Futures are up moderately in advance of this week’s FOMC rate decision.

Of course, it hasn’t hurt that Elon Musk recently bought over $1 billion of TSLA. From Bloomberg:

Of course, it hasn’t hurt that Elon Musk recently bought over $1 billion of TSLA. From Bloomberg:

The purchase amounts to a show of confidence in Tesla’s prospects after a challenging first half of the year in which vehicle sales slumped 13% worldwide. While Musk has talked up Tesla’s pursuit of robotaxis and humanoid robots, he’s also cautioned that the company could be in for “a few rough quarters” after the US phases out electric-car purchase incentives at the end of this month.

Note that we haven’t had a 3% pullback since May.

continued for members…

The recent revision of employment data shows that instead of adding around 200K jobs per month over the past year, we’ve added about 75K. This argues for the FOMC to focus much more on stagnation than it does on inflation. But, the reality is we just can’t trust the jobs data coming out of the BLS since Trump decided to fire (with zero repercussions) the head keeper of the data. What better way to force the Fed’s hand than to send the very signal that was sent?

Obviously the members of the FOMC would be well aware of the tainted data. For those who care (i.e. aren’t vying for Powell’s job), they face a conundrum: focusing on inflation might be justifiable, but would it invite a Lisa Cook-style attack on their backside?

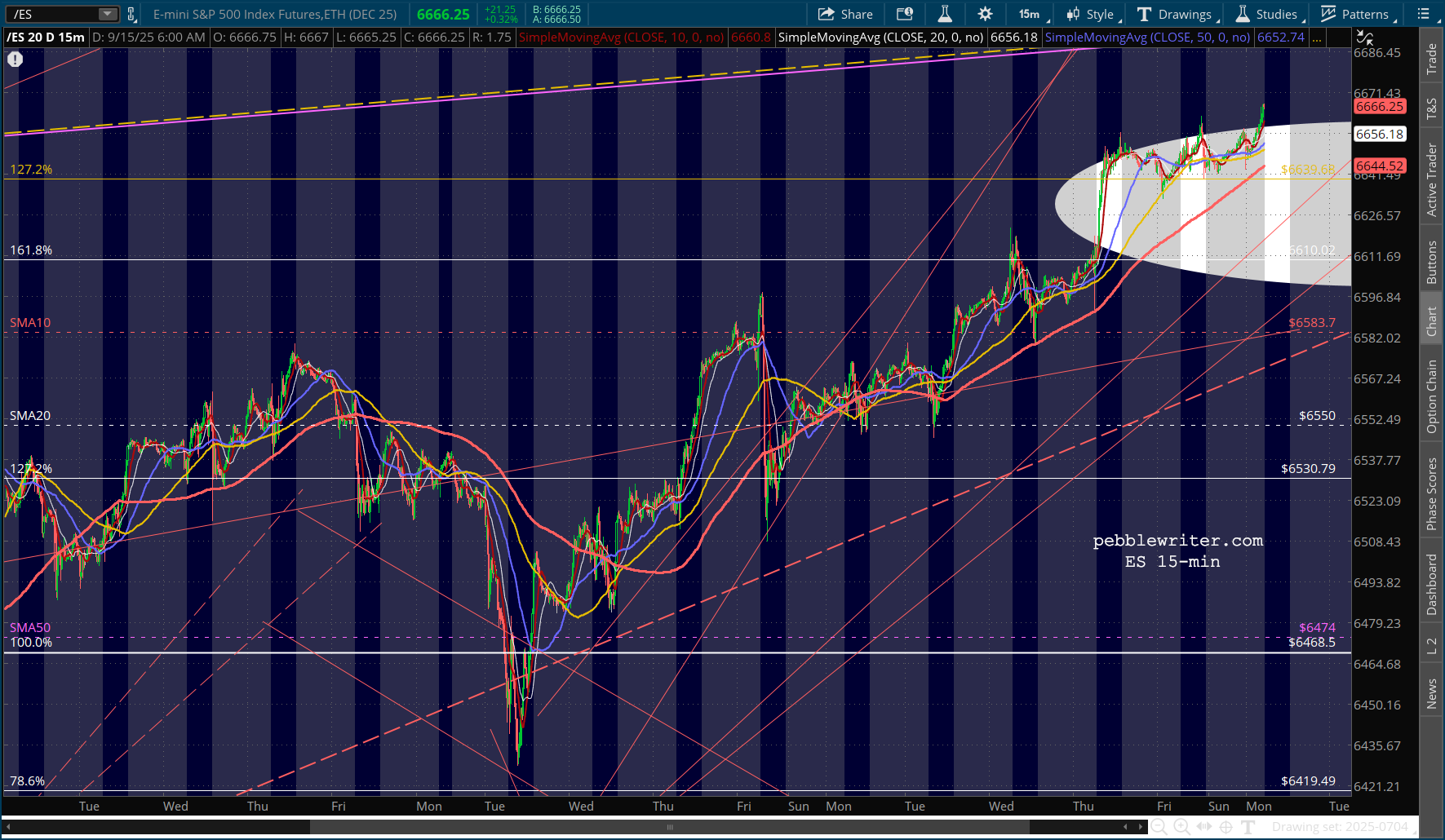

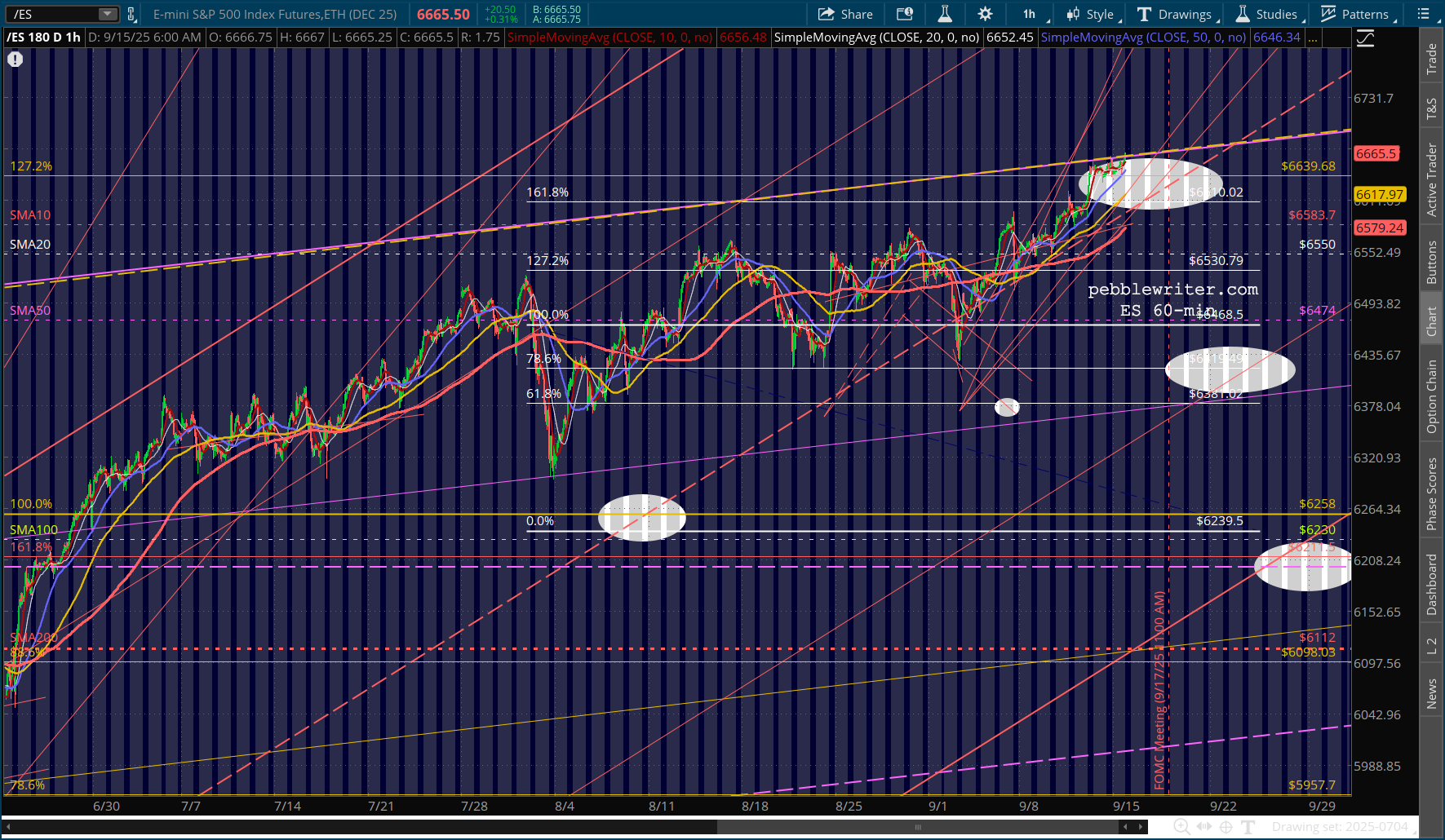

ES and SPX still face channel resistance. A breakout would be significant, but might a 25 bps rate cut disappoint?

ES and SPX still face channel resistance. A breakout would be significant, but might a 25 bps rate cut disappoint?

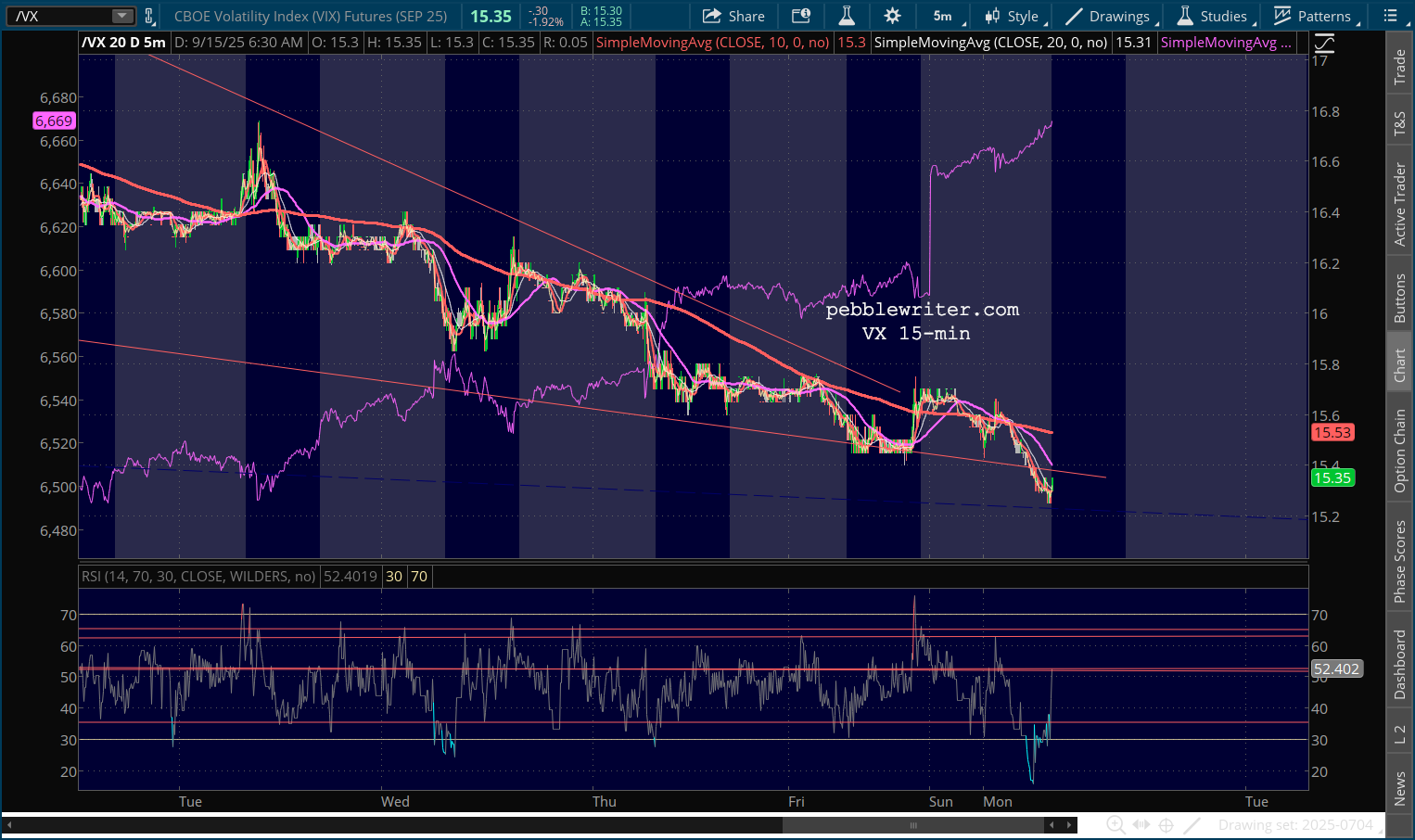

The vol smackdown continues to be the primary driver of the equity meltup.

The vol smackdown continues to be the primary driver of the equity meltup.

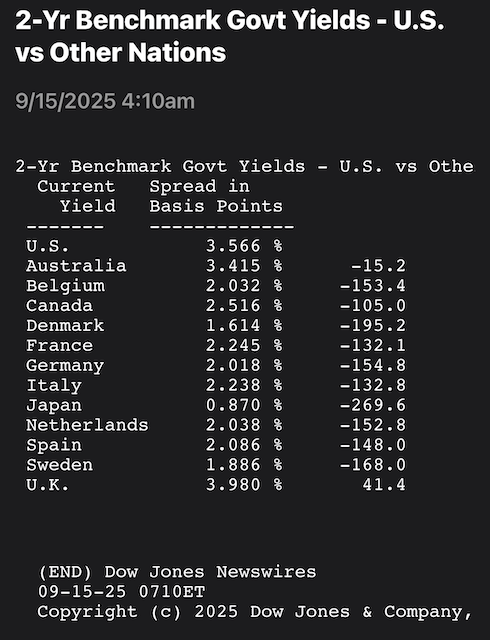

As we discussed last week, the market has already done a pretty good job of lowering interest rates for the Fed.

As we discussed last week, the market has already done a pretty good job of lowering interest rates for the Fed.

Yet, the USD hasn’t really kept up. Note, that while the 10Y is making new lows, DXY hasn’t. EURUSD is holding up, but isn’t pushing to new highs.

Yet, the USD hasn’t really kept up. Note, that while the 10Y is making new lows, DXY hasn’t. EURUSD is holding up, but isn’t pushing to new highs.

And, USDJPY has refused to break down.

And, USDJPY has refused to break down.

So, the DXY just muddles along near recent lows, but not keeping pace with the decline in the 10Y.  Imagine if the US 2Y was anywhere close to the rest of the world’s – what that might do the value of the US dollar.

Imagine if the US 2Y was anywhere close to the rest of the world’s – what that might do the value of the US dollar.

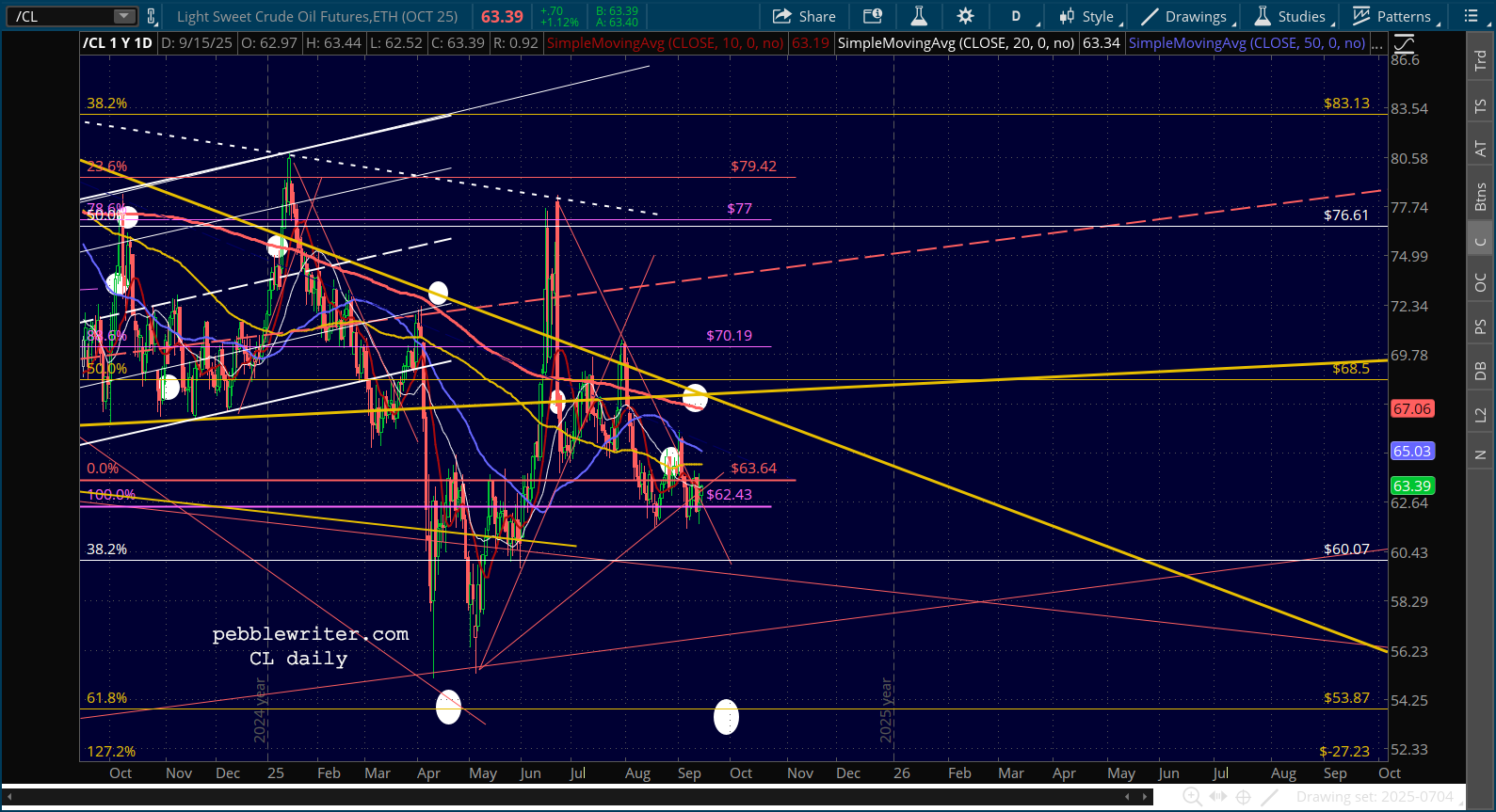

The stable oil/gas market continues to influence inflation. But, as we discussed last week a decline in CPI would require a breakdown in oil/gas prices going forward. And, you have to wonder if there’s a limit to OPEC’s largess. I’m leaning toward RB breaking down between now and the end of the year to either 1.85 or 1.75.

The stable oil/gas market continues to influence inflation. But, as we discussed last week a decline in CPI would require a breakdown in oil/gas prices going forward. And, you have to wonder if there’s a limit to OPEC’s largess. I’m leaning toward RB breaking down between now and the end of the year to either 1.85 or 1.75.

Stay tuned.