If you’ve enjoyed the past few days, you’ll probably enjoy today as well. The market seems to be in maintenance mode, with just enough algo-juicing to prevent anything really nasty, but not quite enough to make any meaningful headway.

Yes, VIX, I’m looking at you.

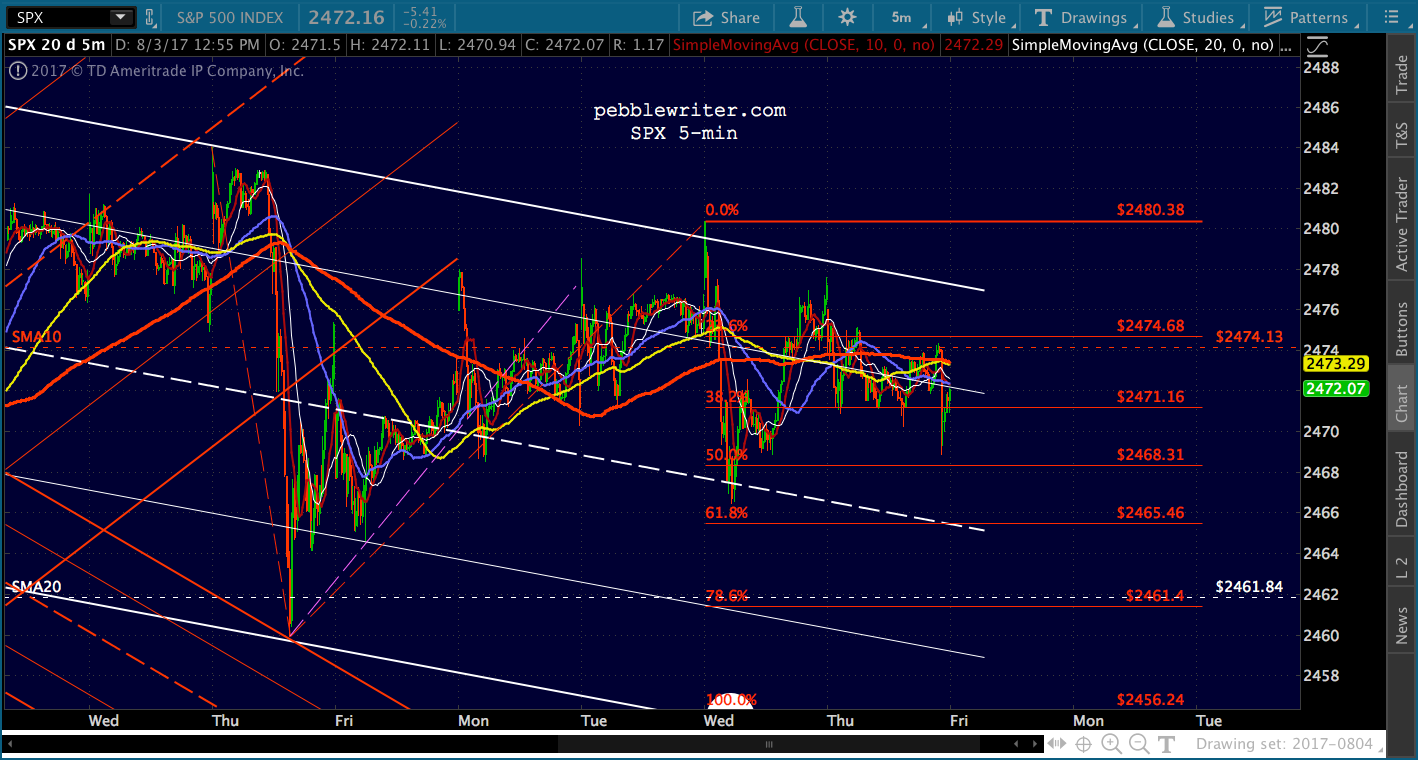

continued for members…

continued for members…

There’s nothing terribly new to report overnight. The payroll data was more positive than most expected, with better wage growth and a lower unemployment number. Some might argue that this removes some of the impetus for easing. But, to listen to the Fed, things were already going great. Chalk this up as another potentially inconvenient data point.

The dollar continues to slip a little lower, with the channel line still looking like the next target. This jibes well with a an interesting target in USDJPY at 109.457.

The dollar continues to slip a little lower, with the channel line still looking like the next target. This jibes well with a an interesting target in USDJPY at 109.457.

Oil is holding on to a fairly tight range so far. As we discussed a few days ago, sharp reversals at its tops have not been a hallmark of CL price patterns. If equity weakness seems to be a threat, look for the downturn to take some time.

Oil is holding on to a fairly tight range so far. As we discussed a few days ago, sharp reversals at its tops have not been a hallmark of CL price patterns. If equity weakness seems to be a threat, look for the downturn to take some time.

If we look at moving averages ytd, we can see a pretty clear pattern of rescuing SPX every time it dips below the SMA10, with the SMA20 serving as important support and the SMA50 as the backup for the SMA20.

If we look at moving averages ytd, we can see a pretty clear pattern of rescuing SPX every time it dips below the SMA10, with the SMA20 serving as important support and the SMA50 as the backup for the SMA20.

The other observation I’d make is that it’s now been almost 9 months since a SMA100 tag. The last time SPX went 9 months without a SMA100 tag was from Apr 21, 2009 to Jan 27, 2010. The end of that stretch was marked by a price pattern very similar to that of the past few weeks.

The other observation I’d make is that it’s now been almost 9 months since a SMA100 tag. The last time SPX went 9 months without a SMA100 tag was from Apr 21, 2009 to Jan 27, 2010. The end of that stretch was marked by a price pattern very similar to that of the past few weeks.

Of course, there was an (arguably more important) SMA200 tag in the midst of that stretch which, from all appearances, represented a concerted effort to get and keep SPX back above the SMA200.

Of course, there was an (arguably more important) SMA200 tag in the midst of that stretch which, from all appearances, represented a concerted effort to get and keep SPX back above the SMA200.

The longest stretch right before that one? Glad you asked. I would be hard pressed to make a case for a 520-pt plunge here, simply because central banks have become so adept at propping up equities. In my opinion, there have been four distinct phases of support.

I would be hard pressed to make a case for a 520-pt plunge here, simply because central banks have become so adept at propping up equities. In my opinion, there have been four distinct phases of support.

I. QE was a blunt force instrument that required trillions of dollars and was hardly precise.

II. The yen carry trade came next, and was relatively precise and very effective. But, it had nasty side effects in that it resulted in very high oil and gas prices for Japan.

III. After the yen bottomed out, oil was effective during its move from 26 to 55. But, the resulting 2.7% CPI was problematic in that it shook investors’ belief in the Fed’s motivation to continue accommodative policy.

IV. VIX bashing has been very effective and is a relatively victimless crime. However, there is probably a limit to how low it can go before even the algos consider its moves ridiculous. And, eventually, the algos might care that there is no “there” there.

In other words, if it gradually cycles lower every day, does it really have any medium- or longer-term implications. The real value is in breaking trend: dipping below support, etc. We’re in a stage, now, where central banks are using VIX in combination with the above tools to prop up stocks.

Lately, this has meant ramping up oil prices in order so that CPI can climb back out of the cellar. Assuming they don’t want CPI to get out of hand, it’s probably now time to let CL drift lower, in order to produce a more accommodation-friendly CPI number. If so, we should expect to see the USDJPY bottom out fairly soon.

A few years ago, suggesting the above was considered grounds for a stay in a padded room. Even as recently as a year ago, it regularly earned me a fair amount of scorn and ridicule.

During my recent 2-week stretch of meetings with portfolio managers, analysts, strategists, etc., not a single one argued with me. A few were skeptical enough to lift an eyebrow. But, the majority looked like they were having a light bulb moment. I believe that for many of them, they finally had an explanation that helped everything make sense.

more later…