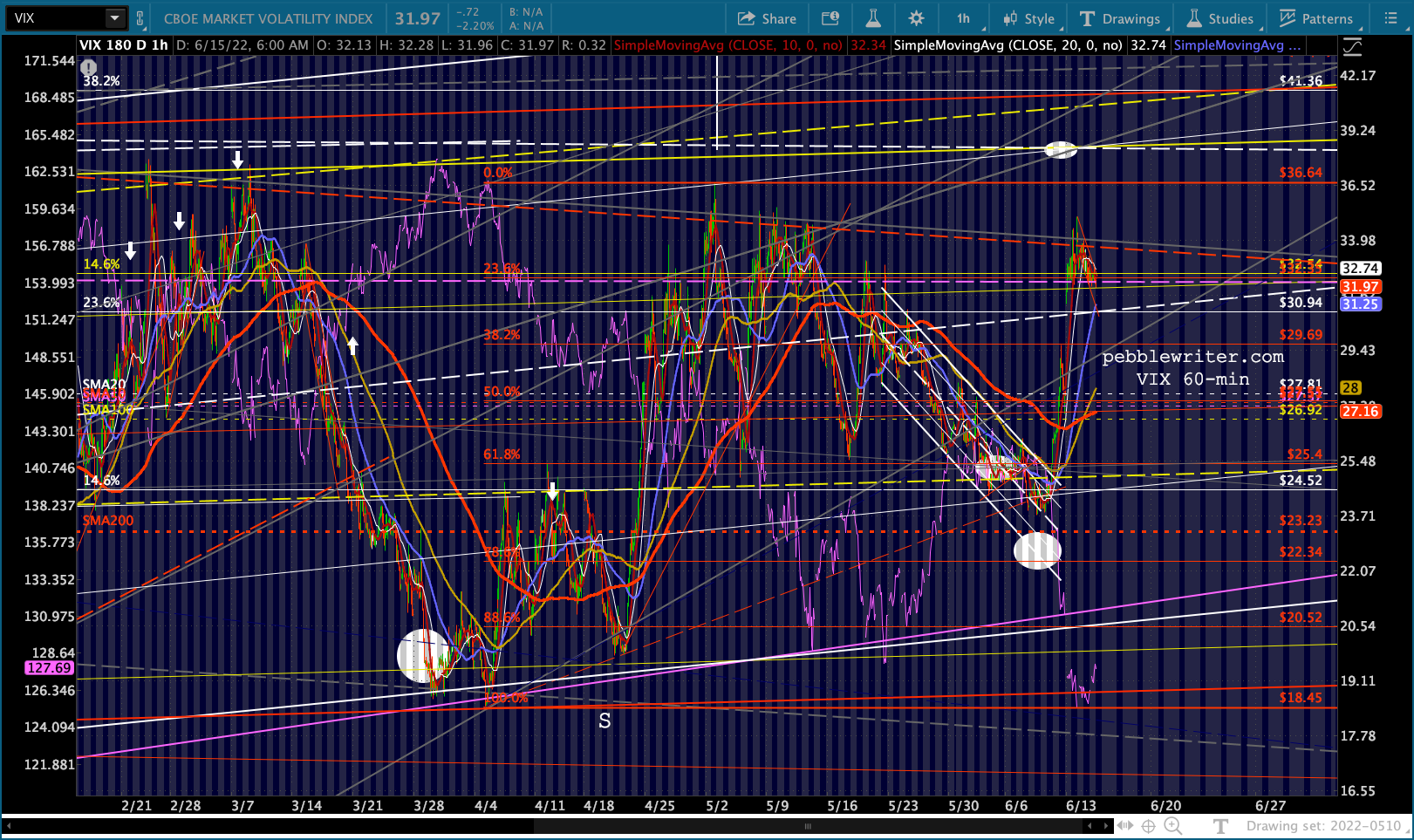

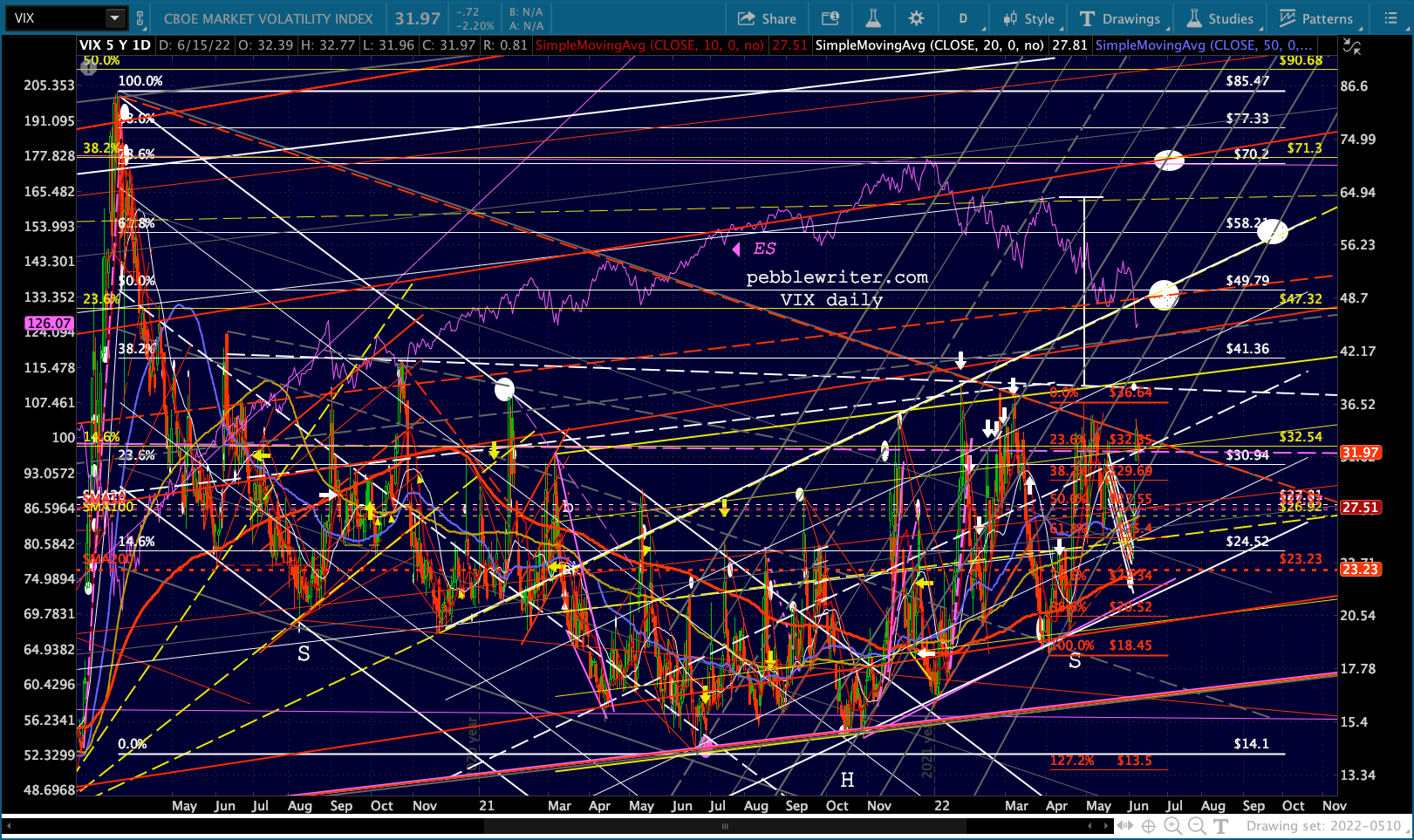

Algos have ramped almost 1% higher overnight on a modest but noticeable breakdown in VIX.

All eyes are on the FOMC which is expected to announce a rate hike of anywhere from 50-100 bps at 2PM ET. Bulls are still clinging to the prospect of a soft landing, while bears see dark economic storm clouds approaching.

All eyes are on the FOMC which is expected to announce a rate hike of anywhere from 50-100 bps at 2PM ET. Bulls are still clinging to the prospect of a soft landing, while bears see dark economic storm clouds approaching.

Given this morning’s disappointing retail sales data, which saw spending slump 0.3% MoM in May (-0.7% exclulding gasoline sales), it is increasingly difficult to ignore the notion that the Fed is tightening into an economic slowdown.

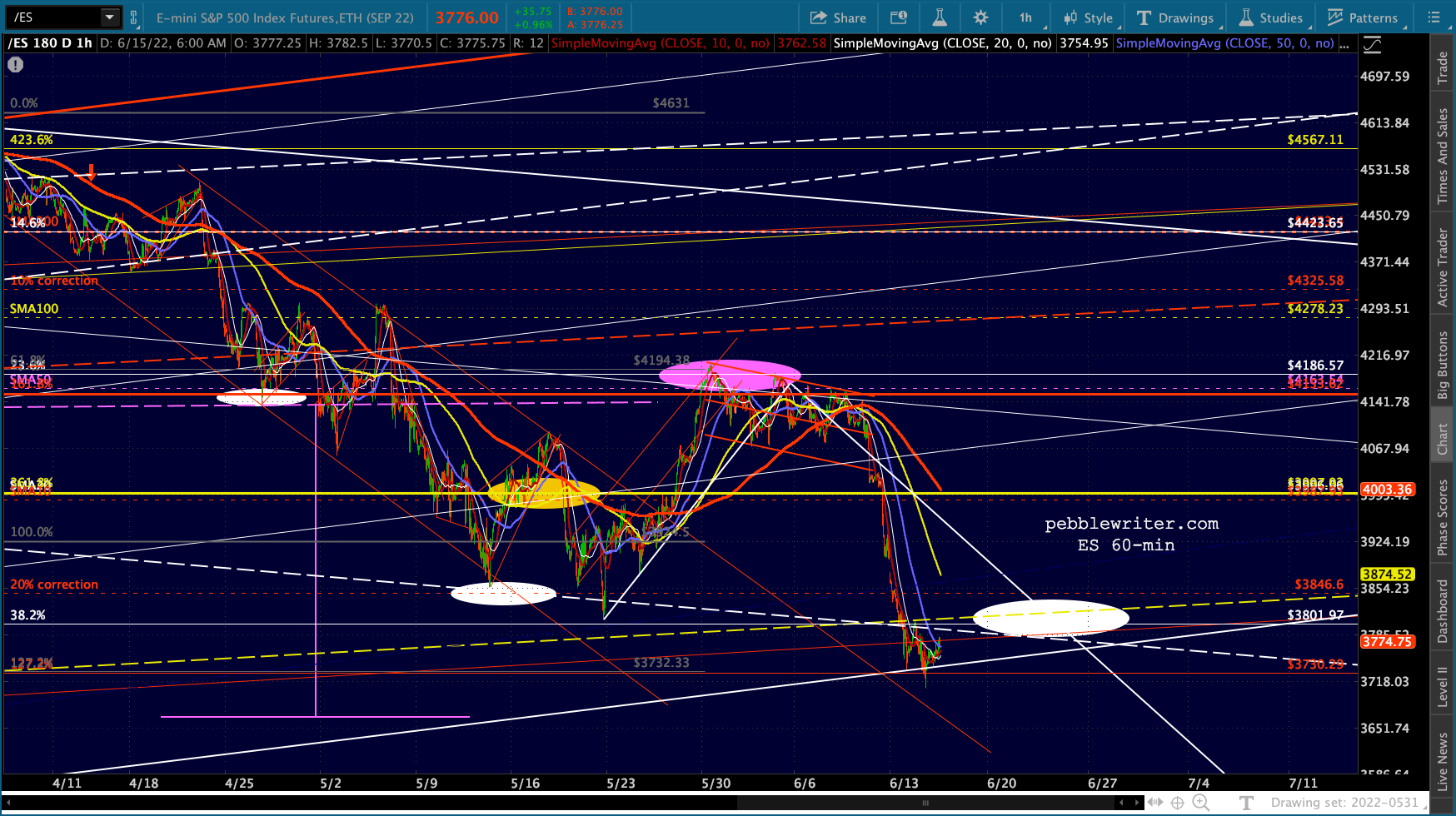

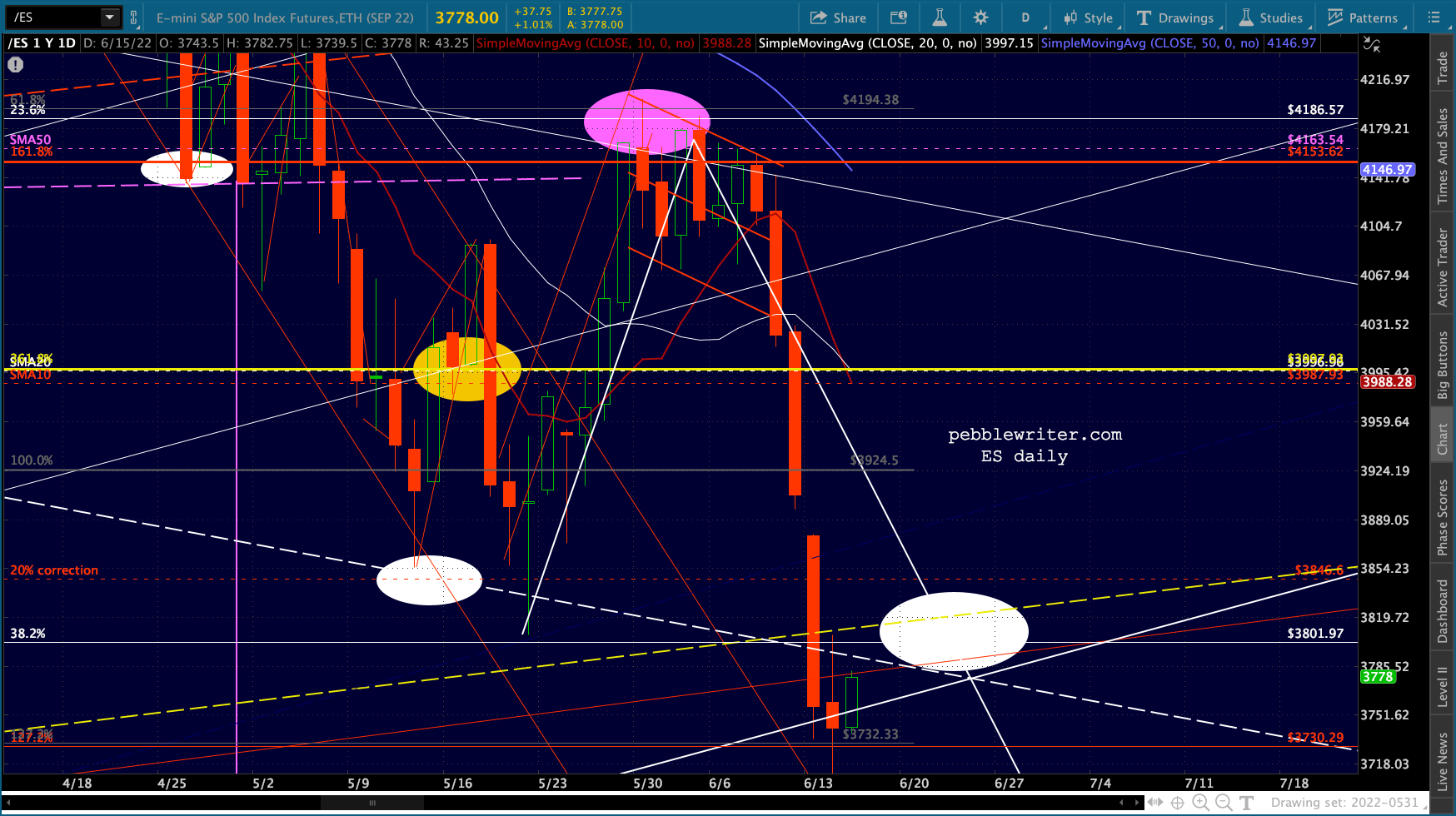

continued for members…At this point, ES is still backtesting the falling white channel midline (3793ish) and might easily push past it to the yellow midline (3812ish.)

Note that the SMA10 has slipped below the SMA20.

Note that the SMA10 has slipped below the SMA20. Ramping up equity prices in the lead up to a Fed meeting is common – especially when a negative market reaction is expected. It is most easily accomplished these days by hammering VIX. Once again, the fan line off the 2020 highs has held – at least for now – and the SMA10 has yet to push past the SMA20.

Ramping up equity prices in the lead up to a Fed meeting is common – especially when a negative market reaction is expected. It is most easily accomplished these days by hammering VIX. Once again, the fan line off the 2020 highs has held – at least for now – and the SMA10 has yet to push past the SMA20.

The Fed might be raising rates, but they are not interested in a market collapse. If our analog suggests anything, it’s that the Fed desires a significant but orderly decline that sees commodity prices and interest rates decline and the dollar rally.

The Fed might be raising rates, but they are not interested in a market collapse. If our analog suggests anything, it’s that the Fed desires a significant but orderly decline that sees commodity prices and interest rates decline and the dollar rally.

US companies which rely on sales outside the US will be hurt, but the price of imports – including oil – should decline.

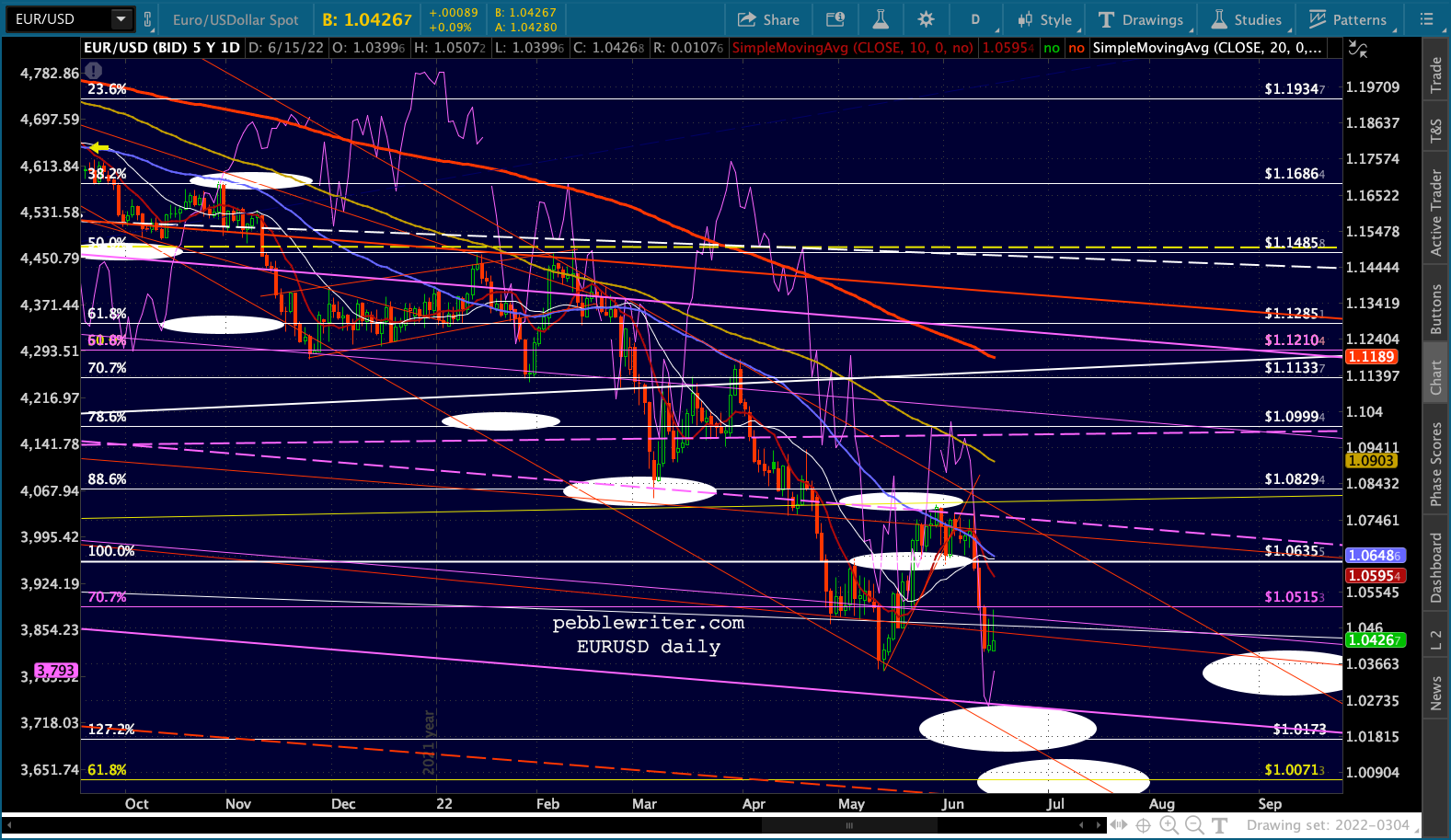

Speaking of currencies, the ECB conducted an emergency meeting this morning to try and address what they term as the fragmentation of member nations’ bond markets – the fact that some countries have experienced higher interest rates.

The euro briefly strengthened on the news, but backed off again as soon as it became clear that the action will essentially mean more QE for weaker members.

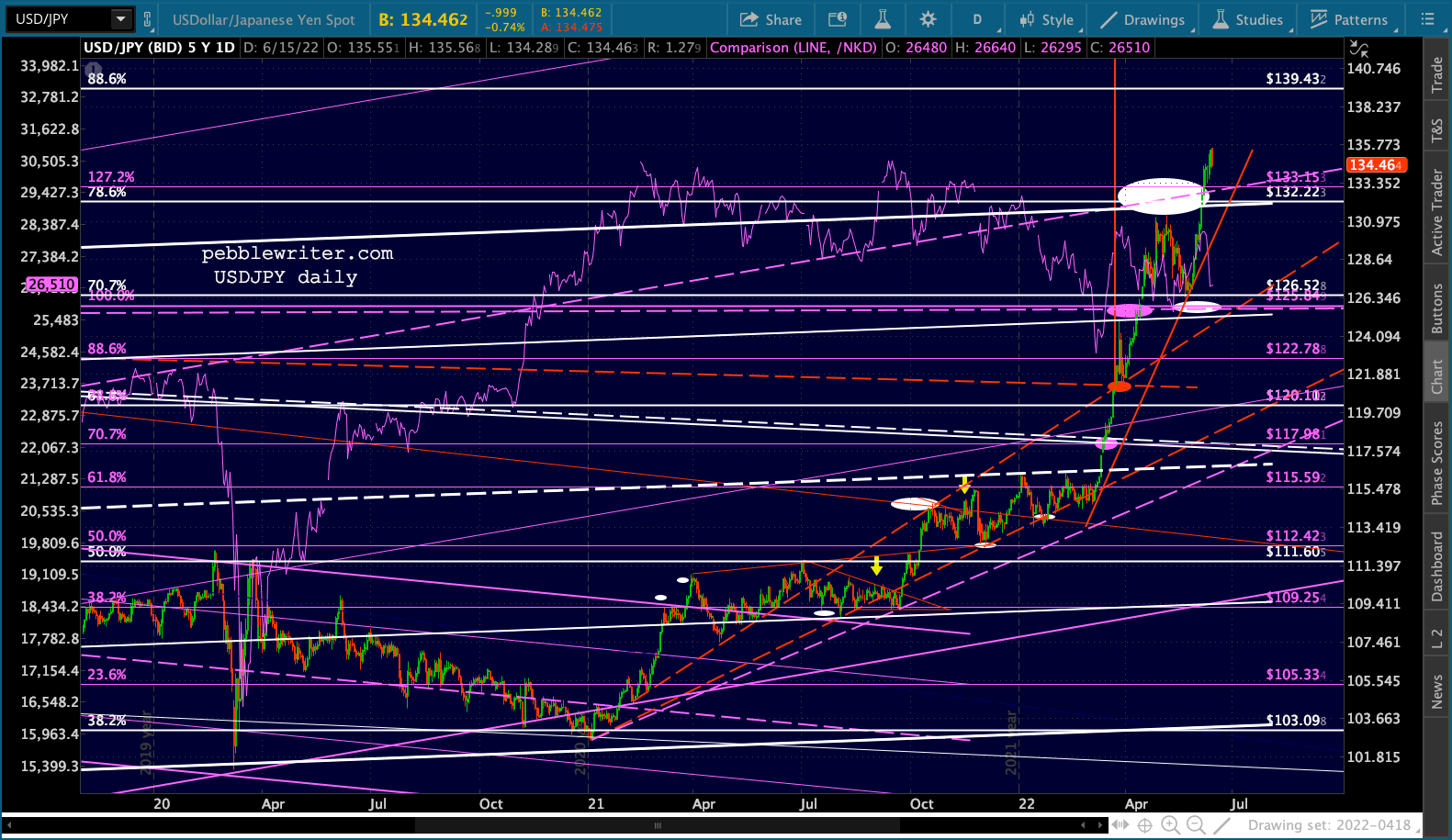

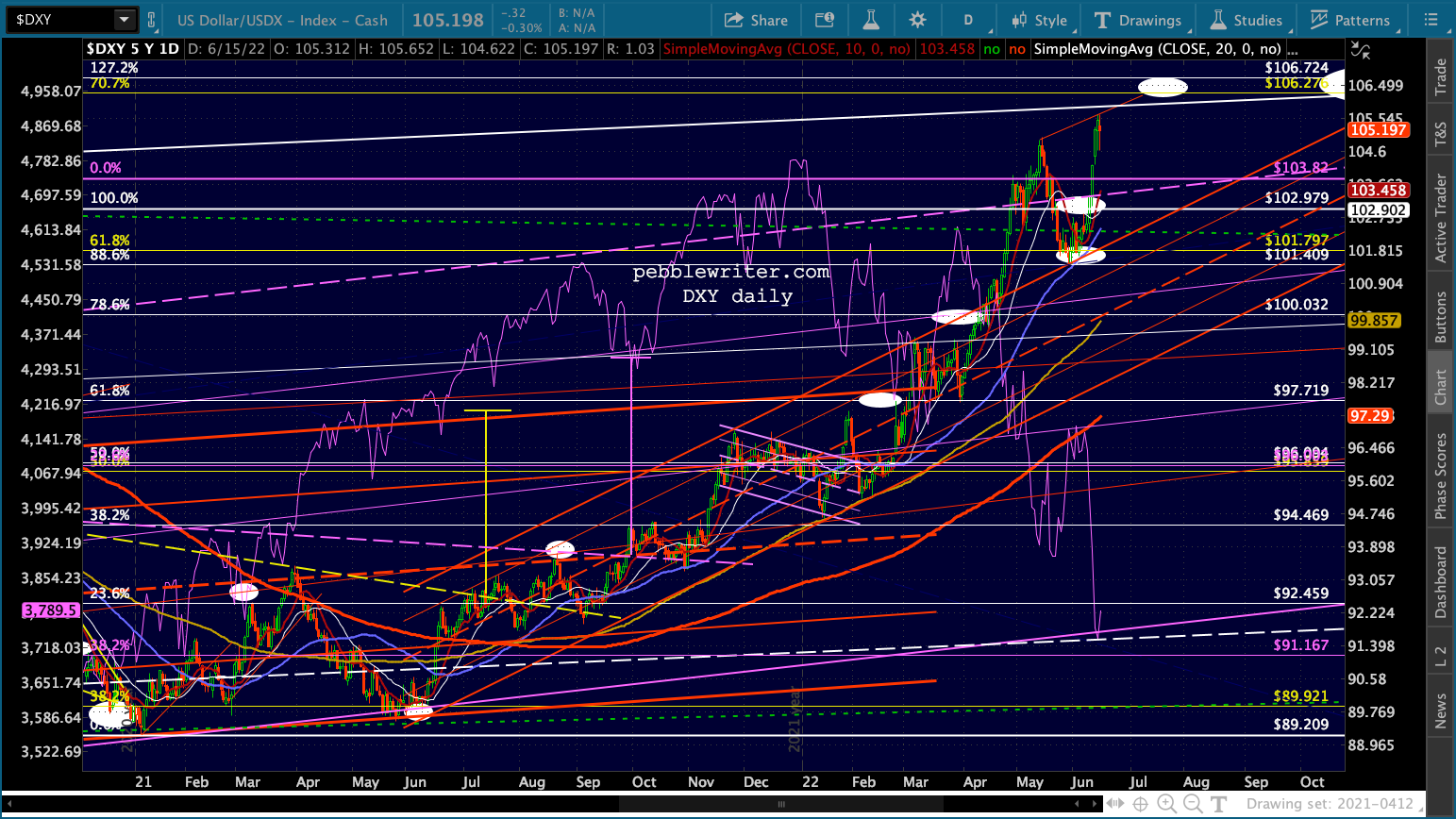

Combined with modest yen strengthening…

Combined with modest yen strengthening… …this has left the DXY within striking distance of out 106.27-106.72 target.

…this has left the DXY within striking distance of out 106.27-106.72 target.  It’s no coincidence that the dollar has been rallying ever since CPI topped 5% in May 2021 and broke out in Apr 2022 when Mar CPI of over 8% was announced.

It’s no coincidence that the dollar has been rallying ever since CPI topped 5% in May 2021 and broke out in Apr 2022 when Mar CPI of over 8% was announced. Bottom line, the Fed has no choice other than to put the economy into a recession with increasingly higher rates (they might end up doing that regardless of where the USD goes.)

Bottom line, the Fed has no choice other than to put the economy into a recession with increasingly higher rates (they might end up doing that regardless of where the USD goes.)

UPDATE: 5:00 PM

75 bps, and a vicious hammer job on VIX.