November PCE came in slightly better than estimates at 0.1% versus 0.2% MoM and 2.4% versus 2.5% expected but higher than October’s 2.3%.

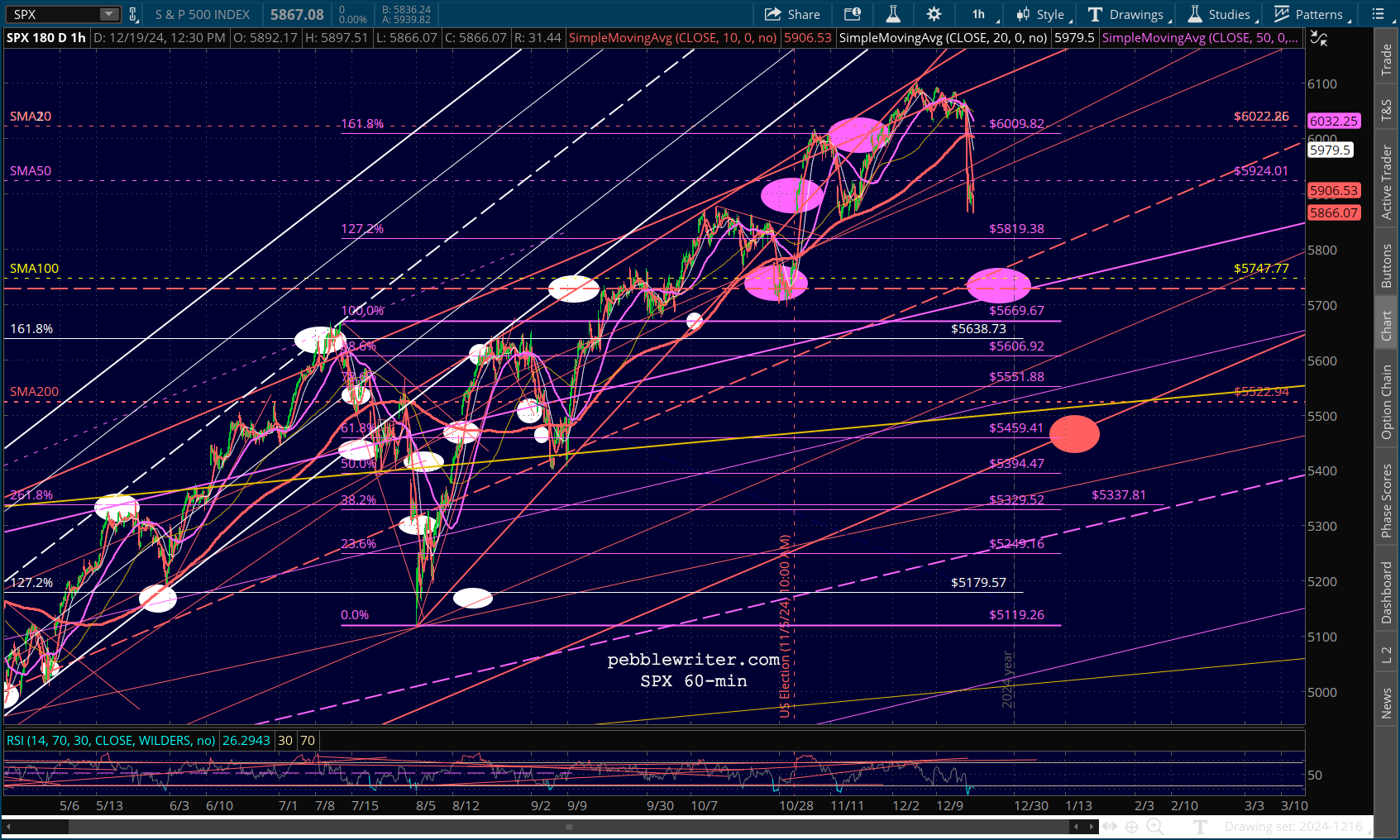

All told, the print took a little pressure off futures, which are still down about 0.5% as we approach the open. Note that ES has nearly reached our 5852 target.

continued for members…

continued for members…

This represented a nice backtest of its July highs for ES, but it leaves SPX well short of its own.

SPX closed yesterday with its SMA10 a few cents higher than its SMA20, so some algos were left in a marginally good place.

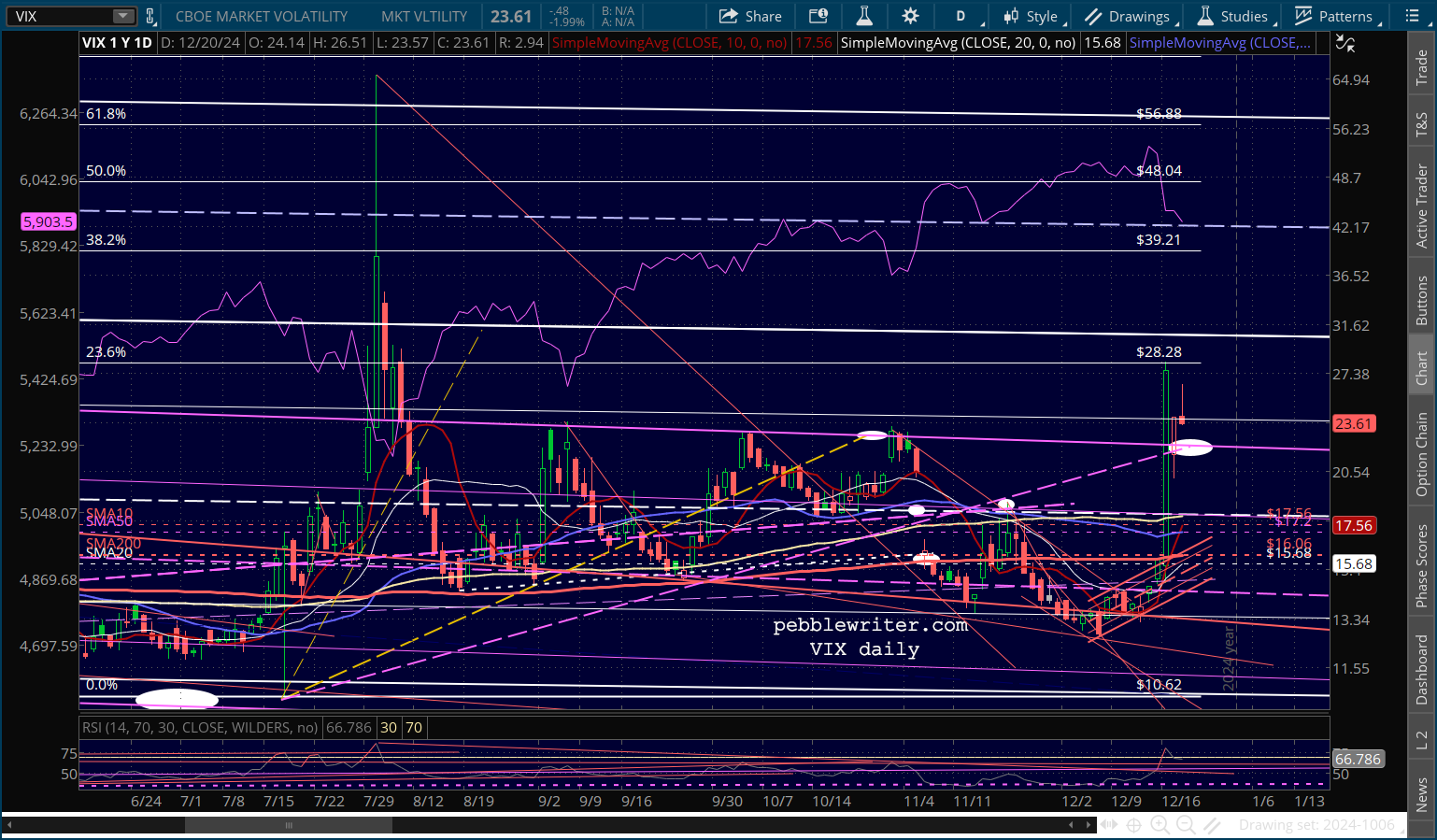

SPX closed yesterday with its SMA10 a few cents higher than its SMA20, so some algos were left in a marginally good place. VIX tumbled from its overnight highs, but remains above the purple channel top, the SMA200, etc.

VIX tumbled from its overnight highs, but remains above the purple channel top, the SMA200, etc.  Currencies also contributed to paring the equity damage, with the EURUSD featuring a decent bounce – though the DXY is still slightly higher.

Currencies also contributed to paring the equity damage, with the EURUSD featuring a decent bounce – though the DXY is still slightly higher.

Oil and gas are both slightly lower, which has helped take some pressure off rates.

Oil and gas are both slightly lower, which has helped take some pressure off rates.

But, the 10Y is still broken out…

But, the 10Y is still broken out…  …and the 2s10s is still signaling a very substantial potential pullback.

…and the 2s10s is still signaling a very substantial potential pullback. The 2Y and 10Y are currently moving in lock step. But, if the 2Y should tumble from here while the 10Y remains elevated, equities will get hammered. The government shutdown could be just the catalyst bears need.

The 2Y and 10Y are currently moving in lock step. But, if the 2Y should tumble from here while the 10Y remains elevated, equities will get hammered. The government shutdown could be just the catalyst bears need.