The worst trade deficit miss ever…

…is what you get when you ramp your currency to unrealistic levels — proof, again, that in currency wars not everybody can win. As we detailed last month, the lower yen/higher dollar/lower euro/cheaper oil/stable inflation/stable interest rates/higher stocks scheme will only work so long as the three or four institutional investors that still give a damn about fundamentals don’t panic.

Negative GDP readings have been known to incite a panic. And, the “higher dollar is better” meme will be a tougher sell going forward.

USDJPY is tumbling, of course.

USDJPY is tumbling, of course.

Yet, futures are only off 5 points (after being off 8 pts earlier.) Because, as we’ve noted countless times before, a weakening dollar (kneejerk reaction to the trade deficit report) strengthens CL — which is a key driver in today’s algo-driven “markets.”

Yet, futures are only off 5 points (after being off 8 pts earlier.) Because, as we’ve noted countless times before, a weakening dollar (kneejerk reaction to the trade deficit report) strengthens CL — which is a key driver in today’s algo-driven “markets.”

The other consideration, of course, is the impact such data might have on Q1 GDP, and the likelihood that a negative print would compel the FOMC to jump in and “save the economy” with QE4.

The other consideration, of course, is the impact such data might have on Q1 GDP, and the likelihood that a negative print would compel the FOMC to jump in and “save the economy” with QE4.

Since the Fed engineered the dollar ramp — thus exacerbating the trade deficit and GDP weakness — rolling out QE4 would be akin to a rattlesnake administering antivenom.

Keep an eye on USDJPY, which TPTB tried to pitch us as breaking out yesterday. It won’t — at least not for a while. A nice reversal, though, is going to ramp up oil and delay DX’s inevitable rebound. No way this won’t present a headwind for stocks today…

Our analog is intact; our targets are intact. Our “markets” are most definitely not.

continued for members…

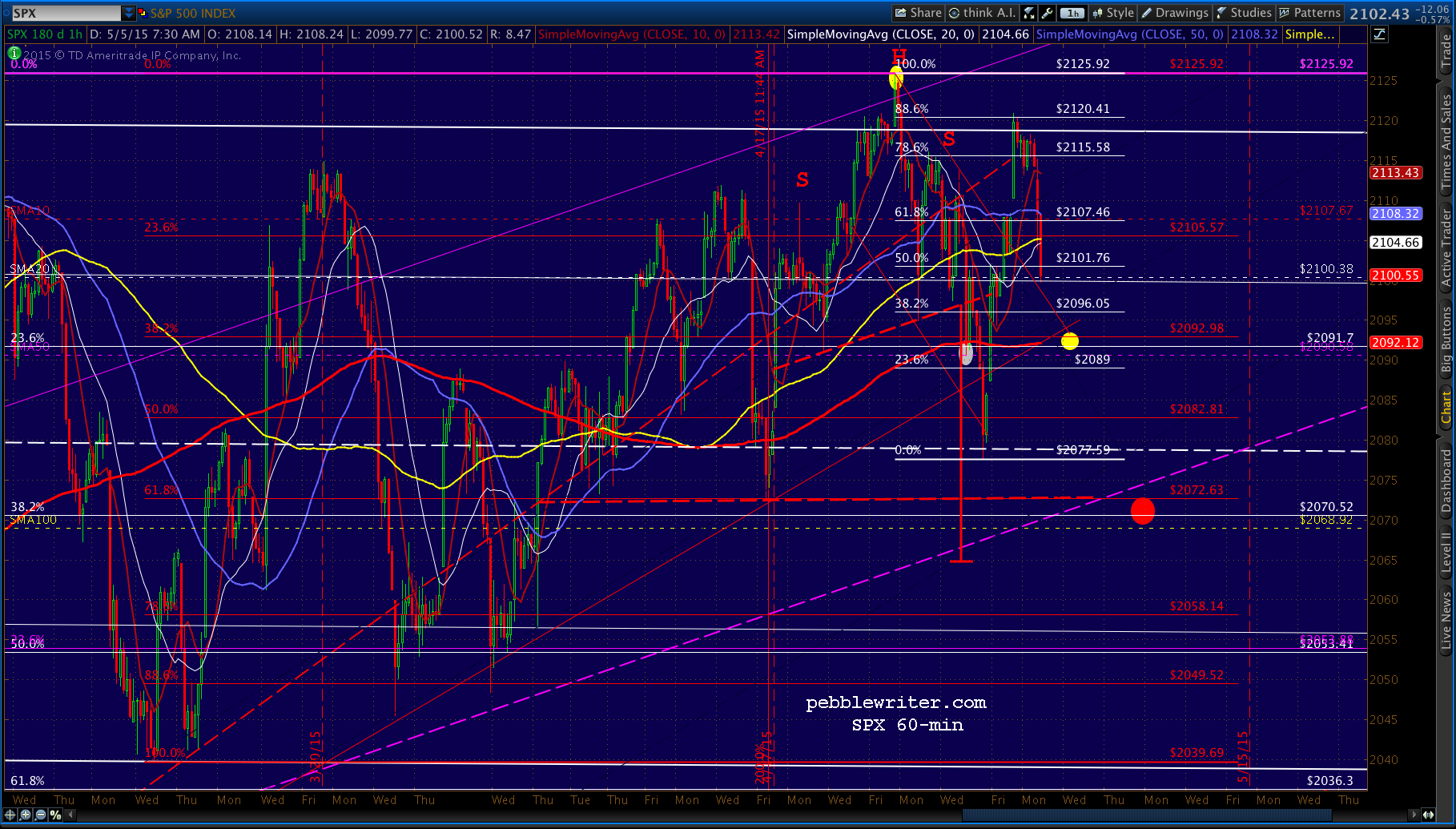

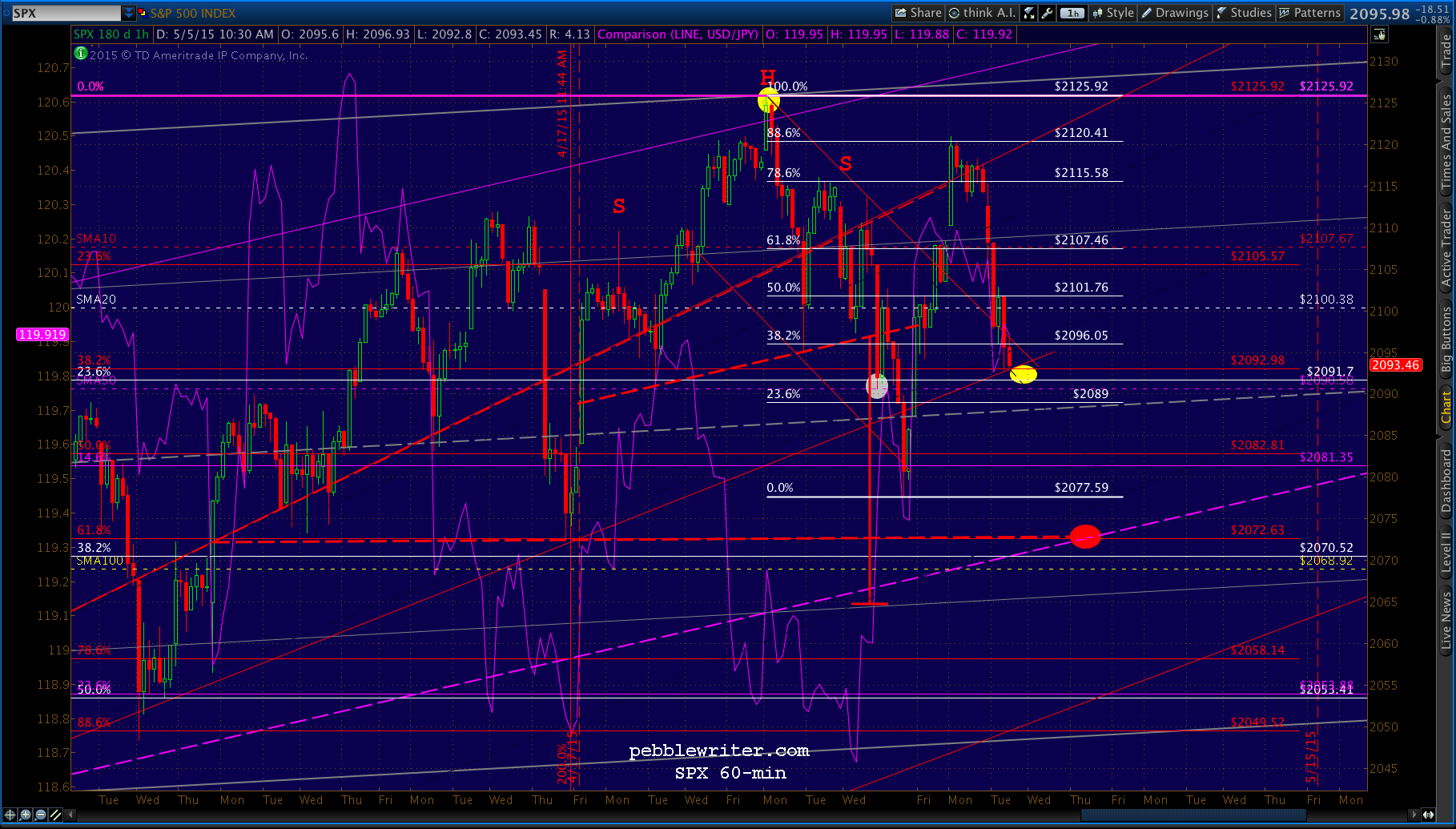

A reminder of our downside targets:

UPDATE: 2:05 PM

UPDATE: 2:05 PM

First target down. A bounce here at 2090-2092 would make perfect sense. The SMA50 is at 2090.58, and a backtest to the SMA20 would put the bounce at 2100ish.

Anyone seriously contemplating playing the bounce should, as always, use appropriate stops and watch their position like a hawk — especially overnight. I’m looking for lower prices tomorrow, and there’s no guarantee that there won’t be a rush to the exits in the final hour.

Anyone seriously contemplating playing the bounce should, as always, use appropriate stops and watch their position like a hawk — especially overnight. I’m looking for lower prices tomorrow, and there’s no guarantee that there won’t be a rush to the exits in the final hour.