Futures are up moderately after the November CPI print, which increased both MoM and YoY versus last month.

continued for members…

continued for members…

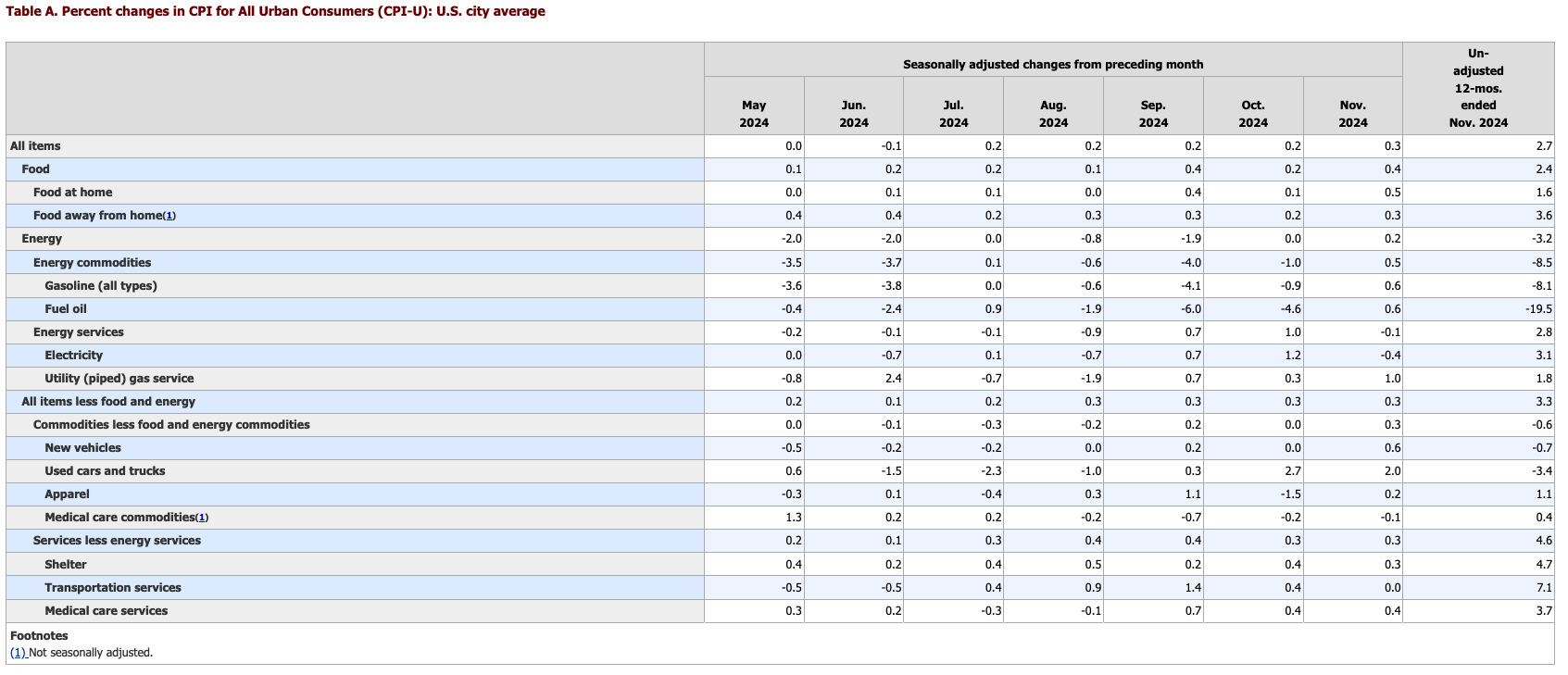

November’s MoM CPI rose 0.3% verus 0.2% in October and YoY rose 2.7% versus 2.6% in October. Core rose 0.3% MoM and 3.3% YoY.

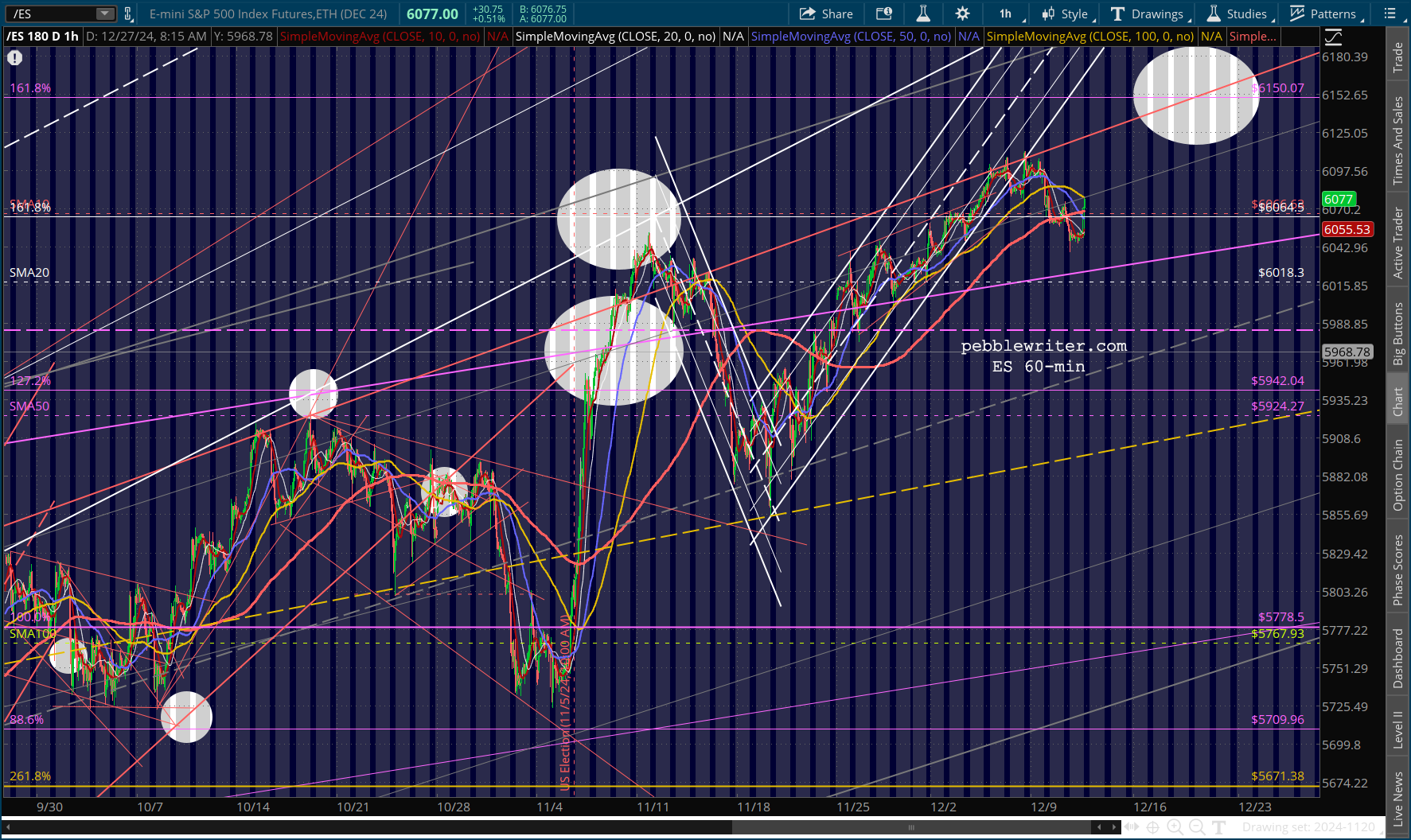

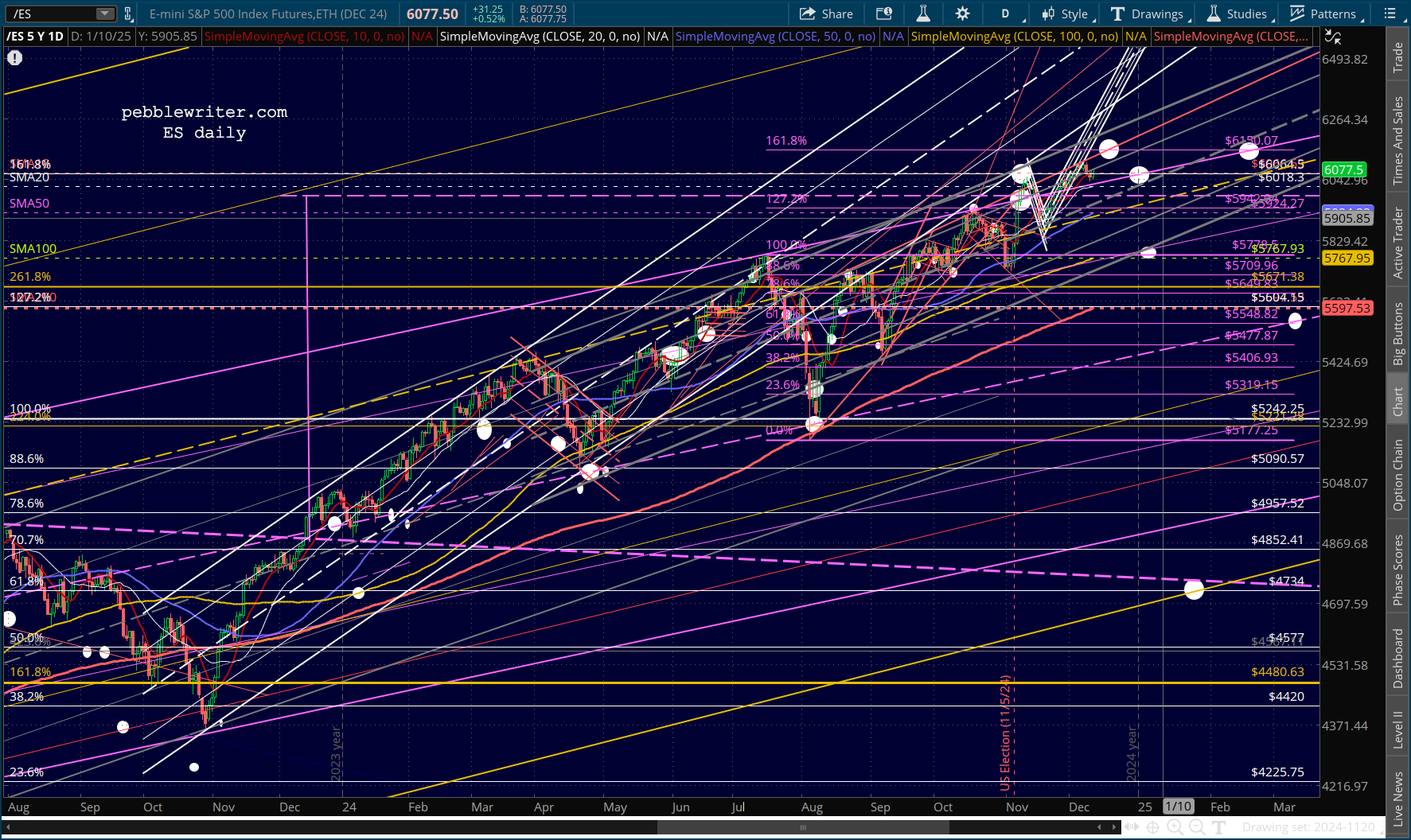

This puts ES back above its SMA10 and increases the odds of reaching the purple 1.618 target at 6150.

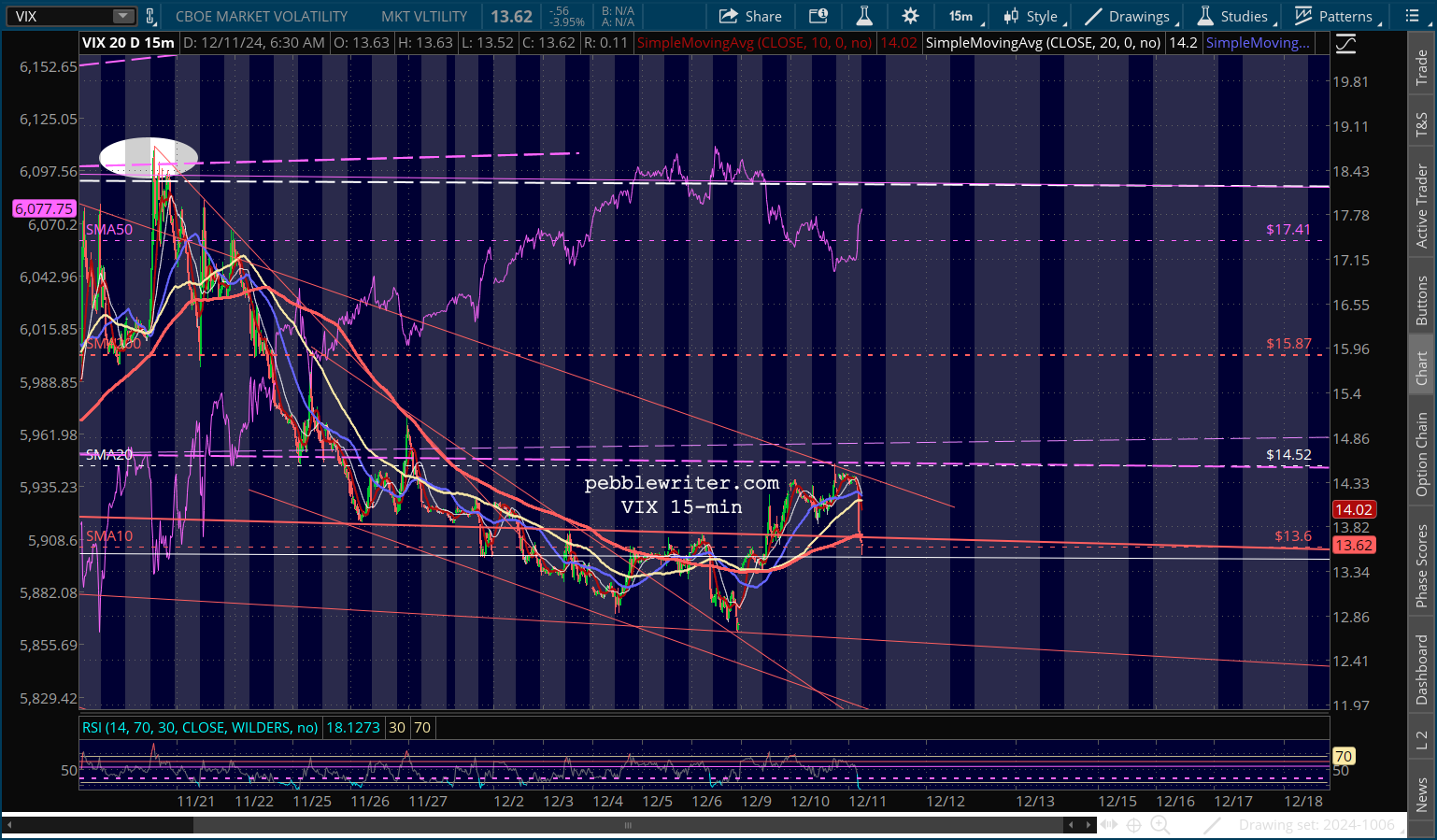

The algos had plenty of help this morning. VIX did a hard reverse to its SMA10…

The algos had plenty of help this morning. VIX did a hard reverse to its SMA10…

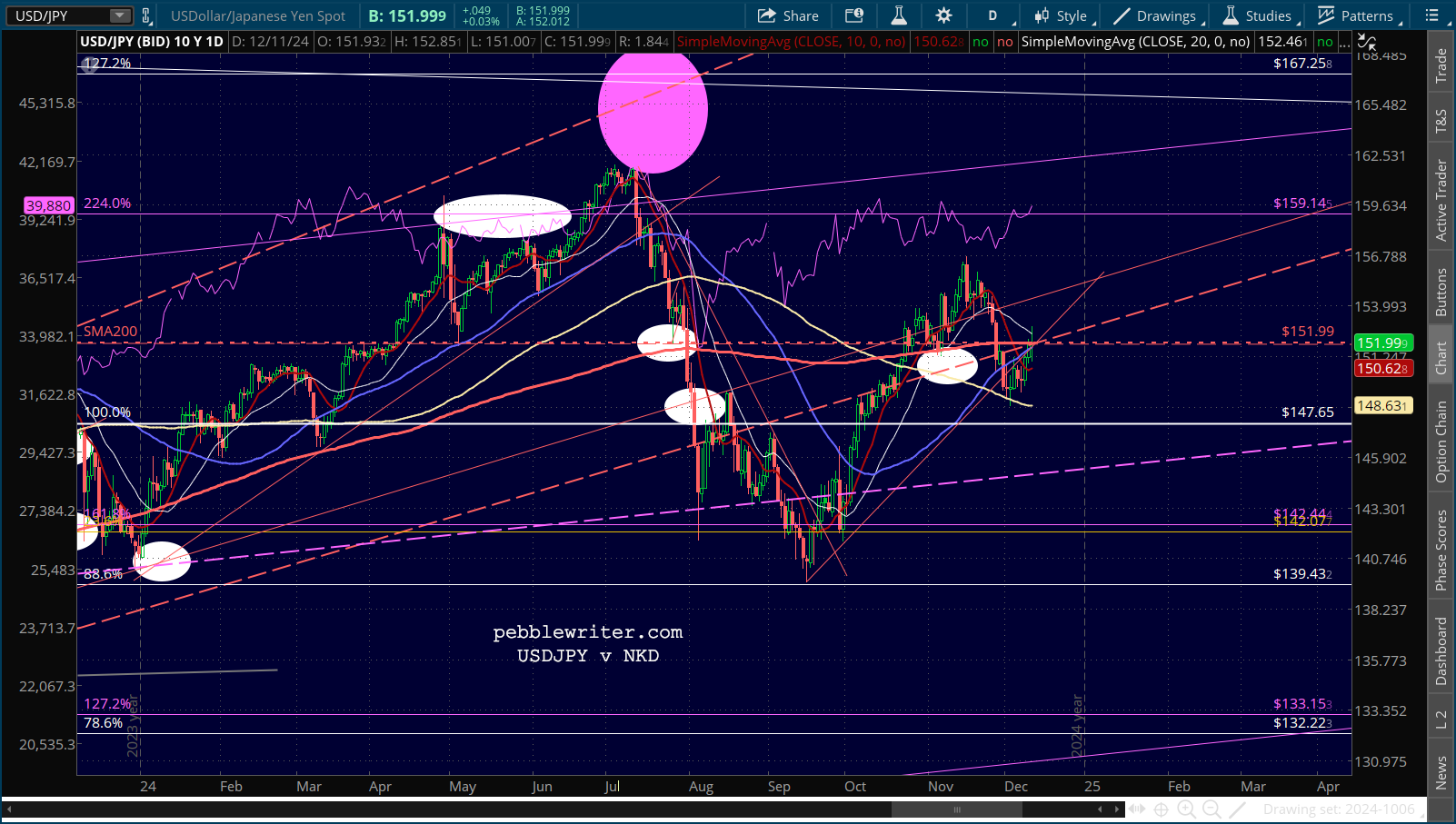

…and USDJPY surged past its SMA200 – at least initially.

…and USDJPY surged past its SMA200 – at least initially.

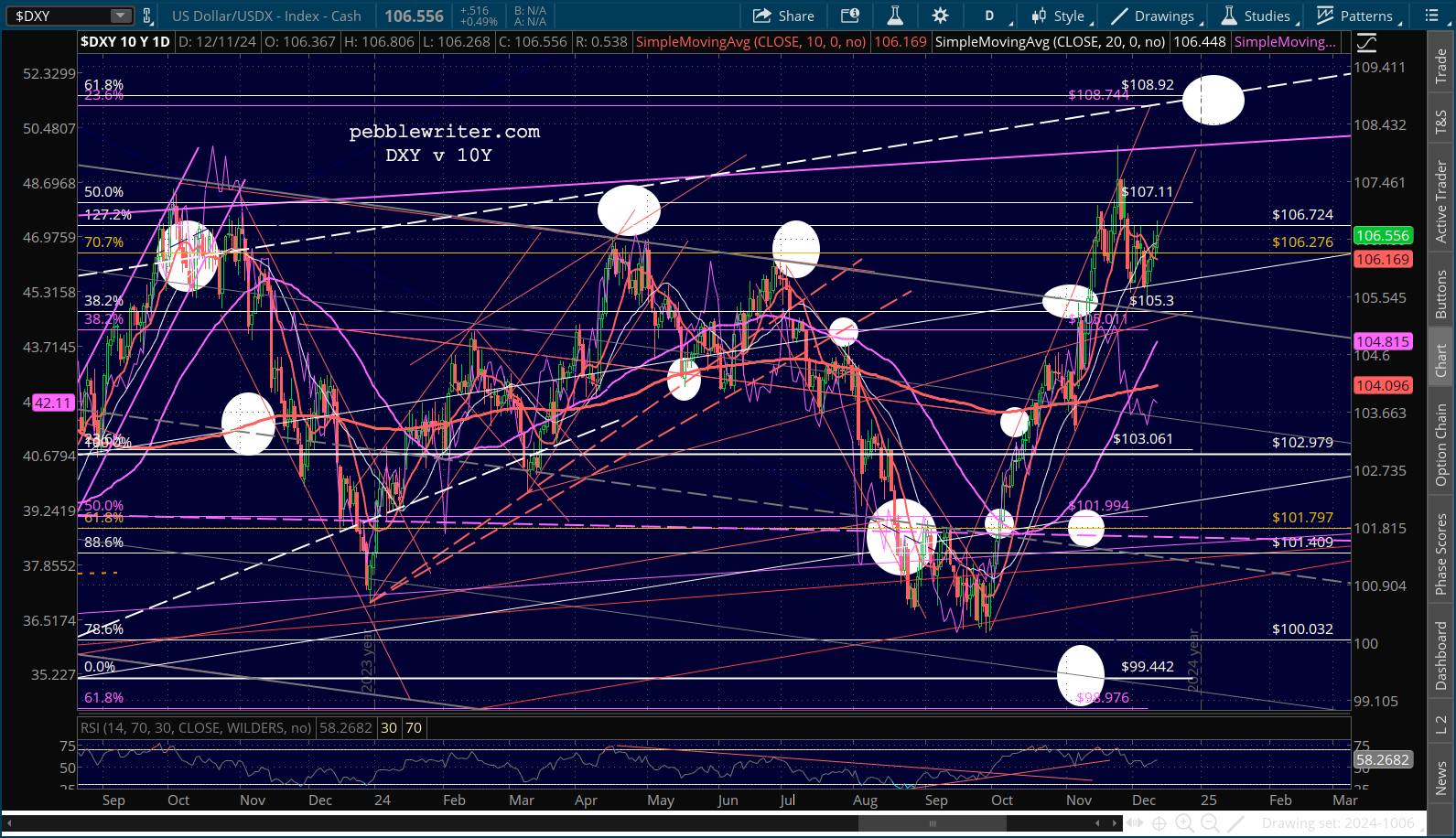

Net net, the DXY rose about 0.5% – a negative for stocks, but one they’re ignoring at the moment.

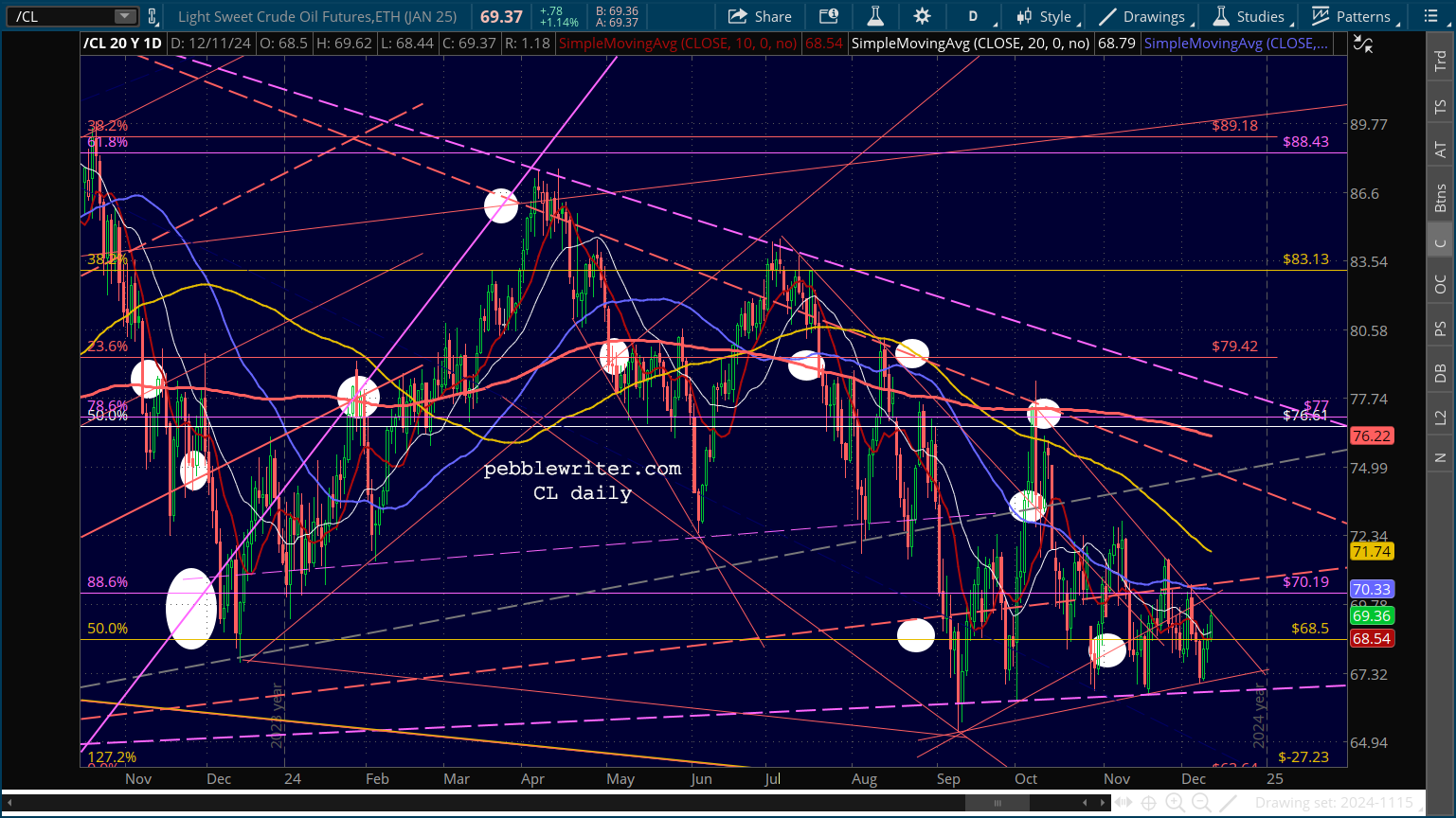

Net net, the DXY rose about 0.5% – a negative for stocks, but one they’re ignoring at the moment. Likewise, CL is pushing up against a falling TL. A rise above it would be bearish…

Likewise, CL is pushing up against a falling TL. A rise above it would be bearish…

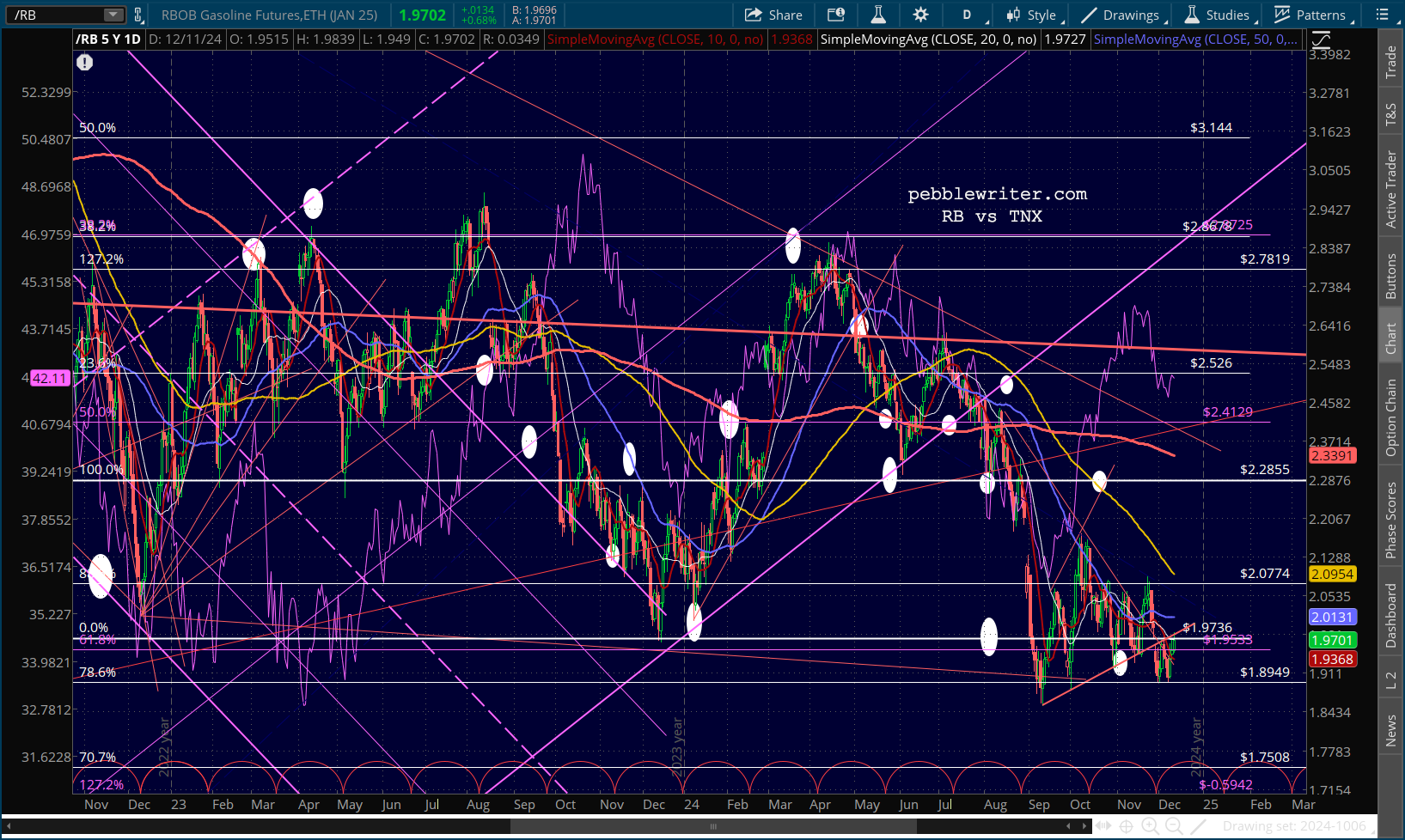

…as would a push by RB above its current TL backtest.

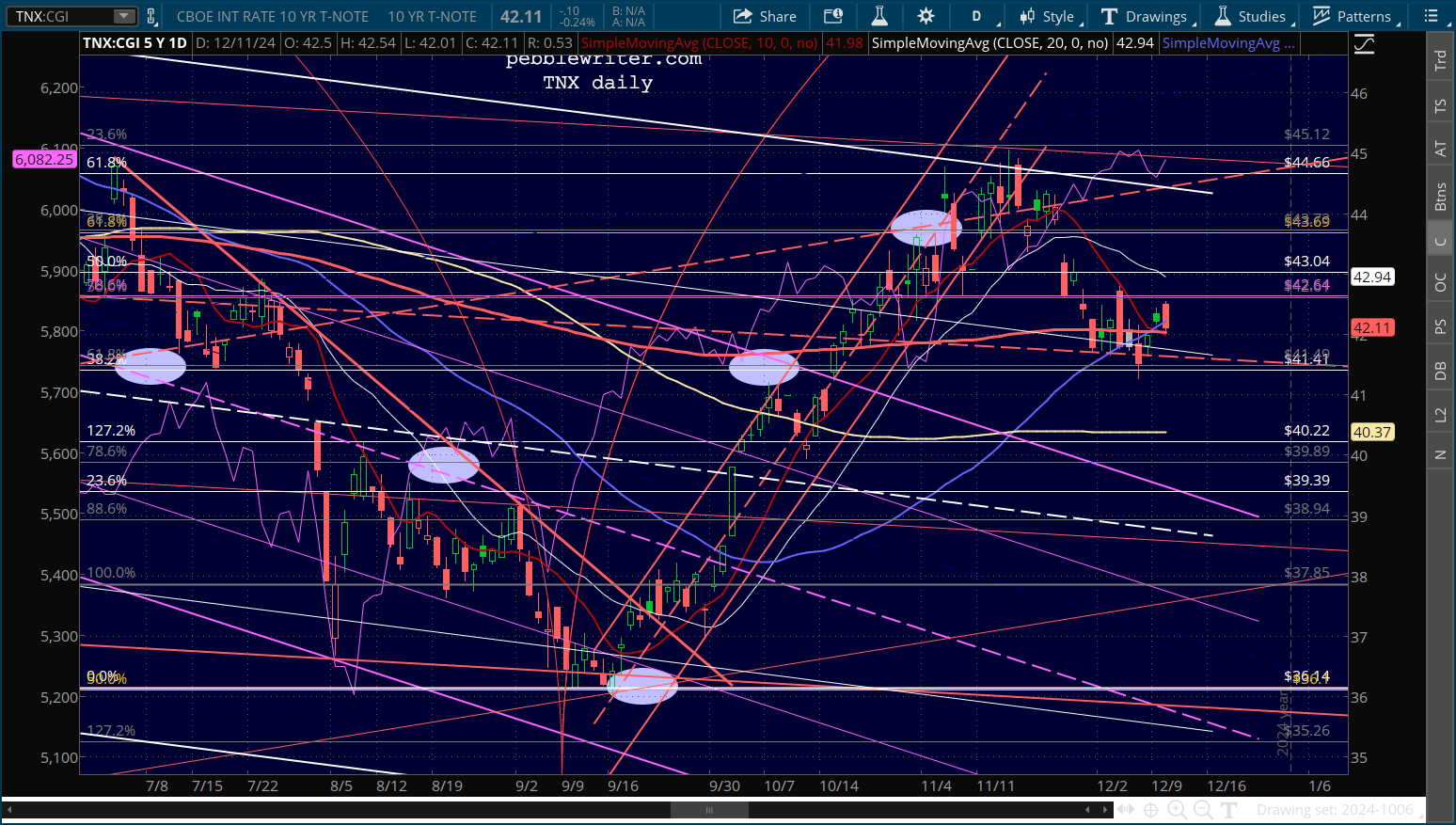

…as would a push by RB above its current TL backtest. But, the tame CPI print has enabled TNX to decline slightly, backtesting its SMA200. Unless it dives back below 4.2%, today’s rally shouldn’t last.

But, the tame CPI print has enabled TNX to decline slightly, backtesting its SMA200. Unless it dives back below 4.2%, today’s rally shouldn’t last.

There’s no doubt that December CPI, reported on January 15, will be substantially higher. But, for now, the algos are okay with the slightly higher November print and the odds of a December rate cut remain greater the same.

There’s no doubt that December CPI, reported on January 15, will be substantially higher. But, for now, the algos are okay with the slightly higher November print and the odds of a December rate cut remain greater the same.

Shelter eased slightly MoM but remains elevated at 4.7% YoY. Food, gasoline, fuel oil, vehicles, and medical care are all running at a problematic MoM rate.

But, the YoY increase in gas prices means inflation isn’t done with this market. And, the prospect of tariffs further elevating prices for nearly everything strongly suggests December inflation could reach 3%, a print that the market likely won’t shrug off.

But, the YoY increase in gas prices means inflation isn’t done with this market. And, the prospect of tariffs further elevating prices for nearly everything strongly suggests December inflation could reach 3%, a print that the market likely won’t shrug off. I find the current and expected data concerning enough that I personally think the FOMC should not cut in December or January. But, this would likely touch off a year end correction – something the Fed is normally loath to do.

I find the current and expected data concerning enough that I personally think the FOMC should not cut in December or January. But, this would likely touch off a year end correction – something the Fed is normally loath to do.

Stay tuned…