…borrowed from spindriftcap.com…

This is not your father’s market.

It continues to grind higher, largely on the back of the yen carry trade (along with stock buybacks, margin expansion, etc..) Recall that at the start of 2014, SPX sold off when USDJPY reached a reversal point (after an overshoot based on USDJPY’s Dec 18 ramp.) But, the Bank of Japan put a floor under USDJPY, enabling the carry trade to keep SPX on an upward track.

The USDJPY breakout in mid-August stopped SPX’s decline in its tracks after only 87 points (4.3%.) Since then, USDJPY has raced higher, barely pausing along the way. Why? Each time it does, stocks stumble. In other words, stocks can’t afford for USDJPY to decline — AT ALL. In fact, SPX has been unable to follow through with new highs since USDJPY reached the 1.618 Fib level, where it was merely expected to correct.

Japan is flat broke. Trashing the yen and buying Japanese stocks with borrowed money are the only tricks Abe and Kuroda can come up with to get back on track. The only thing they’ve accomplished is to increase inflation (esp. food and fuel) significantly for the Japanese taxpayer, who is now paying much higher taxes to service the vastly increased debt.

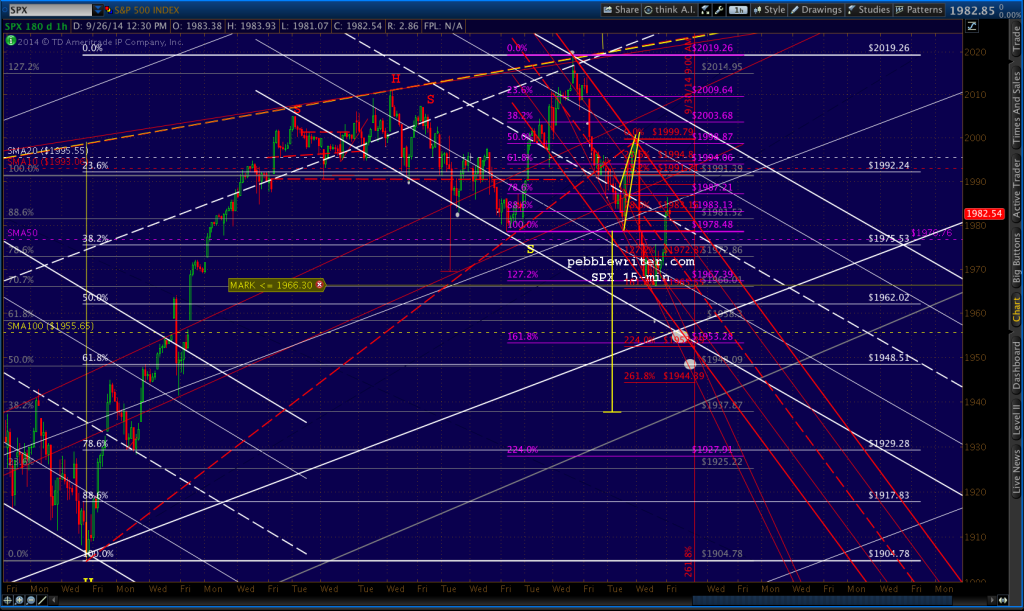

At its current pace, USDJPY should reach our next upside target (110) either today or tomorrow. If it can rejoin its rising red channel, stocks should recover and continue to 2138. If it reverses, it’s hard to believe SPX’s SMA100 will hold yet again.

The euro is another interesting case. Previous tags of the TL from 2009 have resulted in stock corrections. Not so, this time. Past bouts of dollar strength have meant a flight to safety. Now they just reflect the games being played with the yen carry trade. I don’t know how long the rising wedge can continue to rise, but I suspect its days are numbered.

The dollar chart, itself, tells a compelling story. Again, past instances of dollar strength have meant stock weakness (a negative correlation.) Since USDJPY began its meteoric rise, however, stocks have taken off like a shot and are now positively correlated with the dollar.

The index has reached very strong technical resistance, and appears to be in the final days of a throwoever. But, if it can break out, stocks should get a substantial boost (again, not because a strong dollar is good for stocks, but because it means the dollar – or euro? – carry trade is working.)

GLTA.