Jobless claims came in higher than expected, notching the highest level since June. ADP came in very light: 54K versus 59K expected and 106K prior. The 10Y gapped down to the lowest level since May 1, but futures remained flat.

continued for members…

continued for members…

We’ll get ISM services at 10, and of course, lots more jobs data tomorrow.

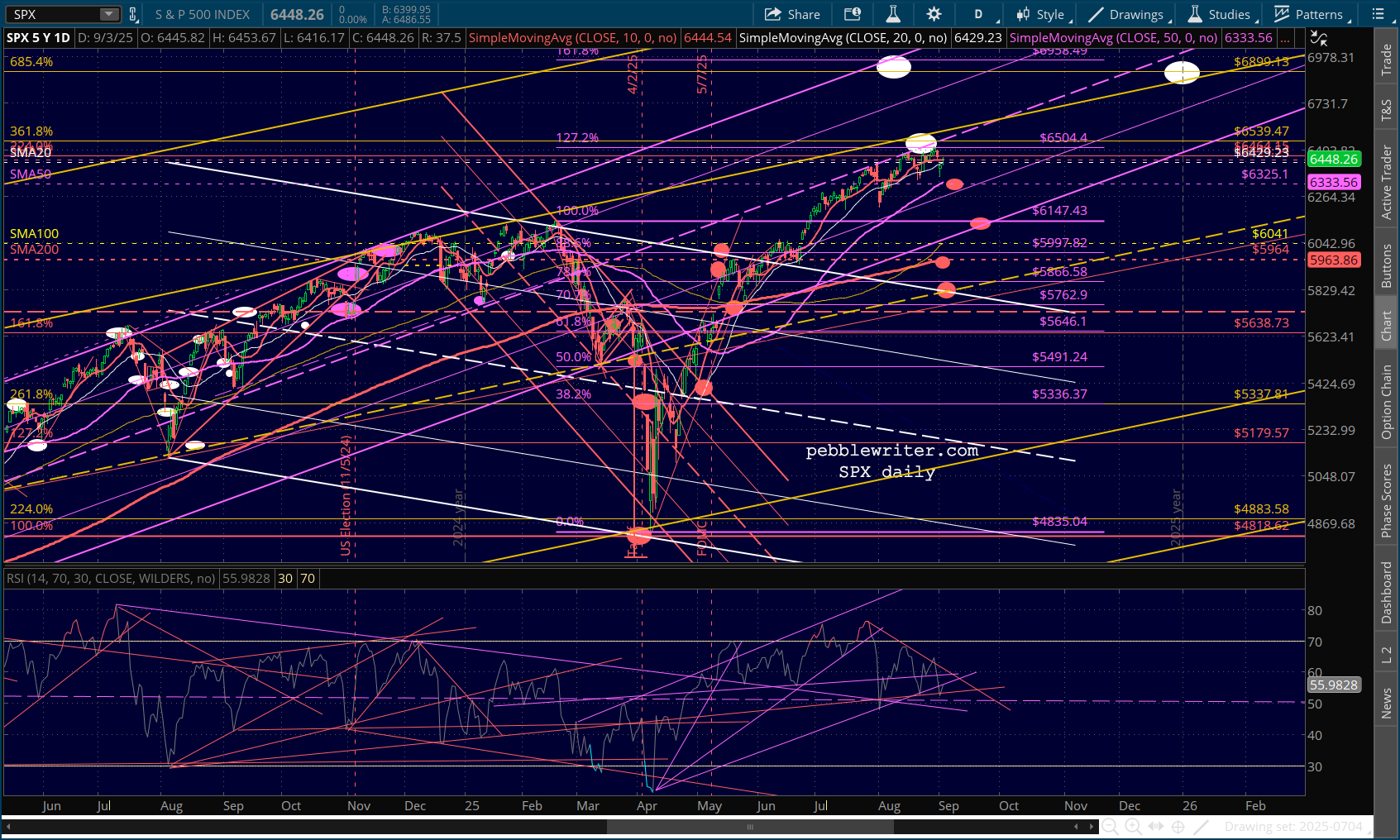

The equity setup remains very similar to yesterday.

The equity setup remains very similar to yesterday.

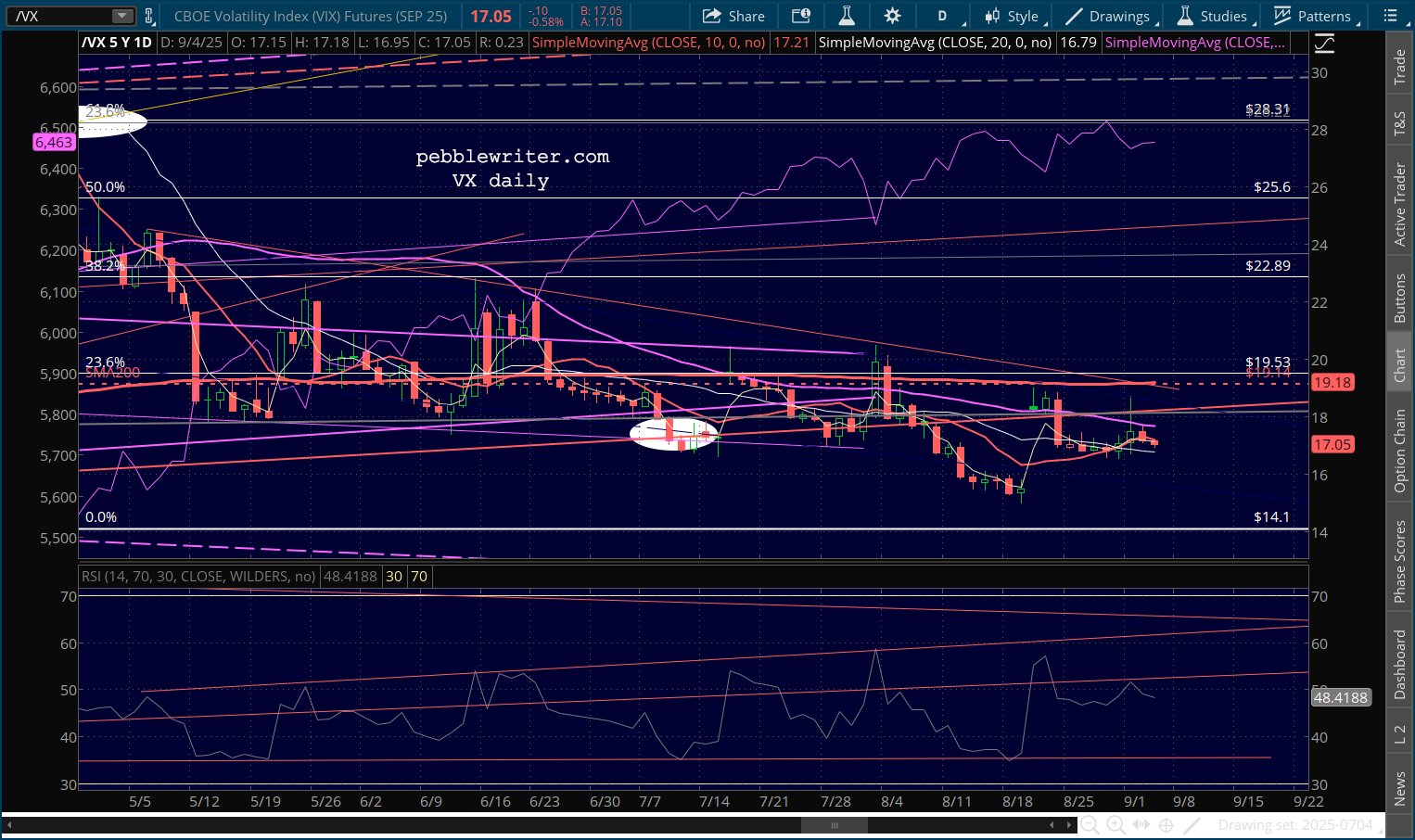

VIX is continuing to slip lower, finally testing its SMA50 overnight.

VIX is continuing to slip lower, finally testing its SMA50 overnight.

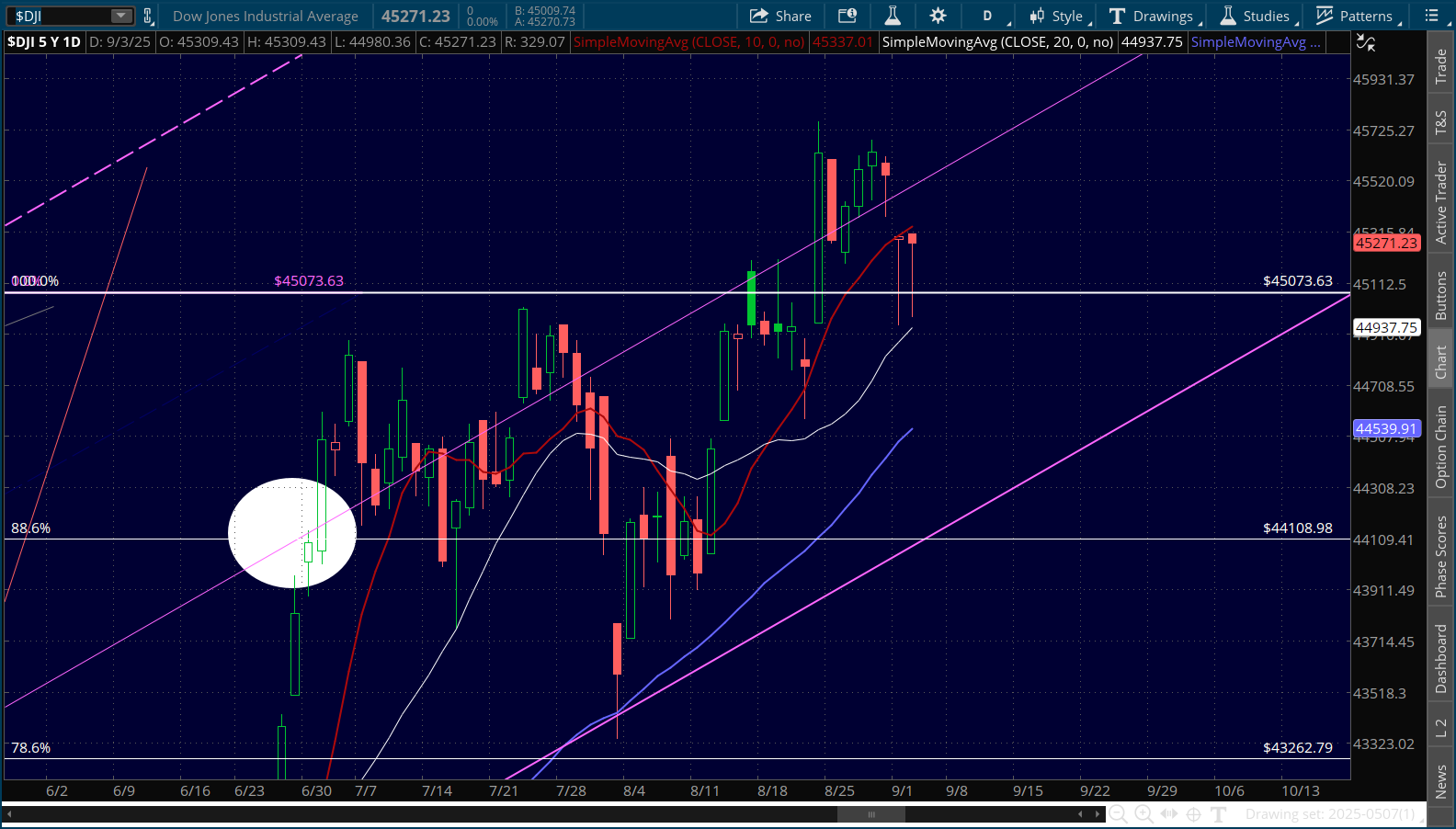

The Dow tested its former highs yet again.

The Dow tested its former highs yet again.

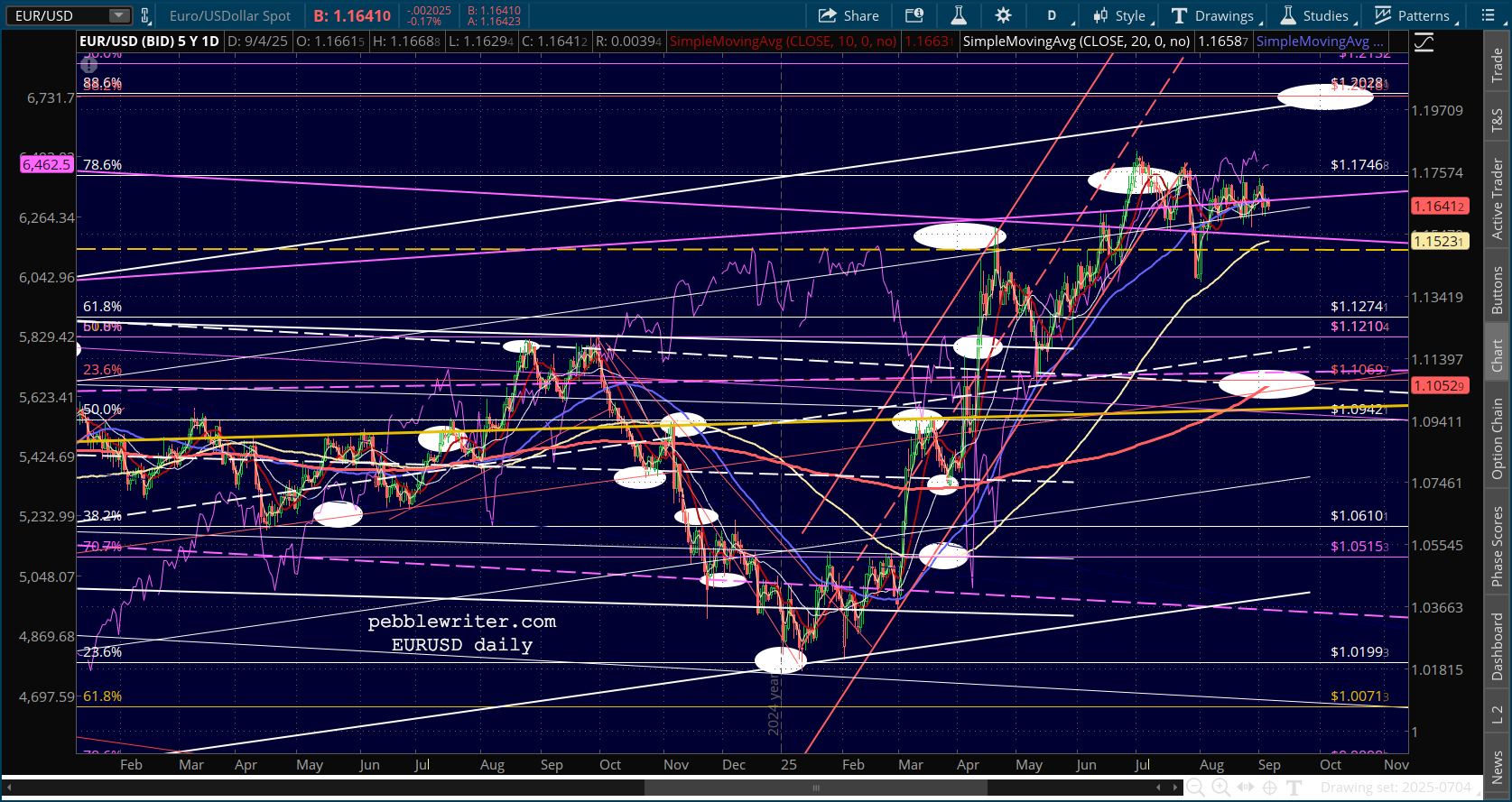

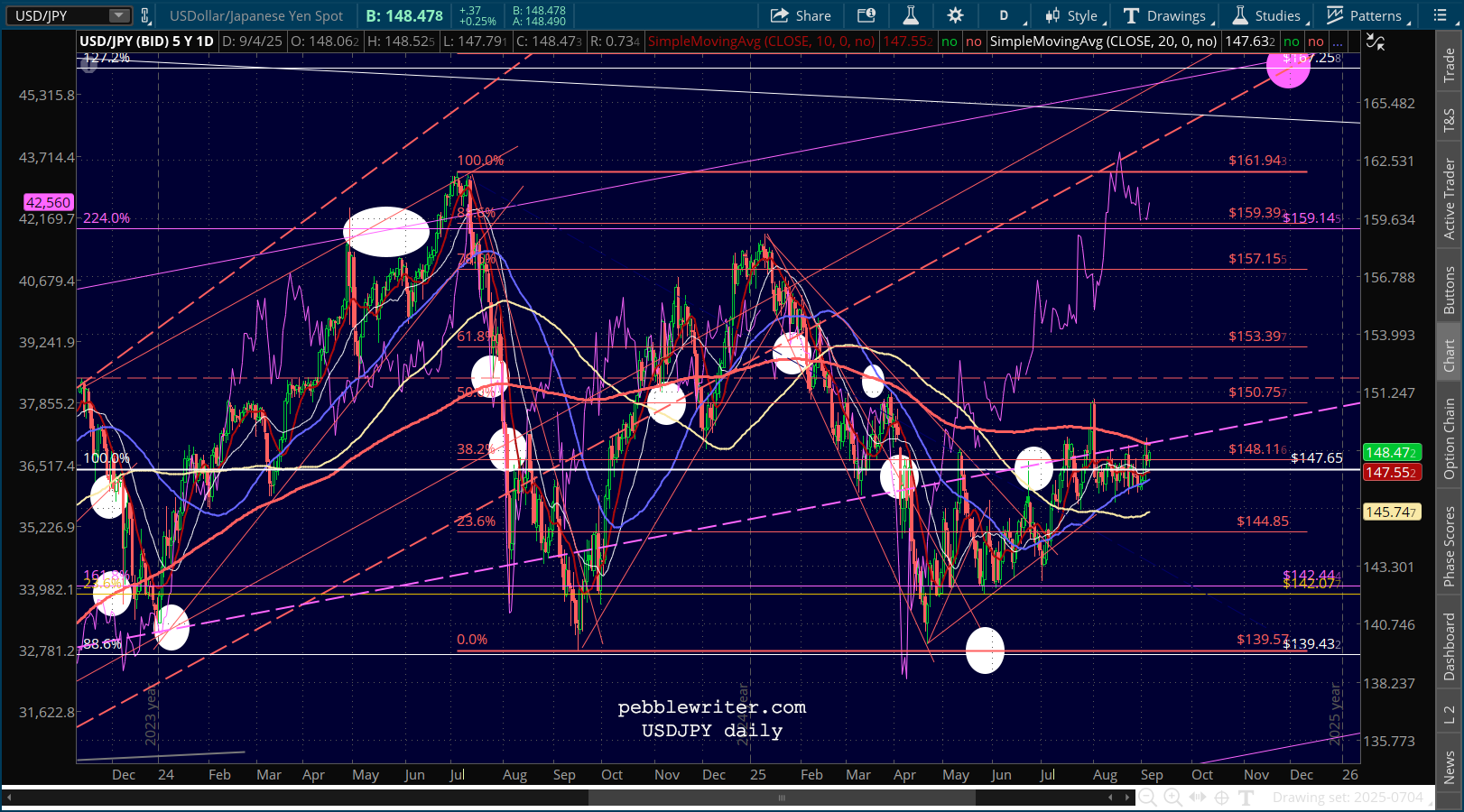

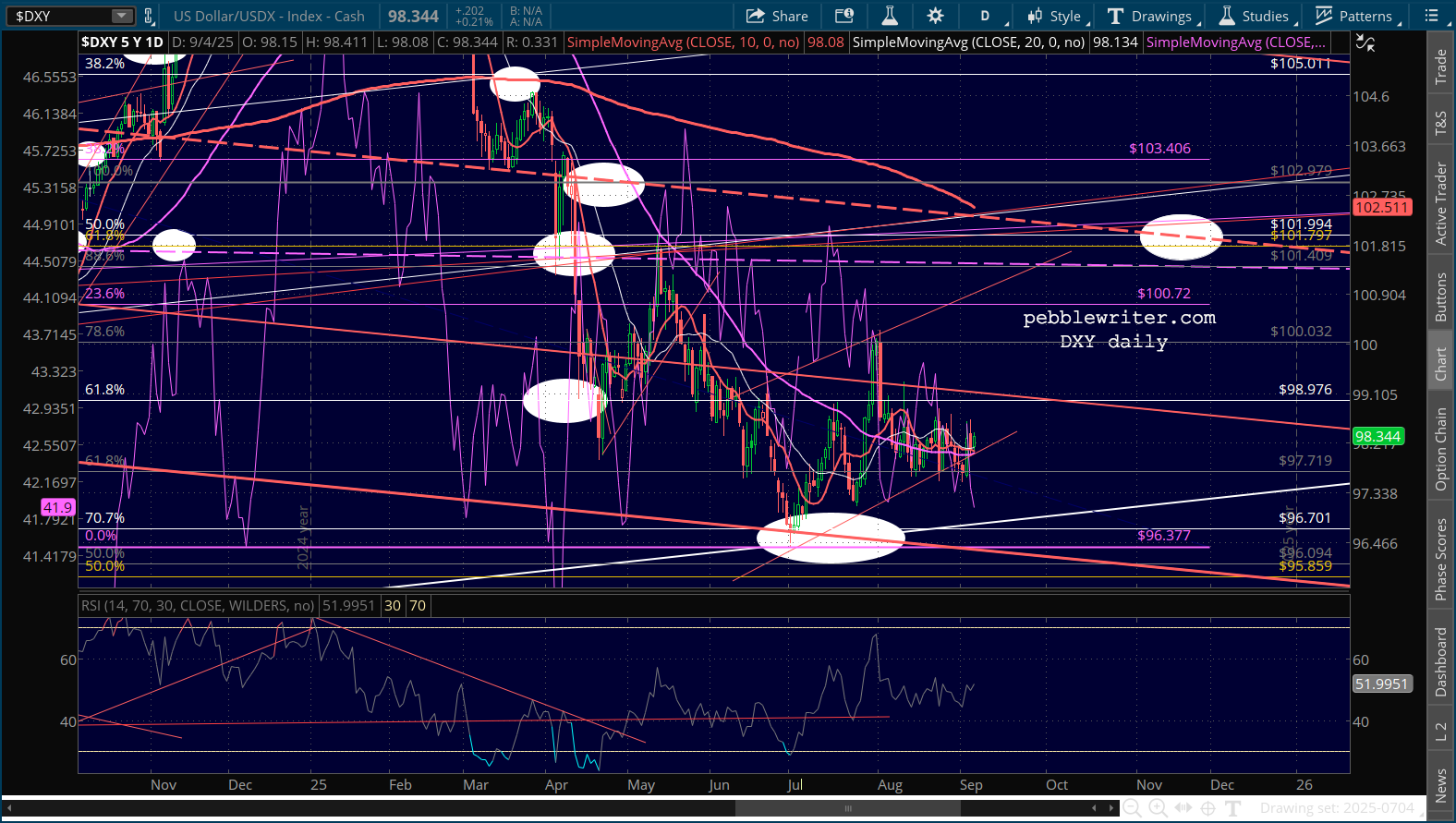

Currencies still aren’t rocking the boat.

Currencies still aren’t rocking the boat.

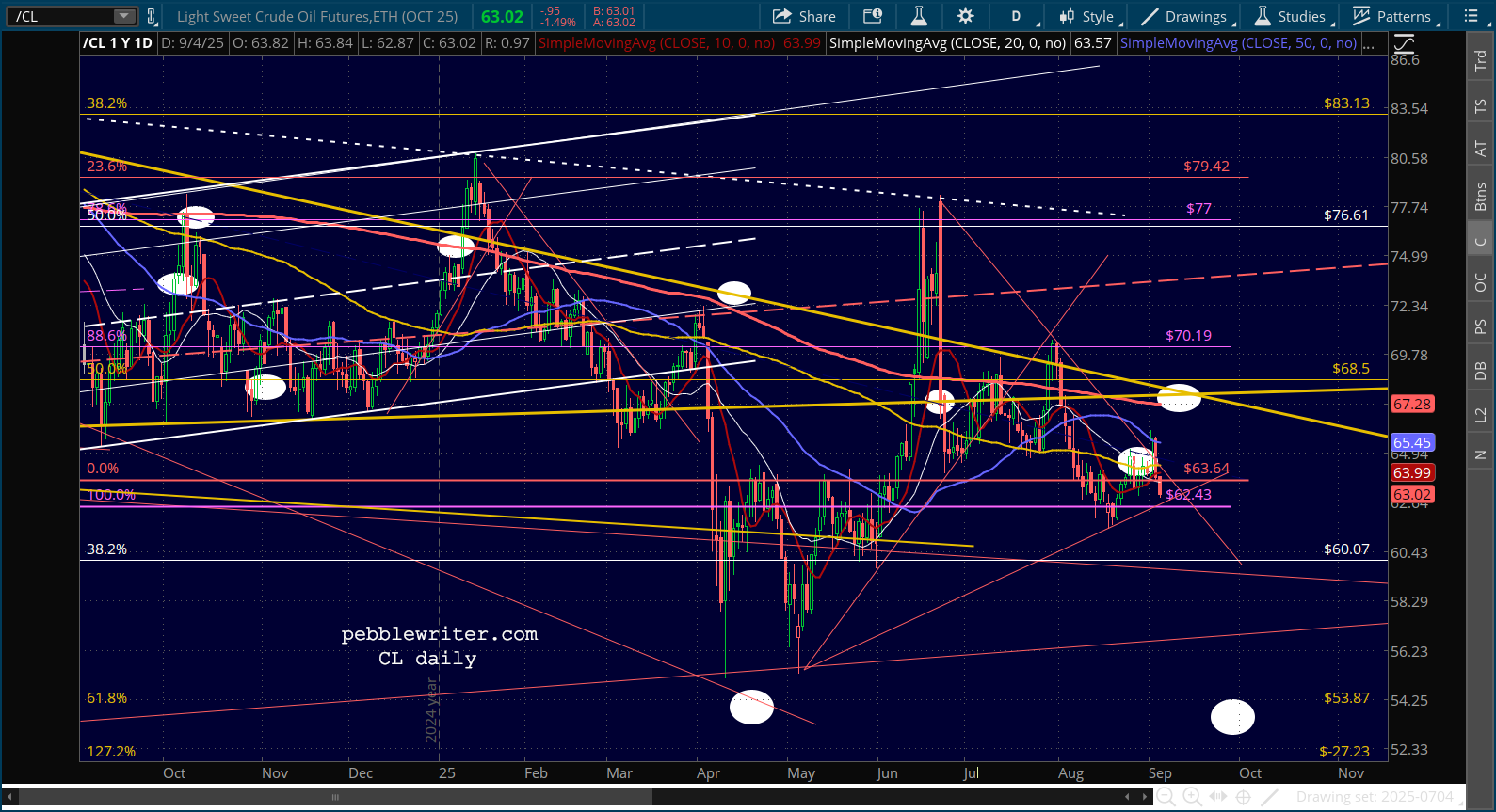

While CL tested an internal TL after a 1% loss, RB is holding steady.

While CL tested an internal TL after a 1% loss, RB is holding steady.

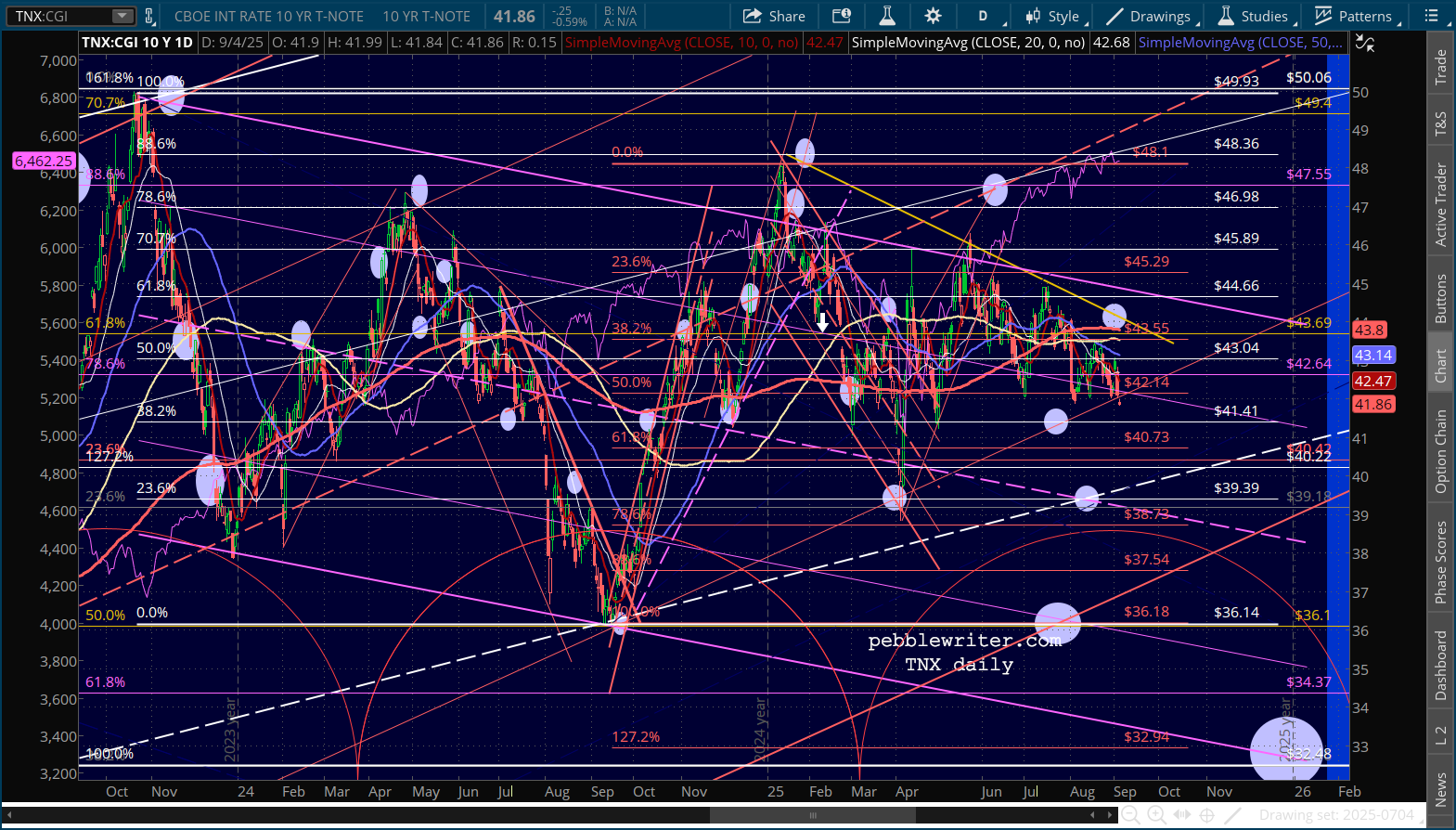

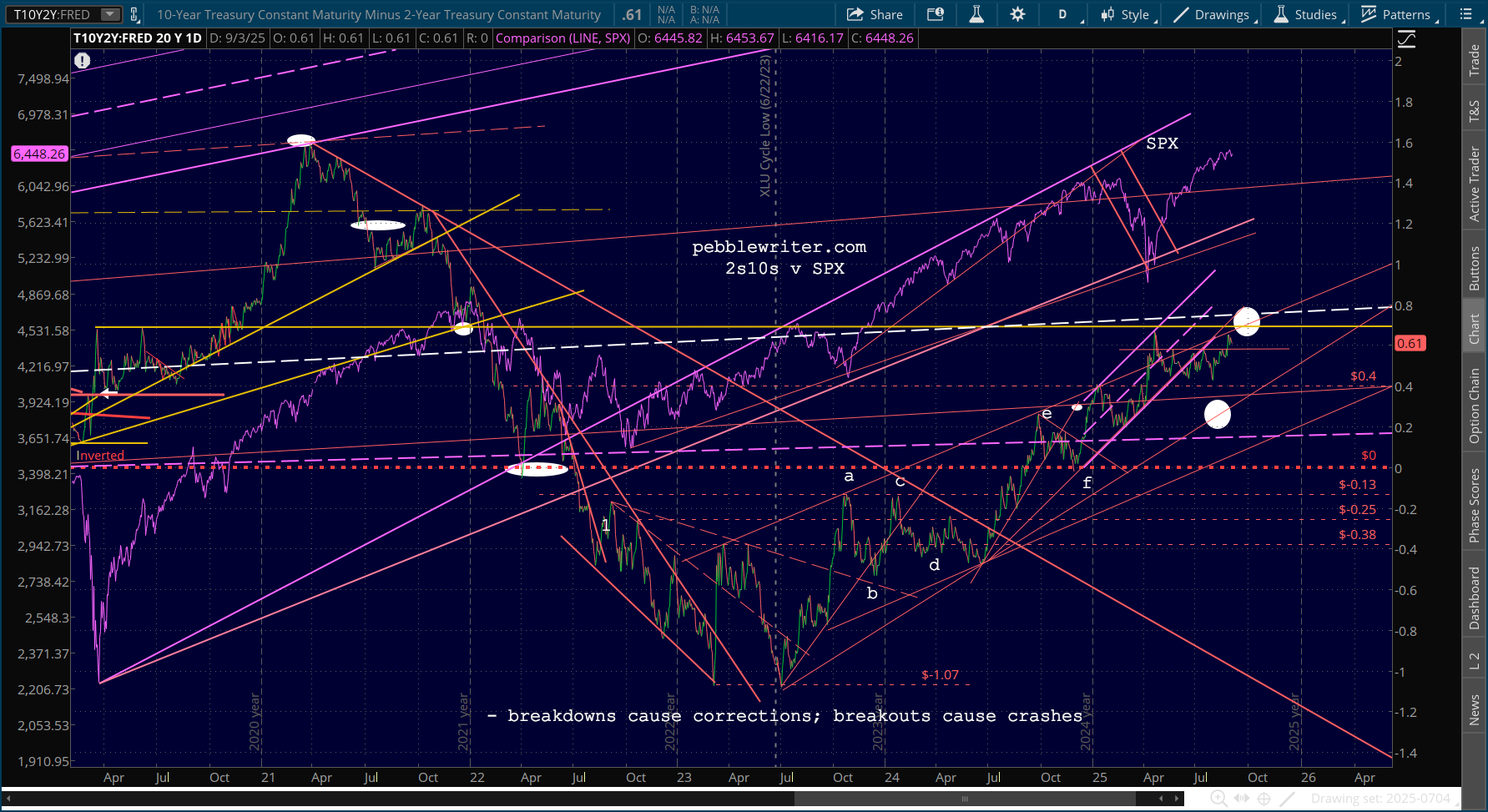

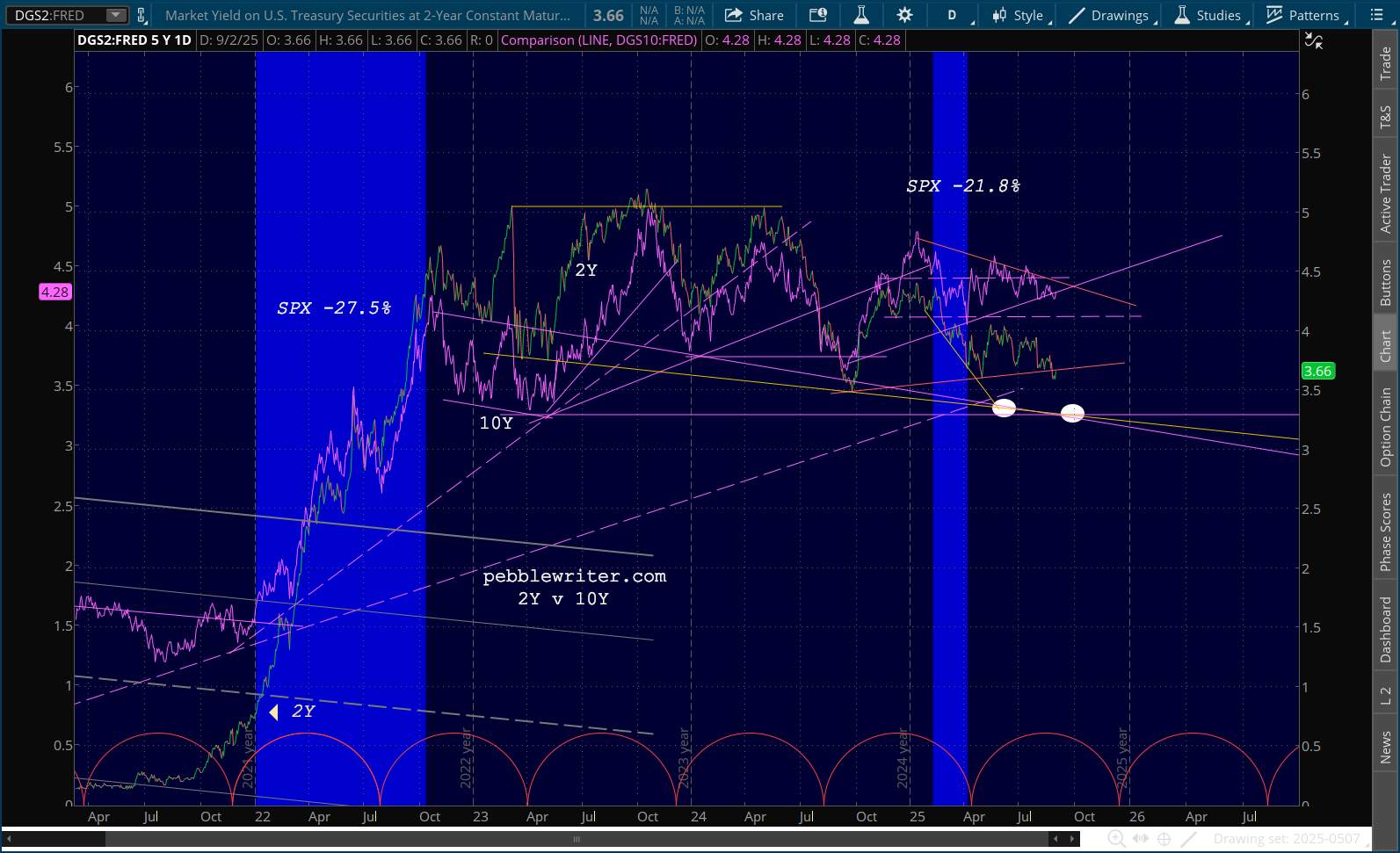

Most of the action was in the bond market. The 10Y dropped as low as 4.18, though the 2s10s remained steady at 61 bps.

Most of the action was in the bond market. The 10Y dropped as low as 4.18, though the 2s10s remained steady at 61 bps.

GLTA