Stocks are mixed after final Q3 GDP revisions came in slightly above the November estimate.

While the print is in line with the pre-COVID data…

While the print is in line with the pre-COVID data…

…we have to wonder whether the economy can hold up in the face of decreasing Fed stimulus and COVID cases which are spiking as we head the holidays.

continued for members…

continued for members…

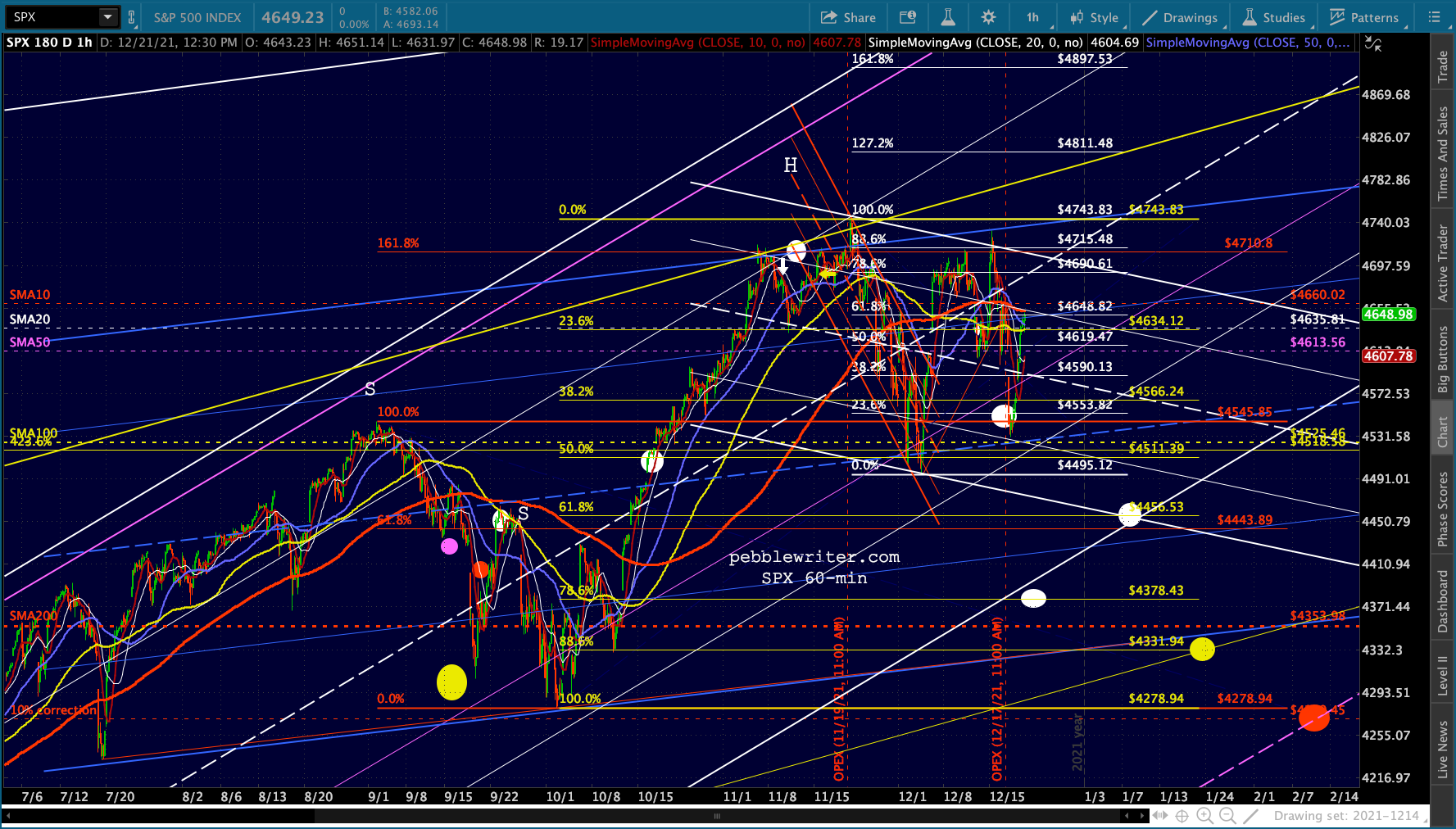

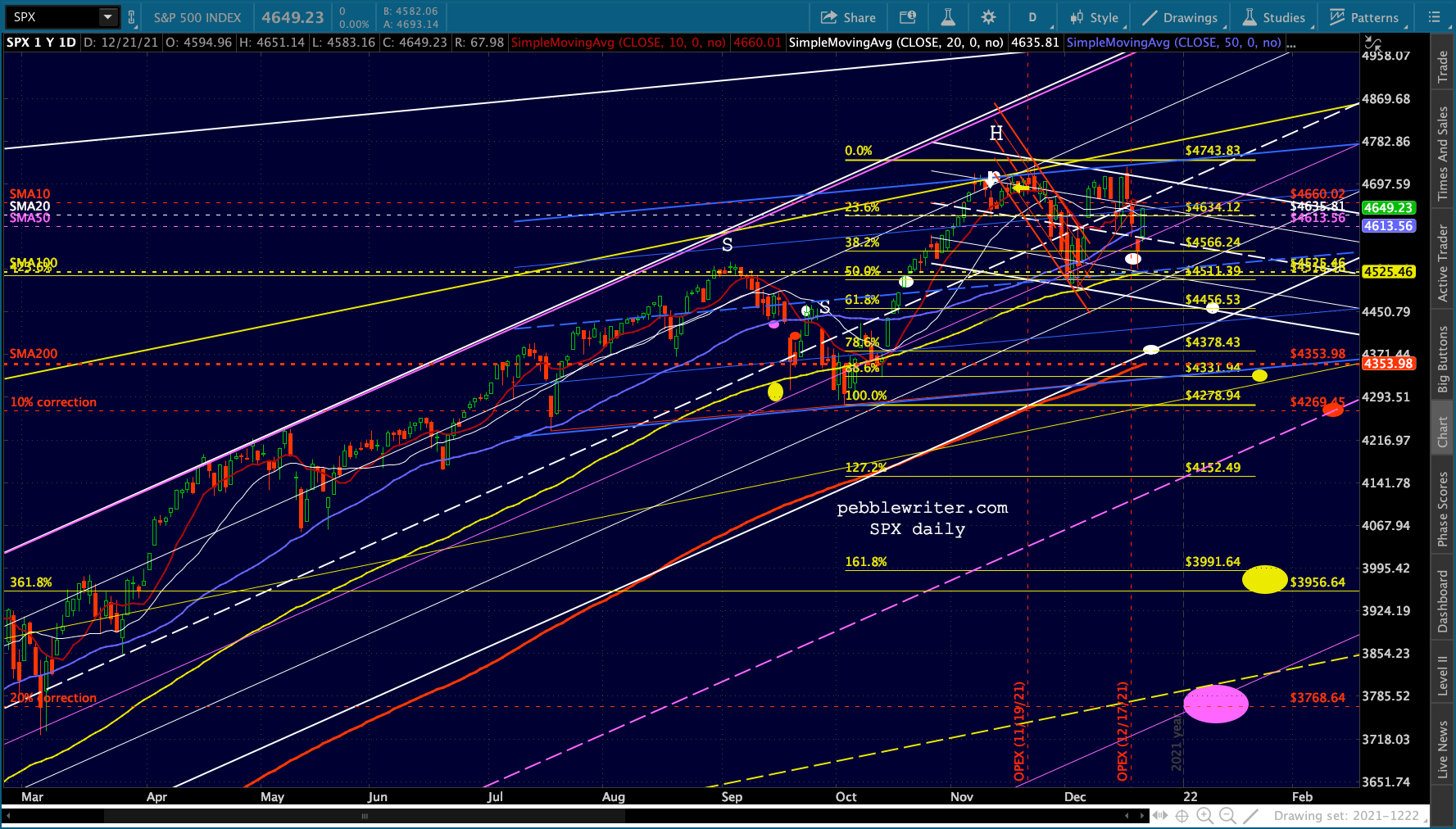

The equity picture: Charts argue for lower prices, but the question is “when?” As everyone knows, we usually get a “Santa Clause rally” the last week of the year. But, there have been notable exceptions such as 2018 when SPX finished off a 20% correction on Dec 26.

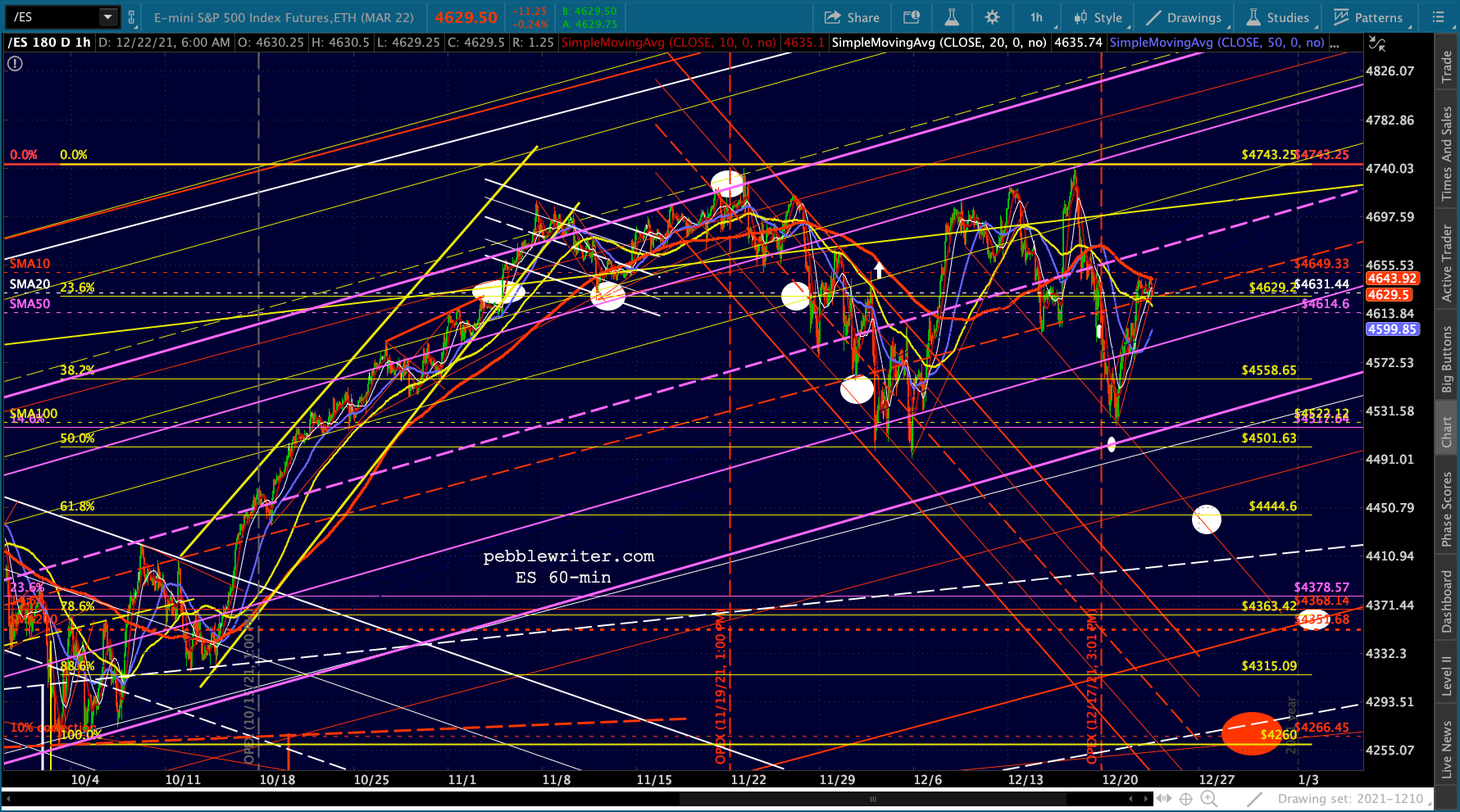

The bounce from just above the SMA100 has stabilized based on the usual support from USDJPY, VIX and CL. As the channels within which ES/SPX continue rising, the odds of a SMA200 tag theoretically continue declining because there is a very strong preference for backtests which don’t result in a channel breakdown.

SPX’s rising white channel would allow a .786 and SMA200 backtest as long as it happened very quickly, as in the next session or two. Otherwise, the channel bottom would have to be breached or the downturn would have to be more limited – say, the .618 in mid-January.

SPX’s rising white channel would allow a .786 and SMA200 backtest as long as it happened very quickly, as in the next session or two. Otherwise, the channel bottom would have to be breached or the downturn would have to be more limited – say, the .618 in mid-January. Of course, if the channel and SMA200 ever broke down, there are many logical downside targets to consider.

Of course, if the channel and SMA200 ever broke down, there are many logical downside targets to consider.  COMP still looks vulnerable to me.

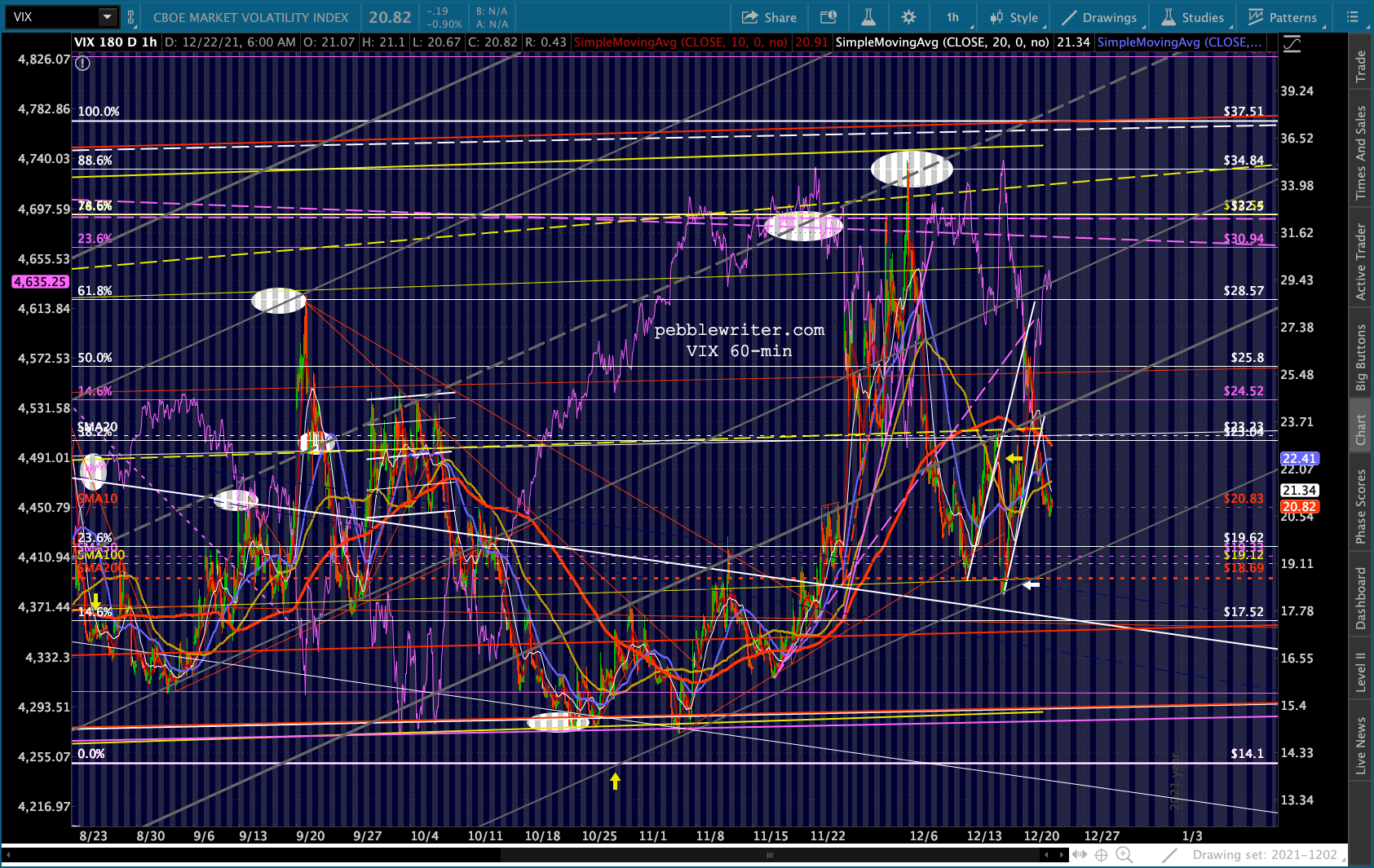

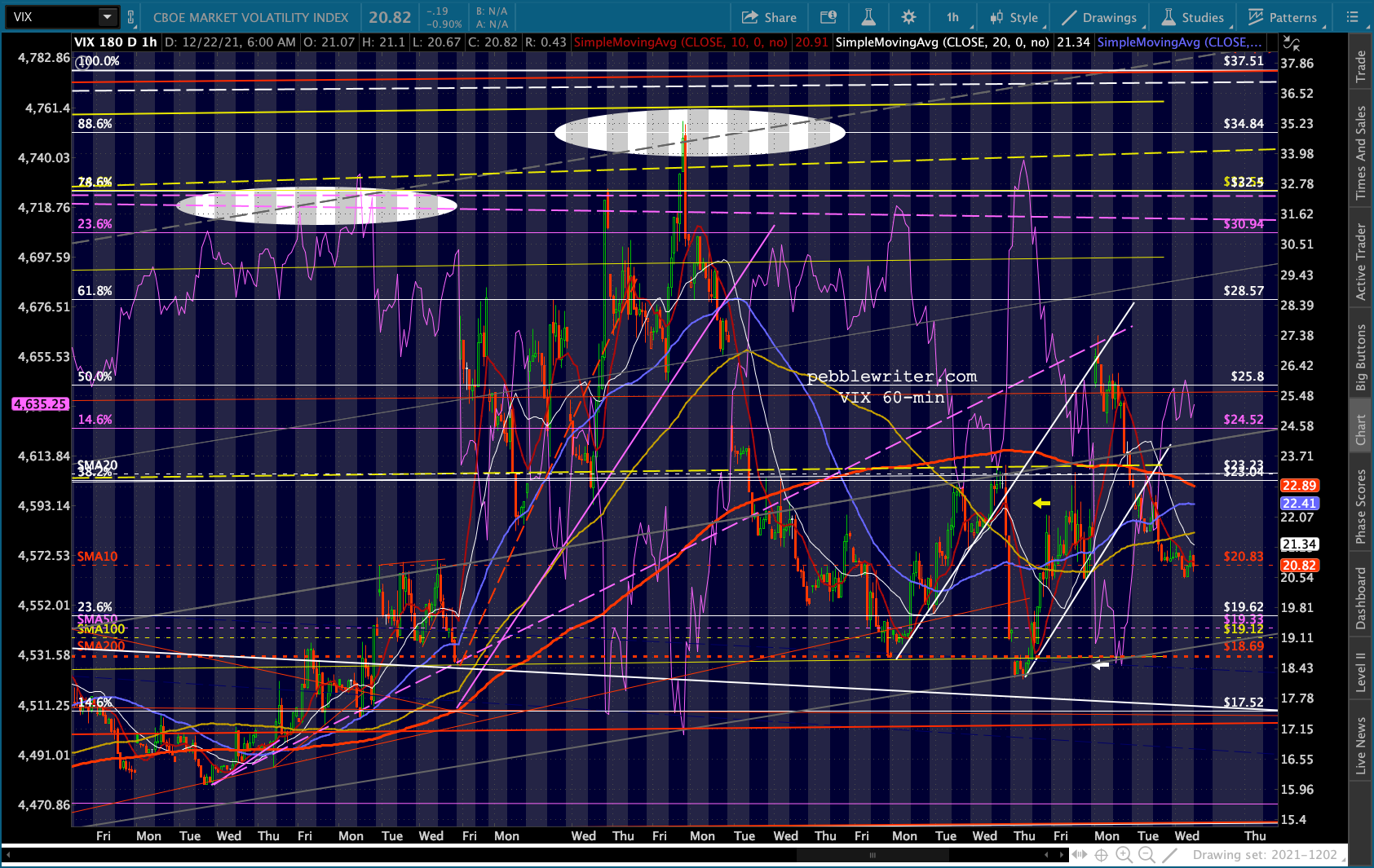

COMP still looks vulnerable to me. VIX has plenty of room to which it can dip, starting with its SMA10 and culminating with the SMA200 not far below at 18.69.

VIX has plenty of room to which it can dip, starting with its SMA10 and culminating with the SMA200 not far below at 18.69.

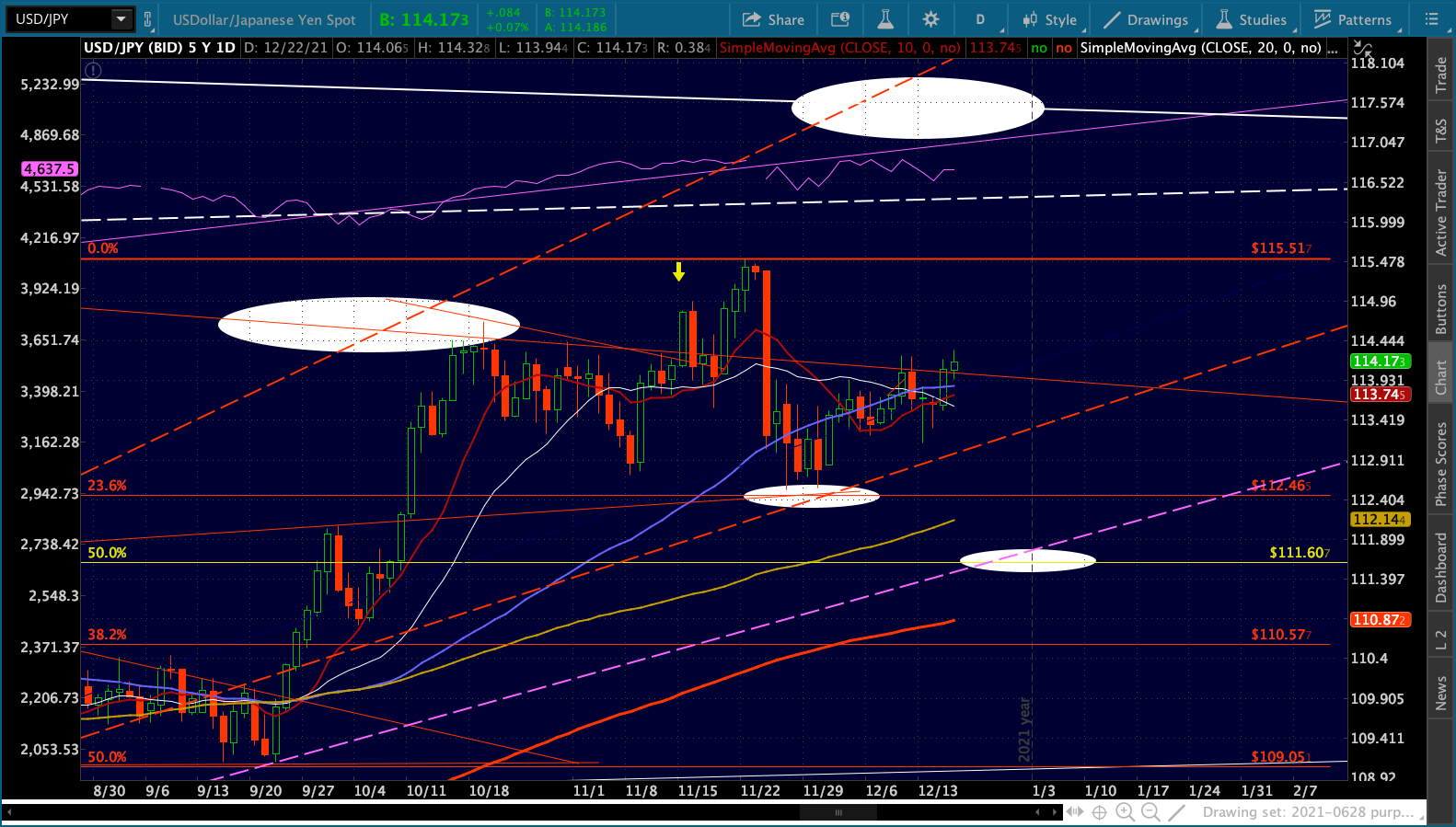

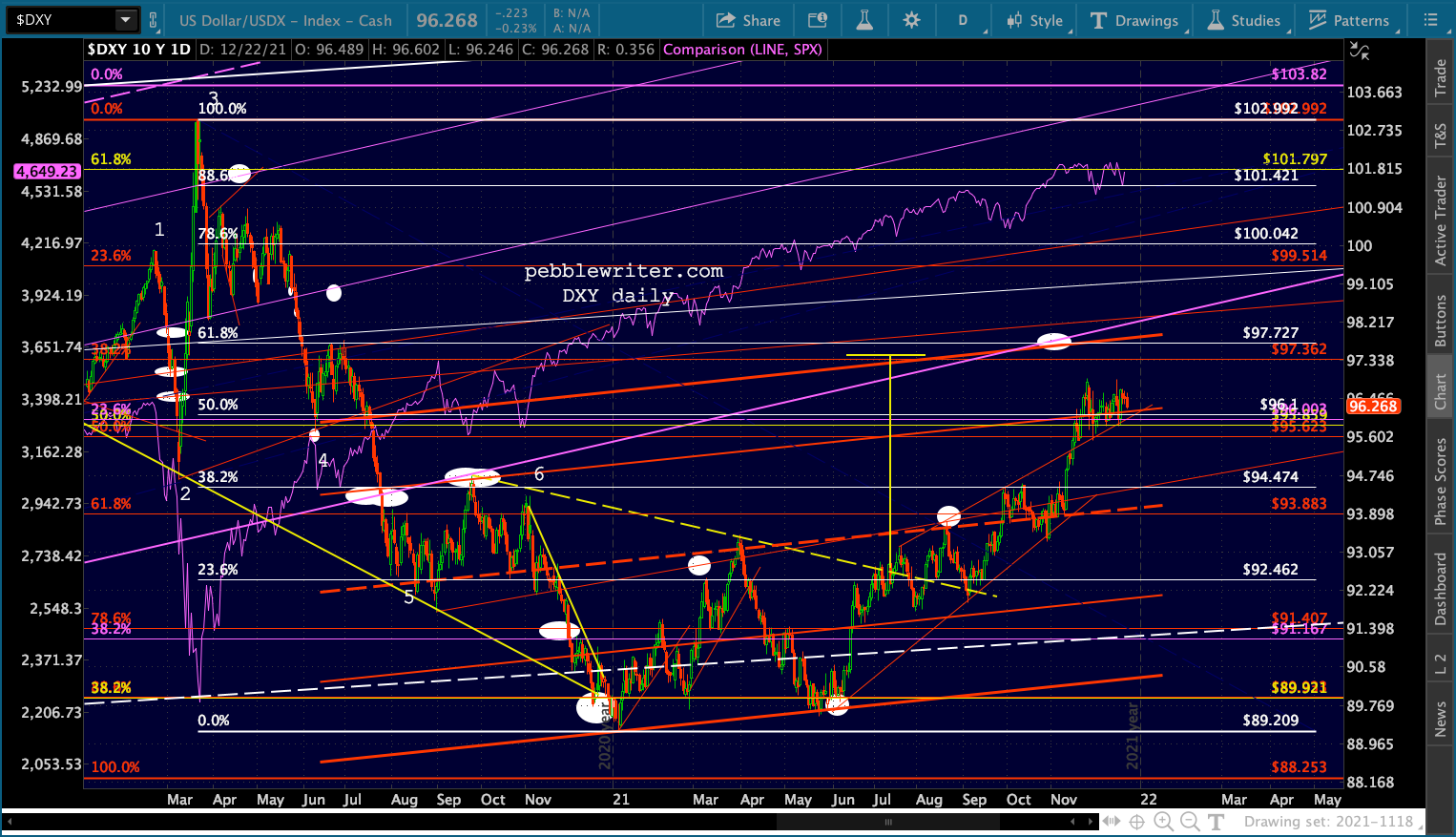

USDJPY is slipping higher…

USDJPY is slipping higher…

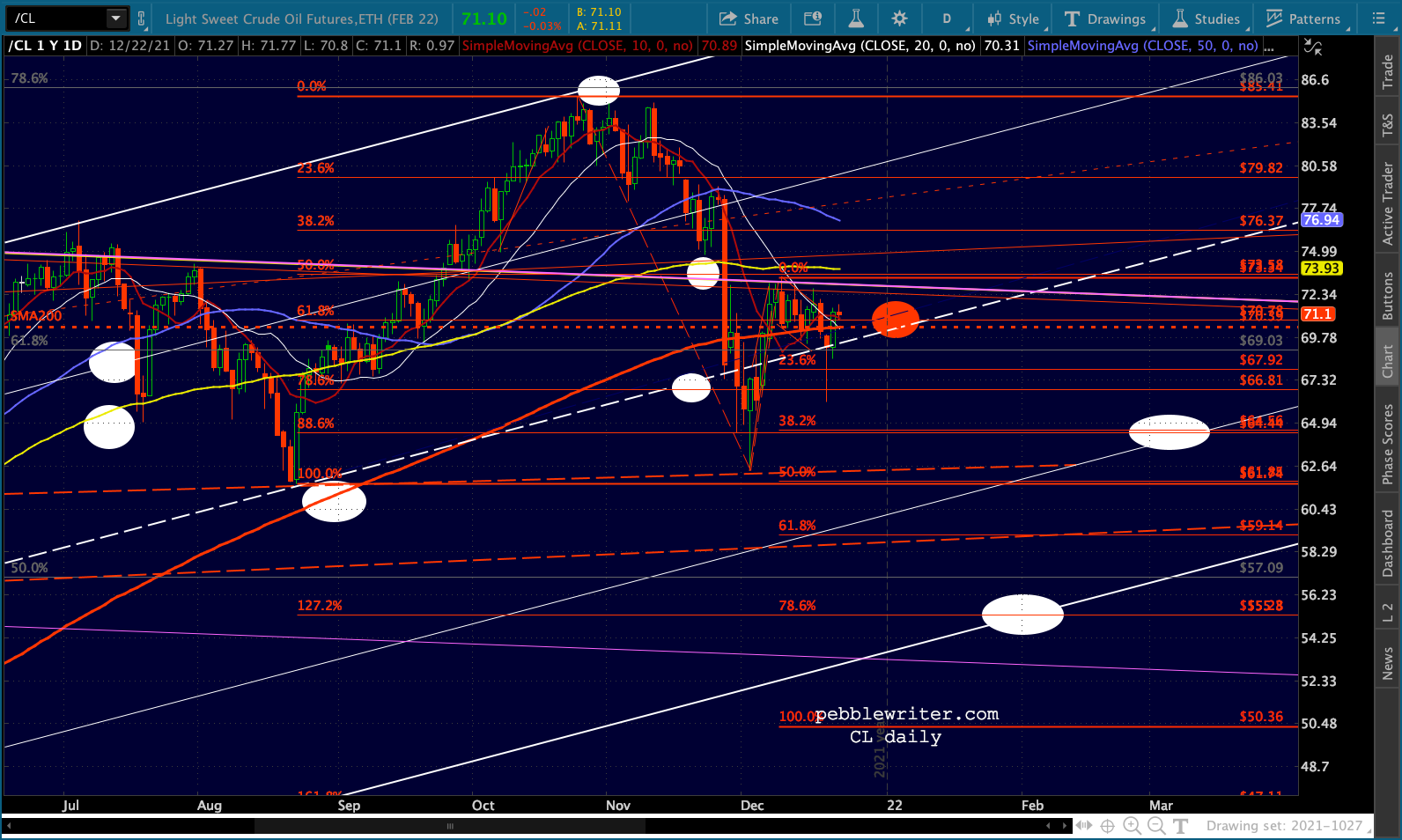

…and CL is of course back above its SMA200.

…and CL is of course back above its SMA200.

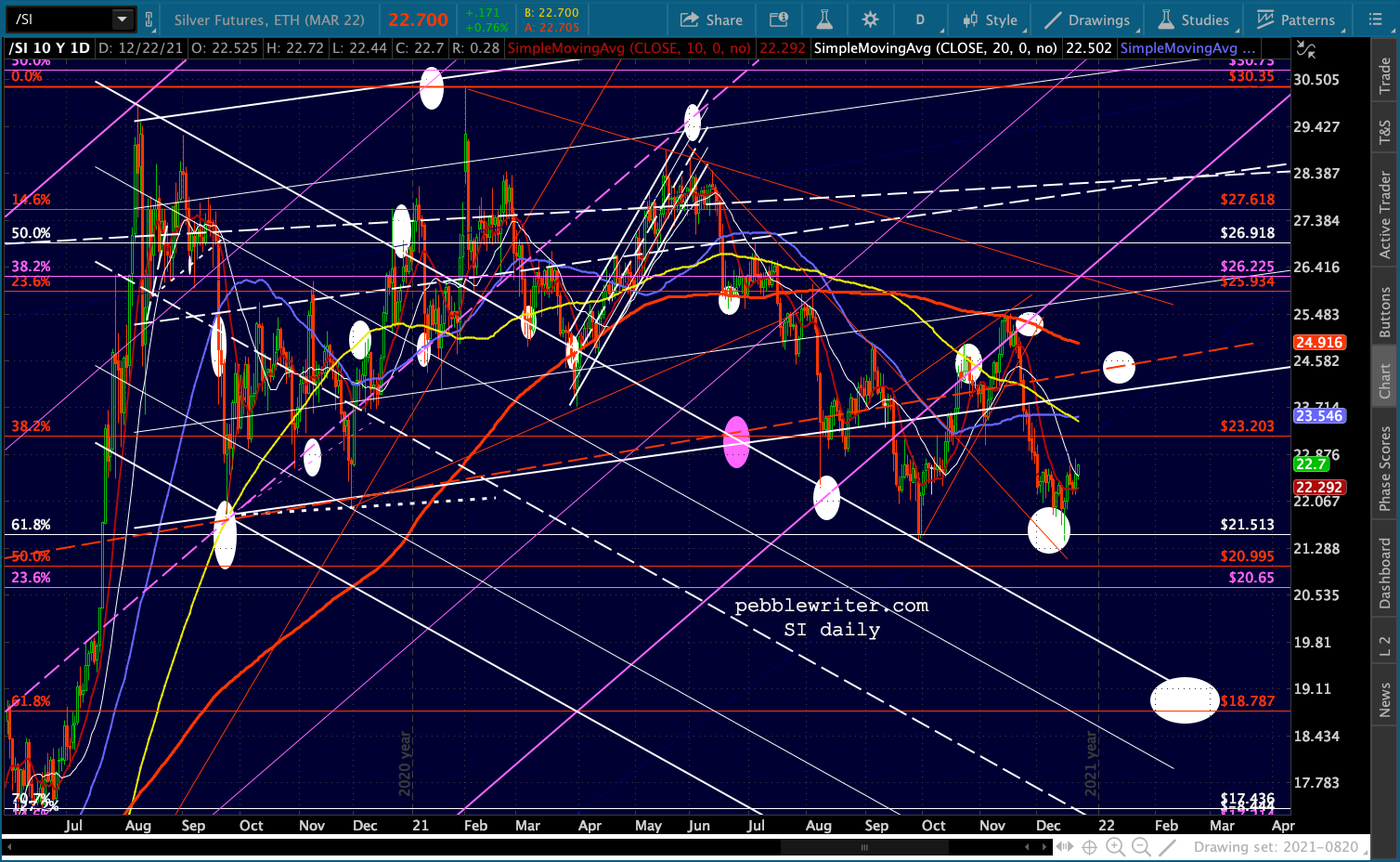

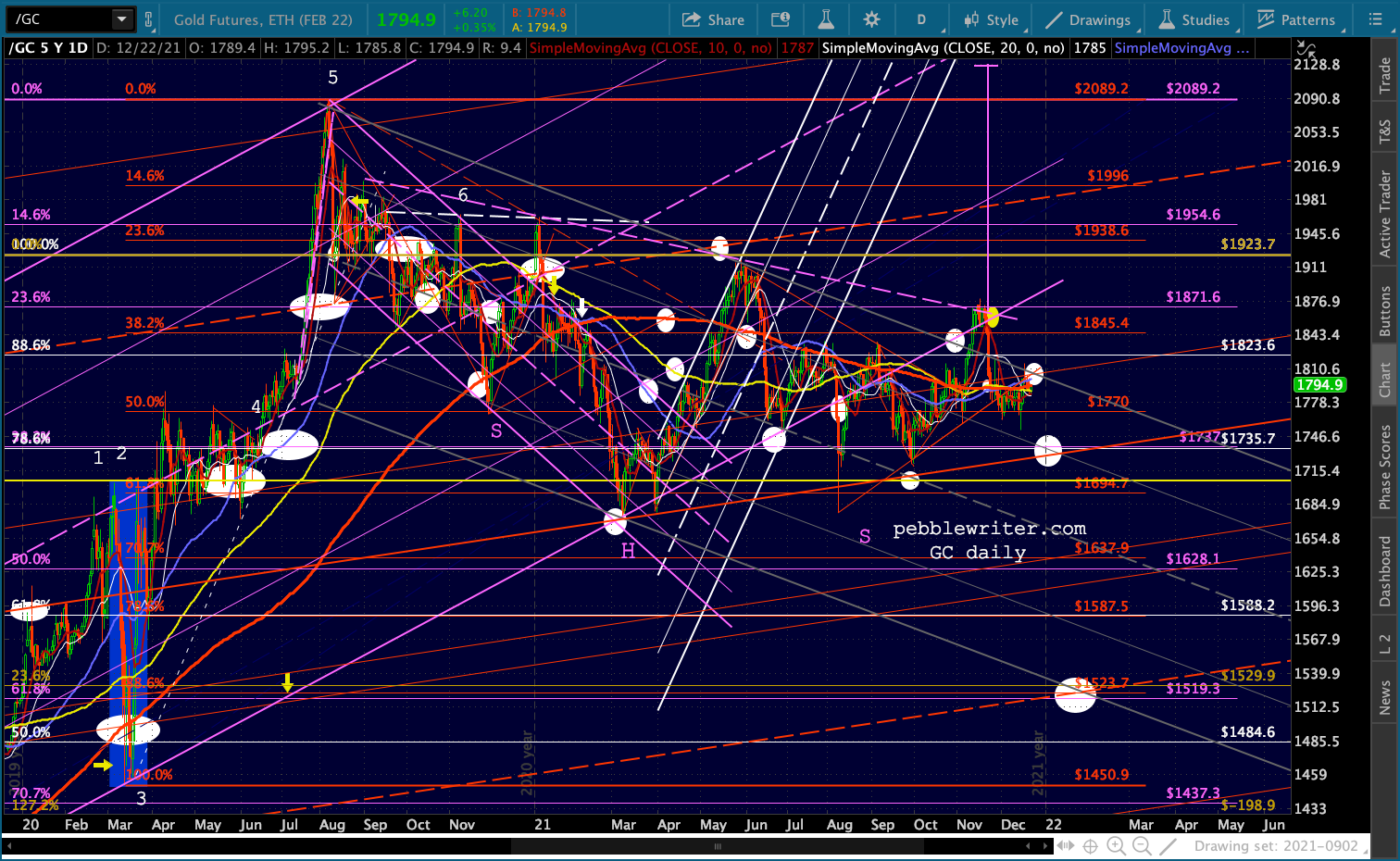

As long as the overall market is being propped up, SI and GC probably won’t decline much. SI, in particular, could easily bounce up to test its SMA200 all over again as it reaches the red fan line at around 24.45. I’ve added a target reflecting that possibility.

As long as the overall market is being propped up, SI and GC probably won’t decline much. SI, in particular, could easily bounce up to test its SMA200 all over again as it reaches the red fan line at around 24.45. I’ve added a target reflecting that possibility. GC is still hemmed in.

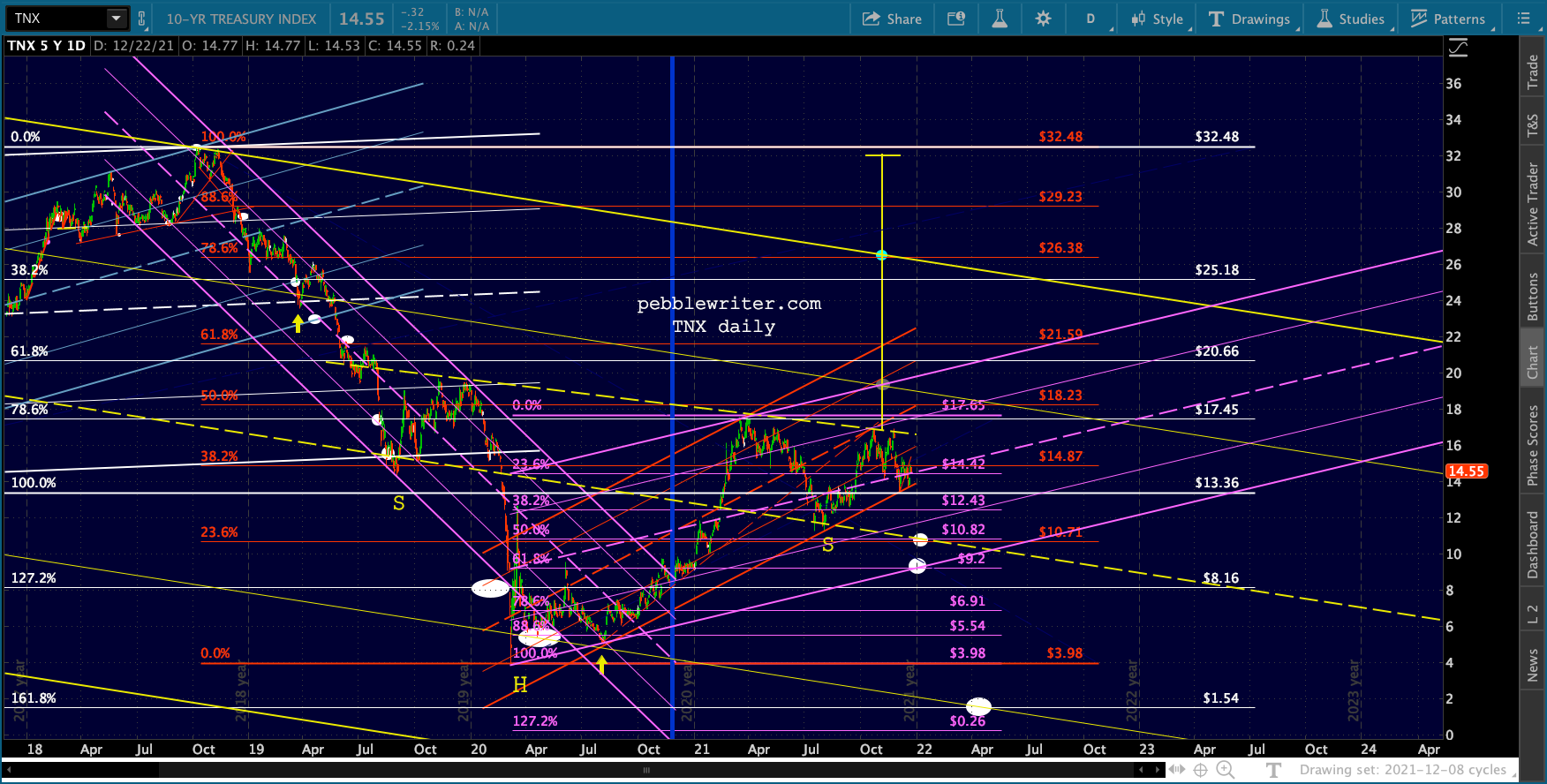

GC is still hemmed in. Last, TNX is still in limbo.

Last, TNX is still in limbo.