I can’t begin to count the number of times I’ve written about the manipulation of VIX futures over the past several years. With 80% of daily equity volume tied to algorithmic inputs, it’s one of several powerful methods by which equity markets are propped up.

My comments have drawn a fair amount of scorn over the years, particularly from those who reject the idea that central bankers are involved in propping up equity prices. That scorn waned over the past year, however, as it became increasingly obvious that VIX was under more pressure than market forces alone would generate.

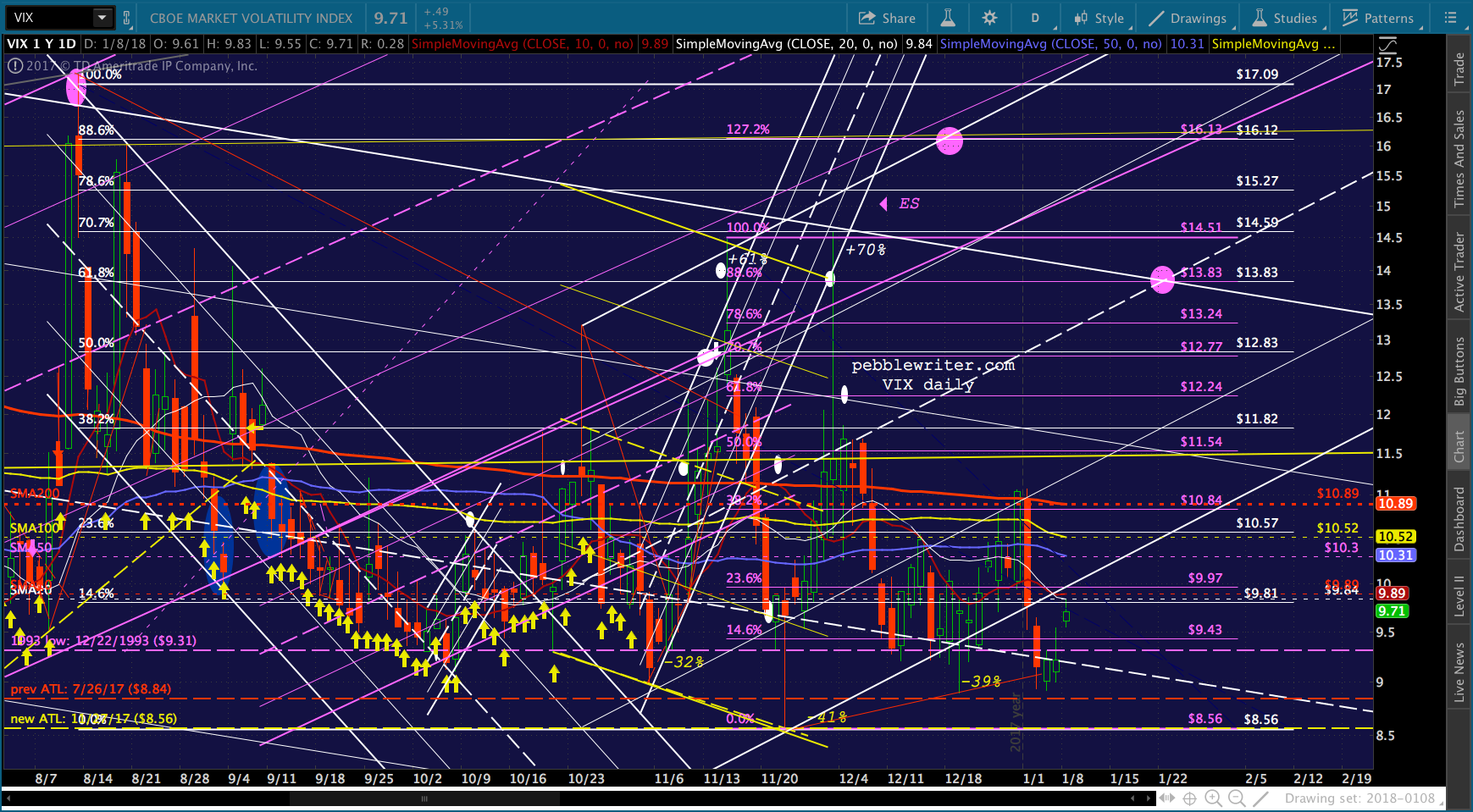

A favorite graph of mine depicts the large channel that has guided VIX gradually higher since Mar 2009 — the depths of the Great Financial Crisis. VIX tagged it roughly once a year (the yellow arrows) until December 2016. Since then, VIX has tagged or dropped below it about 75% of the time. The reasons are perfectly clear. Having plunged 12.5% and 14.5% in two severe corrections in 2015 and early 2016, SPX had attempted a breakout in July 2016. The breakout failed, however, and SPX fell back below support (the neckline of a IH&S Pattern) as the US election approached.

The reasons are perfectly clear. Having plunged 12.5% and 14.5% in two severe corrections in 2015 and early 2016, SPX had attempted a breakout in July 2016. The breakout failed, however, and SPX fell back below support (the neckline of a IH&S Pattern) as the US election approached.

When Trump was announced the winner, equity futures plummeted 4.5%.  Central banks panicked, and took decisive action. USDJPY, which had oringally plunged on the news, suddenly spiked higher — on its way to a 20% gain over the next month. VIX, which had spiked on the news, suddenly began to sell off — even while equity futures were plummeting. This was the equivalent of cancelling ones homeowner’s insurance as a tornado comes into view.

Central banks panicked, and took decisive action. USDJPY, which had oringally plunged on the news, suddenly spiked higher — on its way to a 20% gain over the next month. VIX, which had spiked on the news, suddenly began to sell off — even while equity futures were plummeting. This was the equivalent of cancelling ones homeowner’s insurance as a tornado comes into view.

By the time the market opened the following morning, futures were back in the green. SPX actually booked a gain. It was a gutsy move, but it worked. It worked so well, in fact, that it continues to this day. Moves above VIX’s channel bottom continue to be a rarity and have been largely responsible for the last 32% of gains in SPX.

Who, in their right mind, was ballsy enough to short VIX in the midst of a 4.5% flash crash? Who changed the course/cost of volatility protection, resulting in new all-time lows? Who continues to hammer VIX every time stocks threaten to dip more than the allowed amount? Once the musing of tin-foil-hatted conspiracy theorists, we now have confirmation from incoming Fed Chair Jerome Powell.

Who, in their right mind, was ballsy enough to short VIX in the midst of a 4.5% flash crash? Who changed the course/cost of volatility protection, resulting in new all-time lows? Who continues to hammer VIX every time stocks threaten to dip more than the allowed amount? Once the musing of tin-foil-hatted conspiracy theorists, we now have confirmation from incoming Fed Chair Jerome Powell.

Excerpted from the transcripts of the FOMC meeting, Oct 23-24, 2012.

MR. POWELL.

I have concerns about more purchases. As others have pointed out, the dealer community is now assuming close to a $4 trillion balance sheet and purchases through the first quarter of 2014. I admit that is a much stronger reaction than I anticipated, and I am uncomfortable with it for a couple of reasons.

First, the question, why stop at $4 trillion? The market in most cases will cheer us for doing more. It will never be enough for the market. Our models will always tell us that we are helping the economy, and I will probably always feel that those benefits are overestimated. And we will be able to tell ourselves that market function is not impaired and that inflation expectations are under control. What is to stop us, other than much faster economic growth, which it is probably not in our power to produce?

Second, I think we are actually at a point of encouraging risk-taking, and that should give us pause. Investors really do understand now that we will be there to prevent serious losses. It is not that it is easy for them to make money but that they have every incentive to take more risk, and they are doing so. Meanwhile, we look like we are blowing a fixed-income duration bubble right across the credit spectrum that will result in big losses when rates come up down the road. You can almost say that that is our strategy.

My third concern—and others have touched on it as well—is the problems of exiting from a near $4 trillion balance sheet. We’ve got a set of principles from June 2011 and have done some work since then, but it just seems to me that we seem to be way too confident that exit can be managed smoothly. Markets can be much more dynamic than we appear to think.

Take selling—we are talking about selling all of these mortgage-backed securities. Right now, we are buying the market, effectively, and private capital will begin to leave that activity and find something else to do. So when it is time for us to sell, or even to stop buying, the response could be quite strong; there is every reason to expect a strong response.

So there are a couple of ways to look at it. It is about $1.2 trillion in sales; you take 60 months, you get about $20 billion a month. That is a very doable thing, it sounds like, in a market where the norm by the middle of next year is $80 billion a month.

Another way to look at it, though, is that it’s not so much the sale, the duration; it’s also unloading our short volatility position. When you turn and say to the market, “I’ve got $1.2 trillion of these things,” it’s not just $20 billion a month— it’s the sight of the whole thing coming. And I think there is a pretty good chance that you could have quite a dynamic response in the market. And I would just say I want to understand that a lot better in the intermeeting period and leave it at that. Thank you very much, Mr. Chairman.

Today’s charts are continued below…

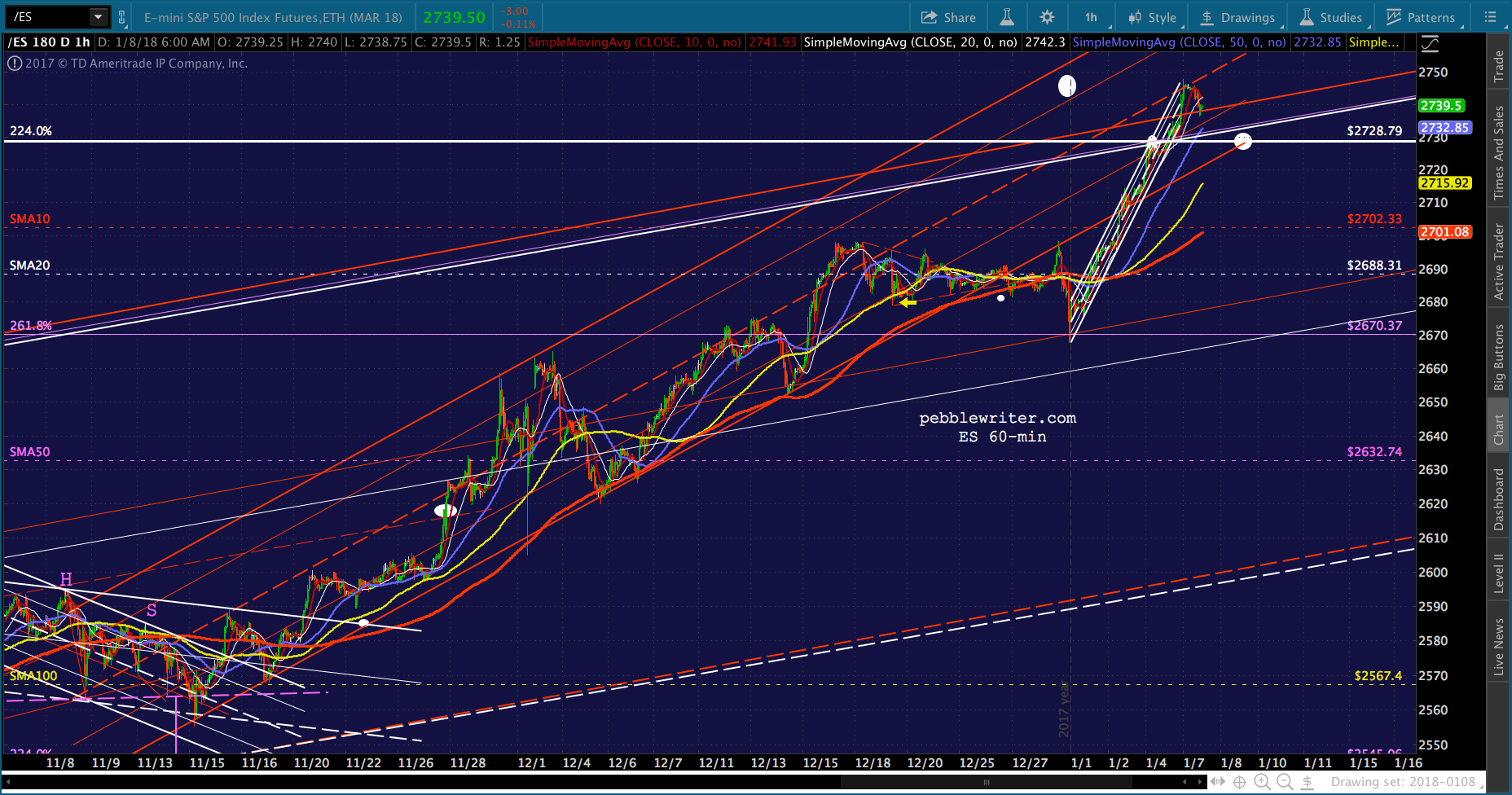

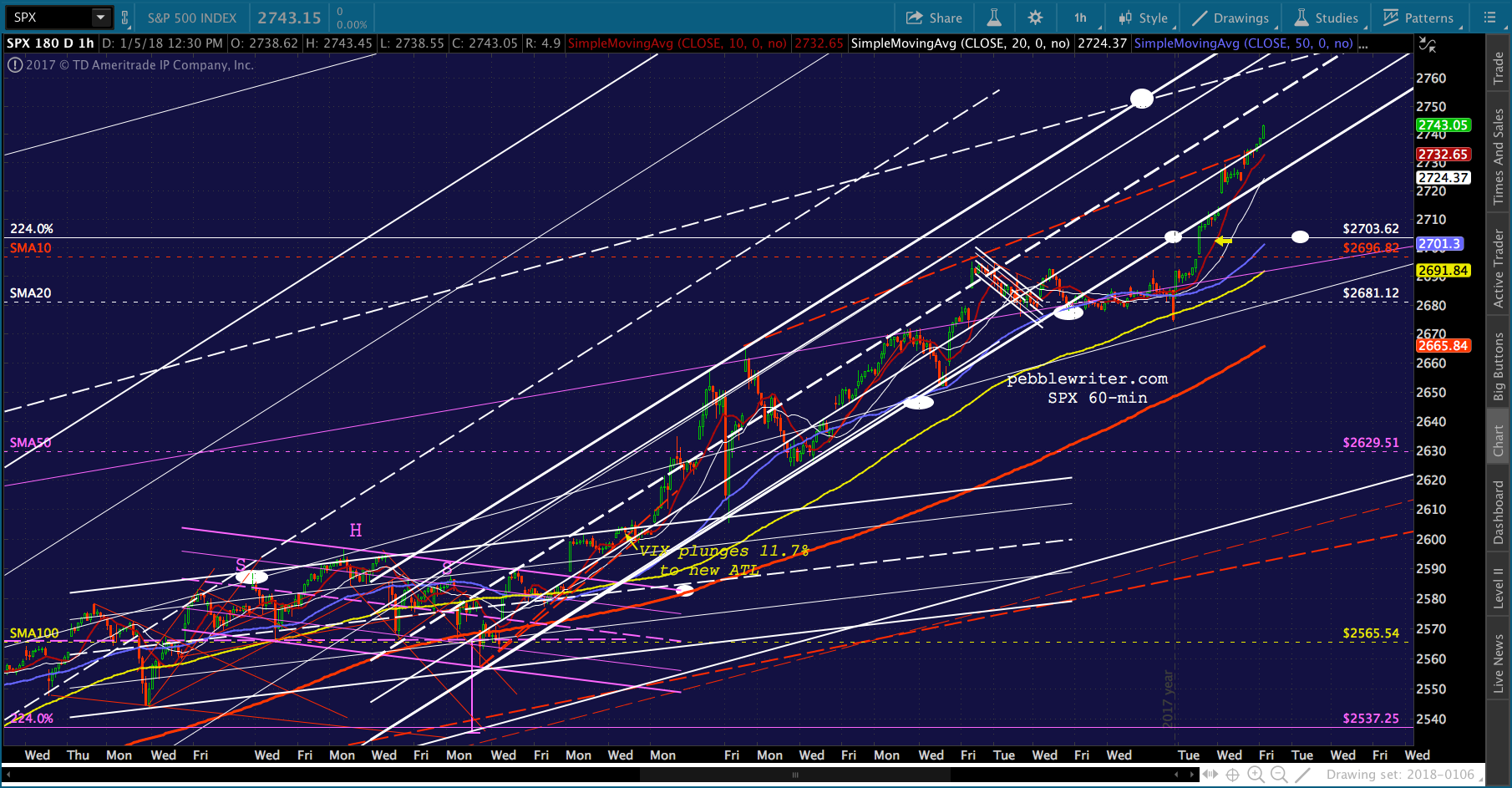

I’m looking for a backtest of ES’ 2.24 at 2728.79. If it falls, it’ll be because SPX needs to backtest its 2.24 at 2703.62. There’s a 25-pt difference between the two, so I’d not count on the SPX backtest until/unless the ES backtest doesn’t hold. The timing could be anywhere from mid-day tomorrow (Tuesday) on.

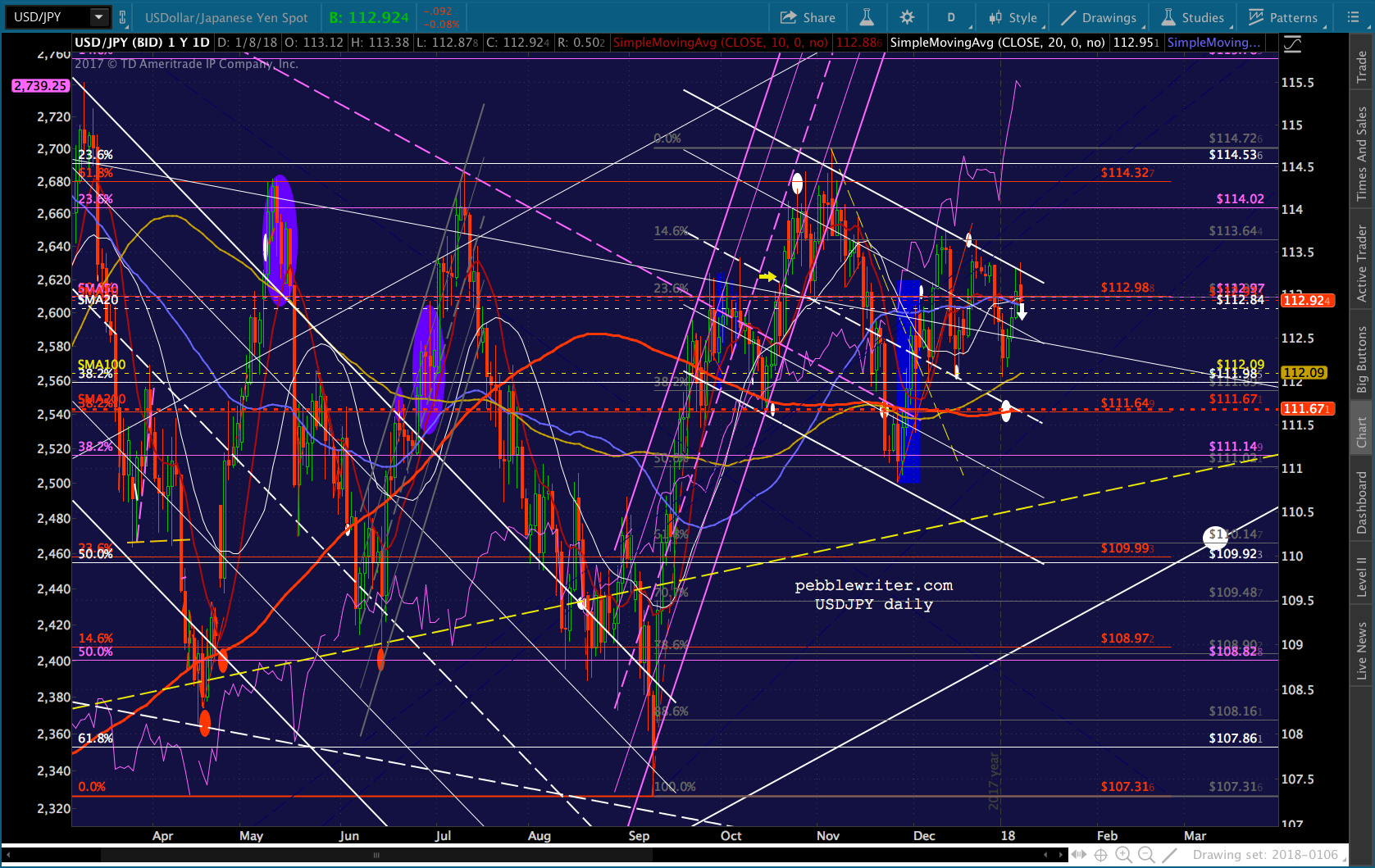

I believe if we weren’t going to see a backtest, USDJPY would have broken out by now.

I believe if we weren’t going to see a backtest, USDJPY would have broken out by now.

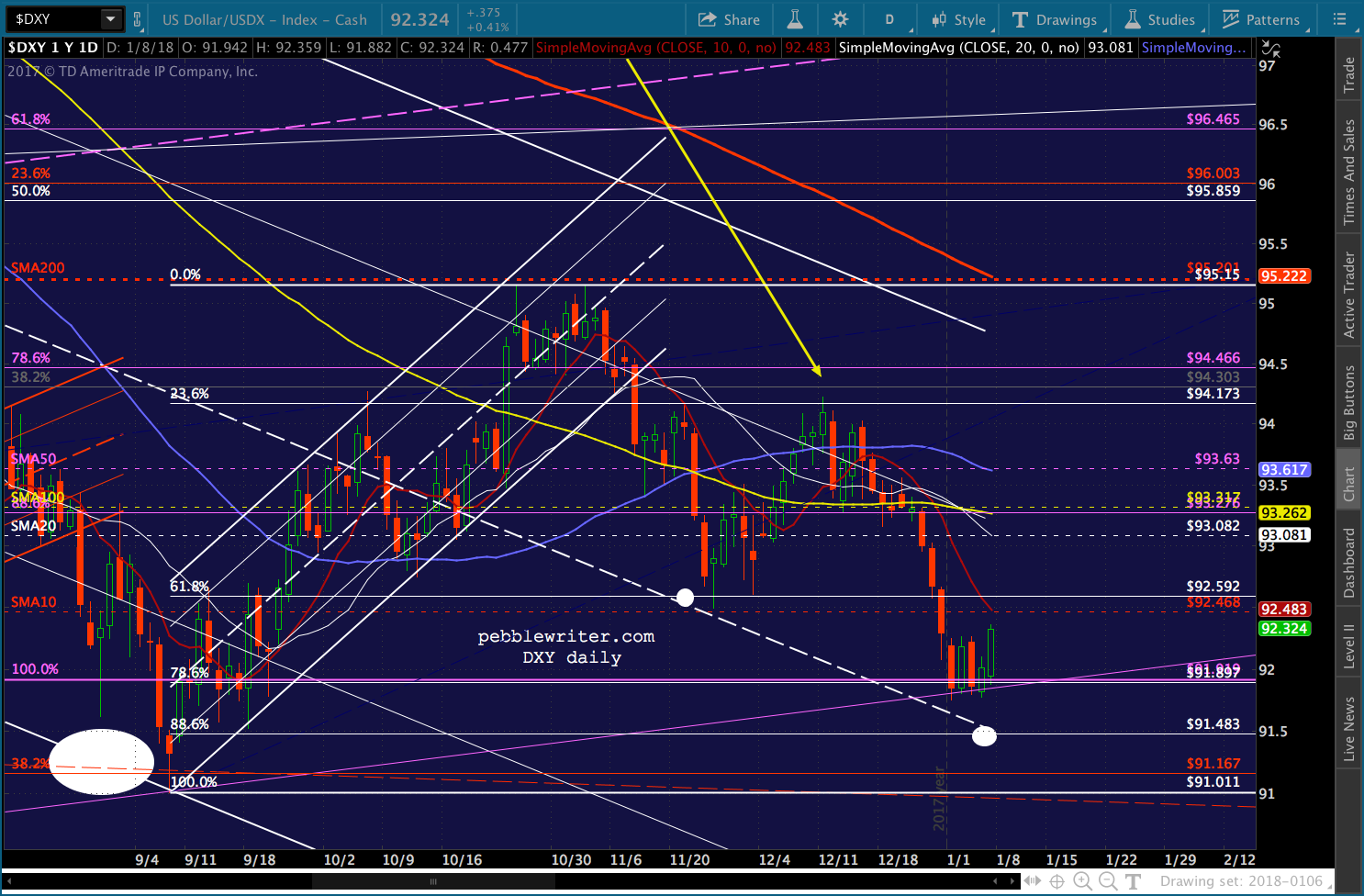

The counter-argument is that DXY is rallying nicely today, up about 0.41%. If it breaks above its SMA10 (92.468) then we’d have to revisit the equity call as well las the 91.483 target — the white .886.

The counter-argument is that DXY is rallying nicely today, up about 0.41%. If it breaks above its SMA10 (92.468) then we’d have to revisit the equity call as well las the 91.483 target — the white .886.

And, VIX has yet to rise above a backtest of the broken white channel bottom.

And, VIX has yet to rise above a backtest of the broken white channel bottom.

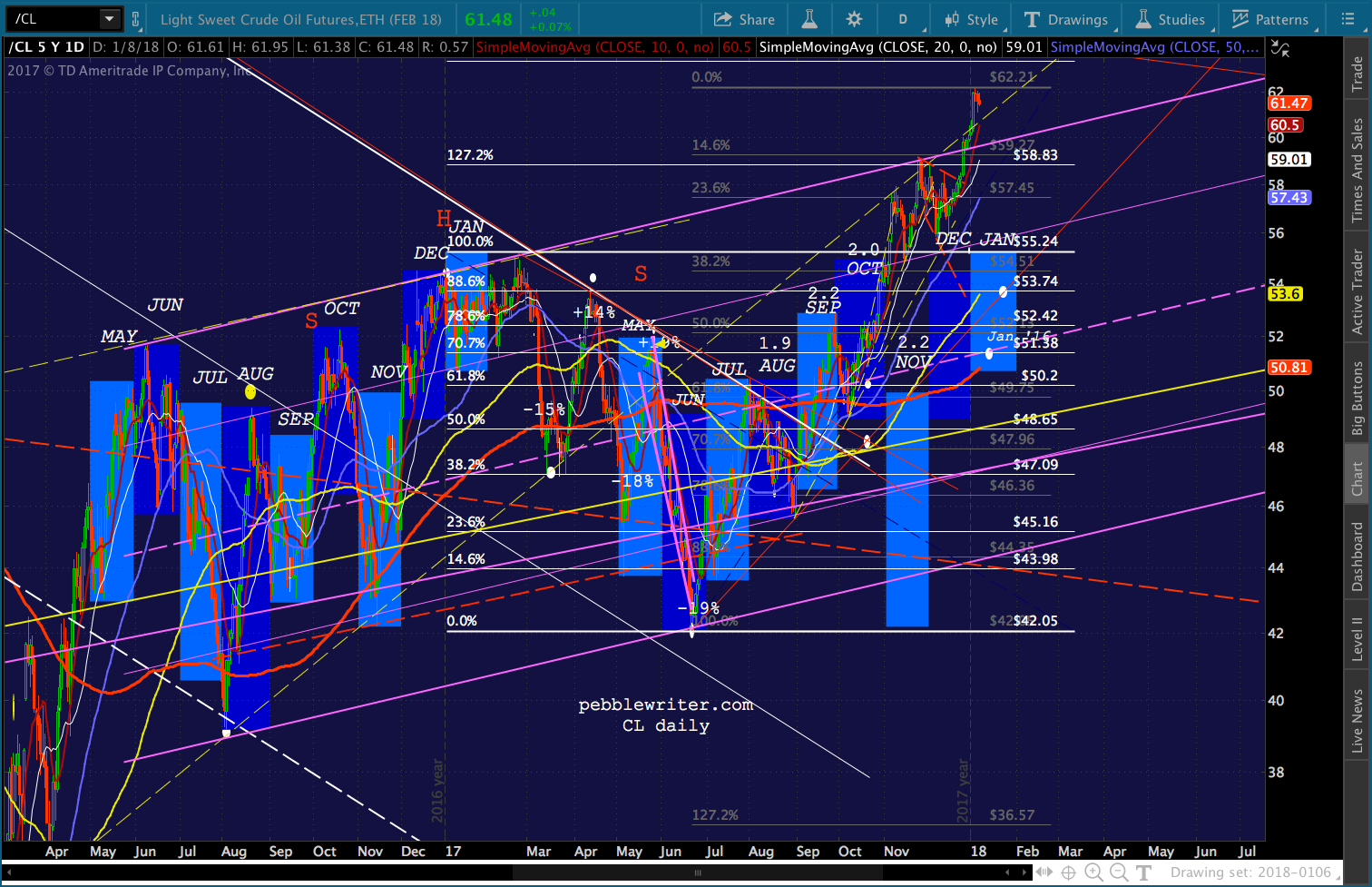

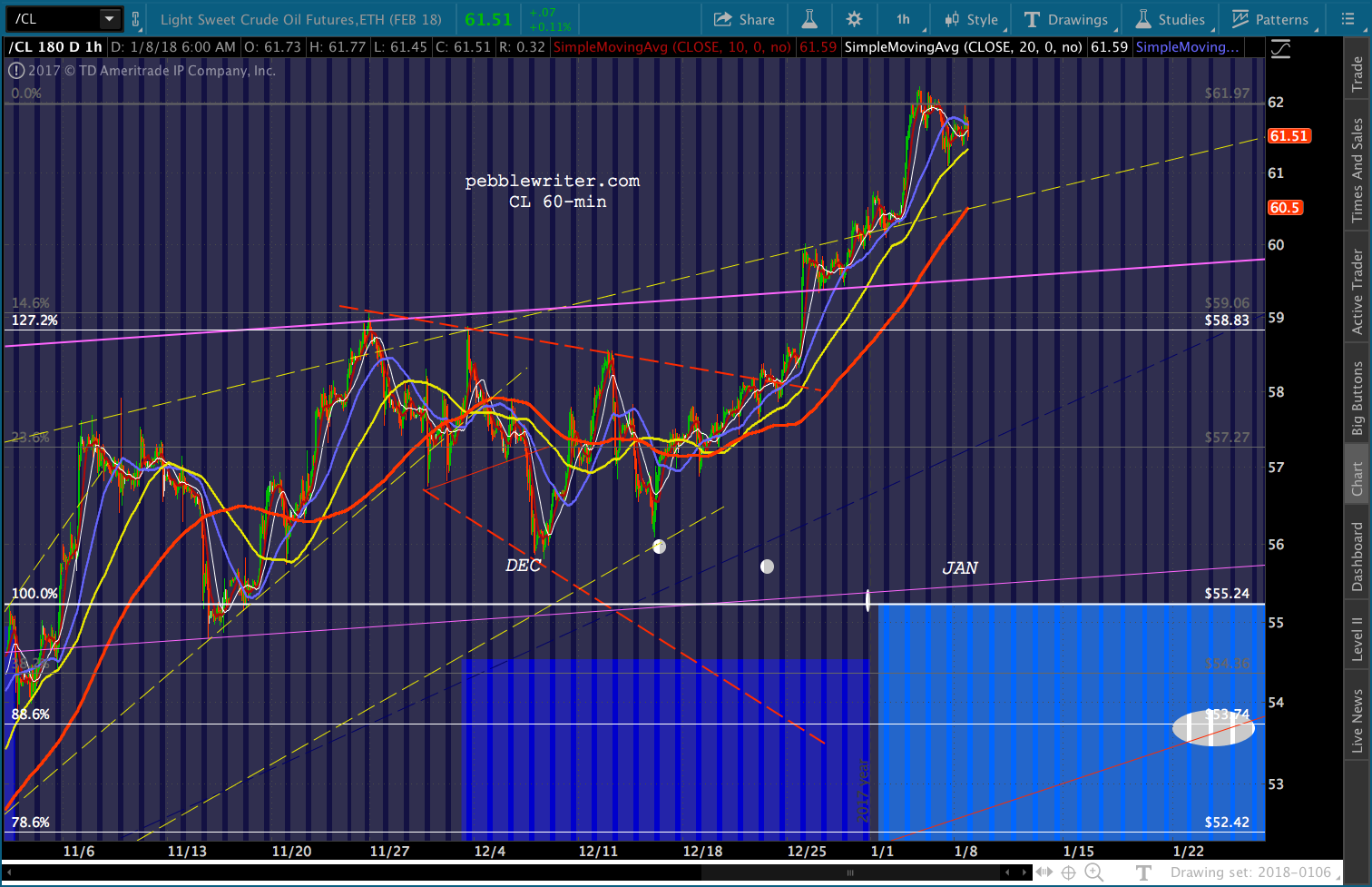

On the oil and gas front, CL is at a loss as to what to do. It has broken out beyond 60 — the price at which pretty much everyone agrees will encourage shale producers in the US to open up the spigots — and, is closing in on our next upside target of 63.39.

On the oil and gas front, CL is at a loss as to what to do. It has broken out beyond 60 — the price at which pretty much everyone agrees will encourage shale producers in the US to open up the spigots — and, is closing in on our next upside target of 63.39. It was needed in order to get ES and SPX up above their 2.24s. Now that they’re there, the breakout is susceptible to a correction at any time.

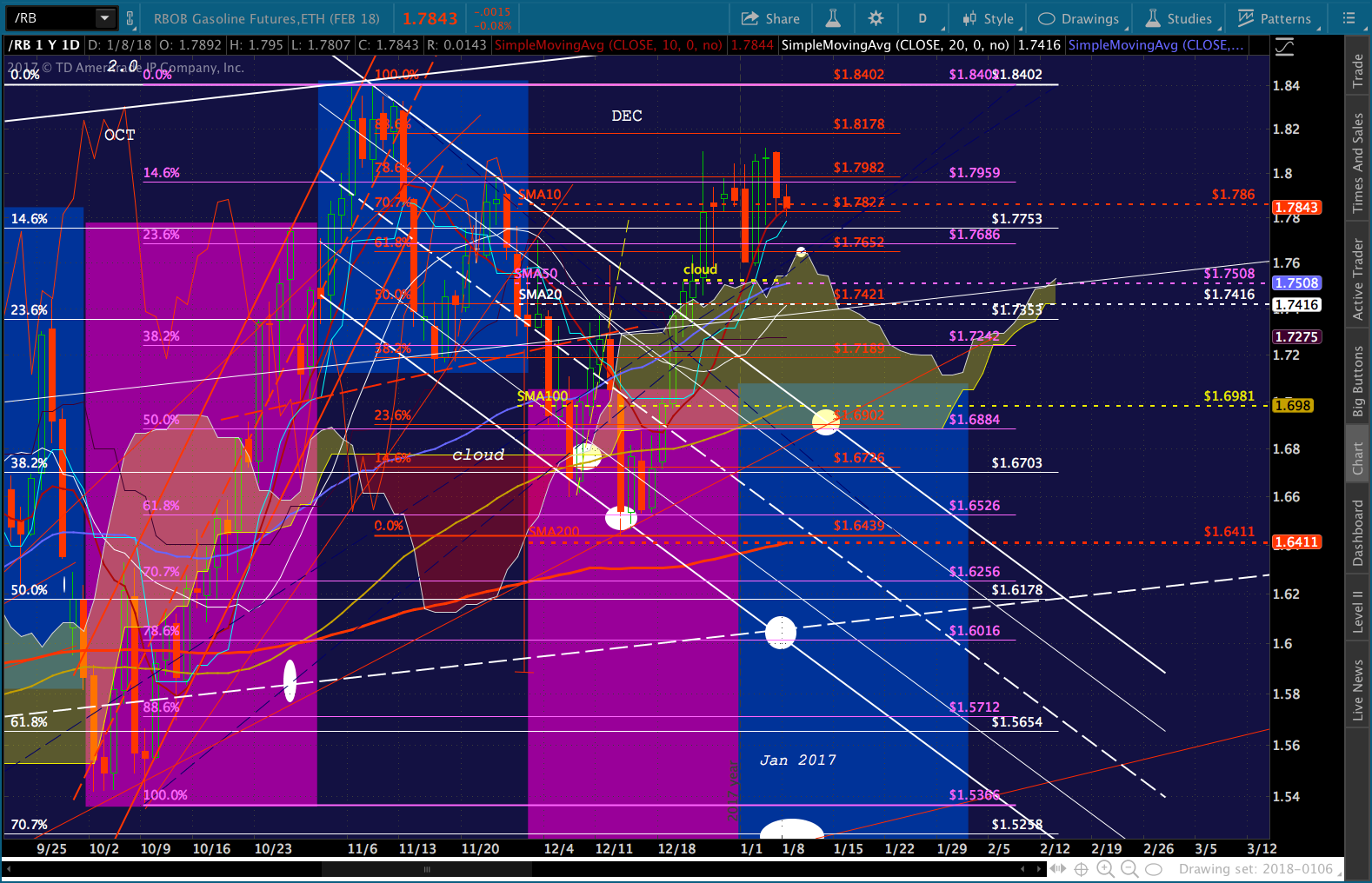

It was needed in order to get ES and SPX up above their 2.24s. Now that they’re there, the breakout is susceptible to a correction at any time. Likewise, RB is nearing its .886 and could be eyeing a backtest of the cloud. The SMA10 is the line in the sand.

Likewise, RB is nearing its .886 and could be eyeing a backtest of the cloud. The SMA10 is the line in the sand. Stay tuned.

Stay tuned.