Futures are off moderately, giving up about half of yesterday’s spike. As of yesterday’s close, the S&P 500 is off just over 20% – the worst calendar year since 2008.

As of yesterday’s close, the S&P 500 is off just over 20% – the worst calendar year since 2008.

continued for members… (more…)

Futures are off moderately, giving up about half of yesterday’s spike.As of yesterday’s close, the S&P 500 is off just over 20% – the worst calendar year since 2008.

continued for members… (more…)

Futures are up moderately as we approach the open, gaining back much of the losses suffered yesterday in the wake of a dismal pending home sales print (-4.0% versus -0.8% expected, the worst since inception in 2001.) Prices fell MoM for the fourth month in a row.

At this point, it appears the bulls are ready to take a knee and let the clock run out on 2022. Unfortunately, 2023 should prove even more difficult.

At this point, it appears the bulls are ready to take a knee and let the clock run out on 2022. Unfortunately, 2023 should prove even more difficult.

continued for members… (more…)

It seems the algos are content to hold the current line instead of rallying into the end of the year – this Friday.

continued for members… (more…)

continued for members… (more…)

S&P futures are quiet this morning, back to even after being up about 30 points overnight. continued for members… (more…)

continued for members… (more…)

What the algos giveth, David Tepper (bearish) and Q3 GDP (+3.2% vs 2.9% est. and -0.6% last) taketh away. Futures are off sharply as we approach the open.

continued for members… (more…)

continued for members… (more…)

Wish I could say that the overnight ramp or the manner in which it’s being conducted was surprising. But, we’ve seen the Look! VIX is breaking down! movie so many times, it’s becoming as normal as negative interest rates.

The algos don’t care whether it’s legit or not. They just see VIX off 21% from last week and ramp higher…

The algos don’t care whether it’s legit or not. They just see VIX off 21% from last week and ramp higher…

continued for members… (more…)

continued for members… (more…)

The Bank of Japan has kept interest rates at or below zero for years. Their bet was that the suppression of interest rates (by purchasing Japan’s net issuance, the BoJ now owns over 50%) would offer sufficient protection against both inflation and the 263% debt:GDP – exacerbated by the rapid depreciation of the yen.

Investors, including yours truly, have had their doubts. While effective at propping up equity prices [see: The Yen Carry Trade Explained], the yen’s plunge greatly amplified food and energy price increases. Inflation reached 3.6% in October. It seemed as though something would eventually have to give.

It just did.

The BoJ just announced that they would allow rates to move to as high as 0.5%, sending the 10Y soaring from 25 to 42 bps…

The BoJ just announced that they would allow rates to move to as high as 0.5%, sending the 10Y soaring from 25 to 42 bps…

…and the USDJPY plunging (yen strengthening) by 3.3% – below its 200-day moving average for the first time since Feb 2021.

…and the USDJPY plunging (yen strengthening) by 3.3% – below its 200-day moving average for the first time since Feb 2021.

The BoJ is essentially betting that the small increase in rates will

continued for members… (more…)

Futures passed on an opportunity to break out this morning, perhaps weighing the potential for a Santa Claus rally against the implications of a slew of important economic data later this week.

Speaking of passing, how about that match between France and Argentina? I’m not a football nut, more of a rugby and basketball fan. But, that was one of the more exciting games I’ve seen in any sport in ages…

continued for members… (more…)

The confusion isn’t over whether the market will continue selling off. It will. The question is how far it can sell off before it’s “rescued.” Different indices indicate anywhere from 2.2% to 20%. And, it totally depends on which index gets to call the shots.

If the Dow has its way, the market is in for another 2.2% decline (our target at its 200-day moving average), at which point Powell would call a press conference and declare “just kidding.”

But, the Dow has already backtested its Feb 2020 highs.

But, the Dow has already backtested its Feb 2020 highs.

continued for members… (more…)

As expected, Powell and Co. were not amused by the market’s recent exuberance and decided to take things down a notch.

The algos haven’t yet given up, though, with VIX still under pressure and DXY remaining oversold.

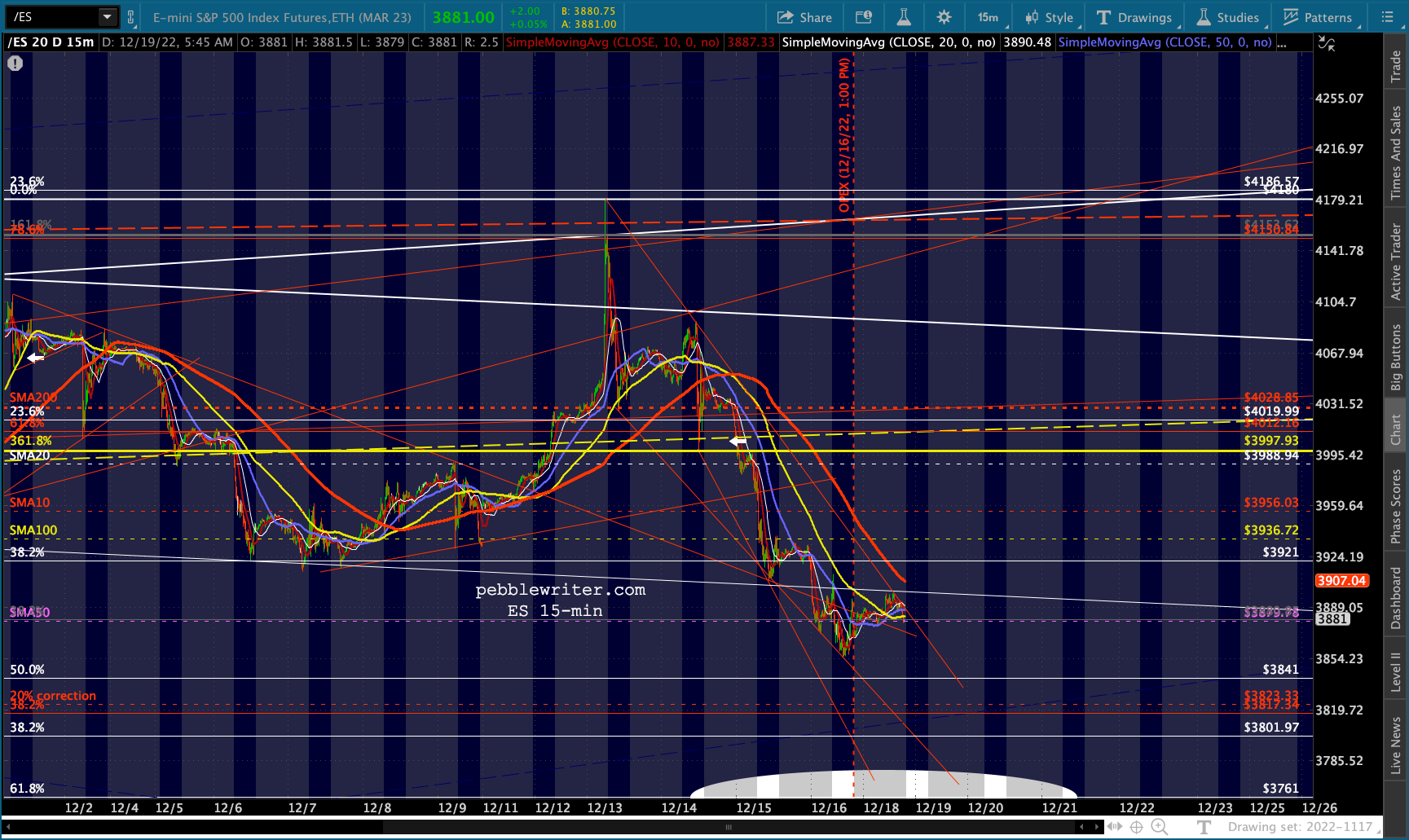

The algos haven’t yet given up, though, with VIX still under pressure and DXY remaining oversold. The reversal is working just fine so far. But, with OPEX tomorrow and two weeks left in the year, we’re left to wonder whether the bulls are ready to throw in the towel.

The reversal is working just fine so far. But, with OPEX tomorrow and two weeks left in the year, we’re left to wonder whether the bulls are ready to throw in the towel.

continued for members… (more…)