While November retail sales gain of 0.7% beat expectations of 0.6%, sales excluding auto and gas came in well below consensus: 0.2% versus 0.4%. Markets are pricing in a 97% chance of a 25 bps rate cut tomorrow, but skeptics (like us) make a great argument that loose financial conditions and recent inflation increases suggest that the FOMC take a pause.

And, although Trump isn’t in the White House just yet, it seems likely that coming tariffs will combine with even looser financial conditions to boost inflation even more. Our inflation model indicates that December CPI (out Jan 15) will mark the 4th increase in a row: approaching 3% from the low of 2.44% in Sep.

Don’t look now, but the 10Y has reached our 4.4% target and is positioned for a potential breakout. continued for members…

continued for members…

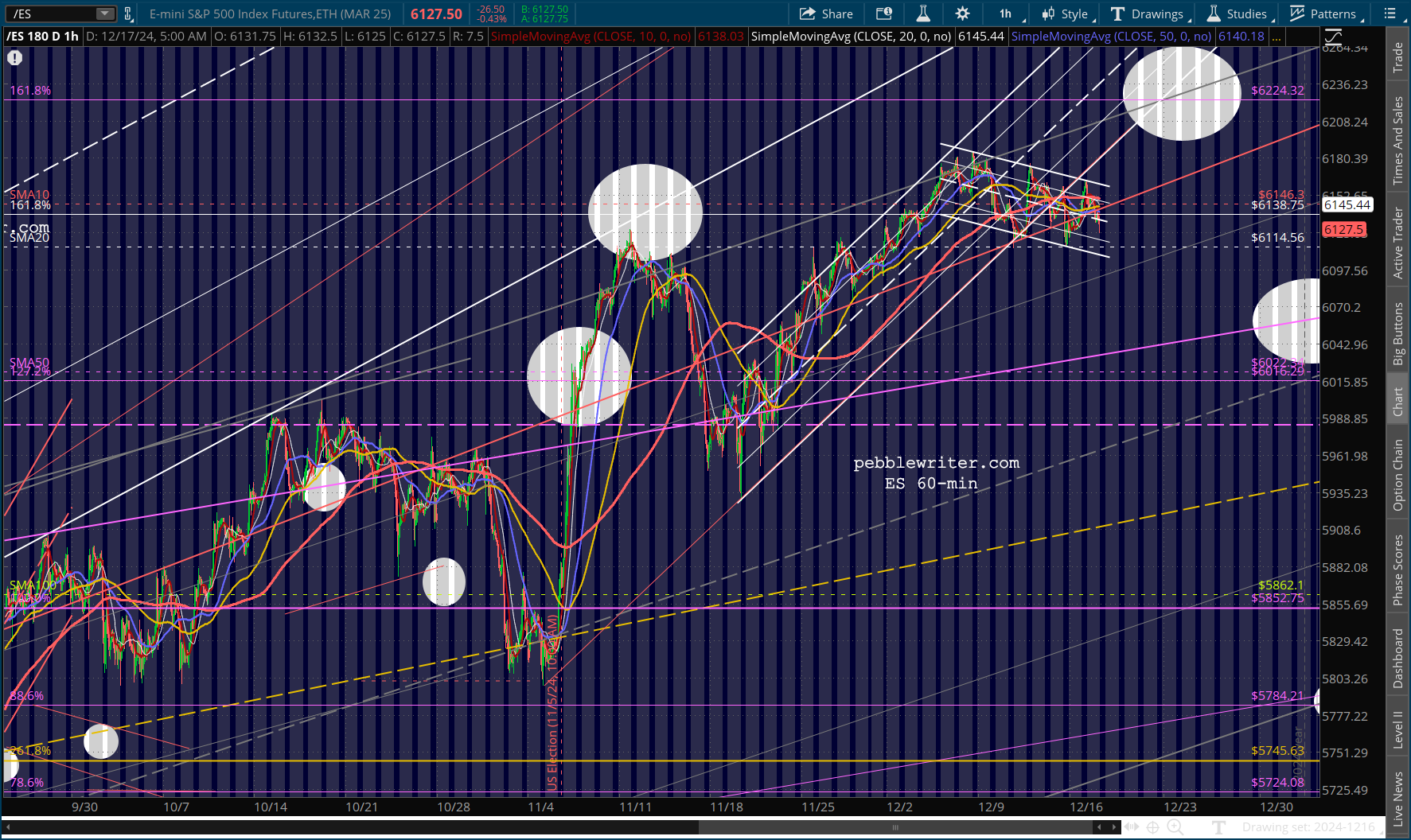

It seems highly likely that ES will backtest its SMA20 again. Whether we get that last minute spurt higher will depend entirely on what the FOMC announces tomorrow. Keep a very close eye on the 10Y, which is back to a critical level that could mean a breakout.

Currencies continue sideways, though the risk remains that DXY breaks higher.

Currencies continue sideways, though the risk remains that DXY breaks higher.

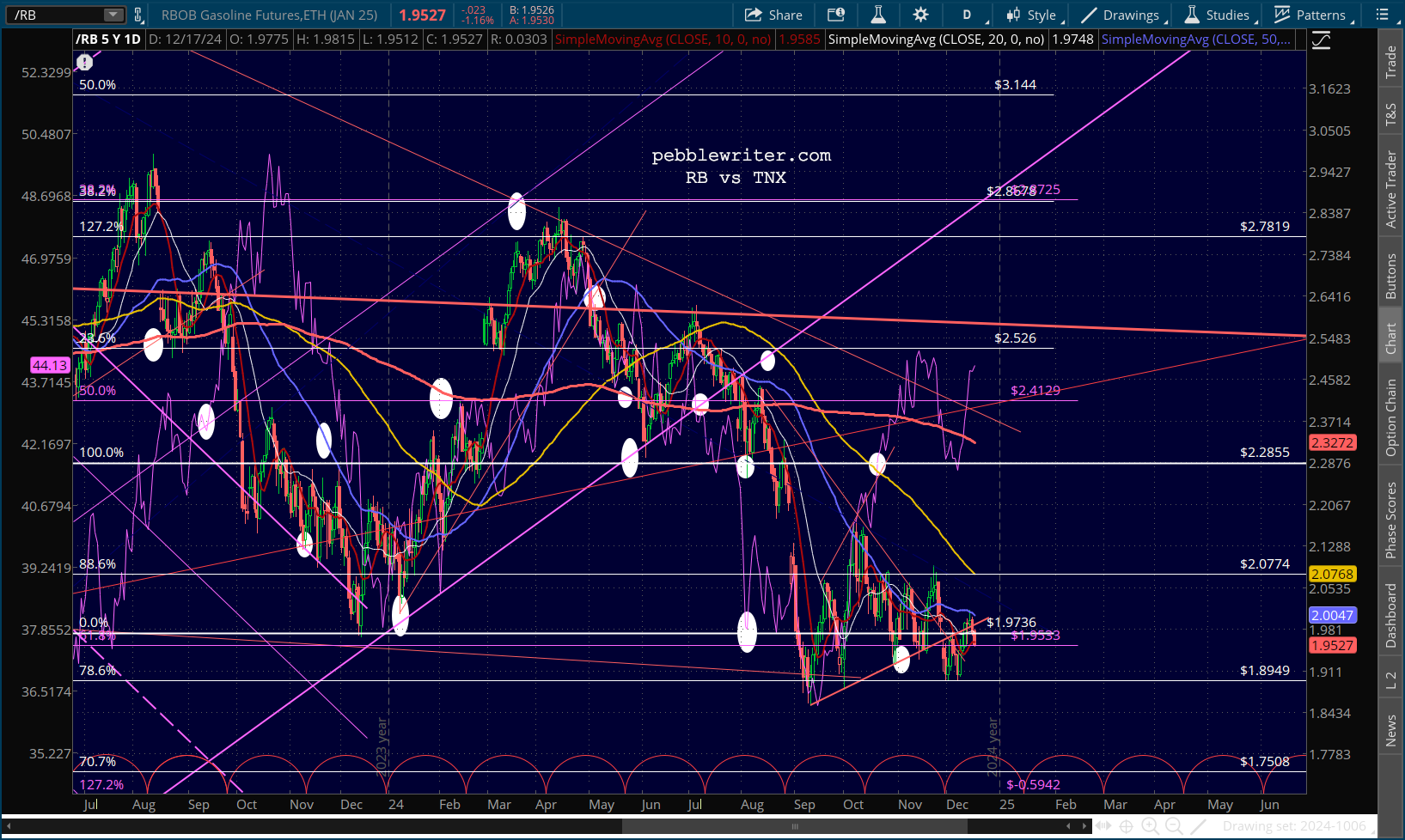

Oil and gas

Oil and gas

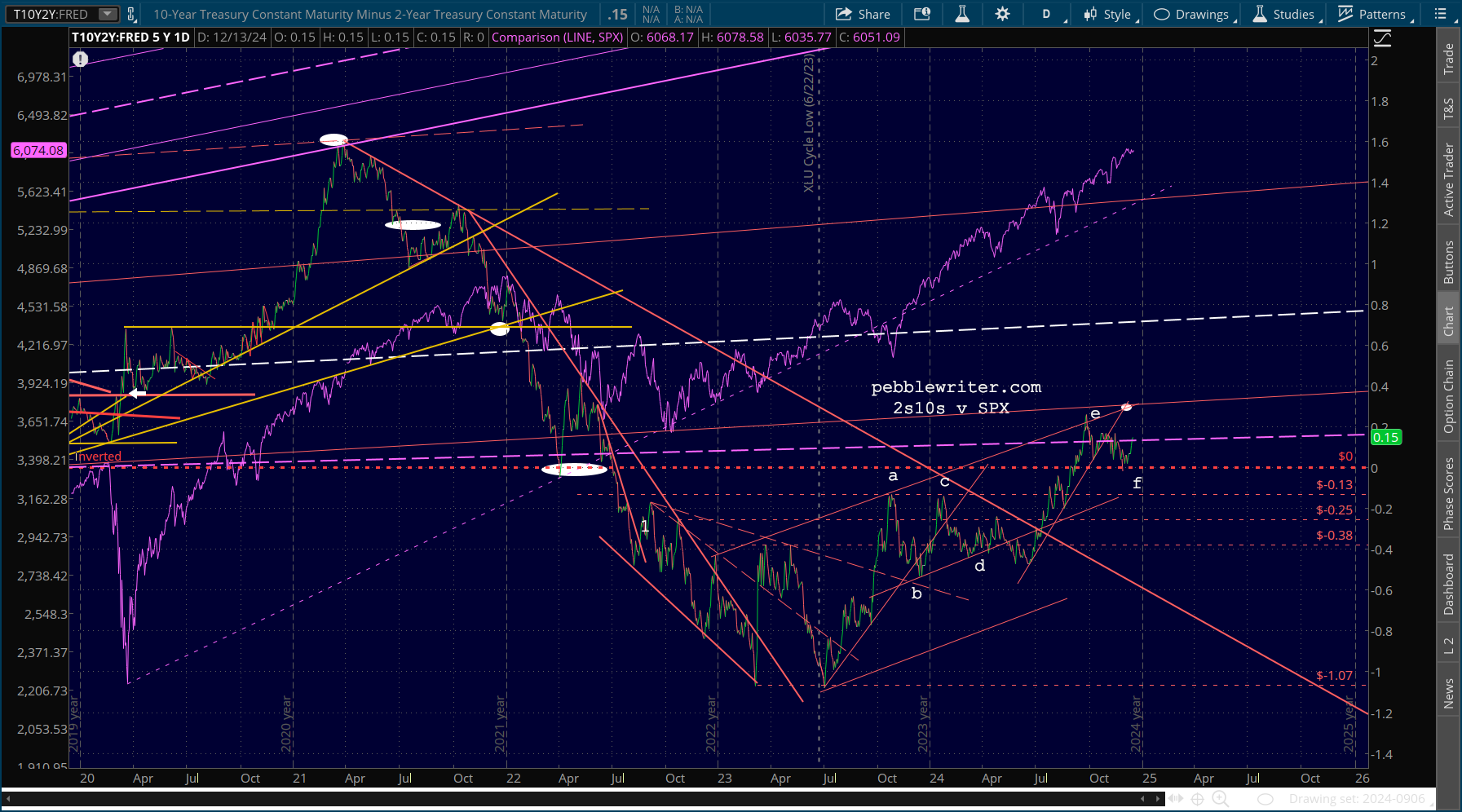

If the 10Y continues higher, the 2s10s is likely to continue its bounce which, in the past, has resulted in equity corrections – or worse.

If the 10Y continues higher, the 2s10s is likely to continue its bounce which, in the past, has resulted in equity corrections – or worse.