They’re certainly working so far, driving major indices below their 200-day moving averages.

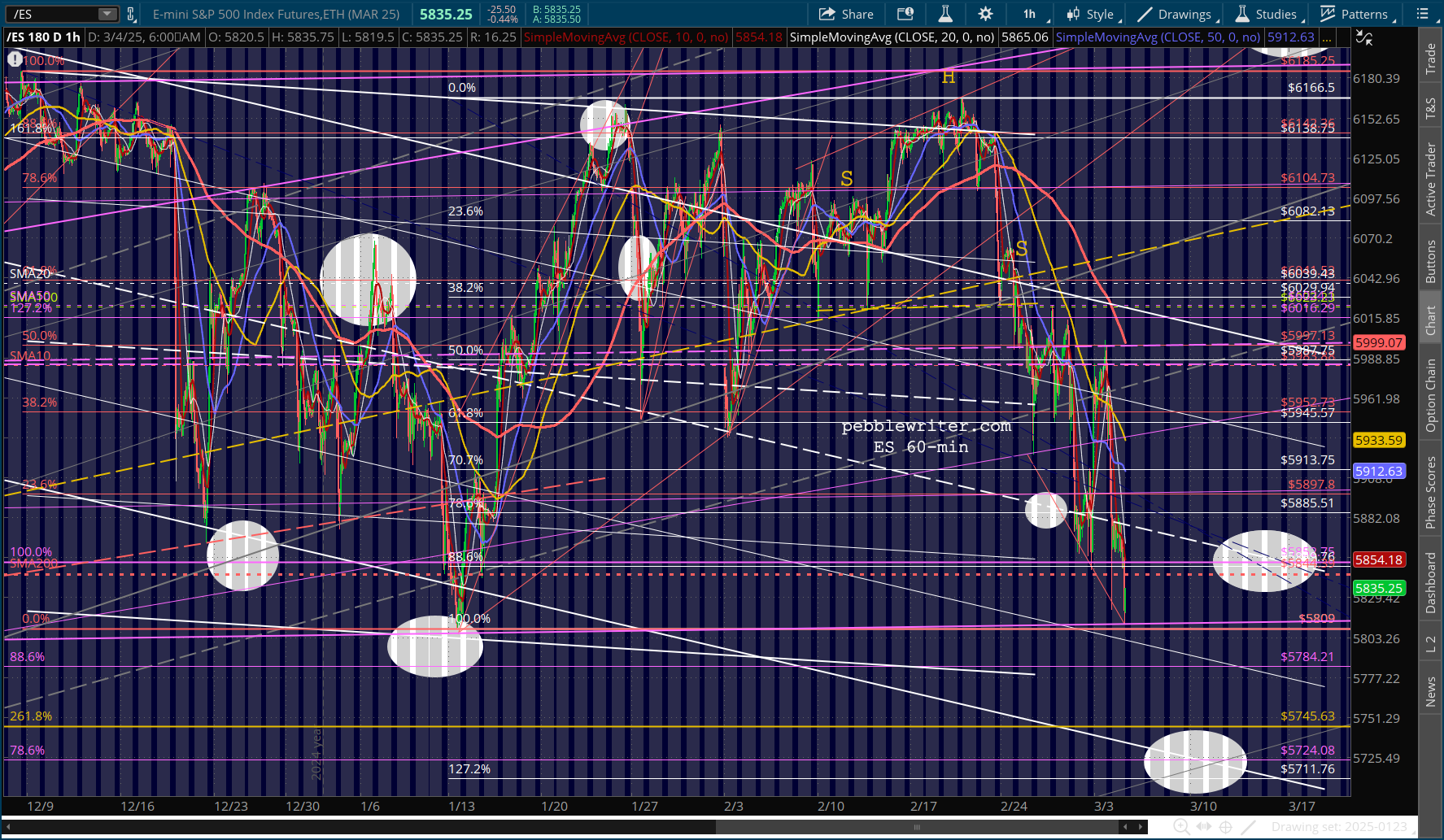

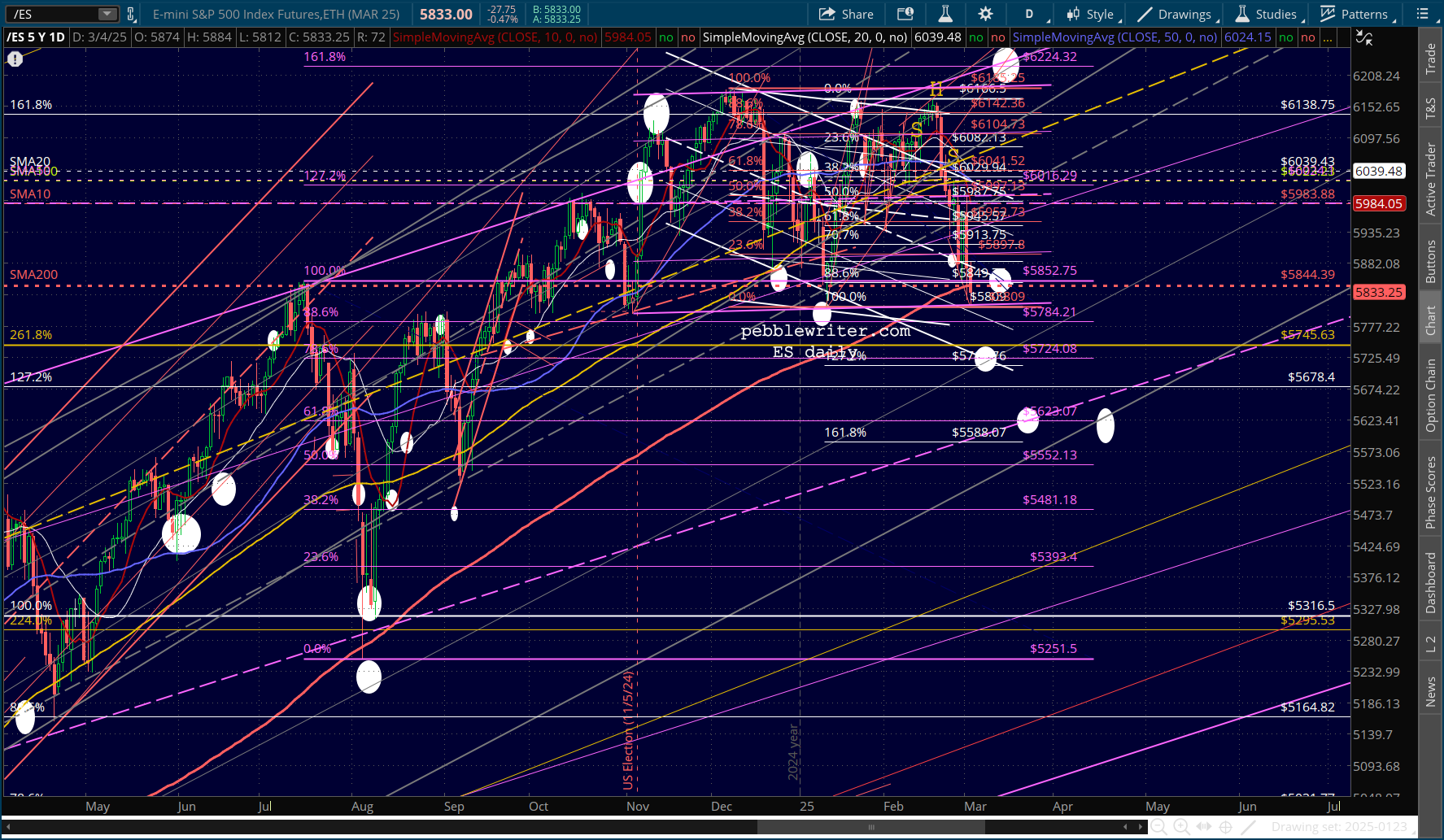

ES reached our 200-day target with ease, followed by an obligatory bounce which failed overnight.

ES reached our 200-day target with ease, followed by an obligatory bounce which failed overnight.

If the tariffs result in a reduction in duties charged by our trading partners, that’s all well and good. The markets wouldn’t bat an eye. Unfortunately, the economic arguments the White House is putting forward are rubbish.

There is no chance of tariffs lowering prices, increasing US jobs or increasing profits. Consider Apple’s recent announcement of a $500 billion investment in the US. Estimates suggest that manufacturing jobs in China pay $5-6 per hour on average.

In the US, similar manufacturing jobs pay about $27 per hour. And, consider that US employees get healthcare, retirement, overtime and other benefits which are practically nonexistent in China. Other Asian countries pay less – often much less.

Obviously, if those jobs were to come back to the US, prices would definitely rise.

continued for members…

BTW, just for the record, I don’t believe the tariffs have much at all to do with fentanyl. Maybe with Mexico. But, with Canada, I suspect it’s much more oriented to oil prices. With Me

The equity picture:

The currency picture reflects equity weakness especially via the USDJPY yen carry trade unwinding.

The currency picture reflects equity weakness especially via the USDJPY yen carry trade unwinding.

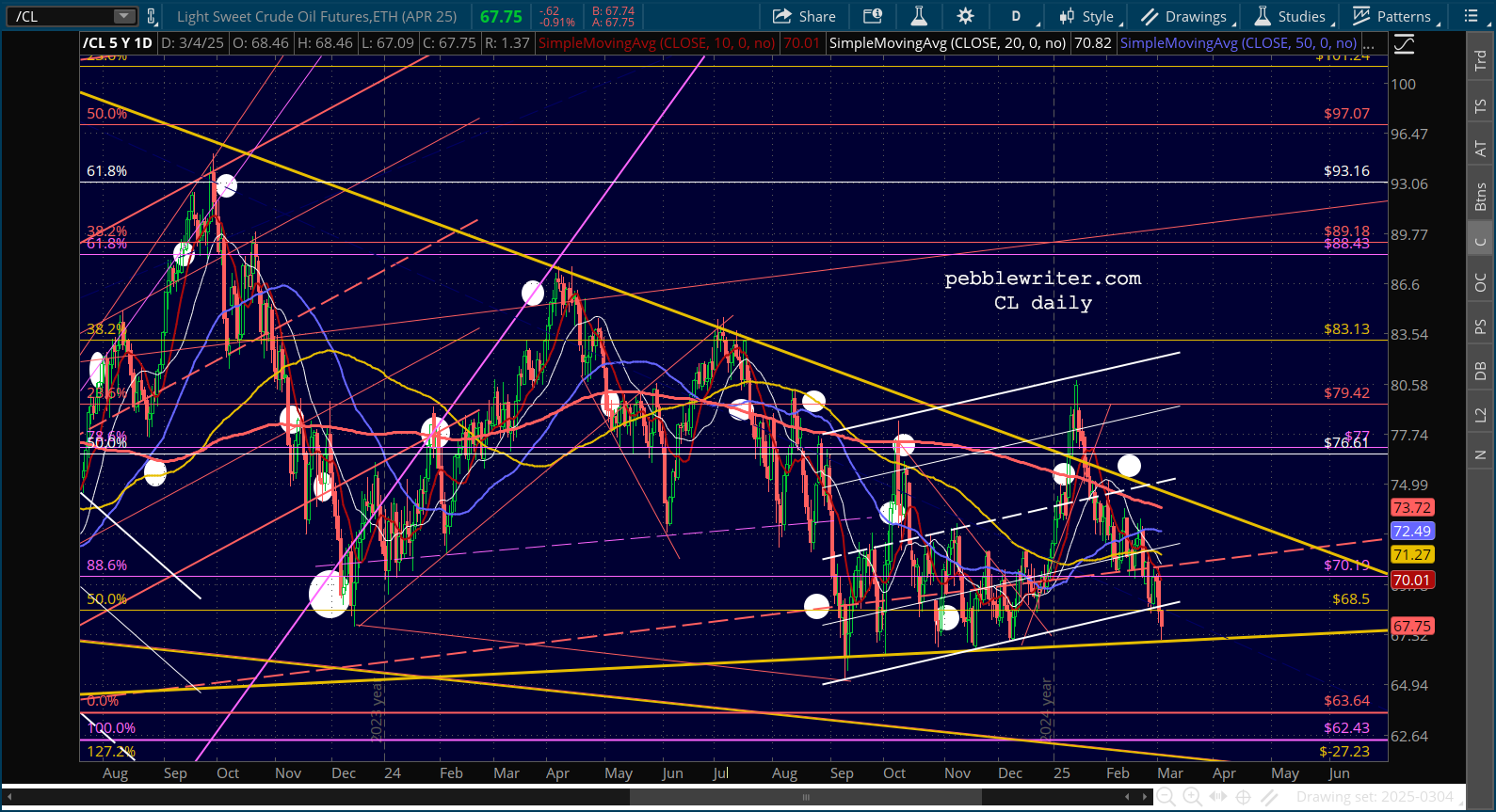

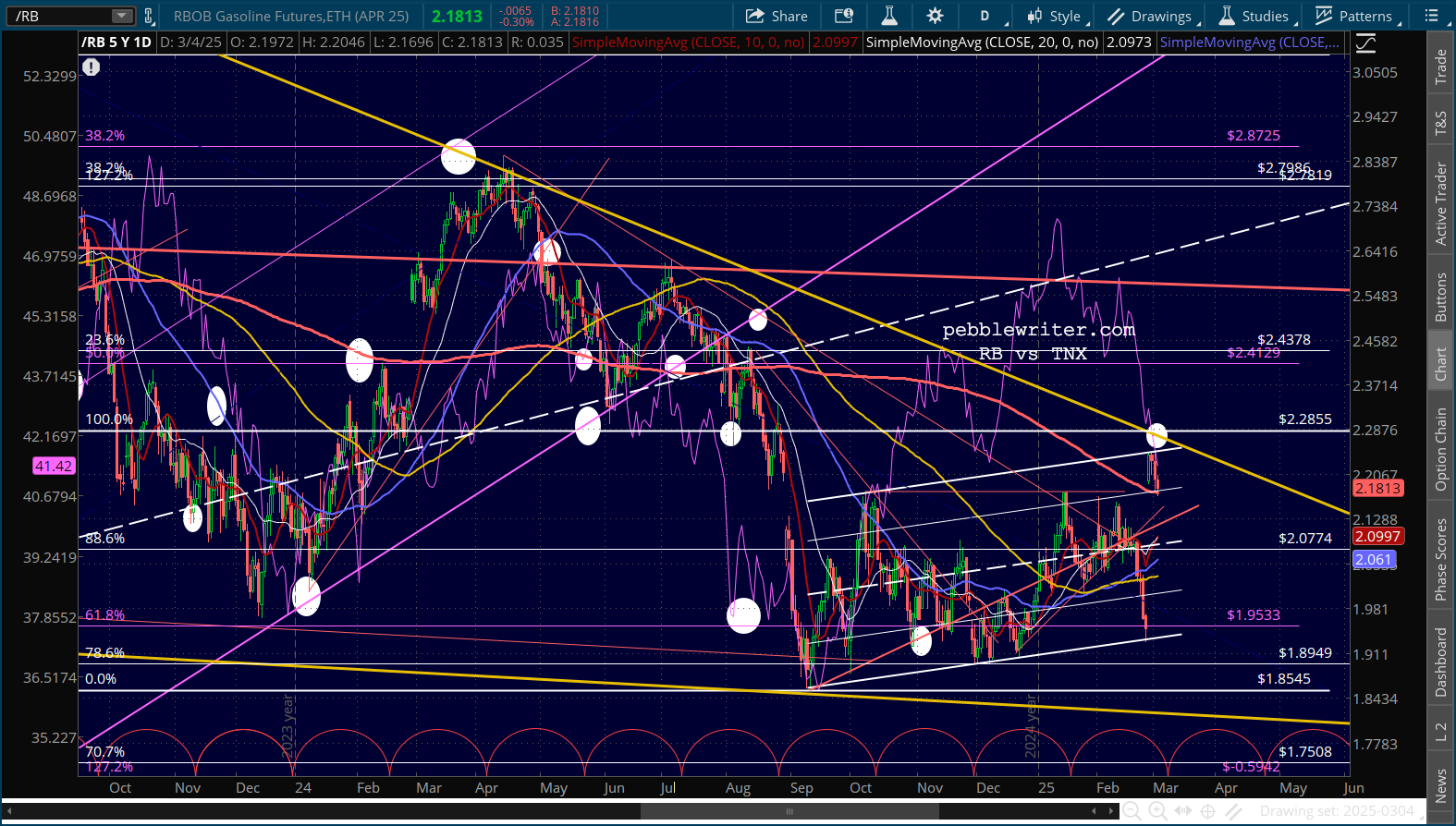

We’re seeing a slight bounce in CL and drop in RB.

We’re seeing a slight bounce in CL and drop in RB.

But, the 10Y is slipping due to equity fears more so than inflation fears.

But, the 10Y is slipping due to equity fears more so than inflation fears. Where will the pain end? It’s hard to say, as I firmly believe there will come a point where Trump calls it off.

Where will the pain end? It’s hard to say, as I firmly believe there will come a point where Trump calls it off.

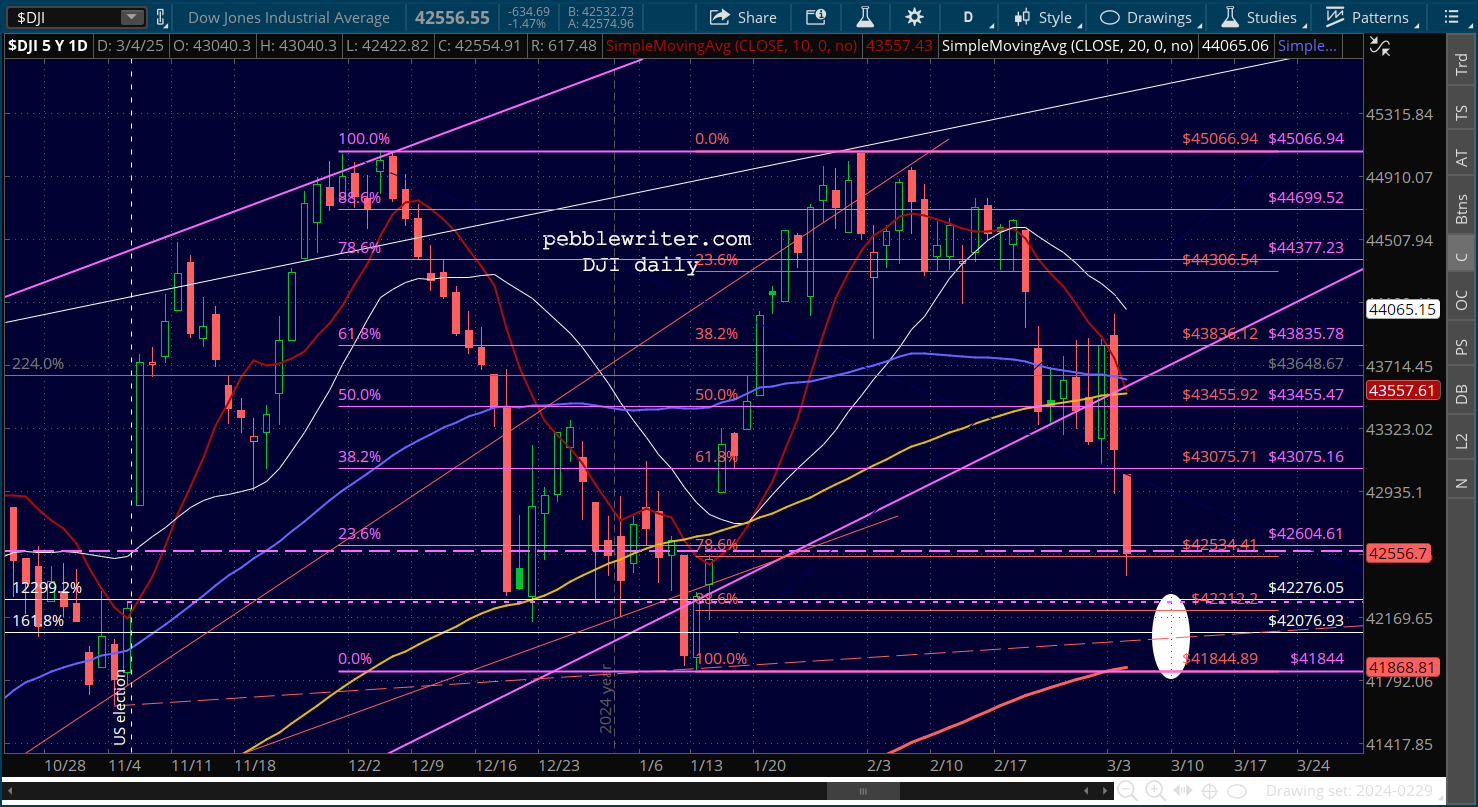

It happened in 2020 when the Dow reached the lows experienced on Nov 9, 2016, the day after Trump won that election. Recall that we didn’t know until the day after the election who had won. This year, the results were clearer, earlier.

On Nov 6, 2024, the DJIA closed at 42,221. The last time the DJIA reached that level was Jan 10, following the release of much hotter than expected jobs data and a breakout in the 10Y.

On Nov 6, 2024, the DJIA closed at 42,221. The last time the DJIA reached that level was Jan 10, following the release of much hotter than expected jobs data and a breakout in the 10Y.

The following day, the Dow popped back above that level. It gained over 5% in the following week. It’s back in that neighborhood, with the SMA200 now above the Jan 10 lows.I believe it’s no coincidence that these tariffs coincided with DJIA’s SMA200 rising above the Jan lows.

The “Trump Put” argument would suggest at least a significant bounce at the Jan 10 close (42,221), the red .886 retracement (42,212) or a TL from the Nov 4 lows (approx. 42.029.)

COMP is already trading below its Nov 5 close (18,439.) It has already reached our SMA200 target (18,375) and has additional support down around 17,426.

COMP is already trading below its Nov 5 close (18,439.) It has already reached our SMA200 target (18,375) and has additional support down around 17,426.

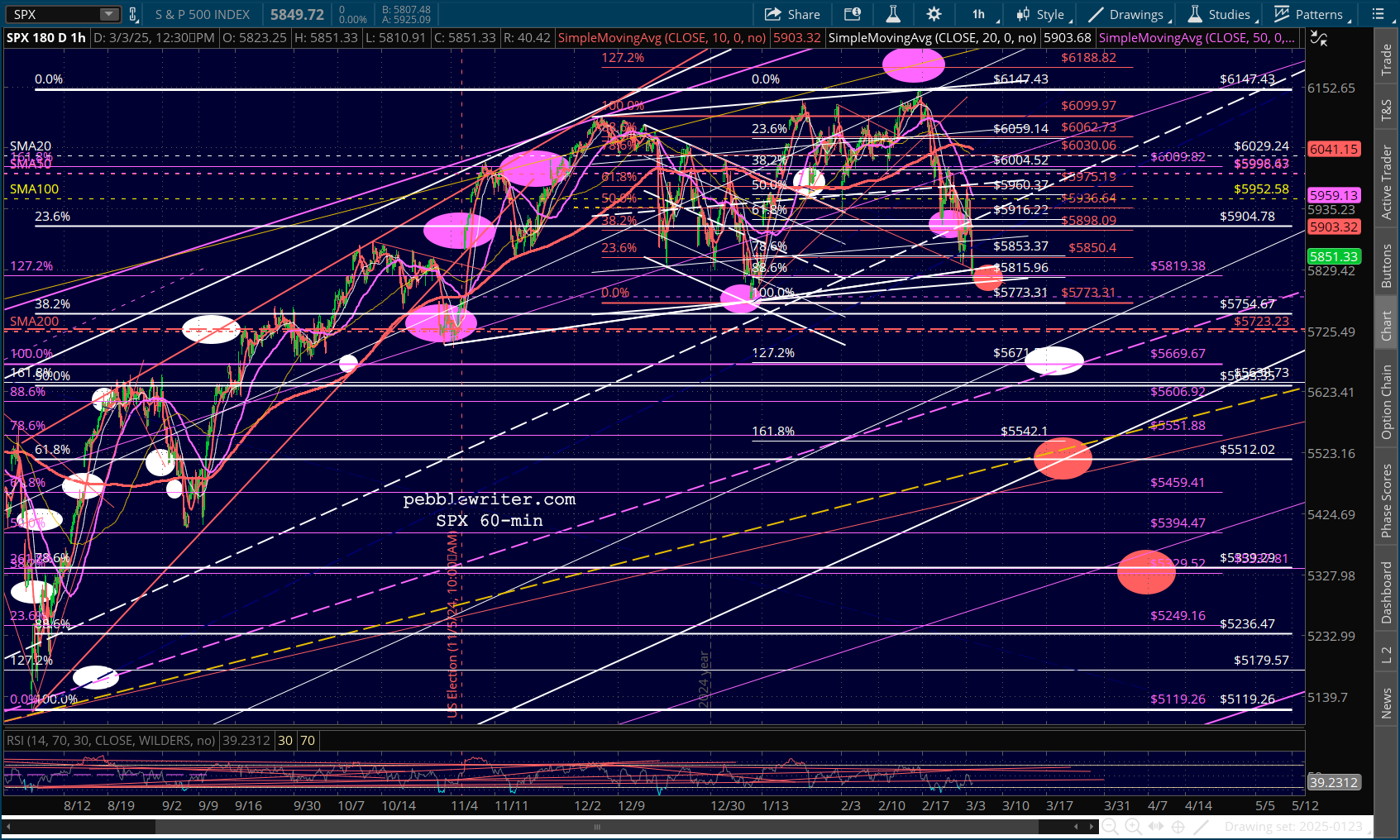

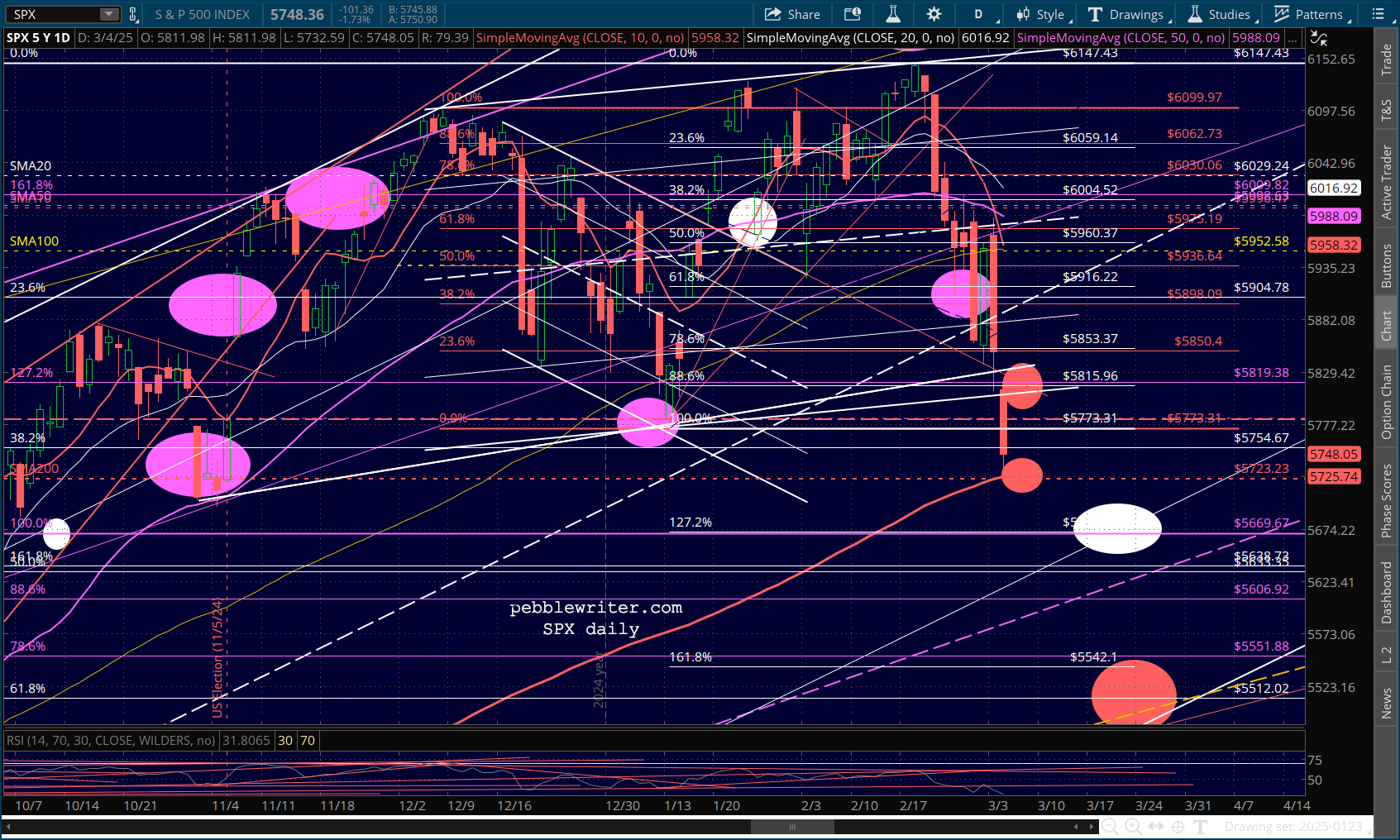

SPX has already traded below its Nov 5 close and is approaching its SMA200 at 5725, with support at its 1.272 Fib extension at 5669. Note that 5669 is also the Jul 16, 2024 highs – making it an extra attractive target.

SPX has already traded below its Nov 5 close and is approaching its SMA200 at 5725, with support at its 1.272 Fib extension at 5669. Note that 5669 is also the Jul 16, 2024 highs – making it an extra attractive target.

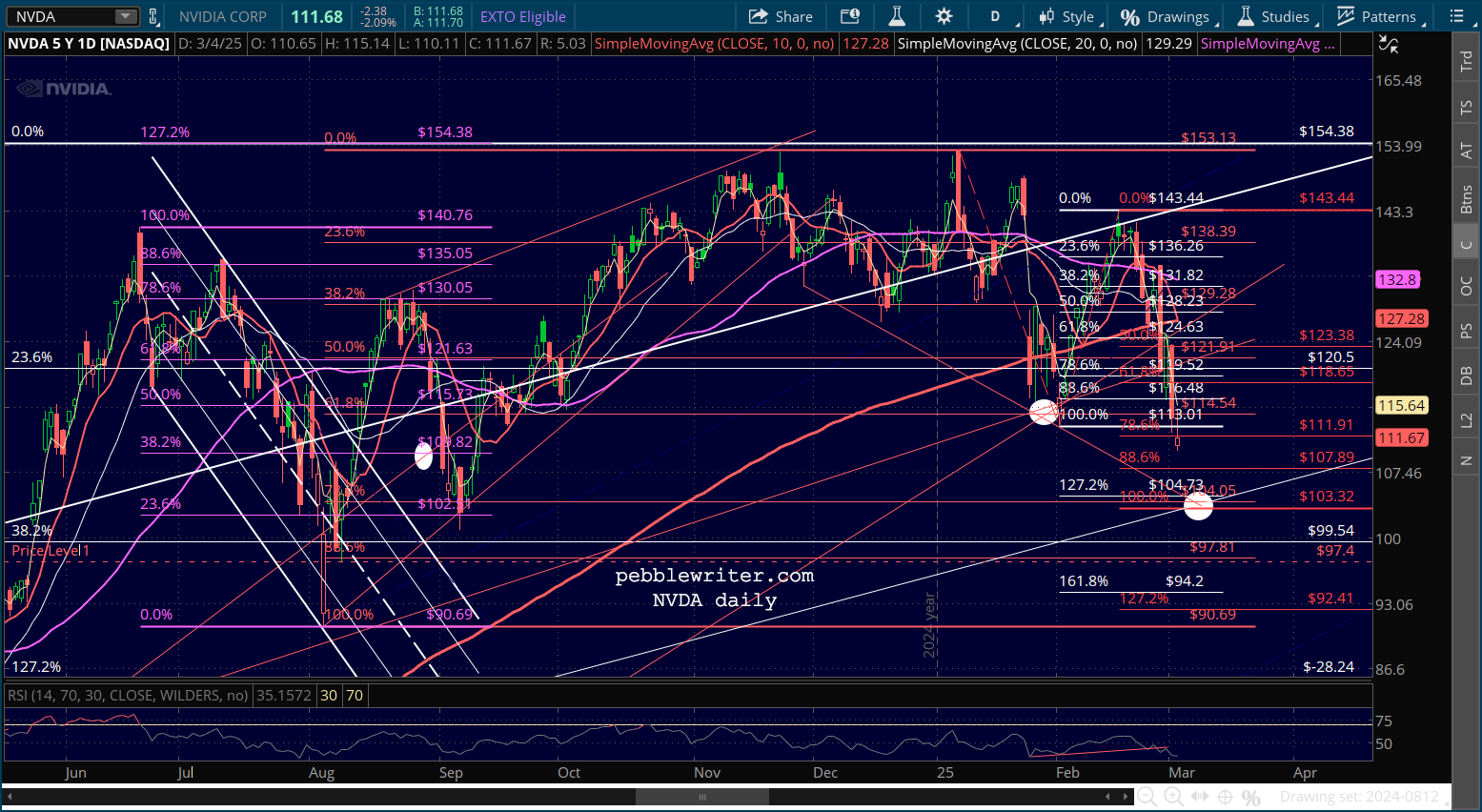

FWIW, NVDA is trading below its Feb 3 lows and closing in on our next downside target at 104. If it trades below 104, it has potential support at numerous levels ranging from 97.4 to 99.54.

FWIW, NVDA is trading below its Feb 3 lows and closing in on our next downside target at 104. If it trades below 104, it has potential support at numerous levels ranging from 97.4 to 99.54.

As to timing, these lows could come as soon as this afternoon and a bounce coming as the result of those lows being reached, a change in the tariff picture, and/or Trump’s address to Congress tonight.

As to timing, these lows could come as soon as this afternoon and a bounce coming as the result of those lows being reached, a change in the tariff picture, and/or Trump’s address to Congress tonight.

GLTA