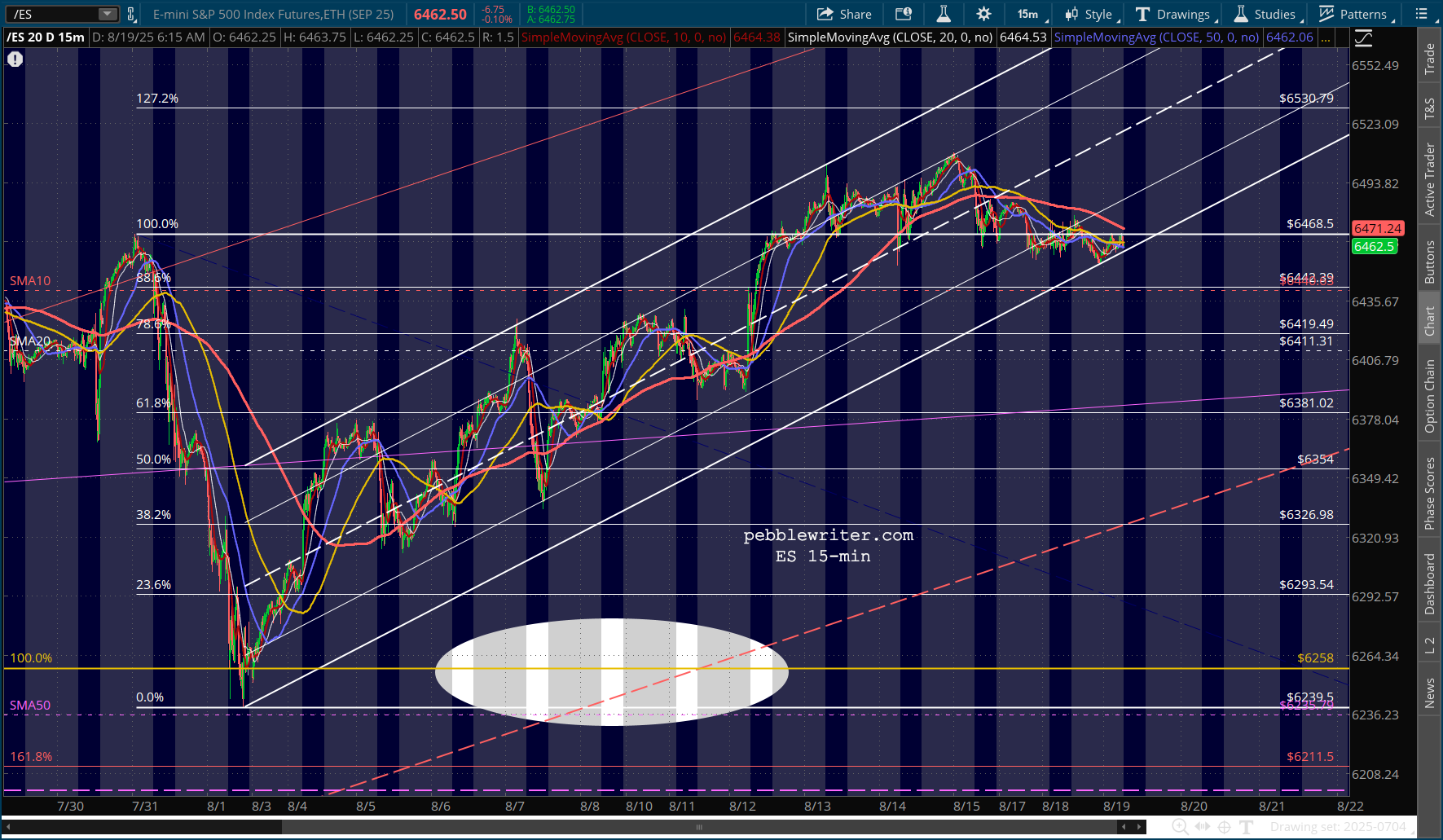

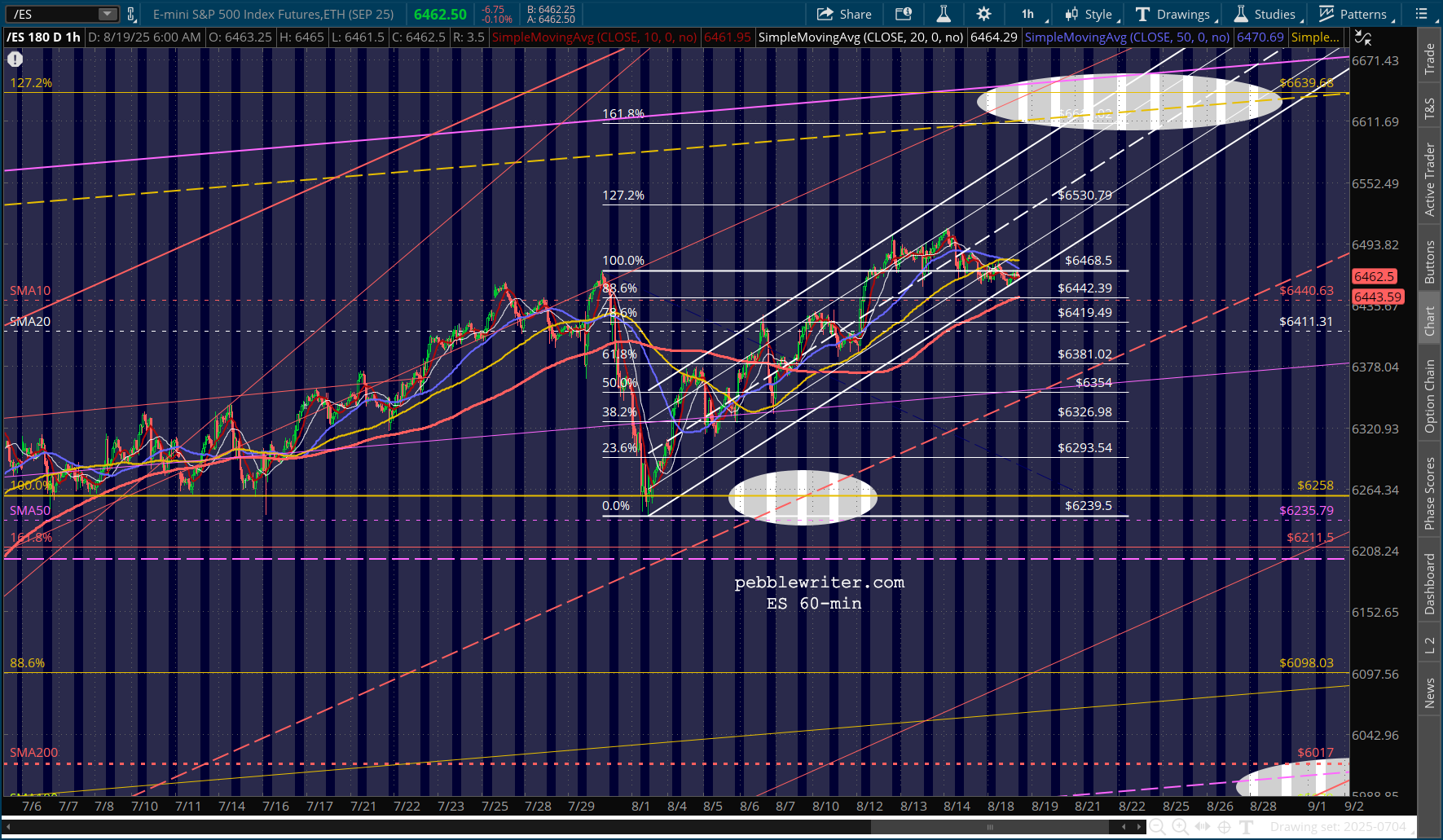

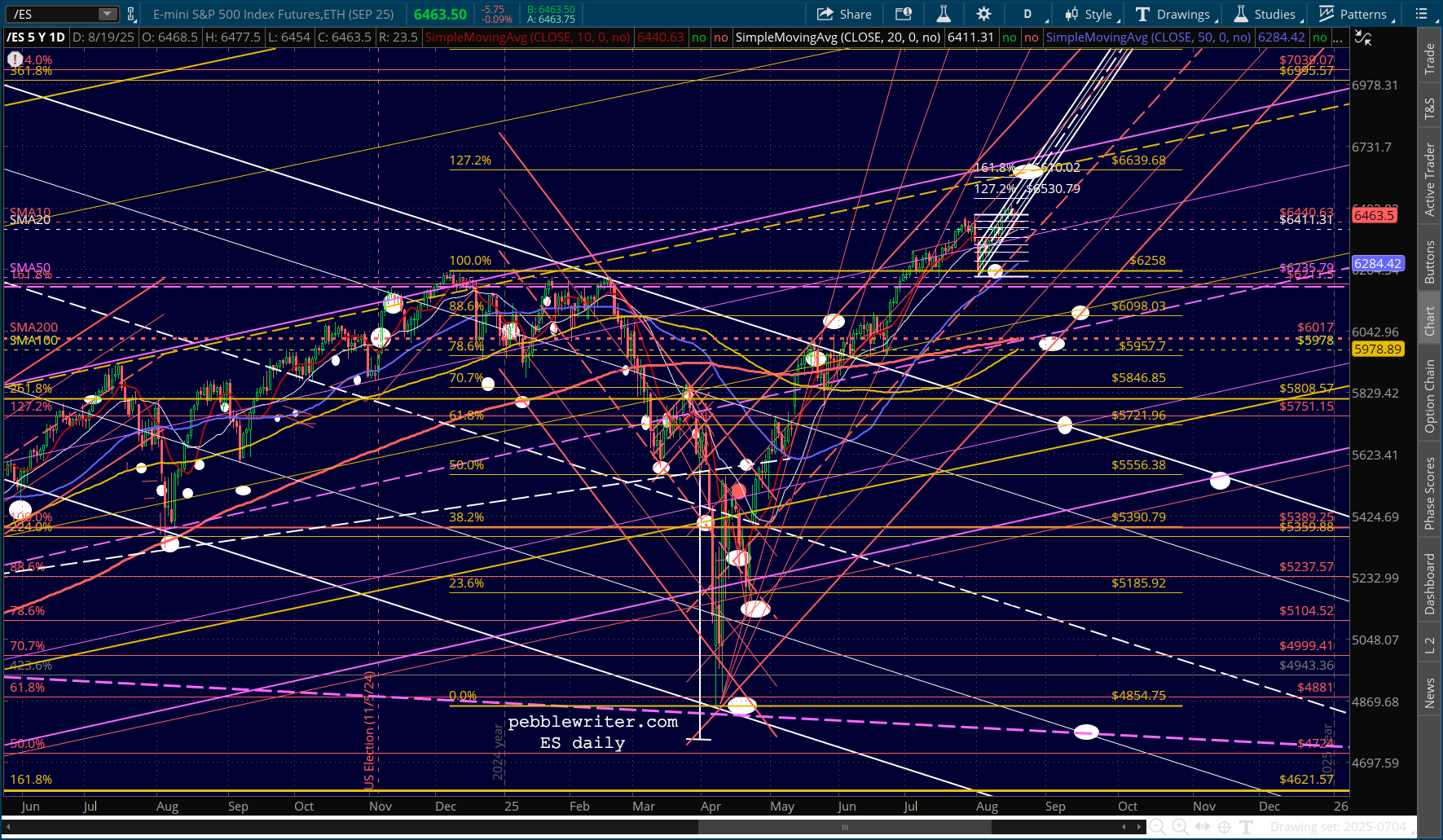

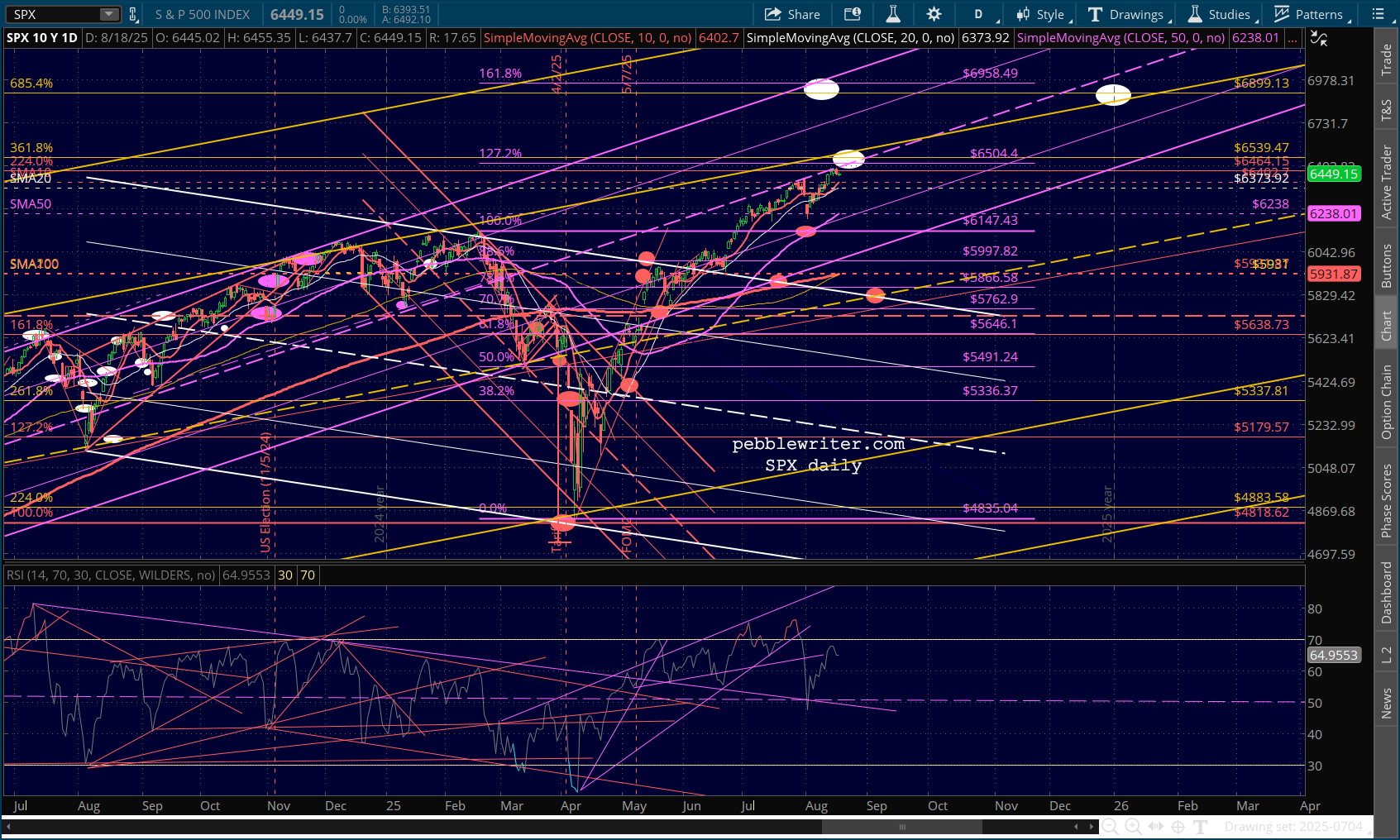

Futures are slightly lower as stocks continue consolidating.

continued for members…

continued for members…

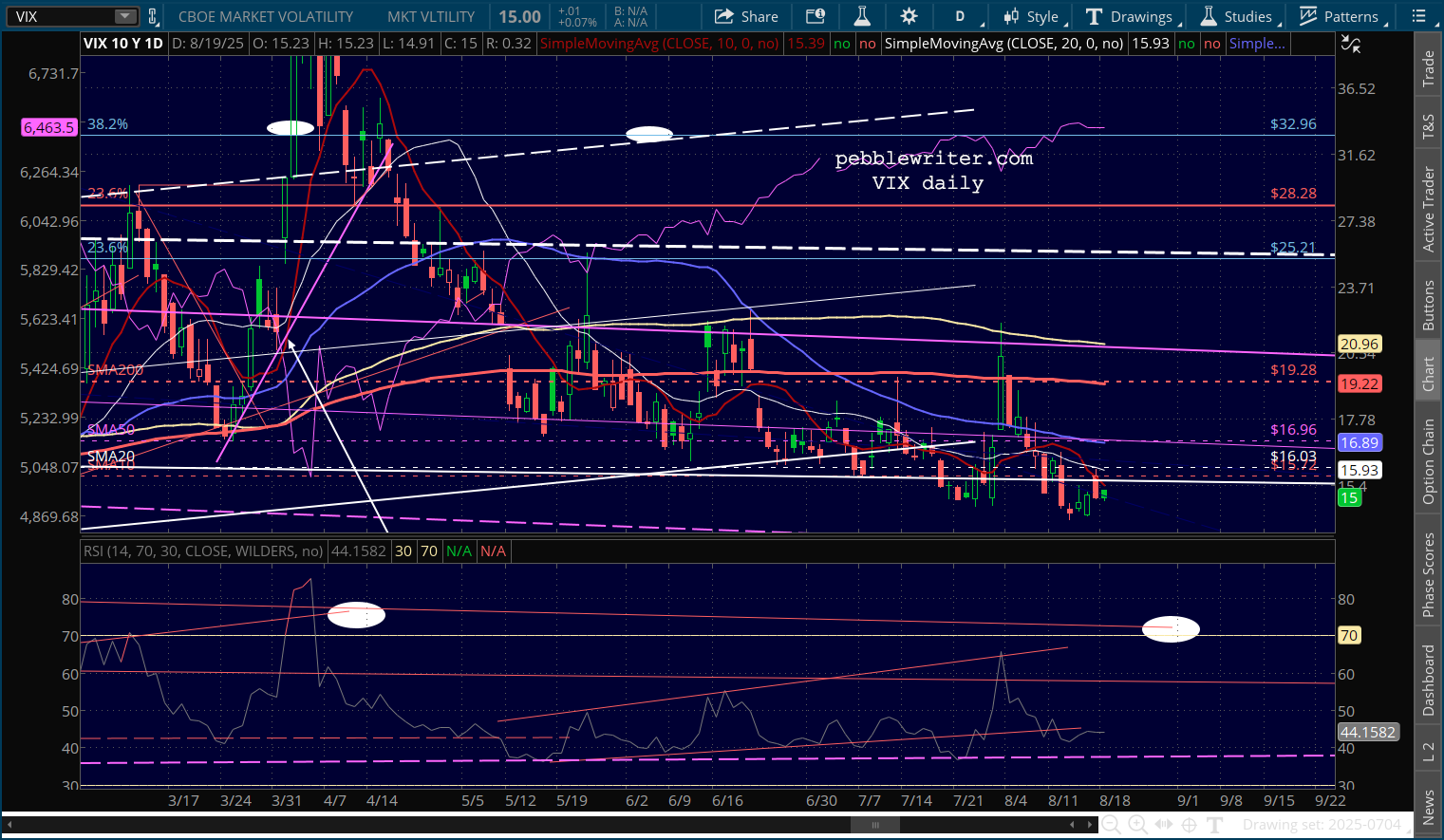

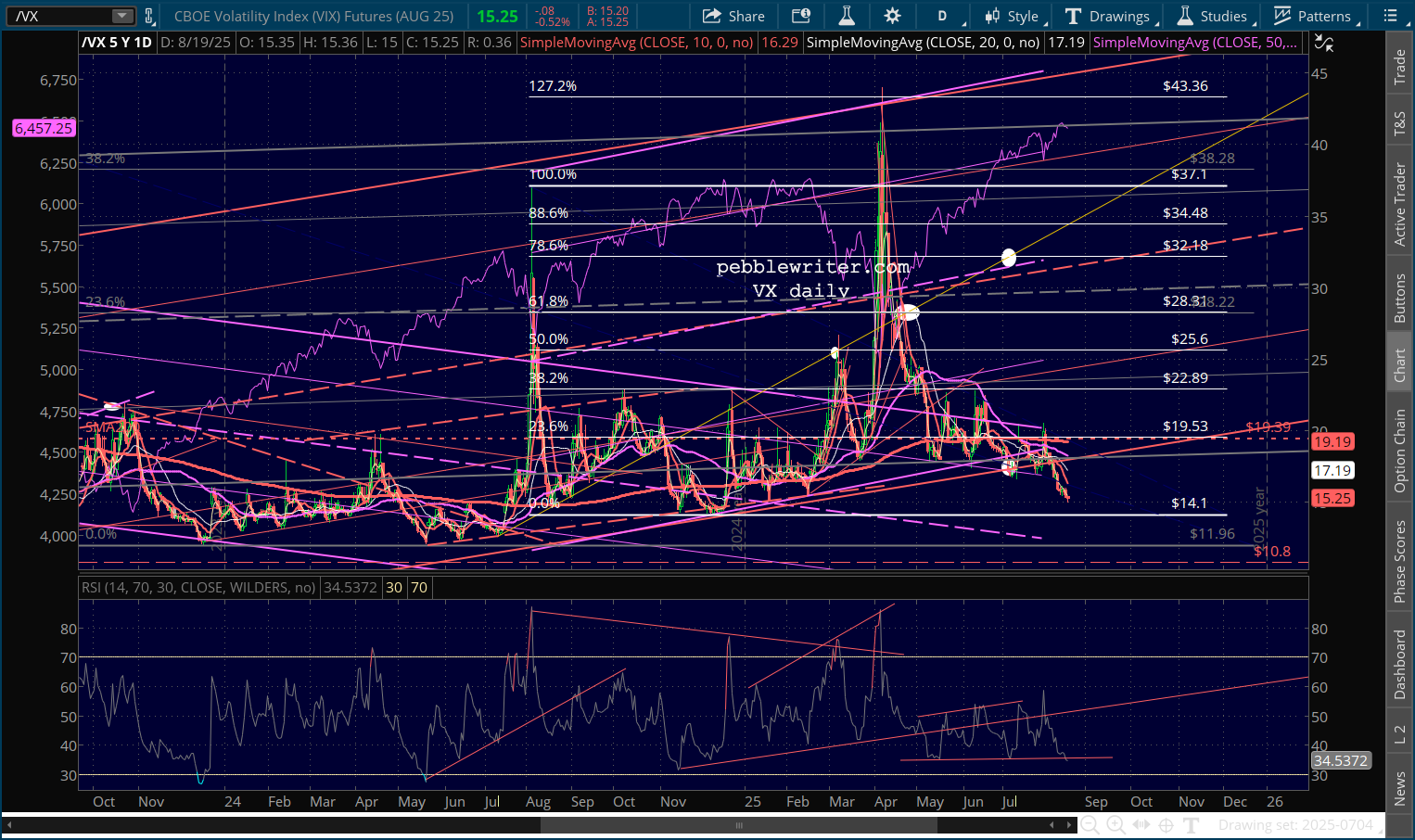

The market would probably be lower were it not for the continuing VIX/VX collapse.

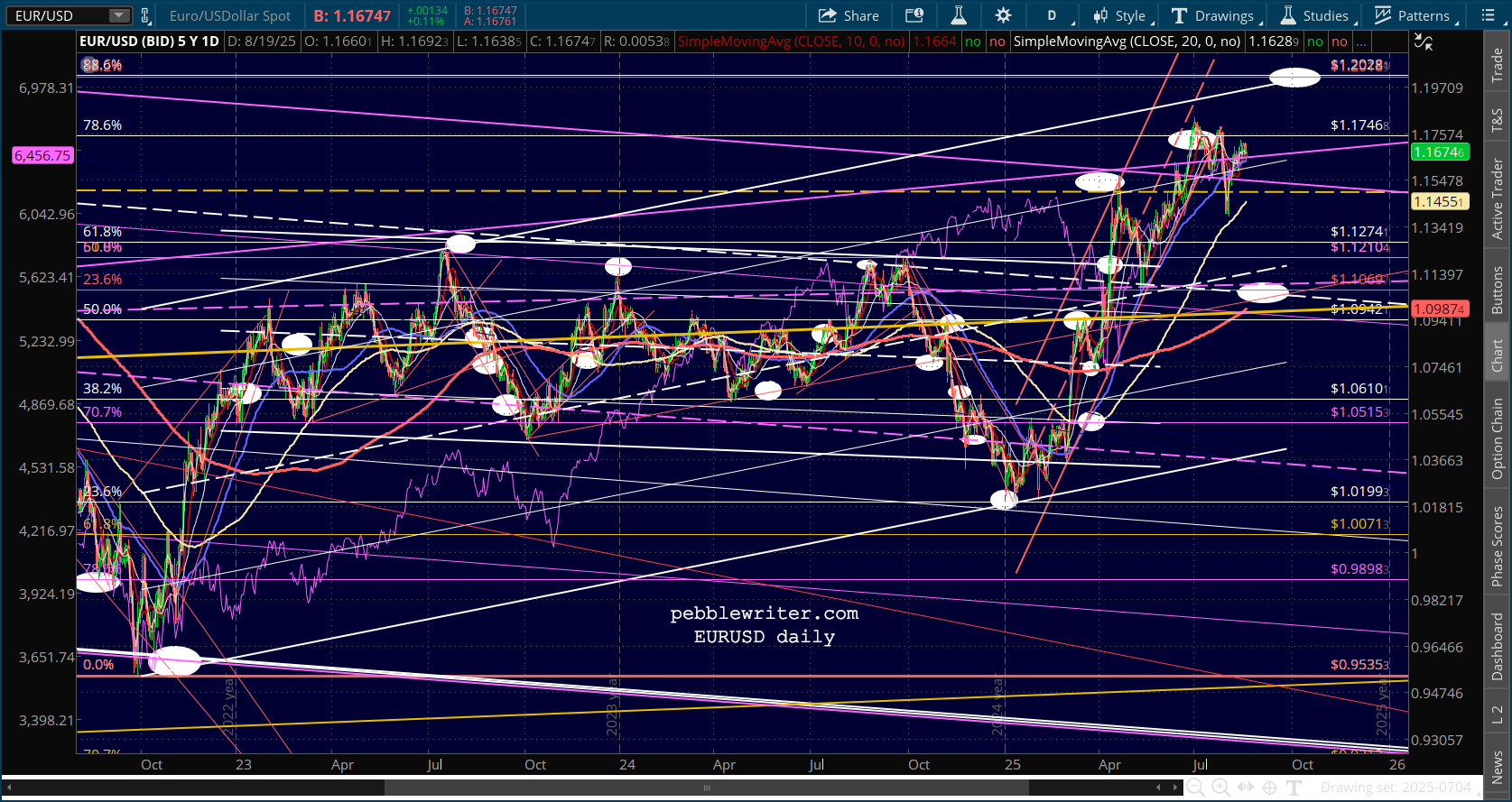

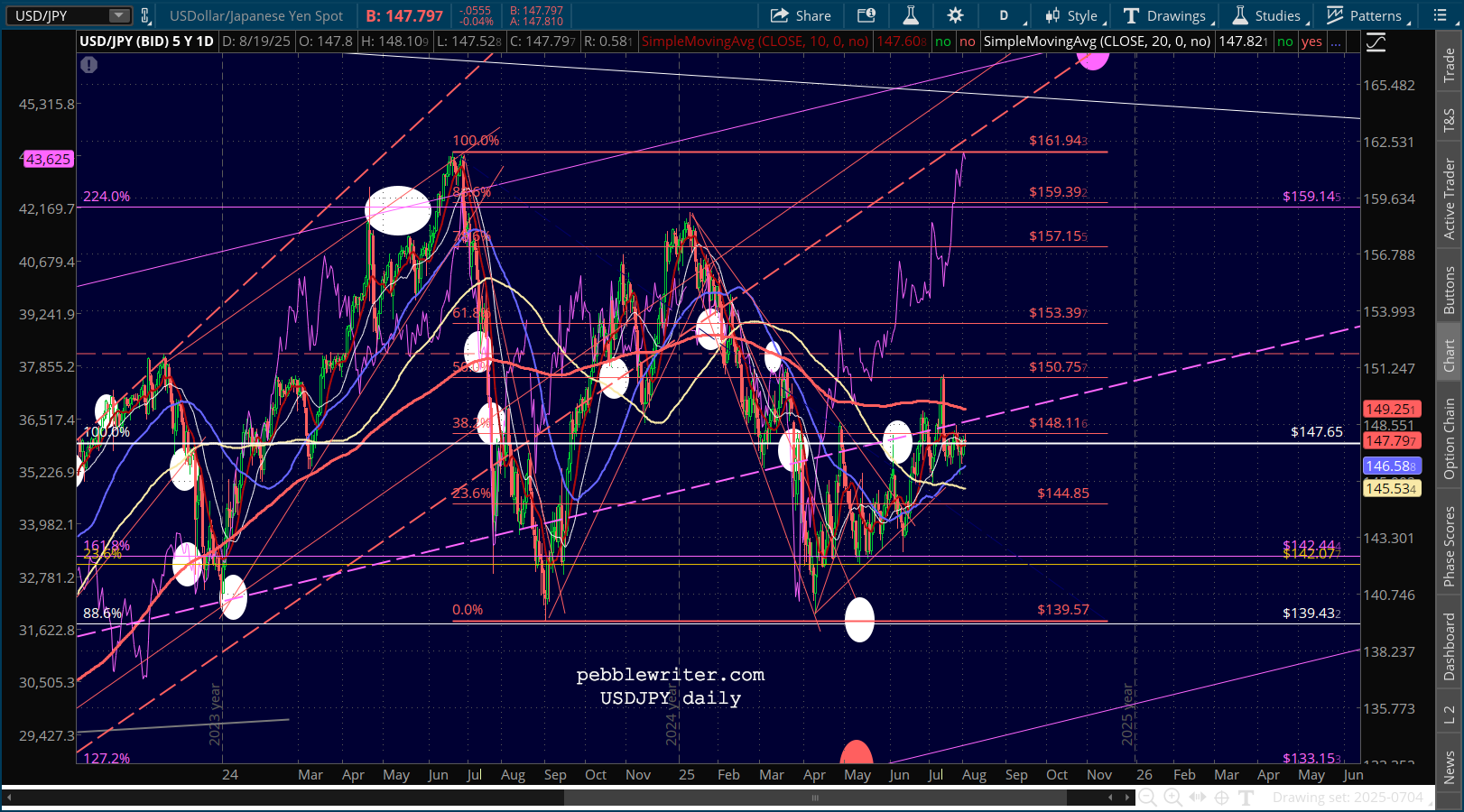

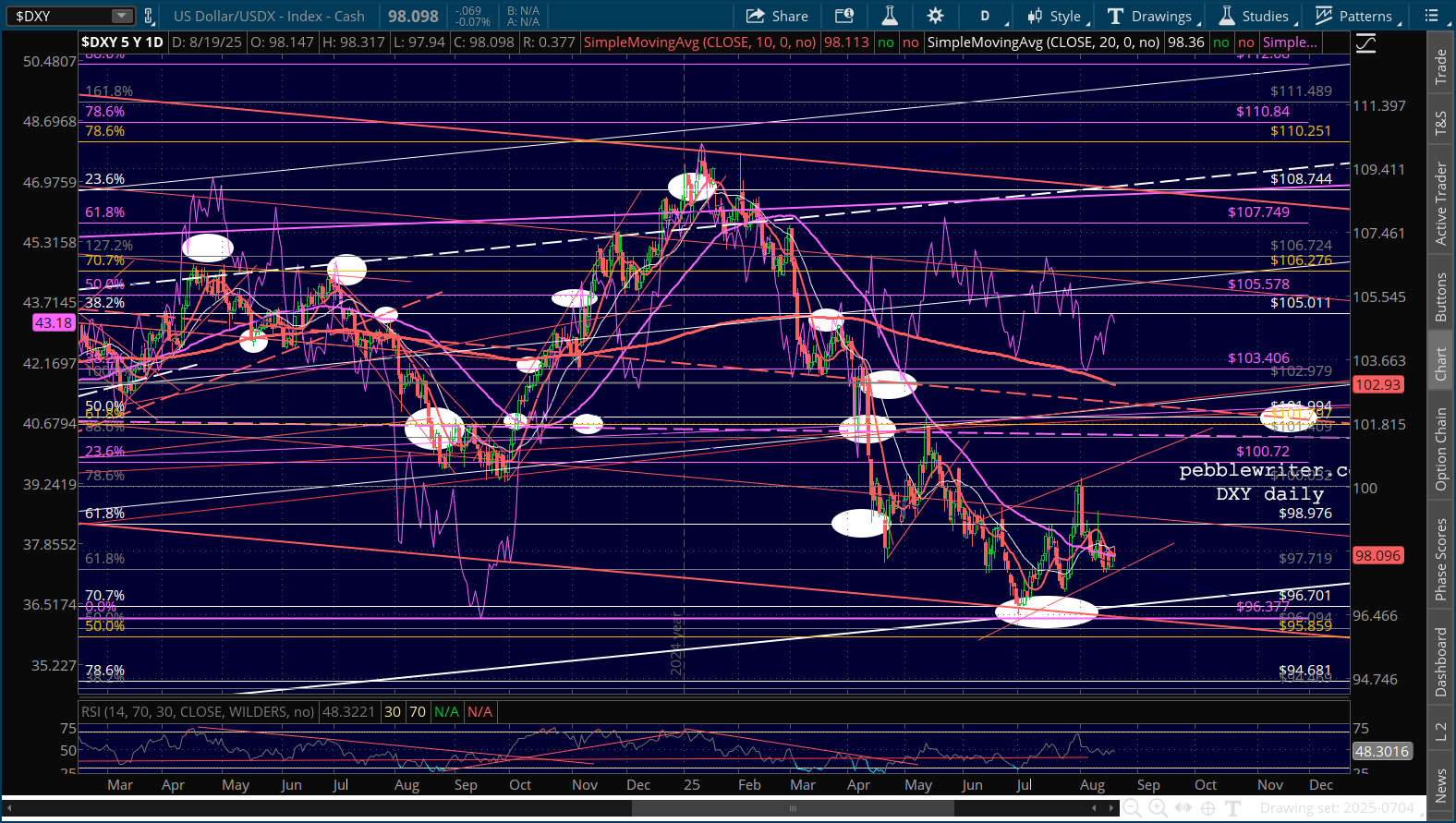

Currencies continue to be managed very closely, with minor moves that keep DXY in check.

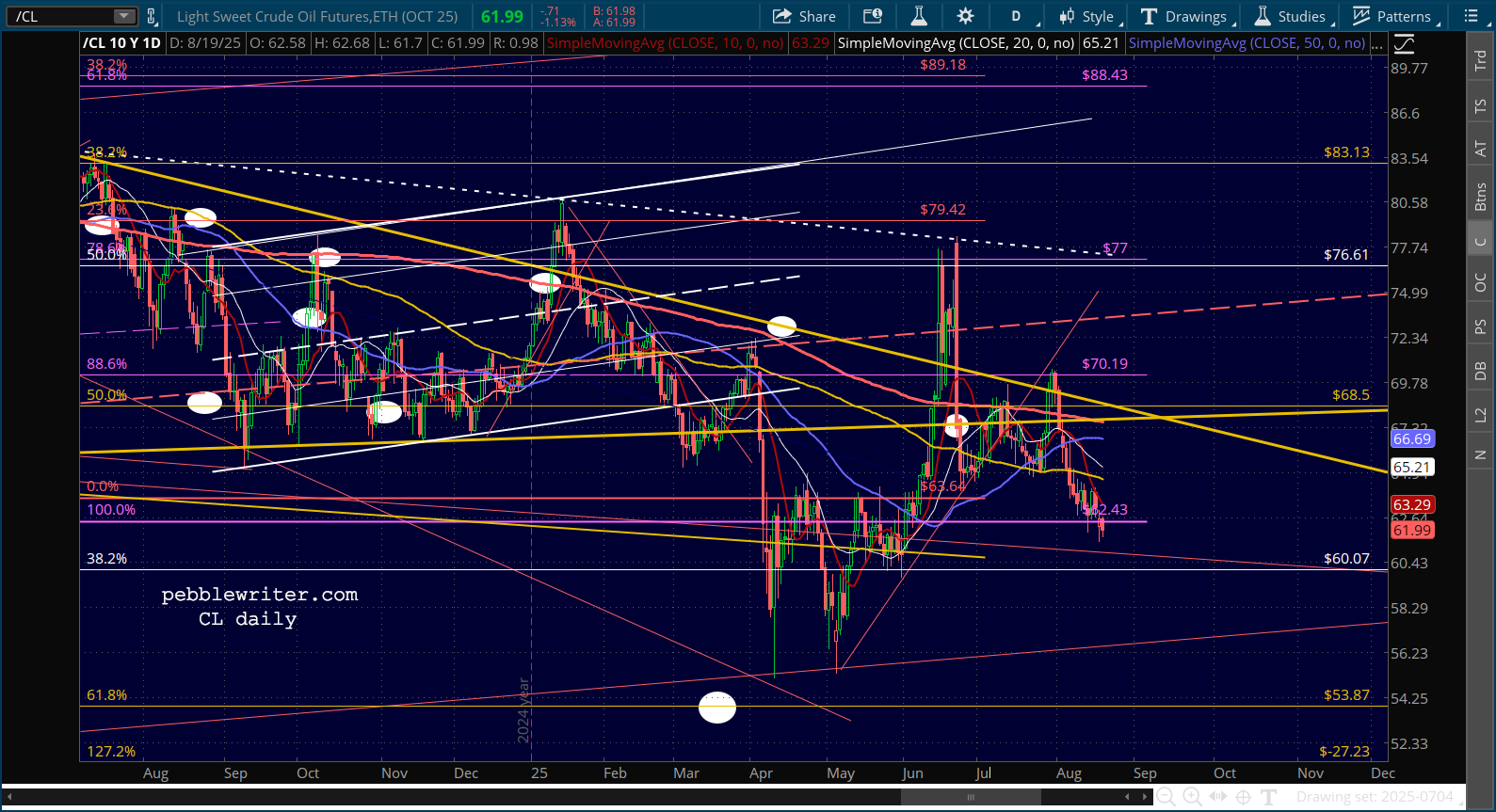

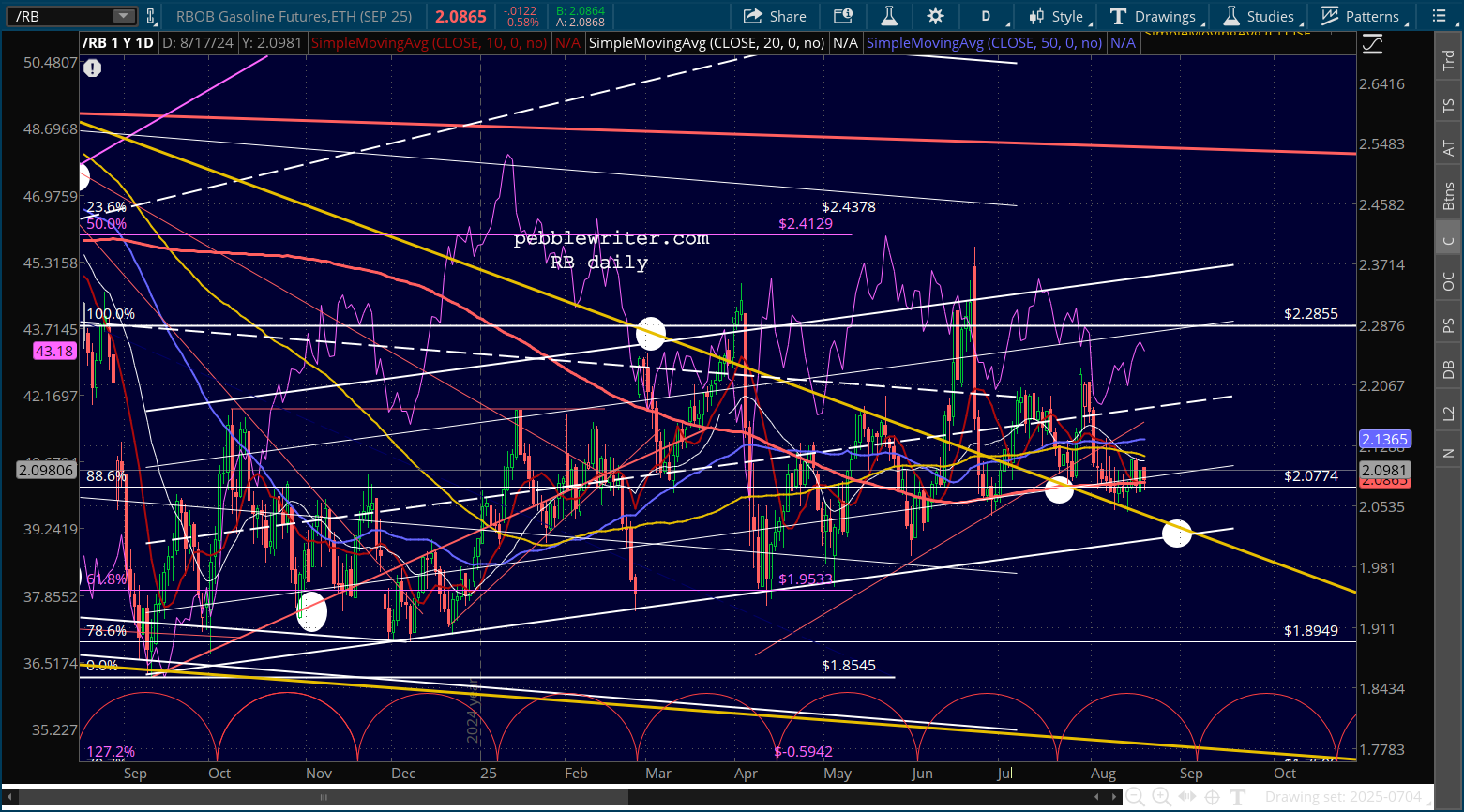

And, CL and RB continue to slip lower.

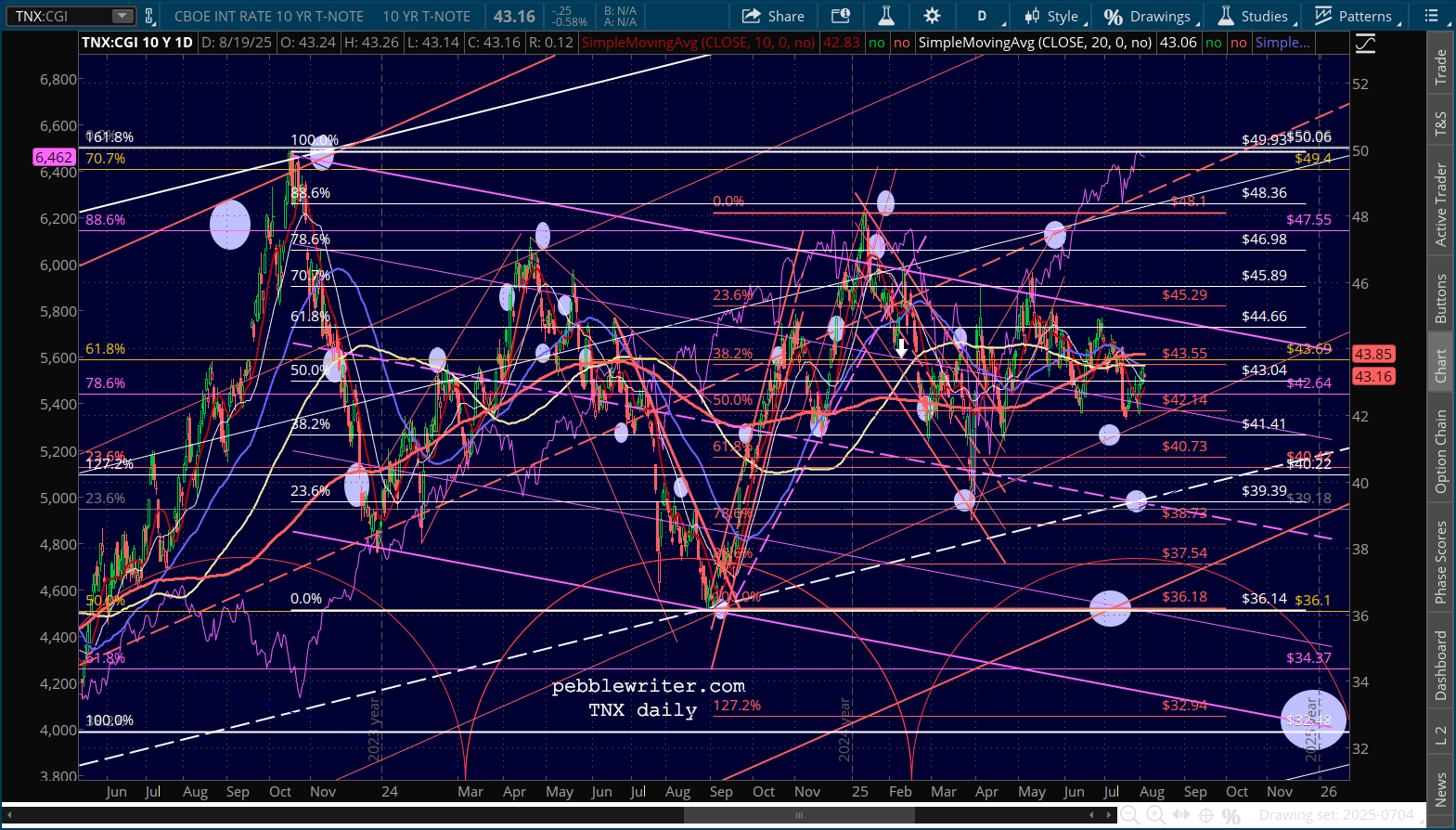

The 10Y is slightly lower this morning after testing its SMA100. The SMA200 is slightly higher at 43.85.

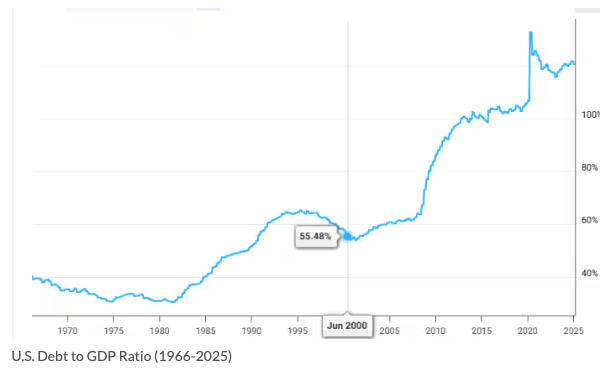

There was an interesting commentary attached to the latest S&P Global assessment of US credit. The AA+ rating was affirmed, but with an important caveat.

…a warning that without the credibility, flexibility and stability the Fed provides, and its crucial role in preserving the dollar’s reserve currency status, the credit rating of the U.S. could be materially lower. For example, Sexton forecasts the U.S. government deficit will average around 6% of gross domestic product through 2028 and its total government debt will exceed 100% of GDP by 2028. Compare this with Brazil, for example, where the deficit is around 7.6% of GDP and total debt is projected to hit 90% of GDP in 2027. Brazil’s rating is BB and so when it sold ten-year dollar bonds this year it paid an interest rate that was 237 basis points higher than corresponding U.S. Treasurys.

Debt never seems to be a problem…until it does. With inflation high and trending higher, and with Powell on his way out next year, and with the next Fed chair almost certainly to be directed by Trump to reduce interest rates, we could easily see rating agencies get more nervous about the US’ growing pile of debt.