It’s pretty interesting that today — one day before the expected cyclical low of our USDJPY-based analog — is the day that Abe’s close advisor Koichi Hamada chose to announce that the yen should increase in value to 105 to the dollar versus the current 120ish. For more on Hamada’s views, check out THIS VIDEO.

The USDJPY’s reaction was swift and unambiguous — though, just as quickly, the pair popped right back to the yellow .618 at 120.11. Is it just a backtest, or something more troubling for Abe and friends?

The futures reacted mildly, but what if carry-traders should get the idea that Abe intends to end the free ride? Would they meekly ride off into the sunset, or would they stand their ground?At the end of the day, who really controls the USDJPY? This is a question the “market” will decide for us. And, given that all of the currency pairs we chart are at important inflection points, it will be a very interesting next couple of days.

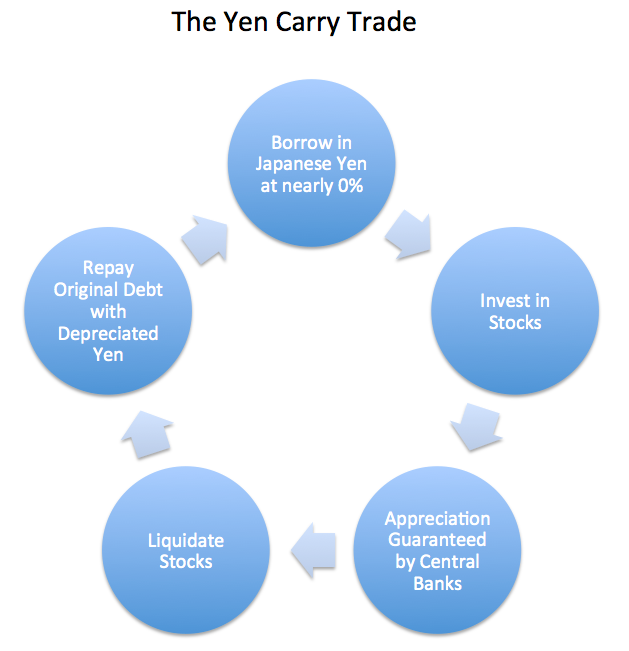

If I loaned you $100 with the understanding you would only have to repay me $75, would you take that deal? What if I charged only 1/10th of 1% interest? What if I threw in an investment vehicle where you could put that $100 and be guaranteed by the government never to lose any money?

Meet the yen carry trade — the primary driver of higher equity prices since at least October 2011. We’ll take a look at how it works, and how it has distorted both equity and debt markets worldwide.

Basics of a Carry Trade

Generically speaking, a carry trade is an arbitrage that involves borrowing cheap and investing rich. In the old days, it usually meant borrowing at a low interest rate (e.g. yen) and investing at a higher interest rate (e.g. US dollars.)

One major risk, of course, was that the currency in which one invested would depreciate — resulting in a higher cost when the time came to repay the borrowing. Given how quickly currency markets move, it could turn a profitable trade into an unprofitable one in a heartbeat.

The Bank of Japan eliminated that risk when it repeatedly assured investors that the yen would continue to fall in value relative to the US dollar. A drop, for example, from 75 to 100 yen per dollar (expressed as an increase from 75 to 100 in USDJPY) represented a major opportunity for investors.

A SIMPLE EXAMPLE:

borrow $100 million in yen (7.5 trillion yen) at essentially 0%

reinvest in T-bills at 10 bps

the T-bills mature in a year, returning $100MM and interest of $100,000

repay the 7.5 trillion yen, which now costs $75 million in US dollars

pocket the $25 million (plus the $100,000 interest!)

A $25 million return on a $100 million investment (25%) ain’t too shabby. It’s downright enormous when the initial investment is a loan collateralized by treasuries or other securities you already own. If the collateral impairment were 5%, for example, the annualized ROI would clock in at 400%.

If a 25% gain seems unlikely, consider that USDJPY rose over 60% between 2011 and 2014. In fact, it rose nearly 25% between Nov 2012 and May 2013 alone.

Most investors would be very satisfied with a 25% return, let alone a 400% return. But, that’s just the tip of the iceberg. Suppose that, instead of investing that $100 million in T-bills at a 10bps guaranteed return (plus the enormous currency benefit), an investor put that money into stocks.

Not Your Father’s Market

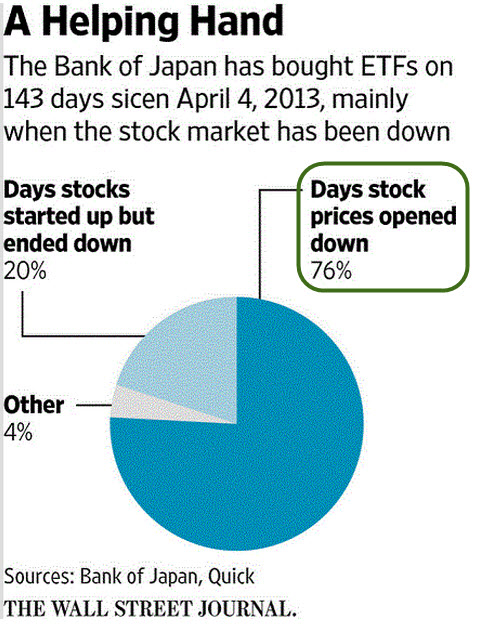

I know what you’re thinking: “what about the risk? Stocks go up…but, they also go down!” Don’t worry. The world’s central bankers have got you covered. The Bank of Japan, for instance, puts nearly 5% of its $720 billion in annual quantitative easing into stocks. It’s not a steady stream — just when the “market” needs a boost.

Don’t take my word for it. According to those tin foil hat-wearers at the Wall Street Journal, 97% of the days the Bank of Japan “invested” money into stocks were days that the market either opened lower, or reversed to close lower after initially opening higher. The Plunge Protection Team at your service.

Last October, the government decided to up the ante, increasing the share of equities in its $1.2 trillion employee pension plan (the GPIF — the largest in the world) to 25% for Japanese stocks and 25% for international stocks. Note that this is money which retiring Japanese public employees might want to use some day to, you know, retire.

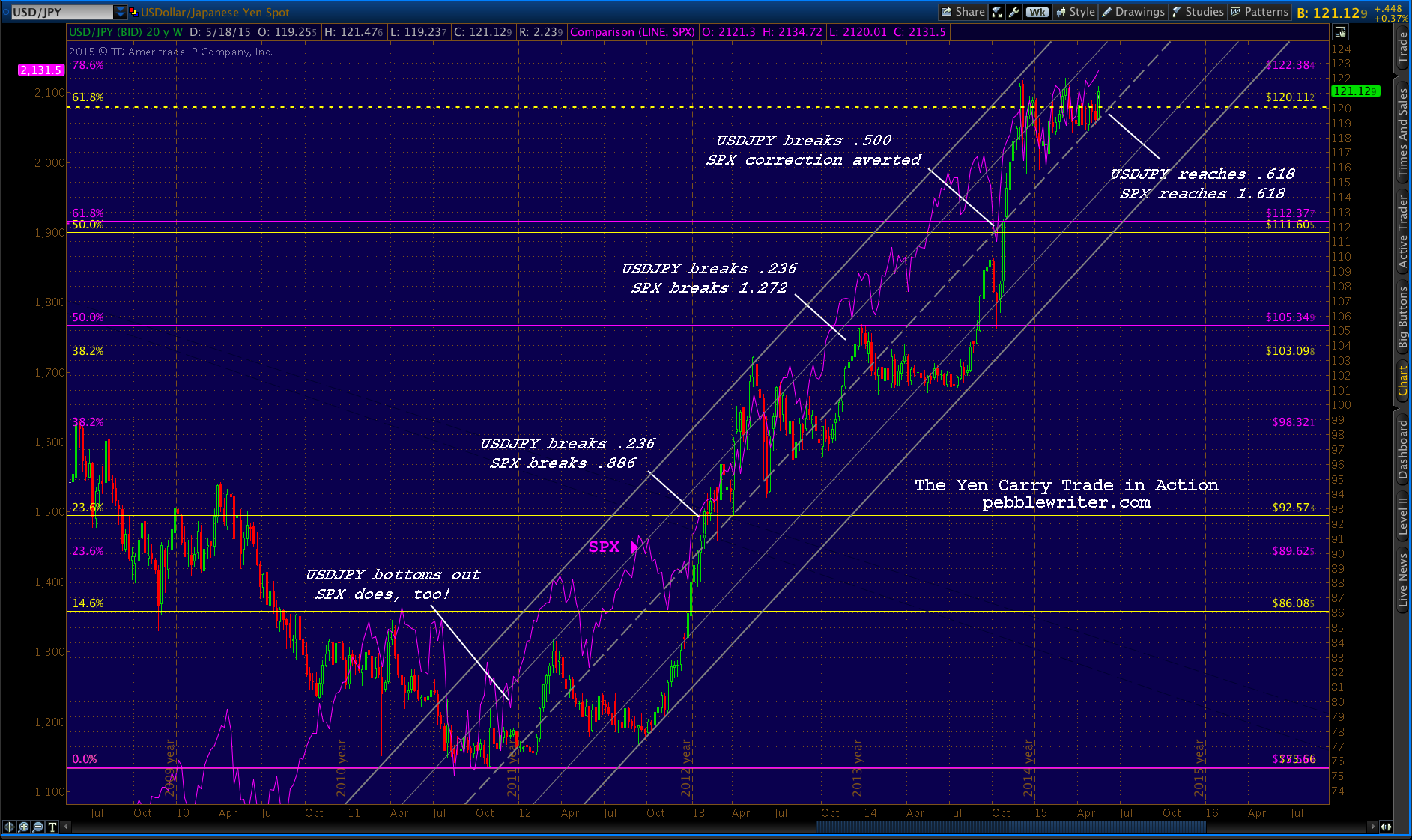

What effect has it had? Judge for yourself…

USDJPY v SPX / updated May 20, 2015

The Downside

If the yen carry trade seems like a win-win, look at it from the standpoint of the Japanese. As a small, island nation that imports much of what it consumes, Japan is quite sensitive to changes in the price of imported items like raw materials, food and oil.

Ceteris paribus, a drop from 75 to 125 yen per dollar would increase the price of oil (traded in US dollars) by a whopping 66%. Knowing this, it’s not so hard to figure out why oil prices crashed beginning in August 2014 — at exactly the same time that USDJPY shot up through long-term resistance.But, that’s another story…

The fact is that continued depreciation of the yen will cost the Japanese people as well as those corporations which rely on imported goods. So, the next time the BOJ clobbers the yen, it does so with the knowledge that for every winner, there are many, many losers. There is no free lunch.

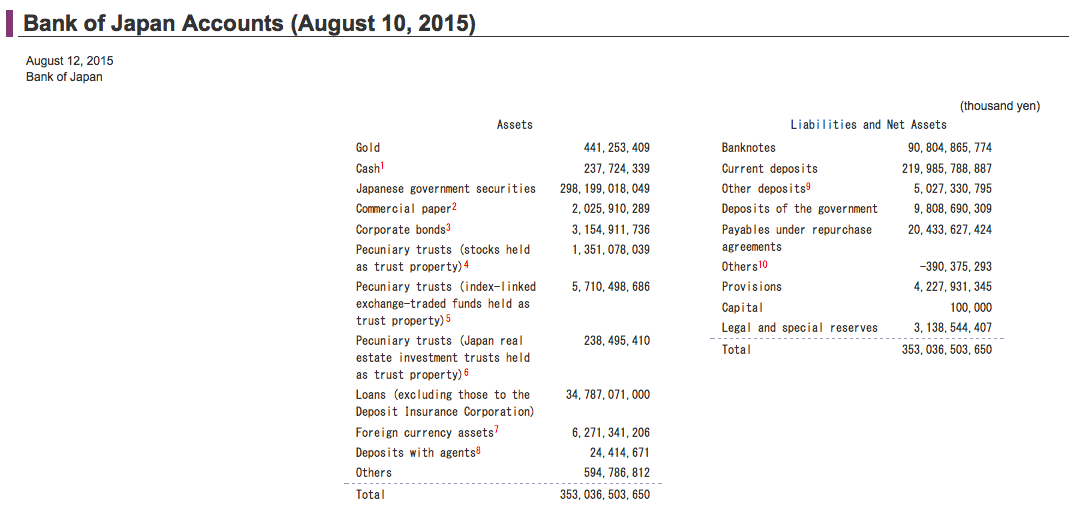

If that’s the case, why not just stop? The most recent data shows the BOJ owns almost ¥7 trillion in stocks. The ¥140 trillion Government Pension Investment Fund has allocated 50% of its assets to stocks. Let’s round it off and say the bank/government of Japan has a heavily-margined (note their tiny capital position below) position of ¥80 trillion ($666 billion) in equities.

First, note that this almost exactly the amount of annual easing that was announced in last October’s QQE expansion.

More importantly, it leaves Japan in a must-win situation. At its lows yesterday, August 24, the Nikkei 225 was off 9.5% from Friday’s close. It’s off a full 18% in less than 2 weeks.

If all of that $666 billion were in the Nikkei, the last two weeks’ exposure to equities would have cost them $120 billion — 2.4% of GDP!

Sure, some of it’s on the books of the pension plan, and the rest is presumably not going to be realized anytime soon. But, the data illustrate just how vulnerable Japan is since it: (1) put that much money into stocks; and, (2) is doing so in such a leveraged fashion.

At the end of the day, taking on this much risk smacks of desperation. With over 40% (and growing) of its borrowings going to pay interest on existing borrowings, and 250% of its GDP in debt, don’t expect things to change anytime soon. And, don’t expect the BOJ to sit idly by and allow the equity spiral to grow out of control.

They will increase QQE and/or devalue the yen again, and soon.

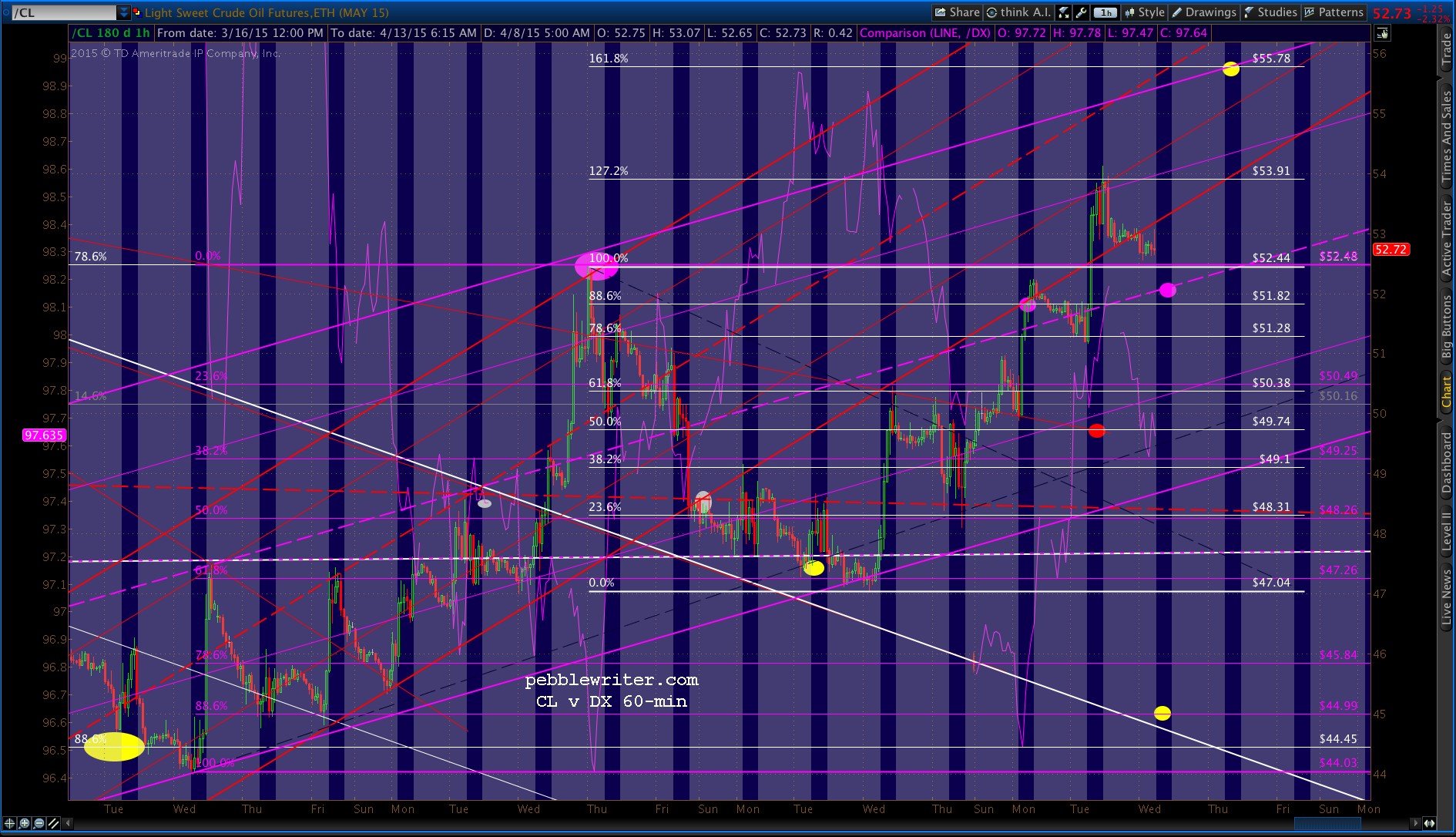

We’ve noted over the past several weeks that only a decline in EURUSD would permit both CL and USDJPY (and hence equities) to sell off at the same time. So yesterday’s failure of EURUSD’s rising purple channel is potentially significant.

To recap, USDJPY’s rallies almost always drive stocks higher — whether or not they last, and despite the fact that they are entirely and openly manipulated by the BoJ and other central banks — not to mention large HFT traders/hedge funds.

CL has joined the algo game over the past several weeks — also driving stocks higher when it rallies. But, it is very highly negatively correlated with the USD dollar.

So, a rally in CL drives DX lower which, everything else being equal, should drive USDJPY lower — unless it’s propped up, which it usually is. Result: rising stock prices.

A decline in CL drives DX higher, which — all else equal — drives USDJPY higher. Result: higher stock prices.

When EURUSD declines, however, DX can strengthen even while the yen strengthens (USDJPY falls.) This sets the stage for CL and USDJPY to fall at the same time, and take ES/SPX with them.

Only a trading halt prevented a truly ugly close and a slip back below the moving averages. Funny how often that happens, and so rarely when stocks are rallying sharply…

This morning, USDJPY remains above the falling red channel, CL remains above the white .786 Fib and SPX remains above its 10, 20 and 50-day moving averages. So, no harm done — yet.

Another day, another central banker propping up the markets…

So, Dudley isn’t so sure that the recovery is exhibiting the strength necessary to allow the Fed to raise rates? What a huge surprise — except to our regular readers (not so sure about the irregular ones…)

The Fed can’t afford a rate increase any more than they can a rebound in oil prices, a slump in the dollar, normalization of stock valuations, requiring banks to markU securities to market, etc.

CL ran out of room at the .886 as expected……though USDJPY was happy to take up the slack. Unfortunately, it has also run into overhead resistance — at the yellow .618 at 120.11.Futures are maintaining yesterday’s CL-driven rally highs, but weren’t able to break through the TL from October. Together with USDJPY and CL topping out, not a great sign for bulls…One potential ray of hope comes from across the pond.

Our analog is right on track, with USDJPY closing below its 100-day moving average on Friday and again on Sunday.Aside from the 2-day delay to accommodate the month and quarter-end numbers, things are playing out as expected.

The eminis are off about 12 points from last Thursday’s close (SPX was closed Friday) and are backtesting the SMA100 after closing below it yesterday.

Today, we’ll find out just how the carry trade-followers react to a strengthening yen. The dollar is falling off as expected.

Will CL’s resulting overnight ramp job be enough to prop up the market?

EURUSD is doing its part, but is nearing its immediate upside potential.

As to SPX, our downside targets from Mar 30 [see: A New Analog, Part II] remain in place.

Looks like the initial targets for our analog should be set up by today’s currency and futures action — a day or two late, but reassuring all the same.

Yen and euro strength and dollar weakness are accompanying a 20-pt ES sell-off just like the good old days. Why? Crude light trading on Globex is closed for Good Friday, so CL is out of commission. DX is free to plunge without igniting CL and, thus, ES.

Will be fascinating to see whether or not USDJPY can close below its 100-day moving average (yellow) as the analog forecasts…

Yesterday’s evil plan was going so well… until CL-driven algos snuck in and unwound it all with a very impressive (even for it) ramp job. We’re left to wonder whether the purple channel might continue to hold, in which case it’s going to be tough for equity bears to make any headway. Note last night’s usual reset of the day’s ramp.

We discussed this last week. With DX and CL so strongly negatively correlated now, a bearish move in USDJPY (pair drops due to a stronger yen) results in a relatively weaker dollar, which facilitates CL’s rally, which tends to pull stocks higher. It’s a recipe for going nowhere fast — a.k.a. “chop.”

Bottom line, industry and OPEC have no interest in playing the HFT/algo game unless it results in higher oil prices — a result the central bankers cannot abide because it would pull the rug out from beneath Japan’s no-inflation meme. As long as a weaker yen is the basis for the biggest carry trade in the universe, this balance will not be upset.

SPX closed above its SMA100 again…

…as did USDJPY.

It was the perfect model of restraint until CL spiked. At that point, it felt the need to backtest the falling red channel top again.

We’ve slightly adjusted the channel to reflect the move. But, the objective remains the same — although delayed by a day.

In our January 27 update, we noted that 10-yr yields had backtested a broken channel bottom and appeared poised to fall further.

But, we also charted an important divergence between yields and stocks.

The last four major declines in yields were accompanied by declines in SPX ranging from 10% – 52%. This one was different:

The decline that began in January 2014 has lasted longer than any since the financial crisis. And, it’s about the same degree as the average of the others. Yet, it’s the only one accompanied by an increase in SPX — a whopping 14% increase, at that.

The difference, of course, is the stunning degree to which central banks have openly manipulated interest rates and currencies. The yen carry trade, in particular, has been the most important factor in stocks’ almost non-stop rally since 2011. We cover the effects in some detail in the latest posts on an analog we’re watching and will detail the carry trade itself in a coming post.

In the first week of February, rates had again fallen through support at 17.45 and SPX looked likely to complete the correction that had been aborted in mid-December. But, USDJPY shot up over 2% in 2 days, busting through its SMA10, 20 and 50 and a number of bearish chart patterns.Stocks rebounded sharply, of course, with yet another nonsensical snap-back rally that took SPX to new highs.

But, bonds also thumbed their nose at the usual charting rules. Yields shot right back through the broken red channel bottom, gaining 60 bps over the next six weeks. At 22.59, however, they ran into resistance from the falling purple channel top.

Not so coincidentally, USDJPY and oil were also running into channel resistance at the time. The upshot was a sharp decline for TNX that has since retraced a little over .618 of that spike from 16.51 to 22.59.

There is initial support at last week’s lows, and at 17.20 from both the red .886 and an interior (.236) purple channel line in the next day or two. The stronger support is white .886 Fib at 15.81. Due to the above-referenced transgression, TNX missed the opportunity to tag it in early March.

Our current analog calls for another opportunity around April 14, with the very good possibility of an overshoot to 14.90-15.10.

For those following along with our analog, today is day 232. Things appear to be right on track, and our downside targets are unchanged from Monday.

Today’s decline should be led by USDJPY. The daily chart looks fairly benign, while the 60-min shows the drama has already begun.

The eminis, currently off 4 at 2057, were as low as 2033.50 overnight — but, bounced back when USDJPY sought the refuge of the critical .618 Fib at 120.11.

Stocks should begin a more significant reaction today, but it should be modest compared to the weeks ahead.

The futures reacted mildly, but what if carry-traders should get the idea that Abe intends to end the free ride? Would they meekly ride off into the sunset, or would they stand their ground?

The futures reacted mildly, but what if carry-traders should get the idea that Abe intends to end the free ride? Would they meekly ride off into the sunset, or would they stand their ground? At the end of the day, who really controls the USDJPY? This is a question the “market” will decide for us. And, given that all of the currency pairs we chart are at important inflection points, it will be a very interesting next couple of days.

At the end of the day, who really controls the USDJPY? This is a question the “market” will decide for us. And, given that all of the currency pairs we chart are at important inflection points, it will be a very interesting next couple of days.