GDP was revised from 2.2% to 2.0% — highlights: personal consumption lower than expected, prices higher than expected. The market was ahead of this, with rates continuing to slide. Bottom line, it doesn’t make a terribly compelling case for two additional rate hikes.

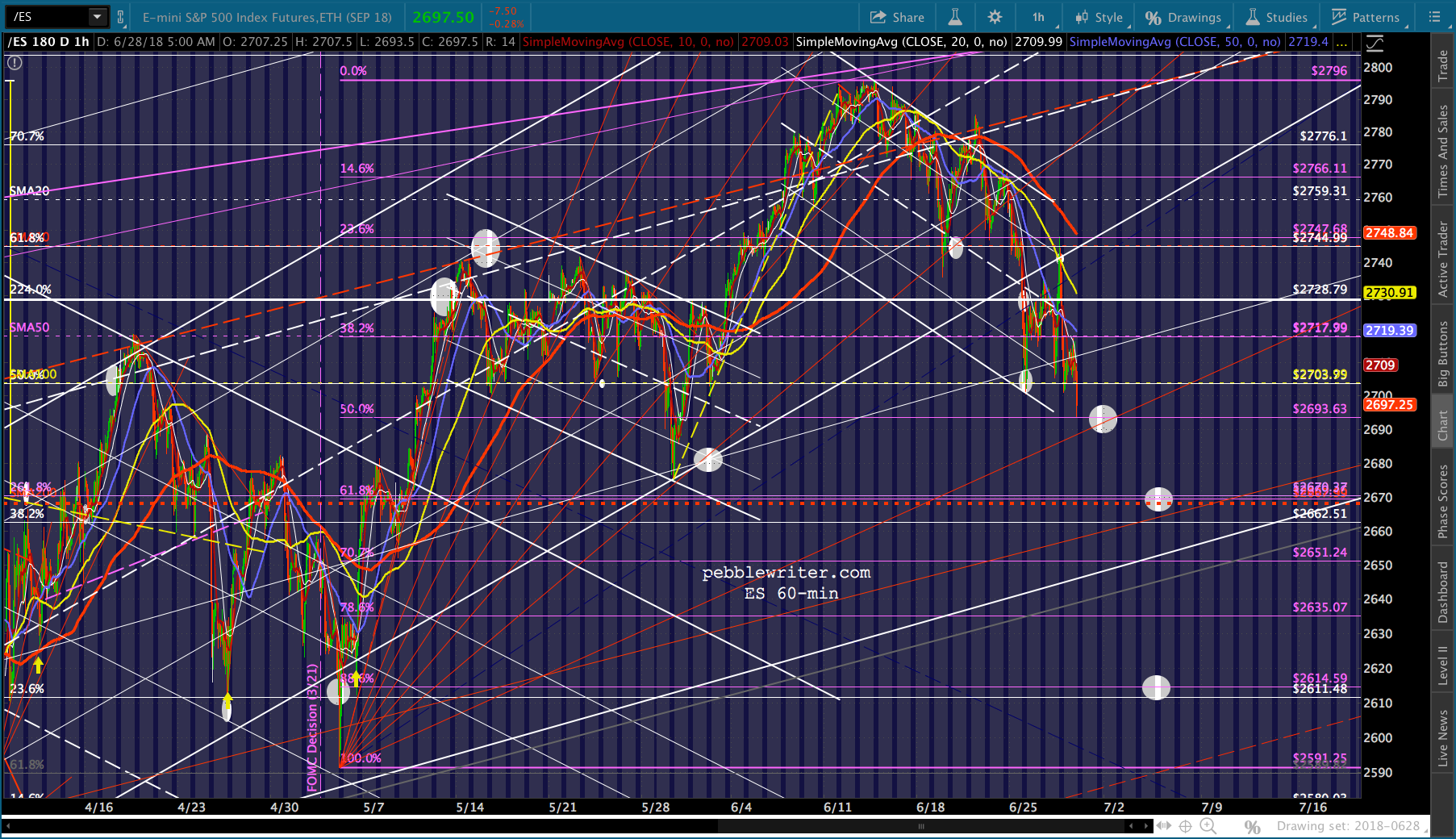

Futures are off about 10 points, tagging our next downside target a day ahead of schedule.

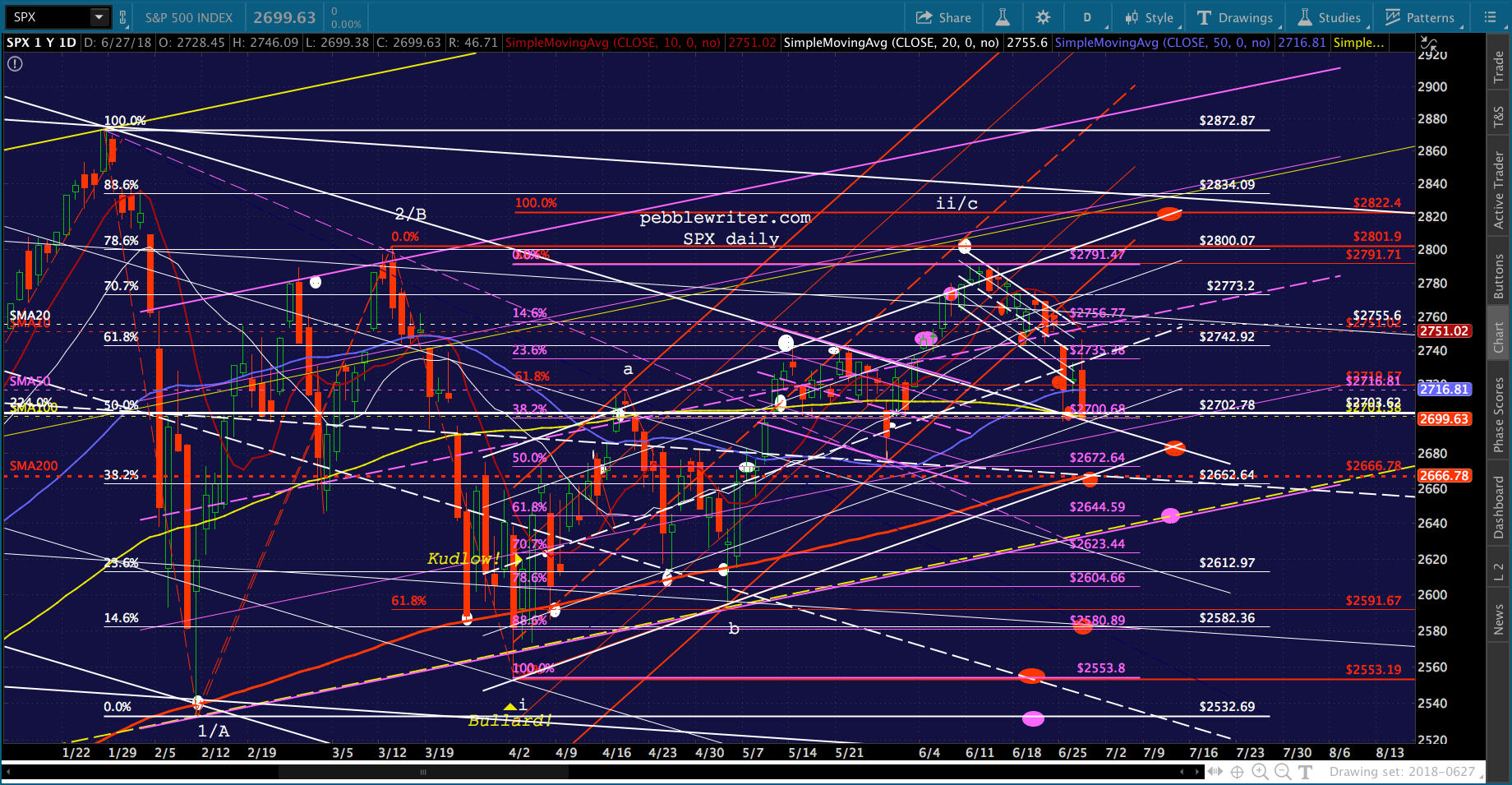

Futures are off about 10 points, tagging our next downside target a day ahead of schedule. SPX closed 2017 at 2673.61. Can it hang on to its slight gain for two more sessions?

SPX closed 2017 at 2673.61. Can it hang on to its slight gain for two more sessions?

continued for members…

Note that the SMA200 is now at 2666.78 – slightly below its breakeven level. So, there’s decent support. If it slips below both, then all bets are off.

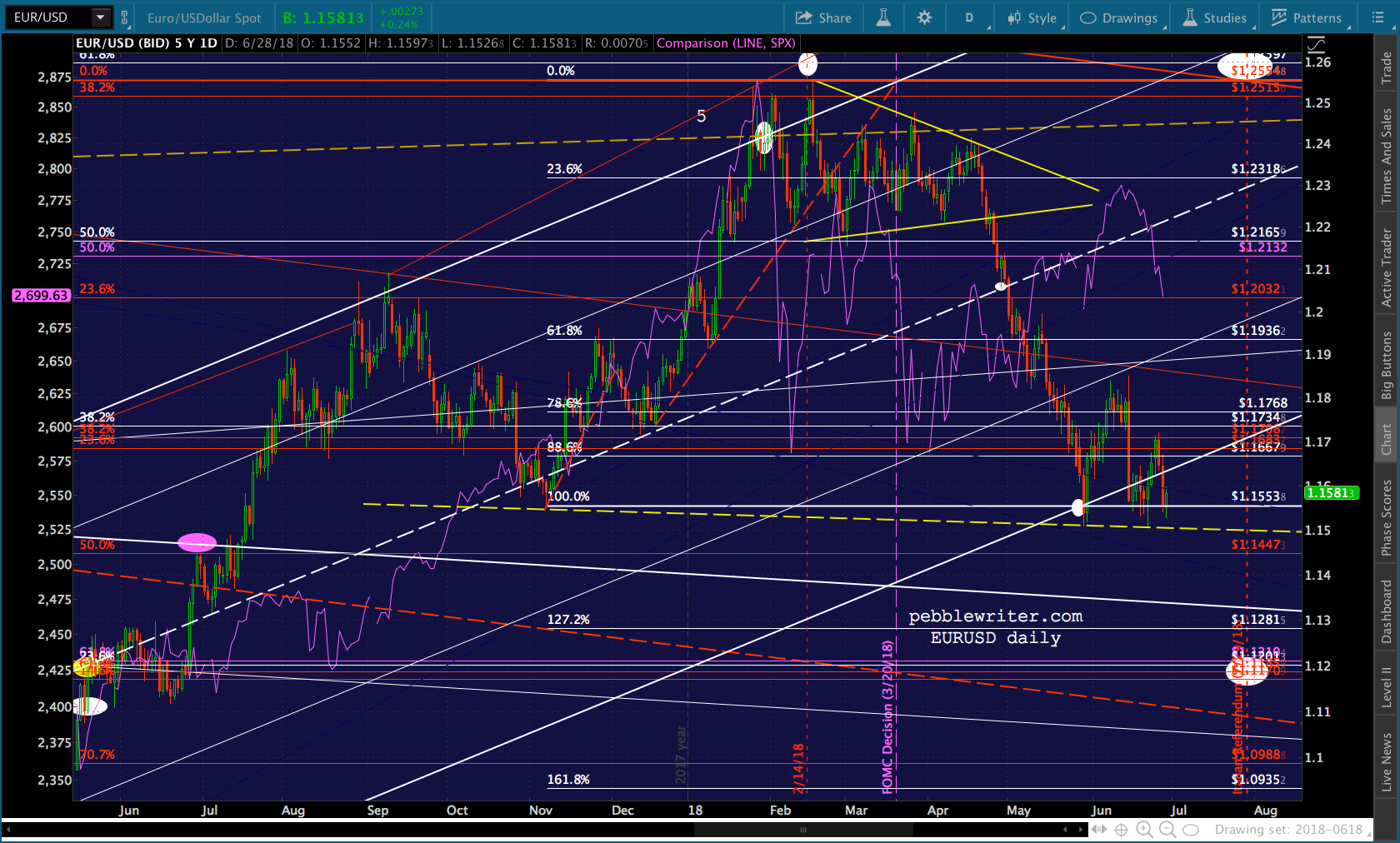

With GDP slipping, the odds of multiple rate hikes keeps dropping. We’re seeing it in the notes.

With GDP slipping, the odds of multiple rate hikes keeps dropping. We’re seeing it in the notes.  But, not yet so much in the dollar.

But, not yet so much in the dollar.

That’s more of a currency game, of course.

Equities should continue to focus onto hanging on to that slight YTD gain.

Equities should continue to focus onto hanging on to that slight YTD gain.

RB gapped lower after yesterday’s close, but has a long way to go if it’s going to produce a drop in CPI for June.

RB gapped lower after yesterday’s close, but has a long way to go if it’s going to produce a drop in CPI for June. There’s a pretty strong thunderstorm going outside at the moment. So, there’s always the possibility that we’ll lose power.

There’s a pretty strong thunderstorm going outside at the moment. So, there’s always the possibility that we’ll lose power.

More later.