Futures are moderately higher, but off their overnight highs following a backtest of the 10-day moving average as expected yesterday.

Initial claims came in lower than expected, meaning the Fed’s 25 bps cut yesterday was in line with conditions.

The main story continues to be the steady, daily decline in VIX, seen here in the daily futures chart. Averaging about 2% per session, it has done more to enable the equity meltup than anything else. As David Tepper stated this morning, a 25 or even 50 bps rate cut might help equity markets but will do little to boost the economy.

As David Tepper stated this morning, a 25 or even 50 bps rate cut might help equity markets but will do little to boost the economy.

continued for members…

The backtest worked for ES as well.

As long as SPX remains above its 3.618 at 6539 and ES remains above its 1.618 at 6666, then the market should have another 5% in it between now and YE.

As long as SPX remains above its 3.618 at 6539 and ES remains above its 1.618 at 6666, then the market should have another 5% in it between now and YE.

Many have noticed the striking negative divergence. It might not be enough, though, to offset the potential USDJPY breakout.

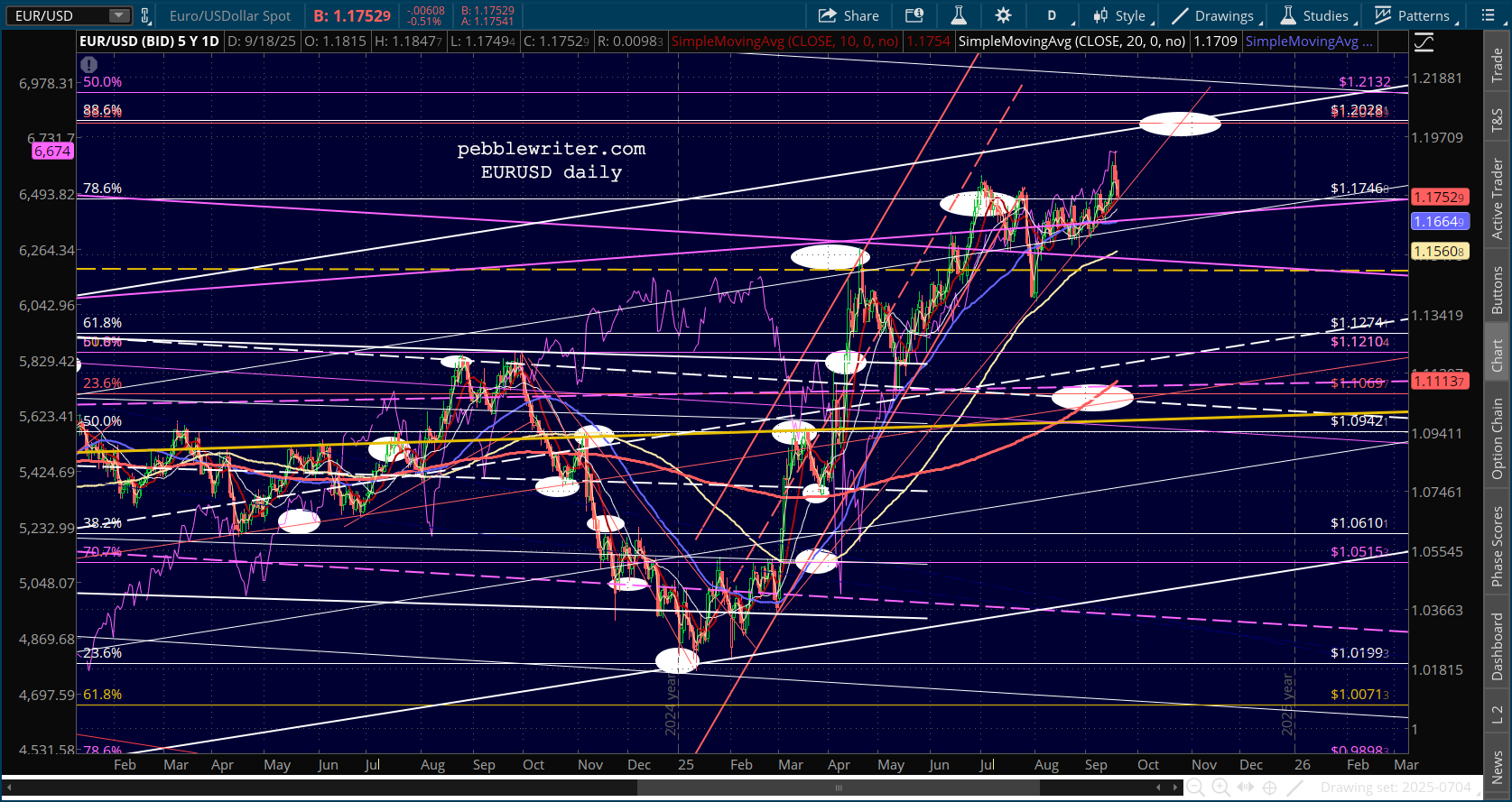

I’ve written often about the weakening USD. I believe EURUSD will run out of upside at 1.2028. But, it could stretch out the tag past late October by heading sideways once it approaches 1.20.

I’ve written often about the weakening USD. I believe EURUSD will run out of upside at 1.2028. But, it could stretch out the tag past late October by heading sideways once it approaches 1.20.

This would keep DXY from rebounding too much over the next few months despite upward pressure from USDJPY rising (cheaper yen, more expensive USD.)

This would keep DXY from rebounding too much over the next few months despite upward pressure from USDJPY rising (cheaper yen, more expensive USD.)

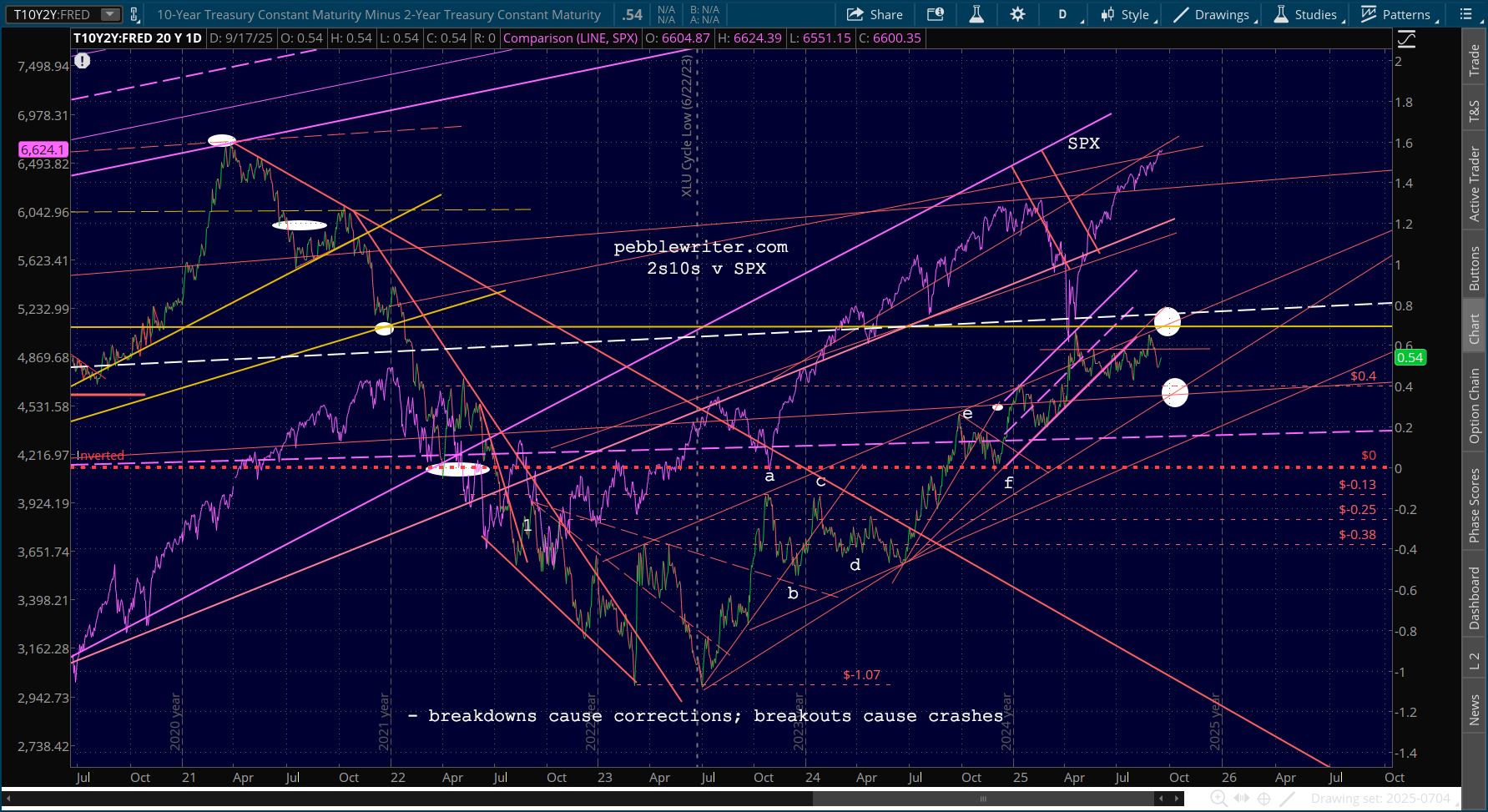

Then there’s the 2s10s, which if it could remain between 44 and 52 bps, would neither break out or break down. Otherwise, tough times for equities.

Then there’s the 2s10s, which if it could remain between 44 and 52 bps, would neither break out or break down. Otherwise, tough times for equities.

As it stands right now, the 10Y is bouncing nicely. I think bond investors are starting to appreciate the inflation risks after Powell’s comments yesterday.

As it stands right now, the 10Y is bouncing nicely. I think bond investors are starting to appreciate the inflation risks after Powell’s comments yesterday. The 2Y is also bouncing, however, so the spread hasn’t blown out.

The 2Y is also bouncing, however, so the spread hasn’t blown out.

The factor that makes it all work is oil/gas which, as we have stated, will contribute to rising CPI unless they head south from here.

The factor that makes it all work is oil/gas which, as we have stated, will contribute to rising CPI unless they head south from here.