Watching the market over the past few weeks reminds me of the Foreigner classic Feels Like the First Time:

It feels like the first time

Like it never did before

Feels like the first time

Like we’ve opened up the door

Feels like the first time

Like it never will again, never again

In this case, the torrid love affair is between algorithms and the things that make them feel all tingly “down there.” As in the song, it’s not the first time…not even close.

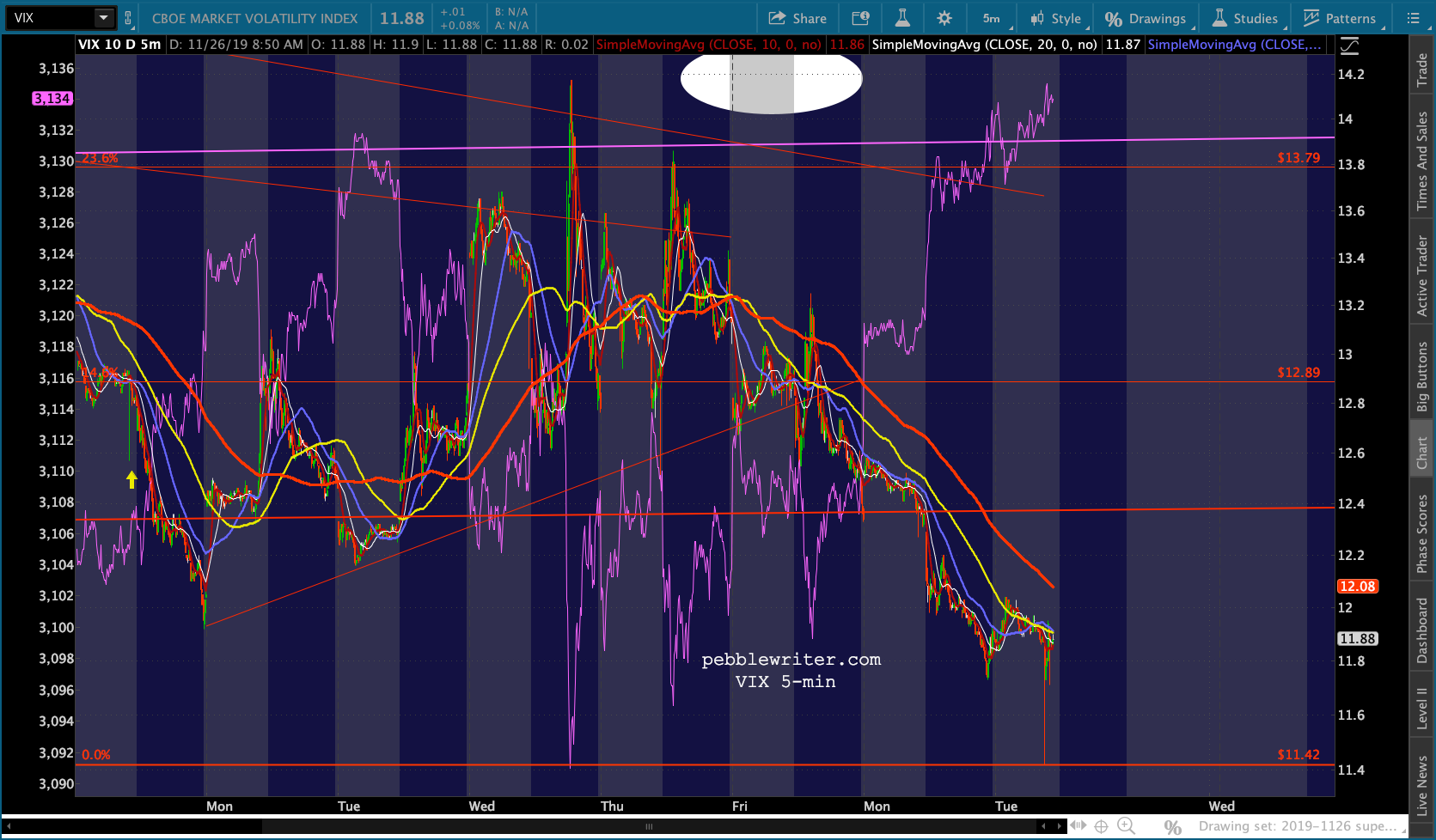

Algos love it when VIX breaks down. The logic is clear: fear must be subsiding for a reason, so buy-buy-buy! And, boy, has it subsided.

It’s not the actual levels to which VIX drops that excites the algos – it’s the trend changes and broken support. SPX made new highs in April because the purple trend line from Nov 2017 broke down. It made higher highs in July because VIX broke down again, pushing below the TL over and over again.

It’s not the actual levels to which VIX drops that excites the algos – it’s the trend changes and broken support. SPX made new highs in April because the purple trend line from Nov 2017 broke down. It made higher highs in July because VIX broke down again, pushing below the TL over and over again.

Only this time, it reinforced the establishment of a new trend line (shown in red.) Because that trend line is also now breaking down, algos are bidding stocks up to new higher highs. Imagine what would happen to stocks if VIX were hammered below 11.03, 10.17 or Nov 2017’s 8.56.

The algos could care less that the tail is wagging the dog. All they know is the tail is wagging.

Likewise, USDJPY keeps whispering sweet nothings to algos. In this case, it’s the 200-day moving average producing all the oohs and aahs. USDJPY first soared back above it on Oct 14 in the wake of the exciting (not) Phase One trade announcement.

Likewise, USDJPY keeps whispering sweet nothings to algos. In this case, it’s the 200-day moving average producing all the oohs and aahs. USDJPY first soared back above it on Oct 14 in the wake of the exciting (not) Phase One trade announcement.

It so titillated the algos that it keeps going back to the well over and over again — just like those trade updates from the White House. One wonders whether it might go blind. Oil futures, the algos’ Desdemona, have adopted a similar technique, popping up above their 200-DMA all but one session since Nov 4. If they looked closely, the algos might realize CL is resetting most nights and, like USDJPY, hasn’t made any actual progress. Ah, but what is love if not blind?

Oil futures, the algos’ Desdemona, have adopted a similar technique, popping up above their 200-DMA all but one session since Nov 4. If they looked closely, the algos might realize CL is resetting most nights and, like USDJPY, hasn’t made any actual progress. Ah, but what is love if not blind? continued for members…

continued for members…

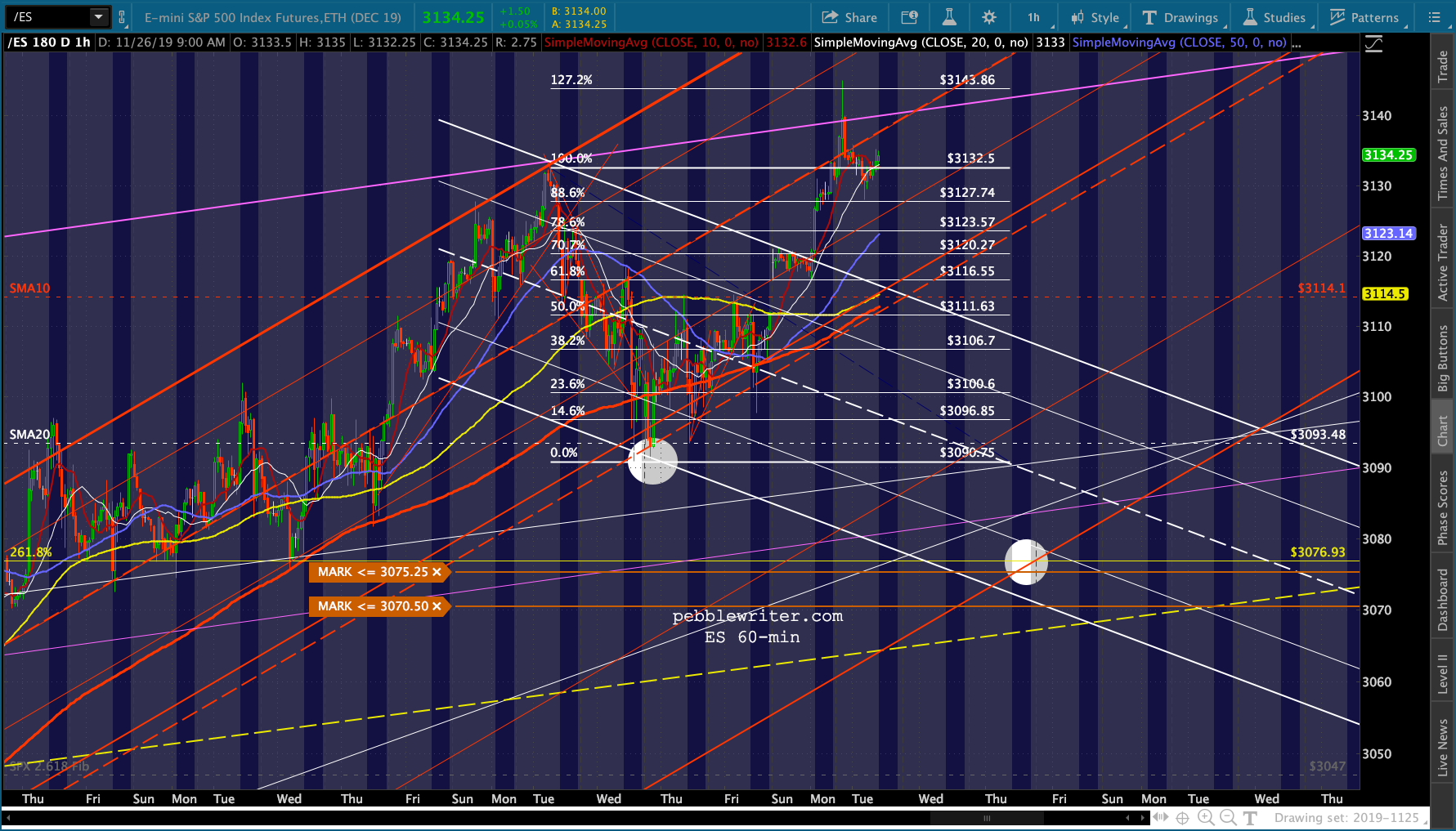

ES tested the purple channel top all over again last night. Again, it was rebuffed — but is holding last week’s highs. If you’re wondering how long this can go on, the answer is indefinitely. I suspect oil and gas will come under pressure after the Aramco IPO is done – lest inflation become an inconvient truth for Powell et al. RB remains my very favorite short.

If you’re wondering how long this can go on, the answer is indefinitely. I suspect oil and gas will come under pressure after the Aramco IPO is done – lest inflation become an inconvient truth for Powell et al. RB remains my very favorite short. But, VIX could continue to get hammered just enough every day to keep stocks on the rise. And, there is no actual limit to the heights to which USDJPY could ramp as long as the BoJ is willing to pay the price in increased (well, less decreased) interest rates.

But, VIX could continue to get hammered just enough every day to keep stocks on the rise. And, there is no actual limit to the heights to which USDJPY could ramp as long as the BoJ is willing to pay the price in increased (well, less decreased) interest rates. As with ES, SPX is tagging a rising channel top again. Having broken out of the rising purple channel, it is now working on the rising white channel (with the smaller red channel inlaid.) Yes, it’s resistance. But, it’s rising every day. So, it’s difficult to say when it will end.

As with ES, SPX is tagging a rising channel top again. Having broken out of the rising purple channel, it is now working on the rising white channel (with the smaller red channel inlaid.) Yes, it’s resistance. But, it’s rising every day. So, it’s difficult to say when it will end.

The test will come around Dec 4-5, when Aramco is put to bed and oil and gas can come back to Earth. Will TPTB get that much more serious about crushing VIX and ramping USDJPY? Probably. Will it be enough? Hard to say.

As we’ve discussed several times, the potential hitch in all these plans is inflation. Unless RB plunges in the next five minutes, November CPI will be elevated. It will be reported on Dec 11, same day the next FOMC meeting ends.

The last time RB tarried in the same range as in 2018 was in April. Gas prices were slightly higher YoY, yielding headline CPI of 2.00%. Although it was a substantial increase from Jan’s 1.55%, Feb’s 1.52% and Mar’s 1.86%, the Fed declared it not a problem, saying in their statement ““market-based measures of inflation compensation have remained low in recent months” and pointing out that “on a 12-month basis, overall inflation and inflation for items other than food and energy have declined and are running below 2 percent.”

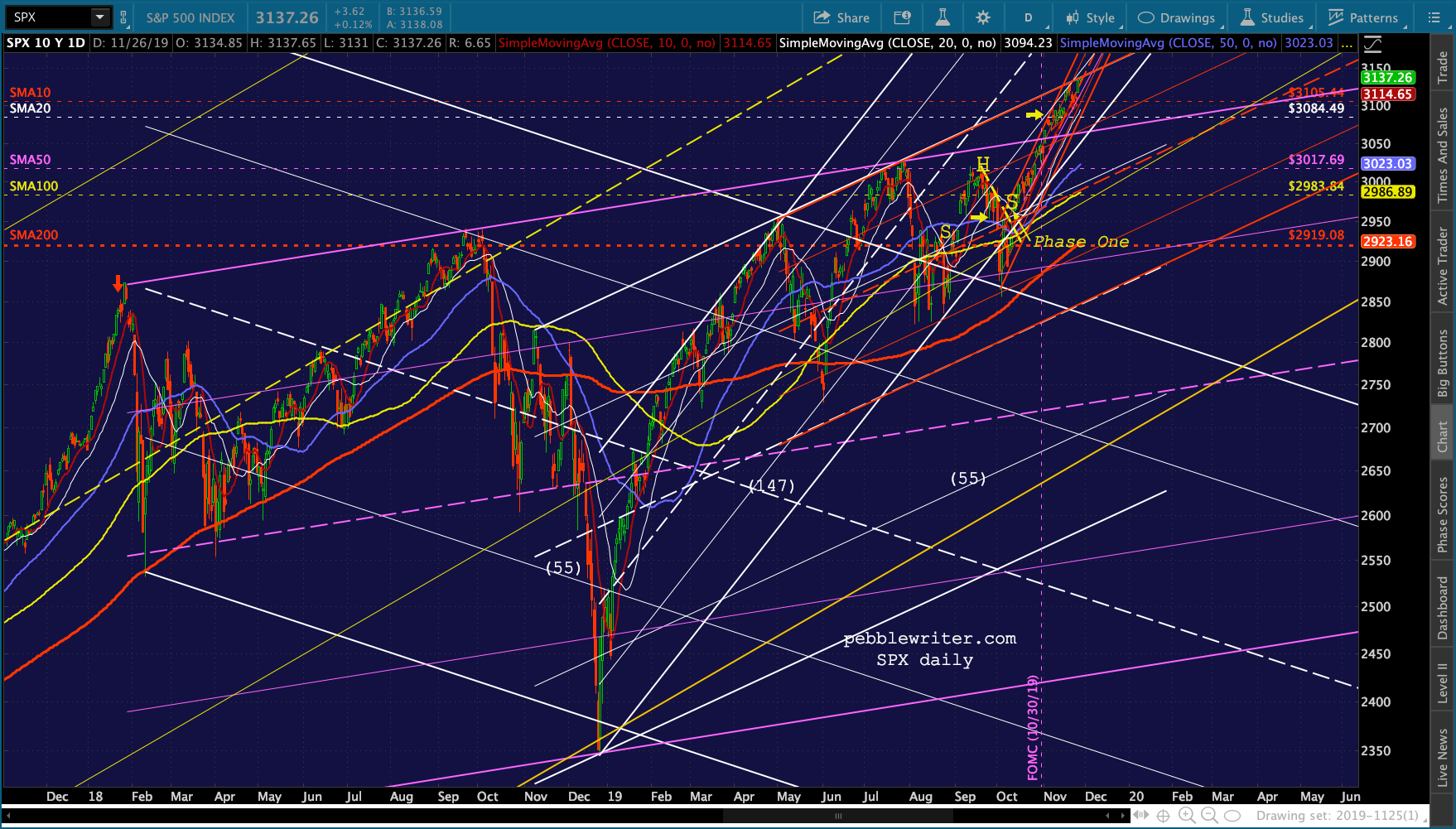

SPX had made new all-time highs that day (the yellow arrow) but plunged 7.6% over the next month – falling and even closing below its SMA200.

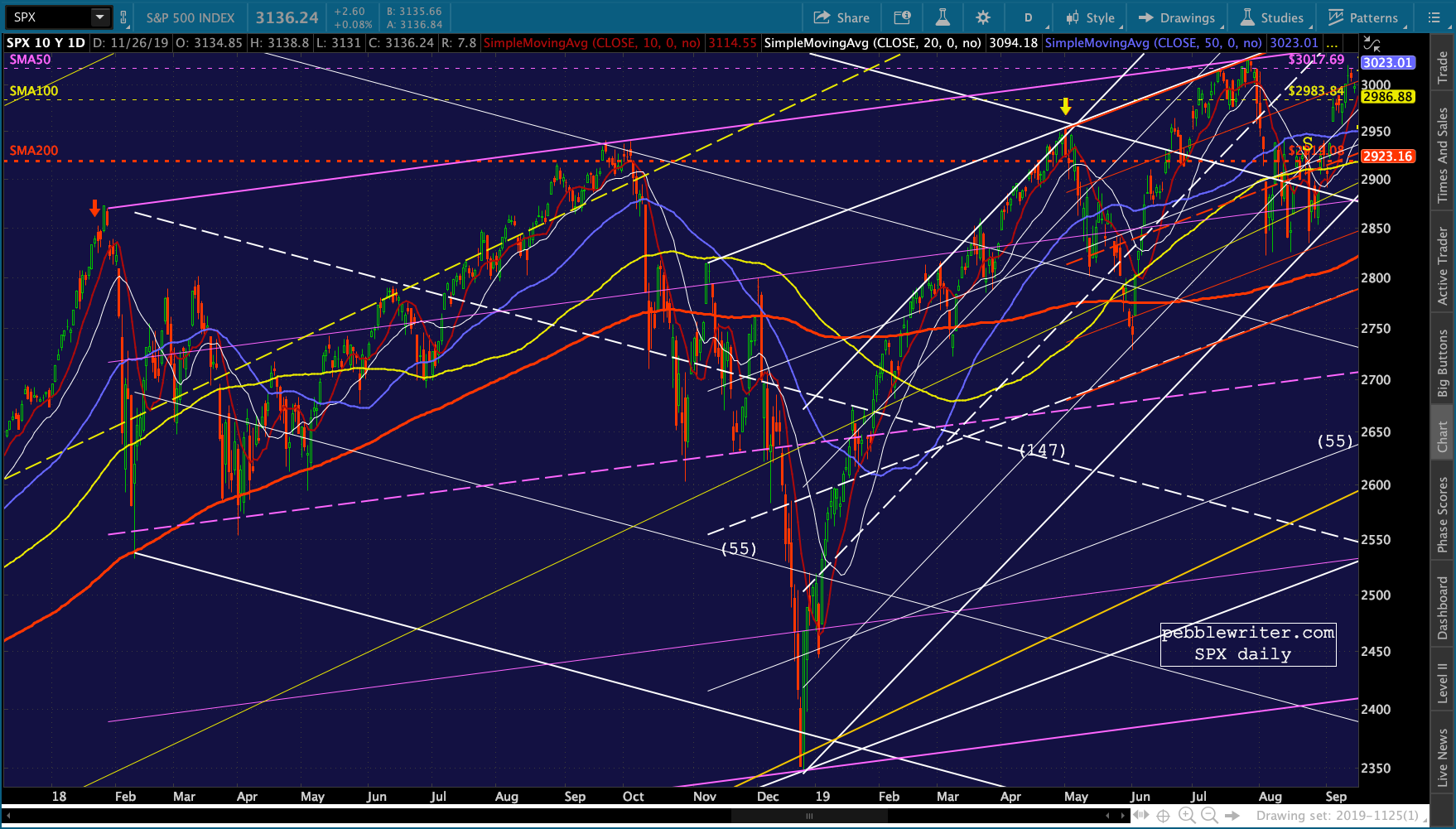

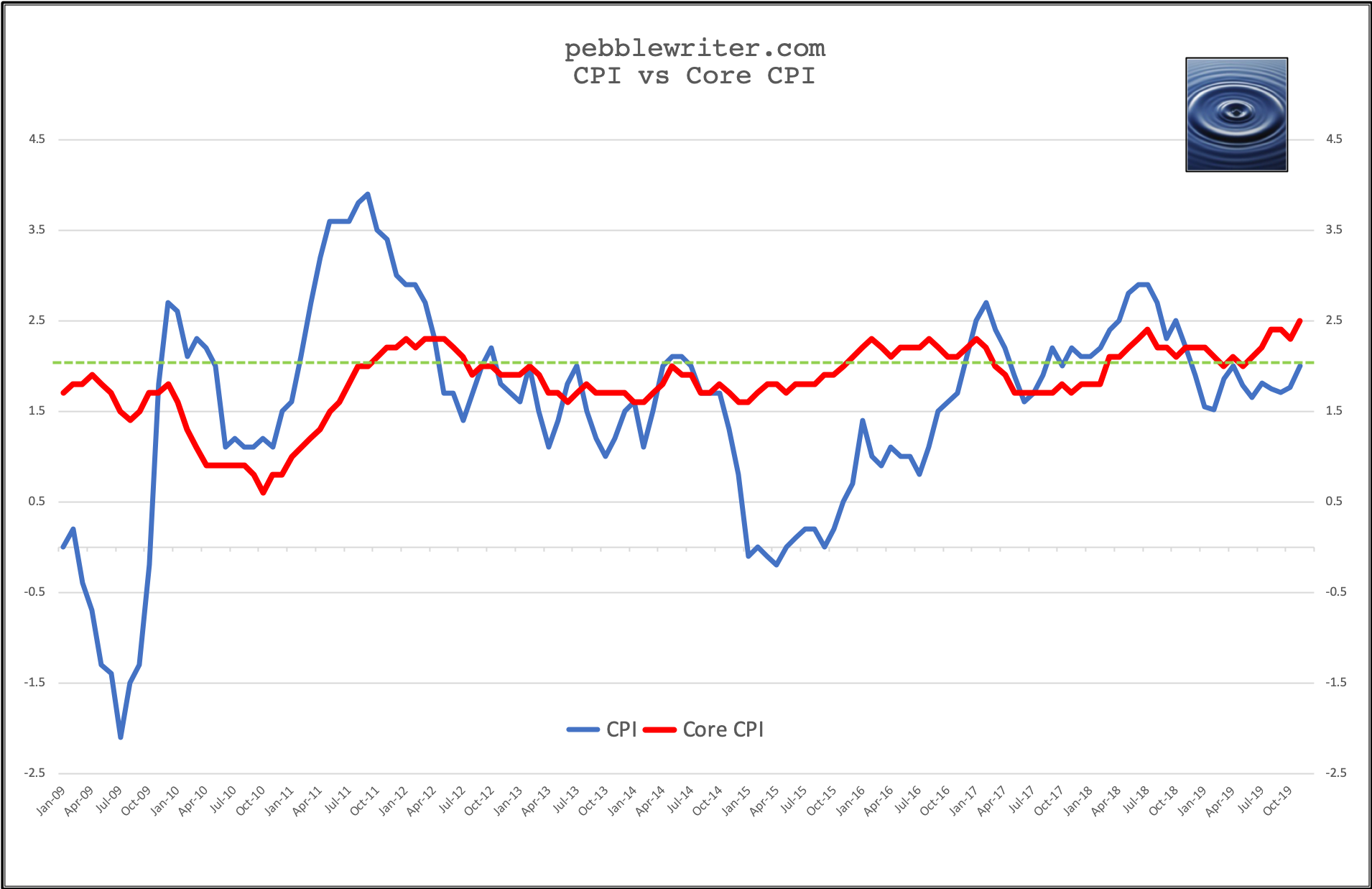

As we’ve discussed many times, Core CPI has exceeded headline CPI every month since December 2018 — the month the last cross occurred. Recall that CPI had recently broken down below a trend line dating back to Sep 2015 after peaking in Sep 2018.  It’s no coincidence that CL and TNX both topped out in Oct 2018. Recall that it was out of necessity as 10Y rates had climbed to 3.25%.

It’s no coincidence that CL and TNX both topped out in Oct 2018. Recall that it was out of necessity as 10Y rates had climbed to 3.25%. Rates are obviously nowhere near that high now. But, it’s worth noting that stocks experienced period of weakness whenever: (1) CPI peaked and turned downward; (2) CPI dropped below Core CPI; and (3) Core CPI rose above 2%. It’s also worth noting that unless oil/gas prices plunge right away, Core CPI could rise above 2.5% for the first time since Sep 2008 — not exactly conditions which are conducive to accommodative Fed policy.

Rates are obviously nowhere near that high now. But, it’s worth noting that stocks experienced period of weakness whenever: (1) CPI peaked and turned downward; (2) CPI dropped below Core CPI; and (3) Core CPI rose above 2%. It’s also worth noting that unless oil/gas prices plunge right away, Core CPI could rise above 2.5% for the first time since Sep 2008 — not exactly conditions which are conducive to accommodative Fed policy.