Futures are flat this morning after coming within 0.25 of the Sep 2018 highs overnight.

The algo factors are generally bearish, but that hasn’t been enough to stop the meltup thus far.

The algo factors are generally bearish, but that hasn’t been enough to stop the meltup thus far.

continued for members… (more…)

Futures are flat this morning after coming within 0.25 of the Sep 2018 highs overnight.

The algo factors are generally bearish, but that hasn’t been enough to stop the meltup thus far.

continued for members… (more…)

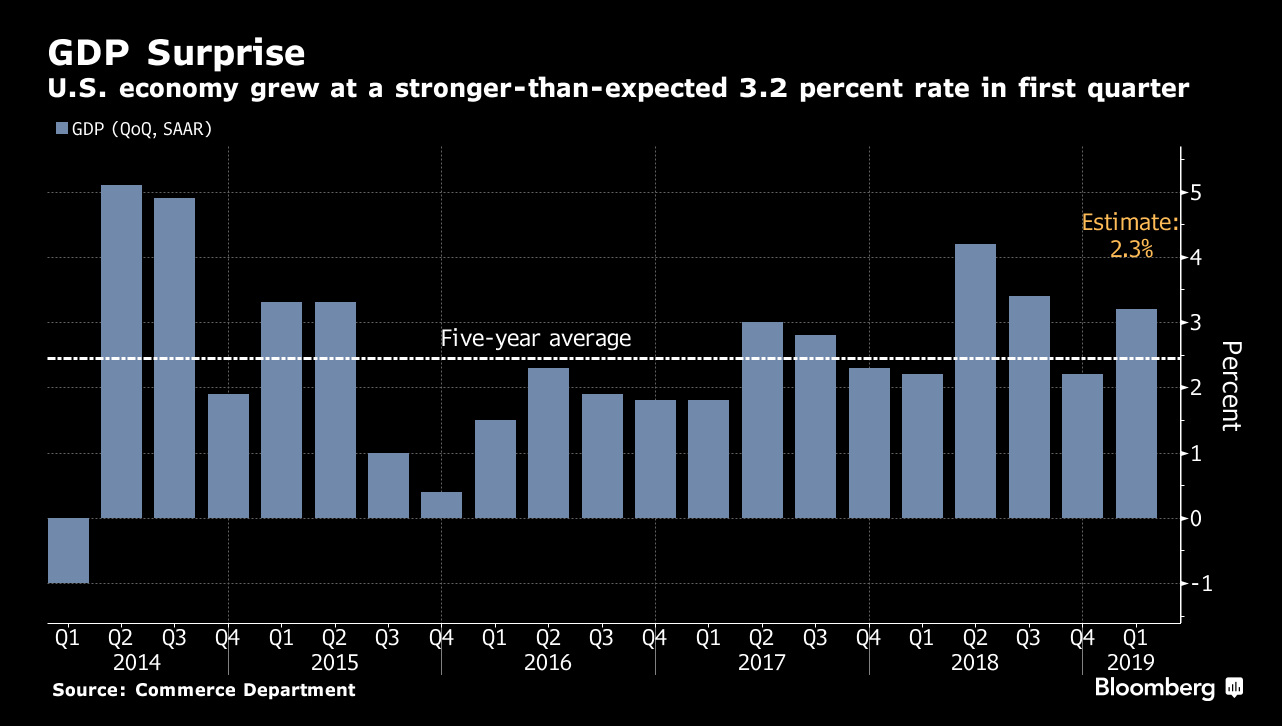

Q1 GDP came in at 3.2%, a big beat versus the 2.3% most expected.

Futures, which nailed our SMA10 target yesterday and had been in the process of breaking down, shot up to the top of the triangle pattern we’ve been watching — not enough to register as a breakout.

Futures, which nailed our SMA10 target yesterday and had been in the process of breaking down, shot up to the top of the triangle pattern we’ve been watching — not enough to register as a breakout.

It will be interesting to see how the Fed spins the latest data to fit their dovish stance. Our downside narrative remains intact.

It will be interesting to see how the Fed spins the latest data to fit their dovish stance. Our downside narrative remains intact.

continued for members… (more…)

Over the last couple of years, the shape of the yield curve has provided some remarkably useful warnings of market turmoil. There are numerous signals and nuances in our yield curve model. One of the most significant is when the 2s10s breaks out above resistance.

It can be seen below in the breakout above the blue trend line (which signaled the Jan-Feb correction) and again in the breakout above the red trend line (which warned us of the Sep-Dec correction.)

What might it mean, then, that the 2s10s is threatening to break out again?

What might it mean, then, that the 2s10s is threatening to break out again?

continued for members… (more…)

SPX came within 4 points of its all-time highs yesterday, a few days ahead of schedule but close enough to be considered a major victory for the bulls. Oddly enough, the futures didn’t seal the deal after-hours.

Is it just possible that the downside case isn’t completely dead?

Is it just possible that the downside case isn’t completely dead?

continued for members… (more…)

SPX has spent 16 sessions at or above its 10-DMA, hardly a record but definitely getting long in the tooth. For those keeping track, this latest run began the day after VIX was hammered back below its SMA200 and CL popped above its SMA200.

But, most of the excitement this morning is in currencies. DXY is testing its Dec 14 and Mar 7 highs, which has nice implications for GC reaching our next downside target. continued for members… (more…)

continued for members… (more…)

One of the more effective factors in prompting algos to buy stocks is the price of oil. Yet, as we’ve been discussing, higher oil prices are a double-edged sword as they can drive inflation to levels which prompt uncomfortably high interest rates.

Thus, even though the latest 3-D chess moves out of the White House have driven oil prices 2.5% higher overnight, S&P 500 futures are off 10 points.

continued for members… (more…)

Futures dipped 11 points below the SMA10 overnight, only to be rescued by retail sales data that beat expectations (+1.6% vs 1.0%) The beat was primarily attributable to soaring gasoline prices and auto sales — a double-edged sword, of course, from an inflation standpoint.

The beat was primarily attributable to soaring gasoline prices and auto sales — a double-edged sword, of course, from an inflation standpoint. The only chart that continues to matter, however is VIX. It has been threatening to break trend for several week, but has managed to hold up fairly well considering the market’s meltup.

The only chart that continues to matter, however is VIX. It has been threatening to break trend for several week, but has managed to hold up fairly well considering the market’s meltup. continued for members… (more…)

continued for members… (more…)

One of life’s certainties over the past decade or so has been that the BOJ would always find a way to keep the Nikkei rallying. When QEn ran out of steam, there was always direct purchases of stocks via ETFs. So, it was surprising to see NKD’s rising channel, in place since Fukushima, break down in December.

True to form, it has since made a strong comeback. But, it has paled in comparison to the S&P 500 (the thin purple line.) While SPX is approaching its all-time highs, NKD is approaching a .618 retracement and a backtest of the broken channel. A possible warning sign?

A possible warning sign?

continued for members… (more…)

As we discussed last week, VIX is at the threshold of what would be a major break in trend. Every such past setup in which VIX broke down resulted in stocks breaking out above important overhead resistance. S&P futures are up 10 points and are now only about 27 points from all-time highs — the result of VIX being hammered to new lows after rallying nearly 10% yesterday.

S&P futures are up 10 points and are now only about 27 points from all-time highs — the result of VIX being hammered to new lows after rallying nearly 10% yesterday. ES’s rising channel from December, kicked off by a meeting of the Plunge Protection Team, broke down two weeks ago. But, it hasn’t mattered. ES continues to melt up, guided by an overhead trend line which will intersect 2947 around Apr 26. Only if VIX bounces strongly will stocks avoid new highs.

ES’s rising channel from December, kicked off by a meeting of the Plunge Protection Team, broke down two weeks ago. But, it hasn’t mattered. ES continues to melt up, guided by an overhead trend line which will intersect 2947 around Apr 26. Only if VIX bounces strongly will stocks avoid new highs. As for earnings and economic data, the algos could care less lately.

As for earnings and economic data, the algos could care less lately.

continued for members… (more…)

Time flies when you’re having fun. It’s hard to believe it’s been almost three years since Brexit first broke.

I initially looked at EURGBP as an interesting trade opportunity. With the EURGBP at .7622, it looked like there was a good chance it would end up at .86 or so. This was our daily chart from June 22, 2016 [see: The Eve of Destruction.]

It reached our initial targets of .8262 and .8411 by June 30, and reached .8599 on July 6 — a nice 13% return in two weeks. It might have stopped there, as it represented the .886 Fib retracement as well as the channel midline.

It reached our initial targets of .8262 and .8411 by June 30, and reached .8599 on July 6 — a nice 13% return in two weeks. It might have stopped there, as it represented the .886 Fib retracement as well as the channel midline.

As we had discussed in The Eve of Destruction, sharp rallies and pushes above resistance were bearish for stocks.  So, I expected heroic central bankers to swoop in and save the world at that point. To be sure, it needed saving. Futures crashed 6.5% overnight. Additional carnage-depicting charts are available at It’s a Brexit! posted live that evening.

So, I expected heroic central bankers to swoop in and save the world at that point. To be sure, it needed saving. Futures crashed 6.5% overnight. Additional carnage-depicting charts are available at It’s a Brexit! posted live that evening.

In any case, TPTB didn’t save the world by putting a lid on EURGBP — which popped above the former highs.

In any case, TPTB didn’t save the world by putting a lid on EURGBP — which popped above the former highs.  Instead, USDJPY made a heroic reversal and VIX collapsed to some of the lowest levels seen in over a decade…

Instead, USDJPY made a heroic reversal and VIX collapsed to some of the lowest levels seen in over a decade… …all because EURGBP couldn’t be contained. It’s important to note that even though SPX didn’t completely collapse, it tested important lows and took almost a year to regain its 2015 highs (the shaded area below.)

…all because EURGBP couldn’t be contained. It’s important to note that even though SPX didn’t completely collapse, it tested important lows and took almost a year to regain its 2015 highs (the shaded area below.) There were other things going on. But, GBP’s weakness was certainly a drag on stocks as had been the pattern in previous years.

There were other things going on. But, GBP’s weakness was certainly a drag on stocks as had been the pattern in previous years.

As it turned out, EURGBP’s ascent wasn’t without a target in mind. It had passed up the purple .886 to focus on a different one. On Oct 7, 2016, it came within .0039 of its white .886 Fib based on its all-time high and its post-GFC lows. Since then, it has been consolidating. The highs have been very well aligned — preserving the narrative of a downward trend. Does this mean we can count on the GBP to steadily increase in value? Maybe.

Since then, it has been consolidating. The highs have been very well aligned — preserving the narrative of a downward trend. Does this mean we can count on the GBP to steadily increase in value? Maybe.

continued for members… (more…)