Many analysts and managers whose work I admire who have become increasingly bearish in recent weeks. The general thesis usually posits that as central banks normalize rates and cut back on asset purchases, equities will tumble back to where they were before QE began.

While I would be thrilled to see even a modicum of integrity return to the markets, I think it is dangerous to assume that central bankers will suddenly develop backbones and admit that re-inflating bubbles in nearly every asset class was a colossal mistake.

Regular readers know that I am a big believer in the power of algorithms. With roughly 80% of daily equity volume comprised of indexers, closet indexers, ETFs and other trend following/shadowing machine-based strategies, it has become increasingly simple to manipulate equity prices.

Algorithms are the key. The yen carry trade, for instance, proved its mettle following the 2011 mini-crash. Stocks can easily be driven higher by a noticeable triggering event such as the USDJPY bouncing at or moving above a moving average, breaking out of a price channel, etc.

Spot USDJPY trading averages around $800B – $1 trillion per day. It would typically take only a tiny fraction of that amount to push the pair above any particular price point that would be recognized by algorithms as a bullish development (sometimes, merely “higher.”) Consider, then, that a $10B “investment” in the USDJPY could drive the S&P 500 (about $20 trillion) to a new high or past key resistance on any given day.

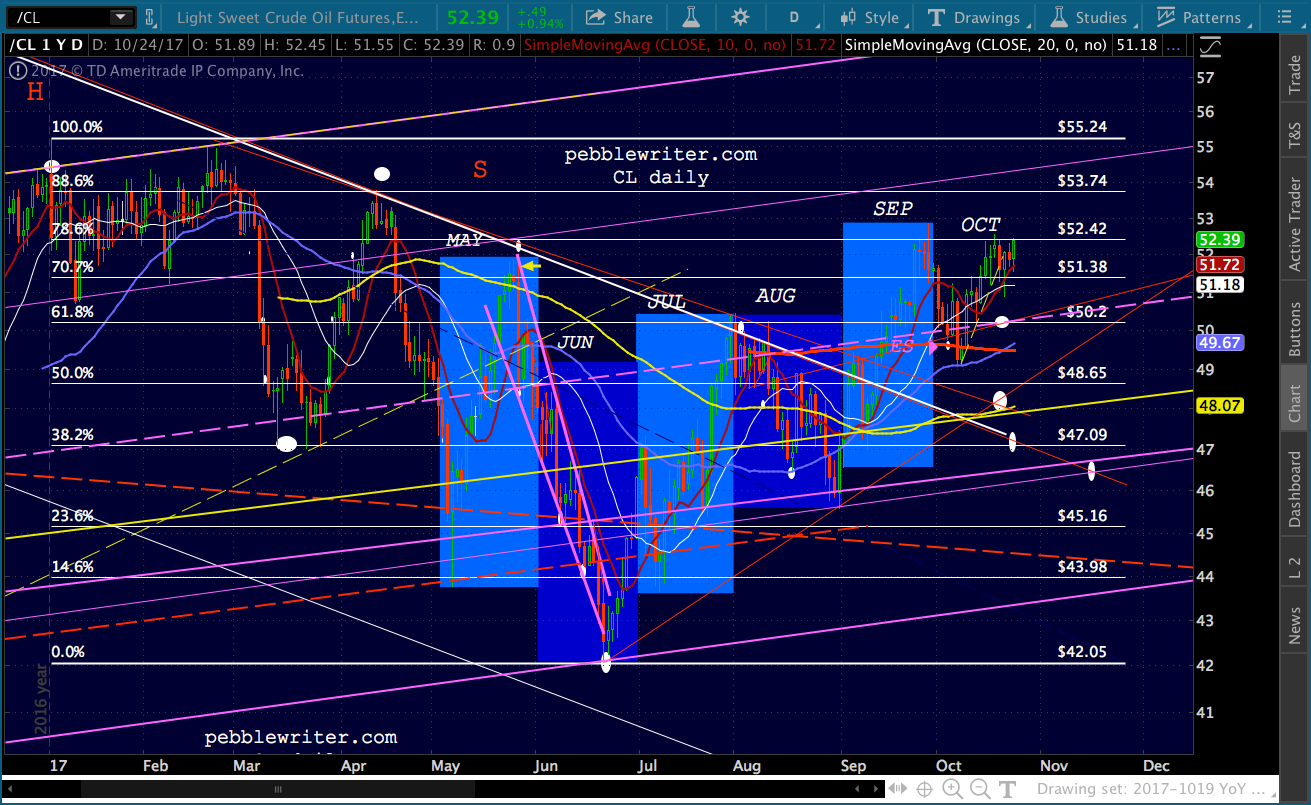

It happens pretty much every day. Note the massive spike in USDJPY following the initial meltdown in equity futures after Trump was elected last November. Since the pair finally topped out in December, repeated “breakouts” (from the falling white channel, above key moving averages, above the purple TL, etc.) have kept stocks (the thin purple line) from stalling. Similarly, light sweet crude oil (CL) futures average about 1.3 million contracts daily ($65B notional) which, at an average margin per contract of $2,000, comes out to a measly $2.6 BB. Yet, significant moves in CL quite frequently drive significant moves in equities. Again, the tail wagging the much larger dog.

Similarly, light sweet crude oil (CL) futures average about 1.3 million contracts daily ($65B notional) which, at an average margin per contract of $2,000, comes out to a measly $2.6 BB. Yet, significant moves in CL quite frequently drive significant moves in equities. Again, the tail wagging the much larger dog.

The most striking example was in February 2016 in the wake of USDJPY’s breakdown [see: USDJPY Finally Relents.] Oil prices nearly doubled in four months, ignoring supply and demand to enable SPX’s breakout past the critical 2138 level. Of course, the winner of the prop-up-stocks derby this past year has been VIX. With average daily notional volume of only $3.2B, it’s also a bargain in terms of controlling stocks.

Of course, the winner of the prop-up-stocks derby this past year has been VIX. With average daily notional volume of only $3.2B, it’s also a bargain in terms of controlling stocks.

Between 2014 – 2016, VIX accurately signaled corrections by tagging (yellow arrows) the bottom of a channel (also in yellow) once per year when volatility was historically low and complacency historically high.

Beginning in December 2016, however, it began tagging and declining below that channel bottom about 75% of the time — repeatedly signaling algos that there was nothing to worry about: buy, buy, buy.

Obviously, VIX can only go so low. Unlike interest rates, it can’t go negative. So, it usually rises a little during the low-volume after-hours when stock futures prices are easily propped up via other means. This gives it room to drop the following day when stocks need more convincing. The same thing frequently happens with USDJPY and CL. Again, this happens almost every day.

Obviously, VIX can only go so low. Unlike interest rates, it can’t go negative. So, it usually rises a little during the low-volume after-hours when stock futures prices are easily propped up via other means. This gives it room to drop the following day when stocks need more convincing. The same thing frequently happens with USDJPY and CL. Again, this happens almost every day.

While VIX continues to make new, all-time lows, there’s a natural limit to the extent to which oil prices can be manipulated. Sure, CL could add .50 every day ad infinitum. But, eventually, inflation creeps up over 2% — which central bankers know would lead to interest rate hikes that would threaten solvency. In banking, as in nature, most parasites know better than to kill off their host.

Likewise, USDJPY spikes eventually cause problems. A USDJPY increase represents a drop in the value of the yen. Importing food and oil becomes more expensive and inflation could become more noticeable. The Japanese government has found a way around this: they leave food and oil prices out of CPI calculations. No fuss, no muss.

These machinations, and many others which play lessor roles, are cheap, effective and (excluding our erudite members) invisible. Remember, central banks have access to virtually unlimited funds at virtually no cost. So, whether the amount needed to goose equity prices is $2B, $5B or $10B is relatively unimportant.

Quantitative easing might well be tapered further, but two things are clear. First, central bankers will quickly abandon any tapering the moment markets fall too far, too fast — whatever that is. Second, given theses other, effective tools at their disposal, QE’s probably not even necessary any more.

The only potential hitch is the bond market which, at $100 trillion, dwarfs equity markets. Bond prices and yields have also been manipulated to a previously unimaginable extent. If tapering were actually to occur, it could do some real damage to bond values.

But, again, I believe central bankers will pull the plug on tightening before things get too dicey. In my opinion, they’re simply trying to build in a little more headroom in the (very likely) event that additional easing is required down the road. This part isn’t rocket science, as a return to traditional interest rates is completely unacceptable. They’ll monetize deficit spending, as has Japan, before we ever see a 6-8% 10-year.

Given the above, let’s go around the horn and see where things stand.

continued for members…

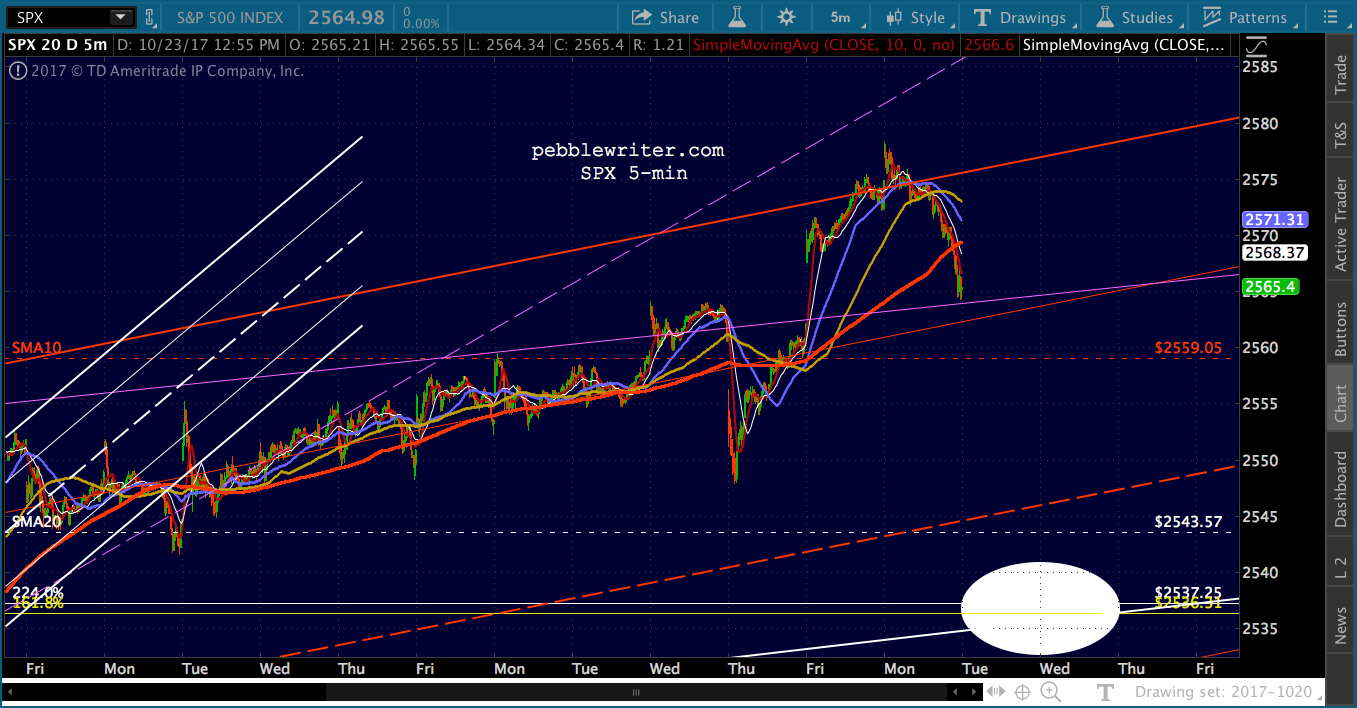

Yesterday’s rollover was halted before SPX and ES could even tag their SMA10s.

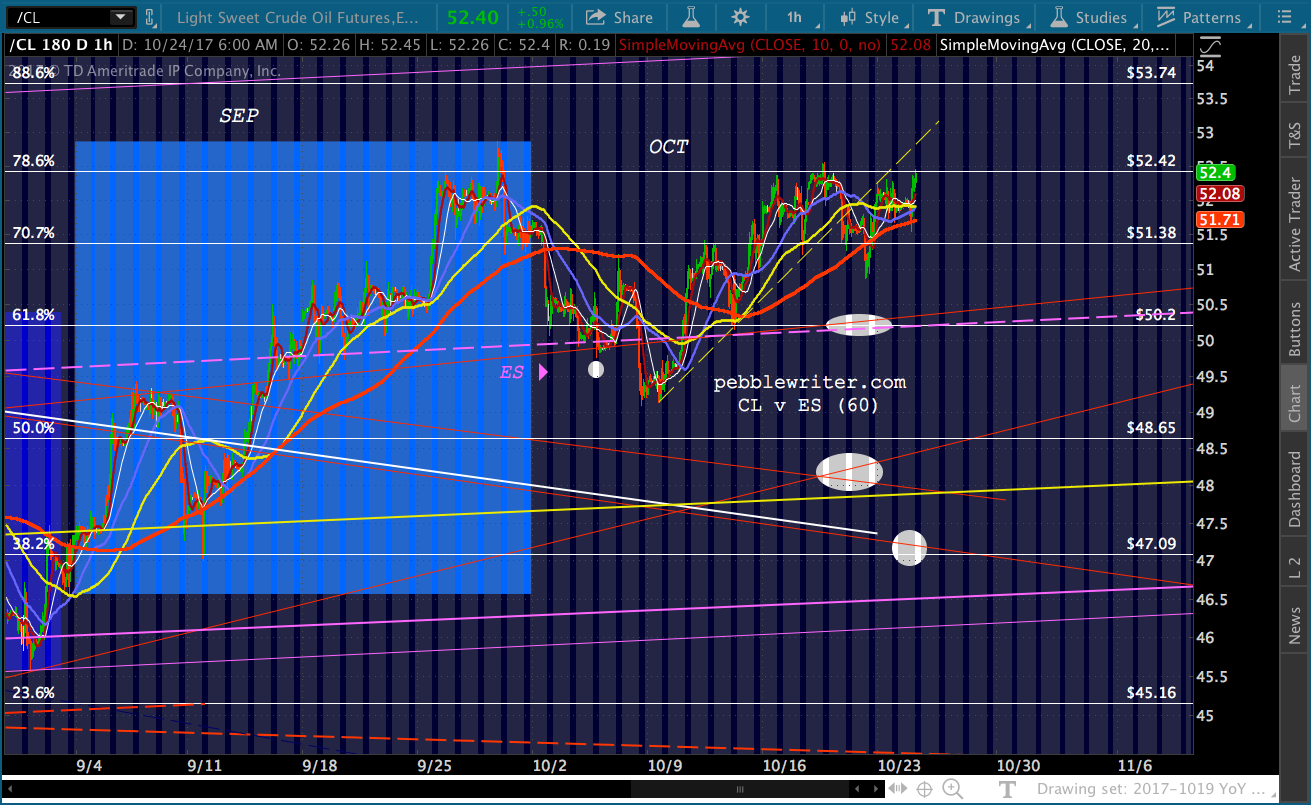

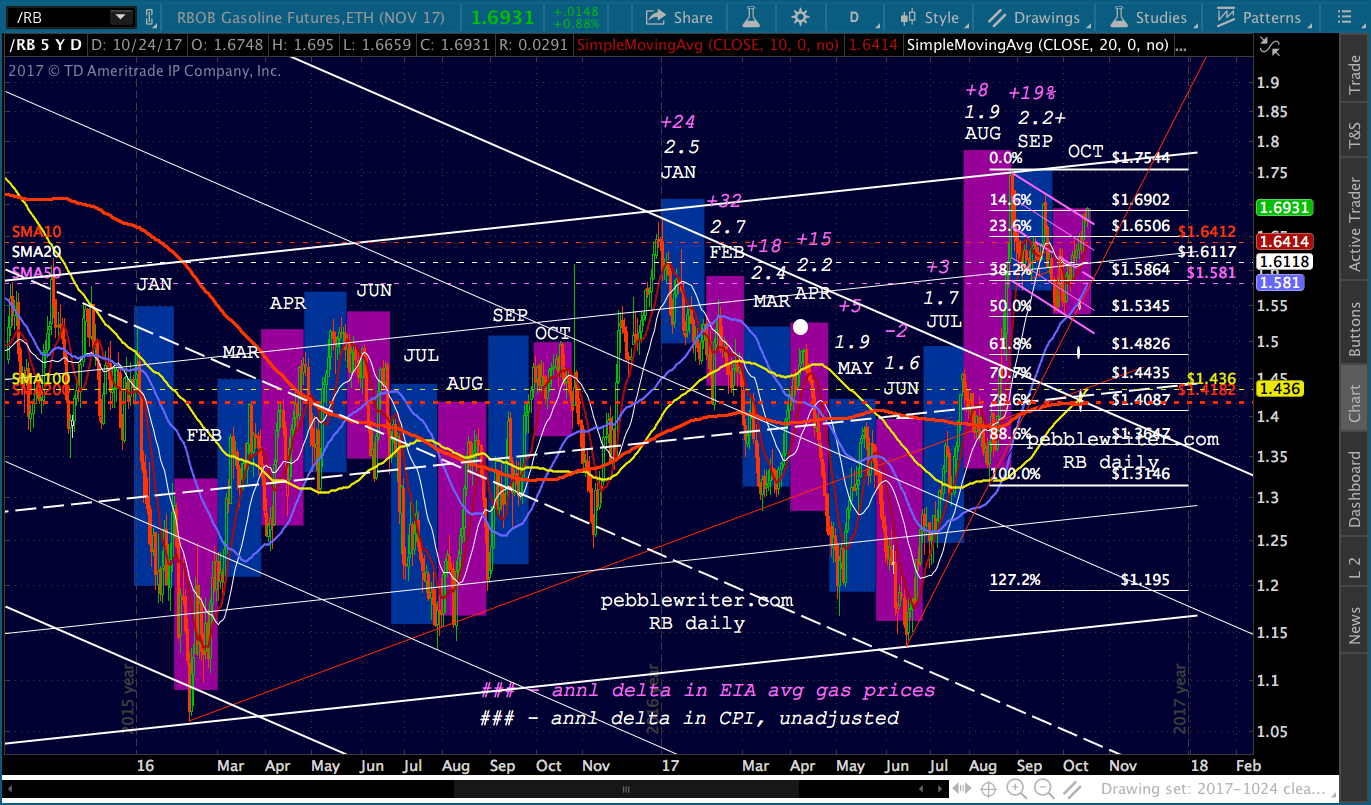

The culprits this time included CL and RB, which have now passed up the best opportunities for a logical backtest — suggesting that our downside targets can be safely abandoned for now.

The culprits this time included CL and RB, which have now passed up the best opportunities for a logical backtest — suggesting that our downside targets can be safely abandoned for now.

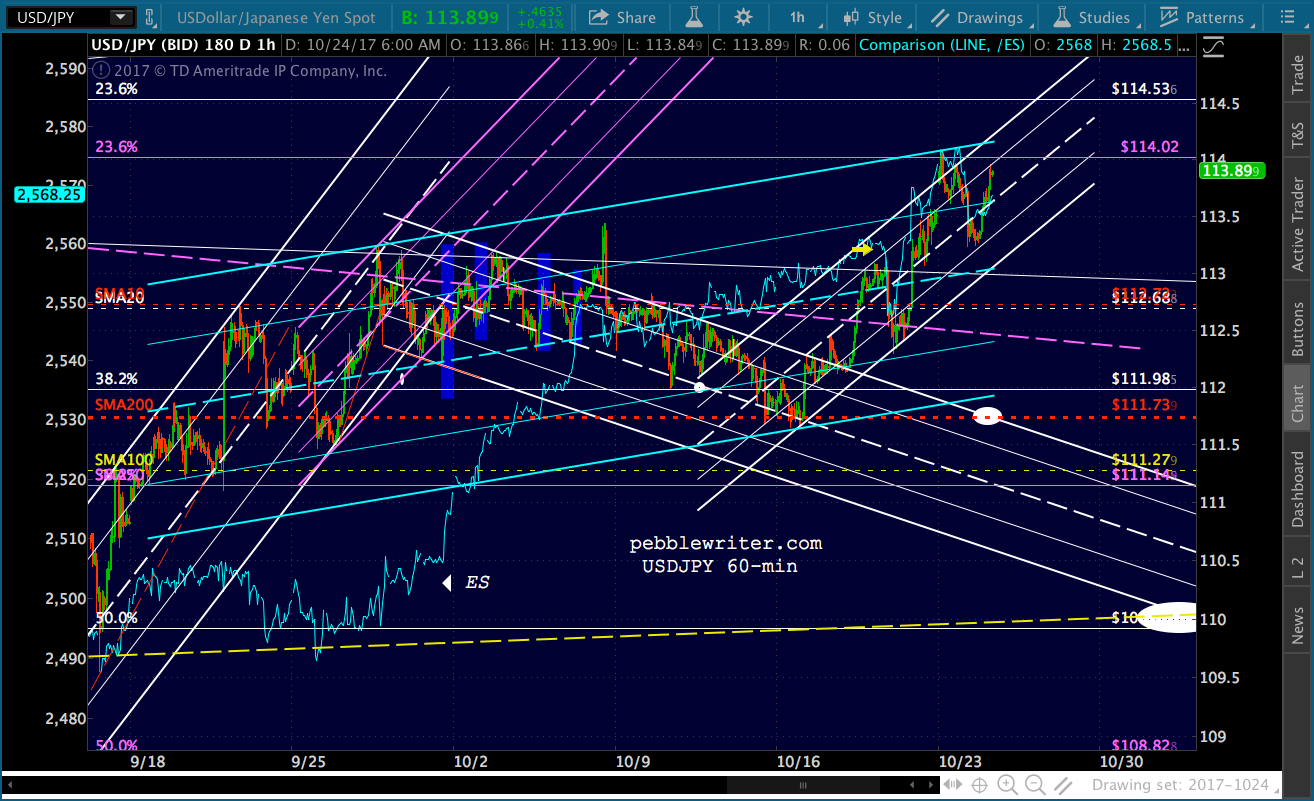

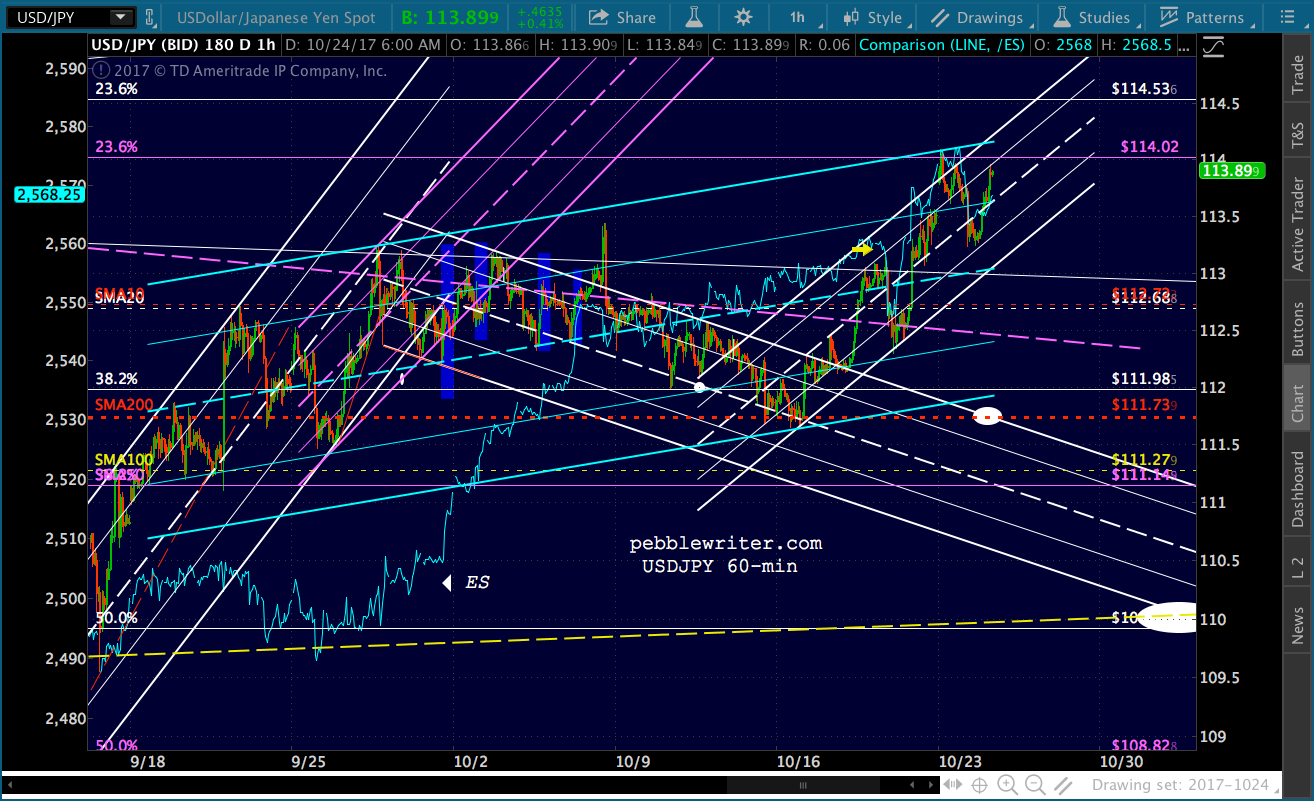

USDJPY has helped with its own little breakout.

USDJPY has helped with its own little breakout.

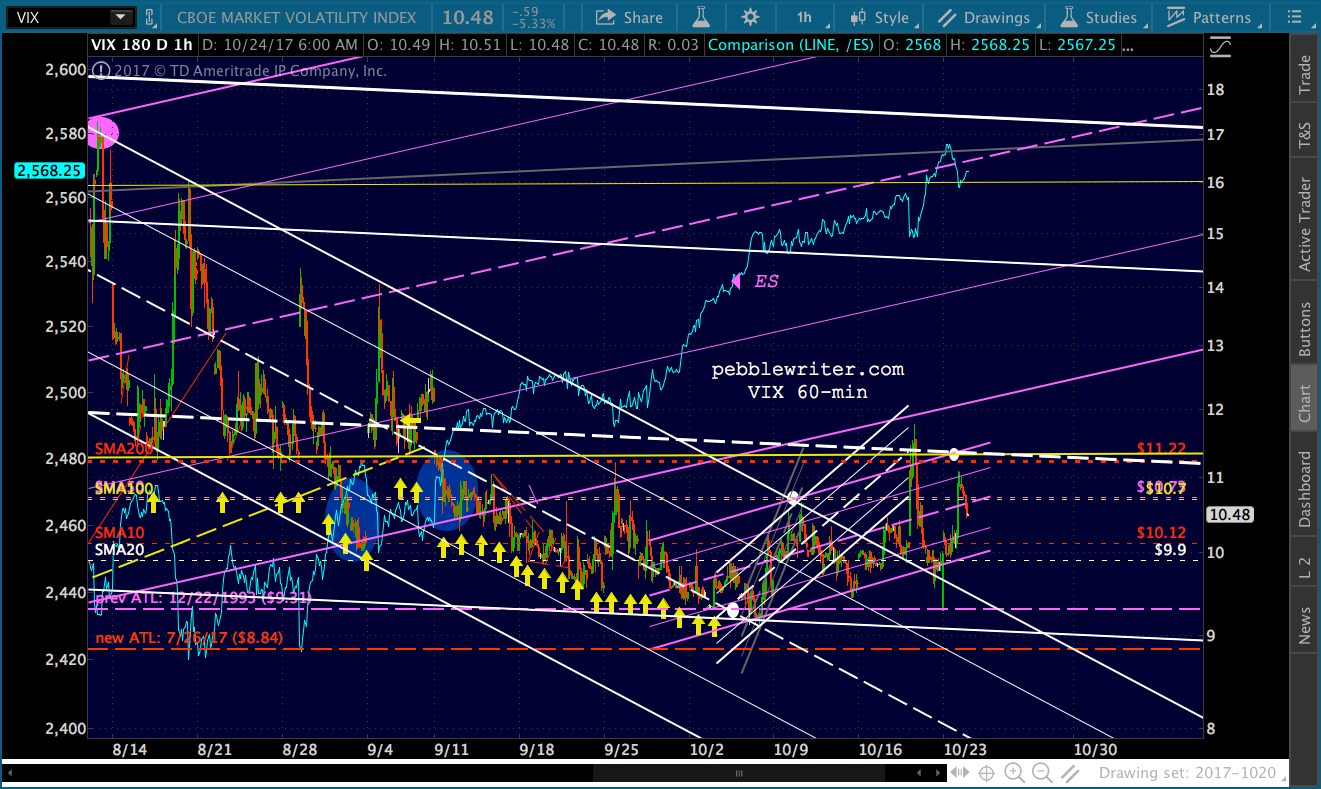

And, of course VIX is reversing.

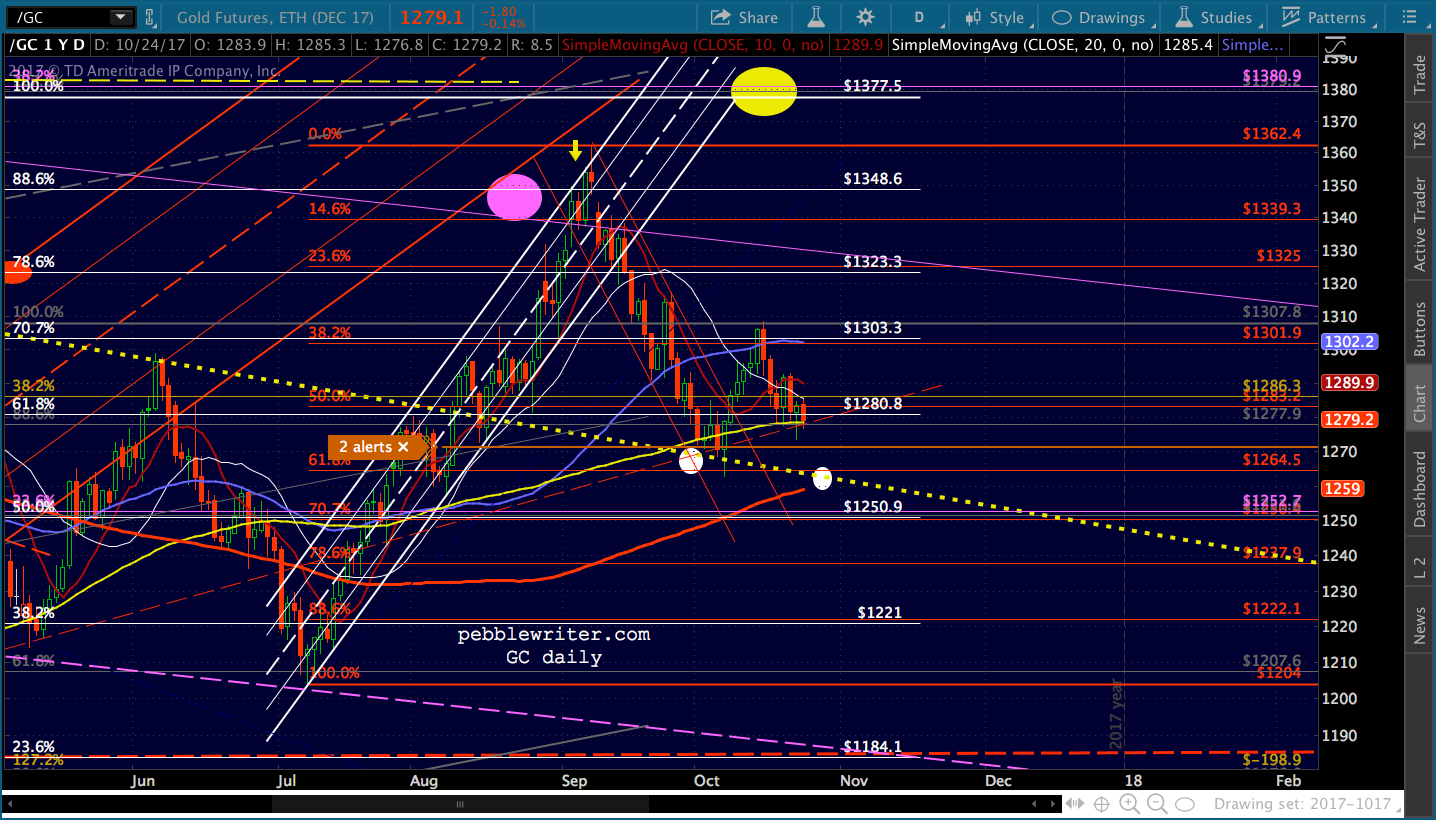

And, of course VIX is reversing. GC continues to settle toward the SMA200, probably setting up a tag around 1259-1263 in the next few days.

GC continues to settle toward the SMA200, probably setting up a tag around 1259-1263 in the next few days. I continue to like the idea of a backtest on SPX/ES, but would be very cautious about shorting until/unless we get a drop through the SMA10.

I continue to like the idea of a backtest on SPX/ES, but would be very cautious about shorting until/unless we get a drop through the SMA10.

GLTA.