The Fed’s annual symposium in Jackson Hole, Wyoming is historically an excellent opportunity to suss out the Fed’s thinking on next steps. While investors agree that a cut is coming in September, there is some divergence on how big a cut and what to expect over the balance of the year.

Futures are generally flat as we approach a week full of potentially important Fedspeak.

continued for members…

continued for members…

The most recent downturn has given up the ghost. We’re waiting to see whether ES can rejoin or is rebuffed by the broken white channel.

SPX hasn’t quite reached its white channel backtest, so potentially has a little more leeway.

SPX hasn’t quite reached its white channel backtest, so potentially has a little more leeway.

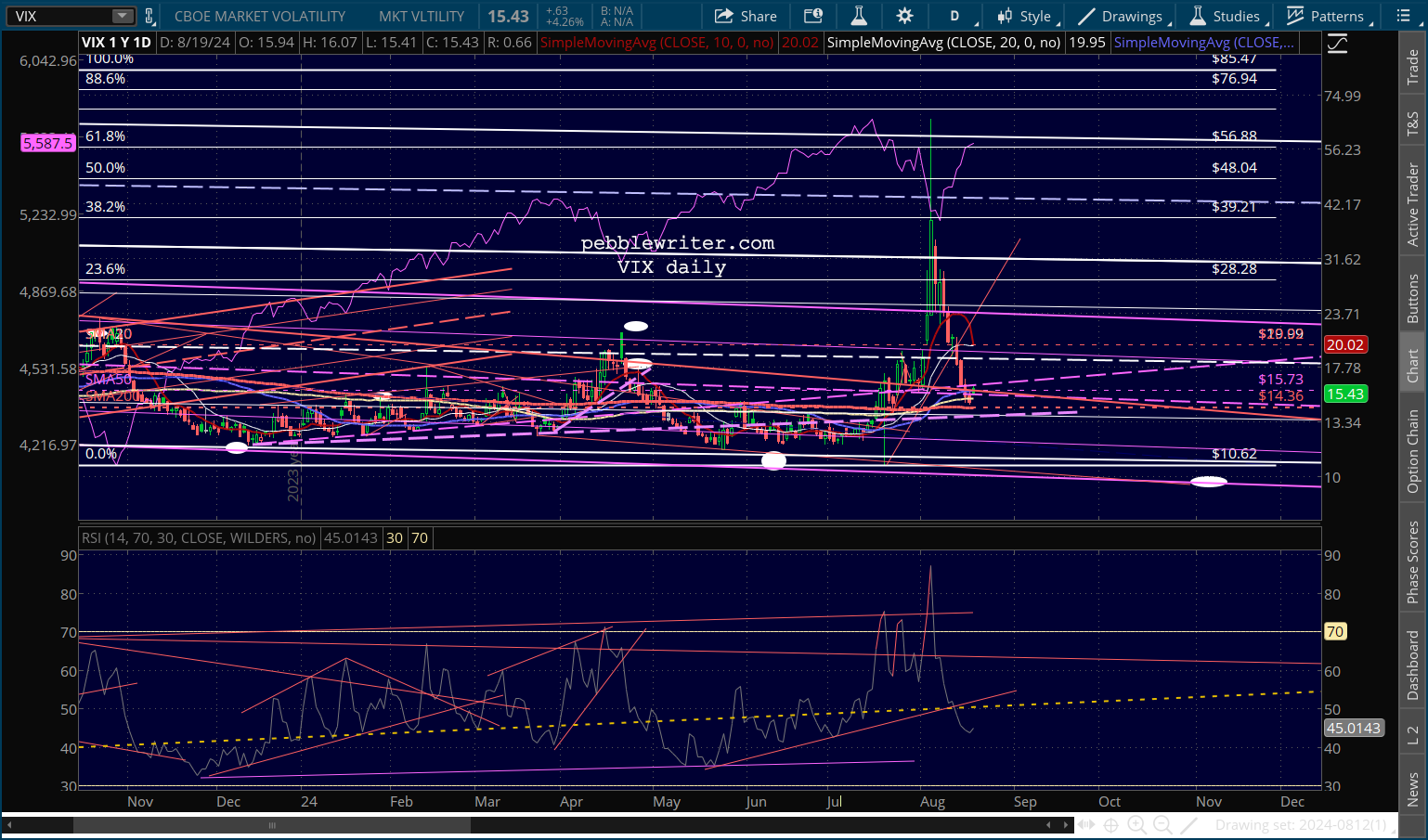

VIX is actually up over 4% this morning, suggesting that equities will falter somewhat at these levels. But, note that VIX’s SMA10 is about to cross back below its SMA20, a positive for stocks.

VIX is actually up over 4% this morning, suggesting that equities will falter somewhat at these levels. But, note that VIX’s SMA10 is about to cross back below its SMA20, a positive for stocks.

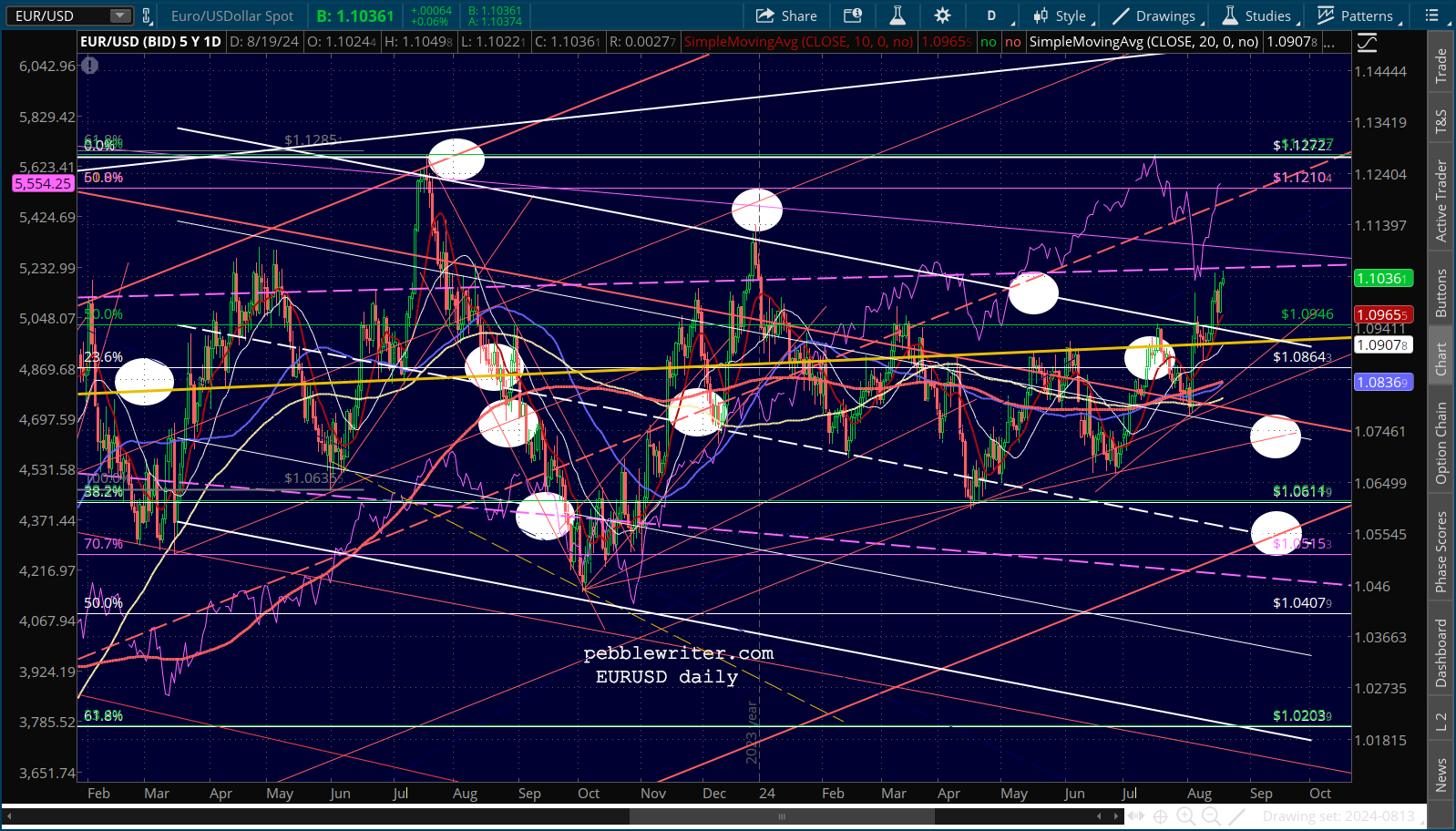

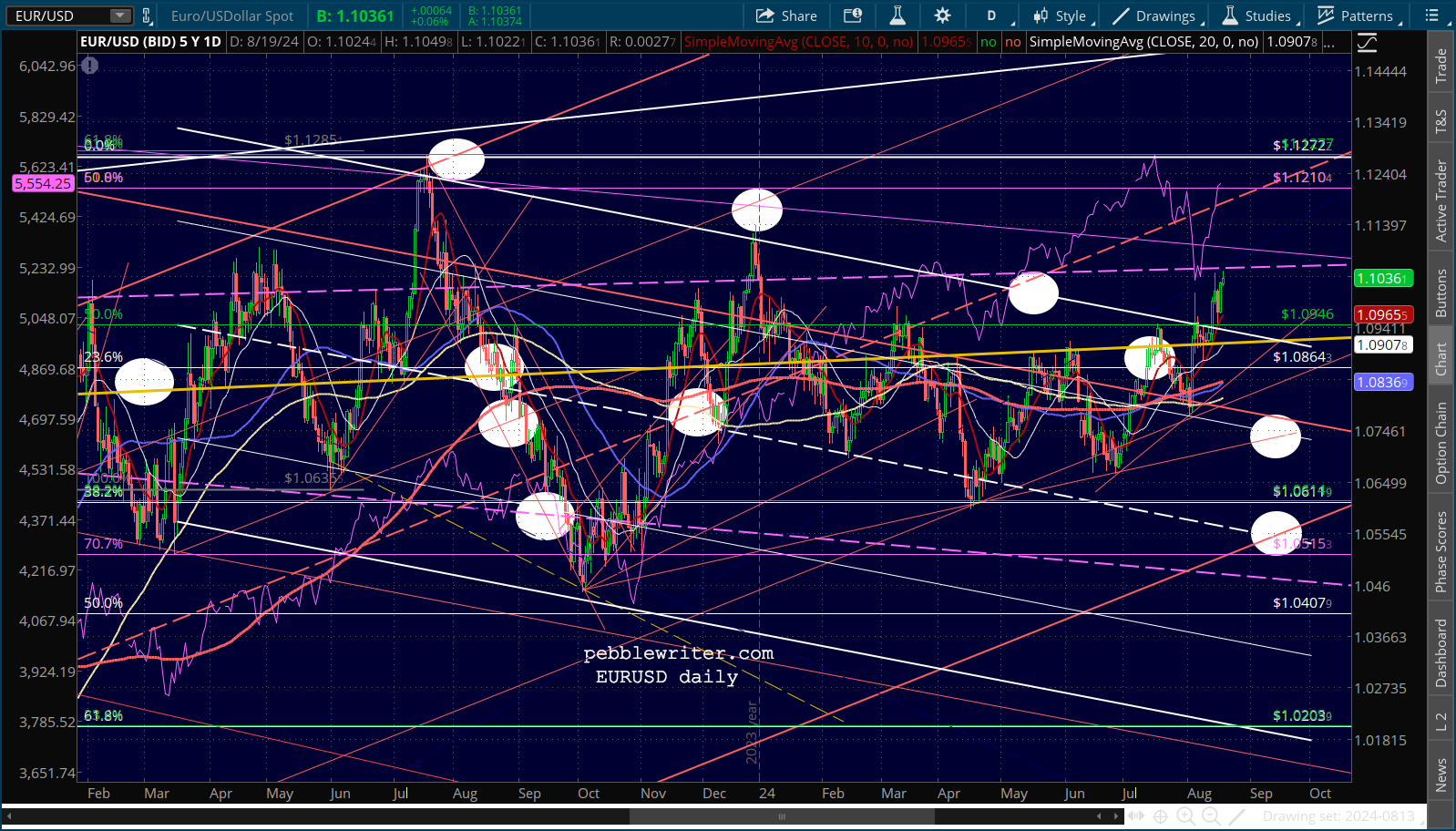

And, while EURUSD has pushed even higher…

And, while EURUSD has pushed even higher…

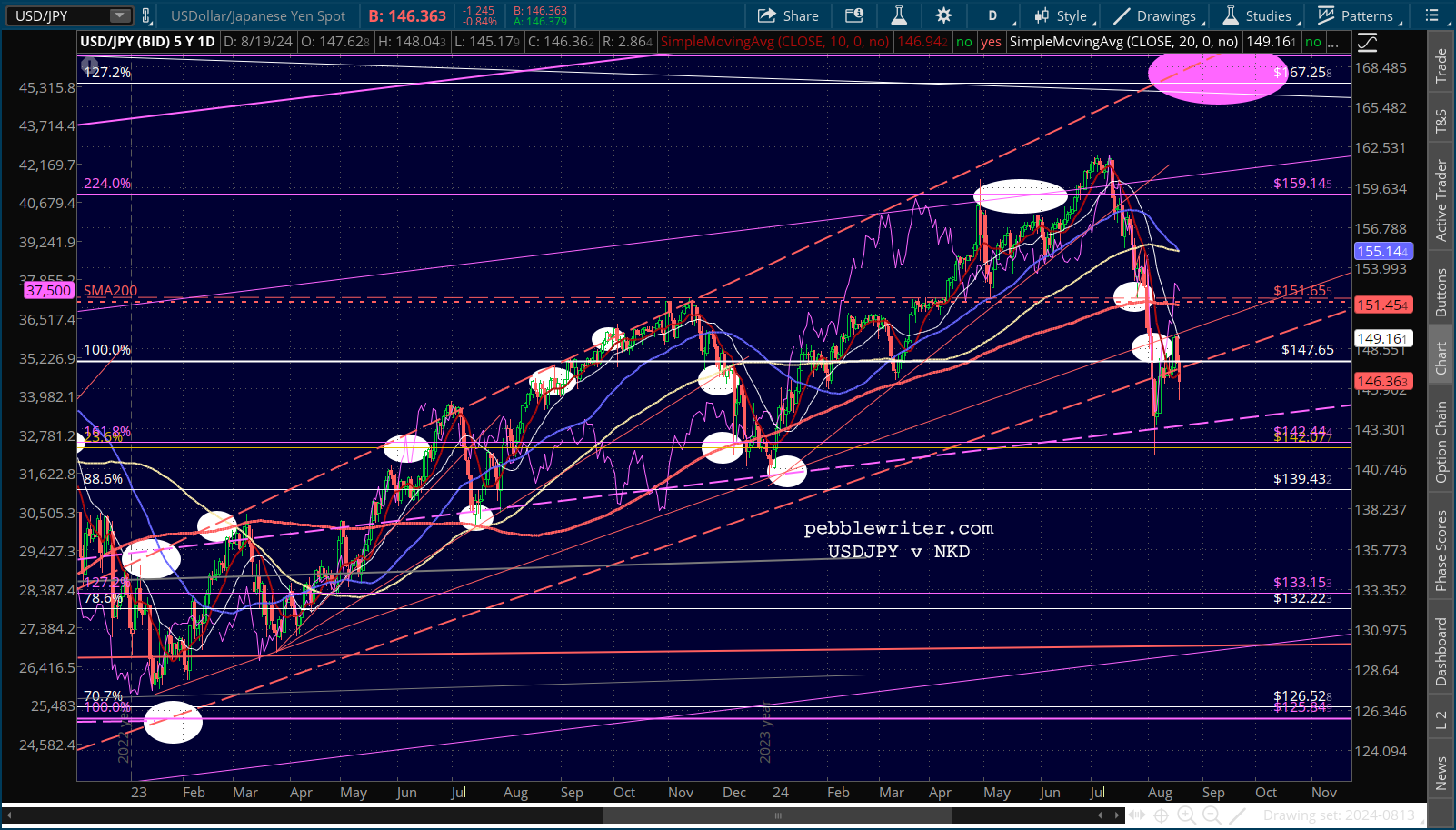

…USDJPY is back below the red TL…

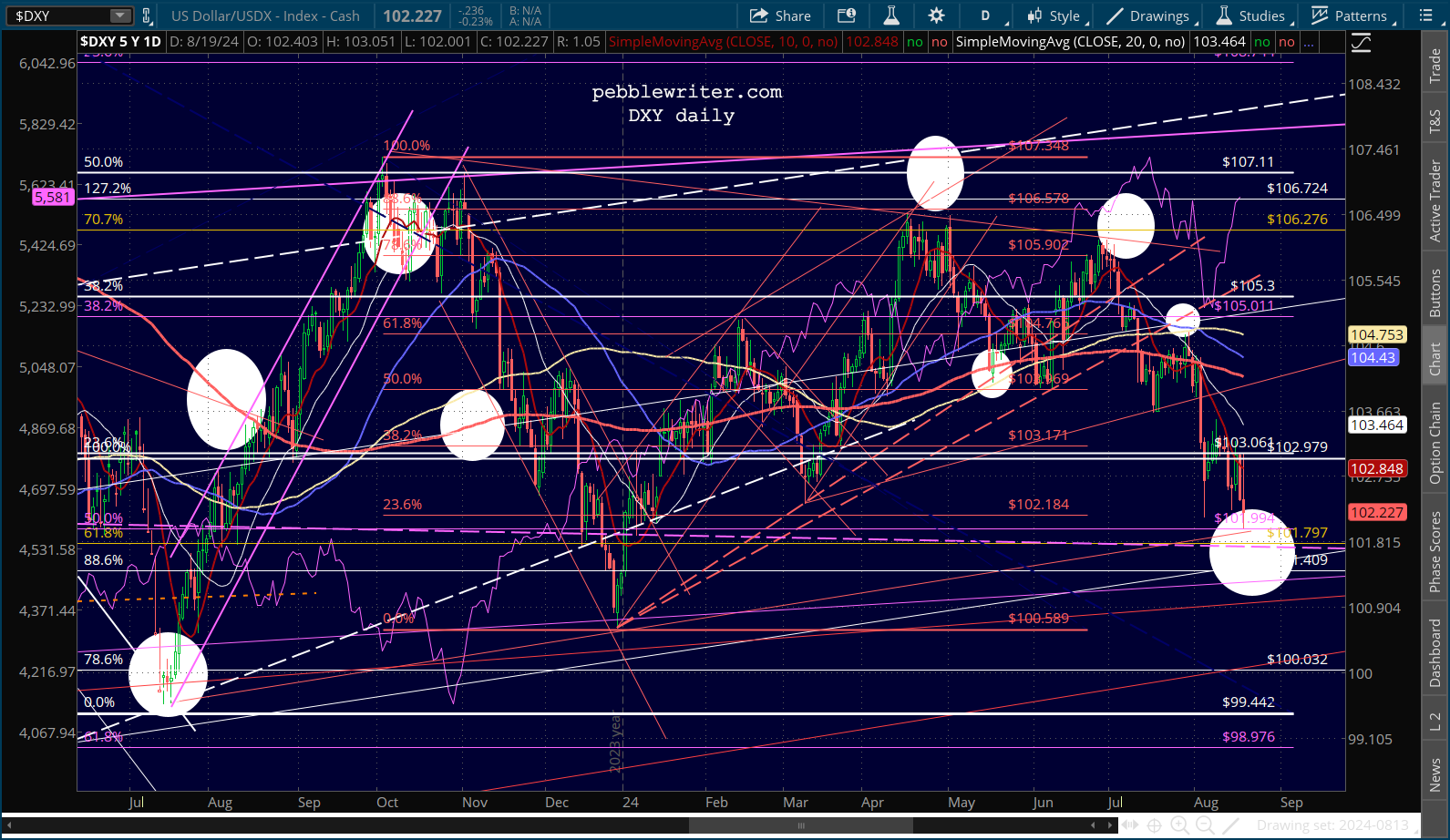

…USDJPY is back below the red TL… …and DXY has reached the upper bound of our next downside target, where it should experience a bounce over the next few days.

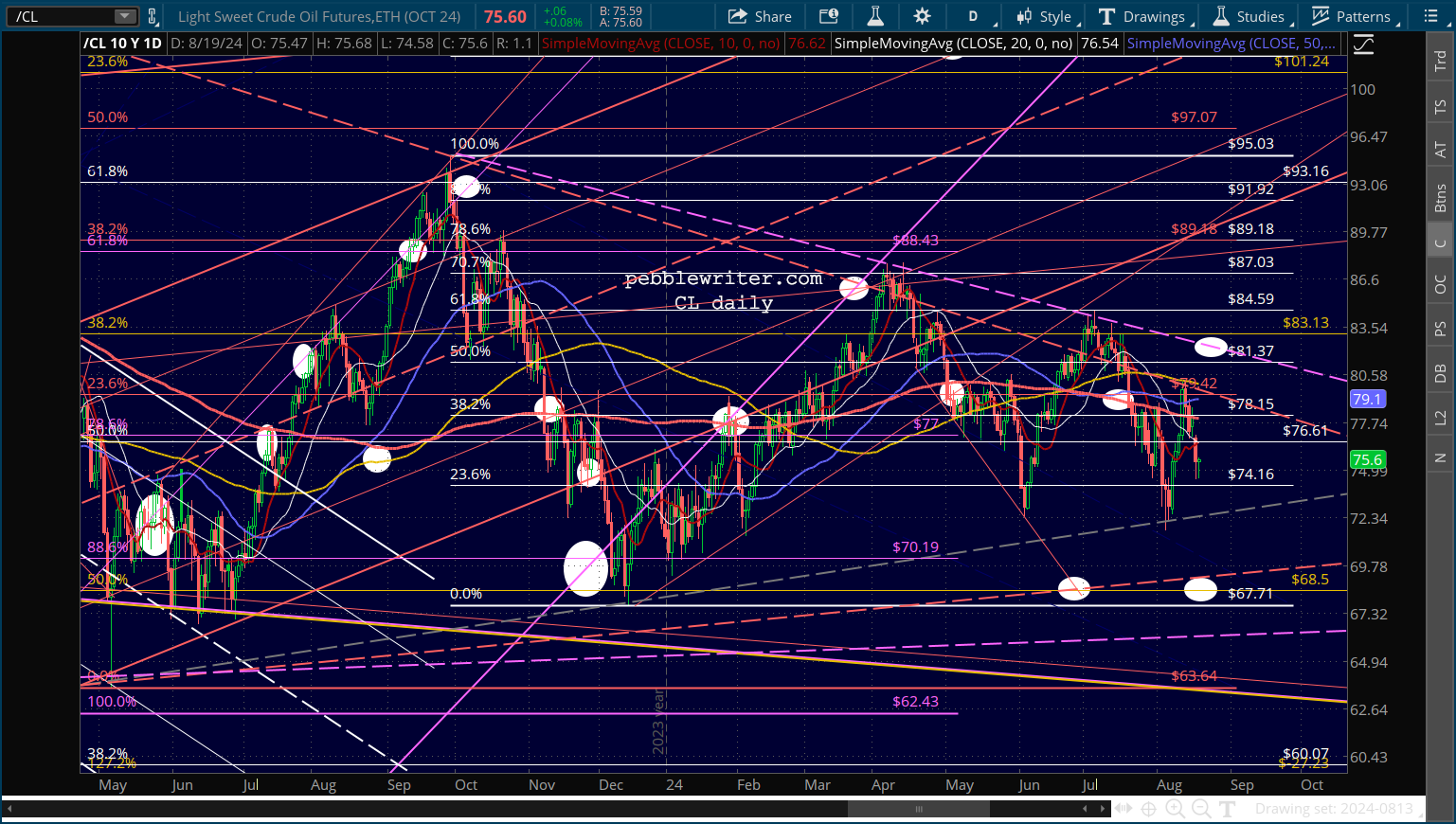

…and DXY has reached the upper bound of our next downside target, where it should experience a bounce over the next few days. Oil and gas are both slightly lower as the US continues its peacemaking efforts in the Middle East.

Oil and gas are both slightly lower as the US continues its peacemaking efforts in the Middle East.

The 10Y is flat, with the 2s10s sitting at -17 bps.

The 10Y is flat, with the 2s10s sitting at -17 bps.

Bottom line, the current narrative remains that the economy is heading for a soft landing with a gradually slowing economy that justifies a modest pattern of rate cuts. As long as nothing happens to disturb that narrative, stocks should continue toward our early November target of ES 5967.

Bottom line, the current narrative remains that the economy is heading for a soft landing with a gradually slowing economy that justifies a modest pattern of rate cuts. As long as nothing happens to disturb that narrative, stocks should continue toward our early November target of ES 5967.

Oil and gas markets remain a huge unknown which could greatly disturb that narrative. As we’ve discussed many times, our model shows CPI rising again in October/November. A substantial rise prior to that would mean no rate cuts and lower stock prices.

Stay tuned…