The quandary central banks have been facing can be summarized as follows:

- stocks can’t move higher without the support of higher oil prices; and,

- oil prices can’t move higher without triggering inflation; and,

- central banks must tighten if inflation surpasses their target thresholds; and,

- the mere mention of tightening sends stock prices lower.

As CL neared critical support (after having reached our upside target last week) stocks were looking decidedly nervous. Clearly, something needed to give. Hence, Janet Yellen’s suggestion that inflation would be allowed to run a little hotter.

Yellen laid out the deepening concern at the Fed that U.S. economic potential is slipping [ed. note: this means lower stock prices] and aggressive steps may be needed to rebuild it.

Yellen, in a lunch address to a conference of policymakers and top academics in Boston, said the question was whether that damage can be undone “by temporarily running a ‘high-pressure economy,’ with robust aggregate demand and a tight labor market.”

In fact, the BoE’s Mark Carney said the same thing on the very same day. From the Telegraph:

Mr Carney told an audience in Nottingham that the current environment of low inflation was “going to change”, with the drop in the value of the pound likely to push up prices across the economy.

He said food prices were likely to be affected first, signaling that the situation was “going to get difficult” for those on the lowest incomes as the UK moves “from no inflation to some inflation”.

Fed followers will find this pivot familiar. Remember when reaching 5% unemployment was the bogie for discontinuing accommodative measures?

continued for members…

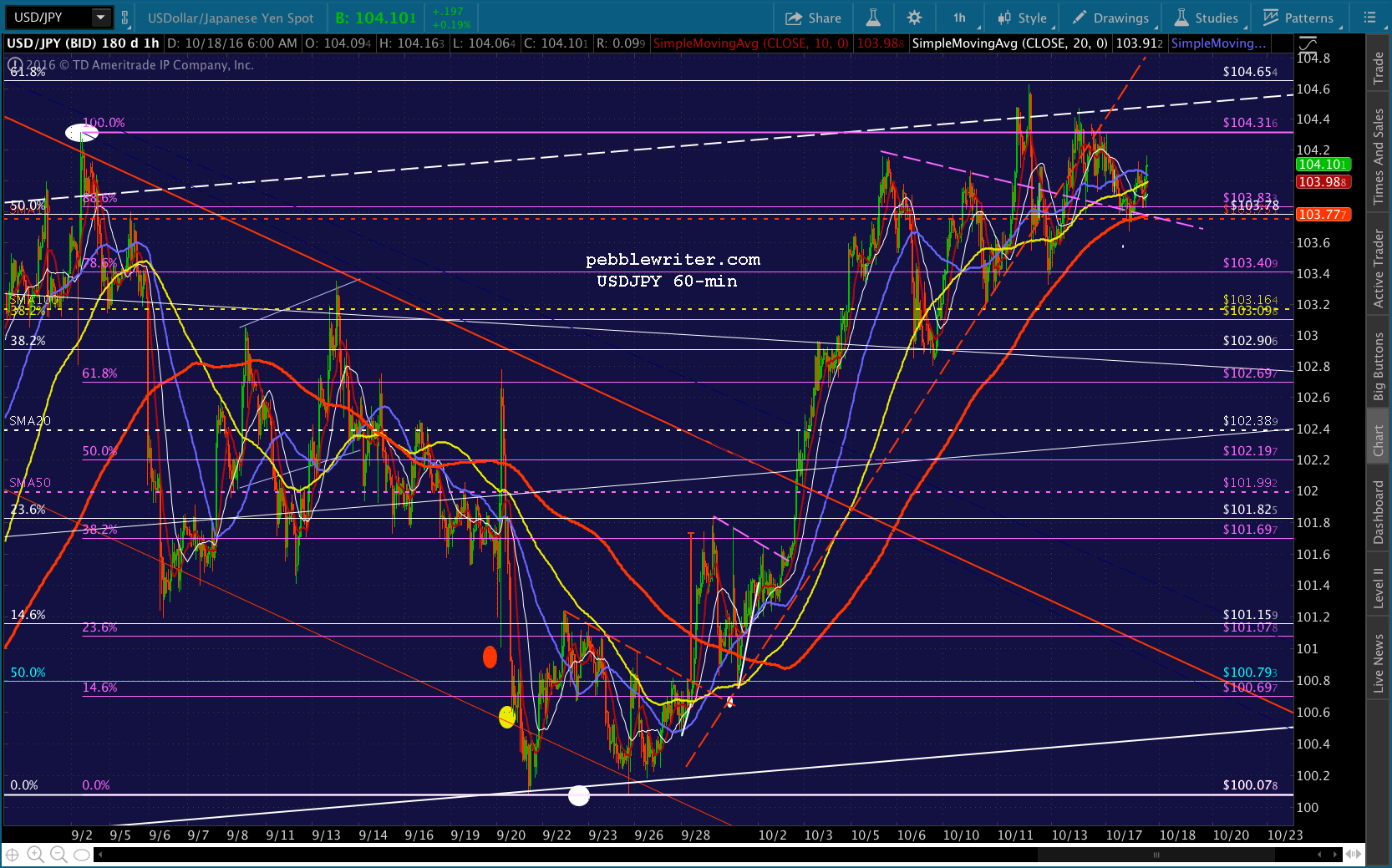

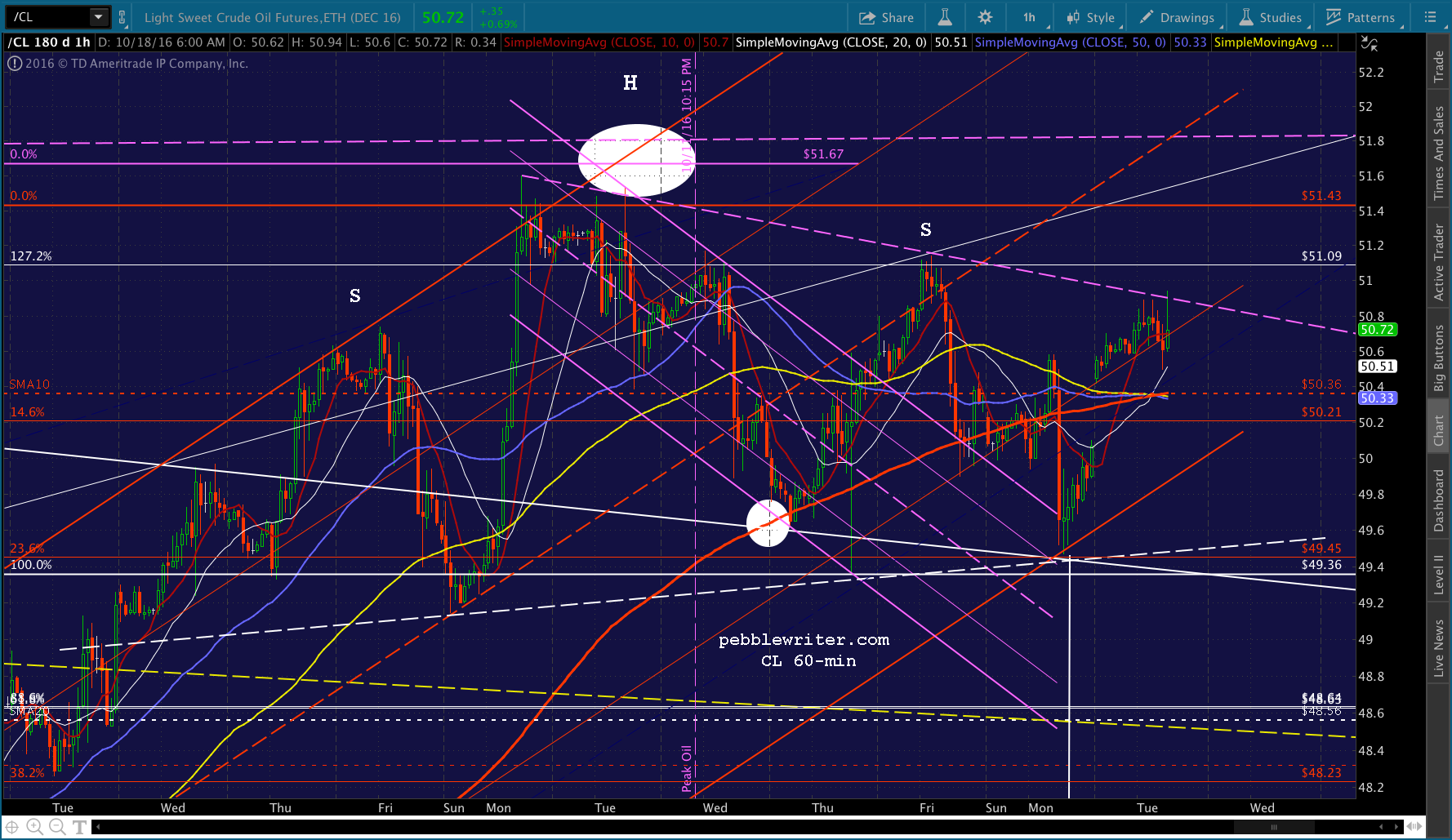

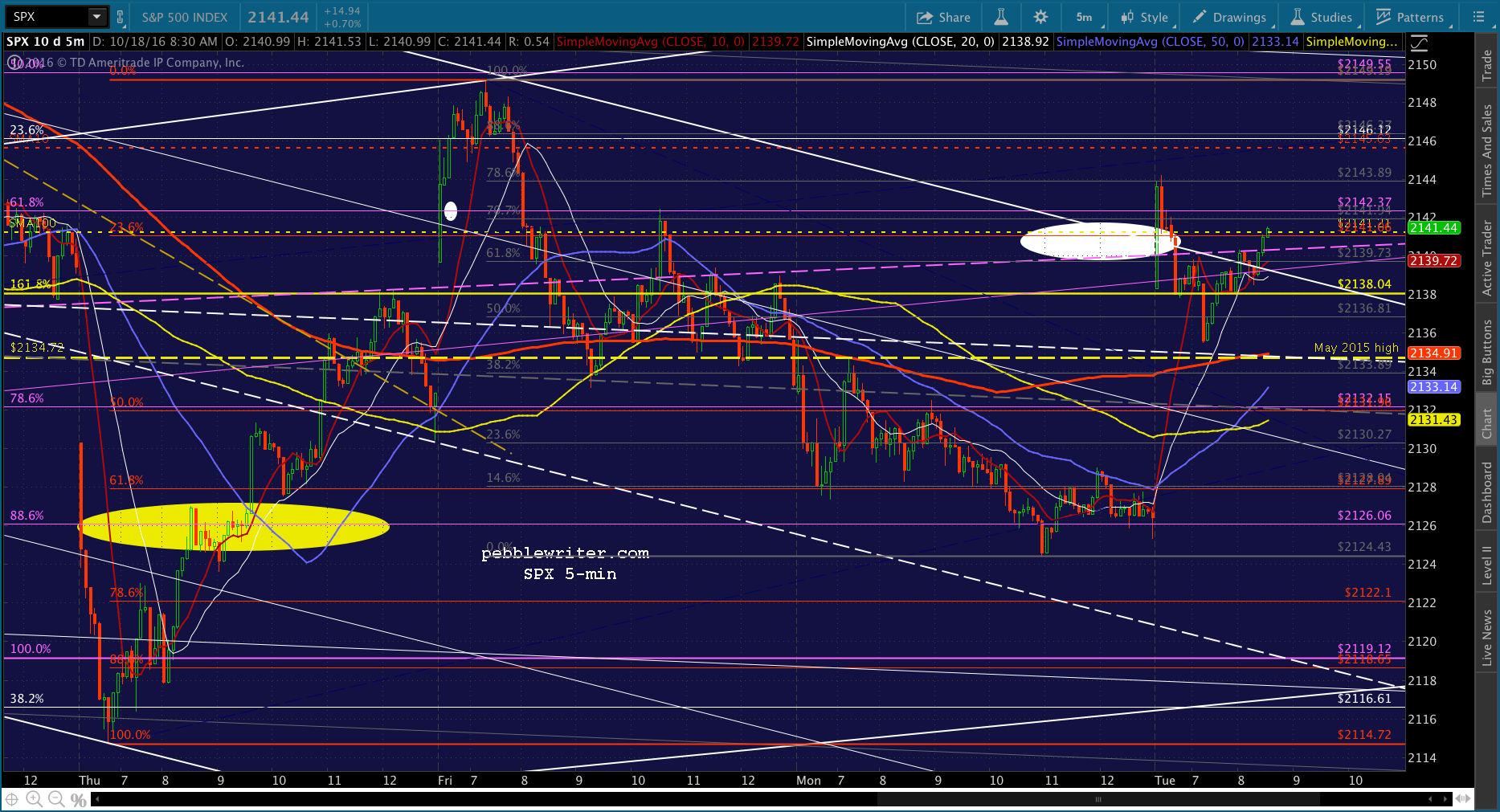

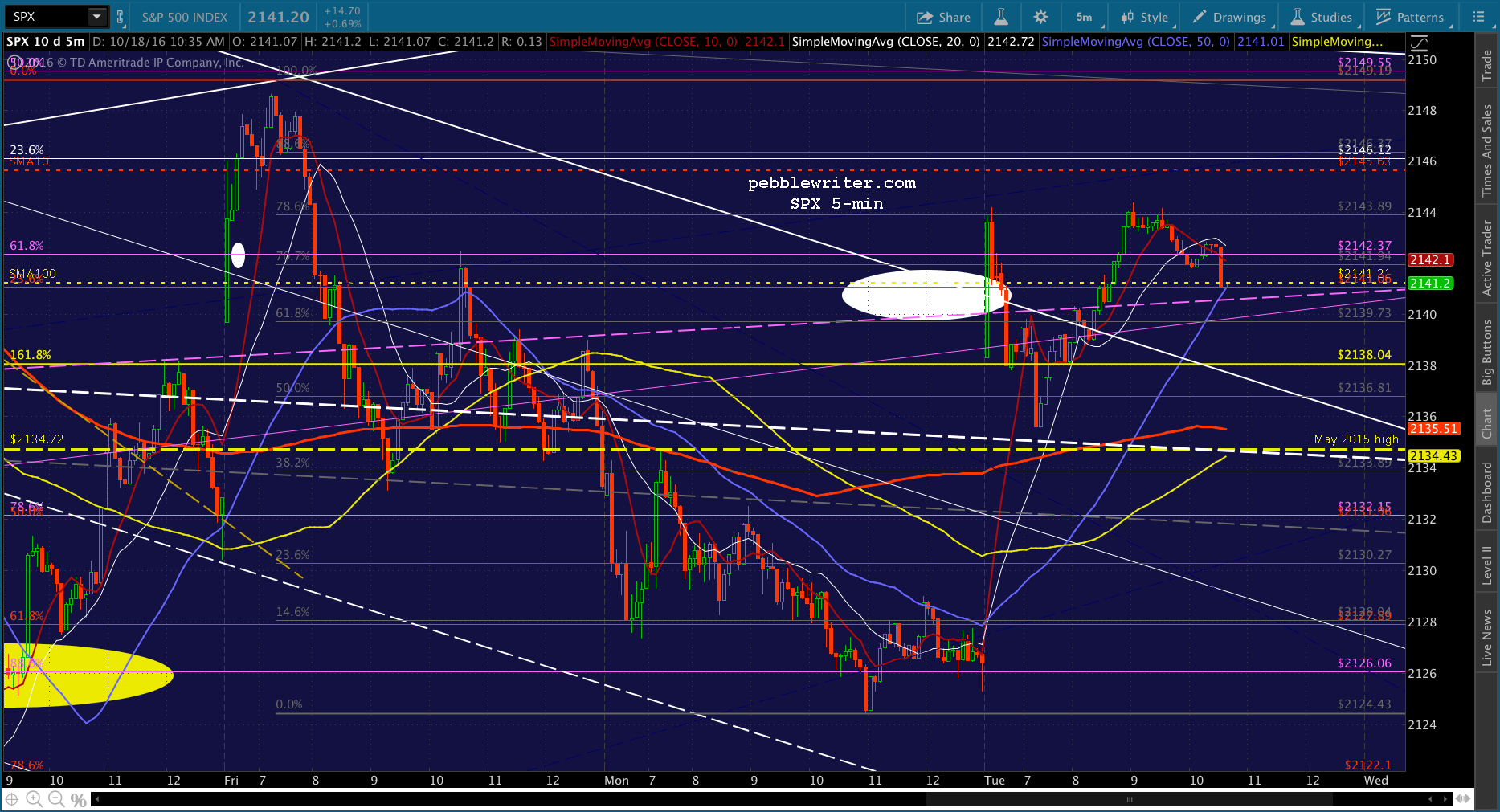

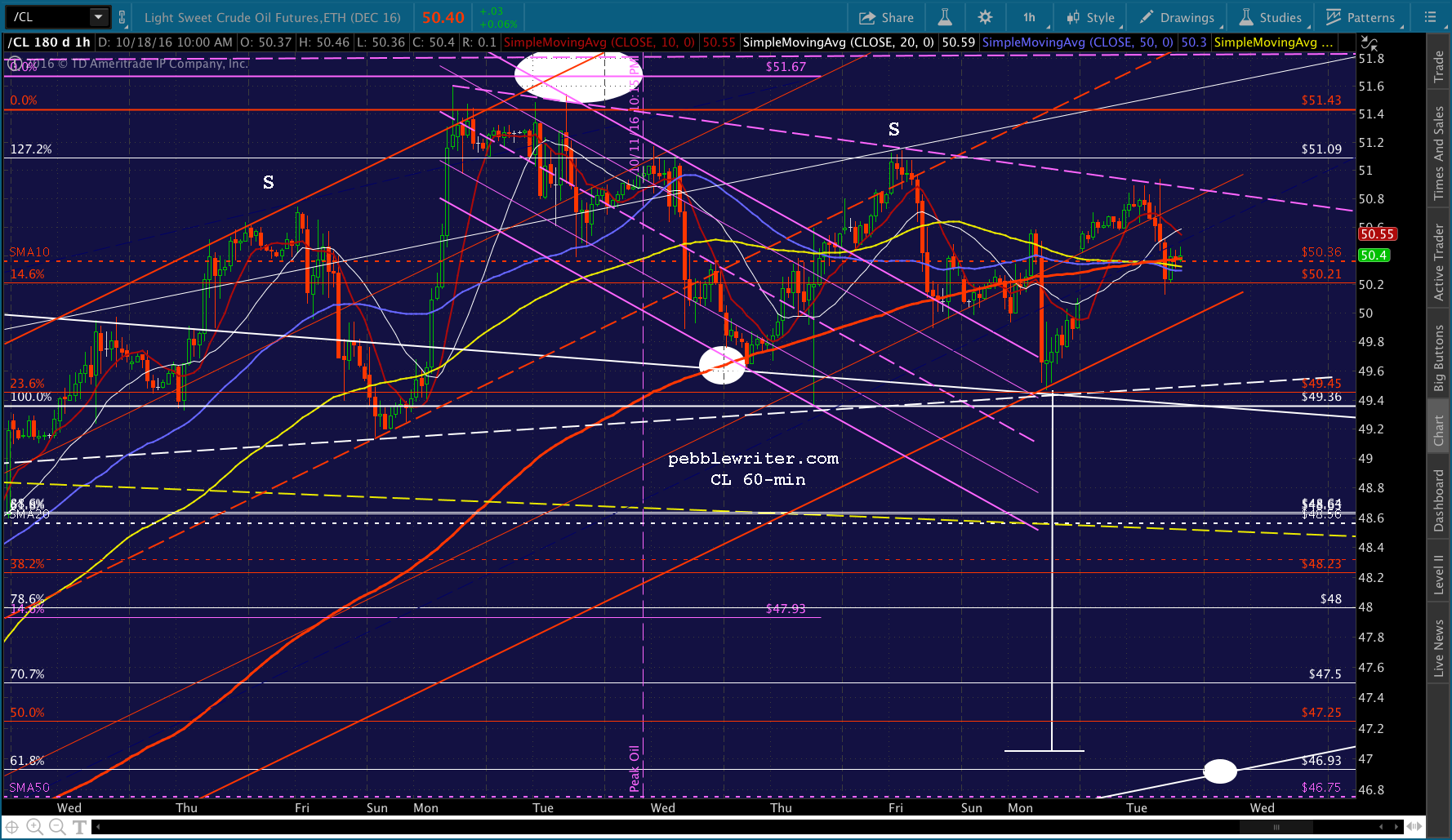

Look for SPX to backtest the purple midline and SMA100 at 2141.21 today. With USDJPY seemingly breaking out and CL having declined to complete the H&S Pattern, it has a very good chance of then breaking out of the falling white channel. USDJPY’s “breakout” isn’t much of one, but it upsets the apple cart for our lower SPX targets. the backtest of the falling red channel is more and more overdue.

USDJPY’s “breakout” isn’t much of one, but it upsets the apple cart for our lower SPX targets. the backtest of the falling red channel is more and more overdue.

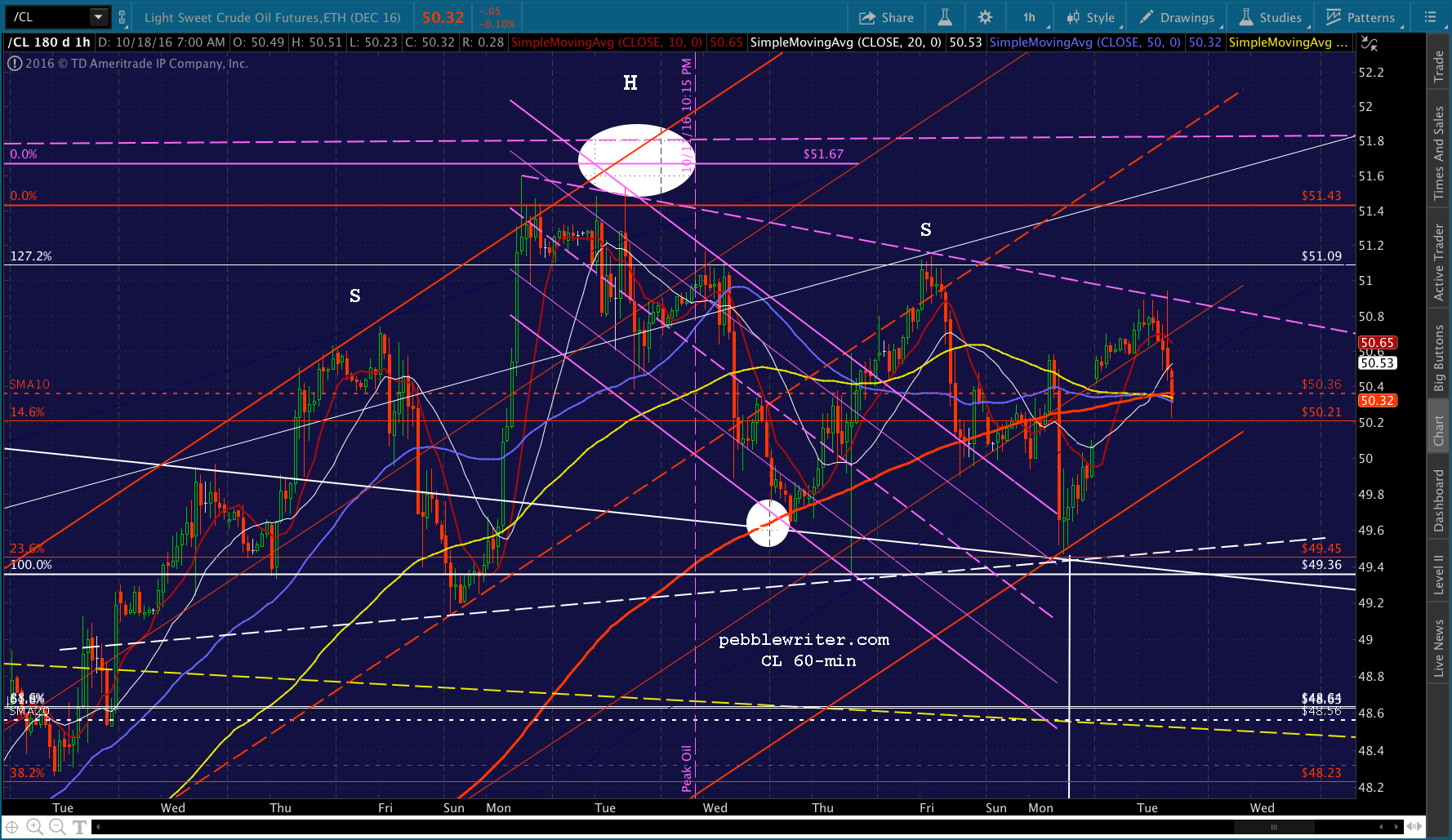

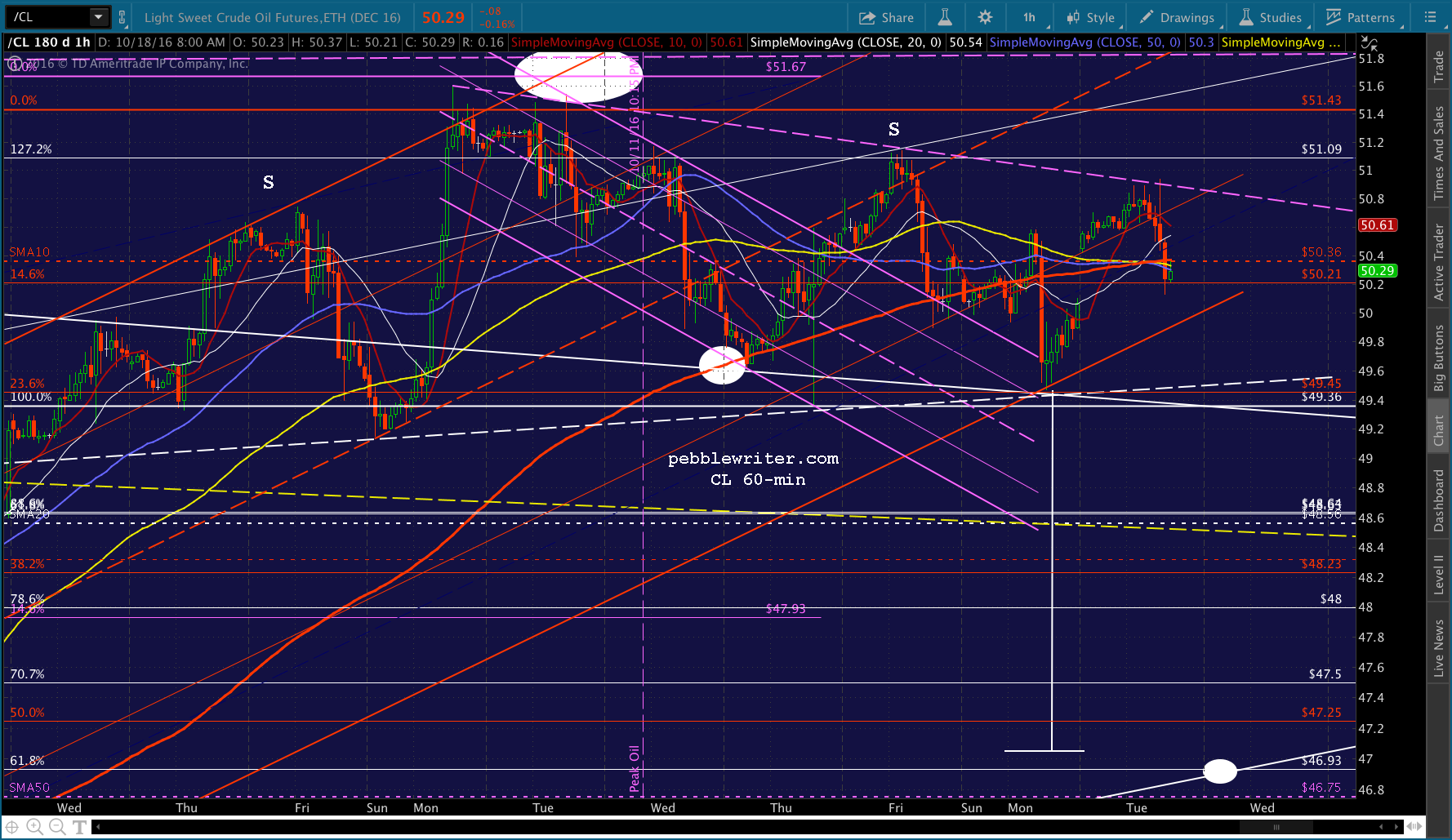

The bigger issue is CL itself, which has a chance to break out after having passed on the H&S yesterday. If it can’t, this morning’s spurt should turn into a pop and drop. If it can, then SPX will be back at the falling white channel top soon enough.

UPDATE: 10:07 AM

The initial spurt coincidentally topped the important 2138.04 Fib, and they’ve managed to hold it as the SMA5 10 approaches. Decision time coming up… USDJPY is back within the flag pattern.

USDJPY is back within the flag pattern. And, CL might or might not be holding the SMA10.

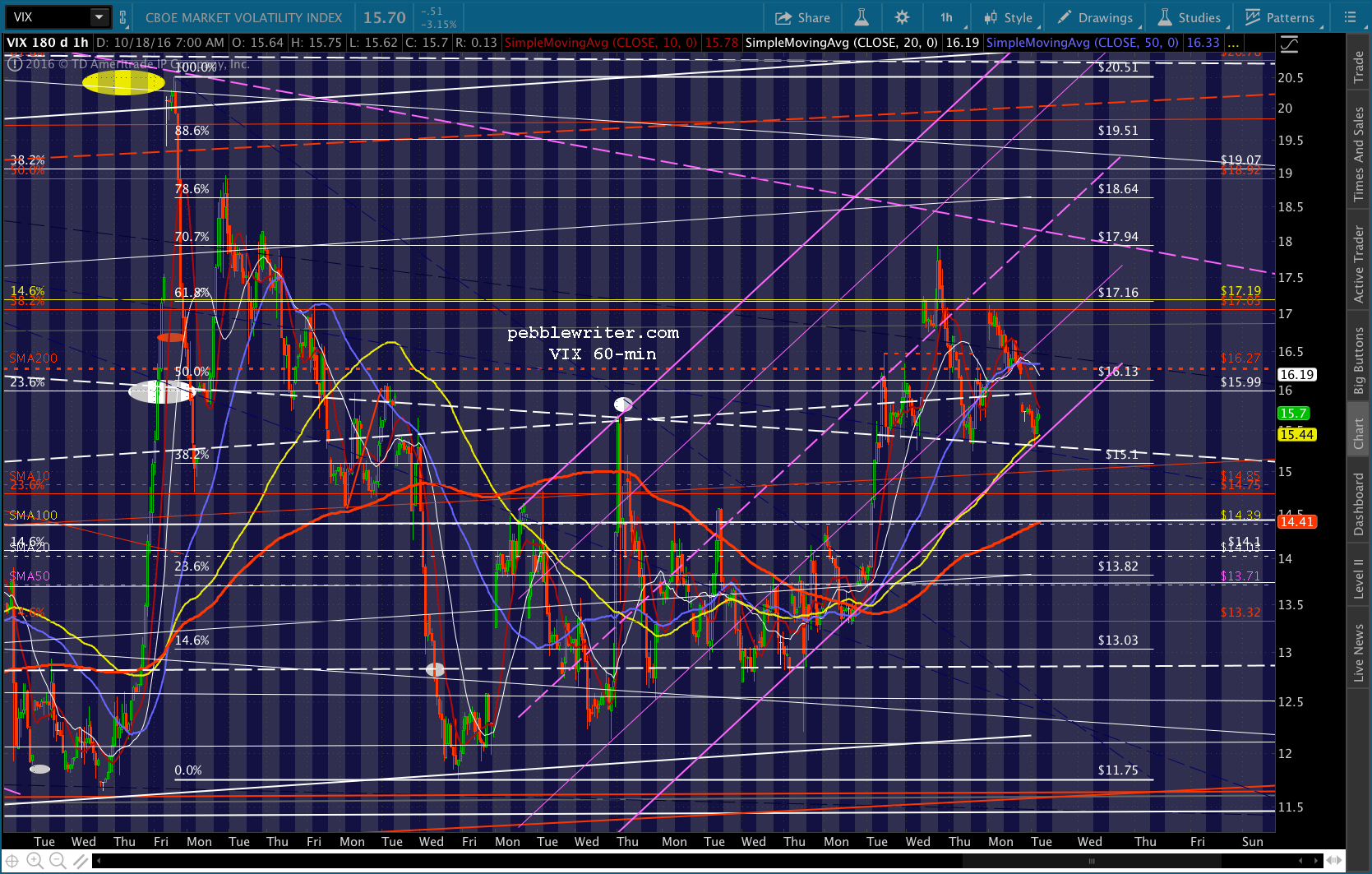

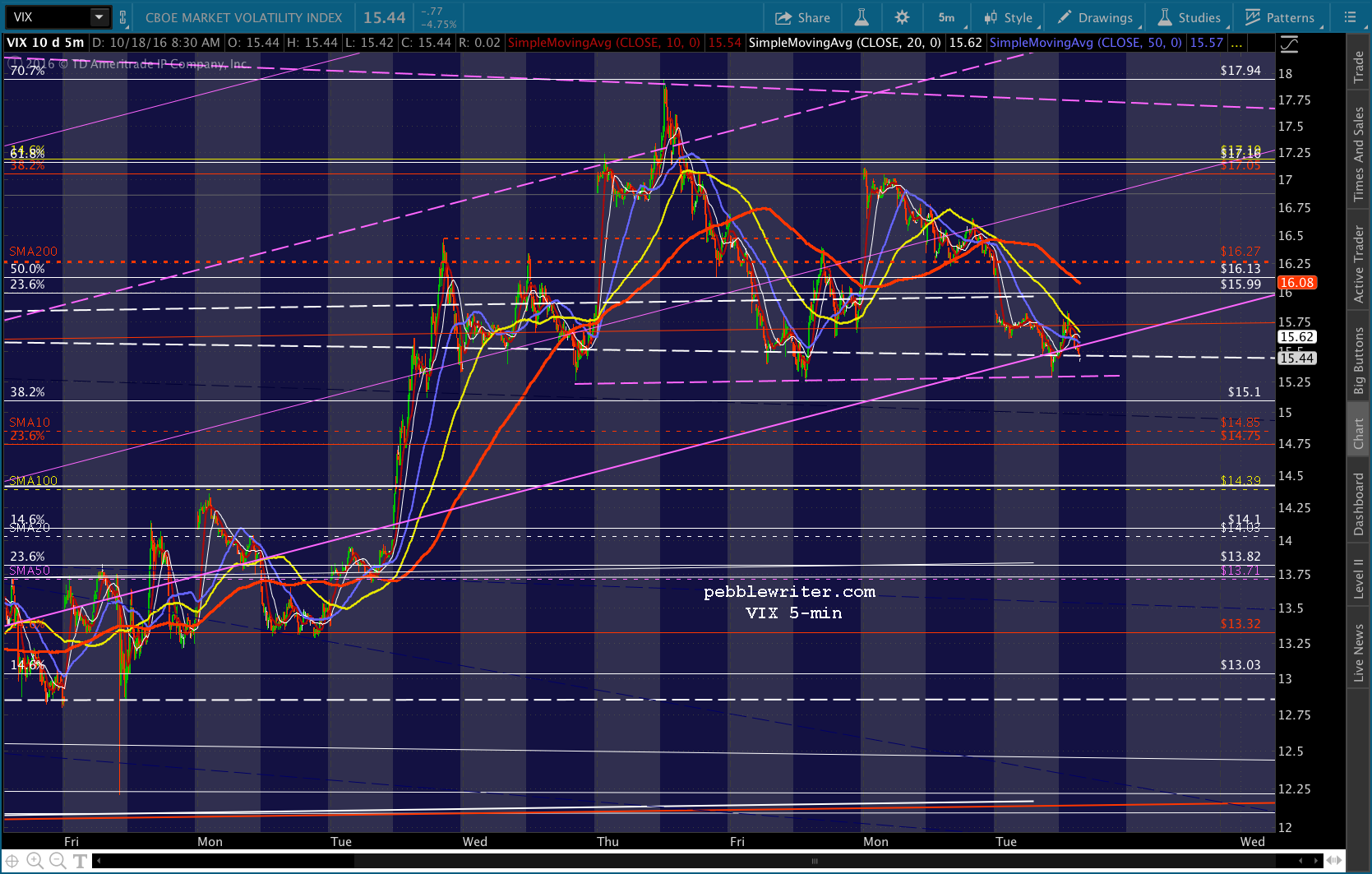

And, CL might or might not be holding the SMA10. One key might be VIX, which has nice support here — if it isn’t hammered lower. It’s already back below the SMA200…

One key might be VIX, which has nice support here — if it isn’t hammered lower. It’s already back below the SMA200…

UPDATE: 11:28 AM

Seeing an effort to break out of the falling white channel and challenge the SMA100 again. It’s being driven entirely by VIX, which continues to trickle lower.

CL continues to remain subdued. And, USDJPY has somewhat broken down, with further to go if the charts have anything to say about it.

And, USDJPY has somewhat broken down, with further to go if the charts have anything to say about it.

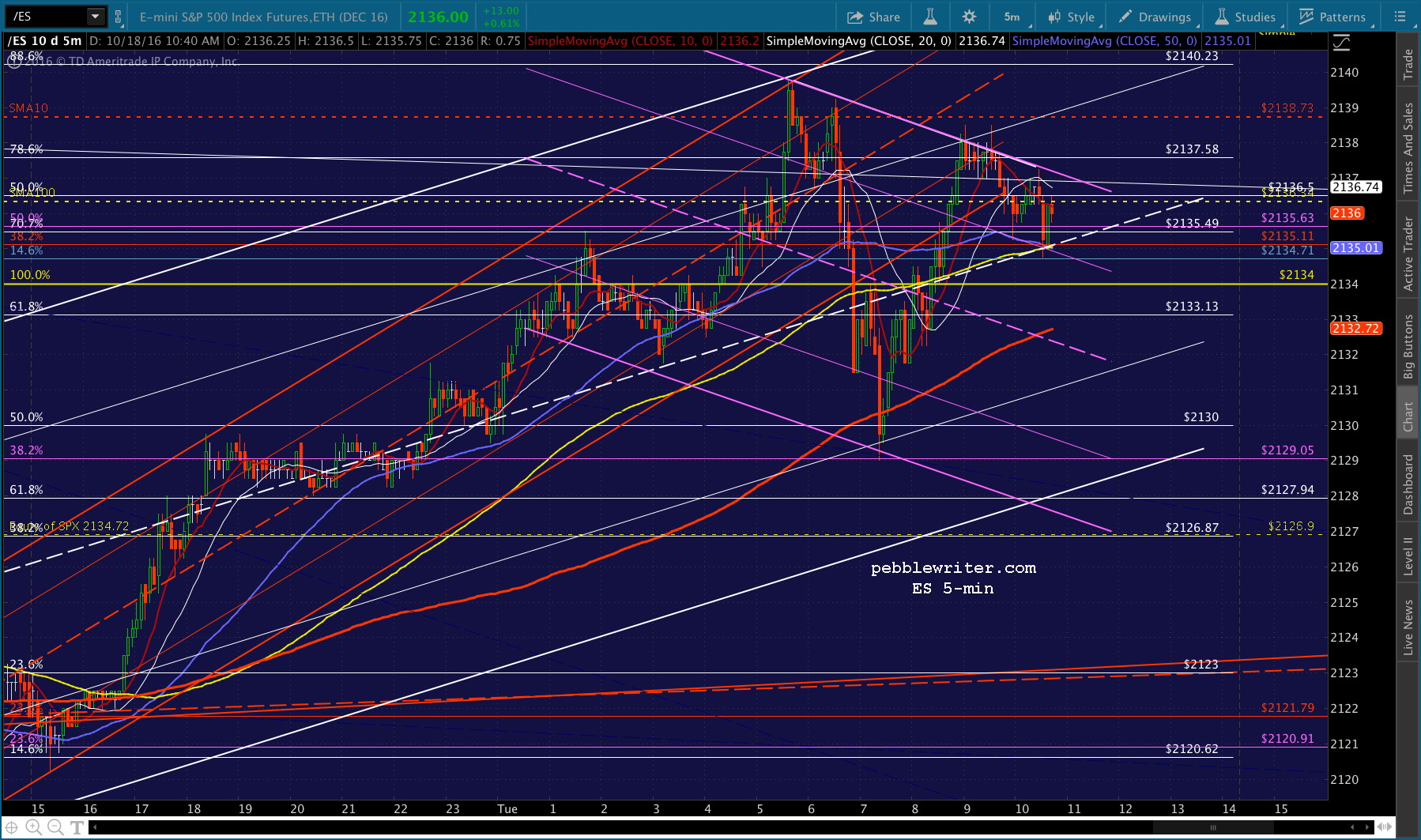

This doesn’t really feel like a breakout as much as it does a delay. If they were trying to actually break SPX out, I imagine we’d see CL above its SMA10, for starters. But, we’ll see. I still anticipate a drop to 2103-2110 if SPX is able to get back down below 2119.

UPDATE: 1:36 PM

We’ve seen this movie before. SPX just fell through the SMA5 10 and 20 and backtested the SMA100, right as the SMA5 50 arrived.  If it can hold the SMA100, I’ll give up on the idea of 2110. But, for now, it continues to merely tread water. The ES, in particular, shows signs of wanting to push lower.

If it can hold the SMA100, I’ll give up on the idea of 2110. But, for now, it continues to merely tread water. The ES, in particular, shows signs of wanting to push lower.

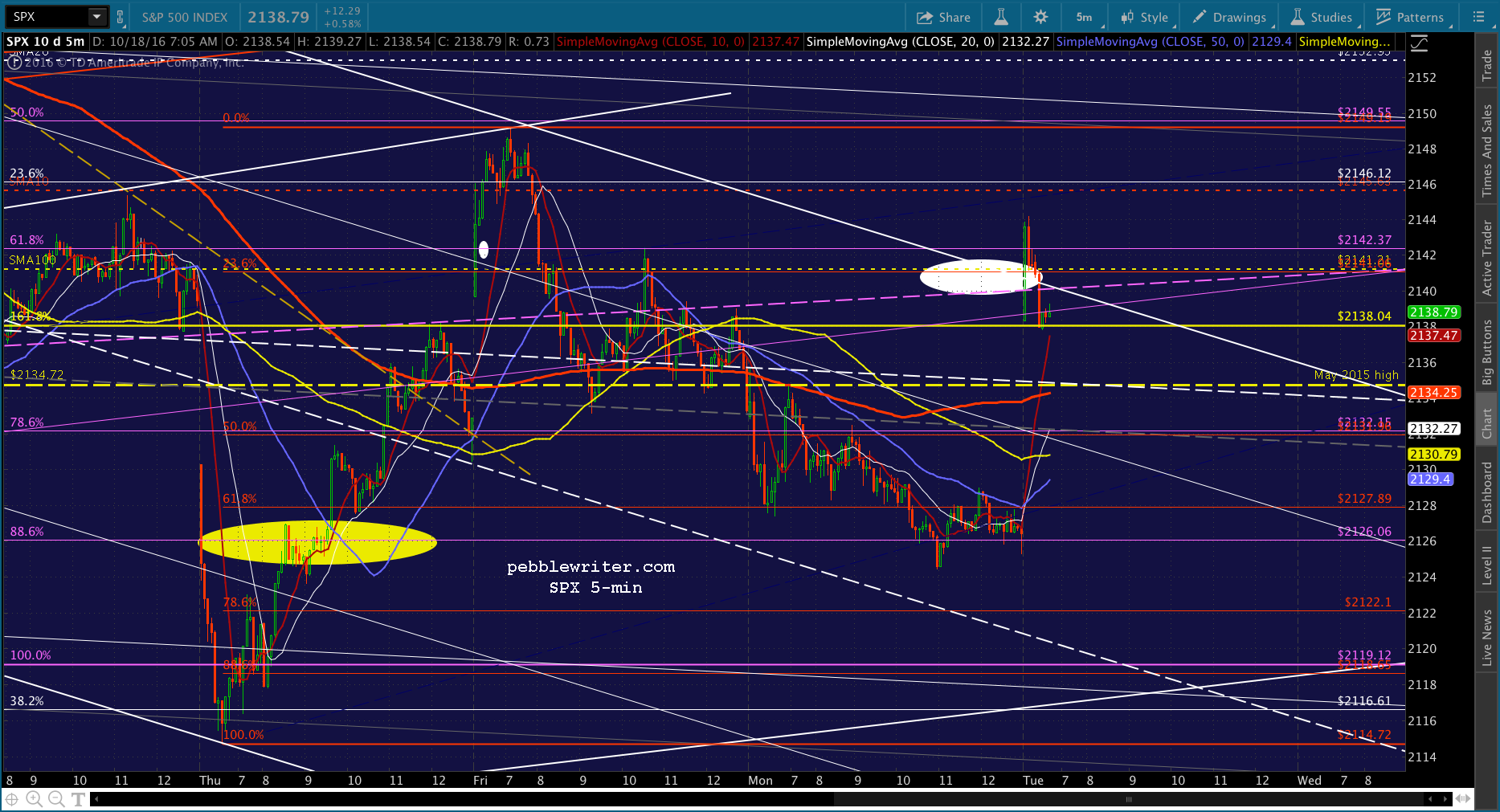

Here’s a clearer view of the quandary: test or backtest?

And, CL is still hanging around the SMA10.  USDJPY could go either way, but is headed for 103.16 if the purple TL ever breaks.

USDJPY could go either way, but is headed for 103.16 if the purple TL ever breaks.

Even VIX, which has done all the propping today, hasn’t really broken down.

The risk of a breakout remains elevated. But, my gut tells me we’re headed lower.

.

Comments

6 responses to “Changing the Rules”

Tomorrow marks the 1987 market crash. Oct 18, 1929 is when the markets began selling-off hard, which help set-up for ‘Black Thursday’ Oct 24th and the following Black Monday and Black Tuesday. I’m sorry to say, I would like to see a repeat of the 1929 chart.

Thank you for that reminder, Timothy. Cue the spooky music!

PW, to what extent do you believe TPTB can slam the VIX? Is there a point where it becomes too expensive/too suspicious? This last candle down in SPX matches with a candle down in the VIX, which is just silly… Is it possible to have a major correction without VIX going over 25 now?

I’m afraid they are old pros at slamming VIX. Re your question, I think it’s about six words too long. I wonder if it’s possible to have a major correction, period. The drops to 1823ish were dramatic, but TPTB managed to stop them when necessary. And, the Brexit correction was practically over before it started. They are deathly afraid of a crash, and rightly so. This “recovery” was built on the unstable sands of unsustainable intervention.

ES is well above the trend line from 10/10. Feels like the market will be forced higher or grind sideways until the election.

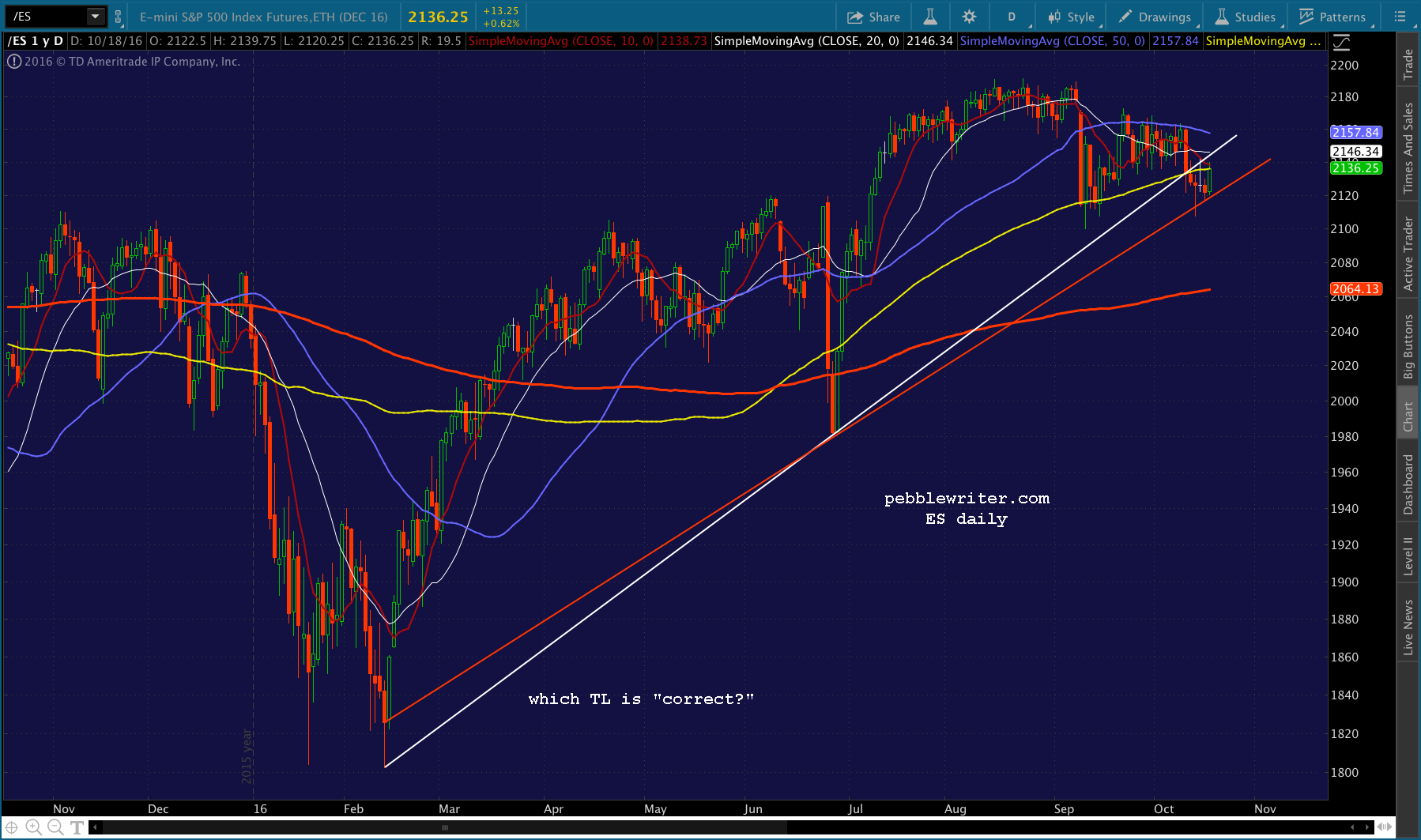

Definitely can’t rule out higher or sideways — which fits with my political take. But there are other TL’s that could exert more influence. See the daily ES chart above.