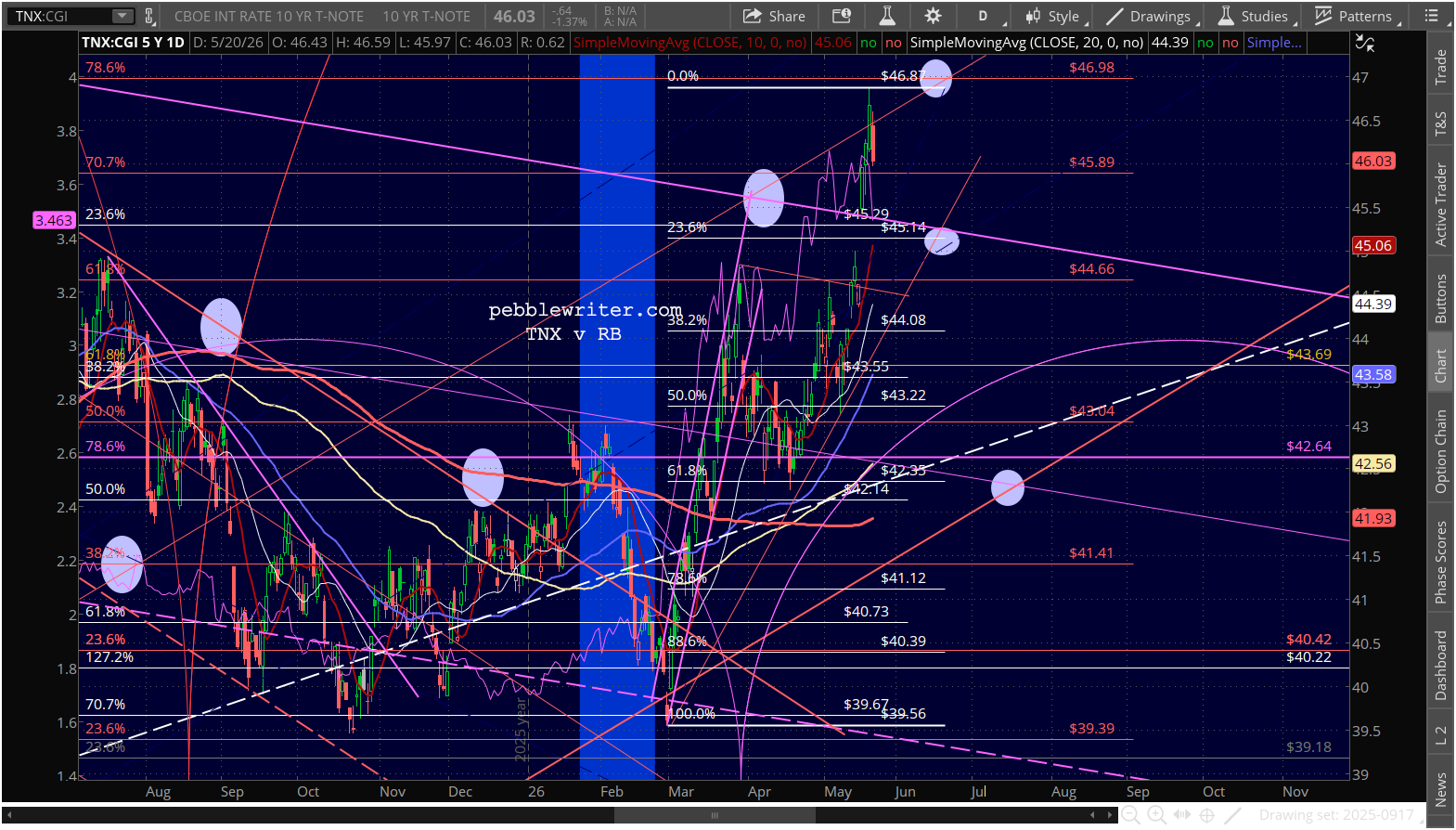

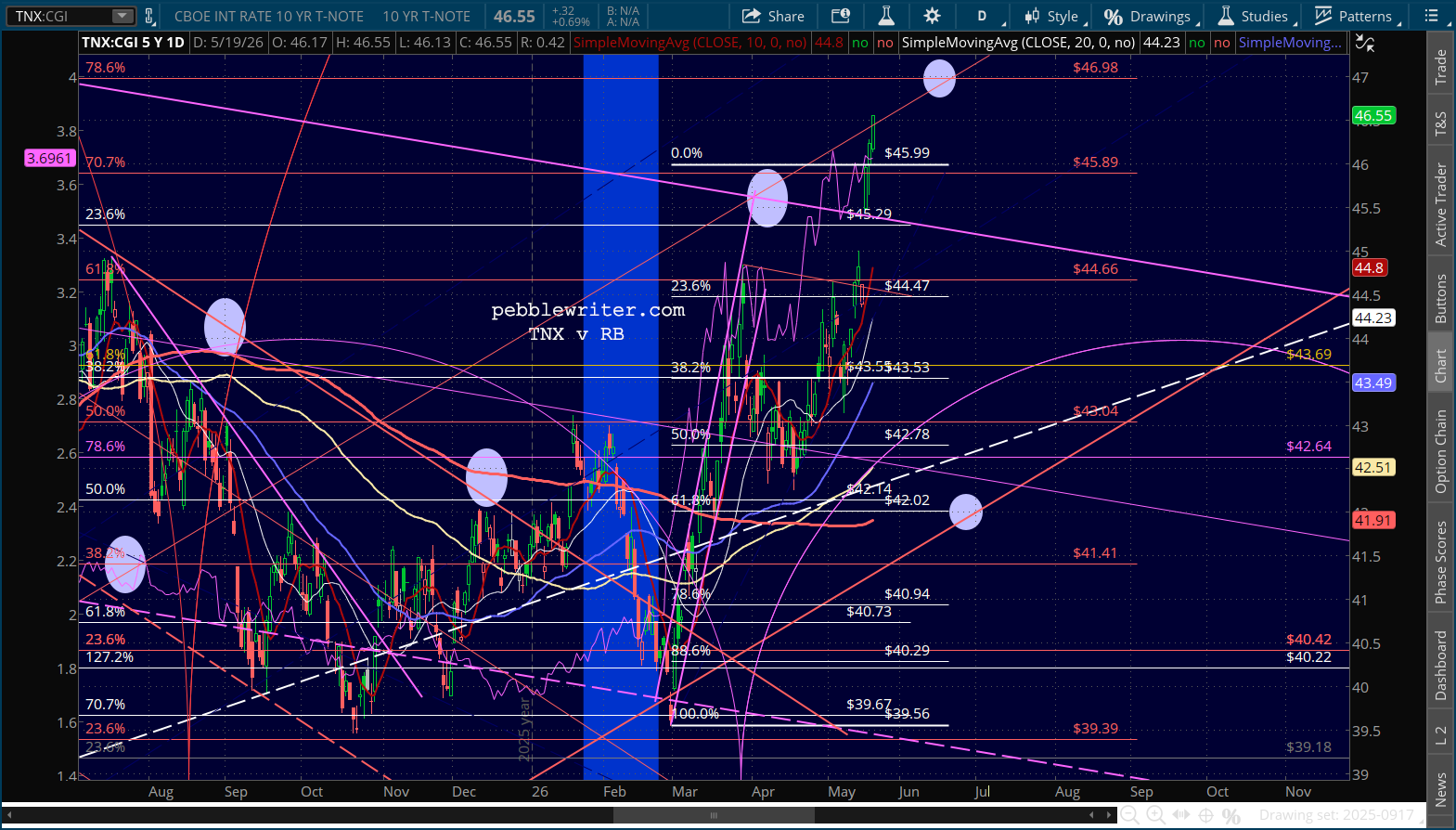

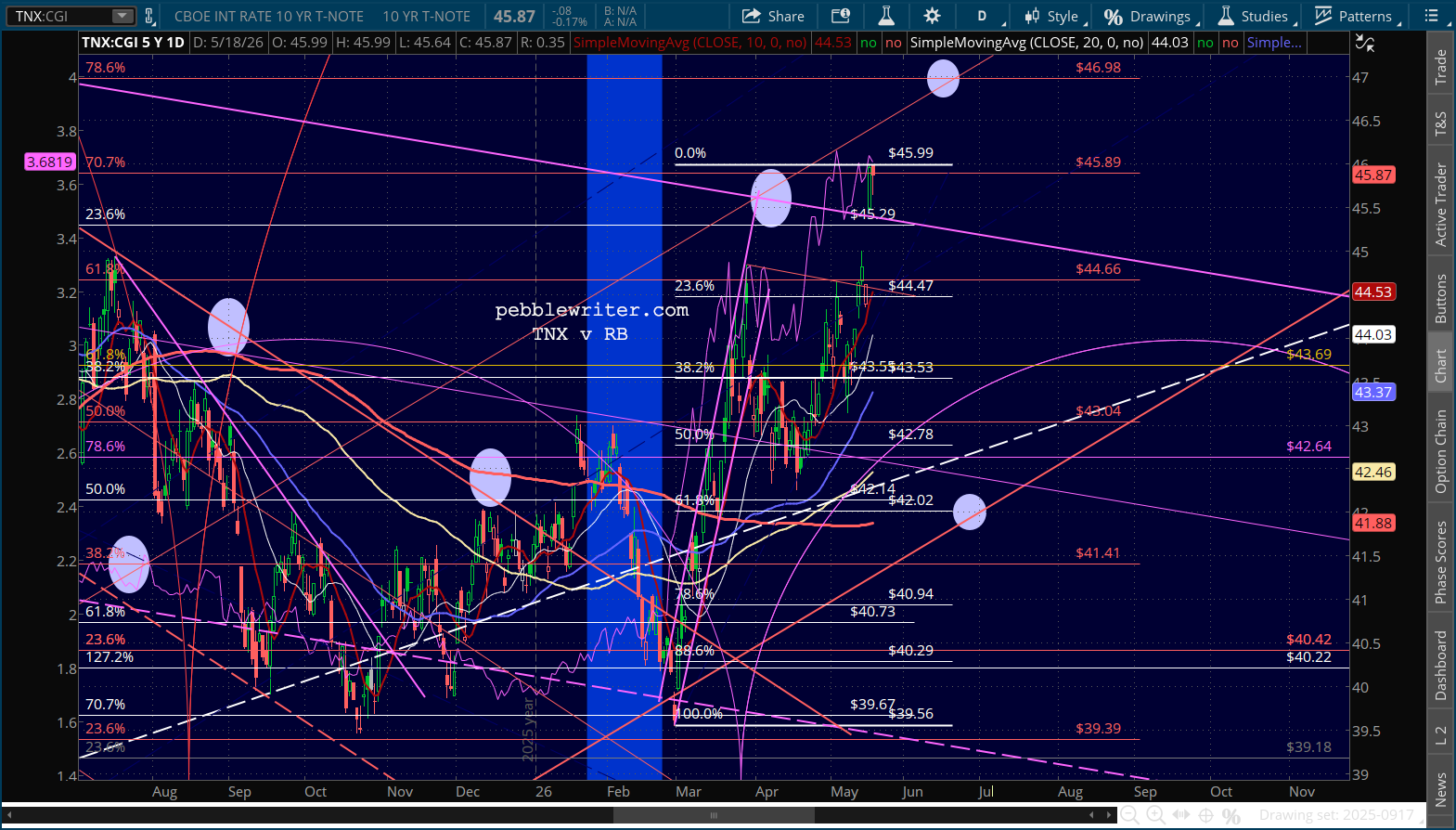

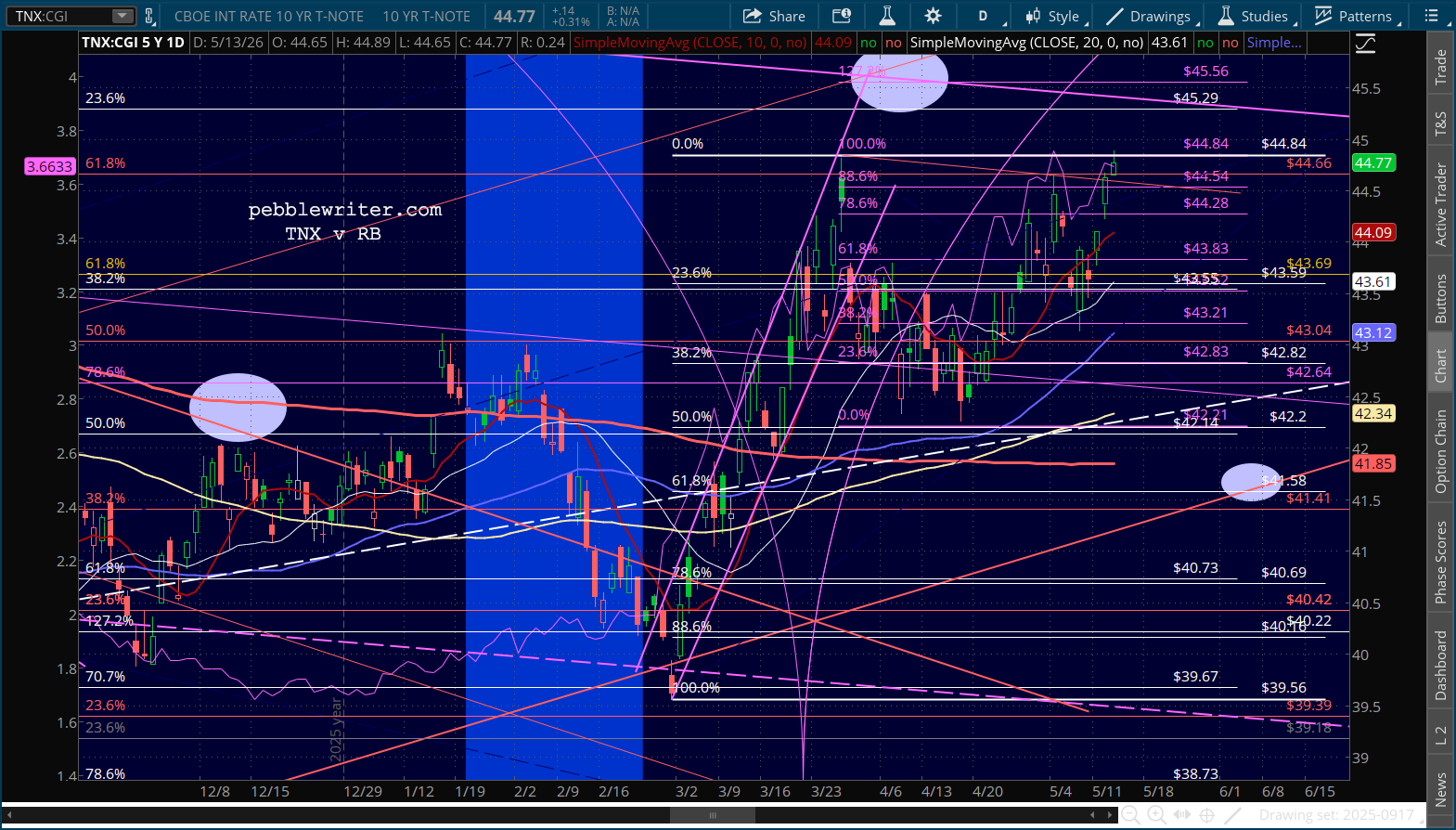

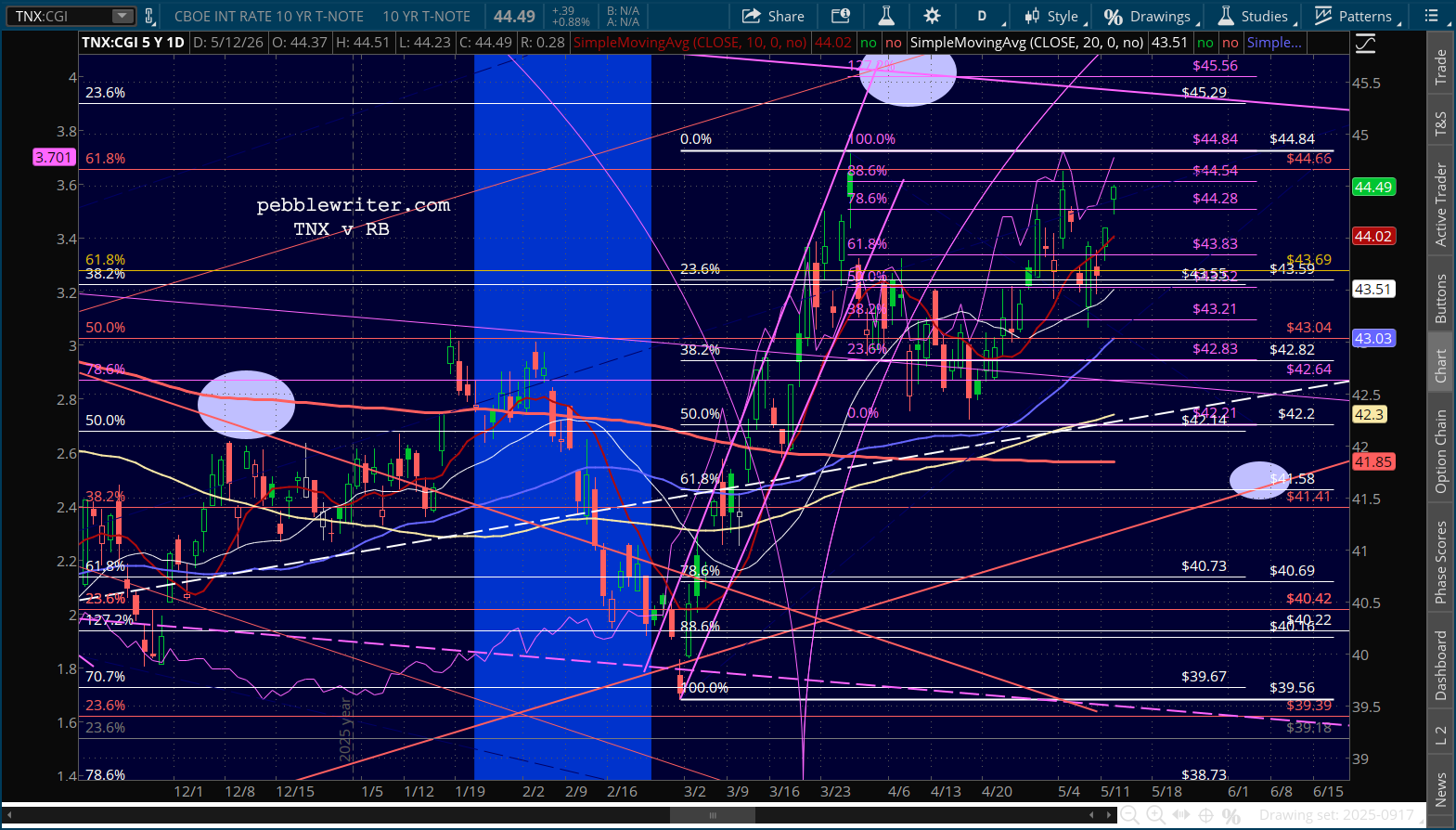

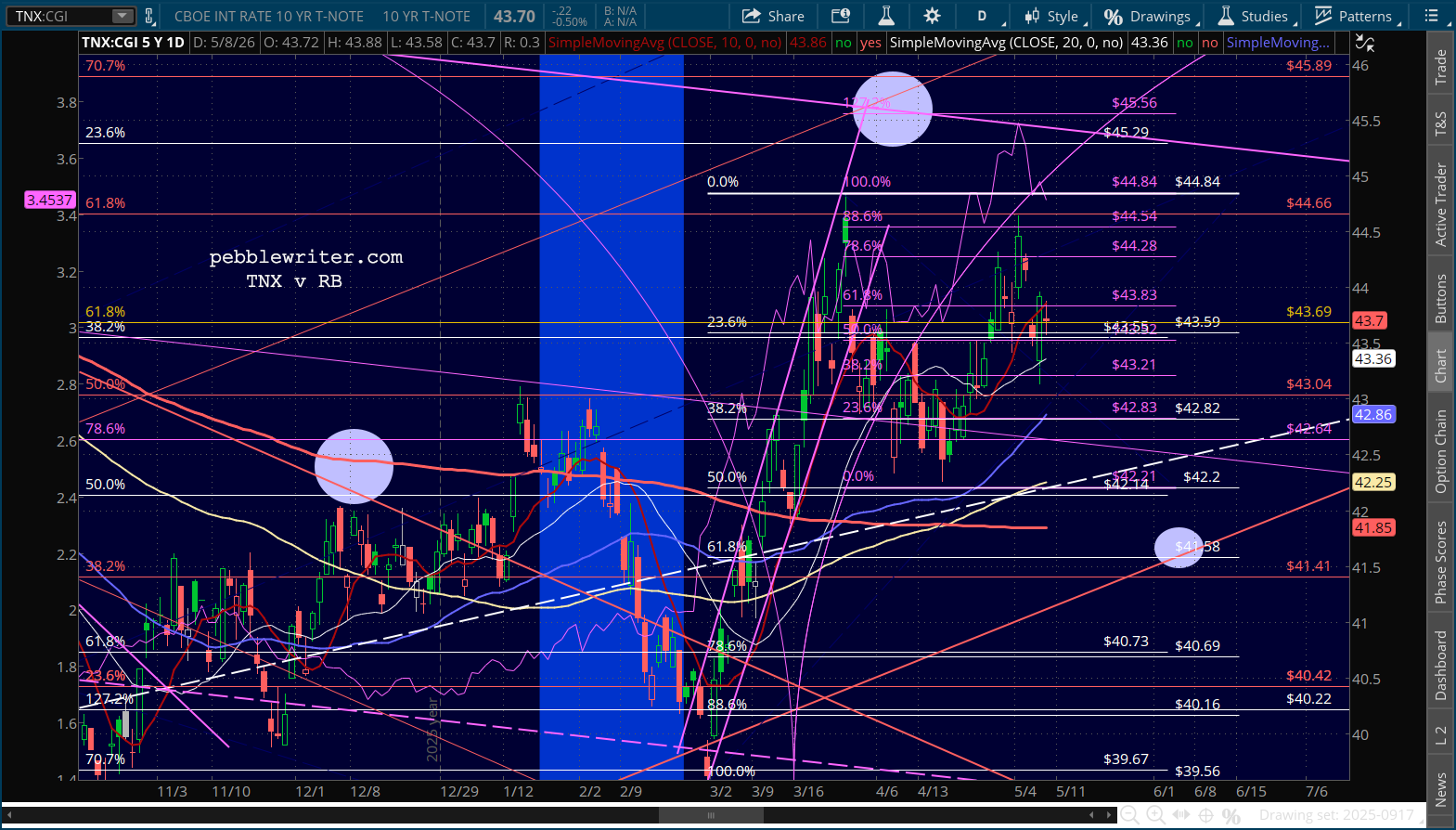

The 10Y has essentially reached our 4.7% target and could even reverse…

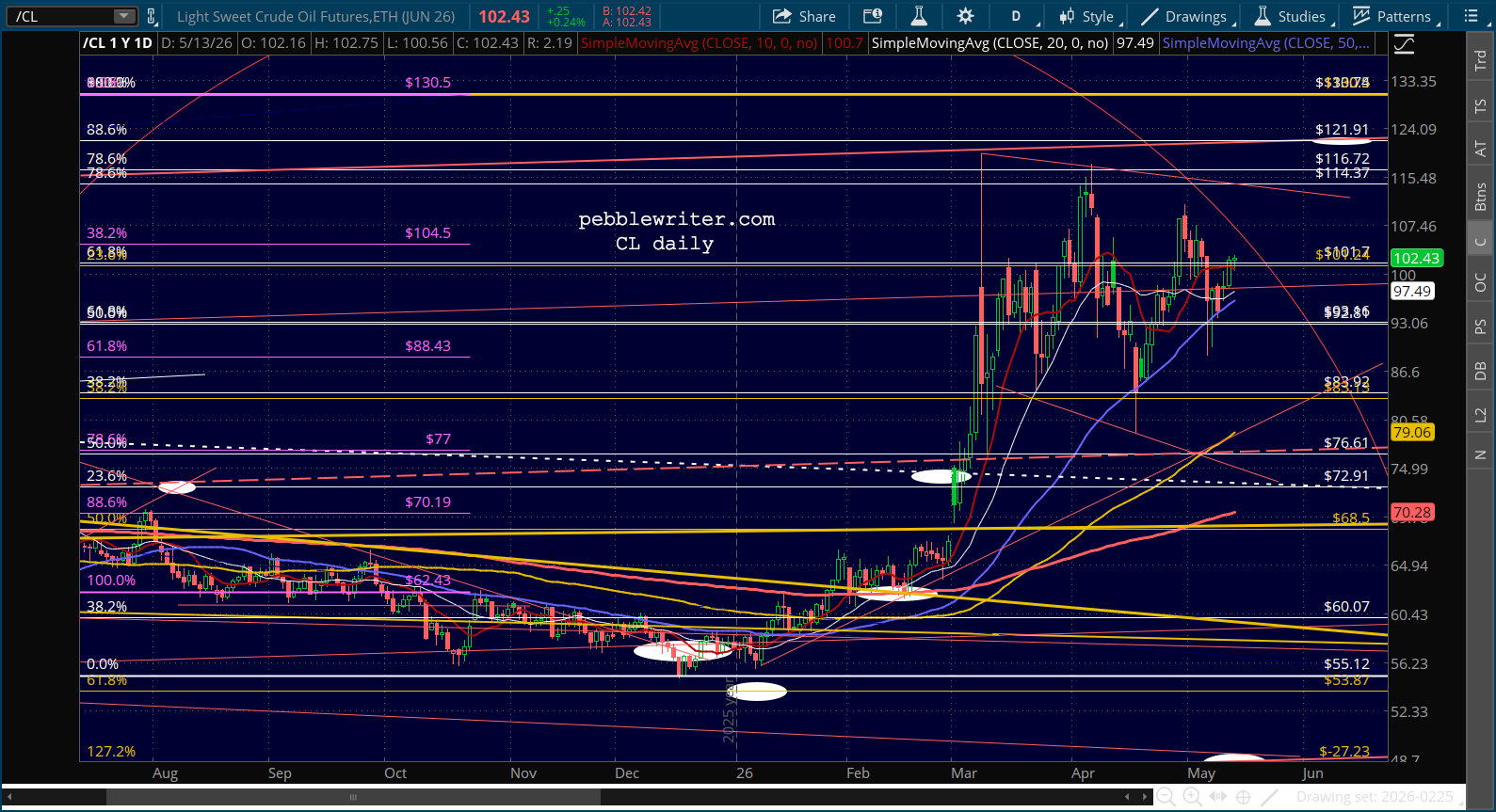

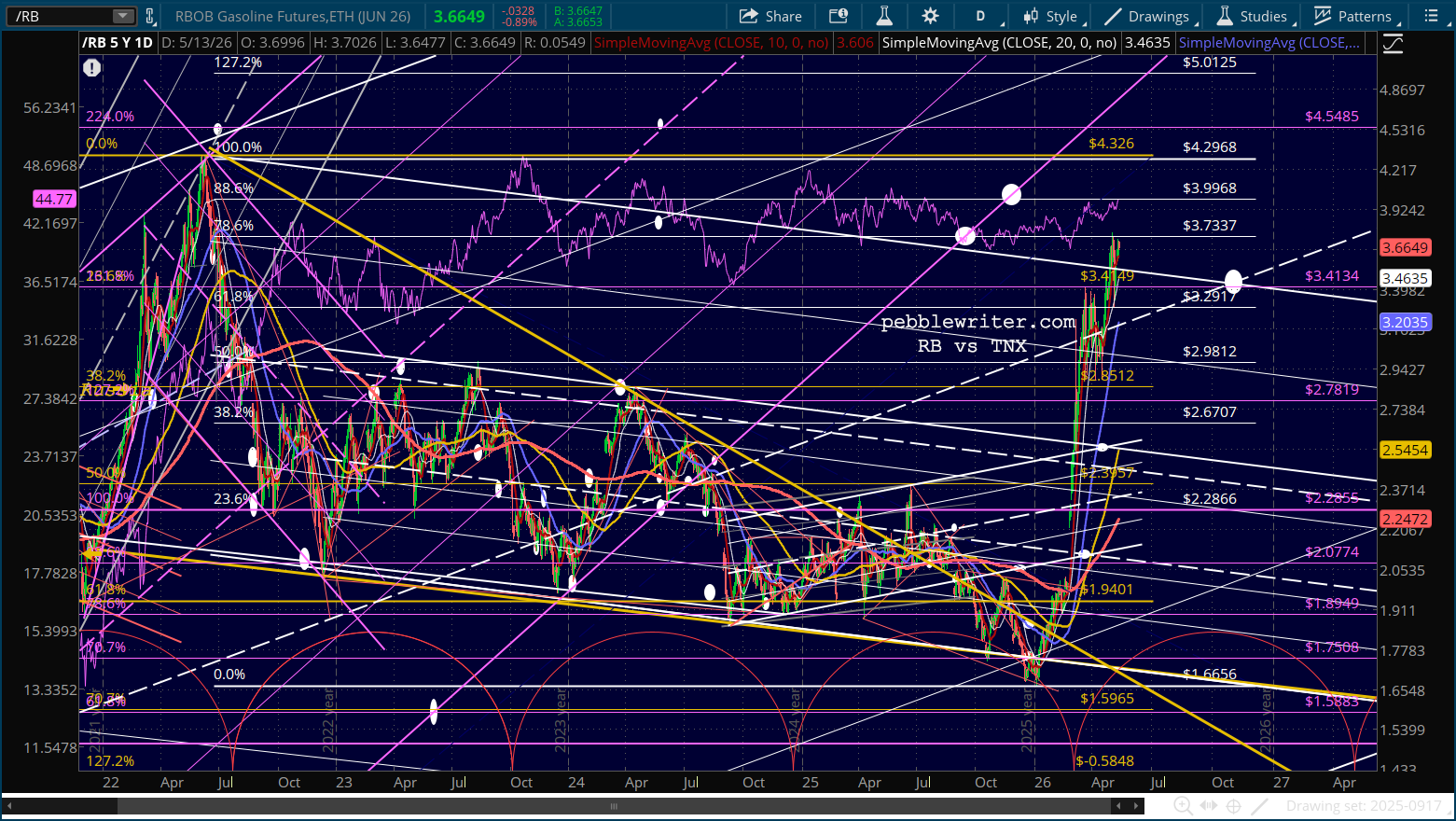

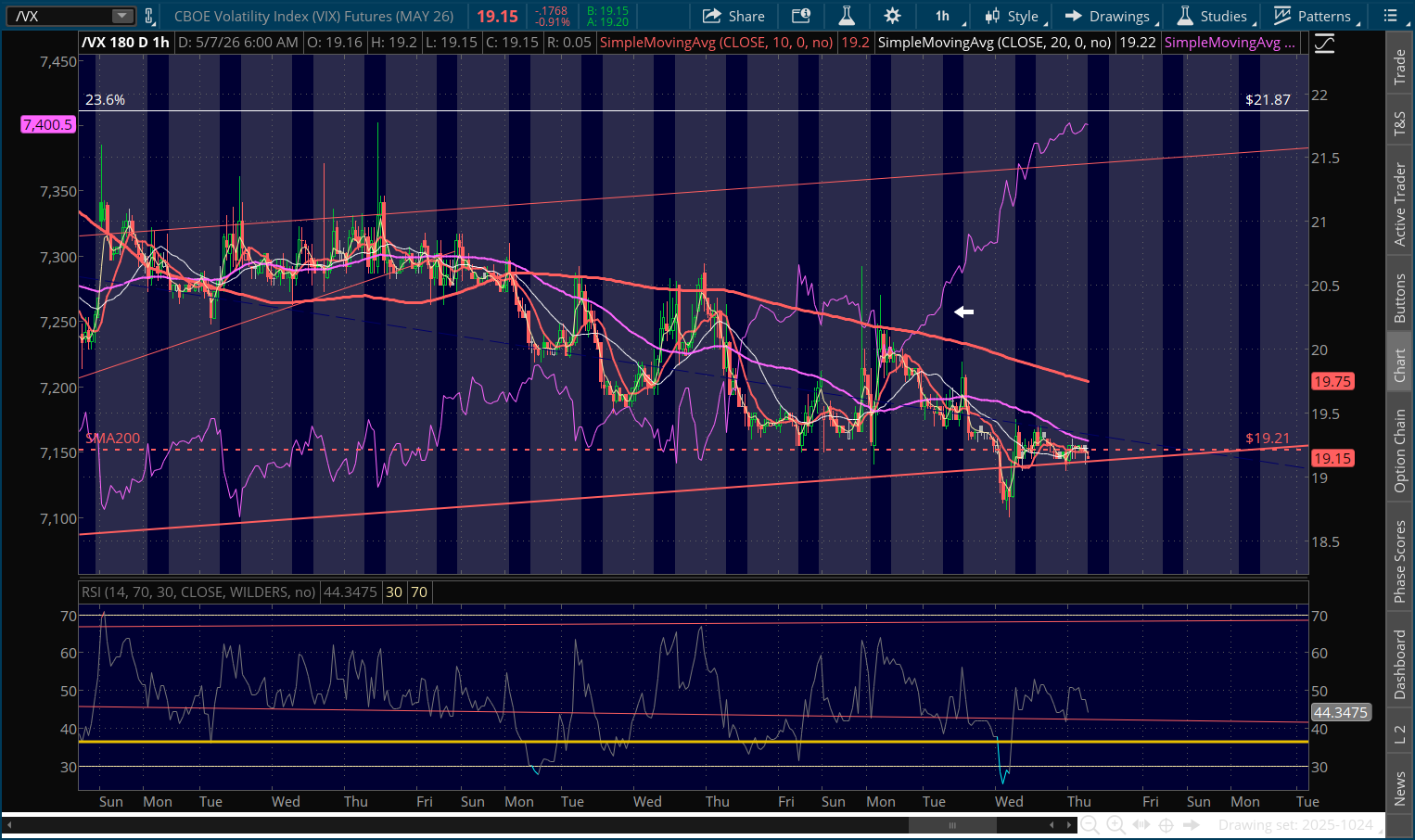

…if only oil prices would break down instead of out. The triangle has only one more day to play out – where the two trend lines converge – so we should know very soon.

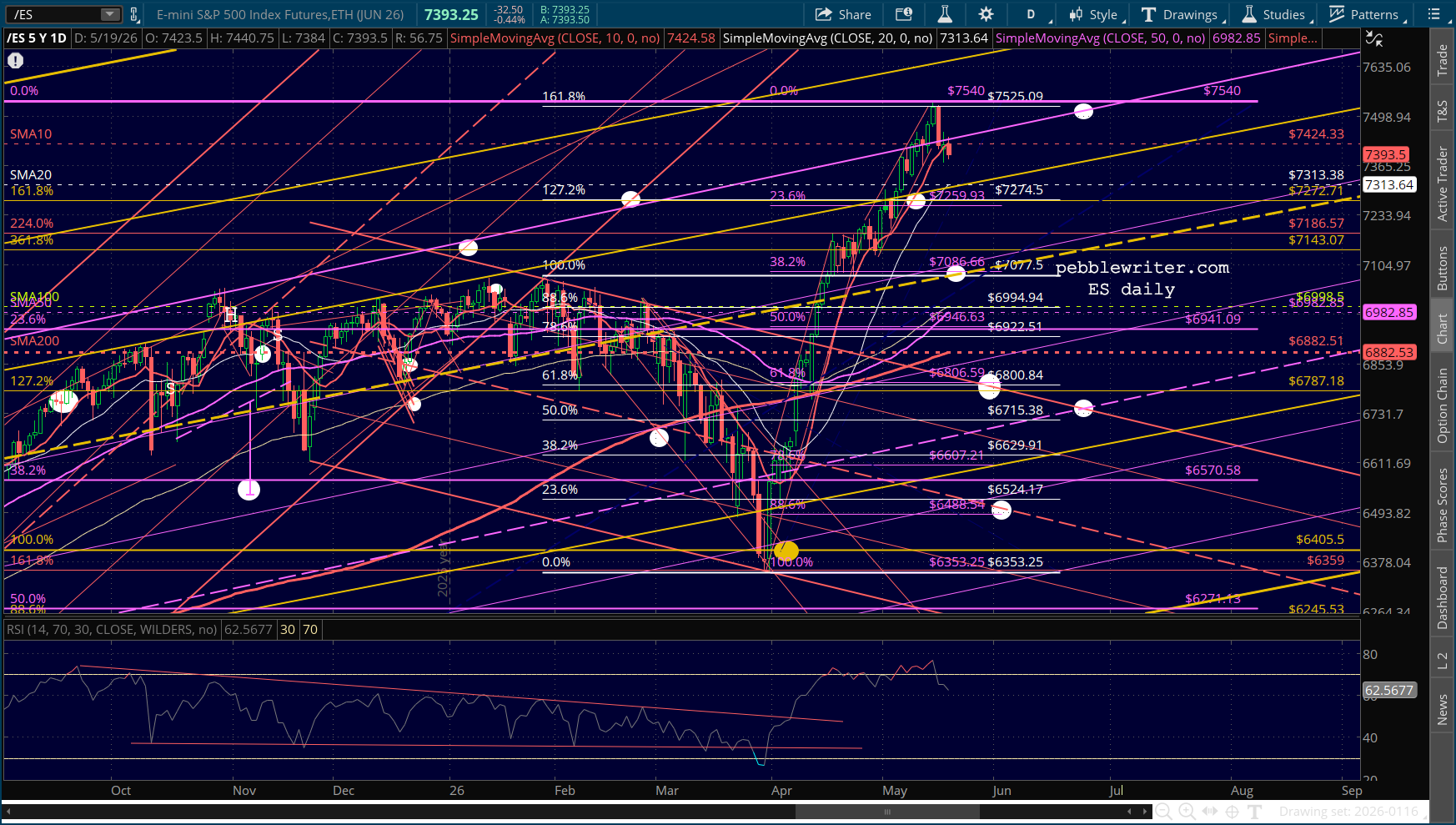

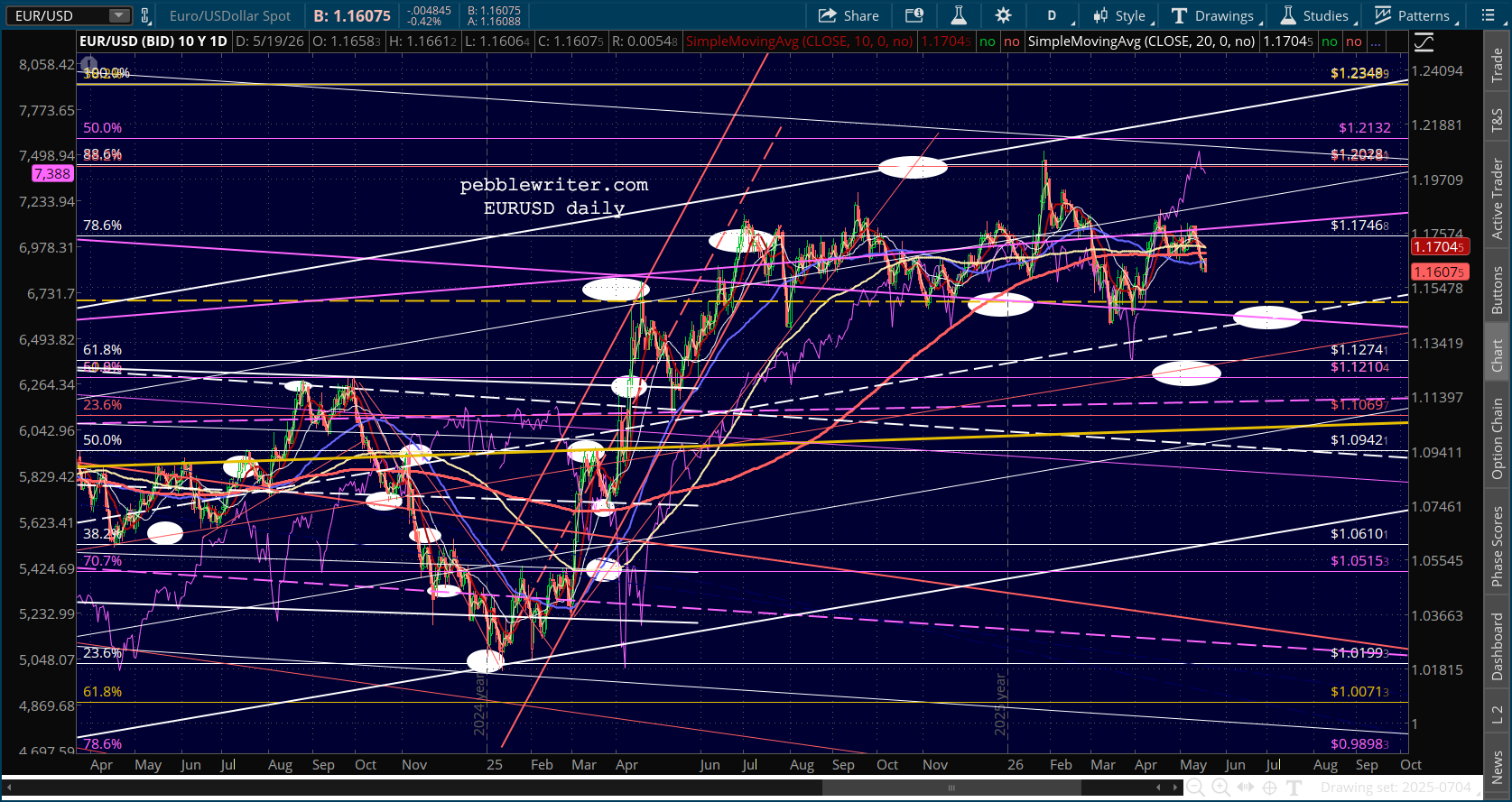

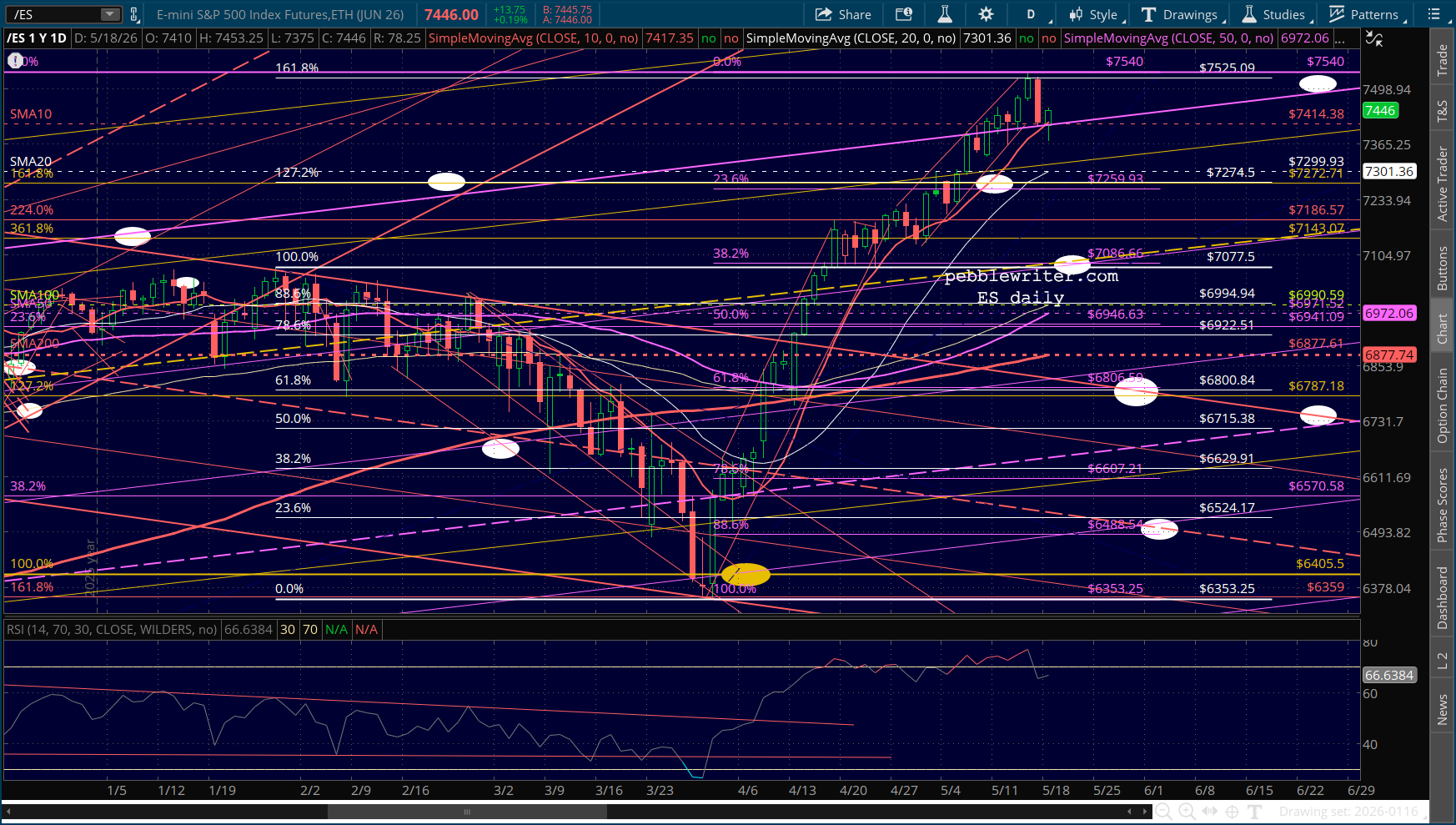

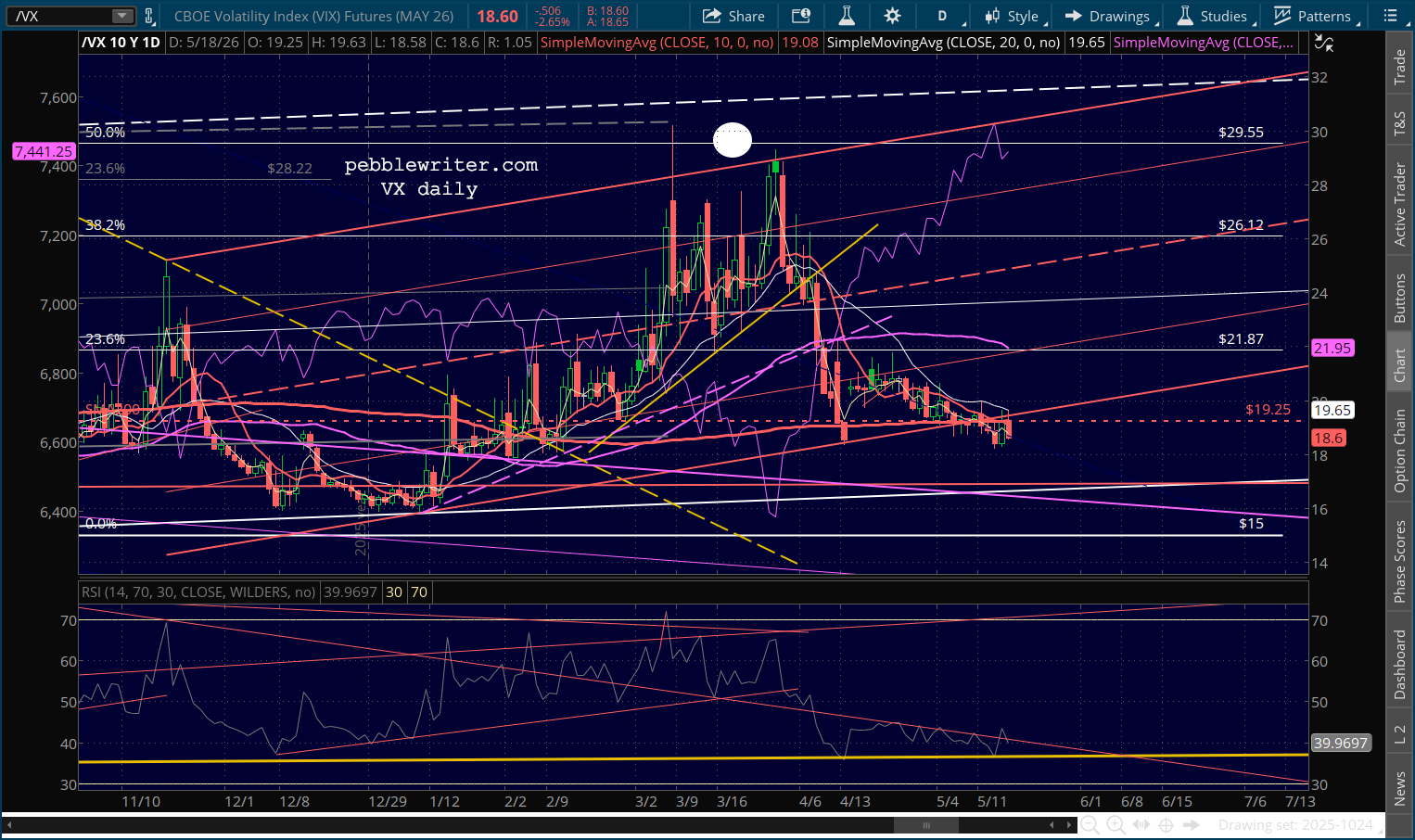

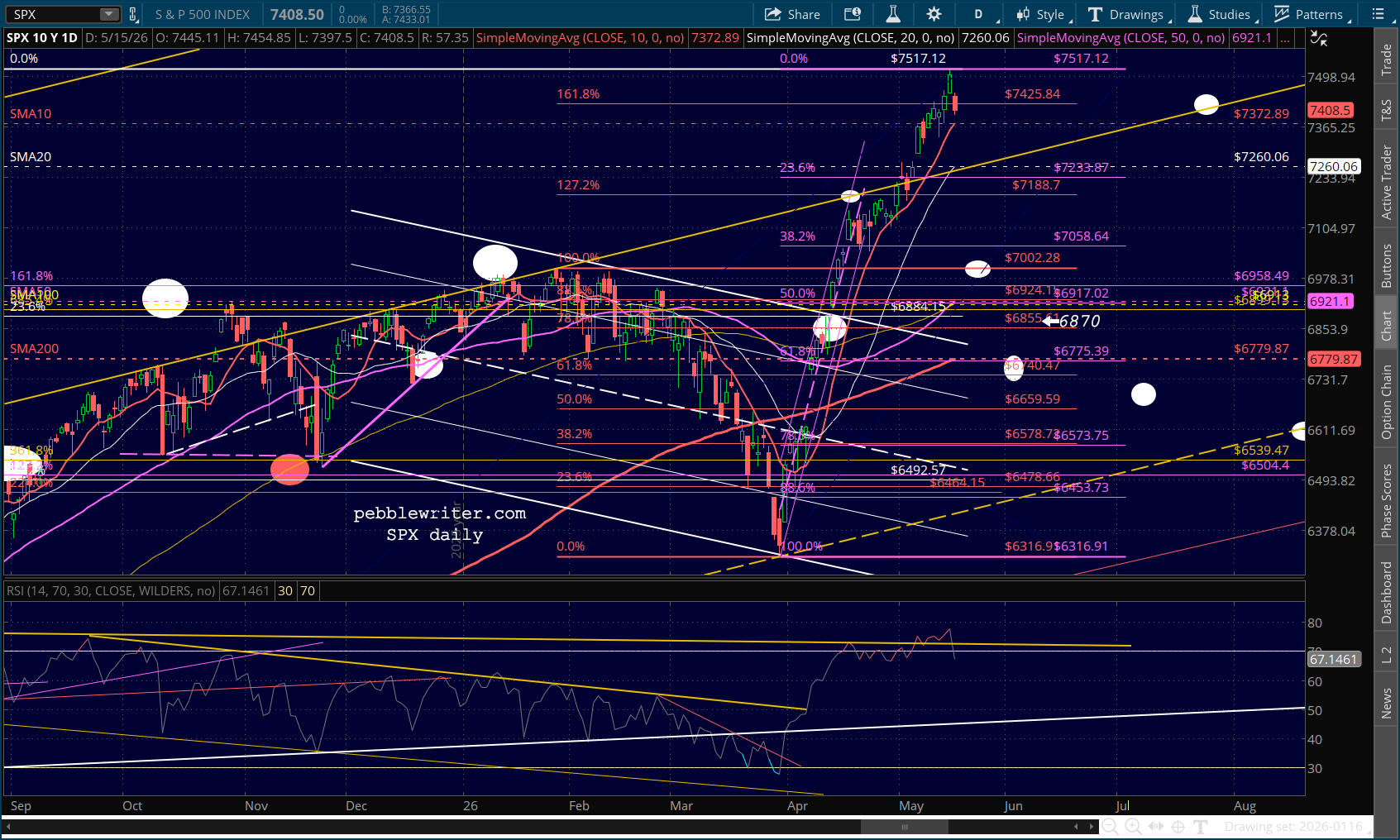

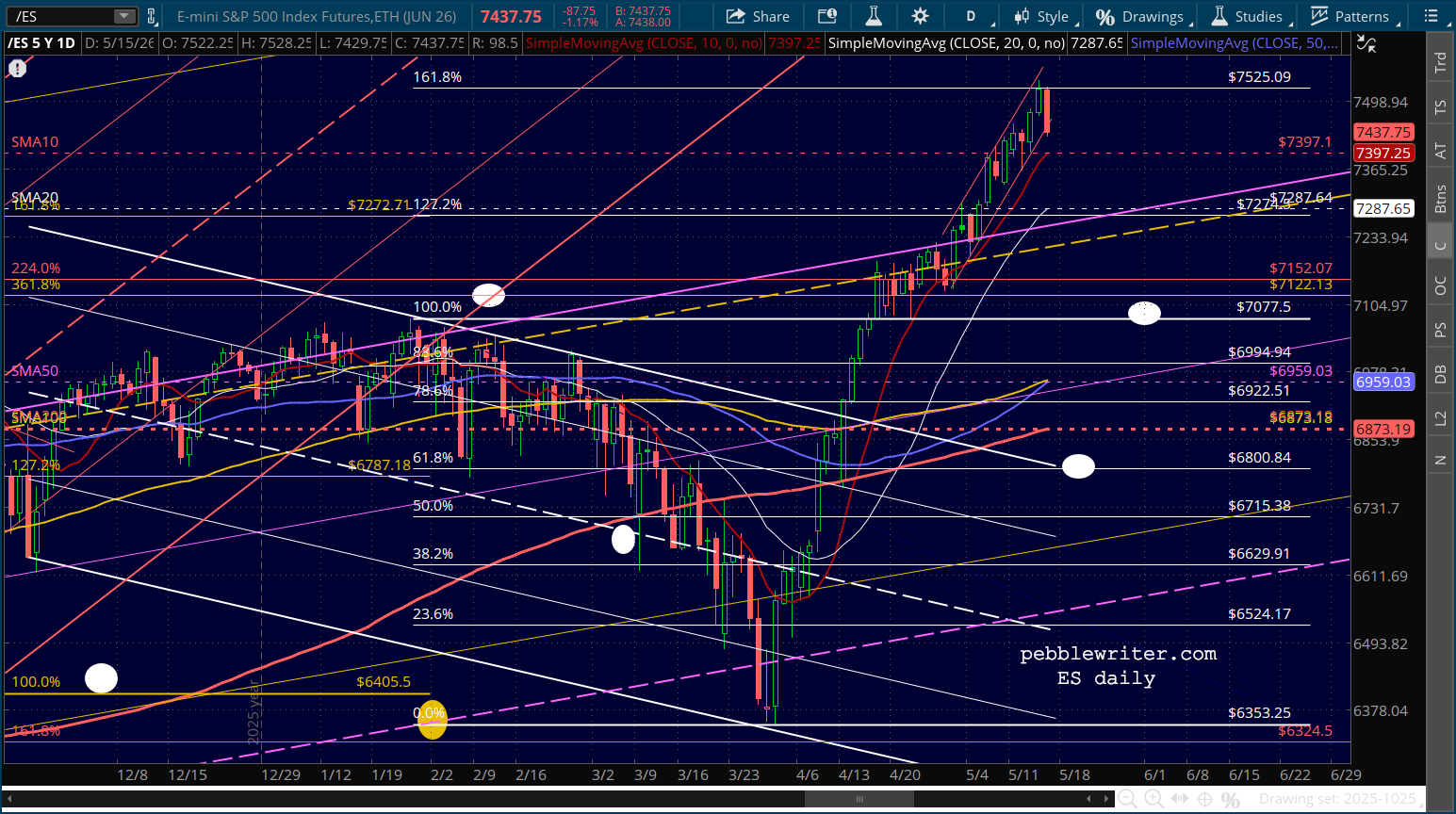

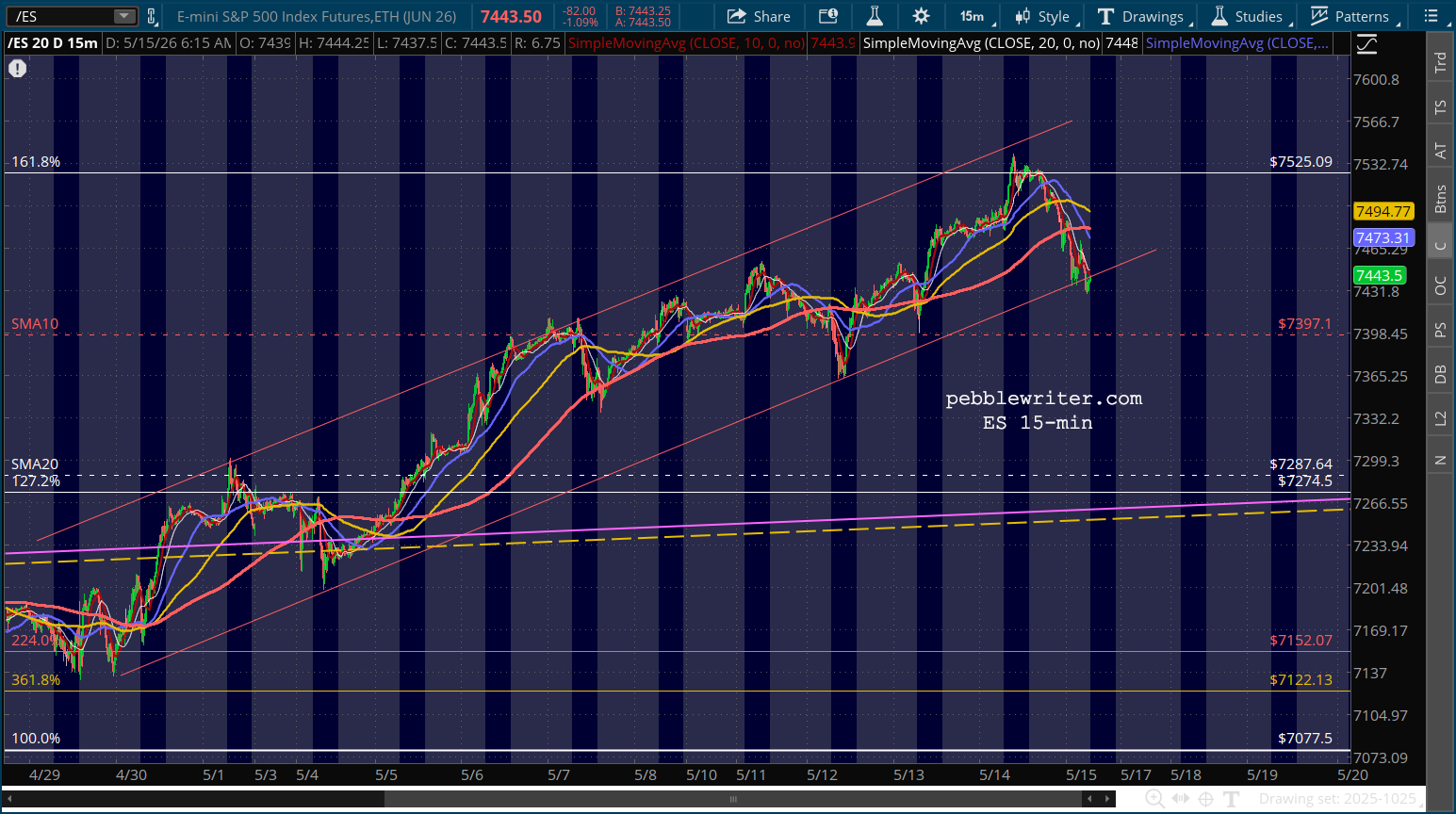

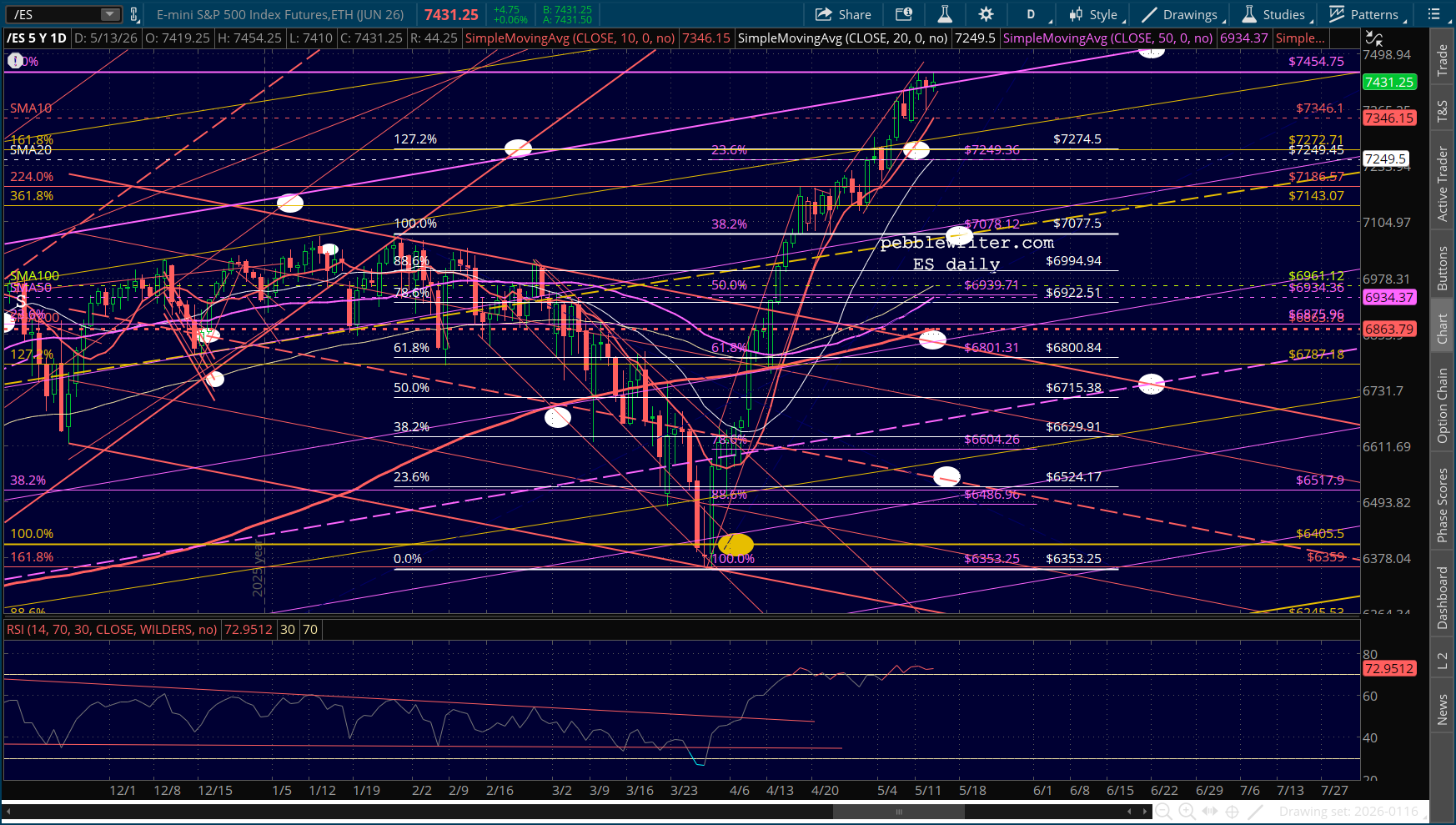

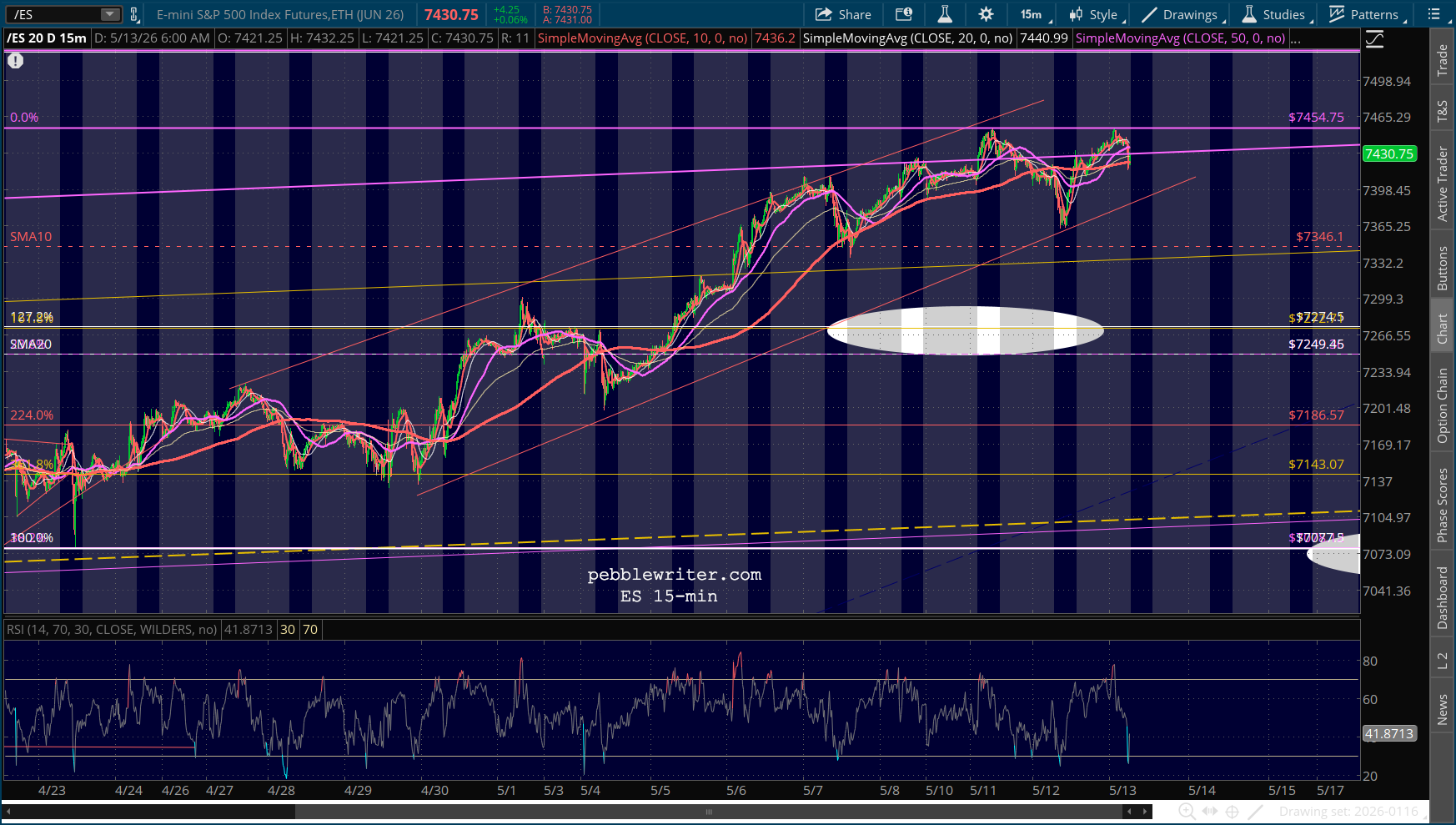

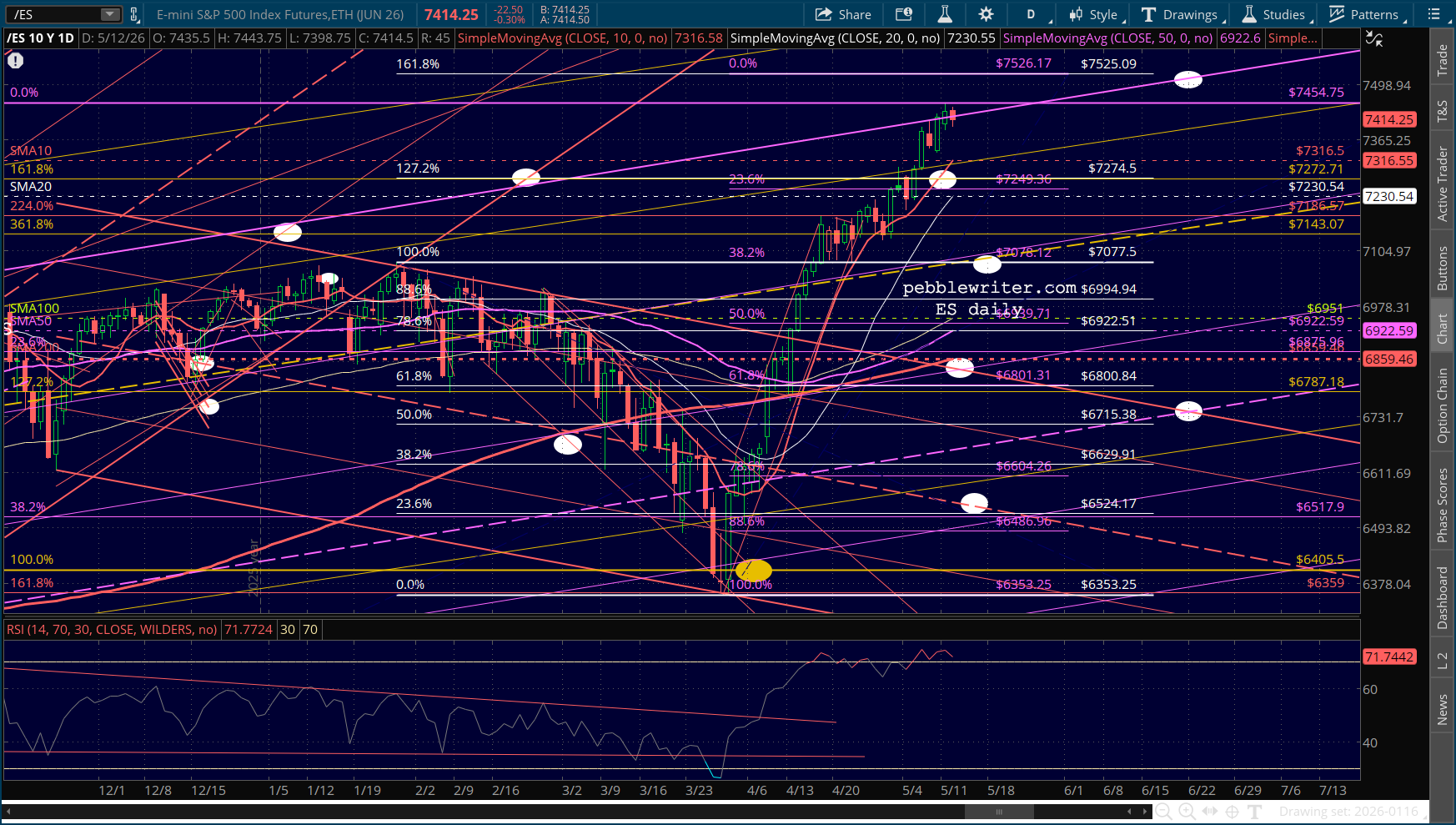

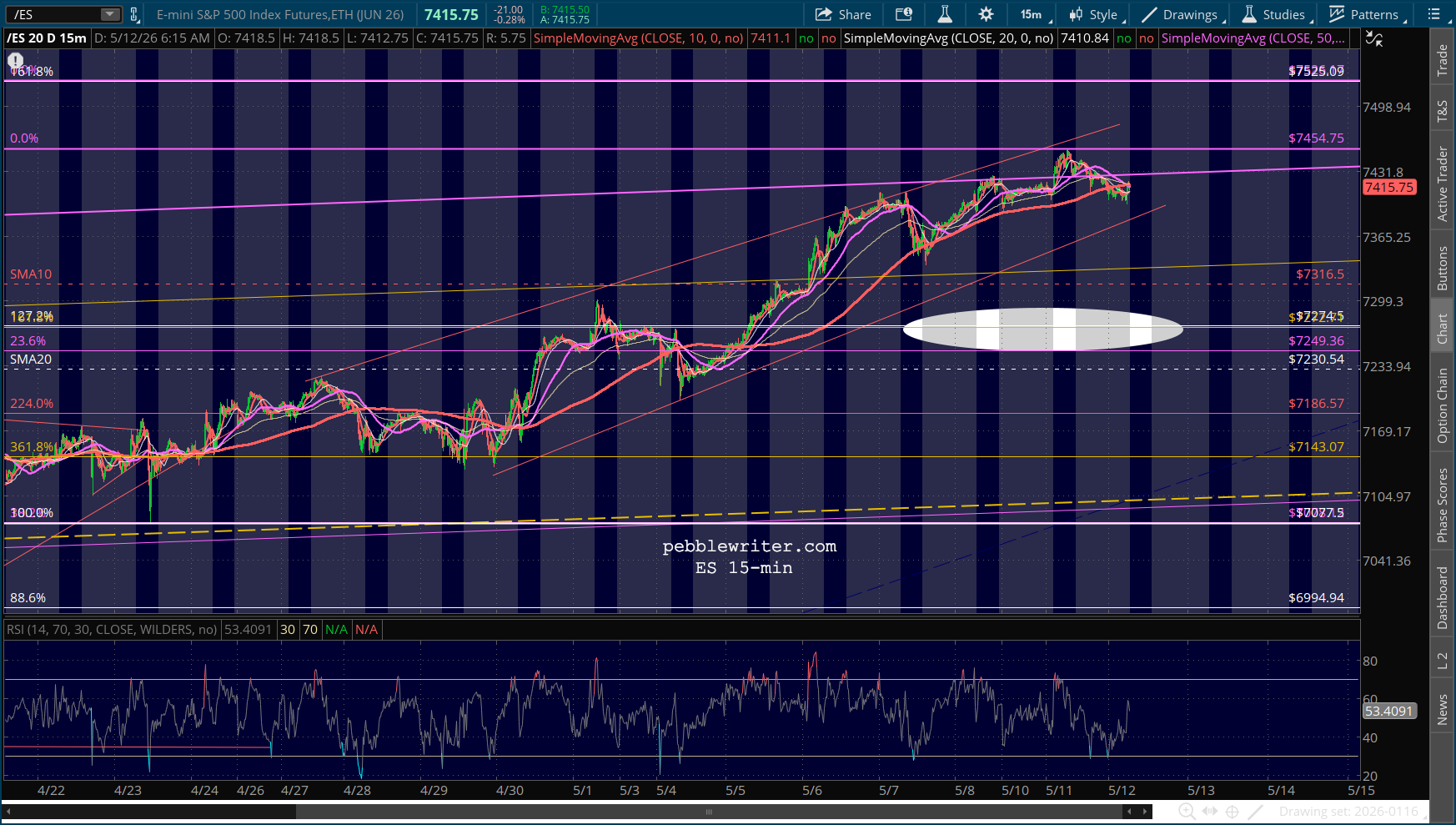

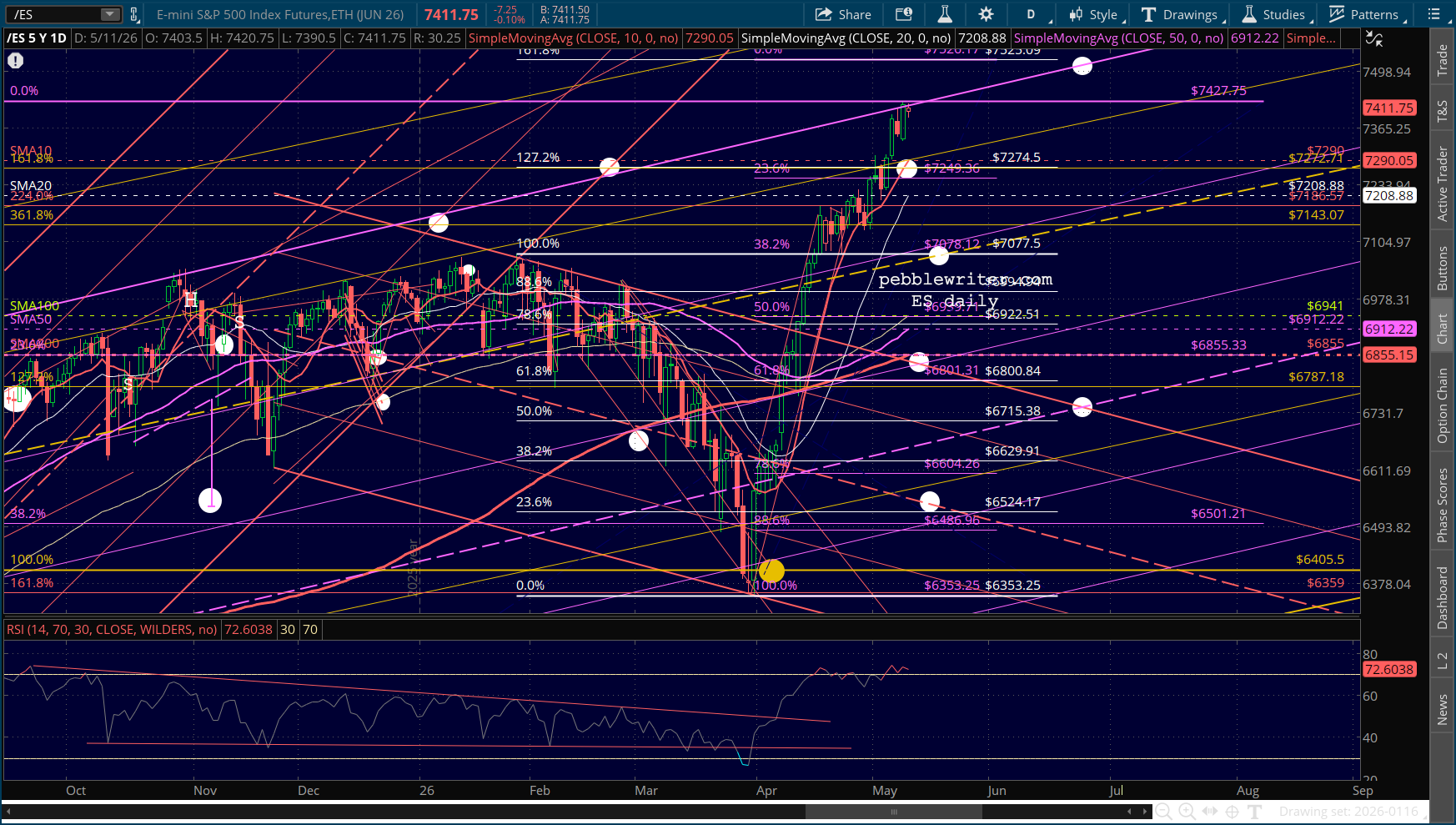

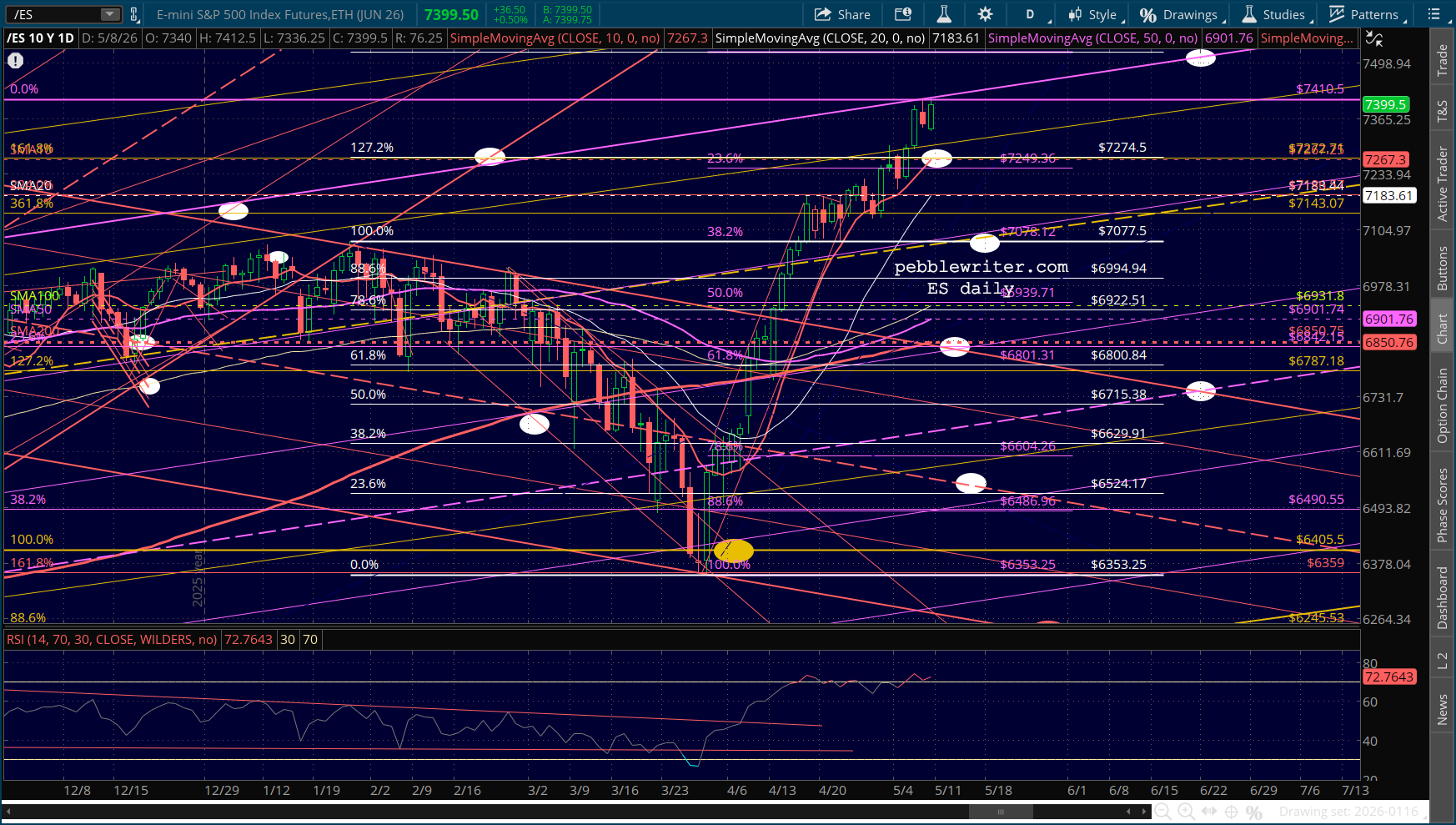

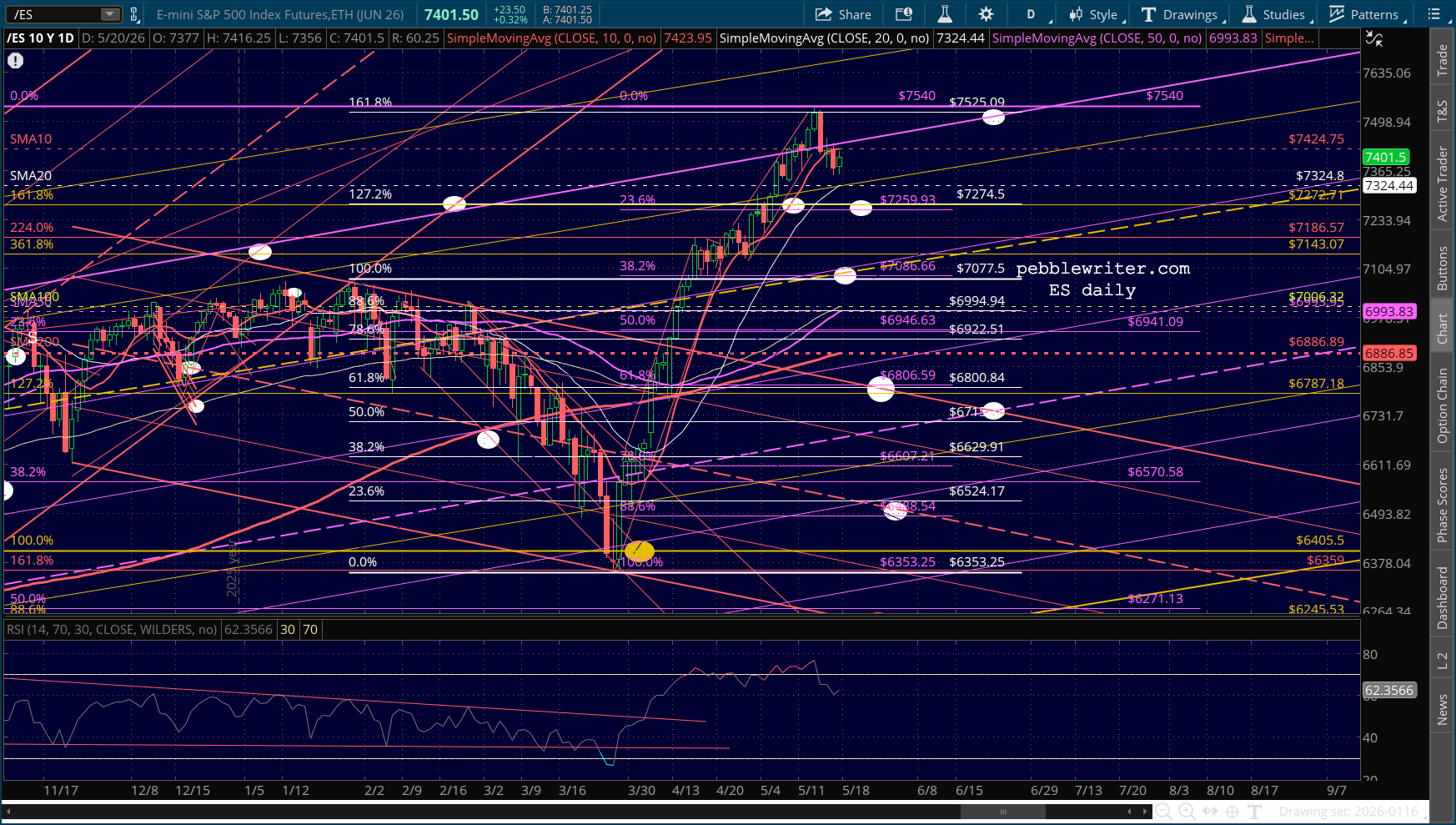

Futures are hanging onto a modest ramp job as we approach the open.

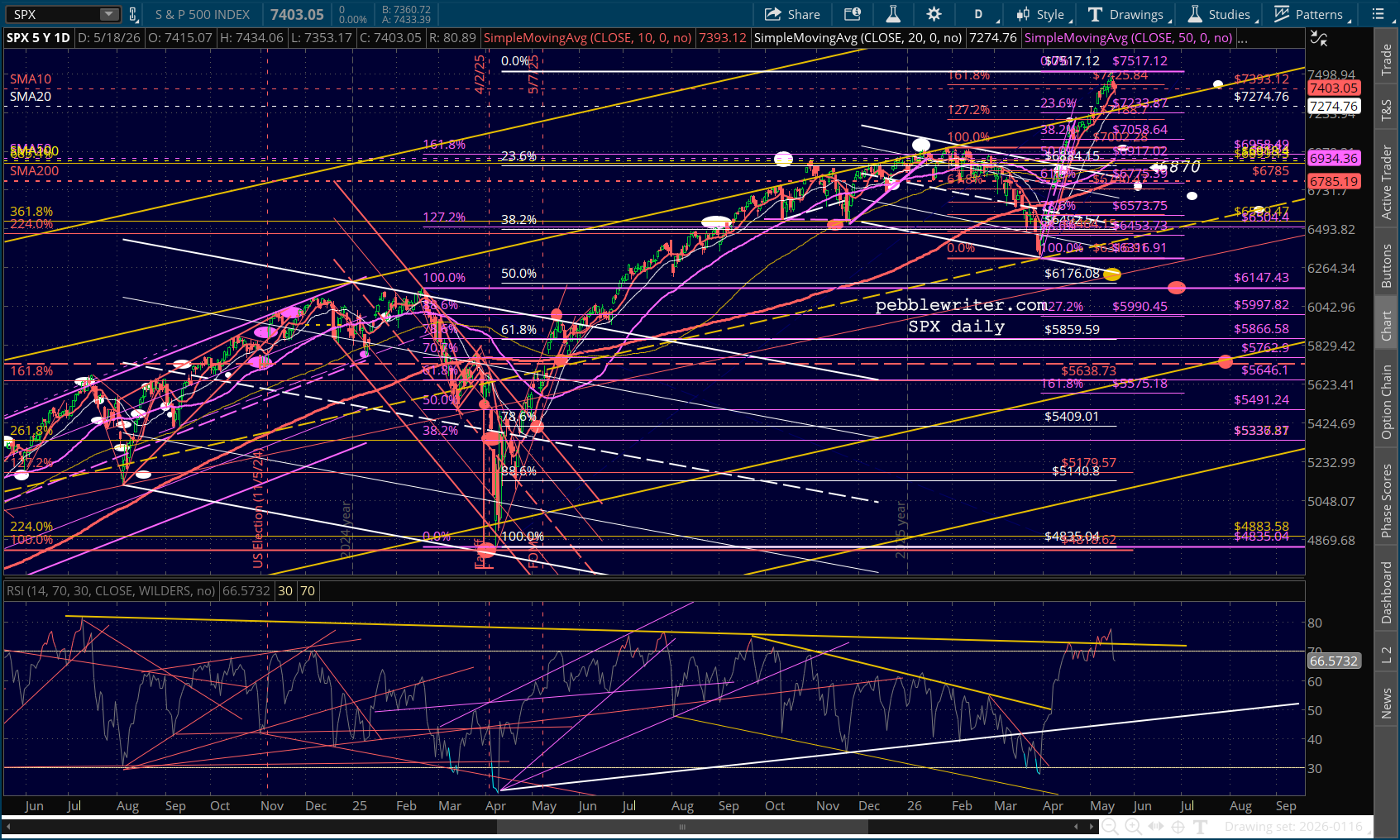

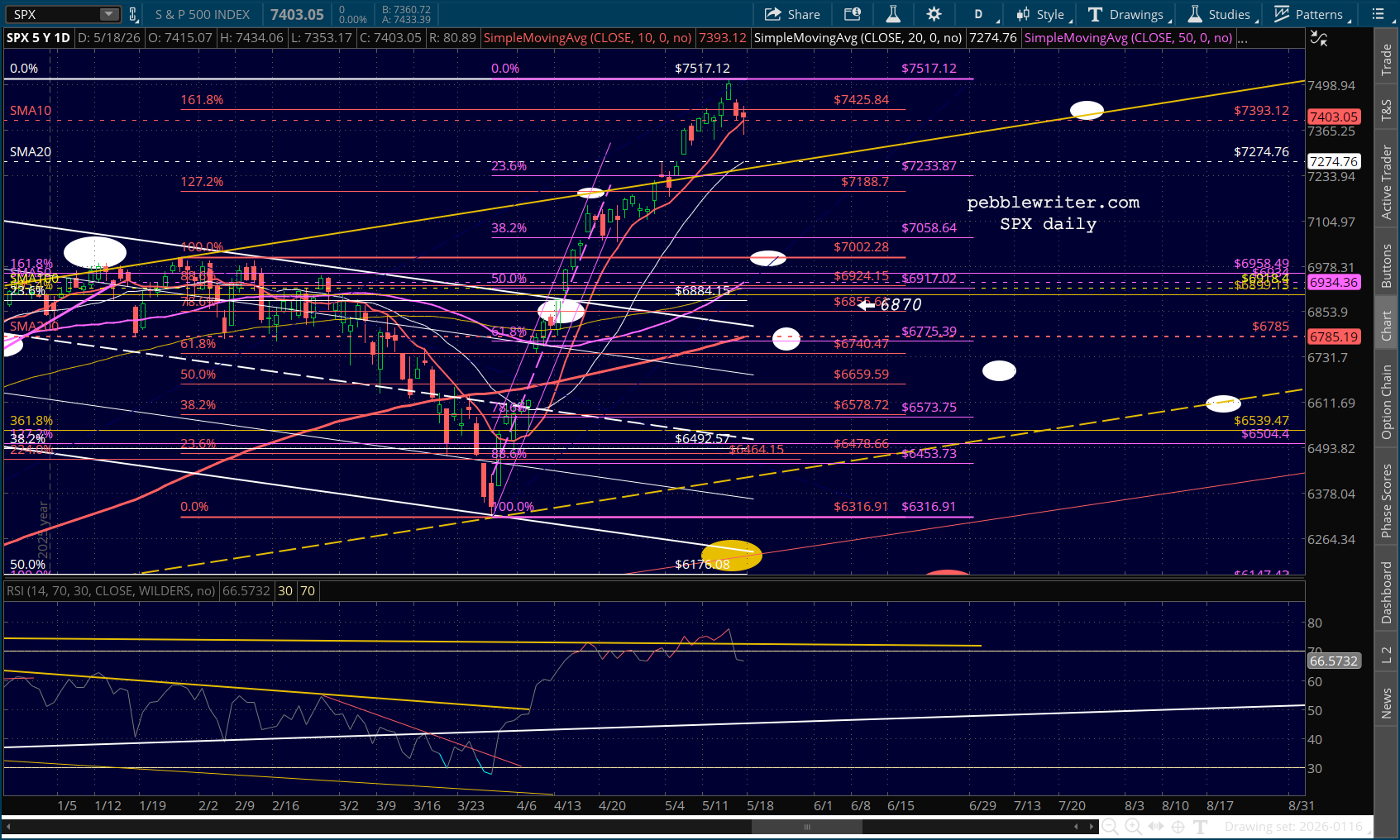

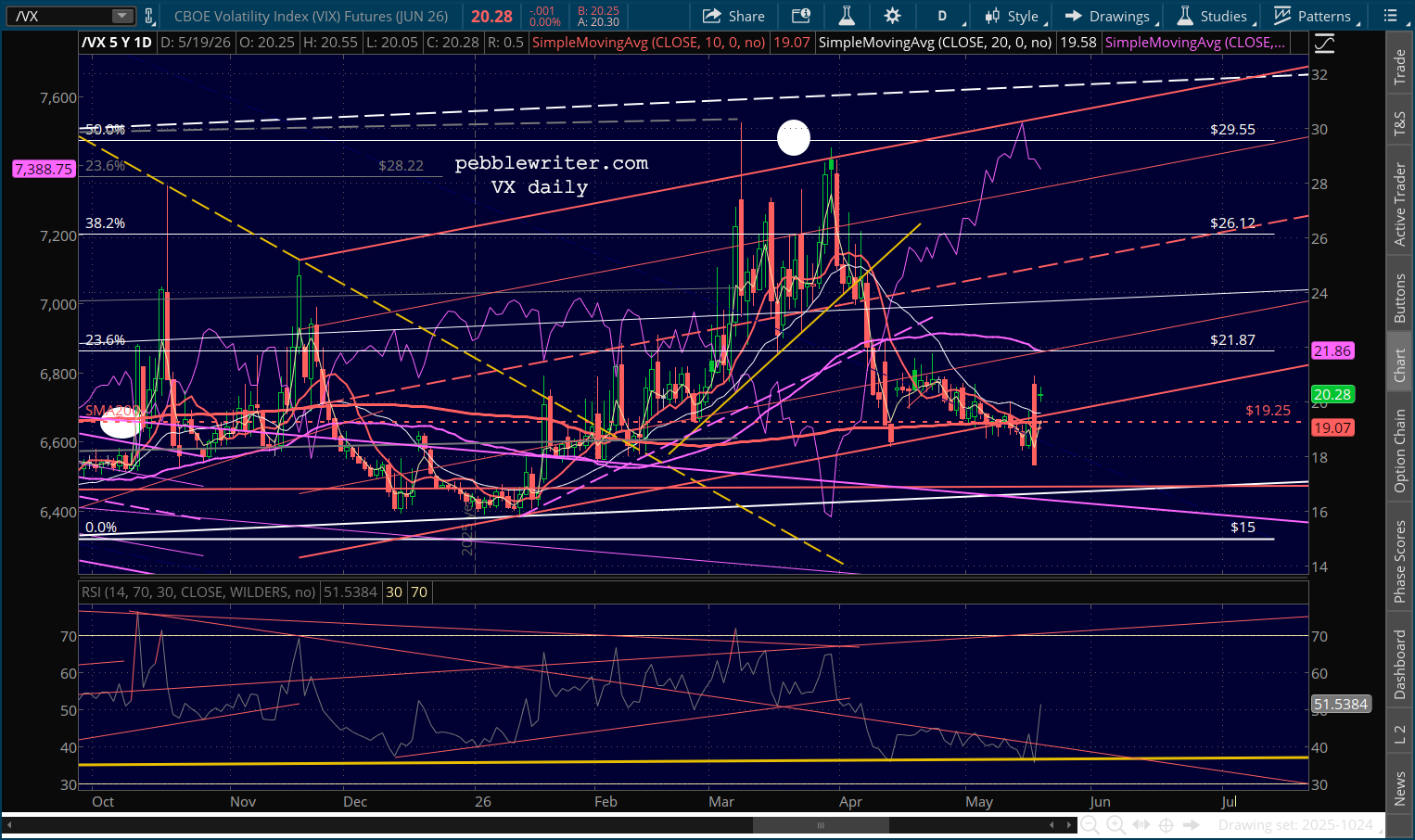

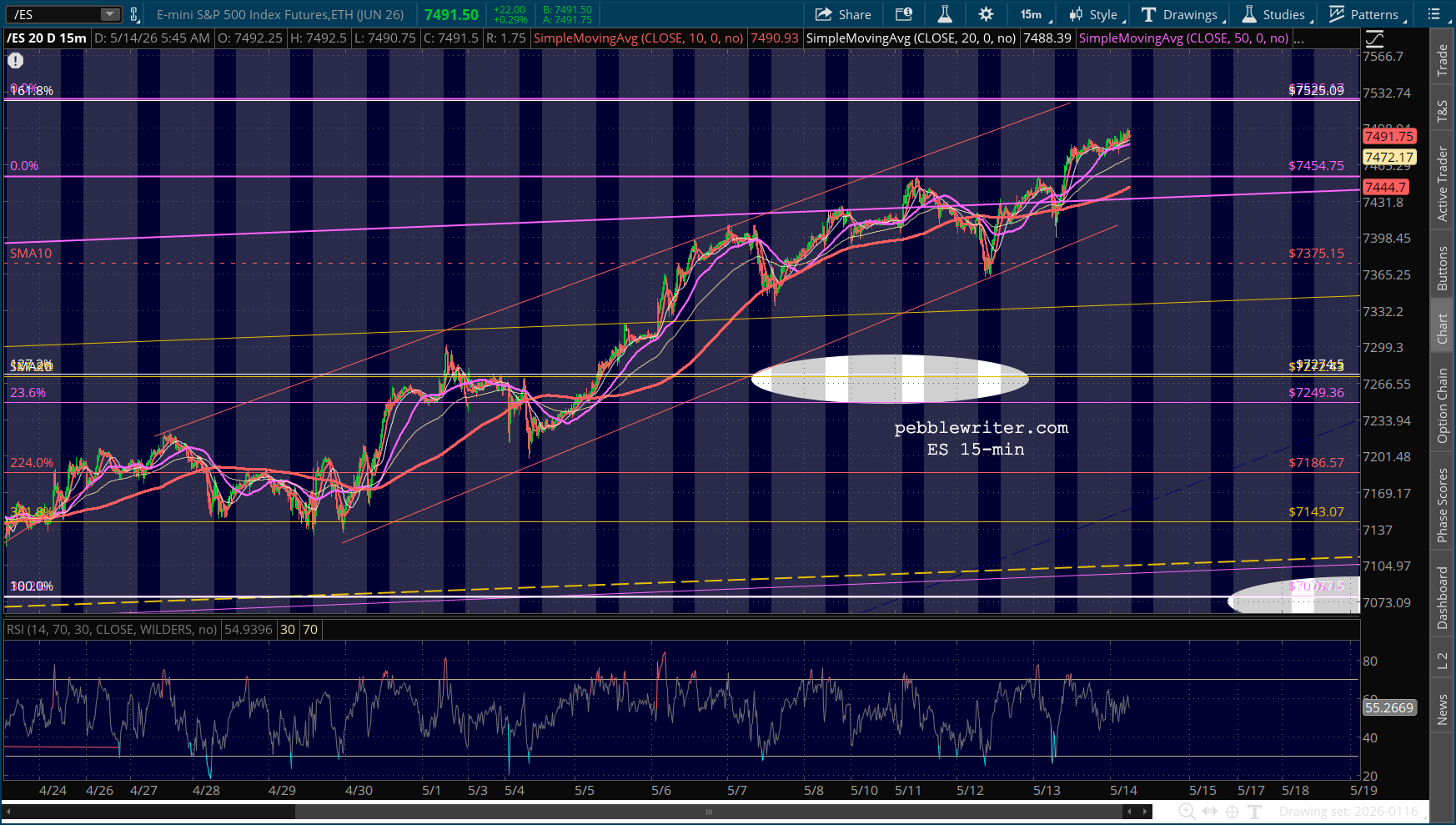

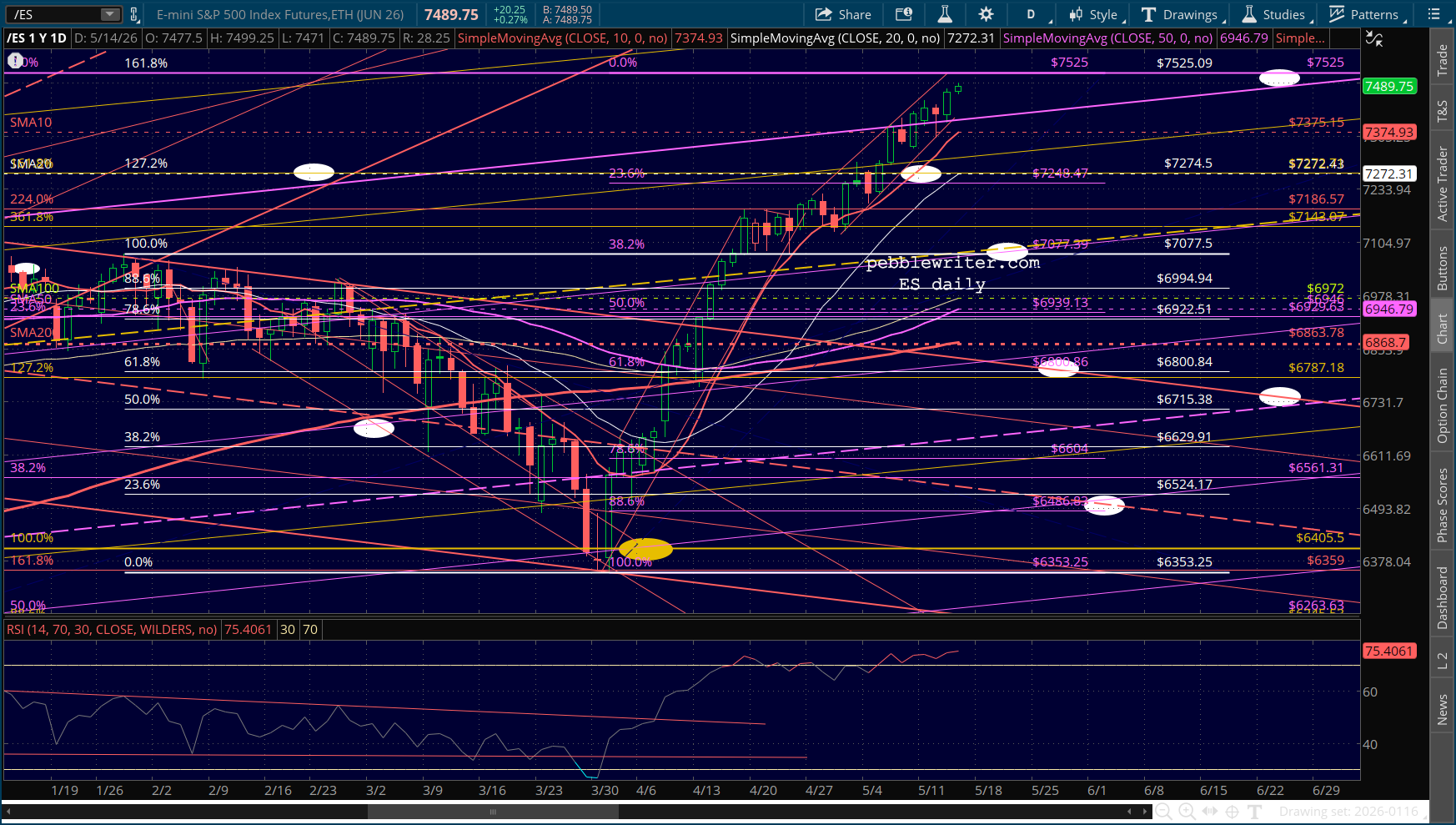

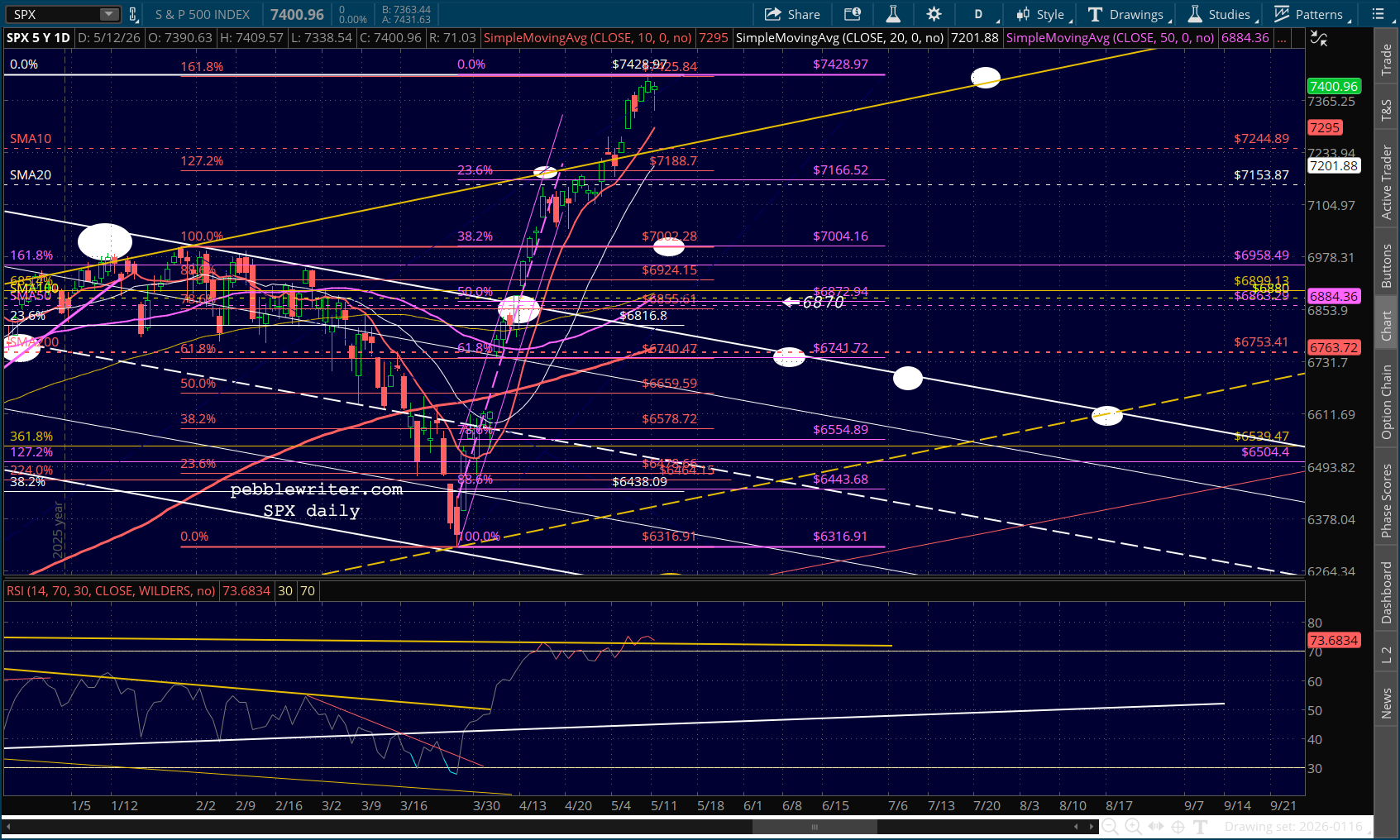

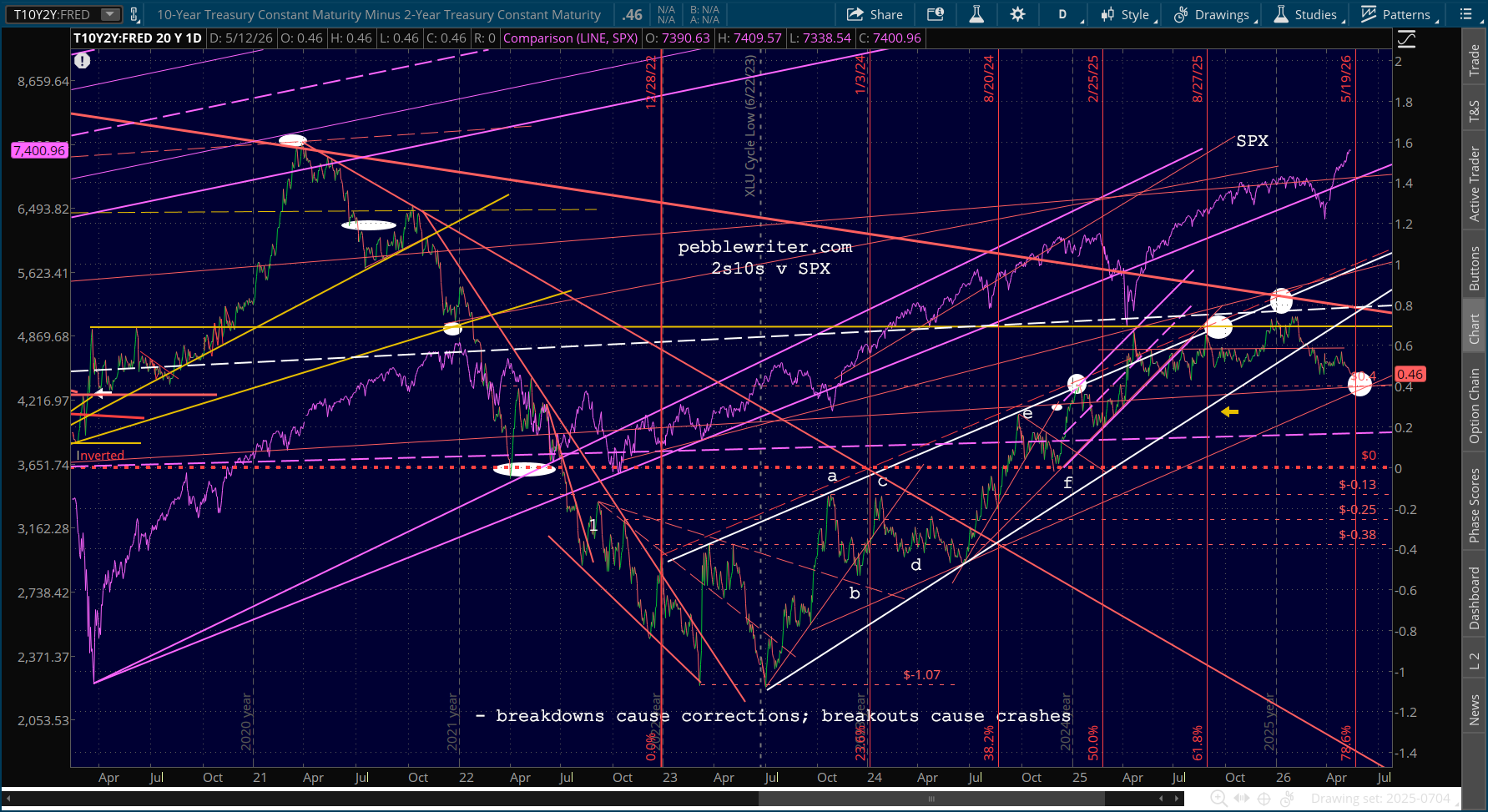

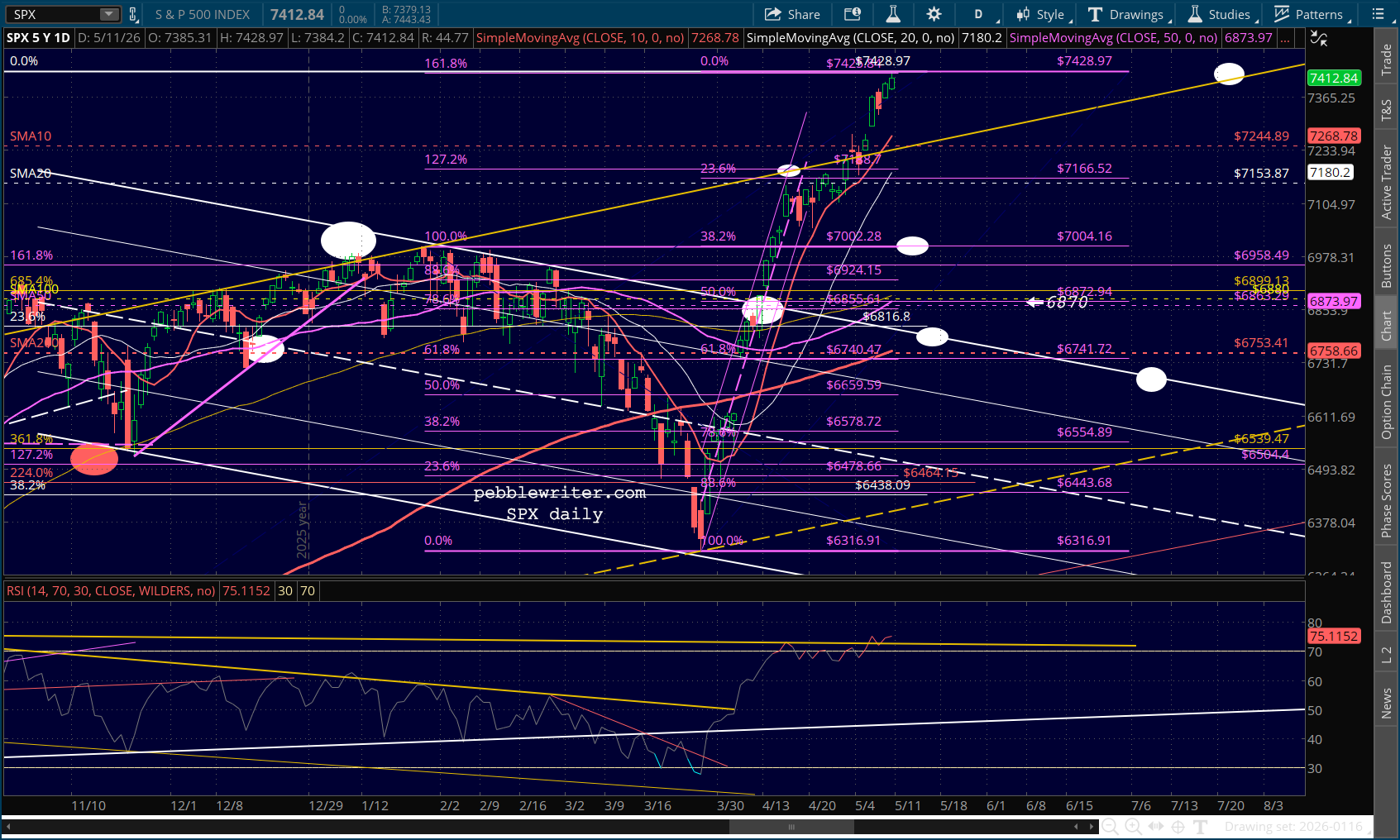

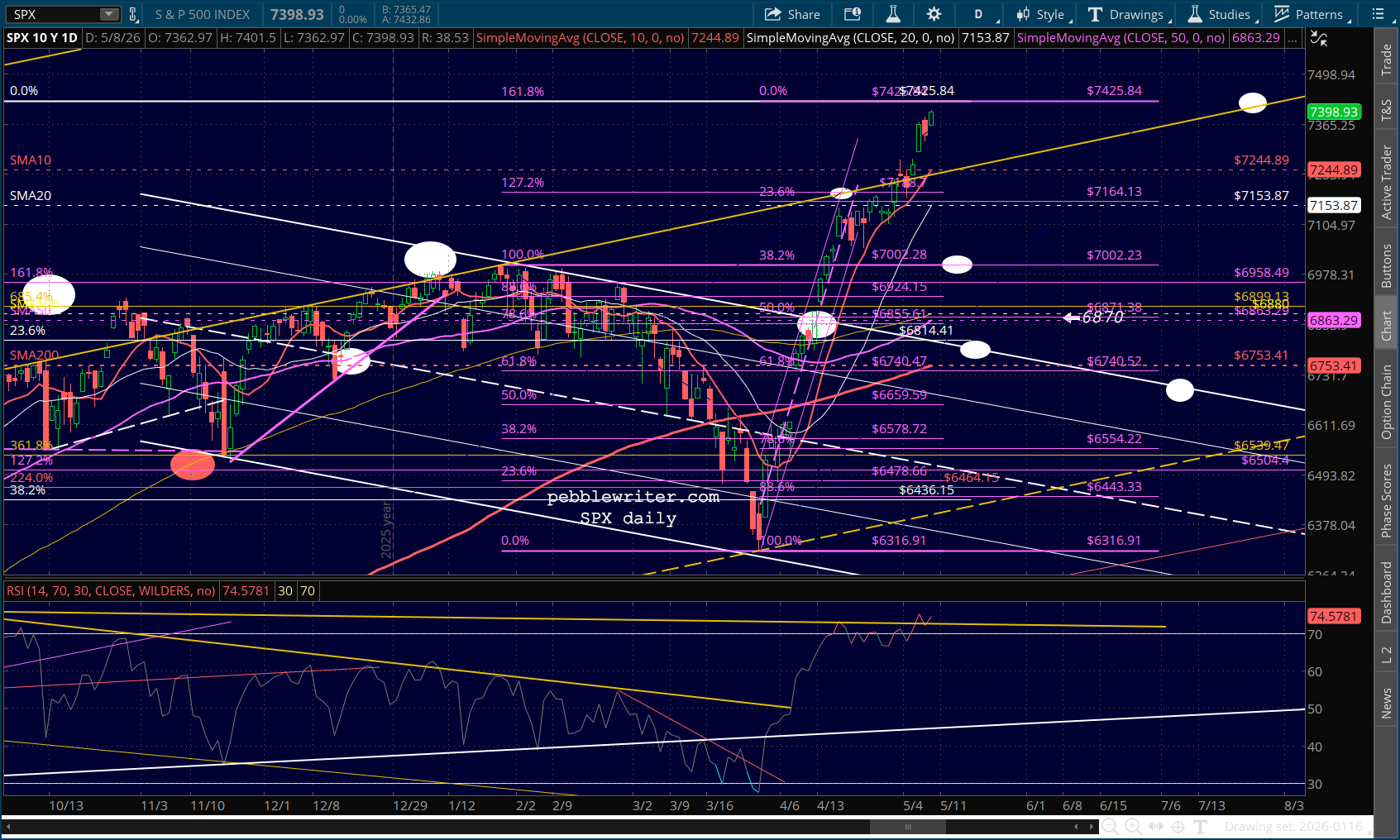

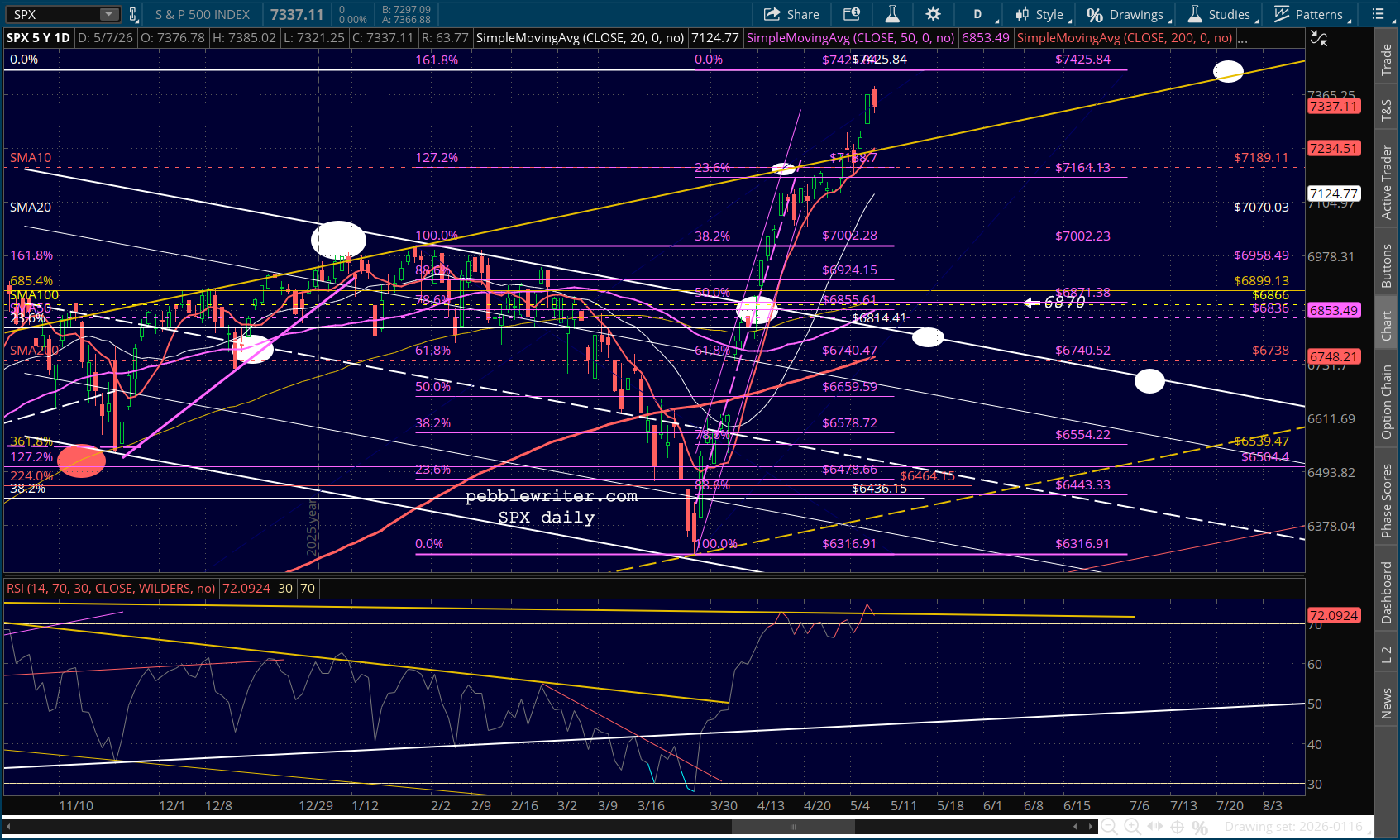

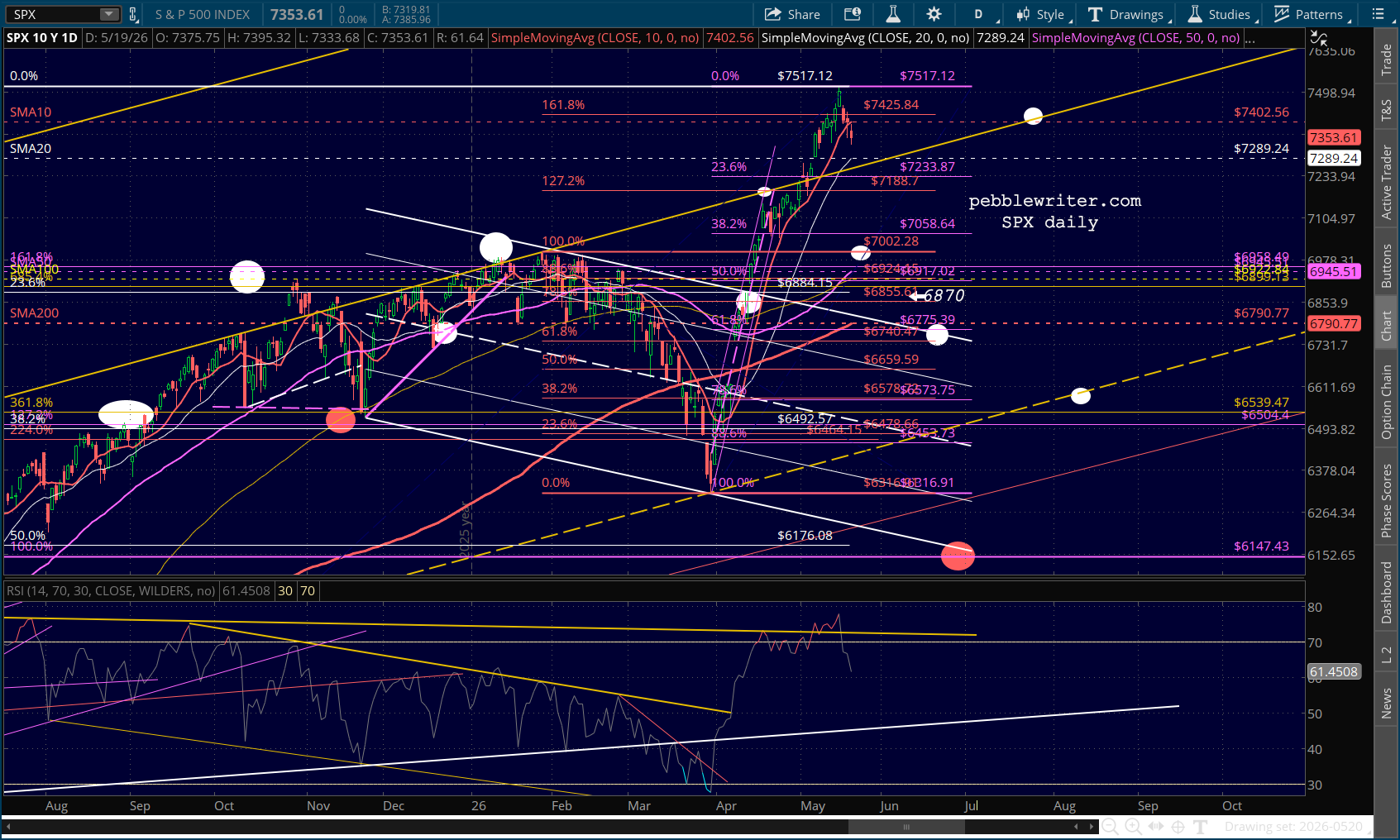

Note that SPX’s RSI has rolled over and backed off its overbought conditions.

We should see the 10Y backtest the purple channel top from which it broke out on May 15. It would also close the gap at 4.46%, ideally between Jun 22 and Jul 22. Obviously, this depends entirely on Trump giving in on Iran, declaring victory and allowing the Strait to reopen. Israel and hardliners would be disappointed, to say the least. But, with the midterms only six months away and an estimated six month glidepath to normalization of oil markets, he has to get started now.

We’ll get Fed minutes at 2pm ET. Stay tuned…

UPDATE: 11:11 AM

We’re off to a good start. Here’s the TNX chart with that initial 4.46% target shown.