The big day is finally here. Everybody’s arguing whether the FOMC will deliver a 25 or 50-bps cut. The real question: Will the market care?

continued for members…

continued for members…

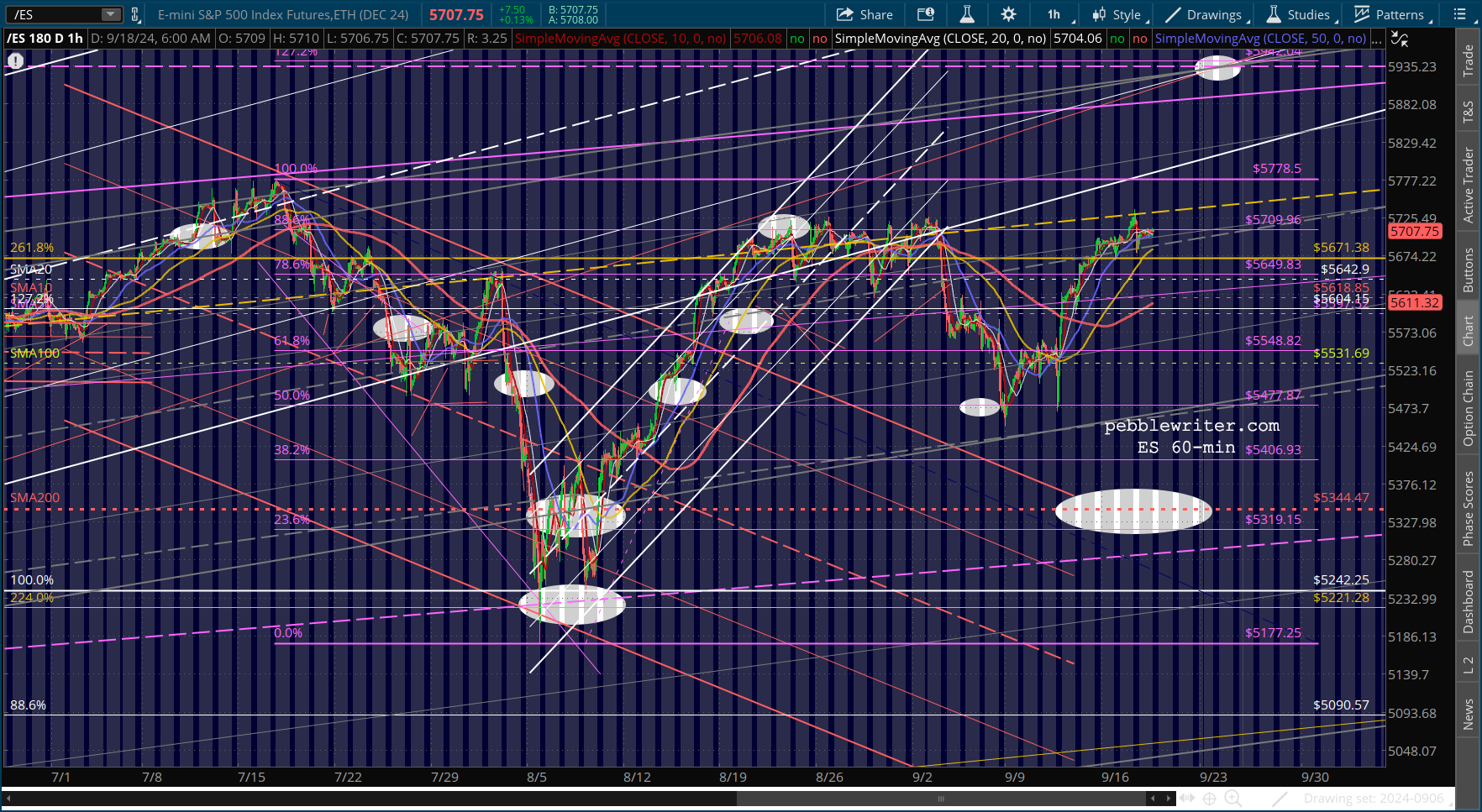

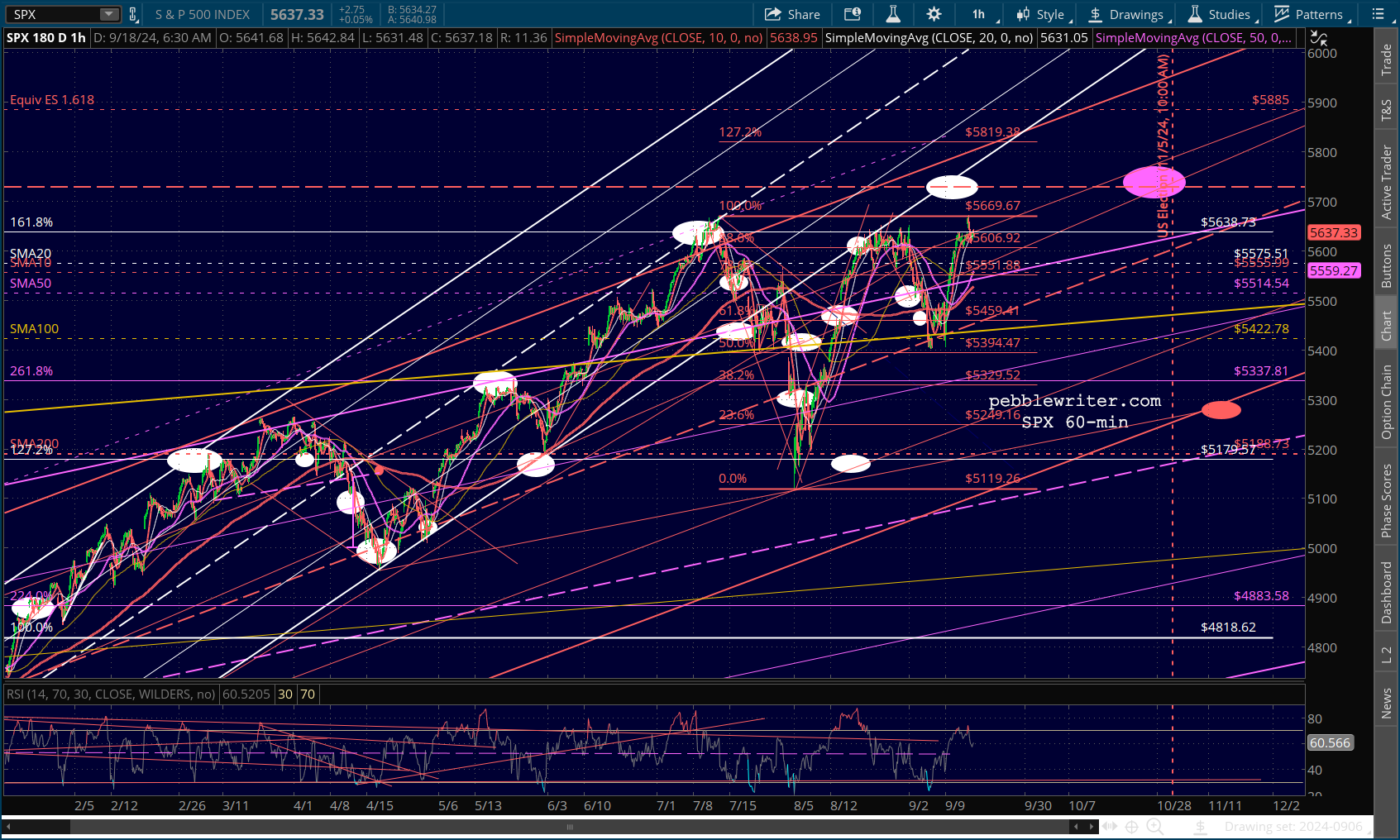

Note that SPX has not yet registered a new high, and the negative divergence is quite striking. With the IH&S target just 57 points above recent highs, it’s fair to ask whether a long position really makes sense for traders. Another way of looking at things is that gaining 57 points over a period of 7 weeks could absolutely involve a near-term pullback rather than a steady 2-pts per day increase.

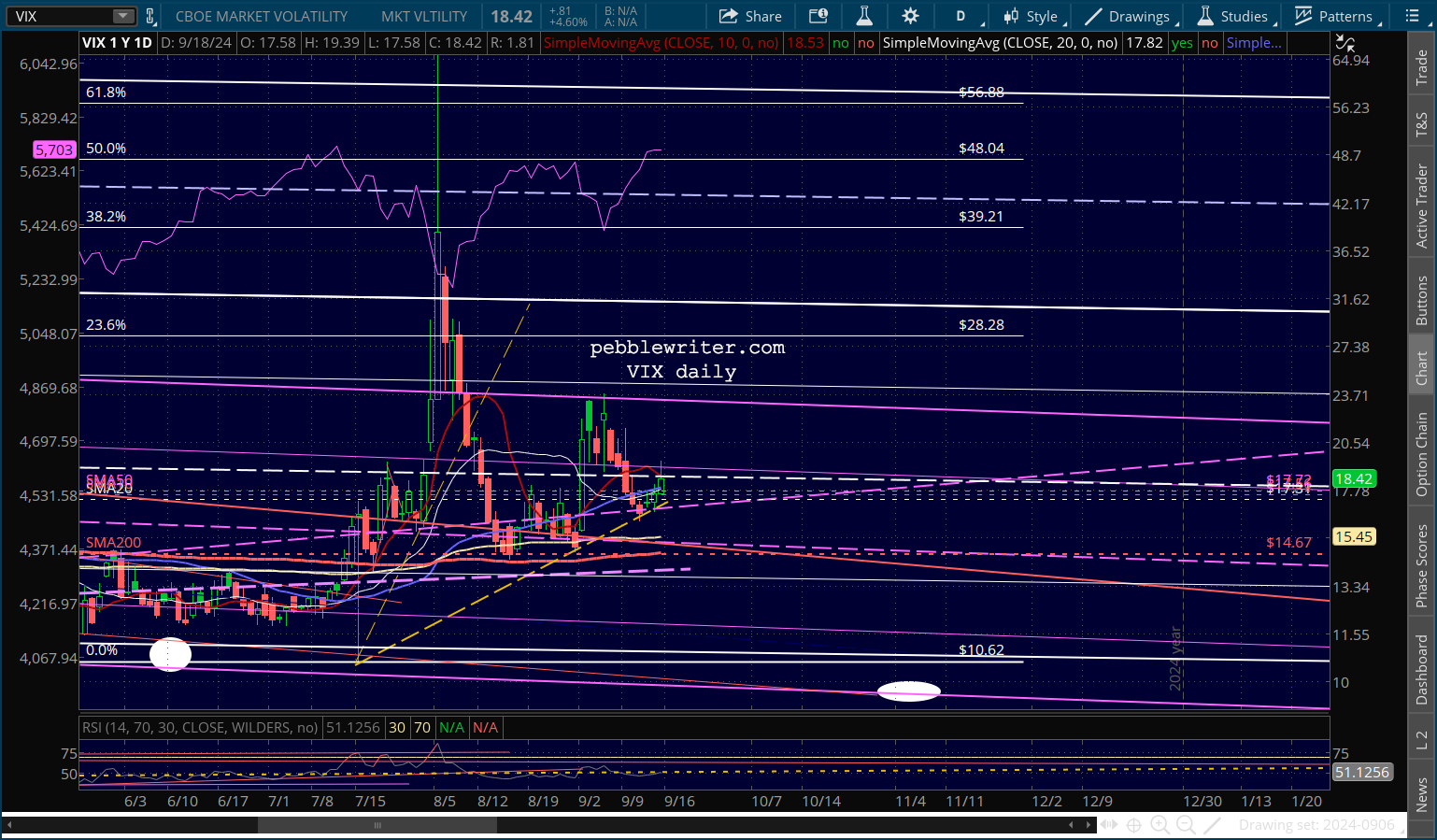

VIX has yet to break down again.

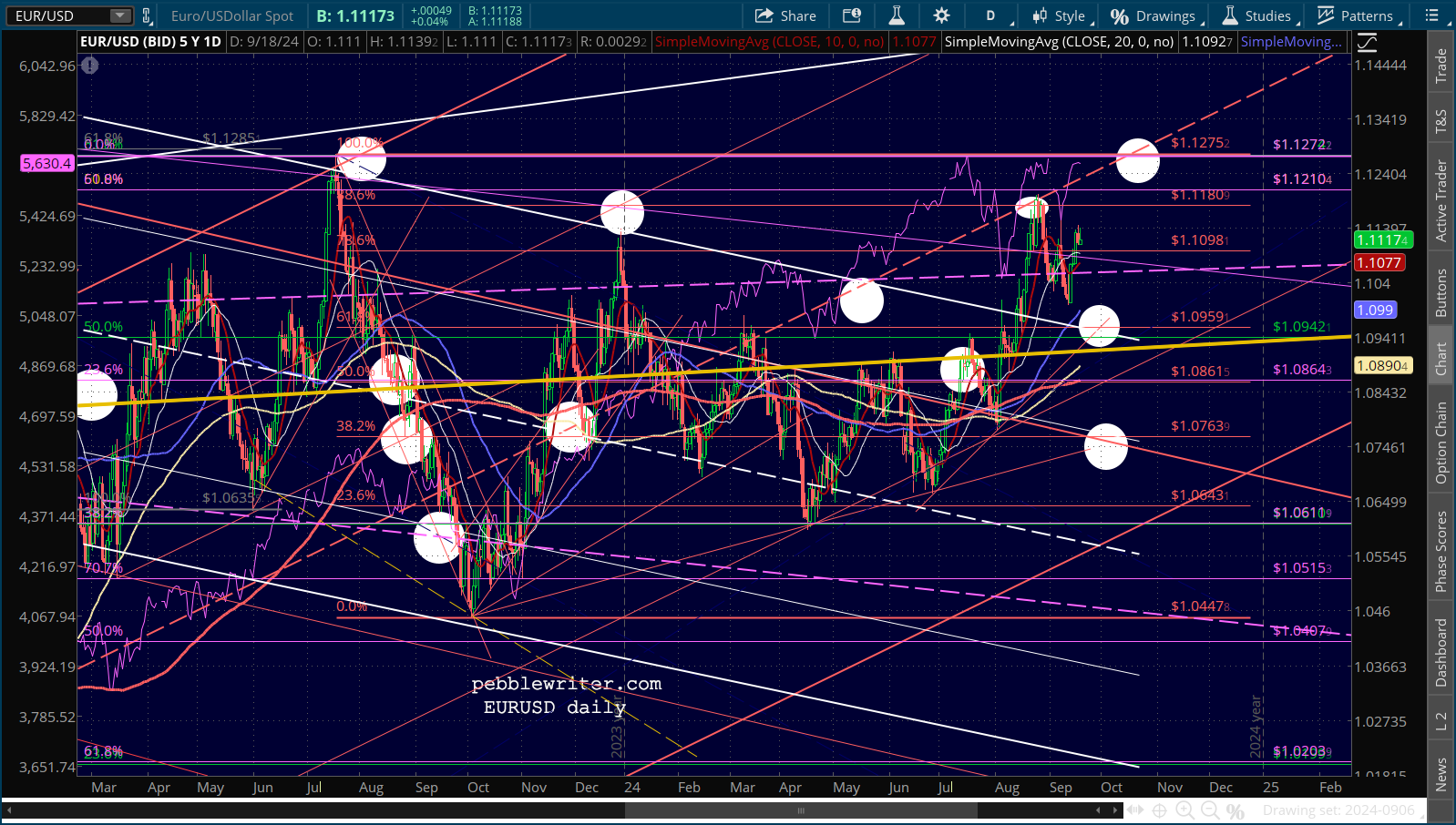

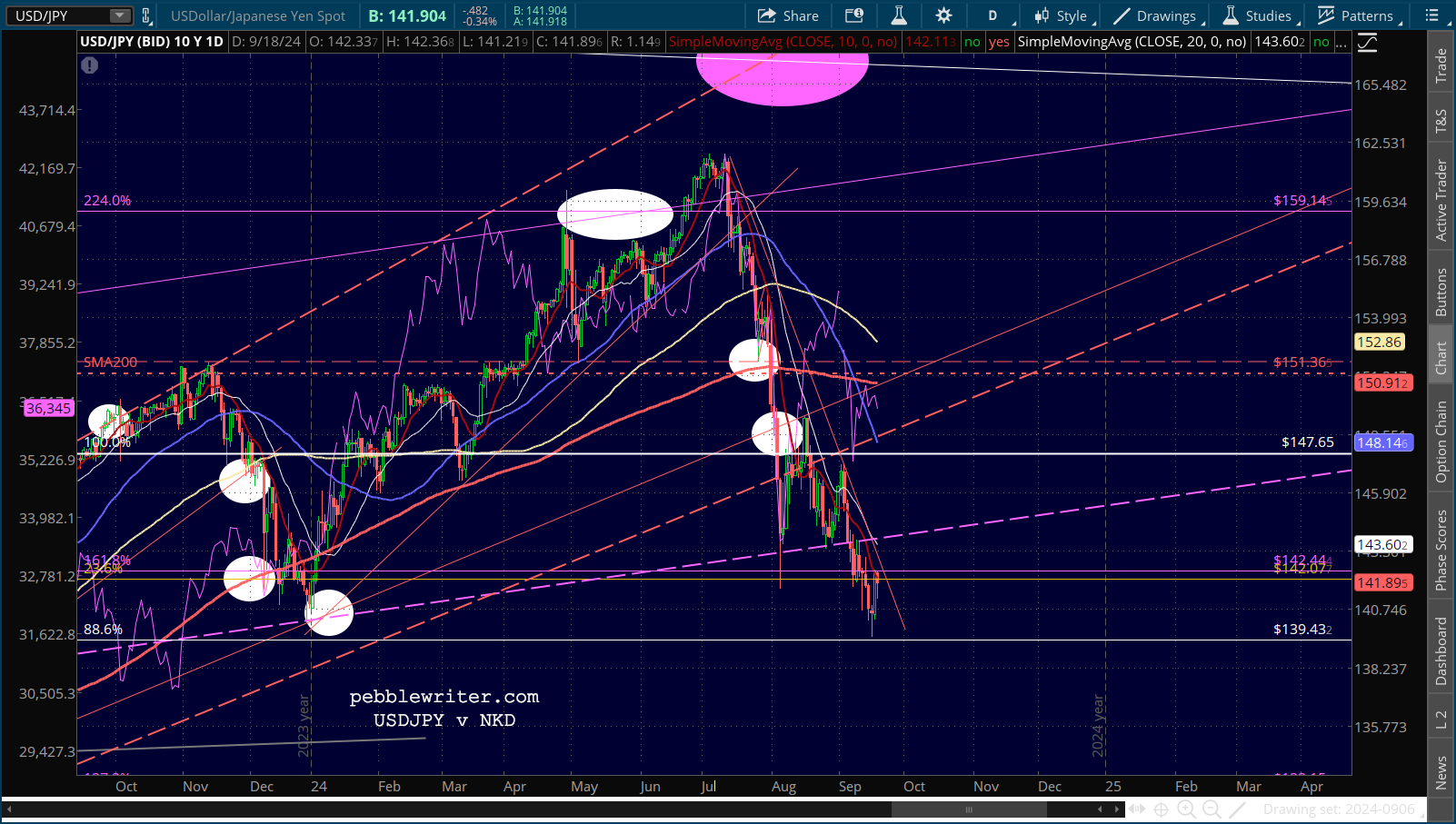

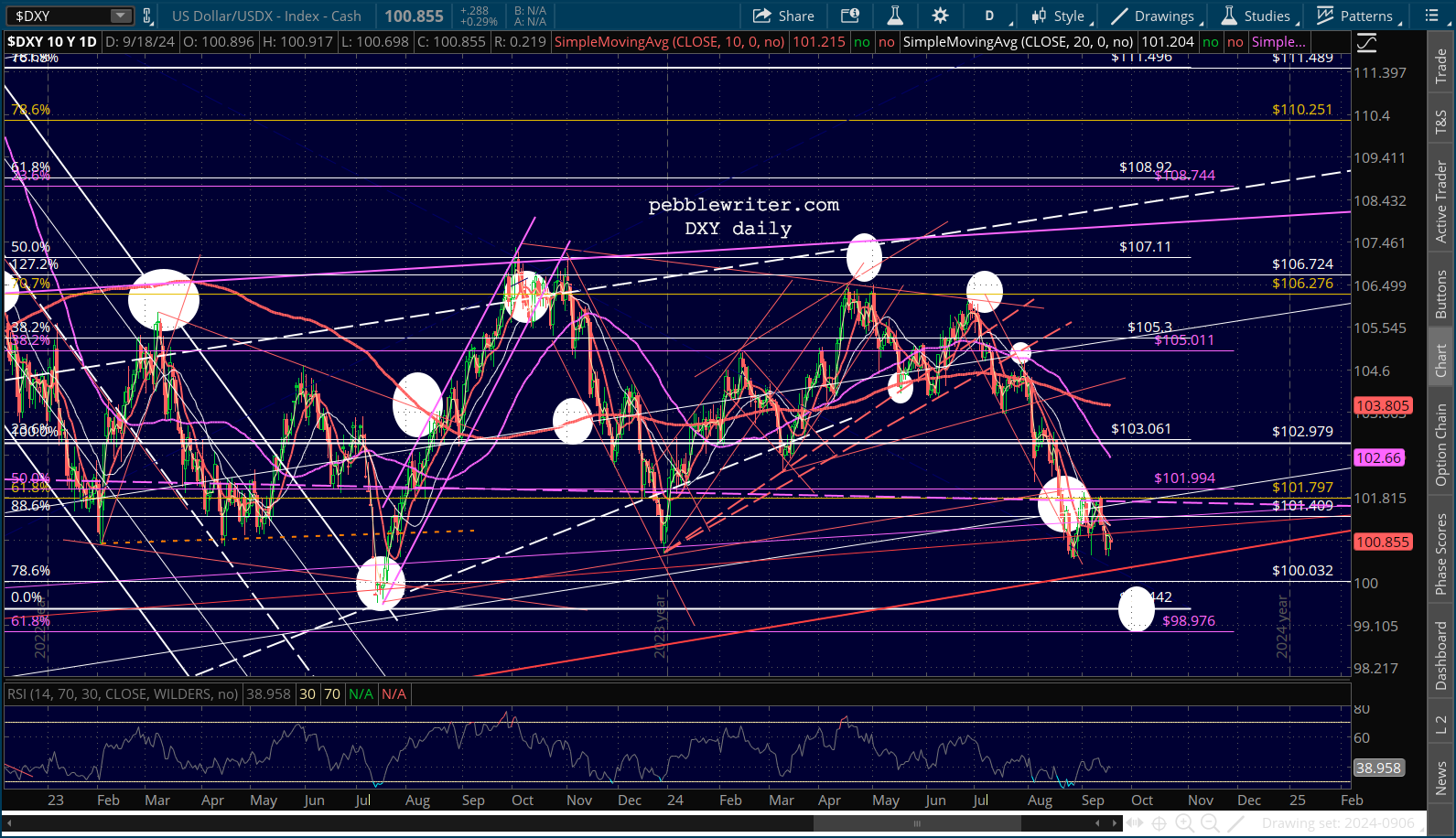

VIX has yet to break down again. And, the support from currencies is waning. Note that EURUSD has declined to push to new highs and, while USDJPY continues to falter, DXY is holding 100.

And, the support from currencies is waning. Note that EURUSD has declined to push to new highs and, while USDJPY continues to falter, DXY is holding 100.

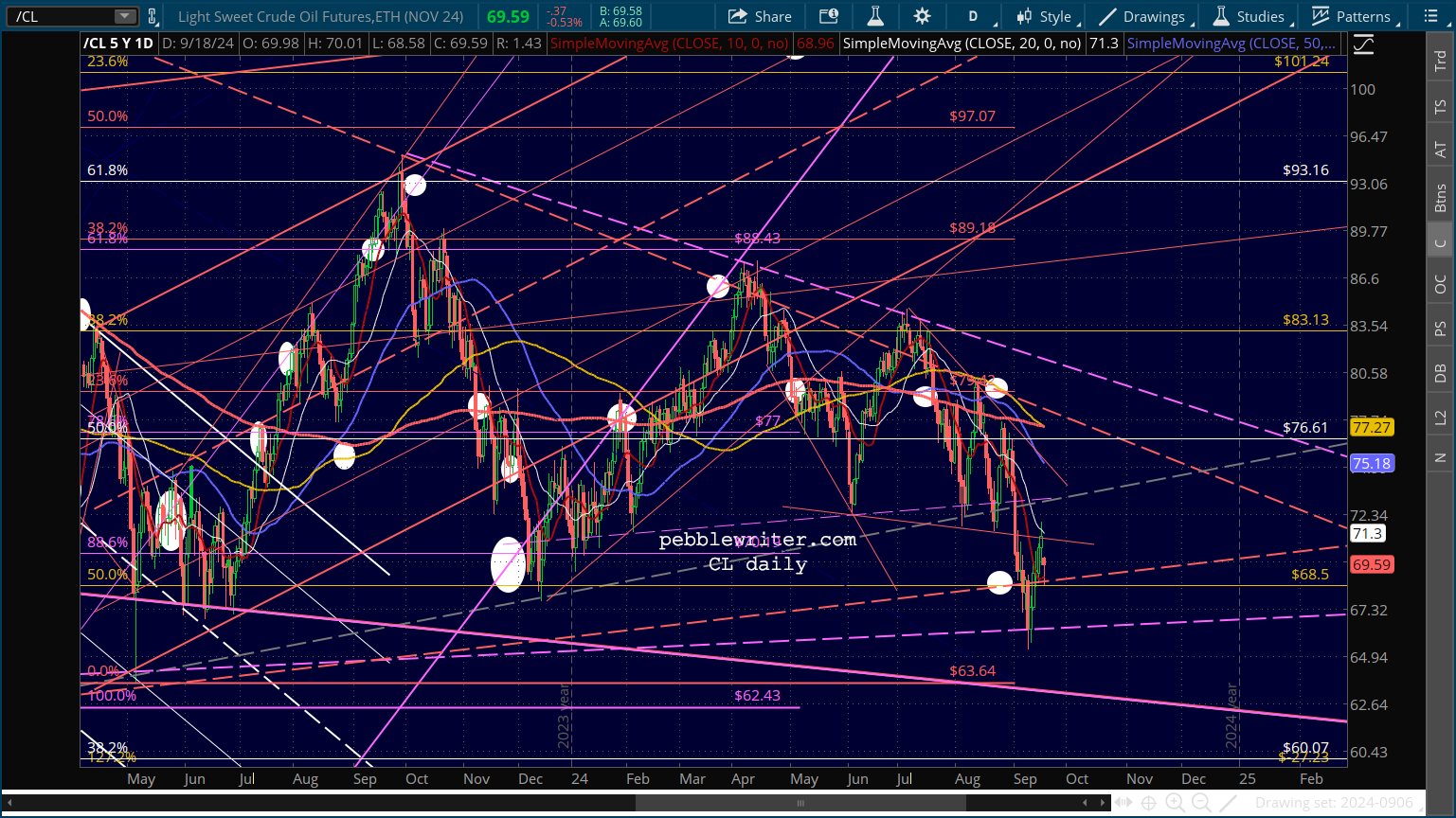

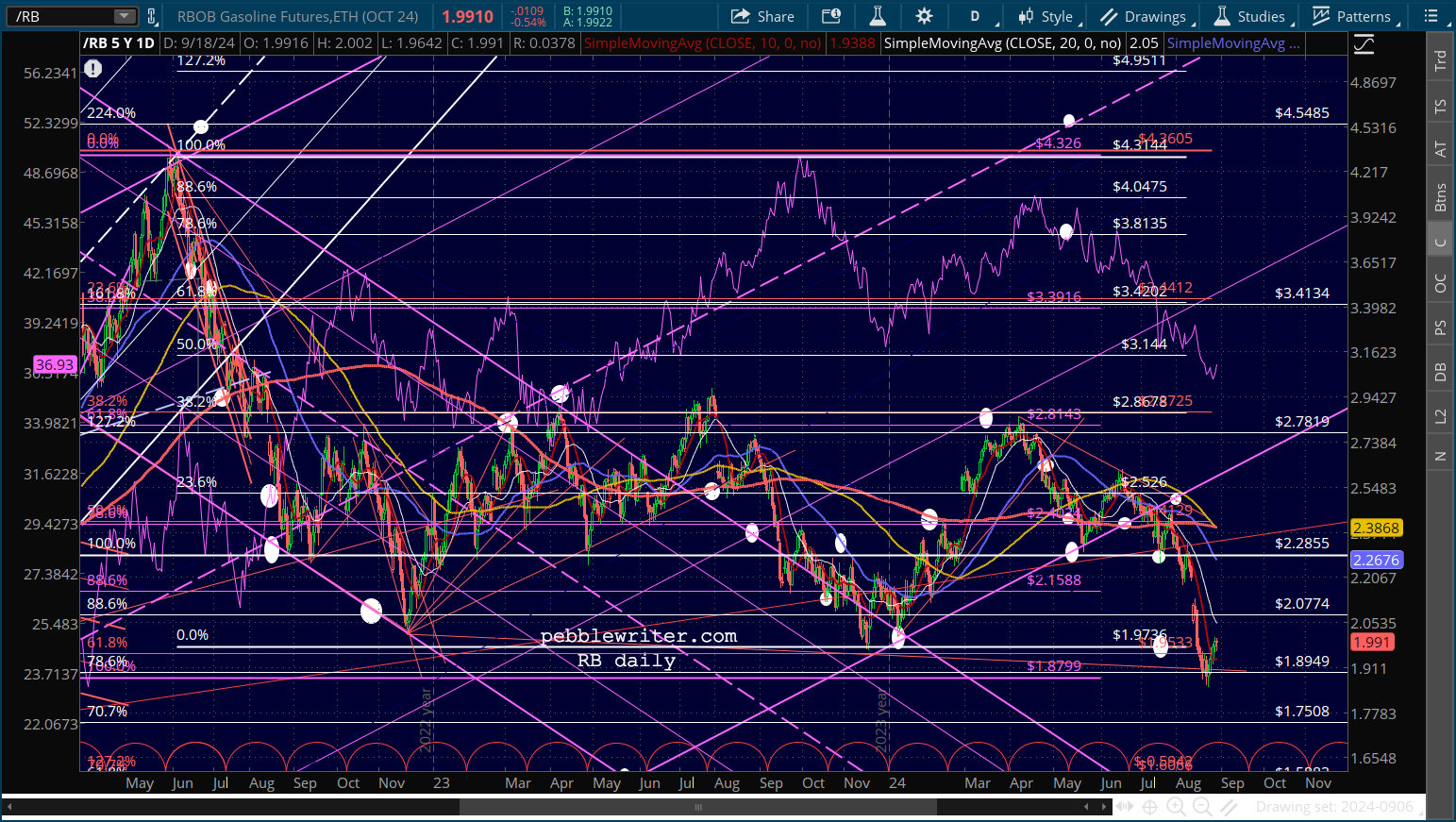

To further complicate things, oil and gas are still bouncing amidst more and more troubling developments in the Middle East. CL just cleared an internal TL of resistance, but has backed off this morning.

To further complicate things, oil and gas are still bouncing amidst more and more troubling developments in the Middle East. CL just cleared an internal TL of resistance, but has backed off this morning.

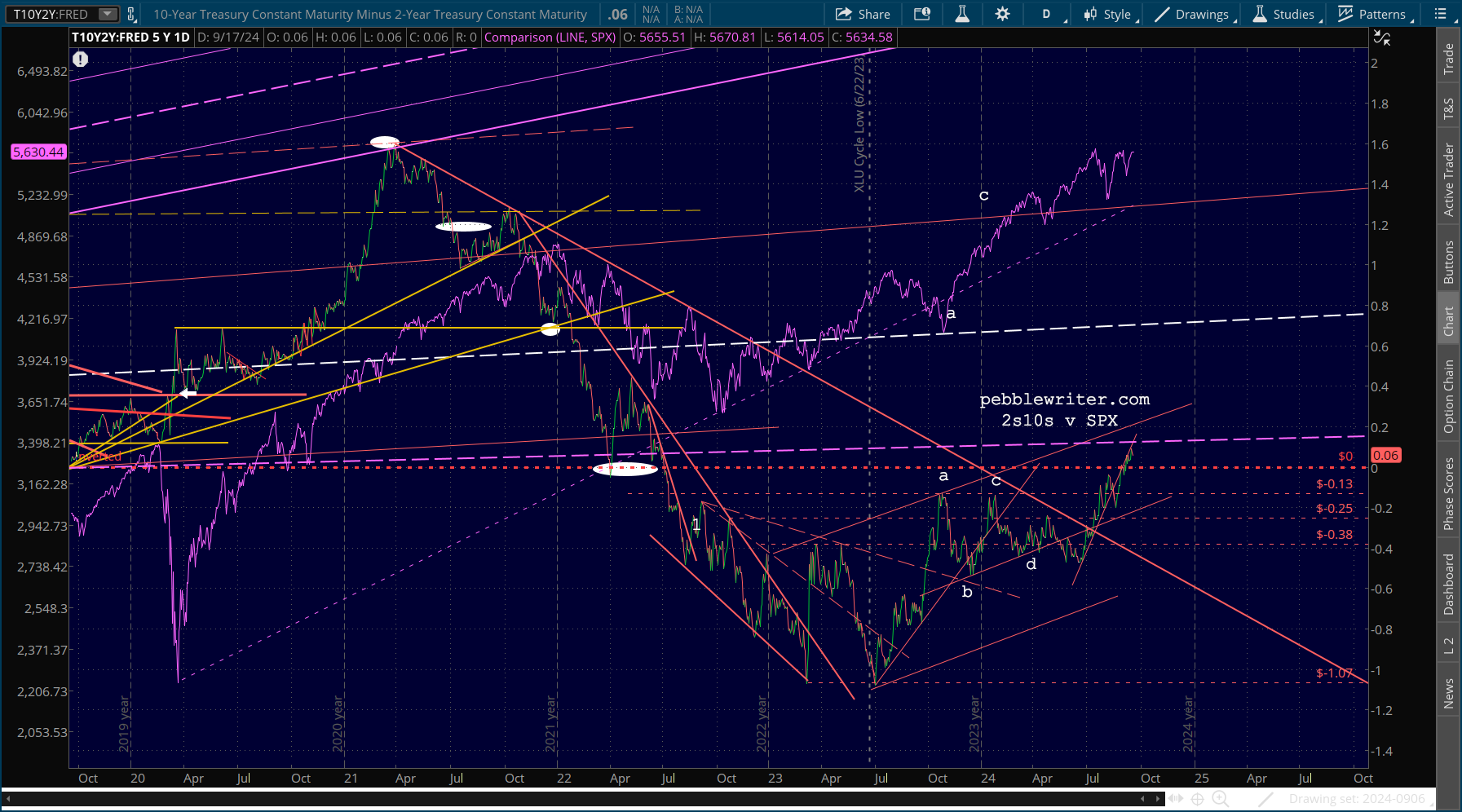

This is placing additional pressure on the 10Y, which is now 6 bps above the 2Y (on the way to 20 bps) as they disinvert.

This is placing additional pressure on the 10Y, which is now 6 bps above the 2Y (on the way to 20 bps) as they disinvert.

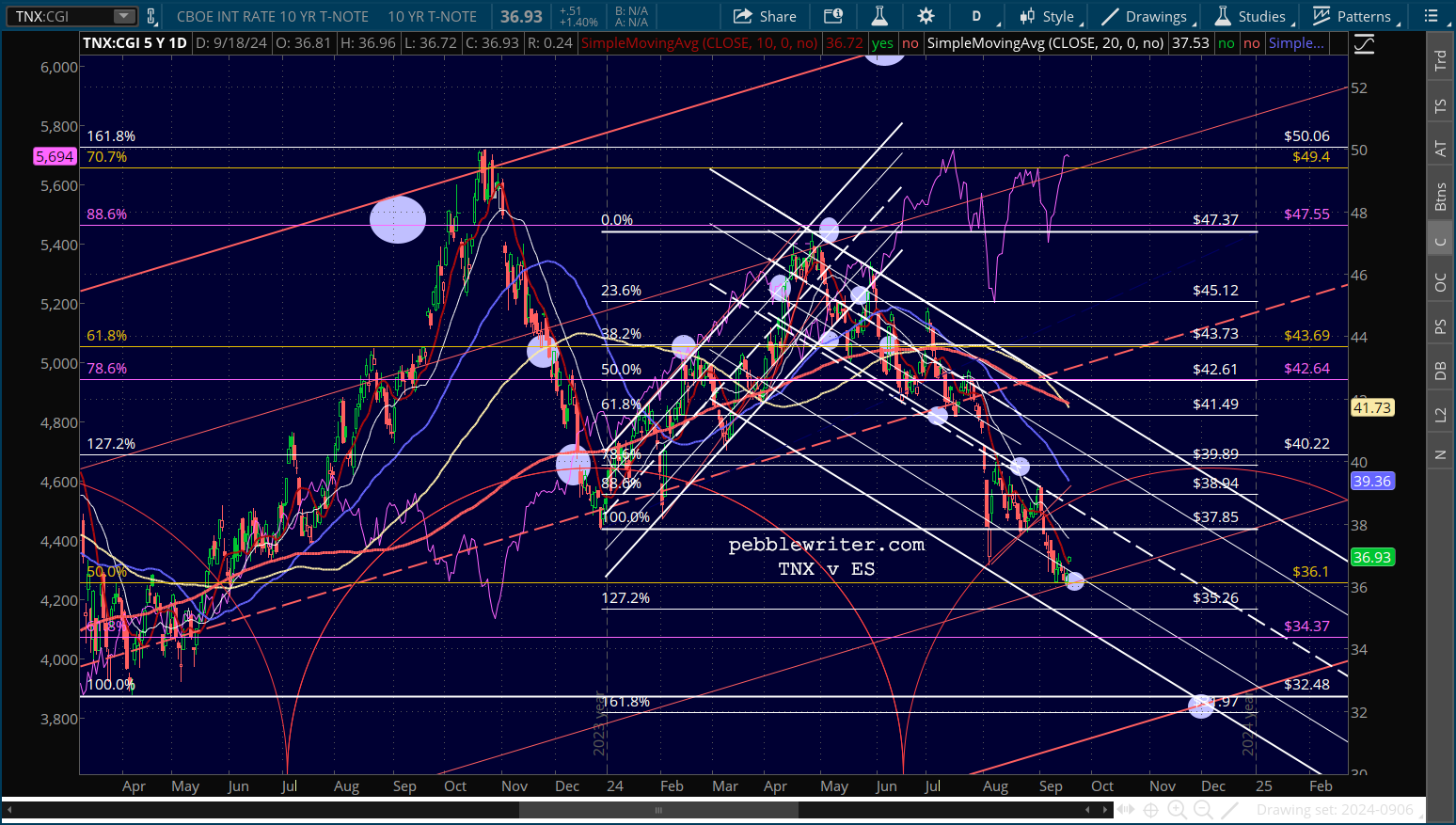

The charts suggest additional drops for the 10Y between now and the election. But, as we’ve discussed many times, rates can drop for a variety of reasons – including market meltdowns.

The charts suggest additional drops for the 10Y between now and the election. But, as we’ve discussed many times, rates can drop for a variety of reasons – including market meltdowns.  While I continue to expect the market to not melt down between now and then, there’s a better than even chance that stocks will have another 10% or greater hiccup after the election.

While I continue to expect the market to not melt down between now and then, there’s a better than even chance that stocks will have another 10% or greater hiccup after the election.

Note: We are having website issues this morning. Hope to get it straightened out this weekend.