.

The 2 year initially popped a little higher, but is backing off. My biggest concerns are USDJPY popping above its SMA200 — only slightly overhead…

The 2 year initially popped a little higher, but is backing off. My biggest concerns are USDJPY popping above its SMA200 — only slightly overhead…

…and, CL breaking out.

…and, CL breaking out. More after the press conference…

More after the press conference…

UPDATE: 6:00 PM

Despite there being no real surprises during the press conference, stocks rallied on an offhand comment that Powell didn’t anticipate any further rate hikes unless inflation moved much higher. Duh.

It moved the algos, along with a momentary spike in USDJPY above the SMA200 but not to new highs…

…a 6.6% drop in VIX, but not below the red TL…

…a 6.6% drop in VIX, but not below the red TL… …no net gains in CL or RB…

…no net gains in CL or RB…

…a brief pop in 10Y yields which was completely unwound by the close…

…a brief pop in 10Y yields which was completely unwound by the close…

…a very modest intraday new high in SPX…

…a very modest intraday new high in SPX… …which closed just below its 2.618 and put the white .500 retracement slightly closer to the 2.24 at 2703.

…which closed just below its 2.618 and put the white .500 retracement slightly closer to the 2.24 at 2703.

For its part, ES pushed up to 3055, slightly closer to its 2.618 at 3076.93.  If it were to rise to exactly 3061.25, its C=A target would rise to the purple .886 at 2807.58 — also a channel line. Is it is, the purple .618 and red .886 are now that much closer to the SMA200.

If it were to rise to exactly 3061.25, its C=A target would rise to the purple .886 at 2807.58 — also a channel line. Is it is, the purple .618 and red .886 are now that much closer to the SMA200. Bottom line, all the factors are still in a position to push stocks higher. But, as of today, they held back. Tomorrow’s another day. Remember, the BoJ announces its own policy updates tomorrow.

Bottom line, all the factors are still in a position to push stocks higher. But, as of today, they held back. Tomorrow’s another day. Remember, the BoJ announces its own policy updates tomorrow.

https://www.japantimes.co.jp/news/2019/10/30/business/boj-policy-meeting-inflation-easing/

GLTA.