Futures are up 40 points off their overnight lows as VIX was hammered after pushing briefly above its 10-DMA.  It’s not unusual for charts to take on a bearish tone going into a holiday weekend. In a low volume environment such as this, however, it’s all too common for trends to reverse, currencies to pop, VIX to plummet.

It’s not unusual for charts to take on a bearish tone going into a holiday weekend. In a low volume environment such as this, however, it’s all too common for trends to reverse, currencies to pop, VIX to plummet.

Will this one be any different?

continued for members…

Note that VIX has, so far, resisted any efforts to break down or out. This leaves ES in limbo. It would be highly unusual after such a rebound as we’ve seen since Mar 23 for it to come so close to the SMA200 without tagging it or punching through.

This leaves ES in limbo. It would be highly unusual after such a rebound as we’ve seen since Mar 23 for it to come so close to the SMA200 without tagging it or punching through.  As we noted yesterday, by delaying the tag ES now has the opportunity to backtest the latest little rising white channel but at a price higher than the SMA200. If an actual backtest had occurred on Wednesday, it wouldn’t have left any upside.

As we noted yesterday, by delaying the tag ES now has the opportunity to backtest the latest little rising white channel but at a price higher than the SMA200. If an actual backtest had occurred on Wednesday, it wouldn’t have left any upside.

We can say the same about SPX.

We can say the same about SPX.

The currency picture is looking fairly bearish, with USDJPY’s rising wedge threatening a breakdown…

The currency picture is looking fairly bearish, with USDJPY’s rising wedge threatening a breakdown… …and EURUSD’s slump…

…and EURUSD’s slump…  …hinting at that DXY spike we’ve been expecting.

…hinting at that DXY spike we’ve been expecting.  NKD continues to sound the alarm. Its chart looks quite bearish. And, as we discussed several days ago, it’s highly unusual for it to reverse without the overall market going with.

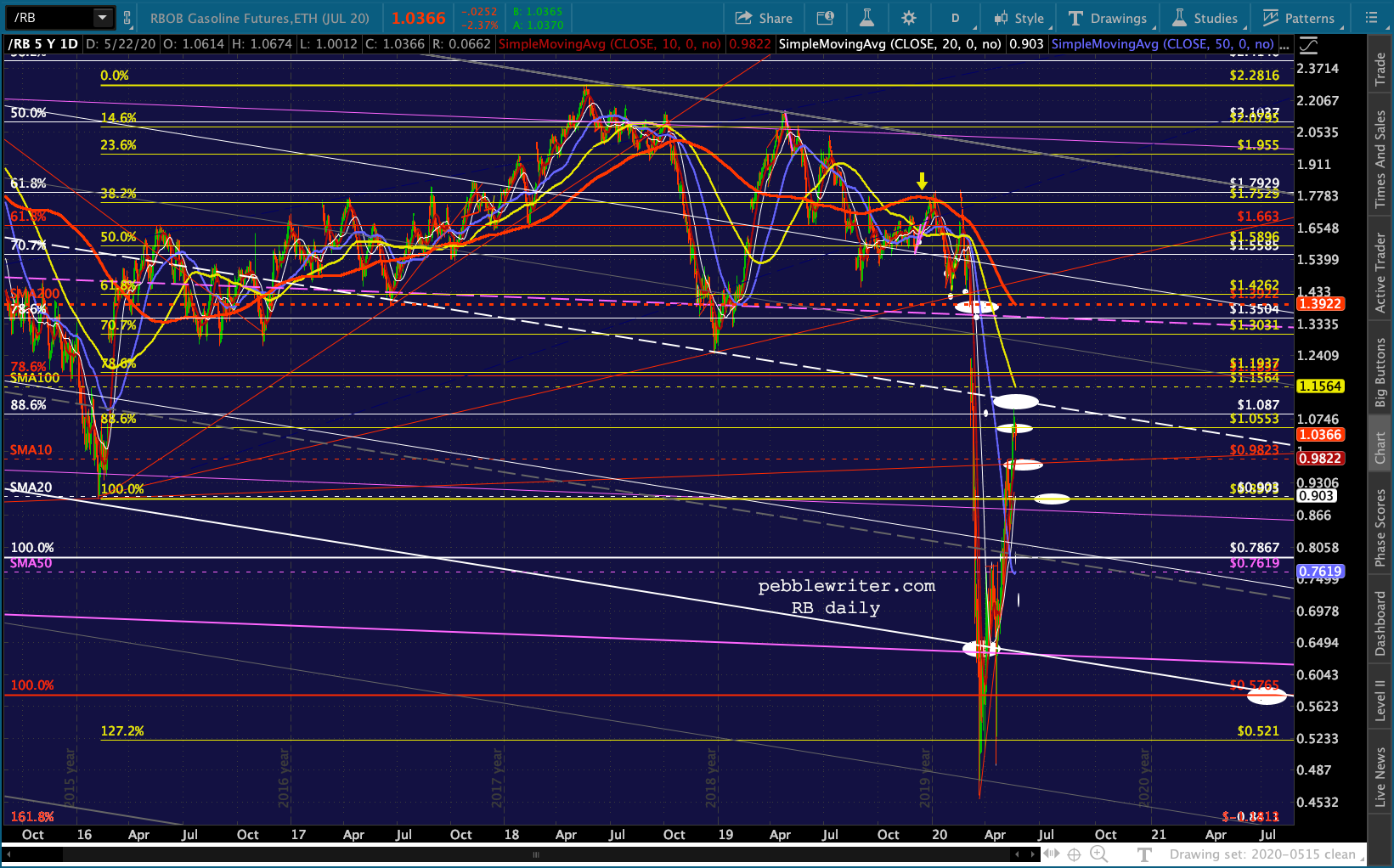

NKD continues to sound the alarm. Its chart looks quite bearish. And, as we discussed several days ago, it’s highly unusual for it to reverse without the overall market going with. RB and CL are both showing weakness – with RB possibly having already peaked.

RB and CL are both showing weakness – with RB possibly having already peaked.

The bond market continues to slumber…

The bond market continues to slumber…

…with the 10Y chart continuing to send bearish vibes…

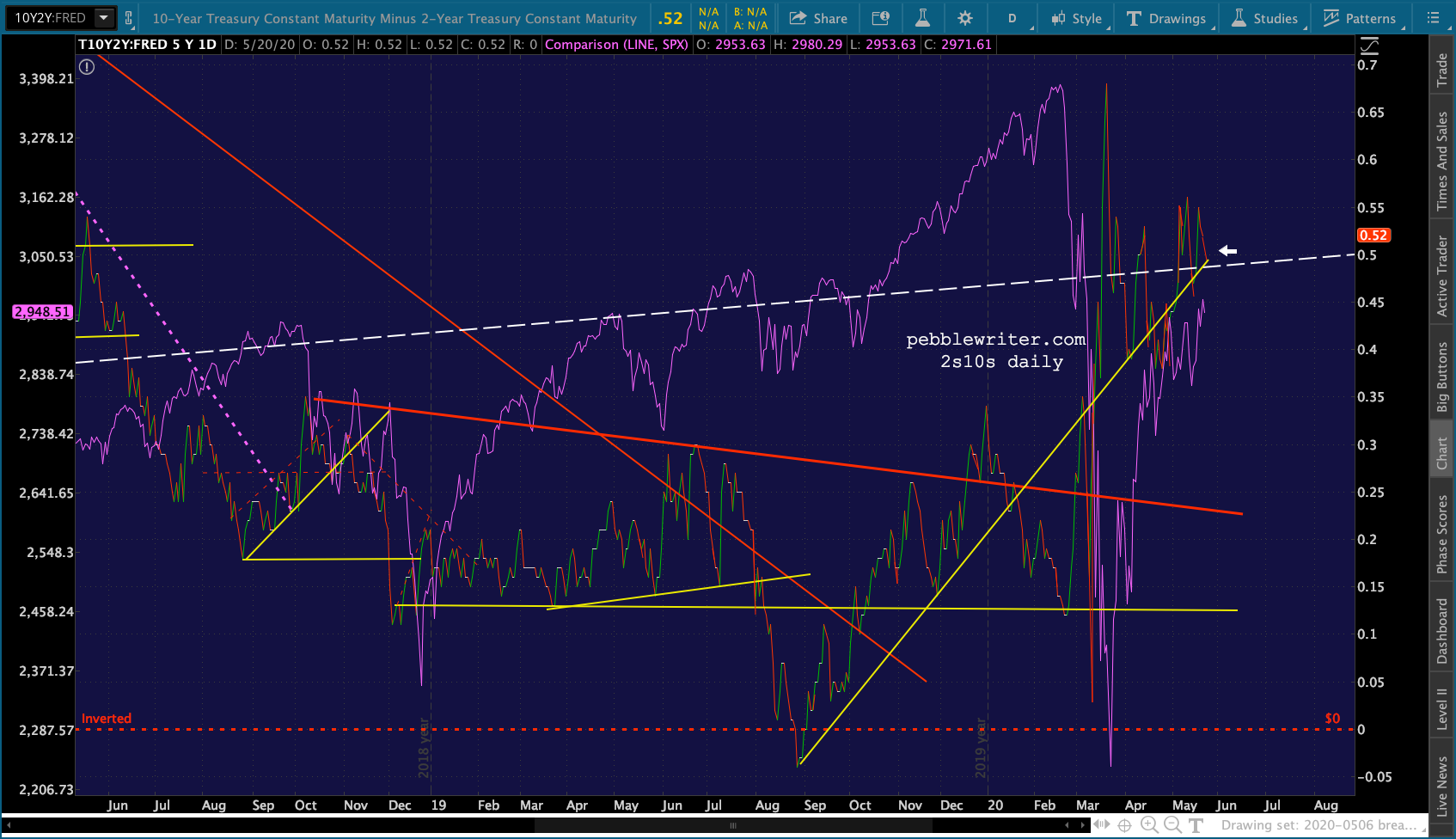

…and the 2s10s continuing to coil. A breakout or breakdown would be bearish for stocks.

…and the 2s10s continuing to coil. A breakout or breakdown would be bearish for stocks.

Note that bellcow AAPL has backed off its breakout…

Note that bellcow AAPL has backed off its breakout… …and DB has backed off its SMA200 attempt.

…and DB has backed off its SMA200 attempt.

Even DJI failed to make a new cycle high or pushed through its channel mideline and hasn’t made much progress since pushing through its SMA200 (which it lost several times.)

Even DJI failed to make a new cycle high or pushed through its channel mideline and hasn’t made much progress since pushing through its SMA200 (which it lost several times.)

Bottom line, looking at the charts there are all sorts of reasons to suspect the overall market is about to tumble. The fundamental reasons to tumble are also painfully obvious.

But, time and time again, we’ve seen holiday weekends result in gaps up over important overhead resistance. And, last I heard, the Fed and the Treasury aren’t taking their feet off the gas.

We have plenty of important economic data coming up next week, but nothing that’s necessarily more important than the data the market has flat-out ignored for the past two months…

…unless the next GDP estimate is much worse than the initial one.

…unless the next GDP estimate is much worse than the initial one.

The other potential issue, of course, is the pandemic. If something should happen to throw the re-open narrative off course, that could throw the market for a loop. Thinking out loud, that could be a major city or state reversing their plans to open back up or a major uptick in cases/deaths in a part of the country that hasn’t yet been greatly affected.

The key levels to watch are the same as yesterday: ES/SPX’s .618s, their SMA10s, AAPL’s .886 at 314.71, VIX’s channel top at 32, the 2s10s breaking down or breaking out. Any of these things could mean a significant tumble for stocks with ES 2728 and SPX 2703 (7-8%) still representing strong downside targets.

Just for grins, let’s look back at the 2000 and 2007 tops. In 2000, once SPX dropped through its SMA200 it missed the opportunity 221 days later to properly backtest it.

After falling 10.8% from its 2007 highs and plunging through its SMA200, SPX had no trouble backtesting it and ultimately pushing above it for at least a few days. On it second drop through the SMA200, it shed 20.3% before attempting a backtest which, again, tagged the SMA200.

After falling 10.8% from its 2007 highs and plunging through its SMA200, SPX had no trouble backtesting it and ultimately pushing above it for at least a few days. On it second drop through the SMA200, it shed 20.3% before attempting a backtest which, again, tagged the SMA200.

This time, of course, it never pushed above it. It wouldn’t tag the SMA200 again until Jun 1, 2009 – three months and 258 points (38%) above its Mar 2009 lows.

During neither of those two instances, of course, did we have a Fed that was as activist and open about its intention to prop up equities.

UPDATE: 3:35 PM

This would be a lot easier if the Fed could just announce where they’d like SPX to close on Tuesday. Another day of going nowhere. Or, if you’re so inclined, another day of coiling.

Nothing has really changed at all. The potential for a gap higher and a breakdown are both still in place. I’d suggest a defensive position and a nice, long weekend without thinking about where the market will open on Tuesday.

Nothing has really changed at all. The potential for a gap higher and a breakdown are both still in place. I’d suggest a defensive position and a nice, long weekend without thinking about where the market will open on Tuesday.

I plan on updating the overall forecast, the big picture, a number of indices and currencies on Monday – possibly sooner. In the meantime, I wish everyone a safe and enjoyable holiday weekend.

I plan on updating the overall forecast, the big picture, a number of indices and currencies on Monday – possibly sooner. In the meantime, I wish everyone a safe and enjoyable holiday weekend.