In the end, Powell said nothing all that consequential in Jackson Hole. The Fed still stands ready to cut interest rates if the risk of rising unemployment begins to outweigh the risk of rising inflation. It’s exactly where we’ve been for months.

It would have been nice if Powell had delved into the relative risks posed by each leg of their mandate, offered more detail re their balance sheet, or even discussed how they expect tariffs to affect inflation.

But, as the philosopher once said: “You can’t always get what you want. But if you try sometimes you might find you get what you need.”

What the algos needed was reassurance that a September rate cut was still on the table. They got it, so the market took off like a rocket.

Strangely, futures didn’t top their previous highs. In fact, they’re pulling back a bit this morning.

Strangely, futures didn’t top their previous highs. In fact, they’re pulling back a bit this morning.

continued for members…

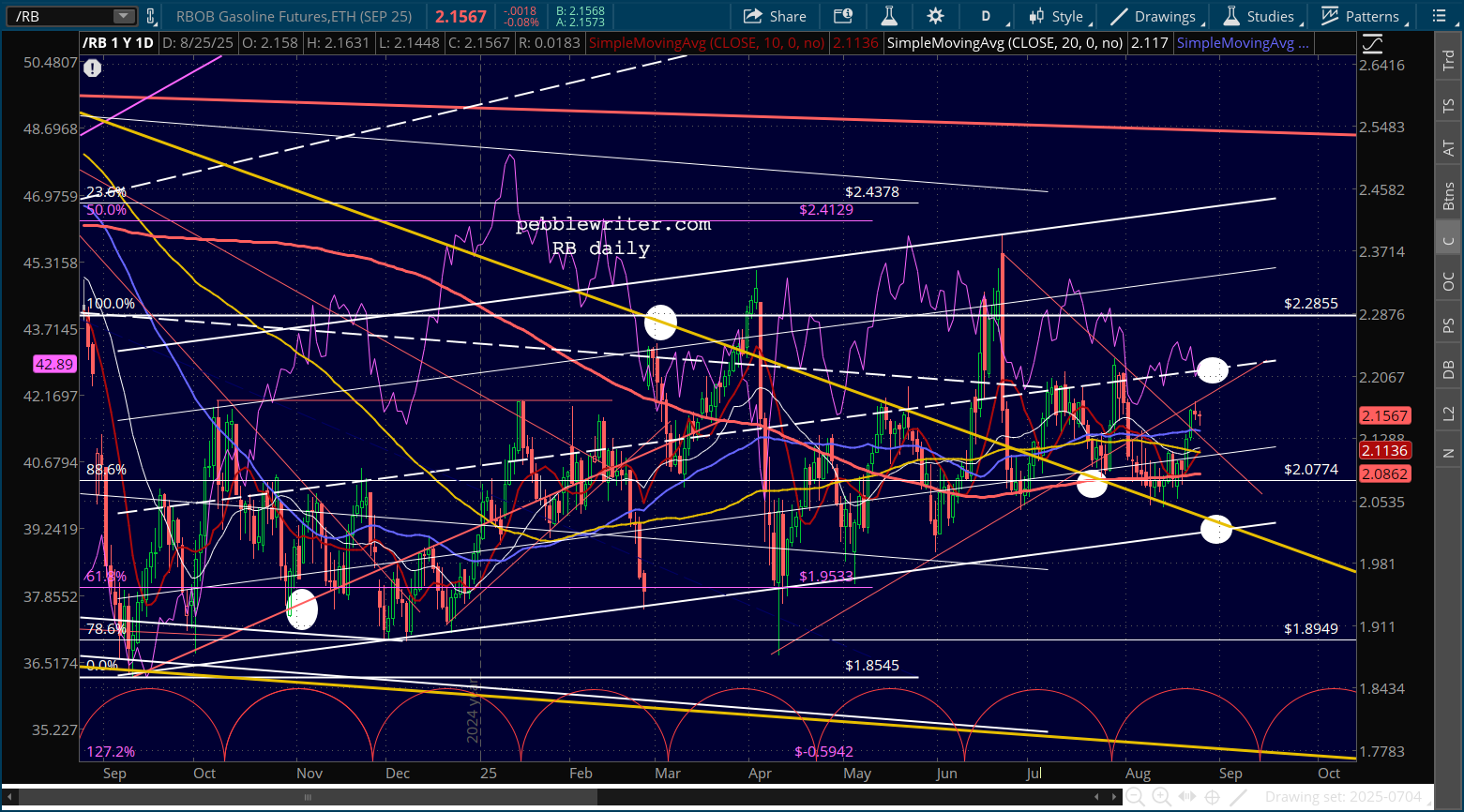

There is still some question as to whether the falling channel will be backtested. If Friday’s spurt had resulted in new highs, the odds would be greatly diminished.

There is still some question as to whether the falling channel will be backtested. If Friday’s spurt had resulted in new highs, the odds would be greatly diminished.

The rollover of short term moving averages was again averted.

The rollover of short term moving averages was again averted.

VIX jumped overnight, but just enough to test the SMA10 and retreat.

VIX jumped overnight, but just enough to test the SMA10 and retreat.

Currencies continue to meander just enough to prevent DXY from breaking down after Friday’s decline back to the red TL.

Currencies continue to meander just enough to prevent DXY from breaking down after Friday’s decline back to the red TL.

For now, the market seems to need a little bad news to justify a September rate cut. With durable orders and GDP coming out later this week, we should see some useful data. But, the really important data will come out Friday: PCE, personal income, and Michigan consumer sentiment.

For now, the market seems to need a little bad news to justify a September rate cut. With durable orders and GDP coming out later this week, we should see some useful data. But, the really important data will come out Friday: PCE, personal income, and Michigan consumer sentiment.

Stay tuned…

Stay tuned…