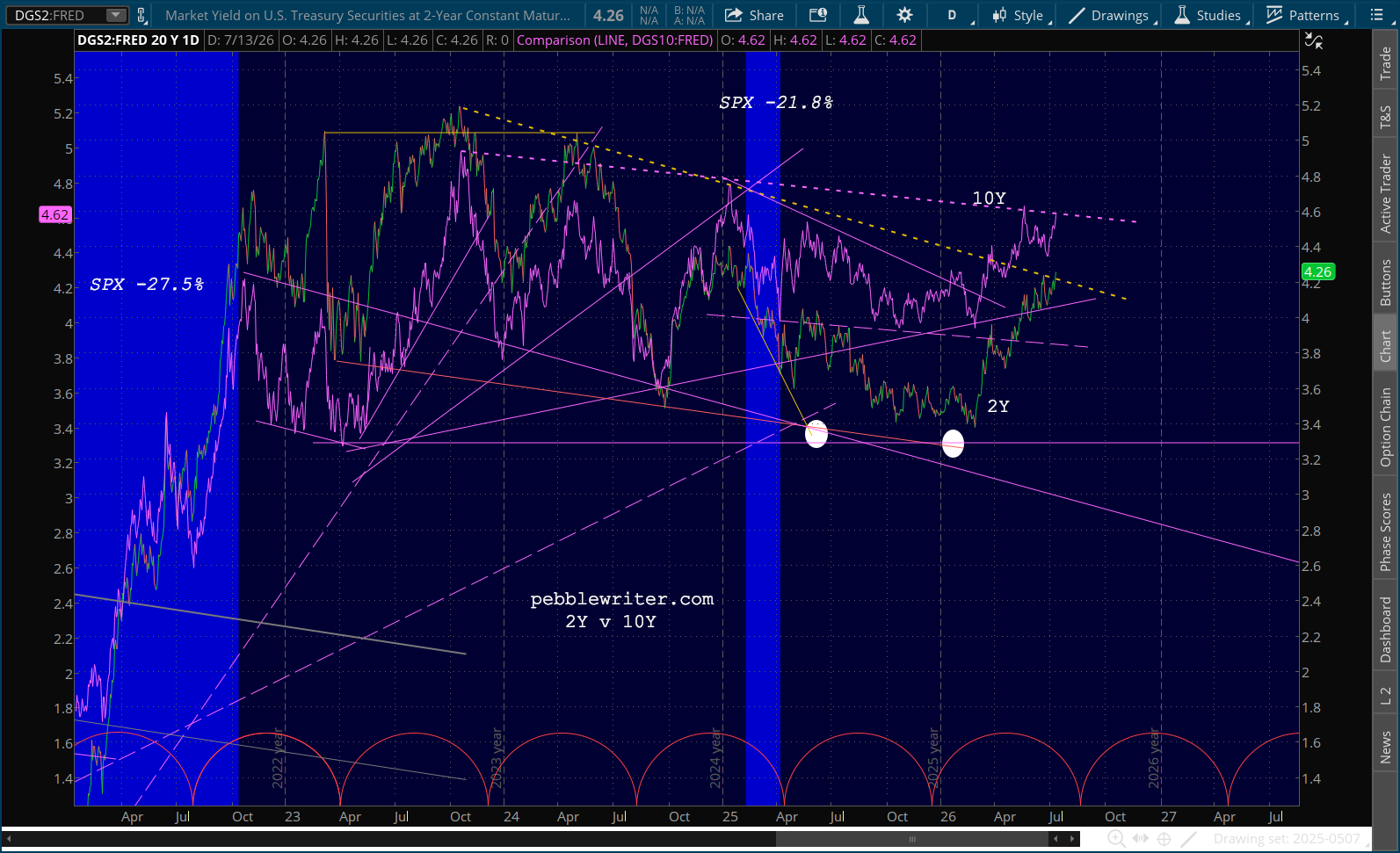

The bond market is once again saying the quiet part out loud. Both the 2Y and the 10Y were bumping up against trend lines which posed breakout risk when both CPI and PPI both posted inflation data that was well below expectations – in fact, the lowest since the depths of the COVID crisis.

Remember, these prints come from the Bureau of Labor Statistics – the very same organization that used to be run by Erika McEntarfer, who was fired by Trump when the BLS released employment data that wasn’t favorable to him. He posted that she was incompetent and unqualified and that the data was manipulated.

Important numbers like this must be fair and accurate, they can’t be manipulated for political purposes.

I couldn’t agree more. The market tanked, as investors everywhere wondered what it meant now that we couldn’t trust the BLS to operate independently of politics.

Now we know. The 10Y has recently broken out, thanks largely to Trump being outplayed by the Iranians, but hasn’t yet popped above the TL from Oct 2023. It would undoubtedly be much lower if Trump hadn’t started the war in the first place. But, here we are.

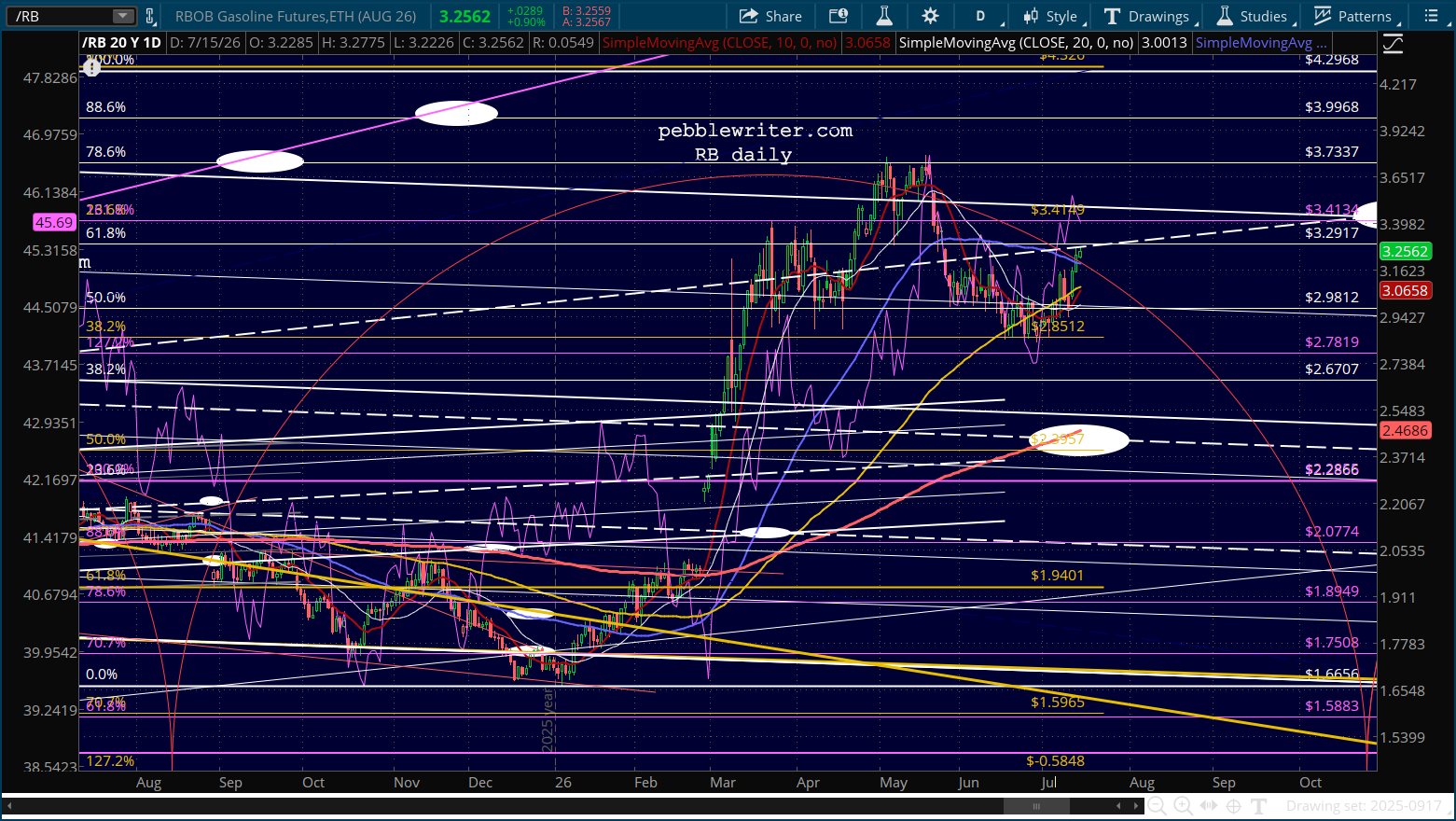

Algos are less impressed than they were yesterday, perhaps due to the latest attacks by both Iran and the US which have left CL and RB pushing new highs.

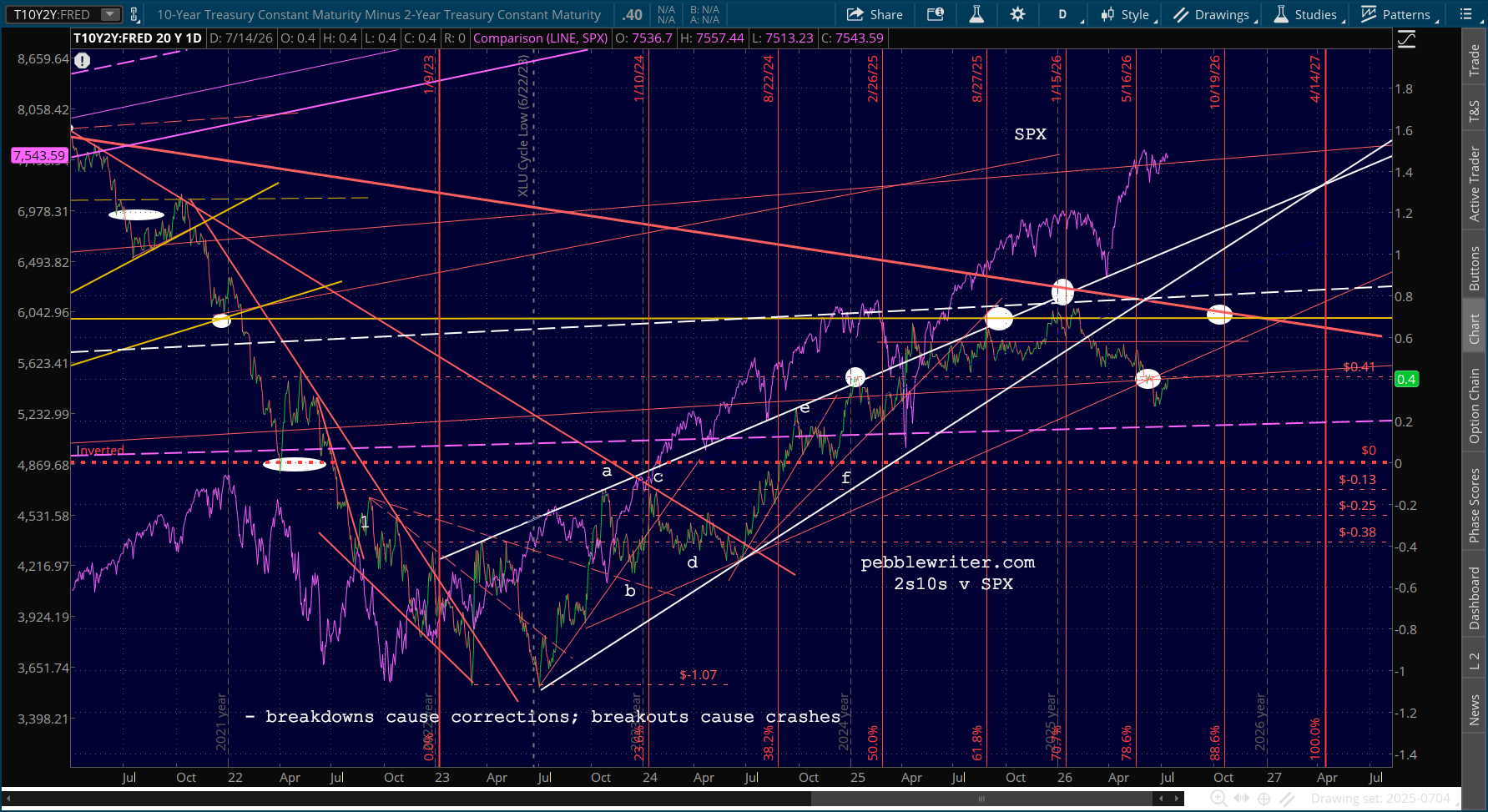

The 10Y has retreated somewhat, leaving the 2s10s backtesting the TL from Sep 2023.

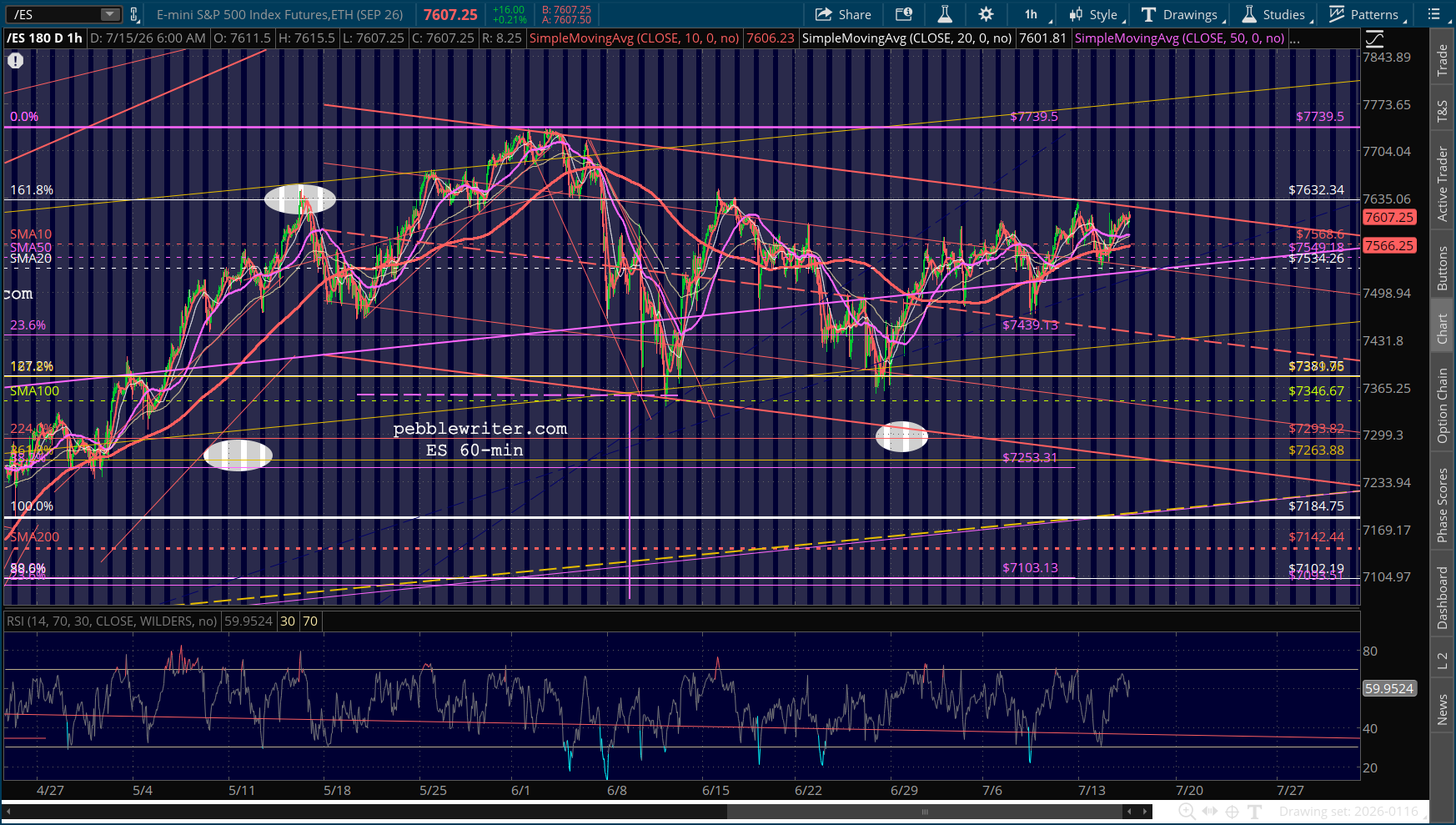

Futures are up modestly.

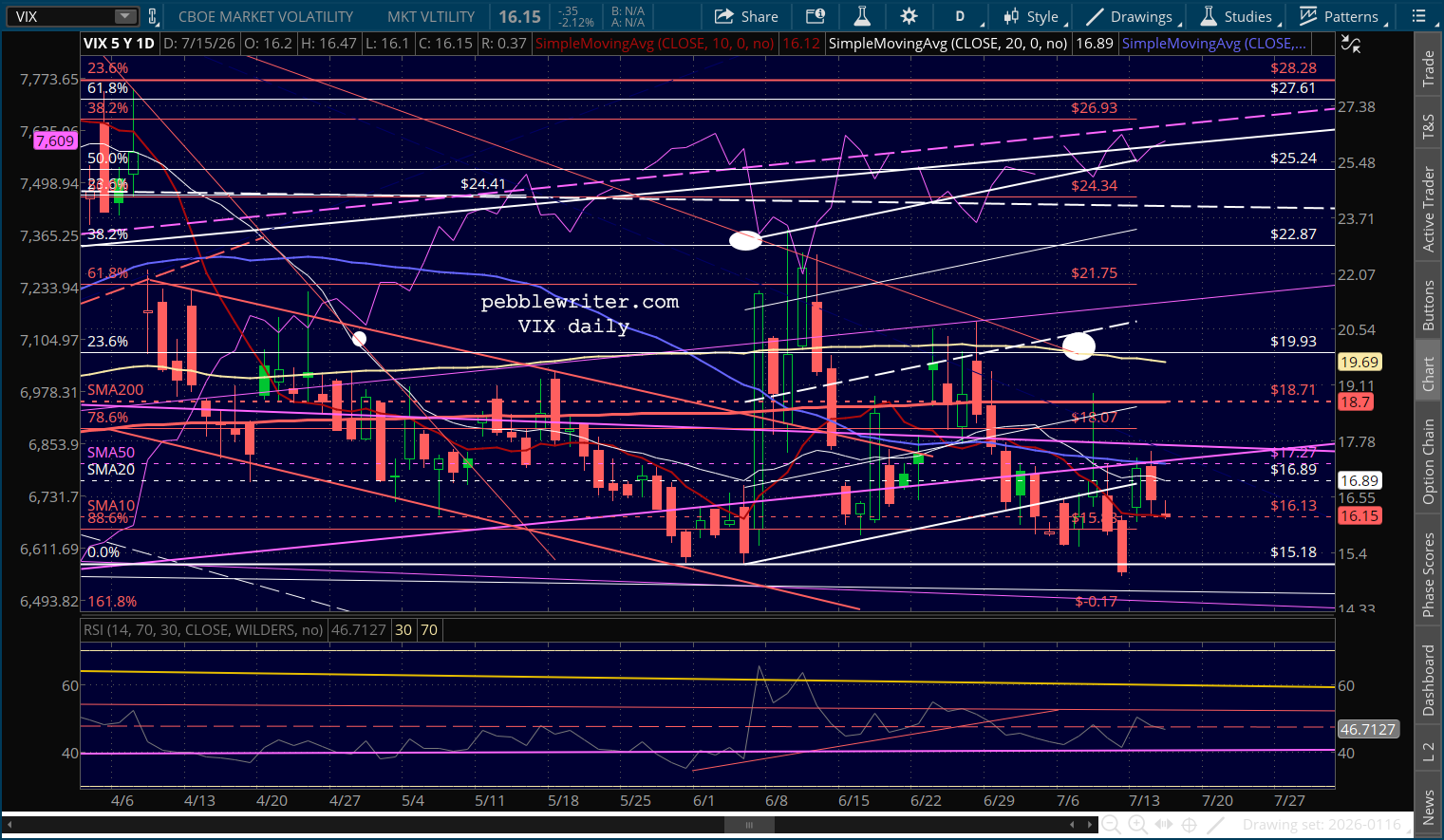

VIX’s dip back below its SMA10 is all it would take for the bulls to keep the momentum going.

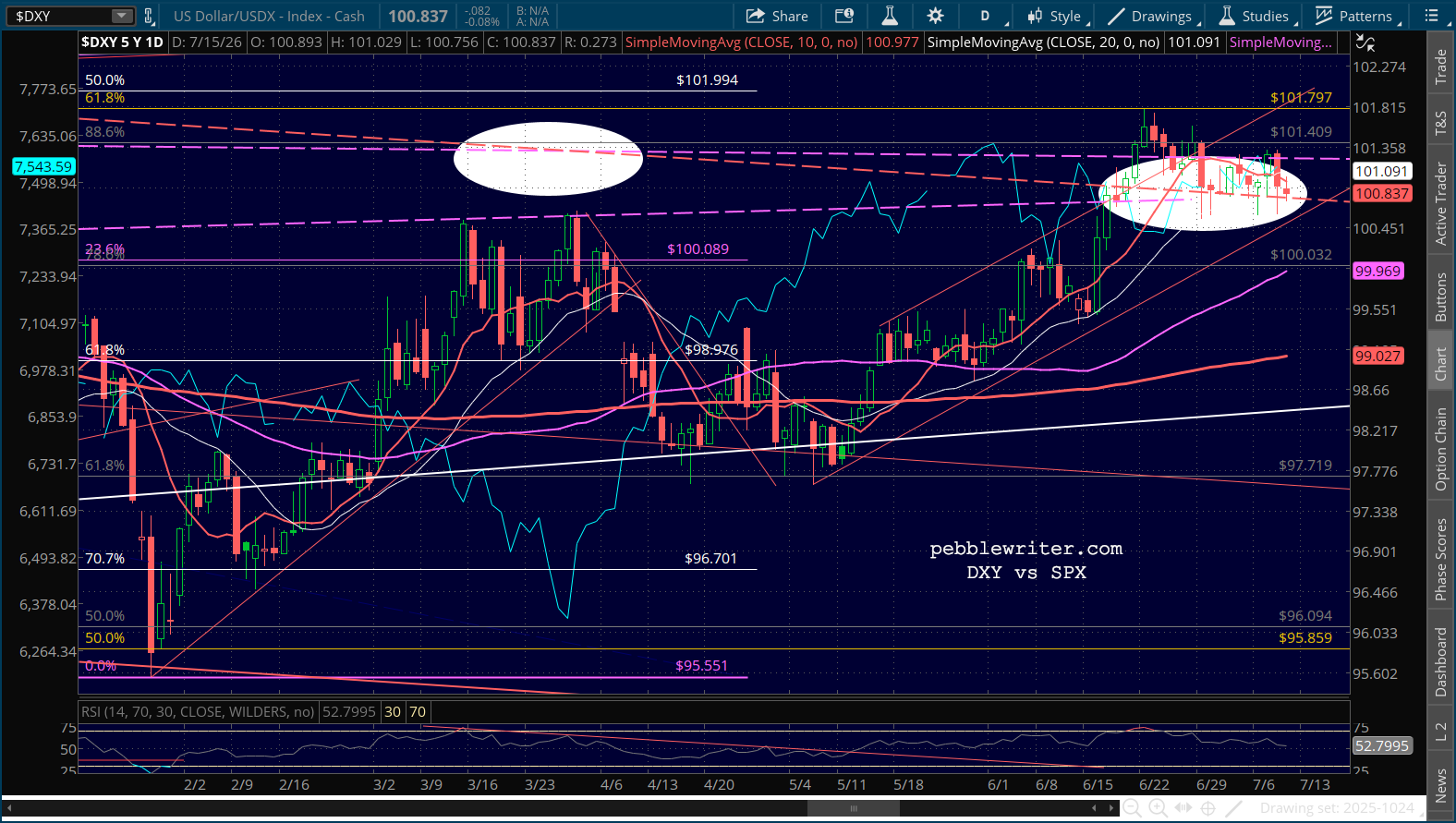

And, the DXY is continuing to trend sideways, for now at least.

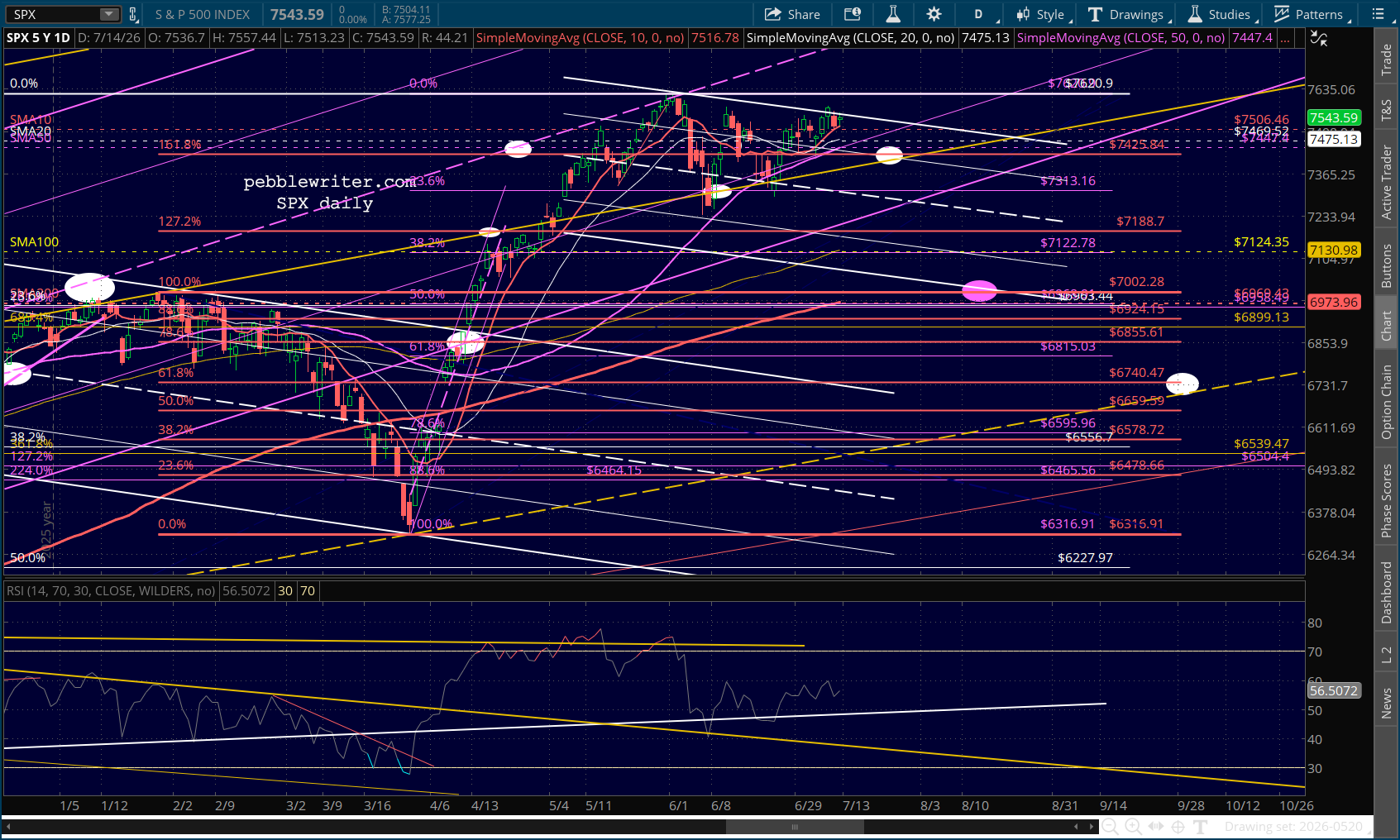

SPX/ES are both at a point where it would be quite easy to break out. But, at the same time, the SMA200 is coming up on the previous high – an enticing target if a backtest will be allowed. There are plenty of available catalysts – both real and fabricated – in either case.

GLTA

Leave a Reply

You must be logged in to post a comment.