The issue isn’t whether the Treasury is ending $454 billion in special lending programs on schedule on Dec 31. It’s that there was obviously a breakdown in communications and, apparently, a disagreement between the Treasury and the Fed. In other words, Mom and Dad are fighting.

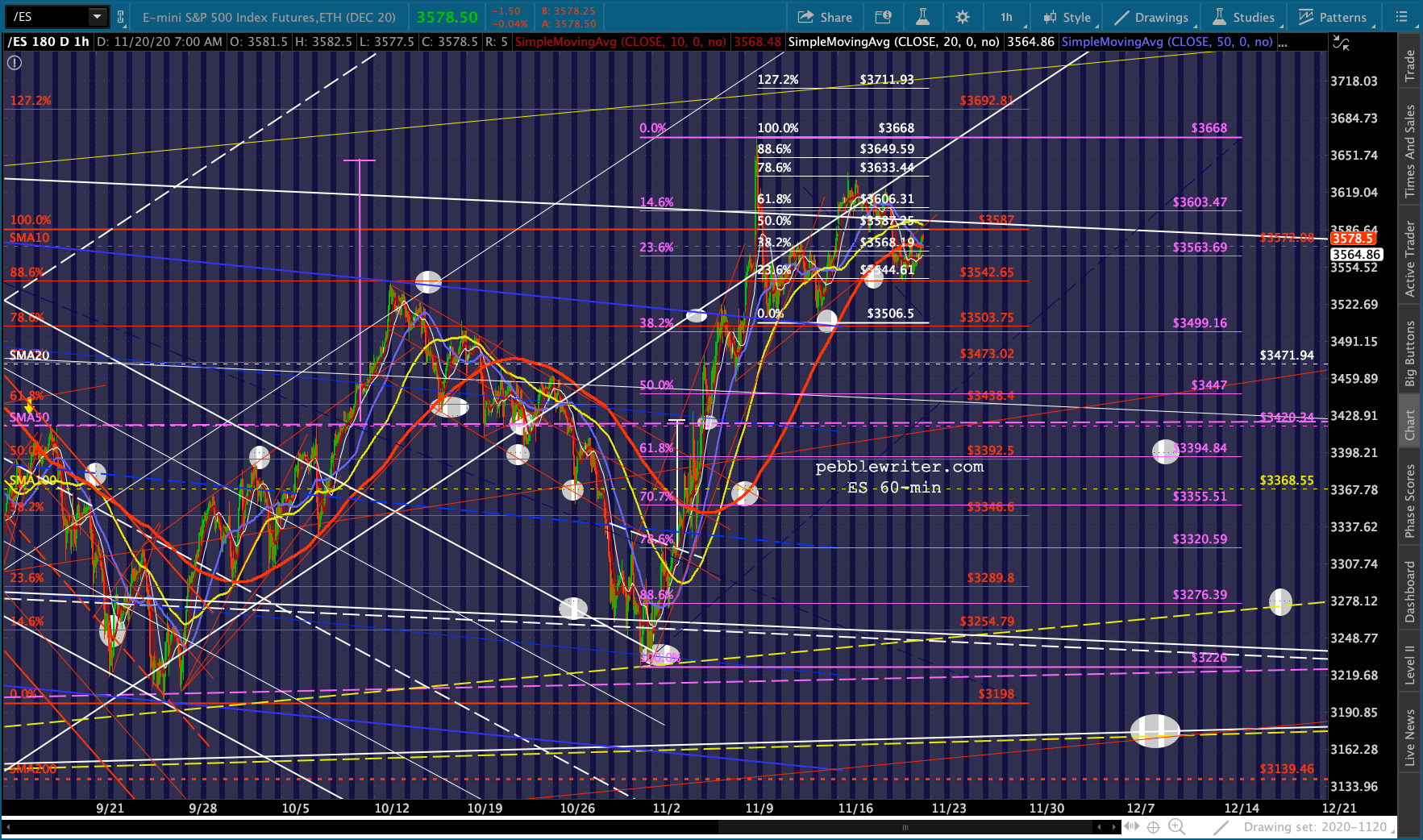

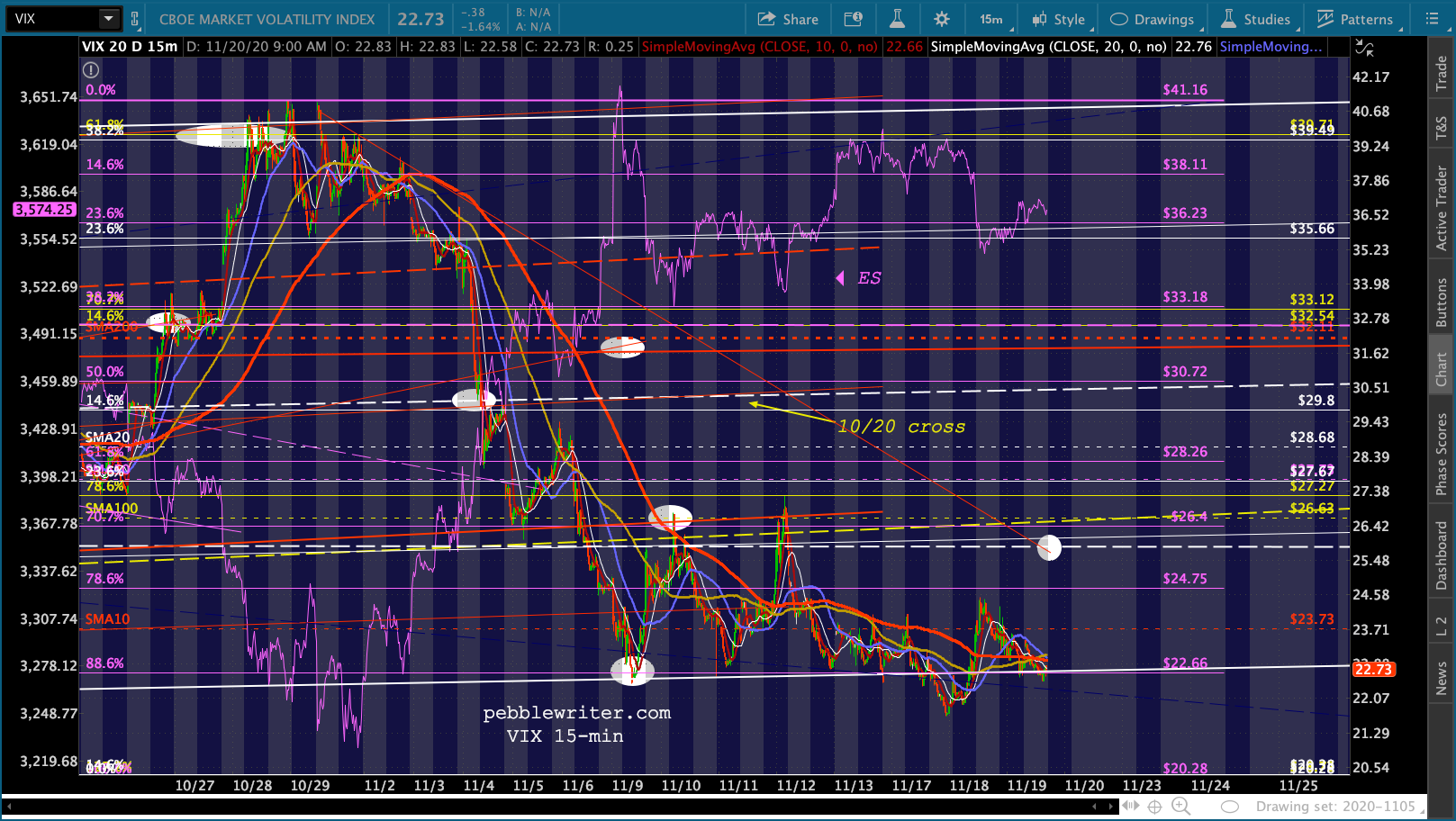

The dollar’s reaction has been muted so far, as the Fed still has plenty of firepower (as they keep reminding us.) But, of course, today is OPEX. The futures’ initial 39-pt nosedive was promptly “fixed” by a timely beatdown in VIX – that pesky .886 Fib at 22.66 again. ES is back above its SMA10, so all is well.

But, of course, today is OPEX. The futures’ initial 39-pt nosedive was promptly “fixed” by a timely beatdown in VIX – that pesky .886 Fib at 22.66 again. ES is back above its SMA10, so all is well.  Next week, though, with low-volume holiday equity trading, should be another story.

Next week, though, with low-volume holiday equity trading, should be another story.

continued for members…

ZN got a little bump on the news, but it was quickly extinguished.  However, note that the 2s10s is sitting slightly below support and should continue to concern bulls – especially if USDJPY breaks down and/or VIX can’t remain below 22.66.

However, note that the 2s10s is sitting slightly below support and should continue to concern bulls – especially if USDJPY breaks down and/or VIX can’t remain below 22.66. The bigger picture shows that ES has still backtested the rising white channel.

The bigger picture shows that ES has still backtested the rising white channel.

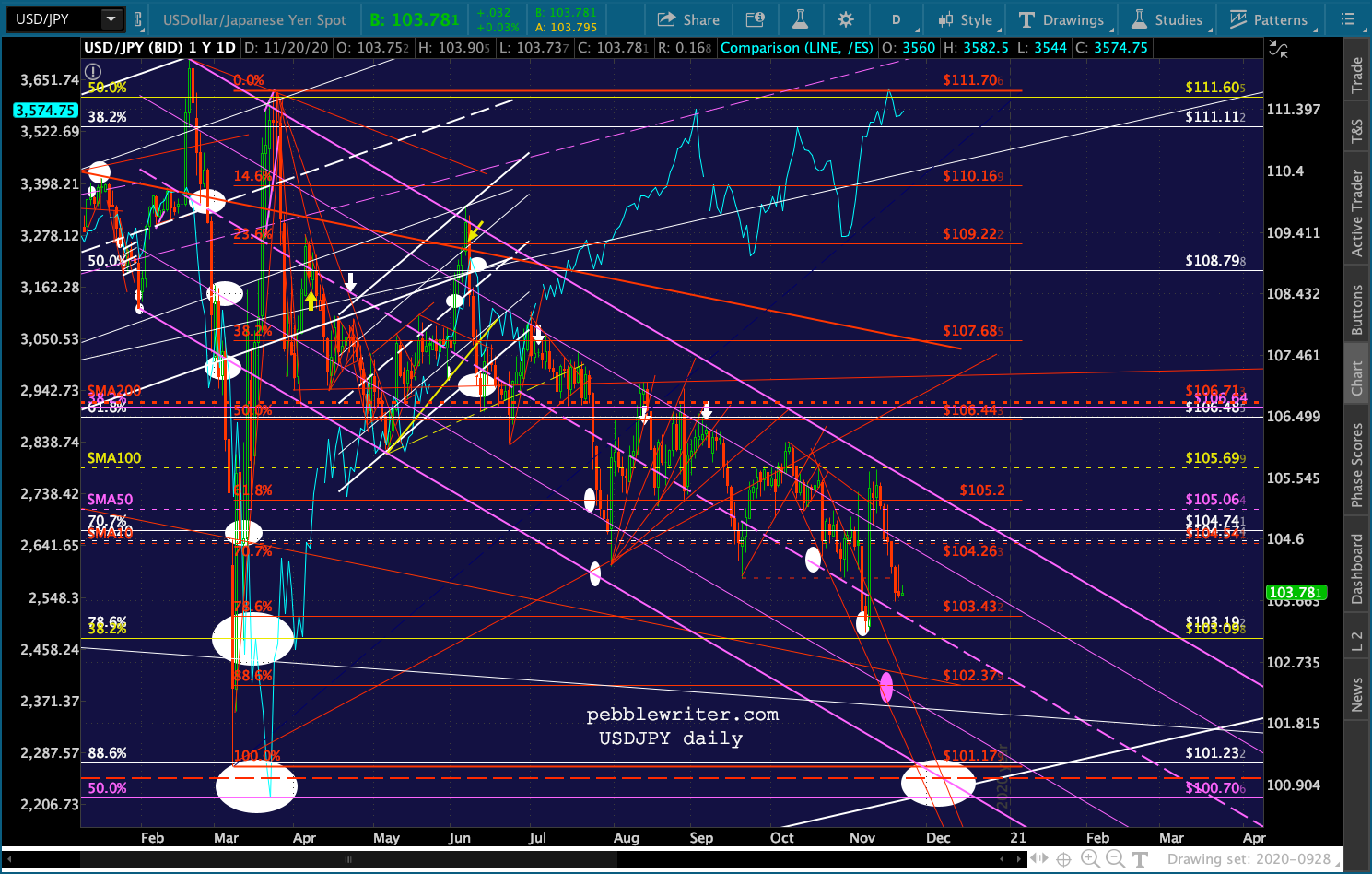

DXY and USDJPY are still poised for a drop – which might well wait until next Friday – one of the easiest days of the entire year to prop up equity prices.

DXY and USDJPY are still poised for a drop – which might well wait until next Friday – one of the easiest days of the entire year to prop up equity prices.

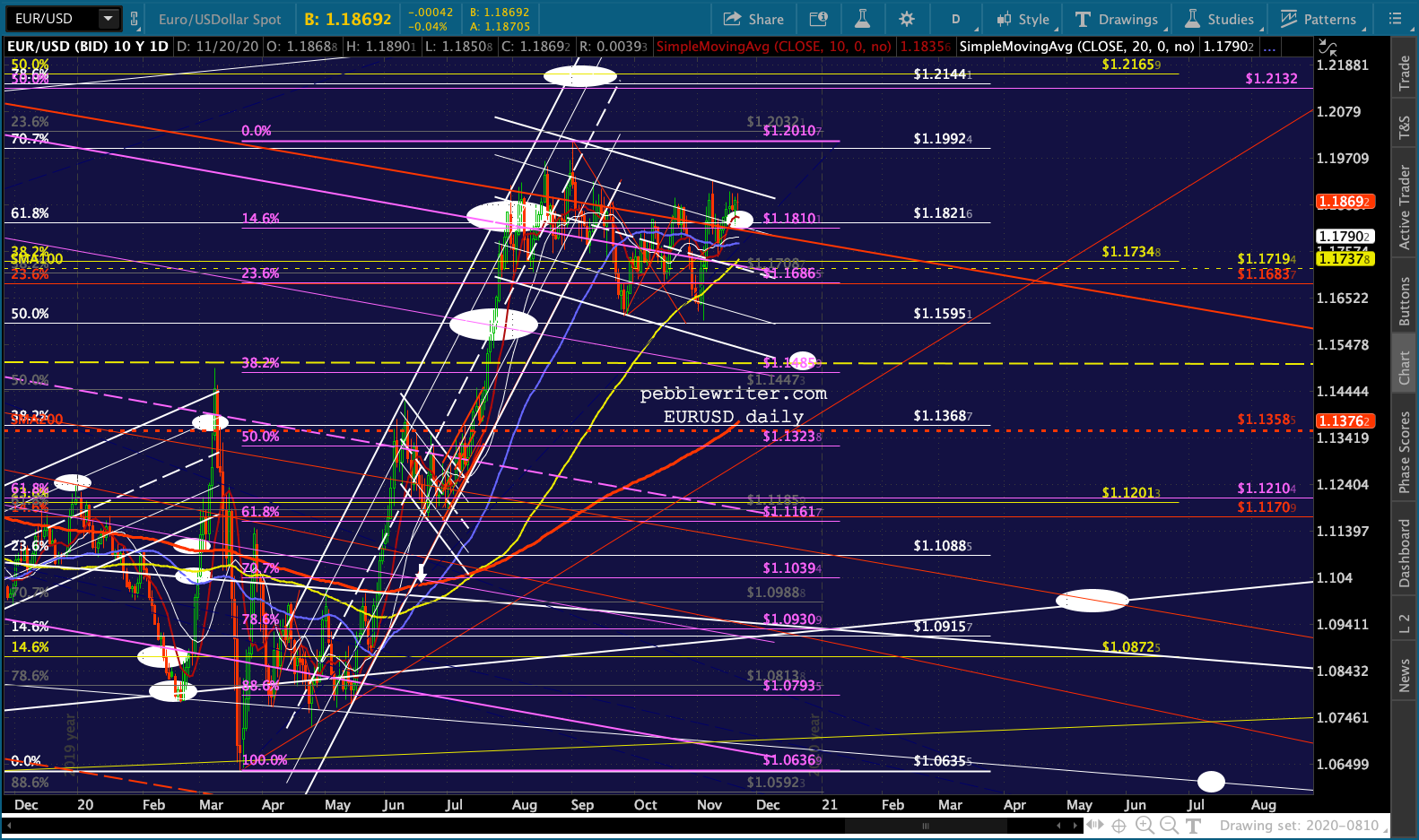

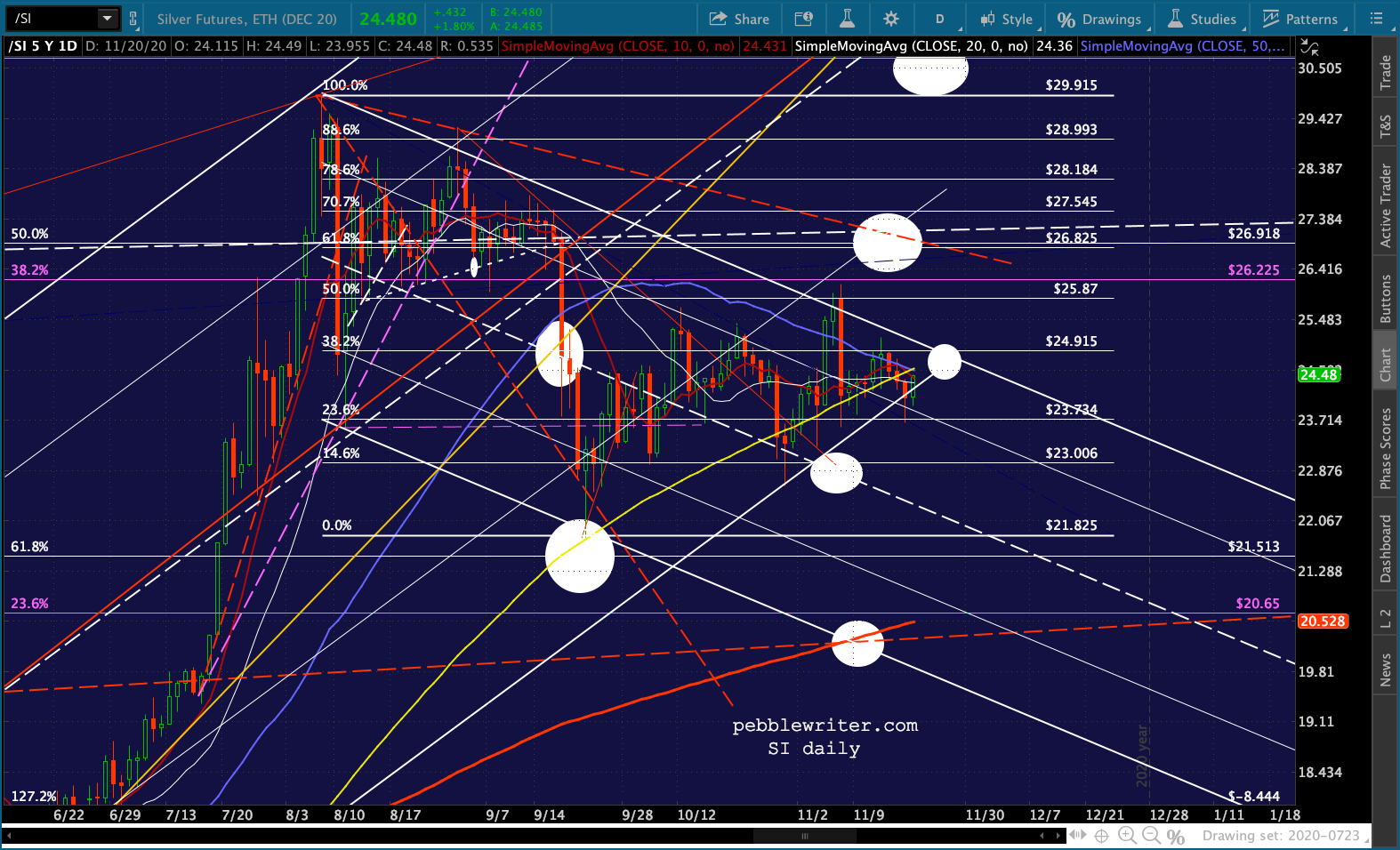

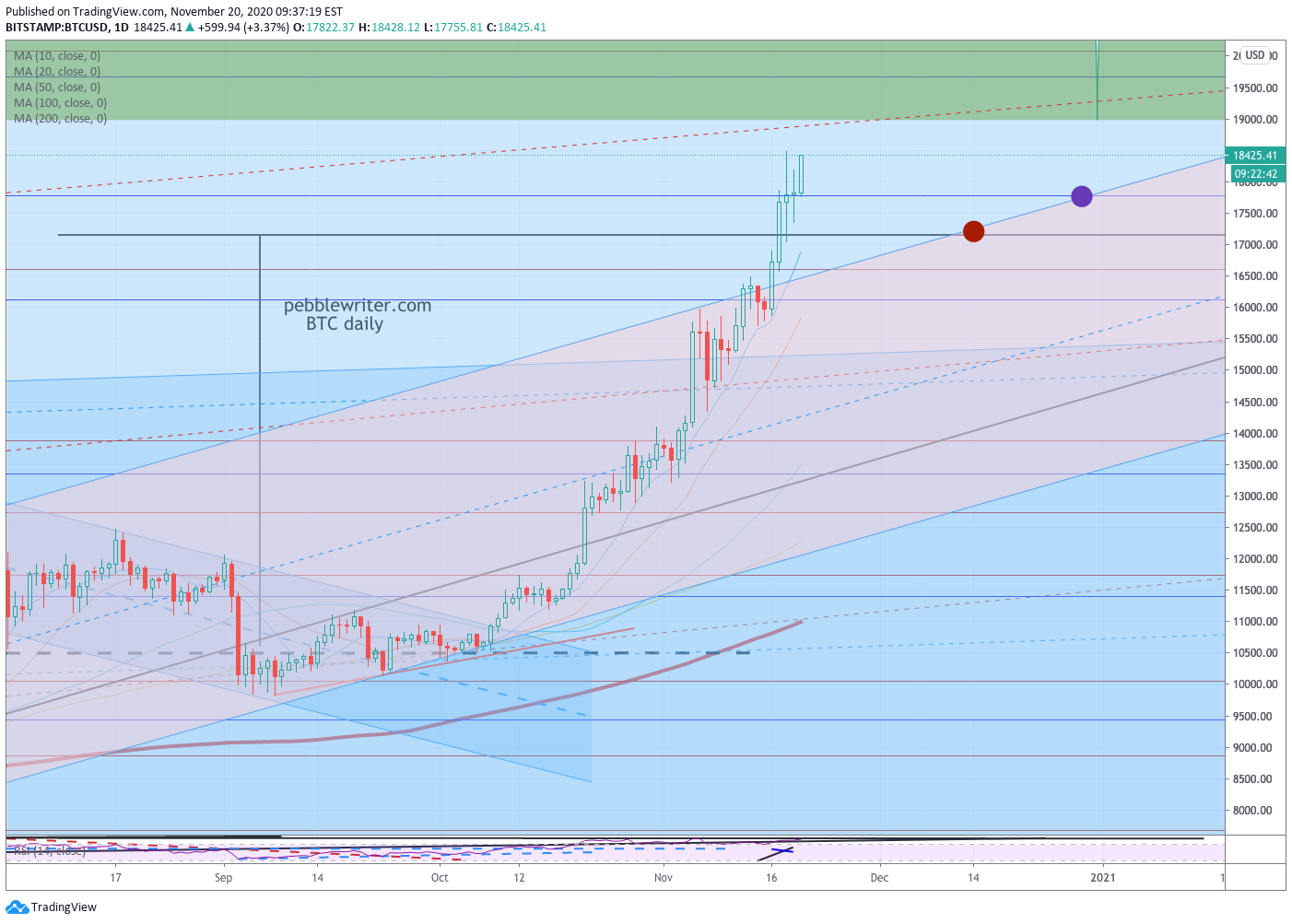

Gold, silver and BTC are all reacting as though the dollar just took a nose dive – or maybe just anticipating one.

Gold, silver and BTC are all reacting as though the dollar just took a nose dive – or maybe just anticipating one.

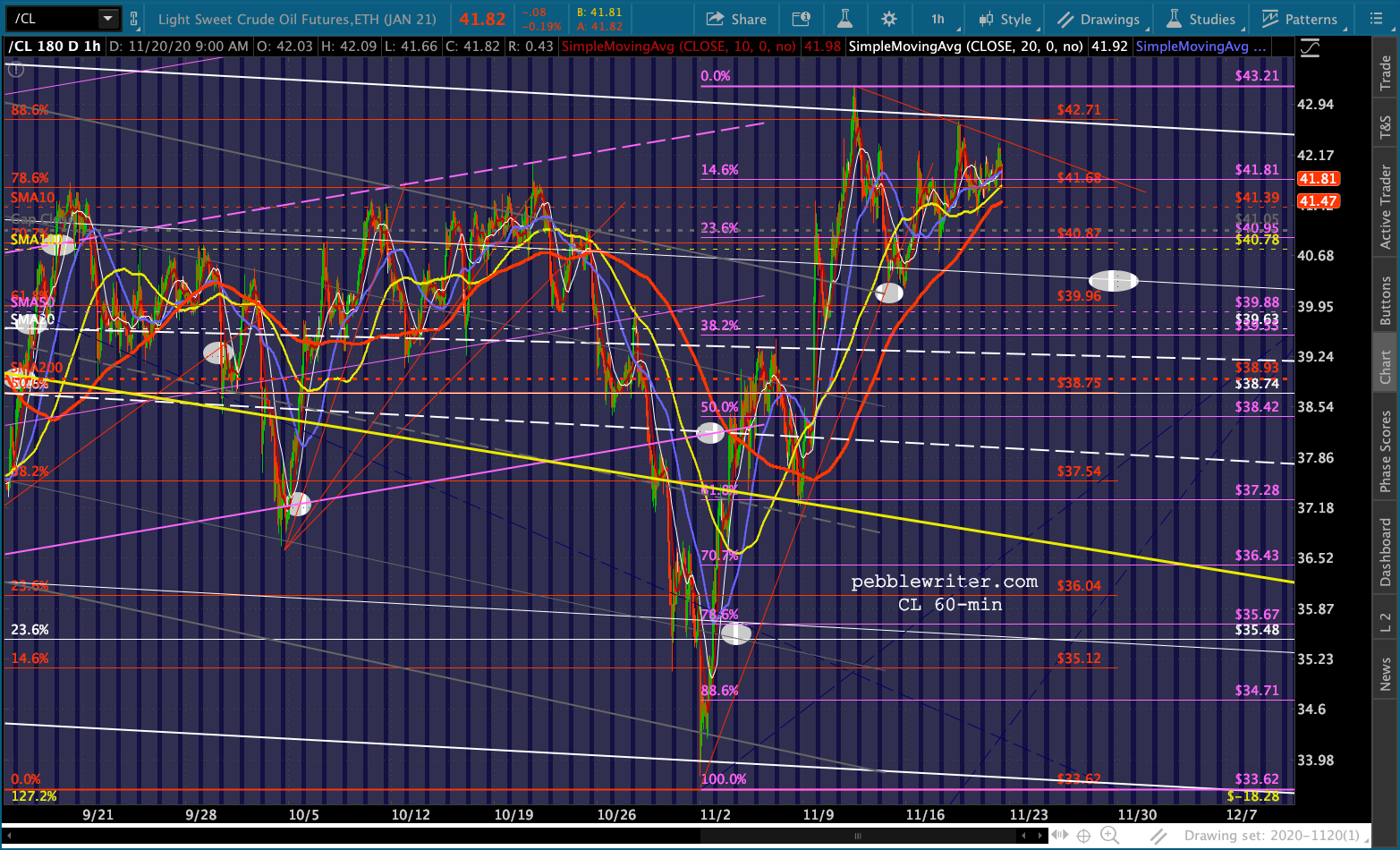

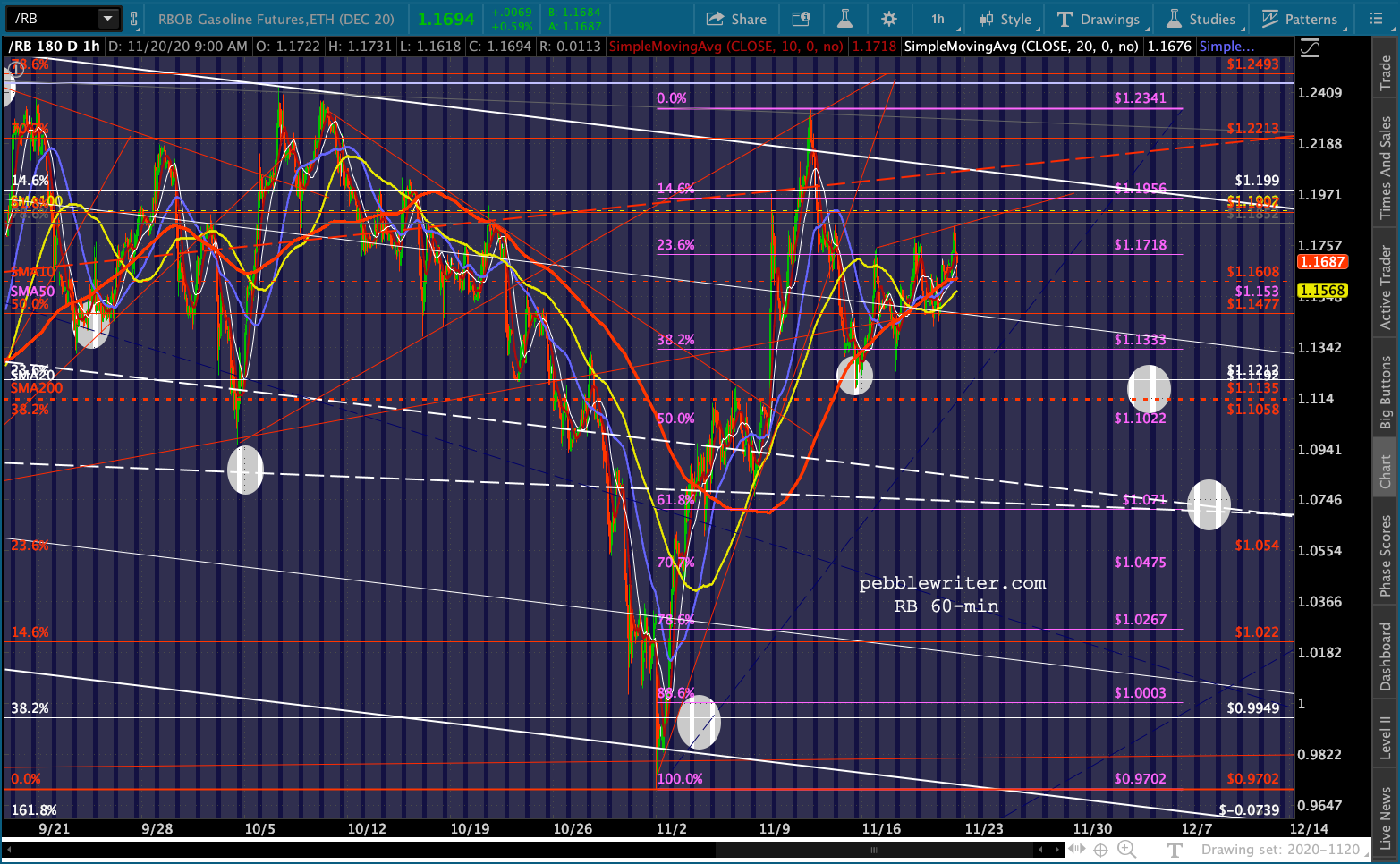

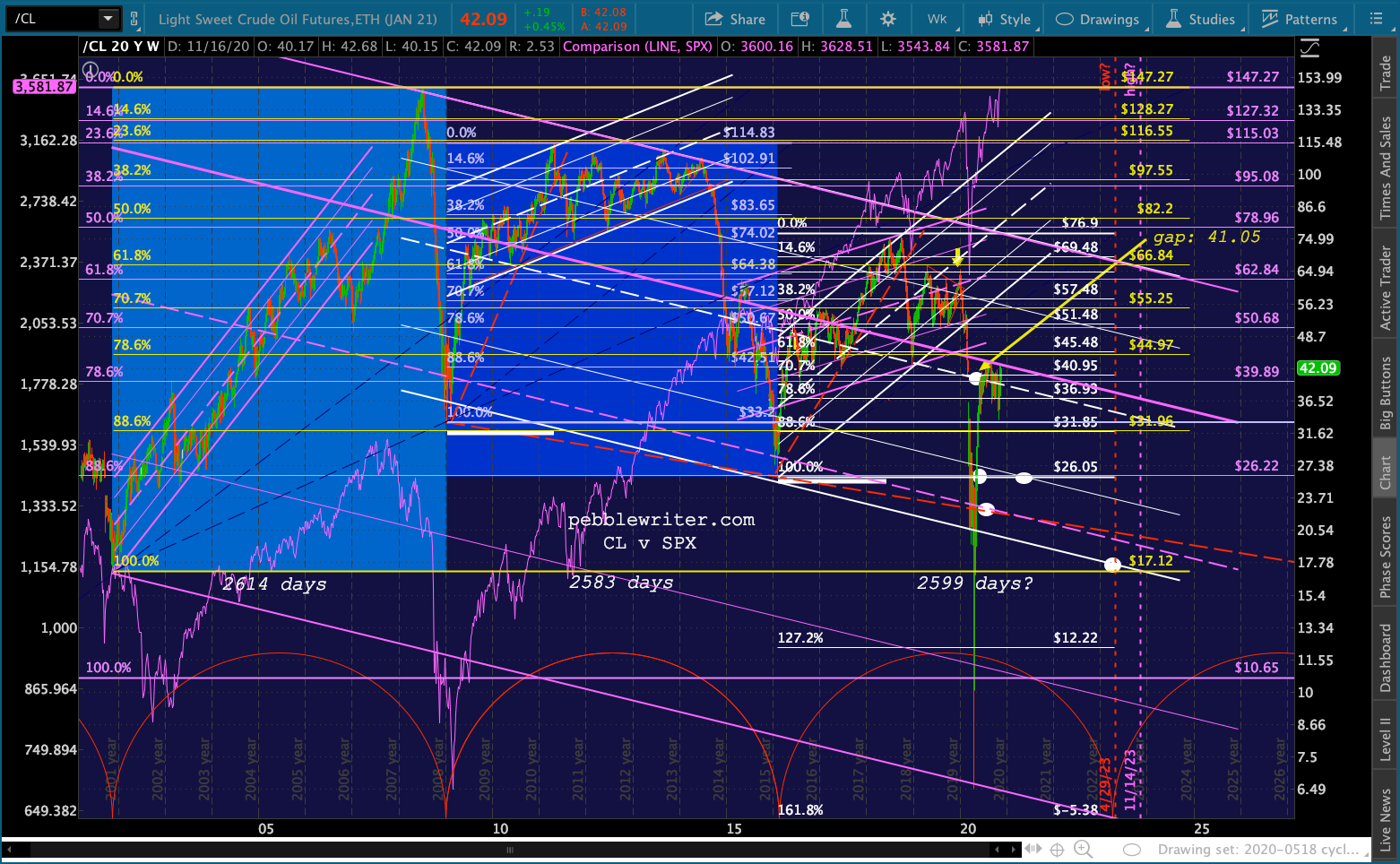

Oil and gas are behaving like they usually do on OPEX – elevated but not breaking out.

Oil and gas are behaving like they usually do on OPEX – elevated but not breaking out.

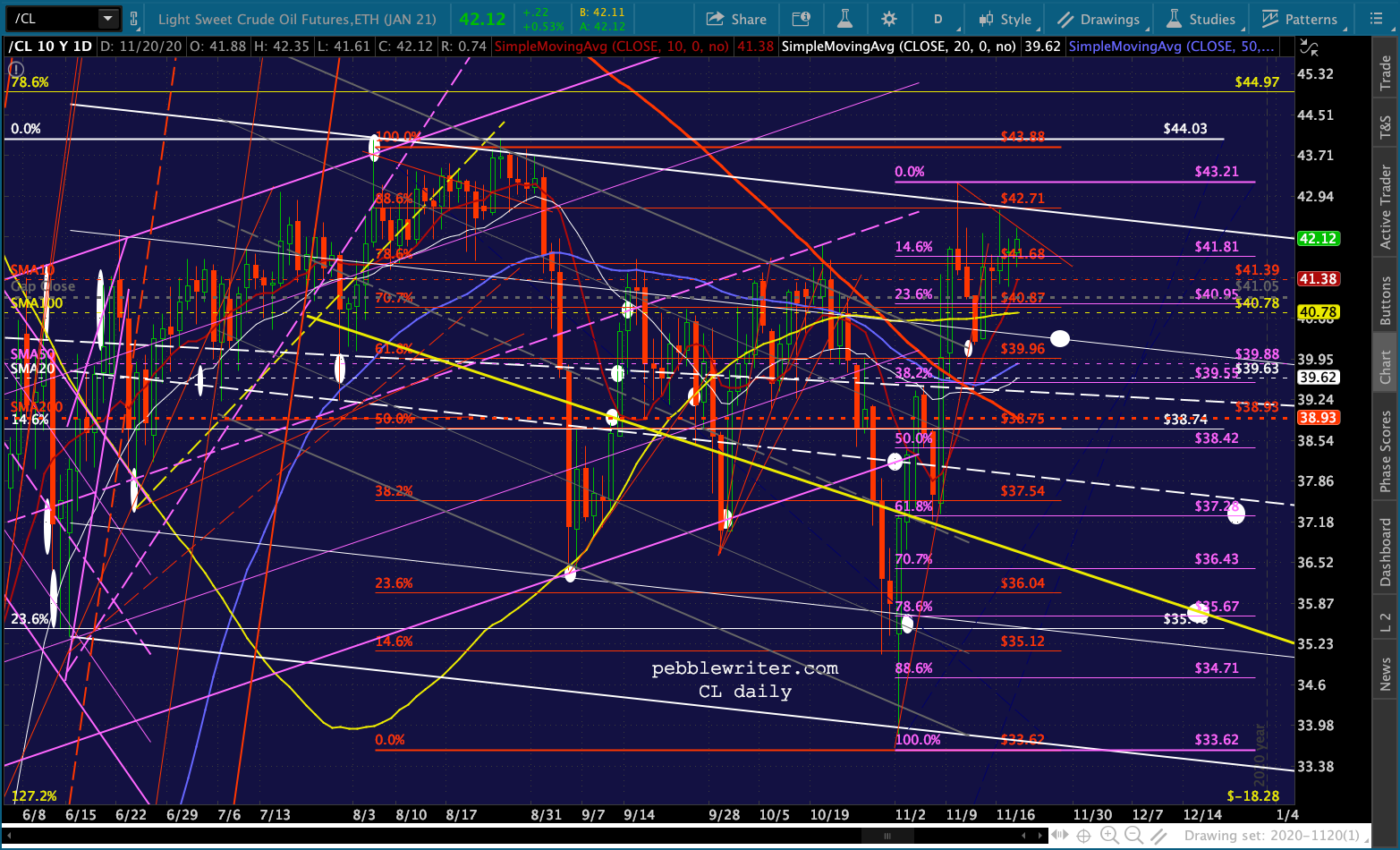

Note that I have redrawn the CL chart in order to accommodate the latest rally.

Note that I have redrawn the CL chart in order to accommodate the latest rally.

The initial falling channel is now shown in gray. It was already backtested, though it could be again as long as CL continues to decline – which it should after retracing .886 of its Aug-Nov drop. The primary falling channel is now shown in white – a very big, lumbering, gently falling channel that leaves plenty of room for volatility.  The falling yellow TL, BTW, is the path to our April 2023 target of 17.12 – seen on the chart below.

The falling yellow TL, BTW, is the path to our April 2023 target of 17.12 – seen on the chart below.

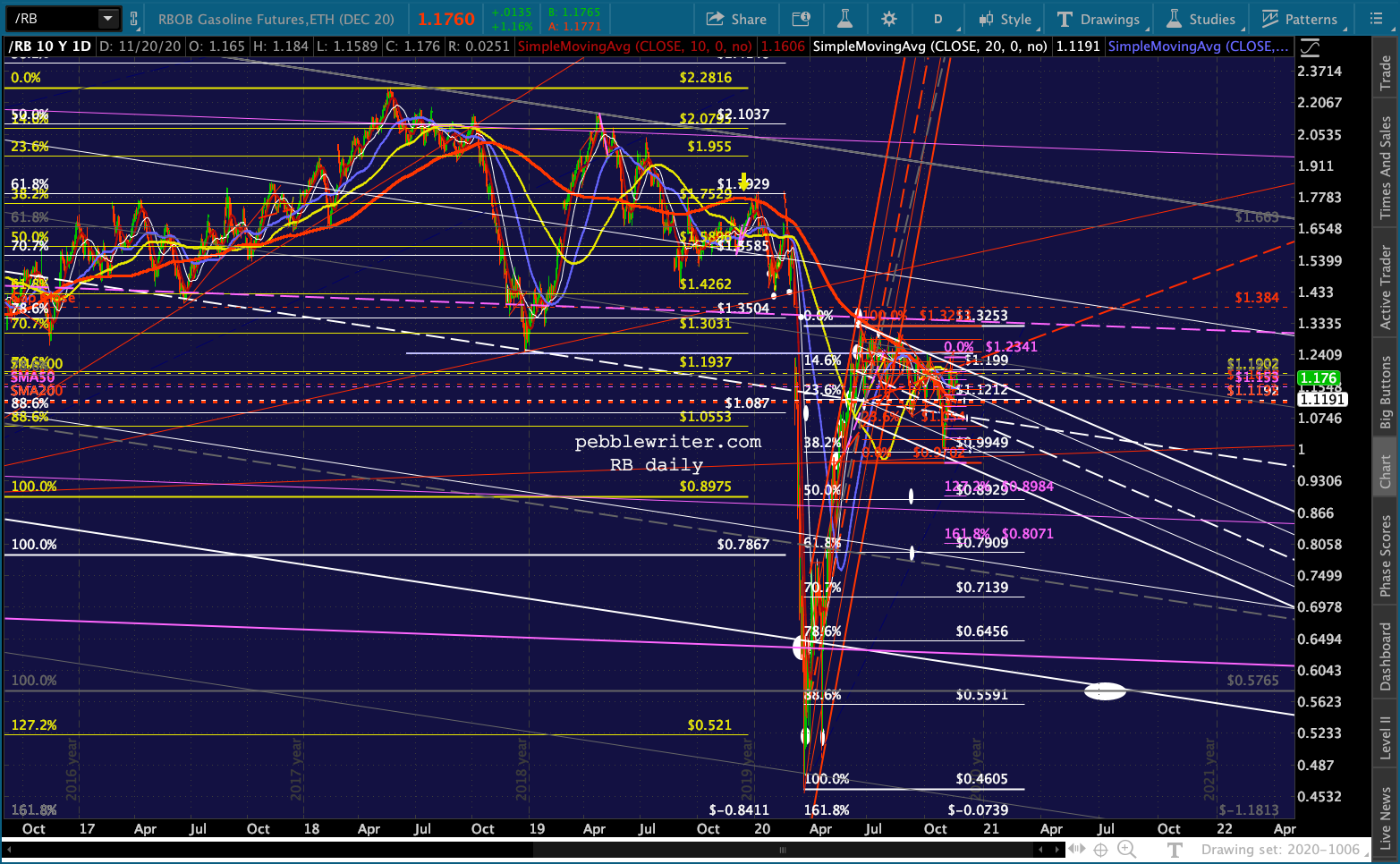

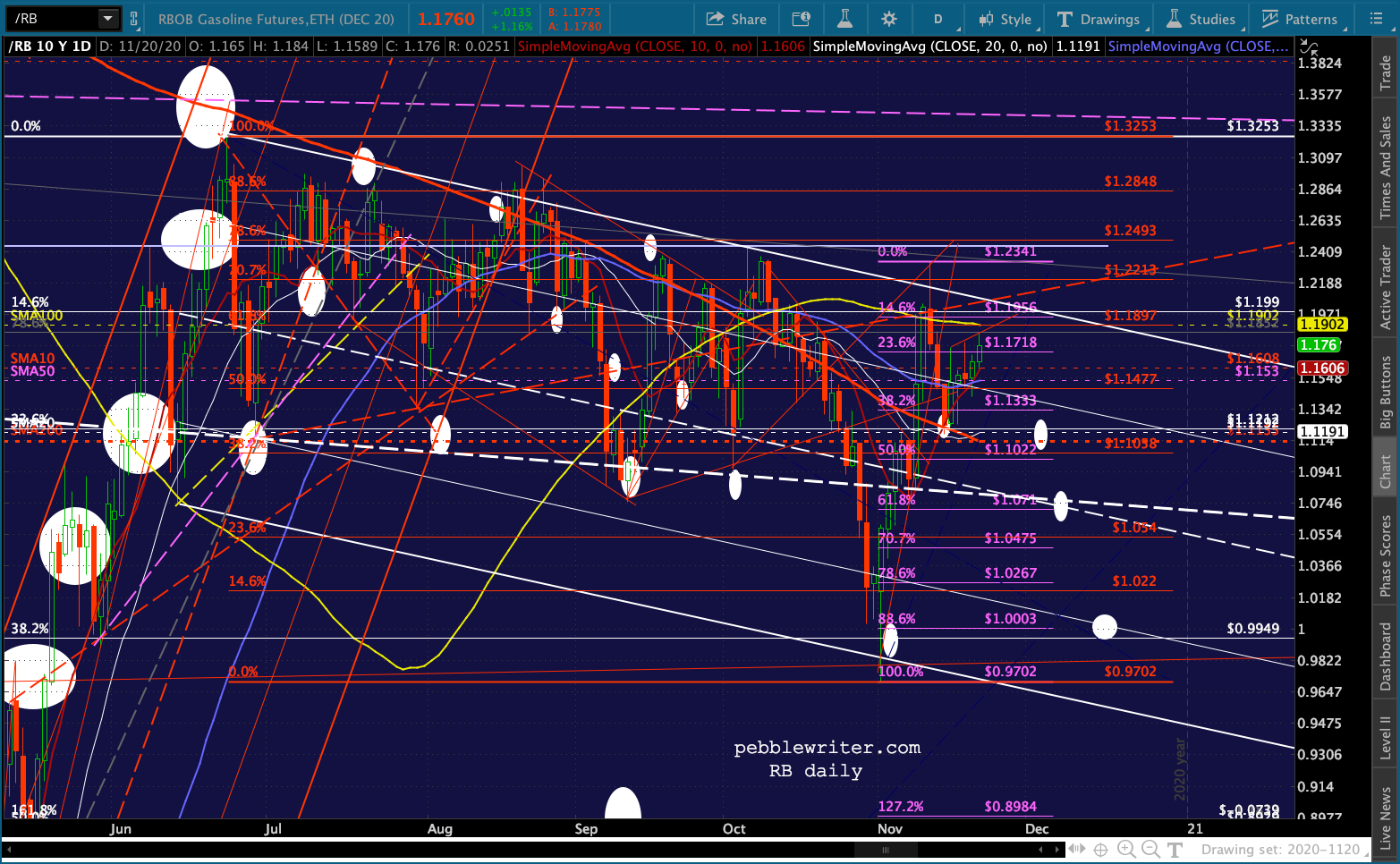

RB’s falling white channel is still intact.

RB’s falling white channel is still intact.