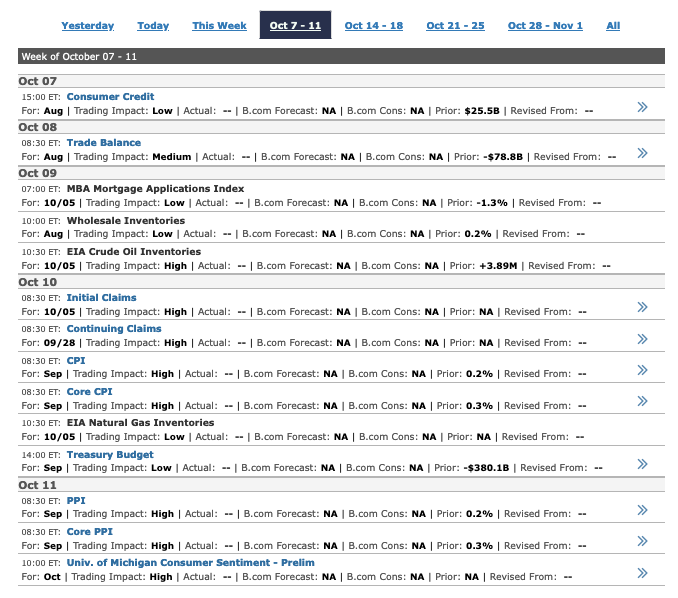

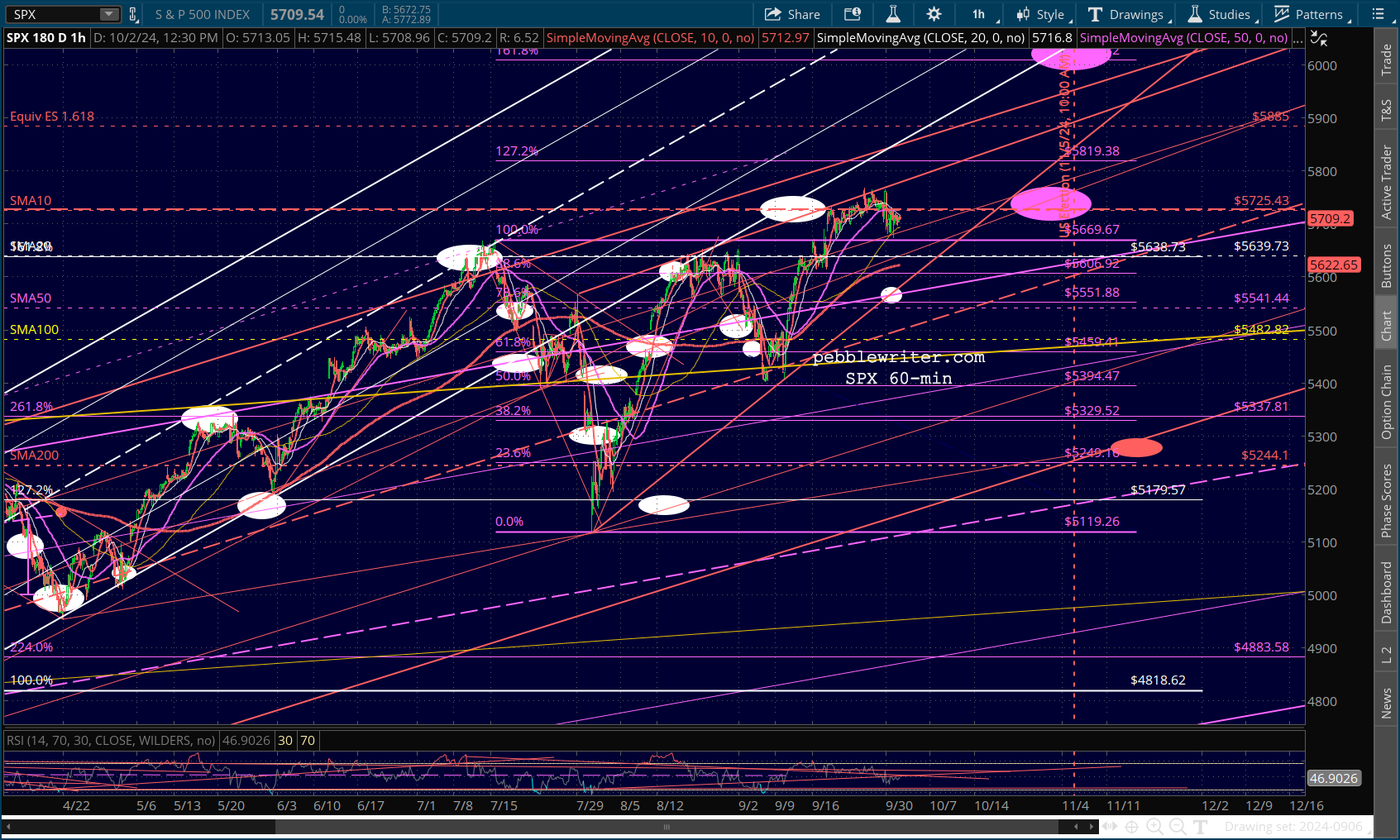

In a week fraught with geopolitical danger, the market has managed to thread the needle thus far – holding support when it counted. Even if it manages to shrug off tomorrow’s nonfarm payroll print, it still faces CPI and PPI next week.

continued for members…

continued for members…

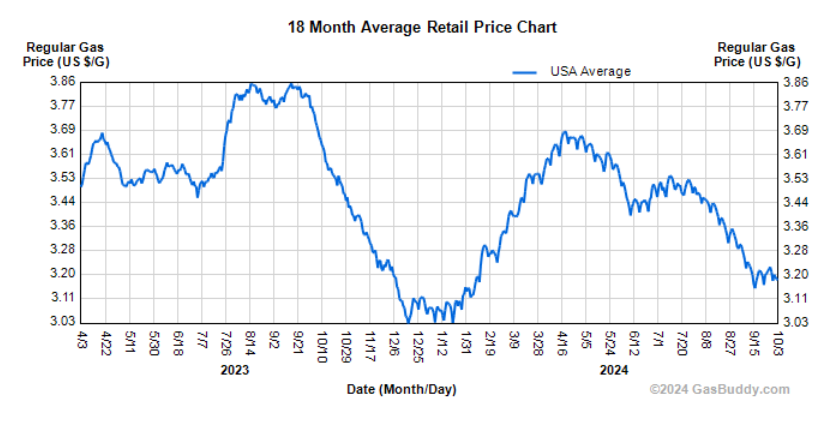

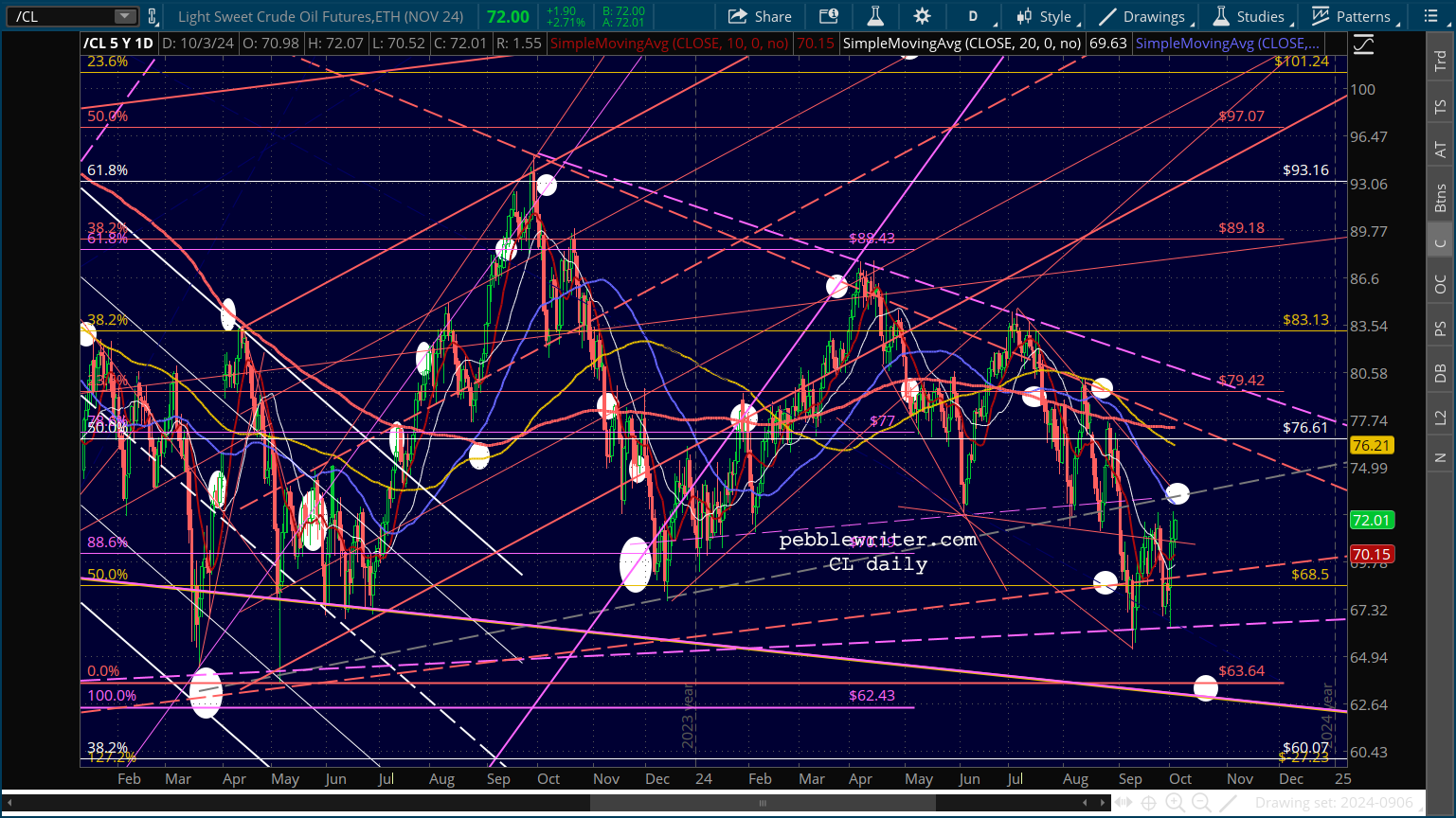

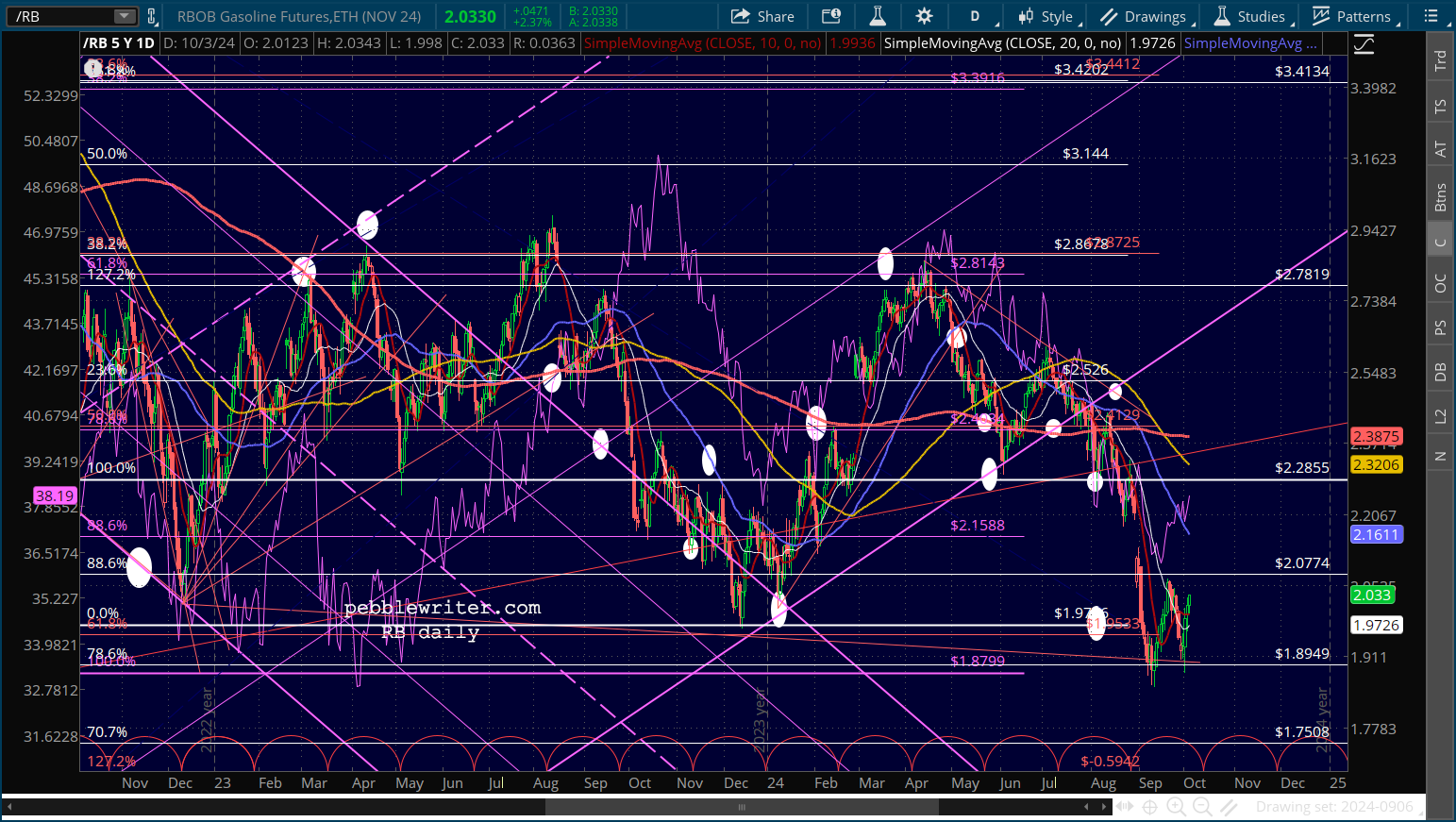

So far, the goings on in the Middle East have not affected the price of gasoline in the US.

So far, the goings on in the Middle East have not affected the price of gasoline in the US. But, that could change at any moment, so the risk we’ve been talking about all week continues. Higher gas prices = higher inflation. But, if we can get past next week’s inflation prints – which reflect last month’s inflation – then the market stands a better chance of keeping things together until the election.

But, that could change at any moment, so the risk we’ve been talking about all week continues. Higher gas prices = higher inflation. But, if we can get past next week’s inflation prints – which reflect last month’s inflation – then the market stands a better chance of keeping things together until the election.

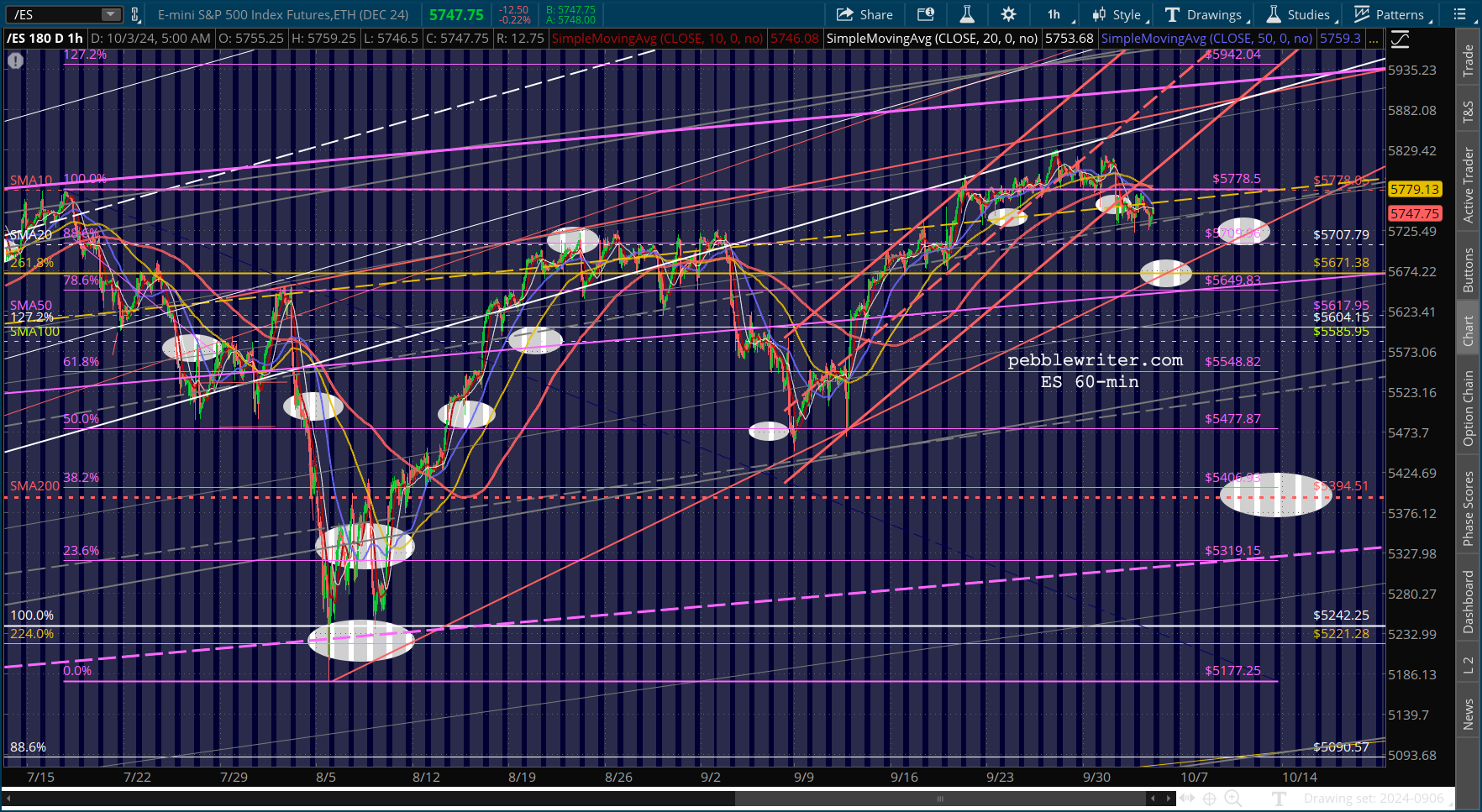

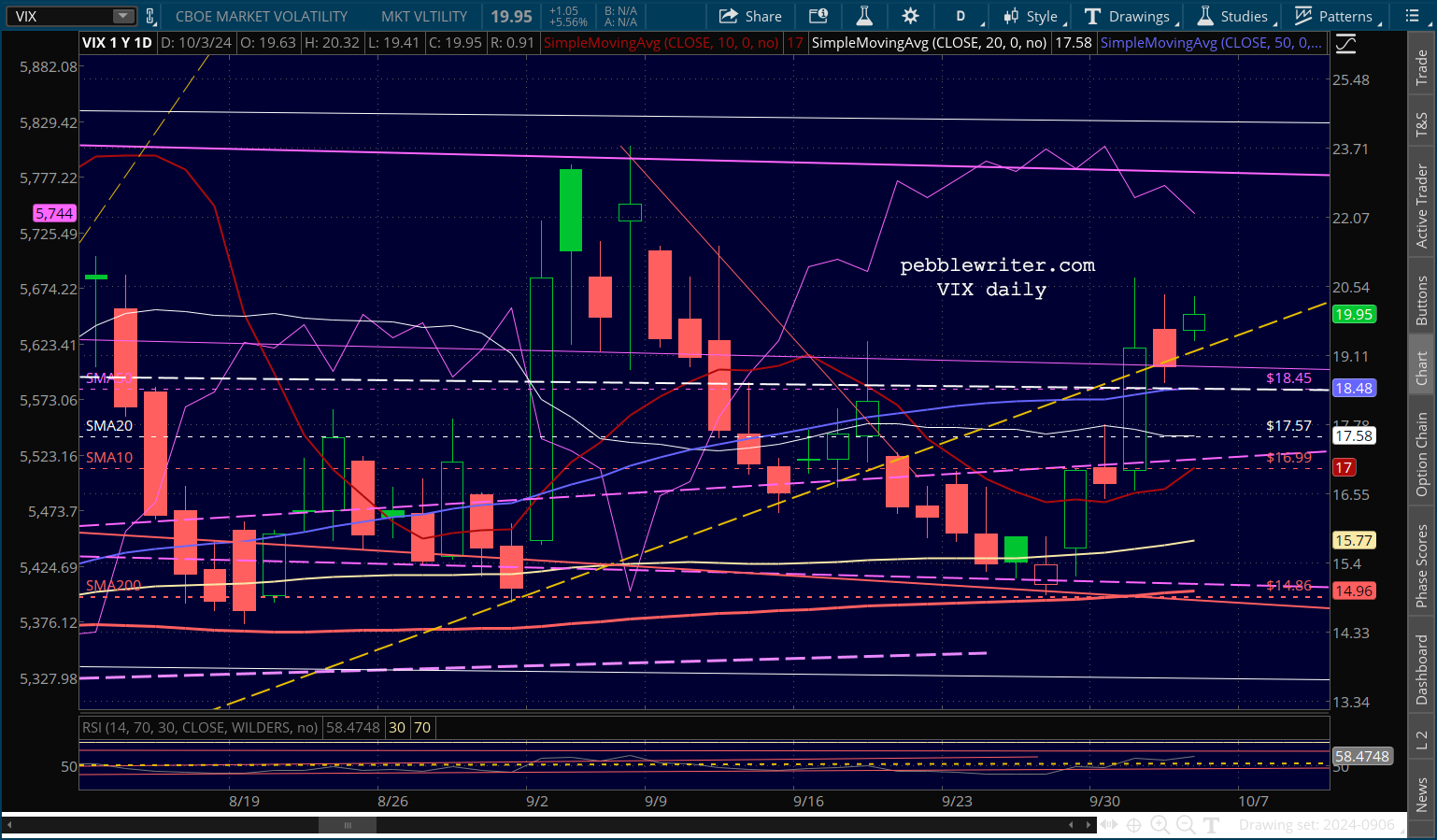

Note that VIX remains not only above the SMA200, but the TL from Jul 19 as well. The SMA10 is also close to rising back above the SMA20.

Note that VIX remains not only above the SMA200, but the TL from Jul 19 as well. The SMA10 is also close to rising back above the SMA20.

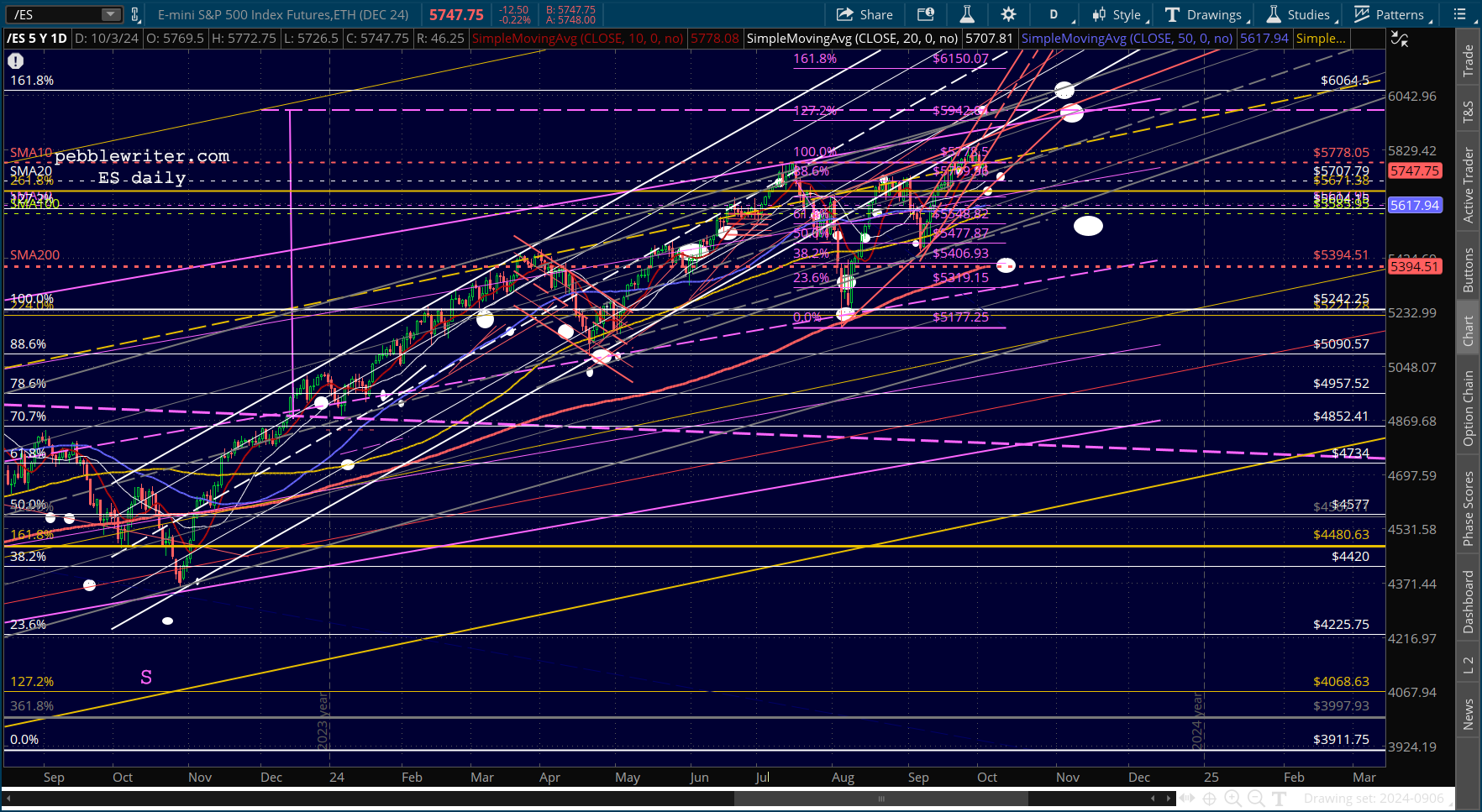

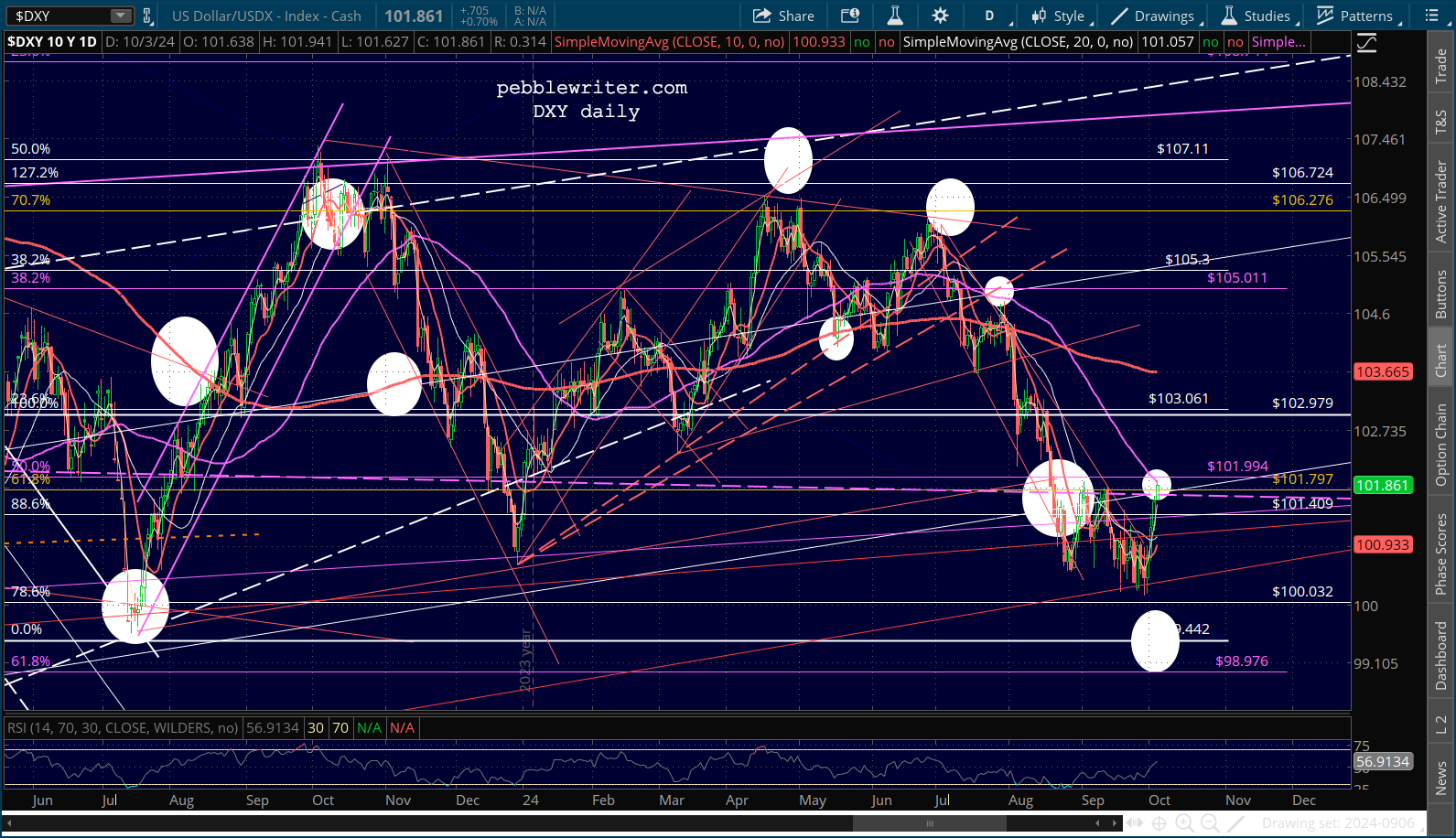

DXY has reached our SMA50 target.

DXY has reached our SMA50 target. And, CL and RB have more upside potential…

And, CL and RB have more upside potential…

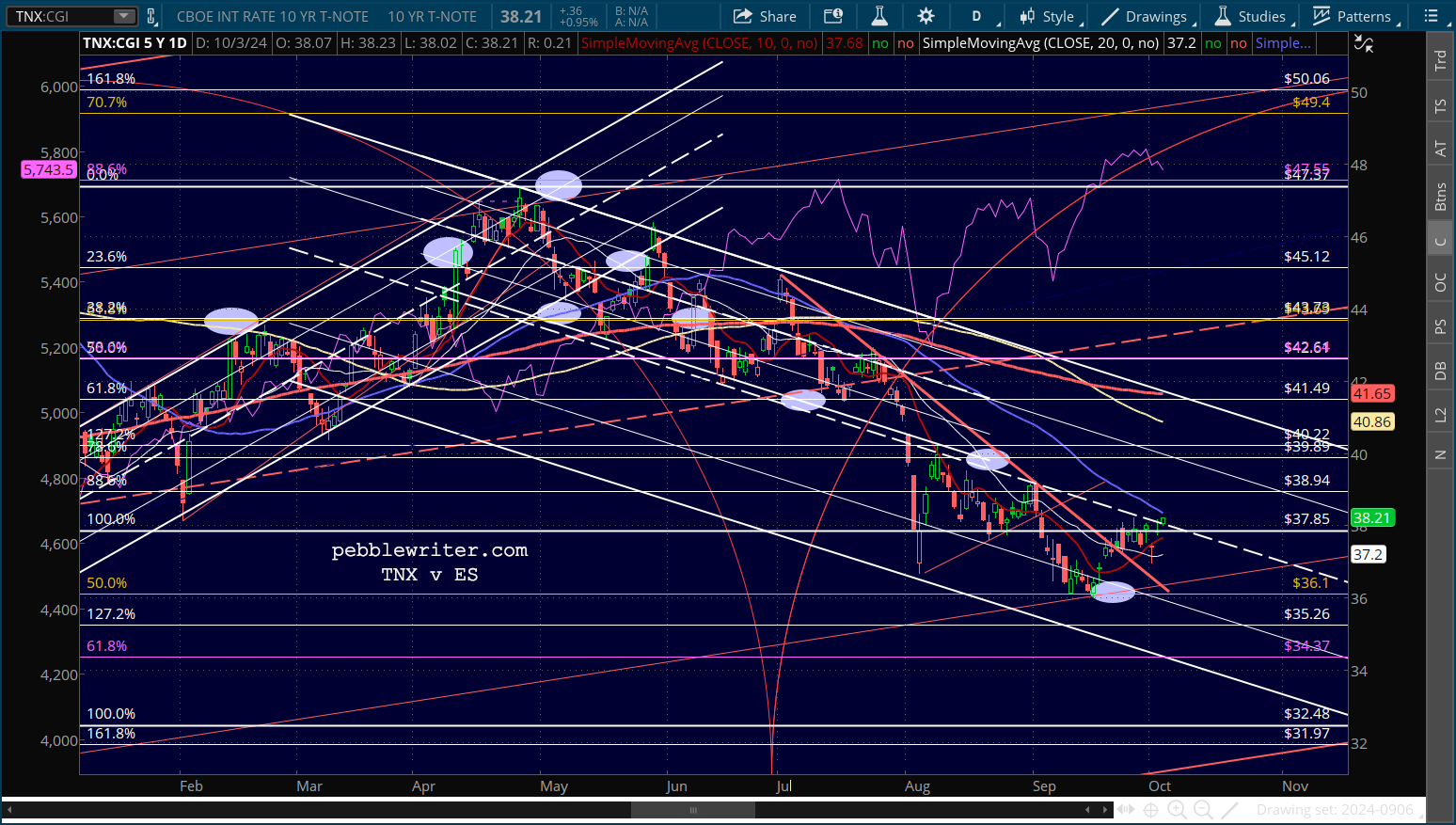

…even as TNX reaches resistance at the white channel midline and SMA50.

…even as TNX reaches resistance at the white channel midline and SMA50. Stay frosty.

Stay frosty.