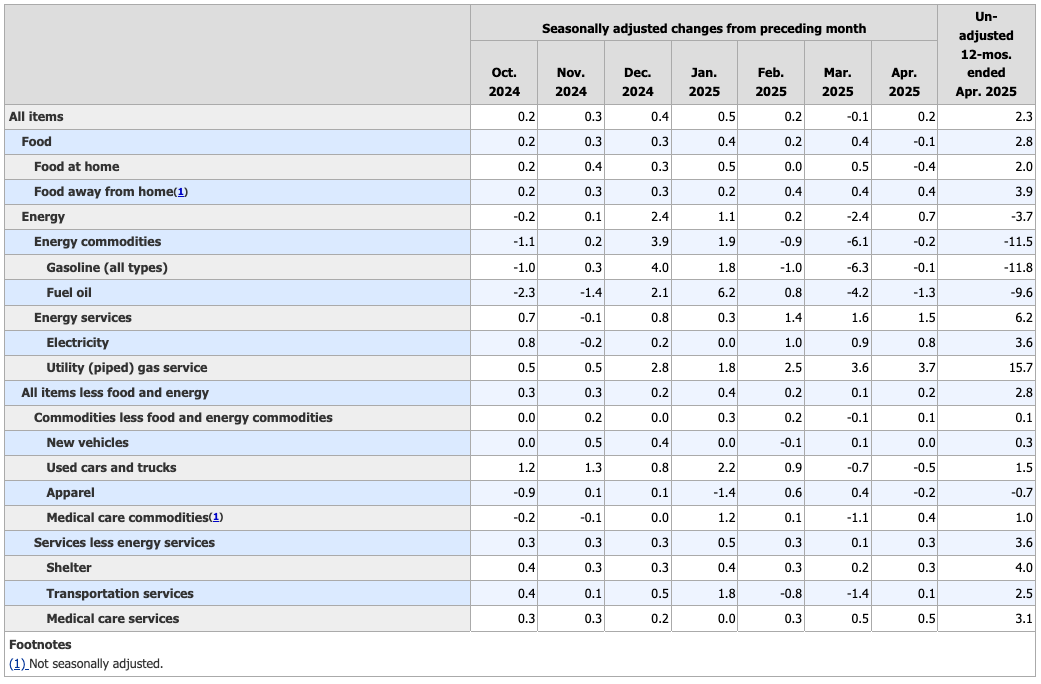

CPI came in at 0.2% MoM and 2.3% YoY, a little lighter than expected – but, only because most tariff price hikes hadn’t worked their way into the official print just yet. There’s very little chance, for instance, that new vehicle price increases will remain tame unless tariffs are eliminated altogether.

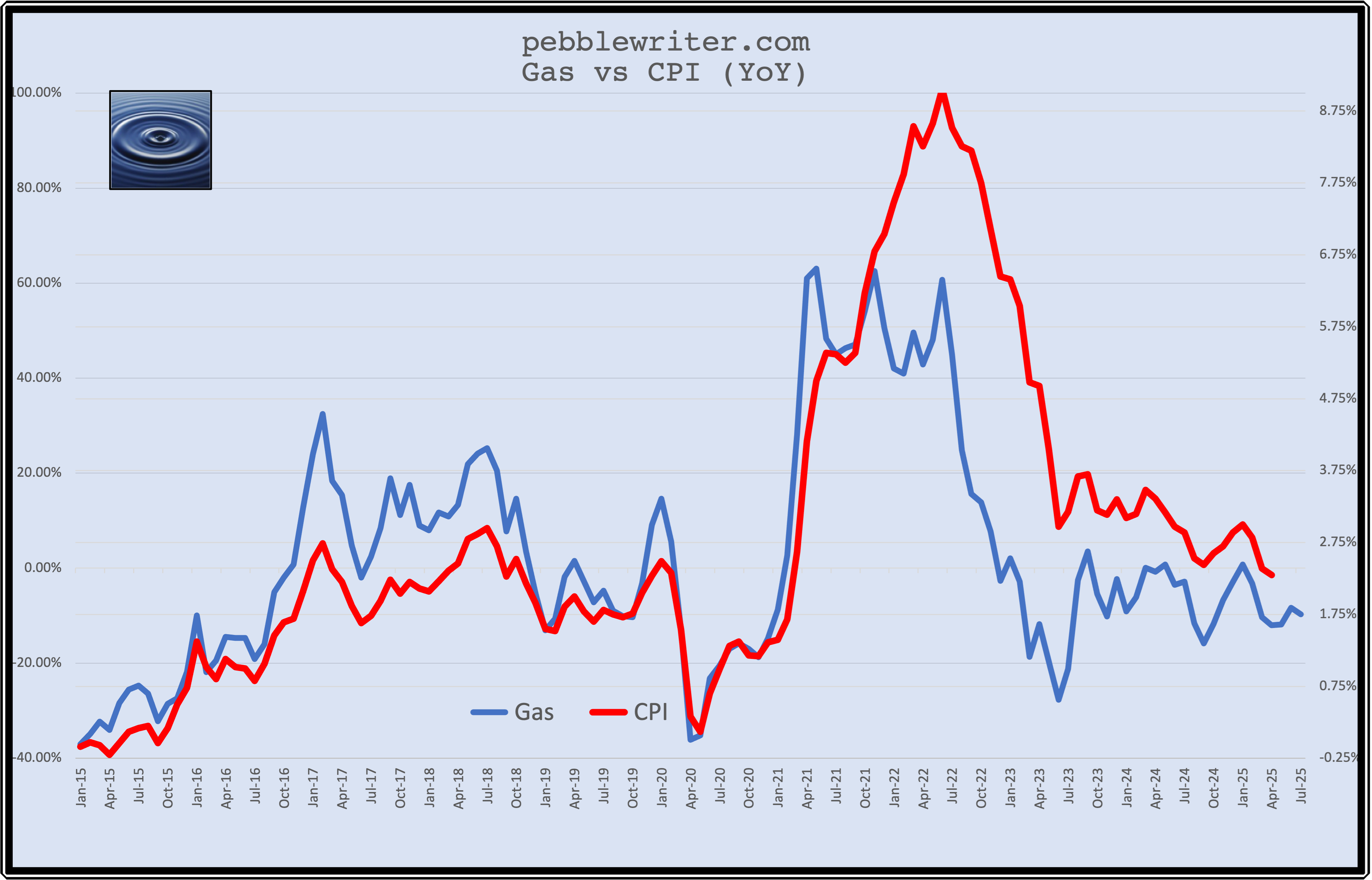

The biggest contributor to lower inflation remains oil and gas, which registered double digit declines. Unfortunately, the 12% YoY decline in retail gas prices has likely bottomed out unless CL and RB continue to fall. At current prices, the YoY delta will be back to flat – removing a key source of falling inflation rates.

The biggest contributor to lower inflation remains oil and gas, which registered double digit declines. Unfortunately, the 12% YoY decline in retail gas prices has likely bottomed out unless CL and RB continue to fall. At current prices, the YoY delta will be back to flat – removing a key source of falling inflation rates.

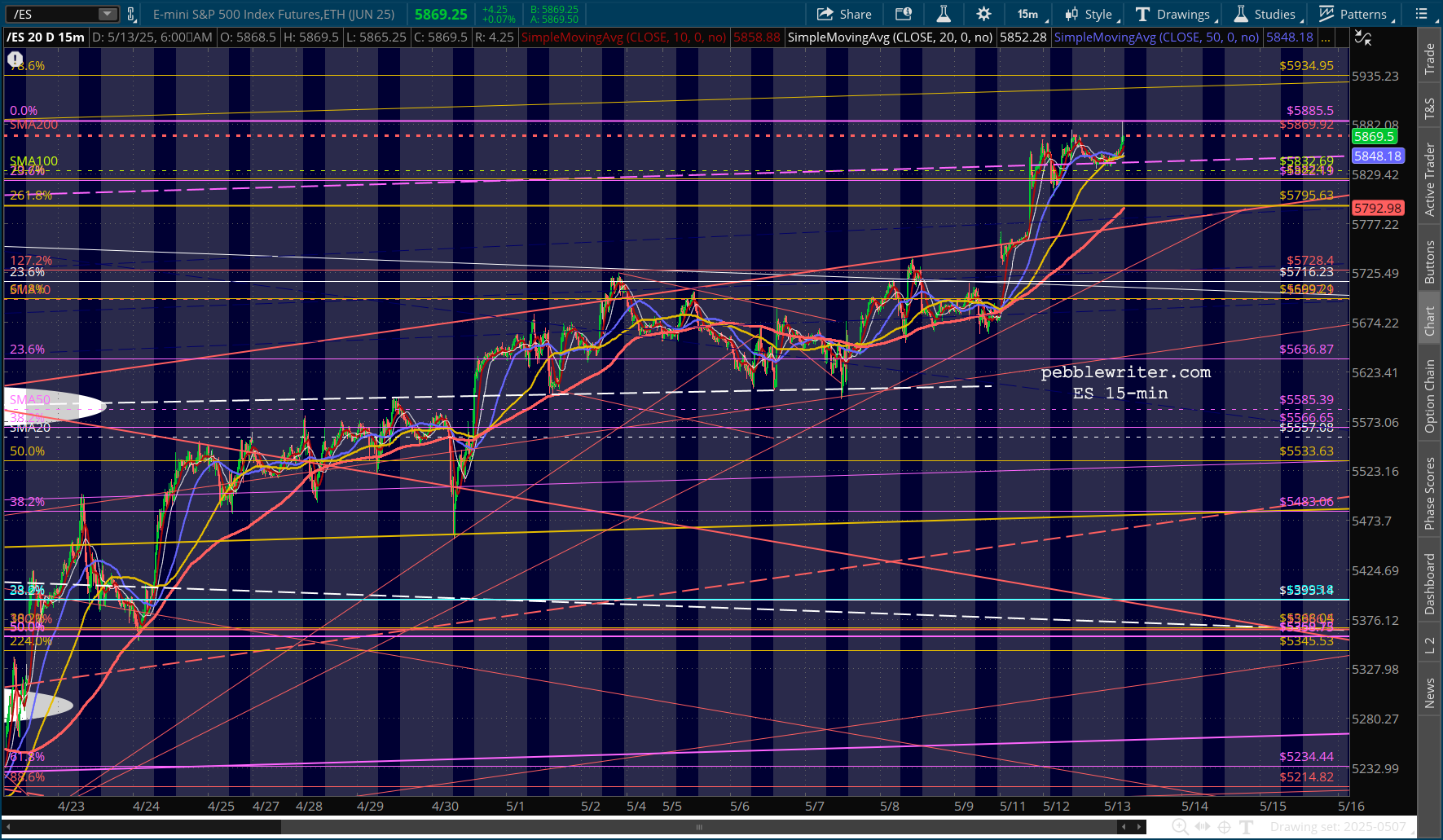

Futures are marginally lower after an initial bump on the news.

Futures are marginally lower after an initial bump on the news.

continued for members…

continued for members…

Thanks everyone for your texts and emails. I am home again after spending Sunday night in the ER with very elevated blood pressure after a painful attack of kidney stones. Not fun. I’m gradually getting caught up again, so appreciate your understanding and well wishes.

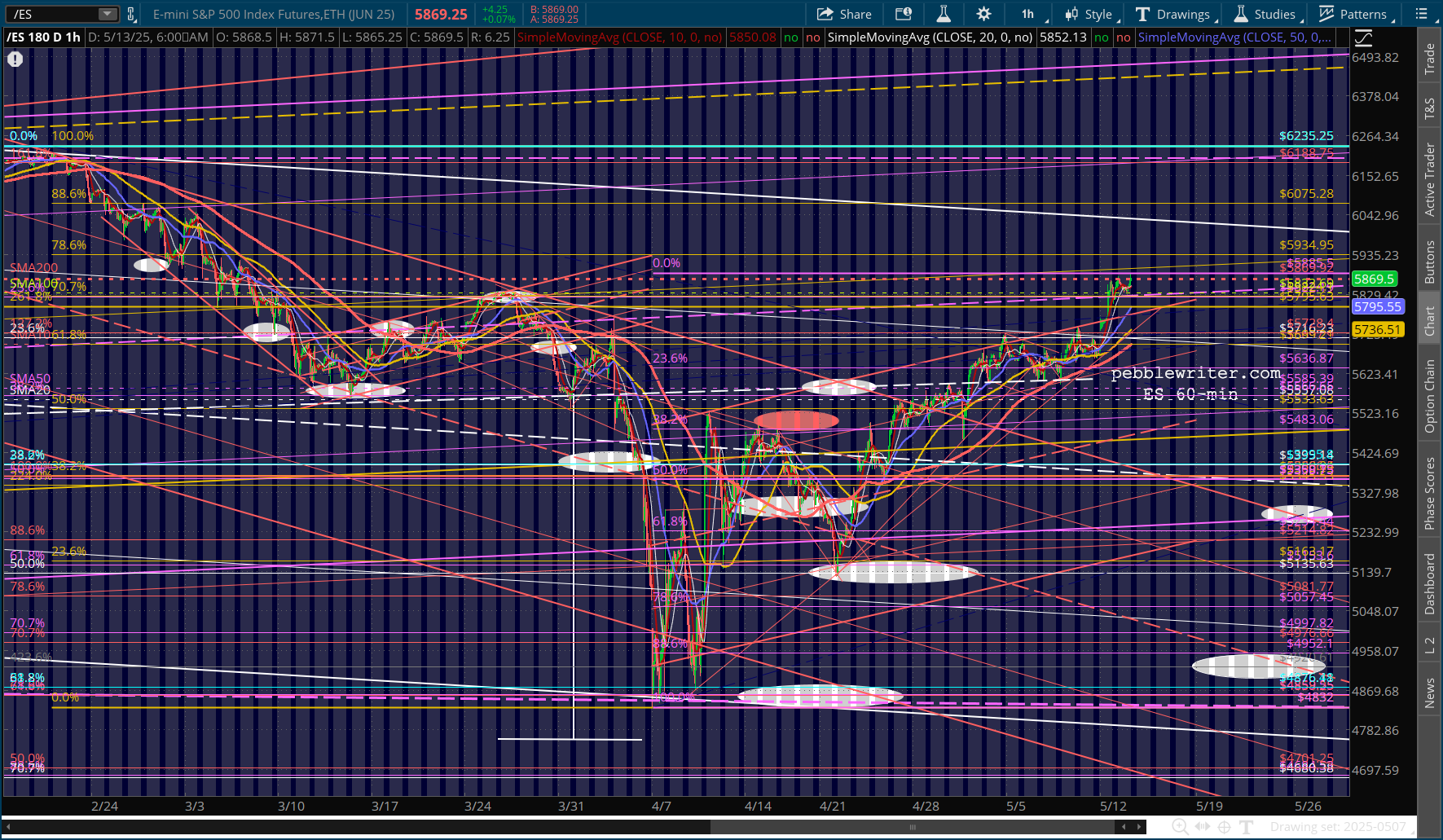

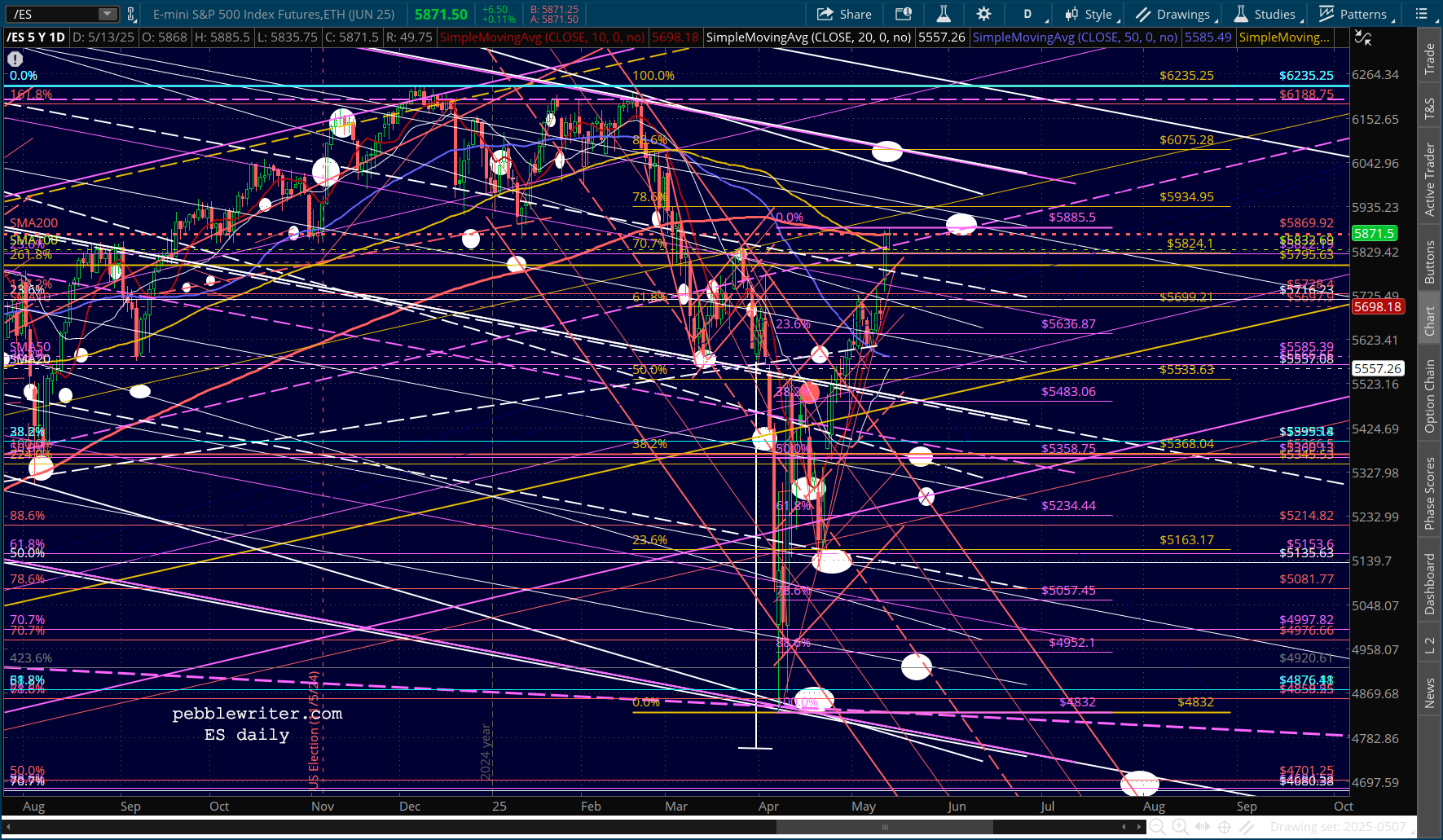

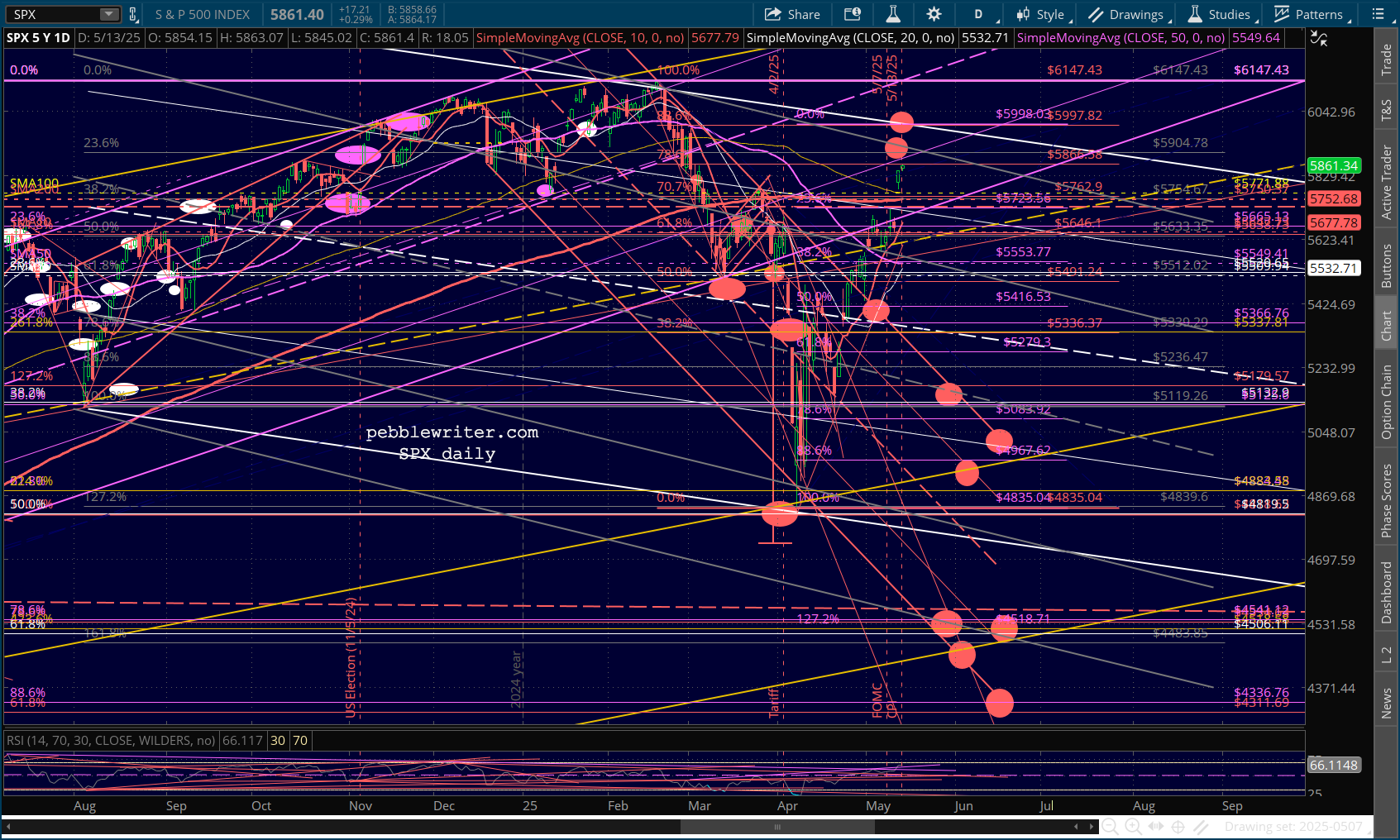

As mentioned yesterday, SPX leapfrogged above its SMA200 on the news that the tariffs on China would be reduced to only 35% for the next 90 days.

As mentioned yesterday, SPX leapfrogged above its SMA200 on the news that the tariffs on China would be reduced to only 35% for the next 90 days. Gotta jump on a call, will continue shortly…

Gotta jump on a call, will continue shortly…