Powell might insist that the word “stagflation” is never mentioned at FOMC meetings, but inflation and labor costs are still hot, and the latest GDP print is still hanging over us like a wet rag.

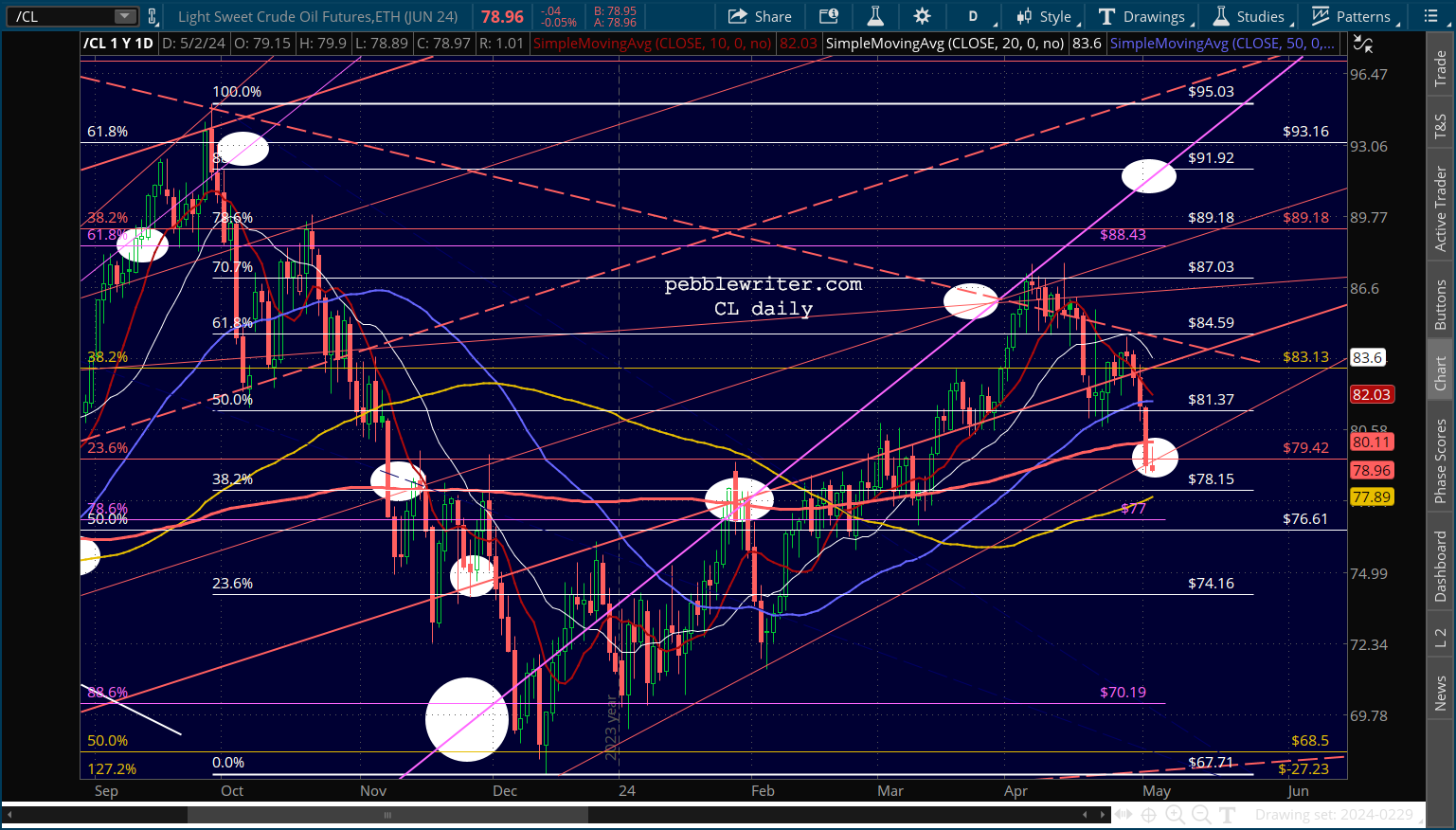

Nevertheless, the algos are content to take their cues from VIX and currencies which, at the moment at least, are ramping stocks higher. Perhaps more importantly, though, WTI has fallen through our 79.42 target which in the absence of a wider conflict in the Middle East creates a real opportunity for lower inflation.

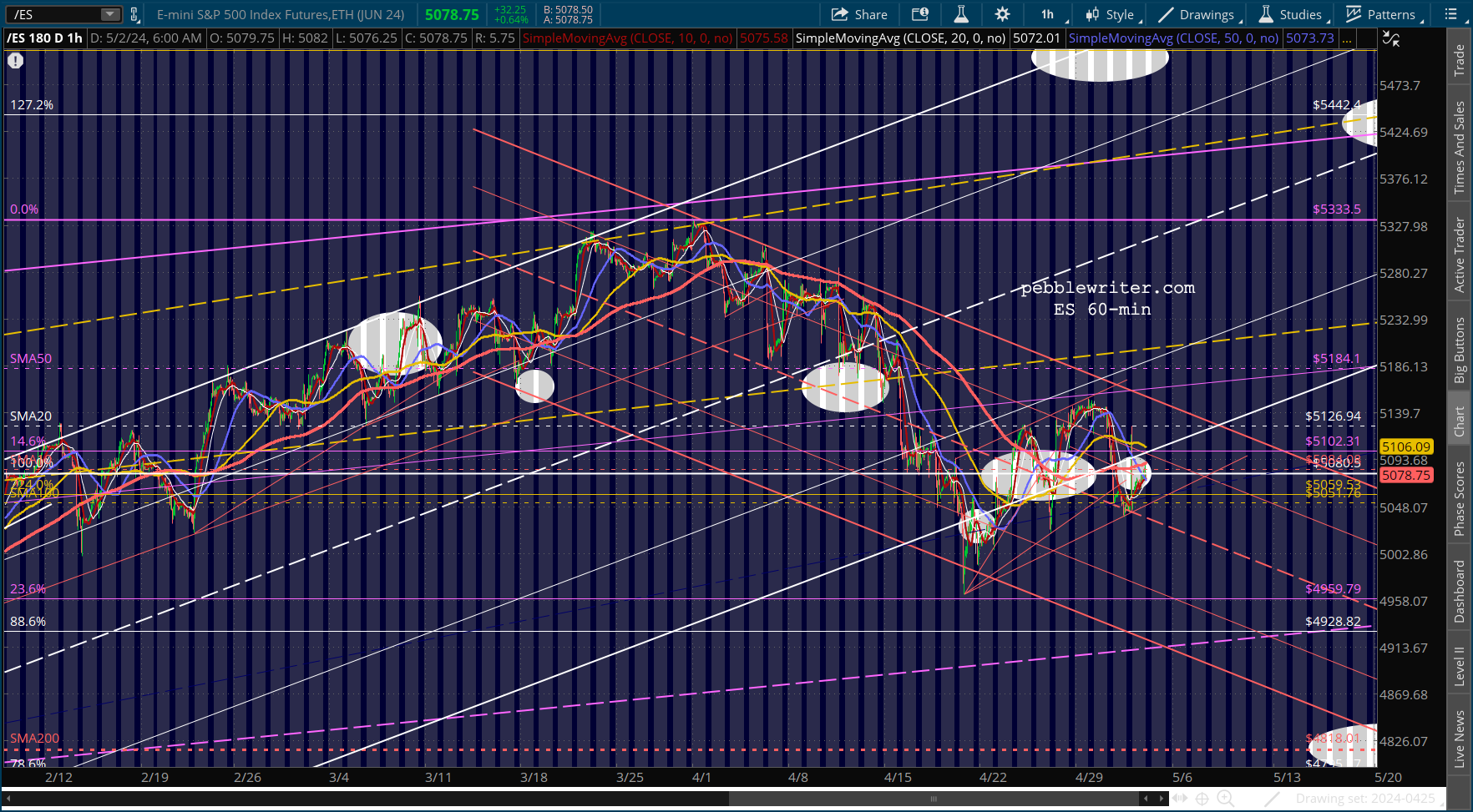

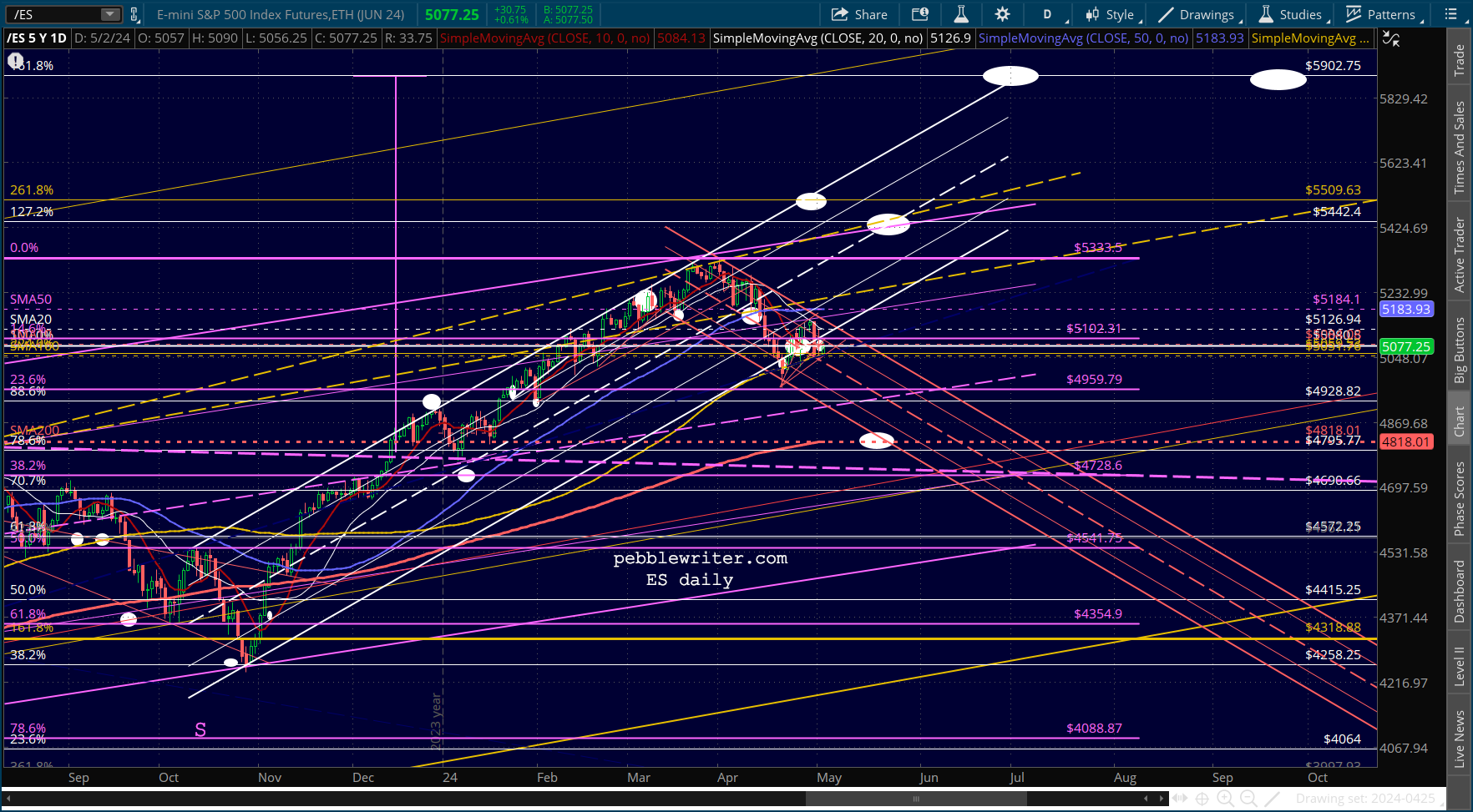

Perhaps more importantly, though, WTI has fallen through our 79.42 target which in the absence of a wider conflict in the Middle East creates a real opportunity for lower inflation. continued for members…The SPX and ES channels have still broken down and VIX is still hanging on above its SMA200. So, this morning’s rally feels more like a stall in advance of lower equity prices.

continued for members…The SPX and ES channels have still broken down and VIX is still hanging on above its SMA200. So, this morning’s rally feels more like a stall in advance of lower equity prices.

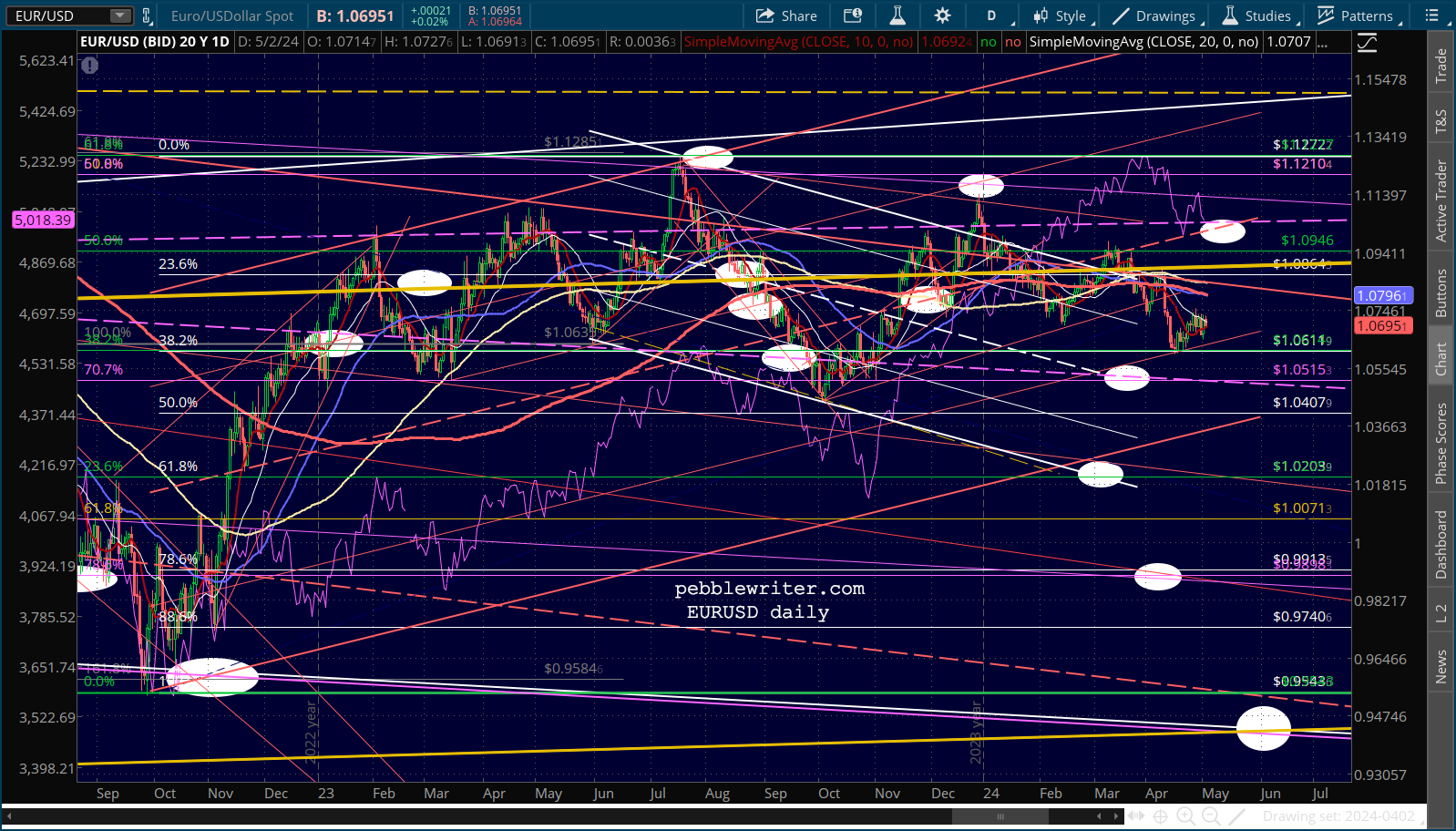

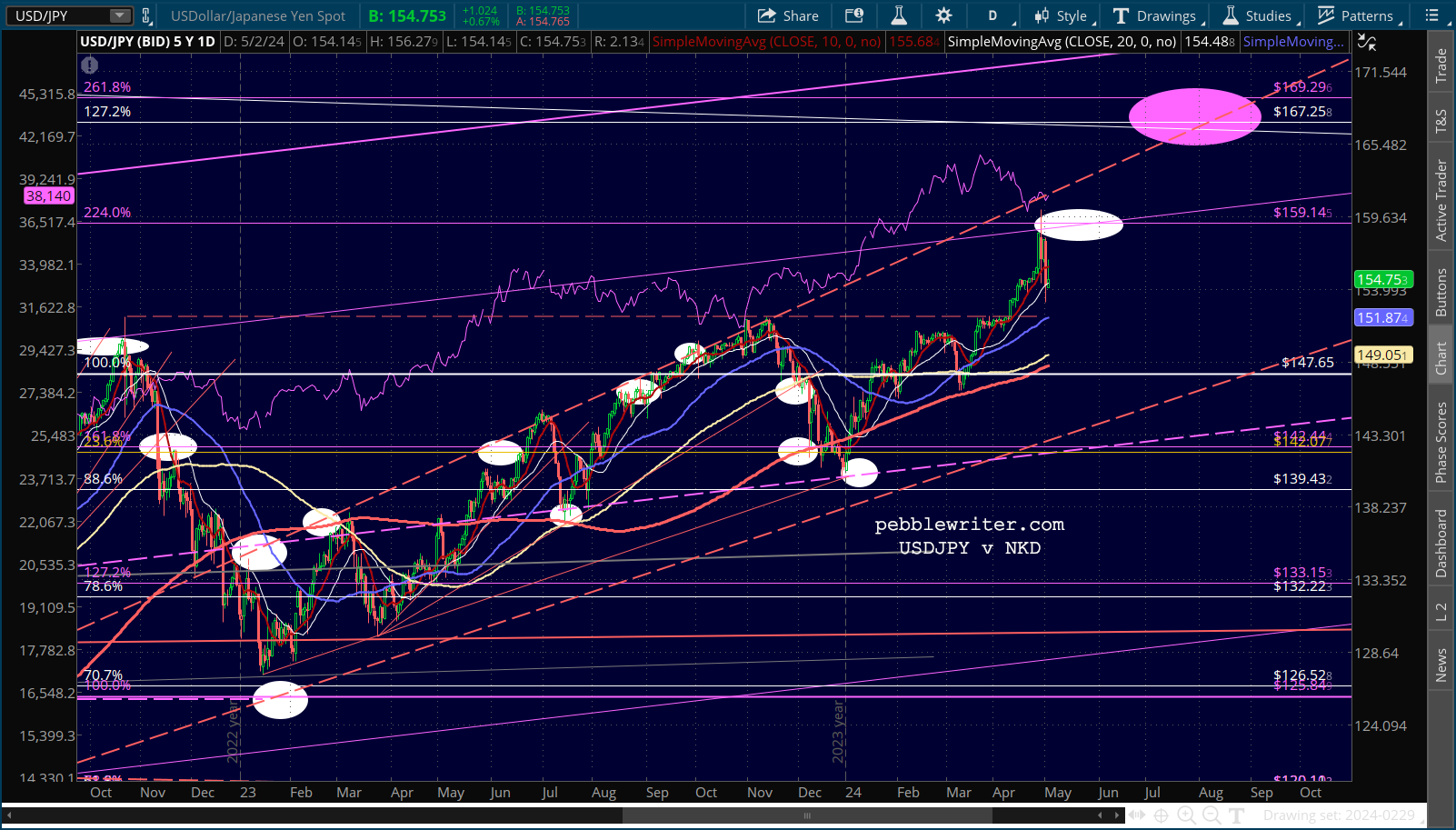

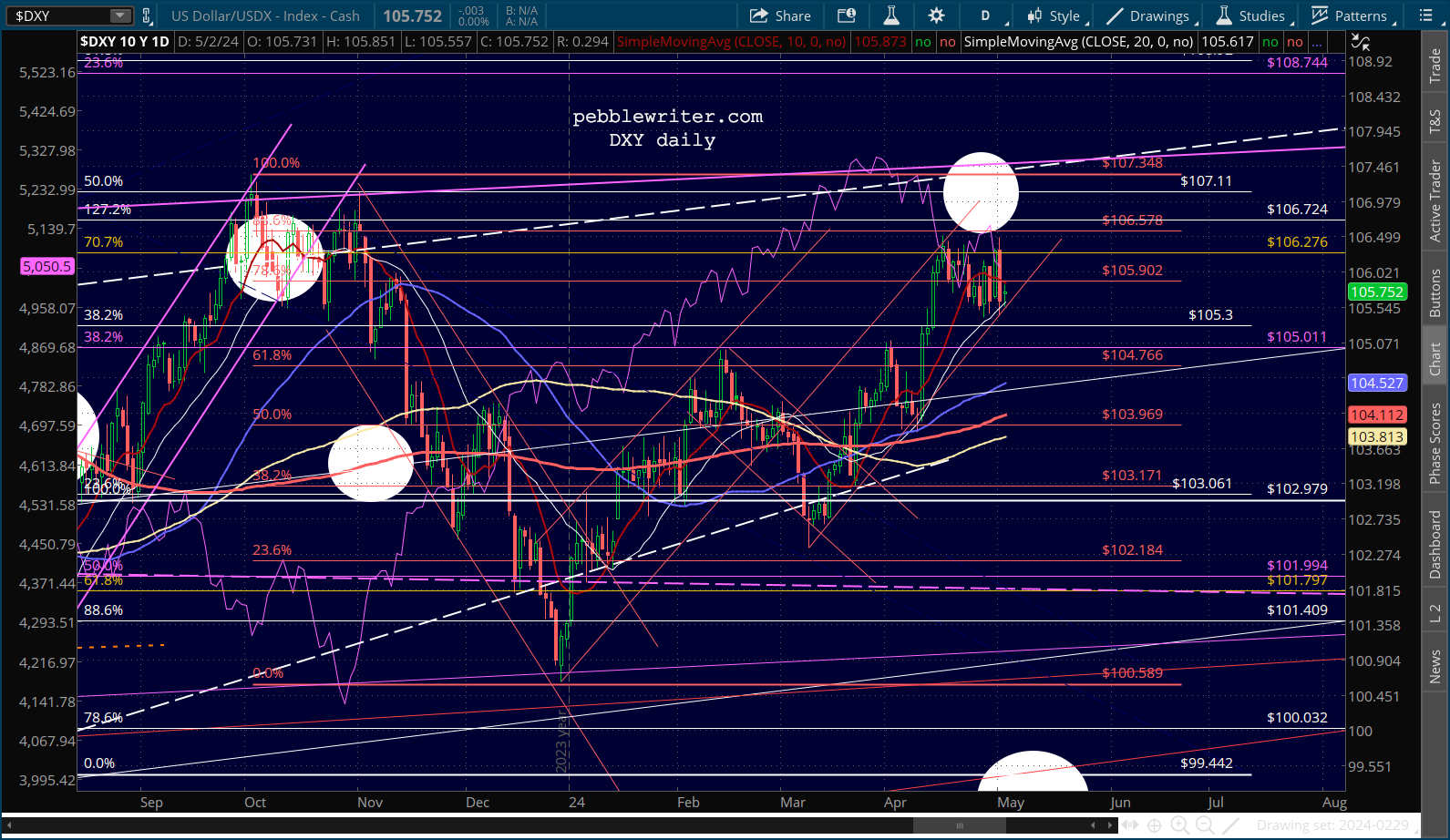

Currencies are still very quiet, which supports the notion of lower stock prices – especially if DXY rallies from here at its channel bottom.

Currencies are still very quiet, which supports the notion of lower stock prices – especially if DXY rallies from here at its channel bottom.

As mentioned above, it’s still oil/gas that have the potential to impact inflation in a meaningful way. If CL falls below the red TL from Dec 13, this could be a real game changer.

As mentioned above, it’s still oil/gas that have the potential to impact inflation in a meaningful way. If CL falls below the red TL from Dec 13, this could be a real game changer.

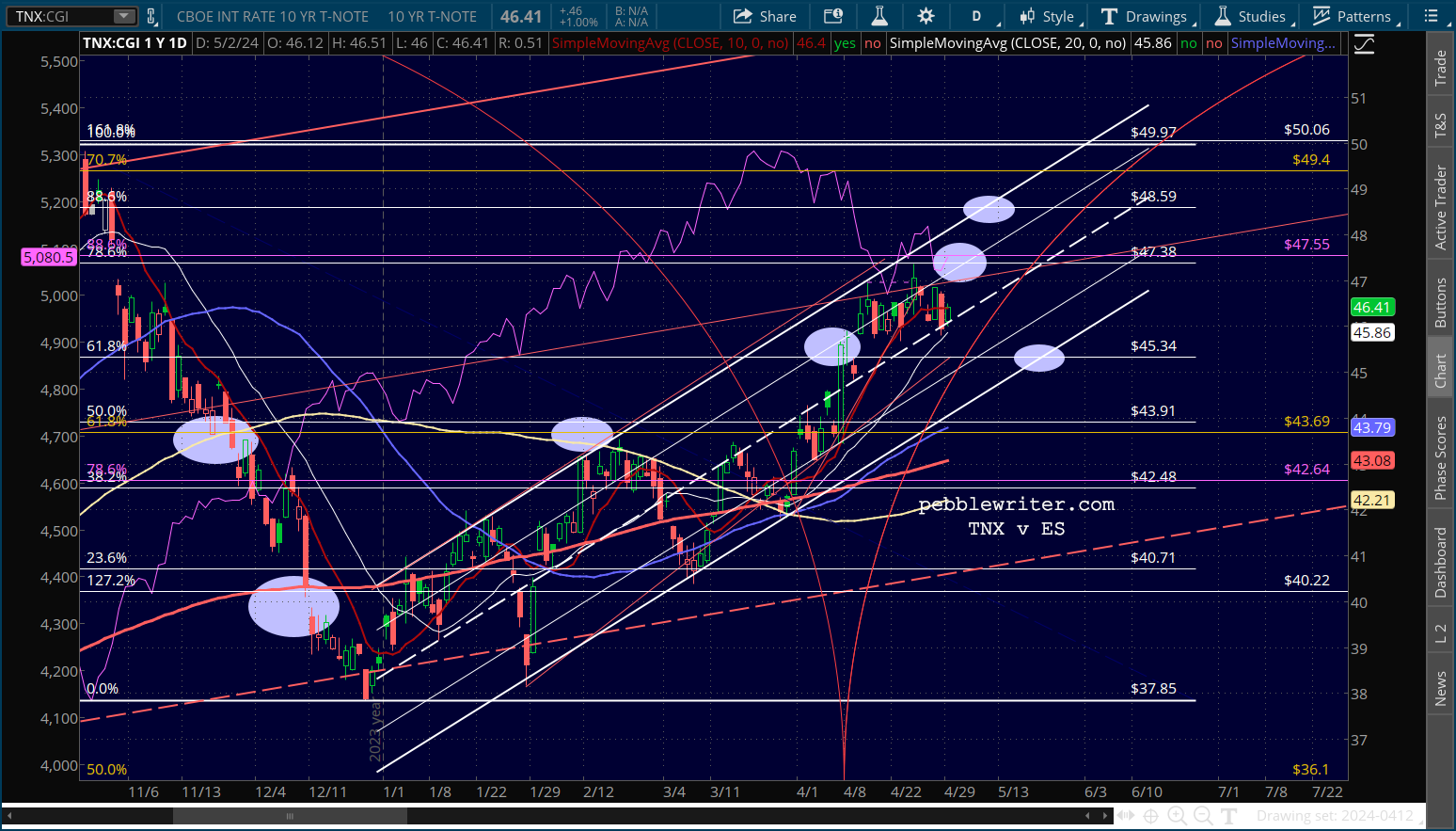

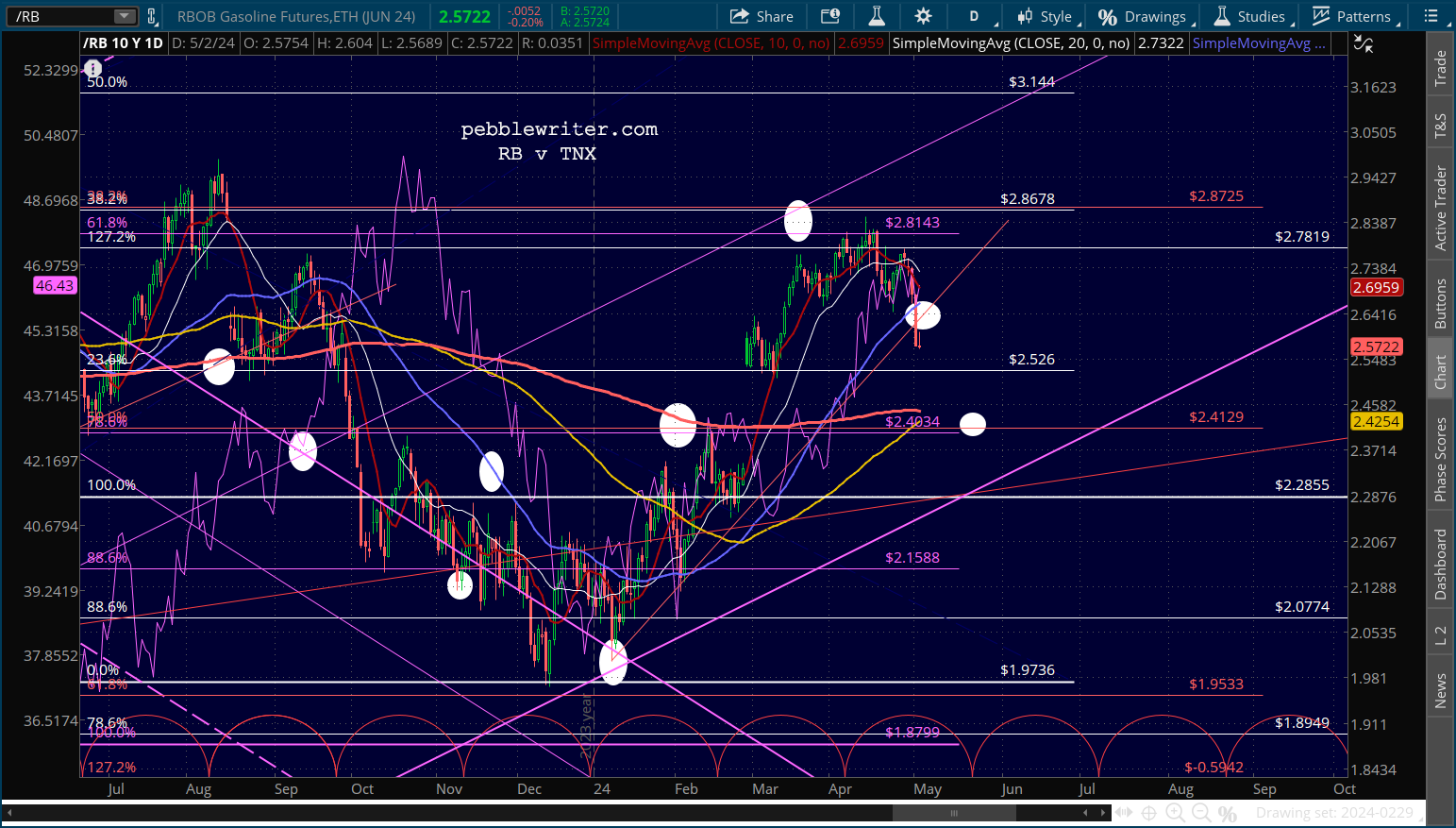

TNX has remained stable though elevated since mid-April. I prefer the 48.59 target around May 10 (next Friday) but if that doesn’t occur then we’re probably looking at a backtest of 45.34 around May 22.

TNX has remained stable though elevated since mid-April. I prefer the 48.59 target around May 10 (next Friday) but if that doesn’t occur then we’re probably looking at a backtest of 45.34 around May 22.