Futures dipped a bit overnight as reports suggested Trump was considering withdrawing from the WTO.  For the second time this week, Mnuchin came to the rescue with a vehement denial. And, for the third time this week, the algos got plenty of support from VIX shorting (breaking trend no less)…

For the second time this week, Mnuchin came to the rescue with a vehement denial. And, for the third time this week, the algos got plenty of support from VIX shorting (breaking trend no less)… …and USDJPY ramping.

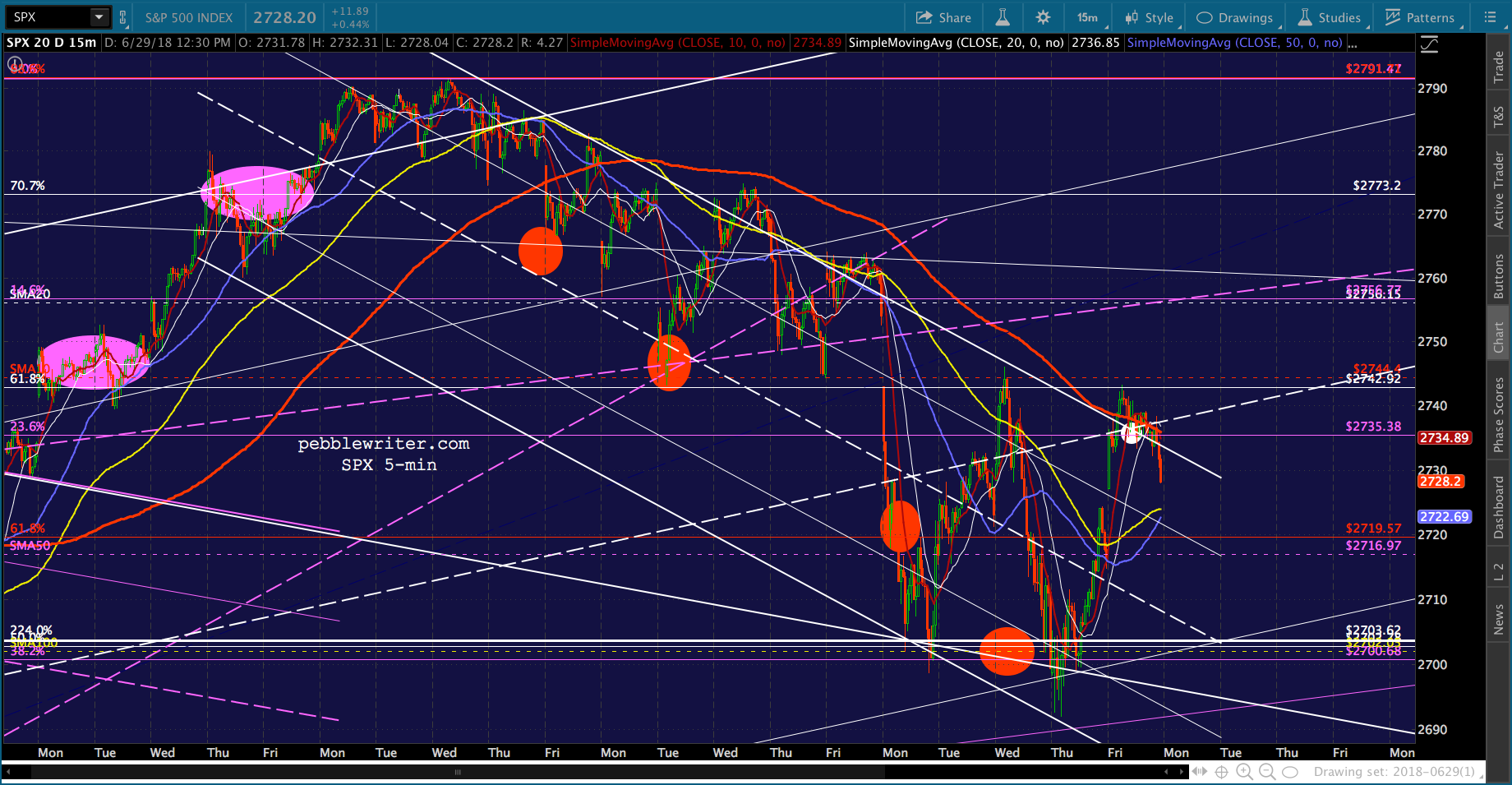

…and USDJPY ramping. What a fitting end to a quarter where politicians, central bankers and corporate buybacks have set the tone, calming the markets at every turn. Still, this isn’t exactly a bullish-looking pattern — especially when SPX fails to break out of the falling white channel.

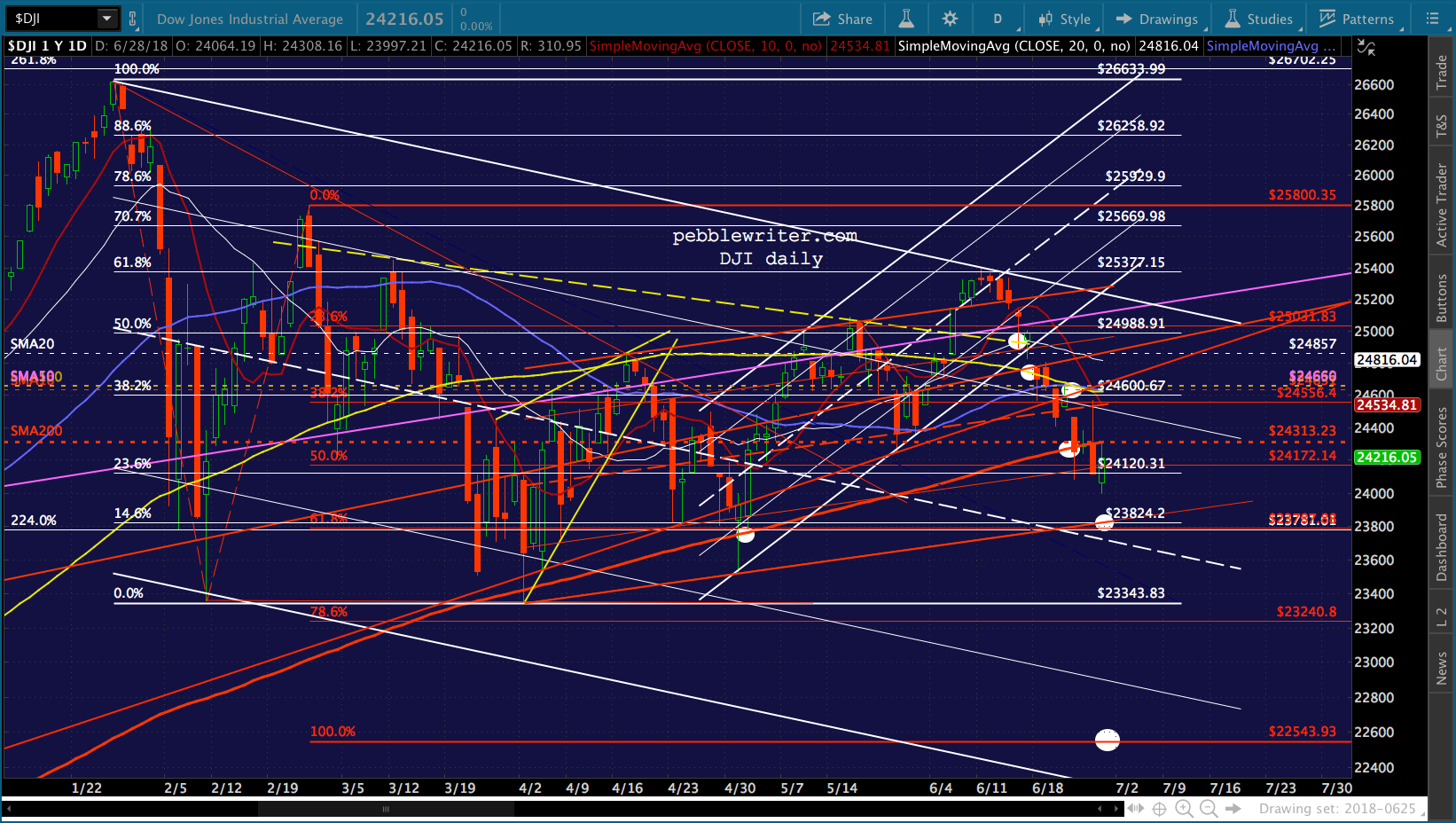

What a fitting end to a quarter where politicians, central bankers and corporate buybacks have set the tone, calming the markets at every turn. Still, this isn’t exactly a bullish-looking pattern — especially when SPX fails to break out of the falling white channel. And, while everything appears copacetic, has anyone noticed that the Dow closed below its 200-day moving average for the past four sessions in a row?

And, while everything appears copacetic, has anyone noticed that the Dow closed below its 200-day moving average for the past four sessions in a row?

continued for members…

There’s a pretty good argument for a drop to 23824 (a 2% drop) though I would imagine it will wait until after the quarter end. Looking at the big picture, I see the dollar as being overbought….

Looking at the big picture, I see the dollar as being overbought….

…the euro as also being irrationally high.

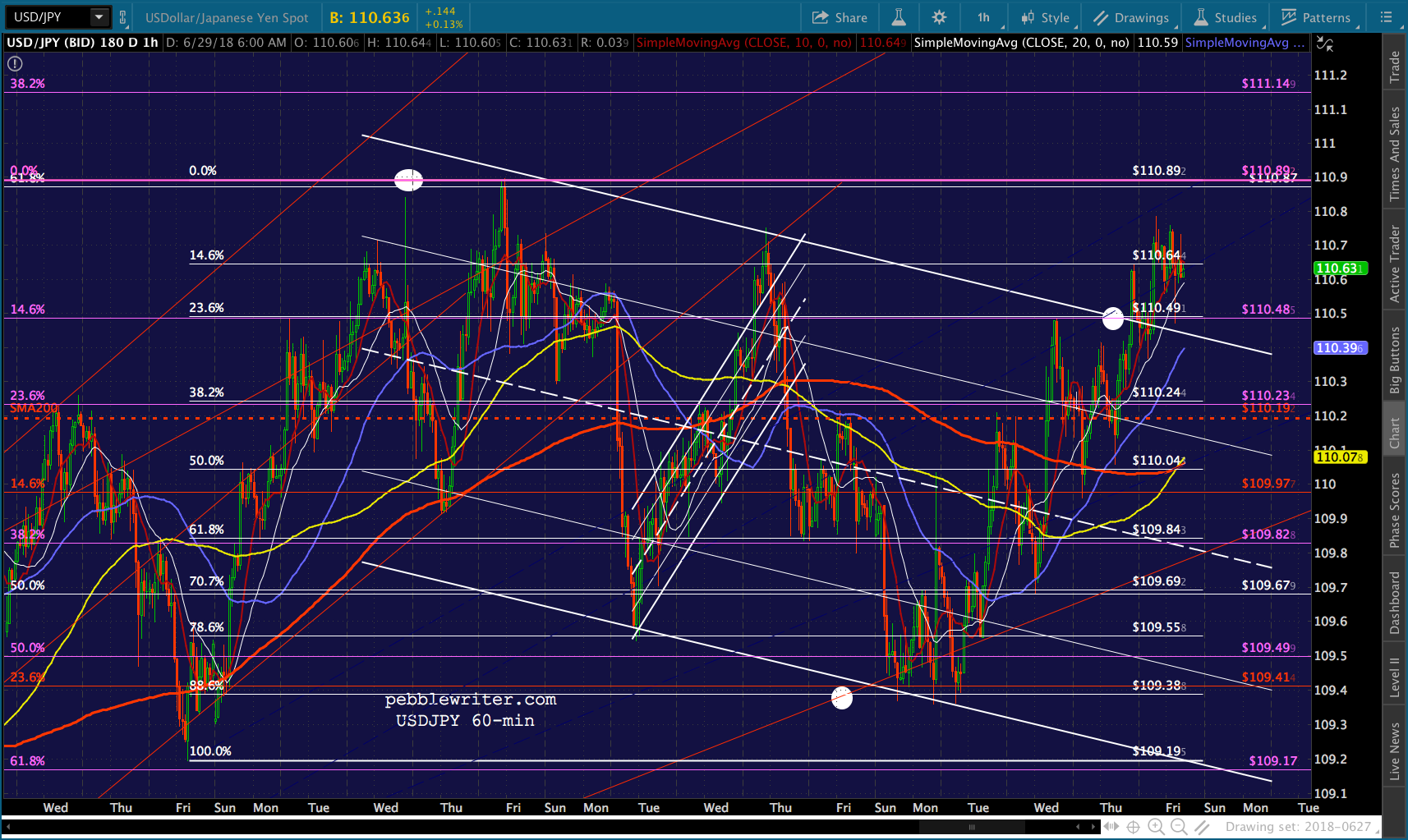

…the euro as also being irrationally high. The USDJPY seems happy to dance about its SMA200, bouncing higher and breaking out of the falling white channel in order to support stocks.

The USDJPY seems happy to dance about its SMA200, bouncing higher and breaking out of the falling white channel in order to support stocks. RB and CL continue their ramps, but perhaps only until the quarter is over.

RB and CL continue their ramps, but perhaps only until the quarter is over.  And, despite all this, SPX is still in a falling channel which broke down and expanded this week. To me, it suggests lower next week, perhaps significantly — whether or not it tops its SMA5 200 (2739ish.)

And, despite all this, SPX is still in a falling channel which broke down and expanded this week. To me, it suggests lower next week, perhaps significantly — whether or not it tops its SMA5 200 (2739ish.)

Bottom line, I don’t buy the growth narrative for a minute. Sure, some countries/regions are doing better than others. But, the economic data is false. Take inflation, for instance. EIA reported an average gasoline price of 2.80 for June.

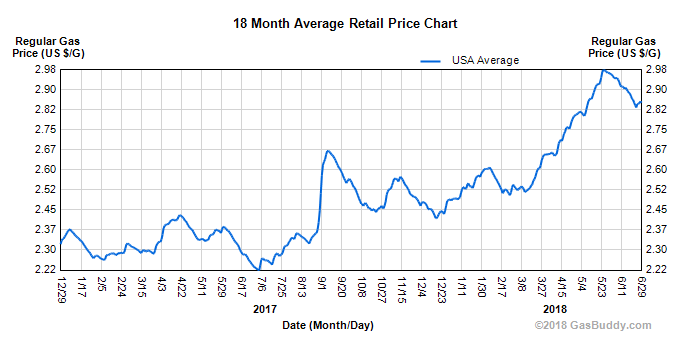

Bottom line, I don’t buy the growth narrative for a minute. Sure, some countries/regions are doing better than others. But, the economic data is false. Take inflation, for instance. EIA reported an average gasoline price of 2.80 for June.

According to AAA and Gas Buddy, the price of gas nationwide never even reached 2.80 in June. It’s not a big difference, but EIA reported a 24.1% increase, while AAA’s data indicates a 29.3% increase. Note that 29.3% would be the biggest YoY increase since Feb 2017’s 32% (CPI was 2.7%.) Last month (May) CPI came in at 2.8% on a 21.9% increase. A 29.3% increase would generate, what, 3%+?

Note that 29.3% would be the biggest YoY increase since Feb 2017’s 32% (CPI was 2.7%.) Last month (May) CPI came in at 2.8% on a 21.9% increase. A 29.3% increase would generate, what, 3%+?

As we’ve discussed many times, the Fed/Administration cannot afford CPI to go any higher because they can’t afford rates to go any higher. So, they lie.

It keeps interest rates under control, and makes all the inflation-based data (ironically, real-whatever) more presentable.

But, there are repercussions. Higher US rates impair free cash flow for over-indebted consumers and businesses, choke off real estate and capital investment, trashes car sales, throw the EM world into a tizzy, etc. You name it. About the only good thing about the higher USD is that it helps mitigate higher import prices and, therefore, inflation.

But, remember, it was higher inflation that raised rates in the first place. It’s a spiral that leads nowhere good.

UPDATE: 3:50 PM

Stocks are losing ground going into the close. With next week being a holiday week, the usual MO is a week-long prop job or even a breakout. But, this is a fairly ugly way to end the day/quarter — leaves me feeling fairly bearish.