The good news is that PCE increased by only 6% in October (0.3% monthly) – down from 7% last summer. The bad news is that financial conditions remain quite loose, particularly from the standpoint of the 10Y, which has dropped from 4.33 on October 21 to as low as 3.57% this morning.

While algos not surprisingly jumped all over the “dovish” Fed outlook, is the prognosis really that rosy for inflation? Headline CPI will no doubt continue to fall as the YoY comparisons – especially in energy prices – moderate. But, consumers are still stuck with the higher prices of the day and wages which have definitely not kept up.

While algos not surprisingly jumped all over the “dovish” Fed outlook, is the prognosis really that rosy for inflation? Headline CPI will no doubt continue to fall as the YoY comparisons – especially in energy prices – moderate. But, consumers are still stuck with the higher prices of the day and wages which have definitely not kept up.

To the extent that the welfare of the average Joe matters, the Fed has not delivered. He must still pay much more for rent, food and transportation than he did last year. And, if he’s one of the thousands being laid off, the cost of those necessities will be even more excessive.

The 15 years of interest rate suppression pumped enormous liquidity into the system, money which – after it saved the banks’ bacon – created bubbles in virtually every investment market. The modest rise in rates over the past 9 months will do little to unwind the excess.

The Fed rightly fears an unwinding – more commonly known as a recession – thus the pivot. But, if it comes without a reset of overpriced necessities or an (unlikely) rise in real wages, the entire exercise will have been for nothing.

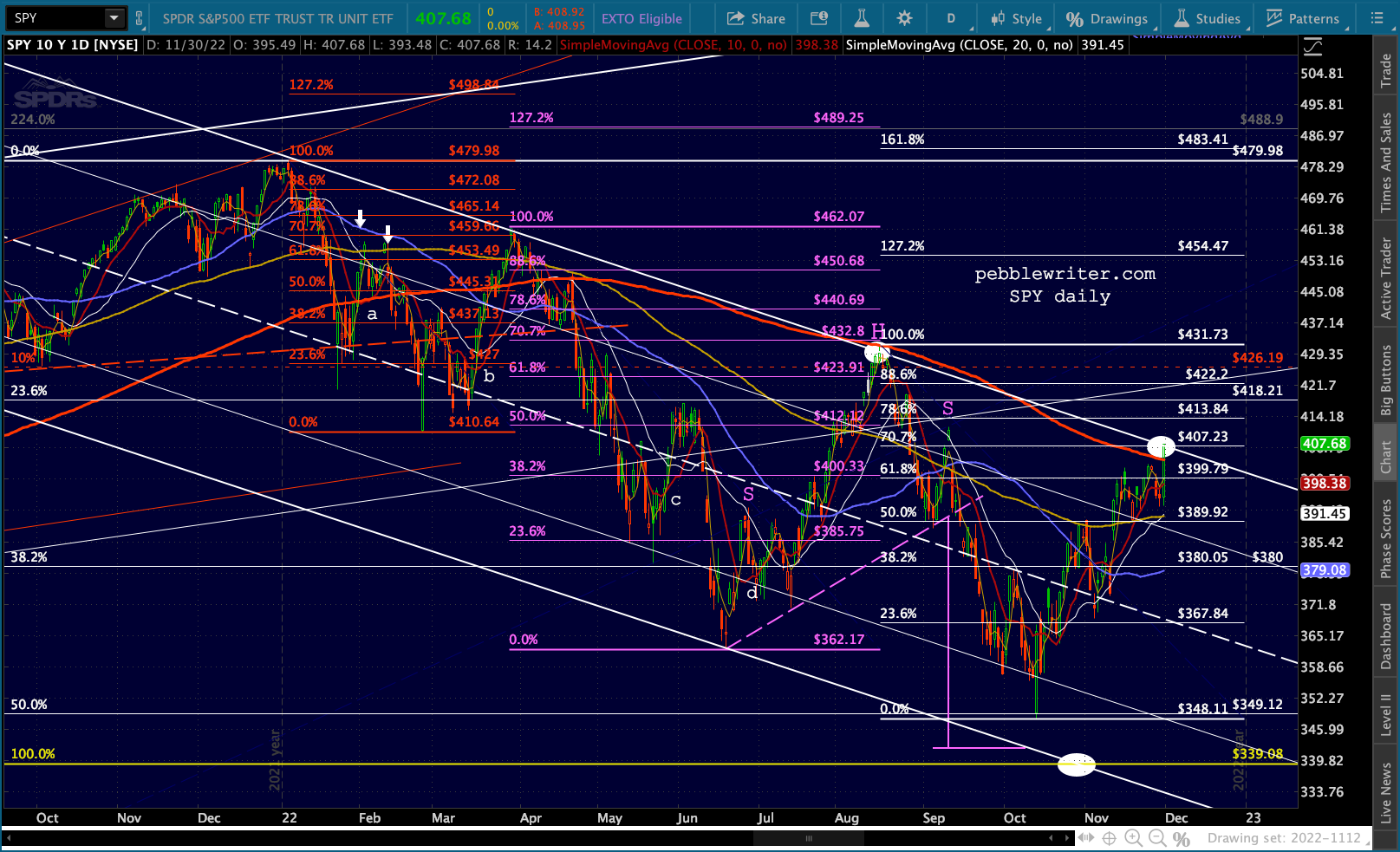

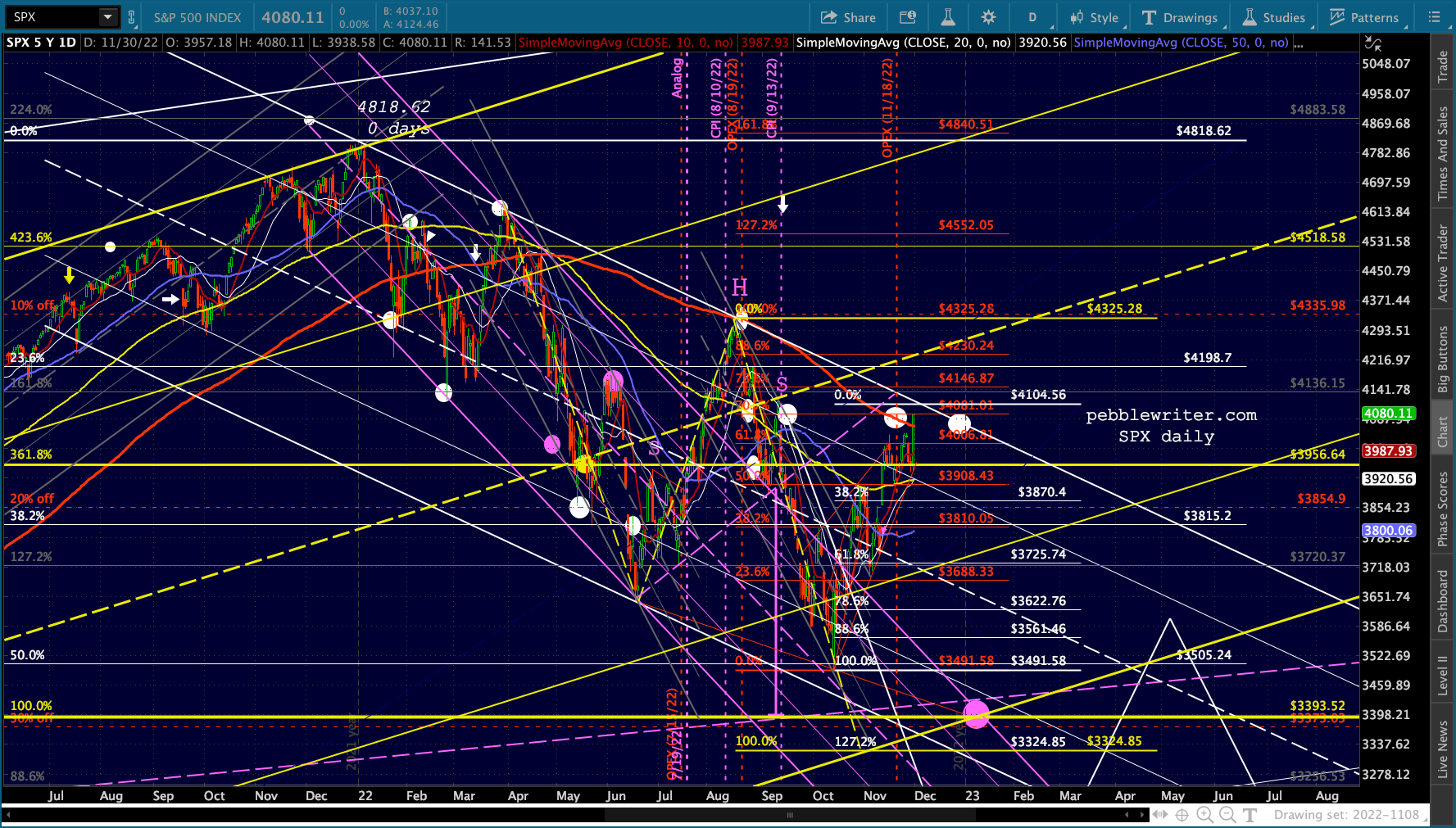

Yesterday, SPY nailed our target at the top of the falling white channel at the close.

The last time this happened, it touched off a 19.3% decline. It’s been a while since we had a nice “pop and drop”…

The last time this happened, it touched off a 19.3% decline. It’s been a while since we had a nice “pop and drop”…

continued for members…

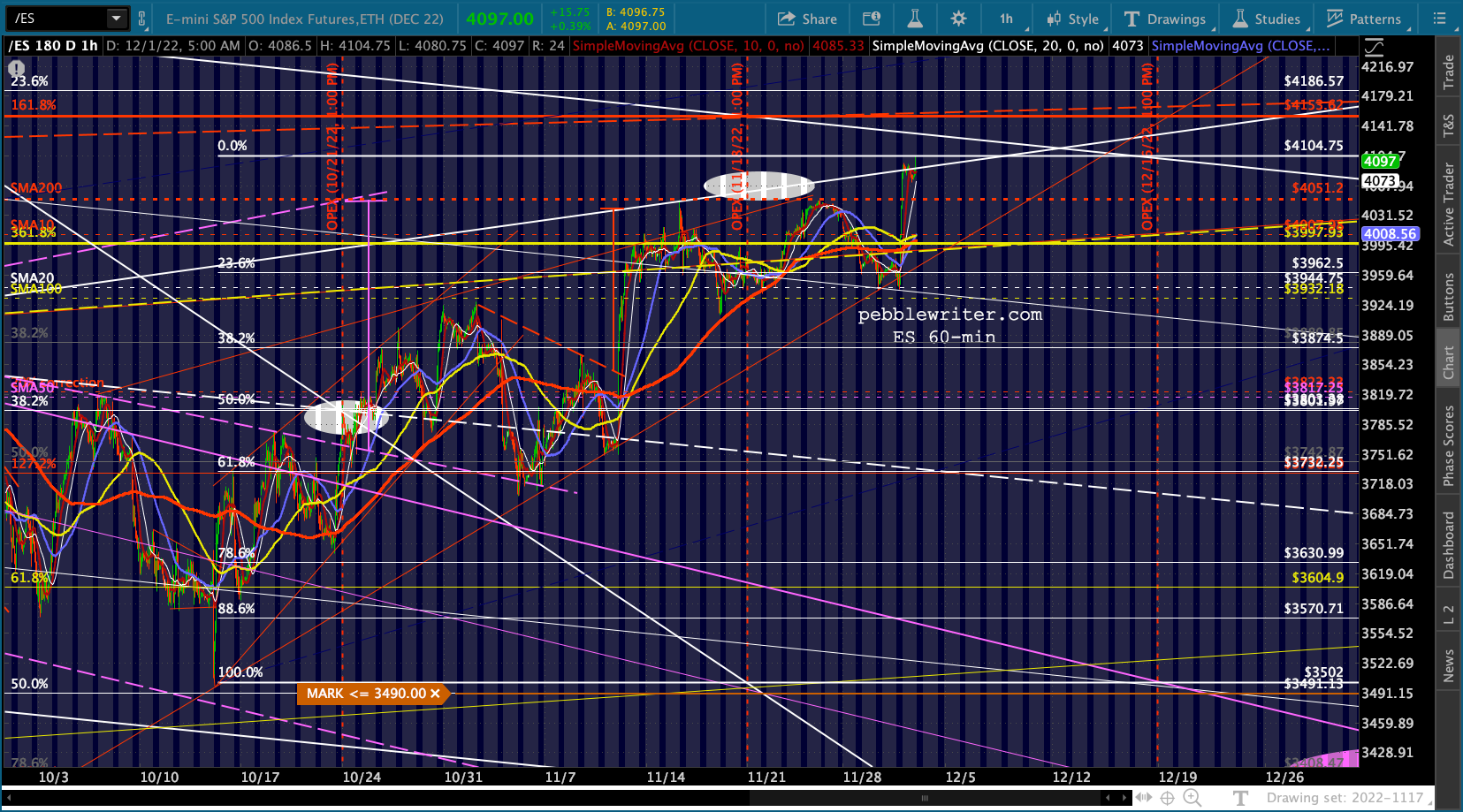

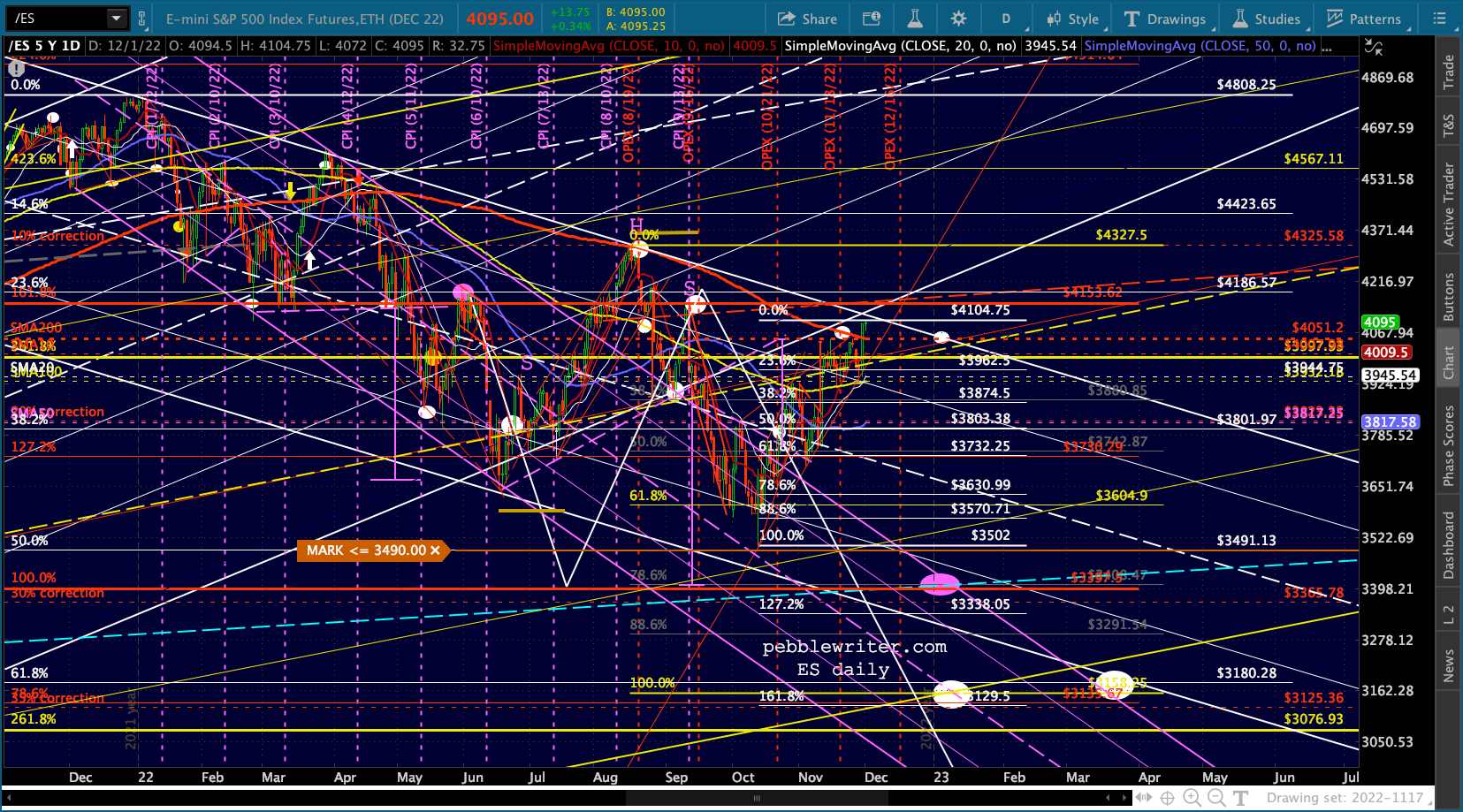

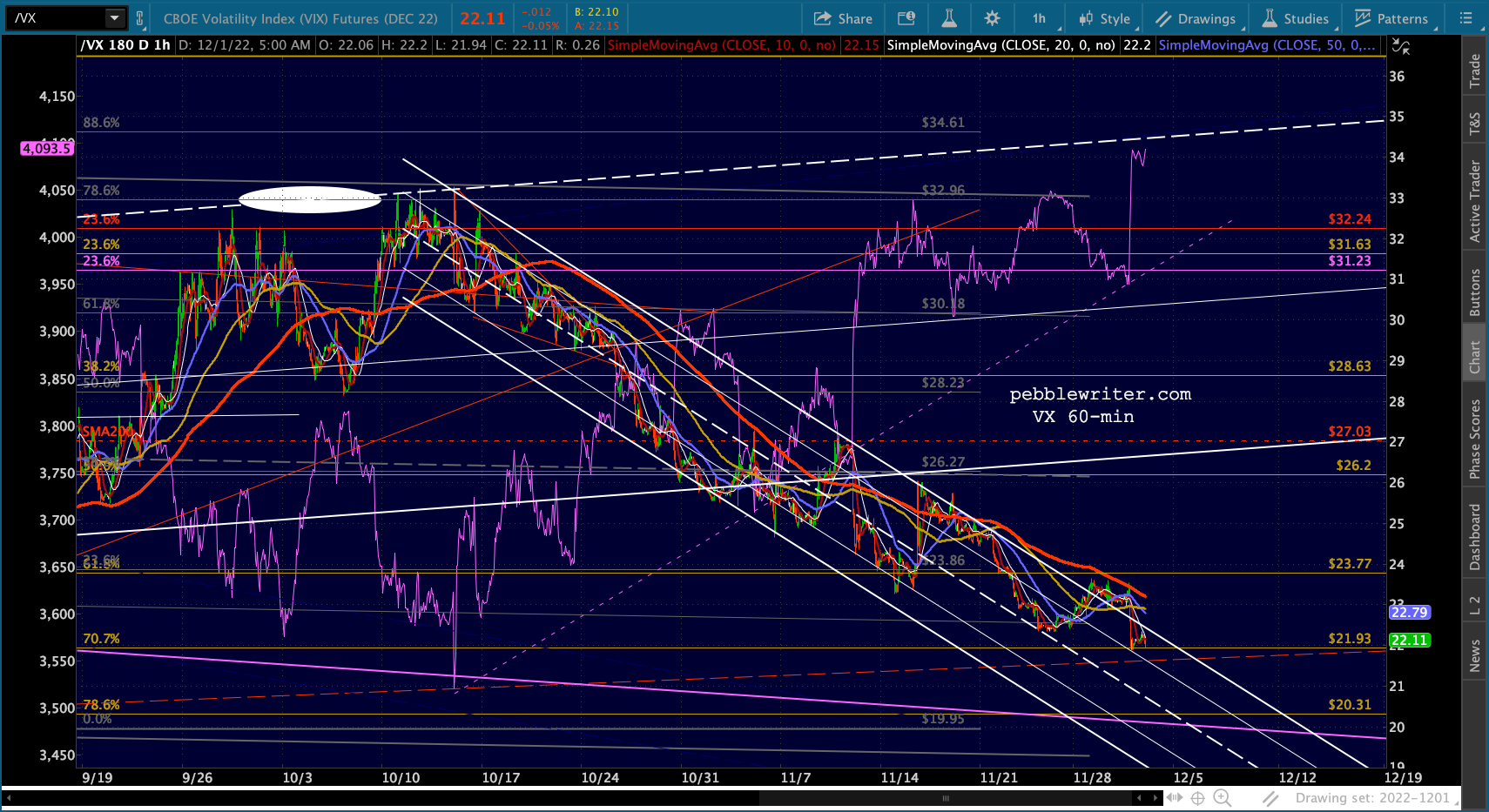

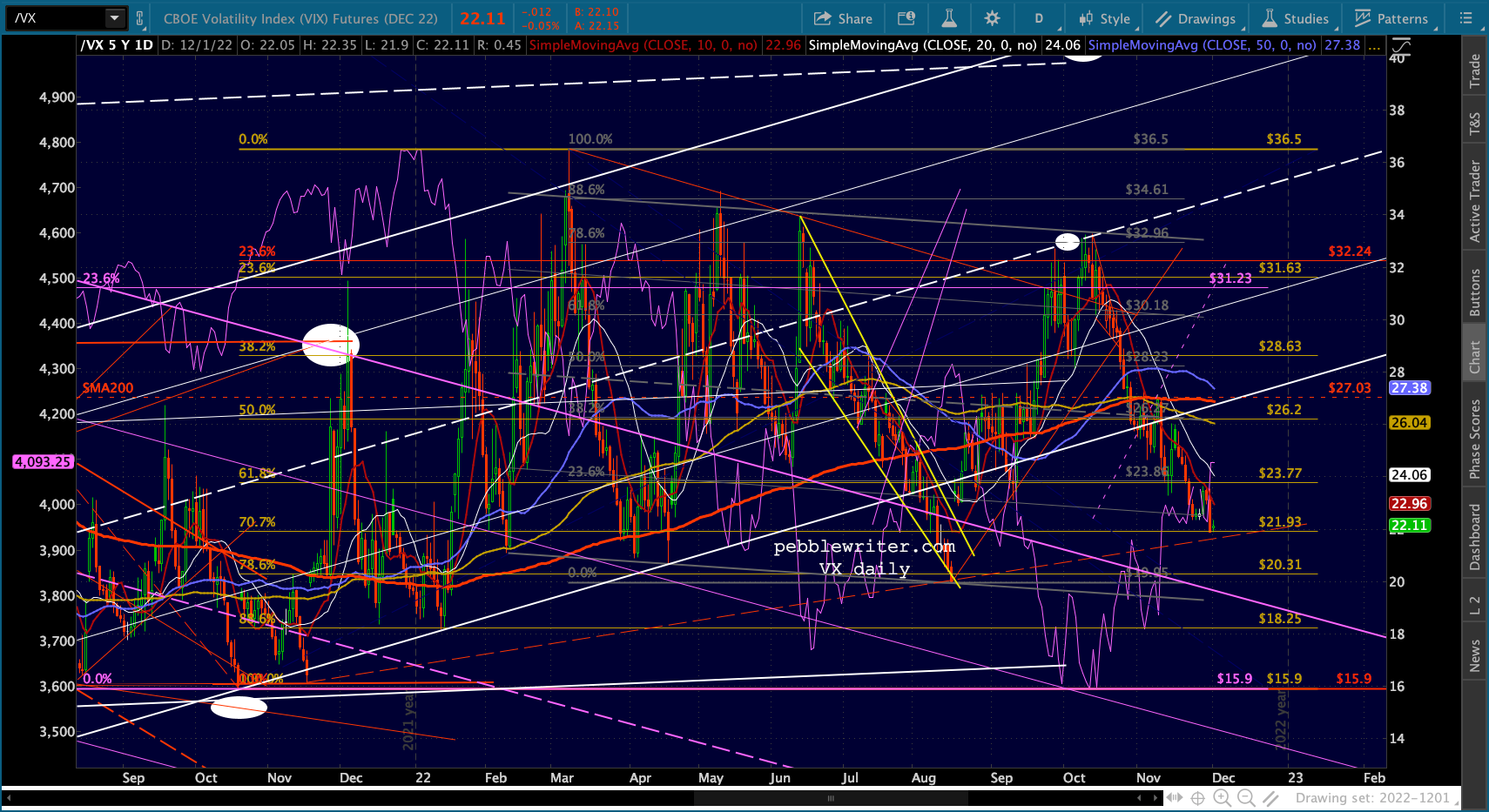

The bigger picture… …and the ES/SPX versions:

…and the ES/SPX versions:

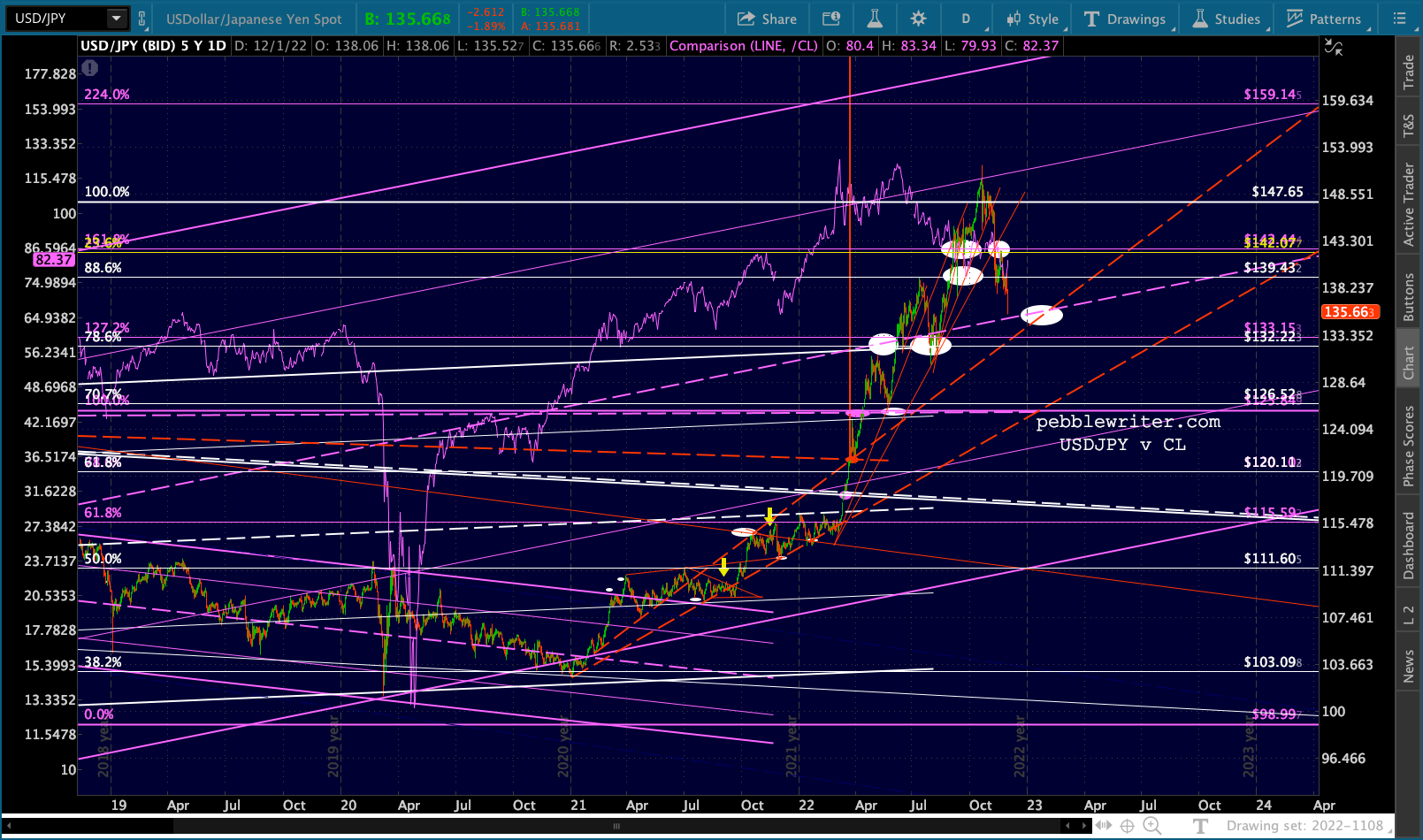

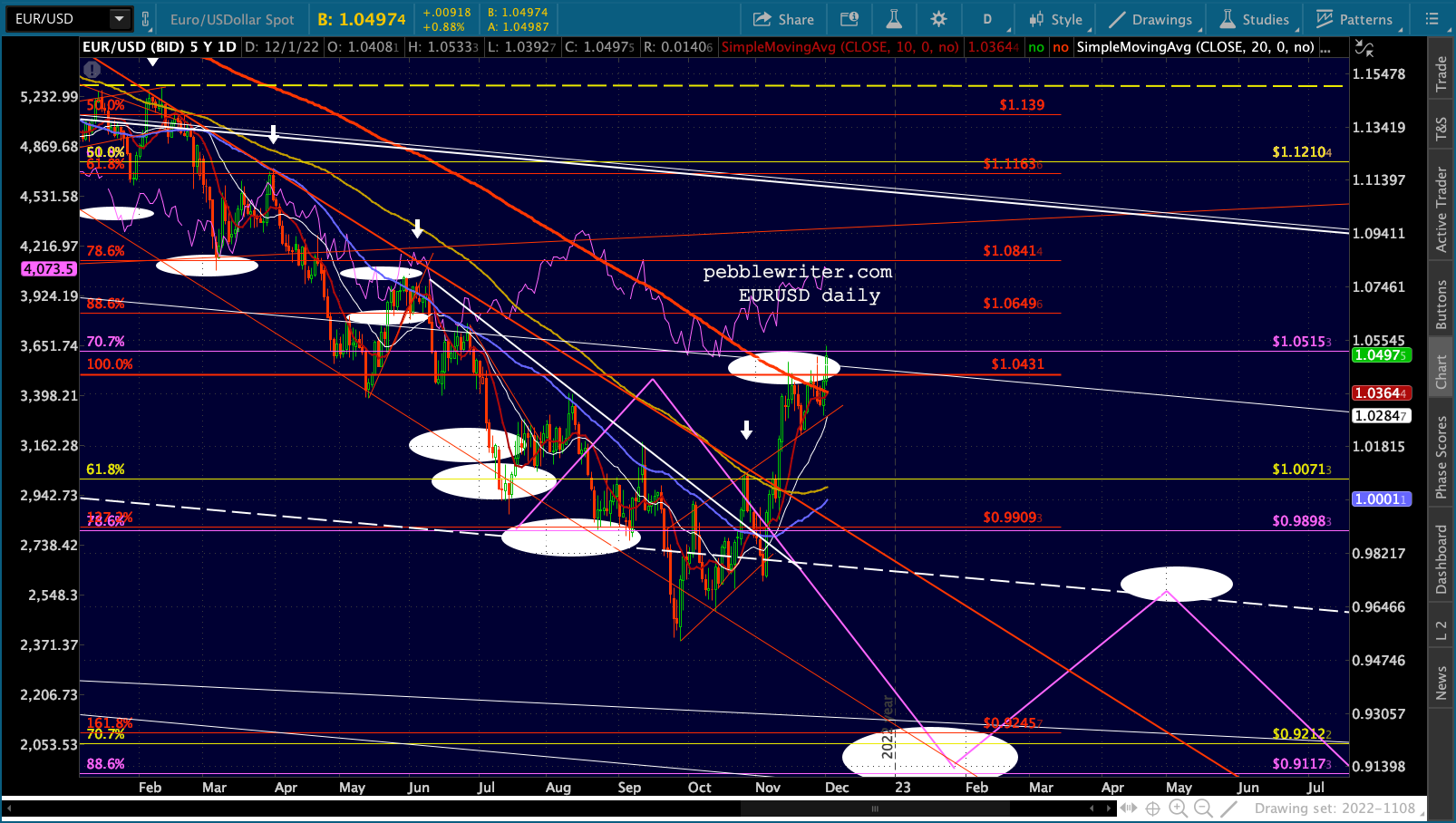

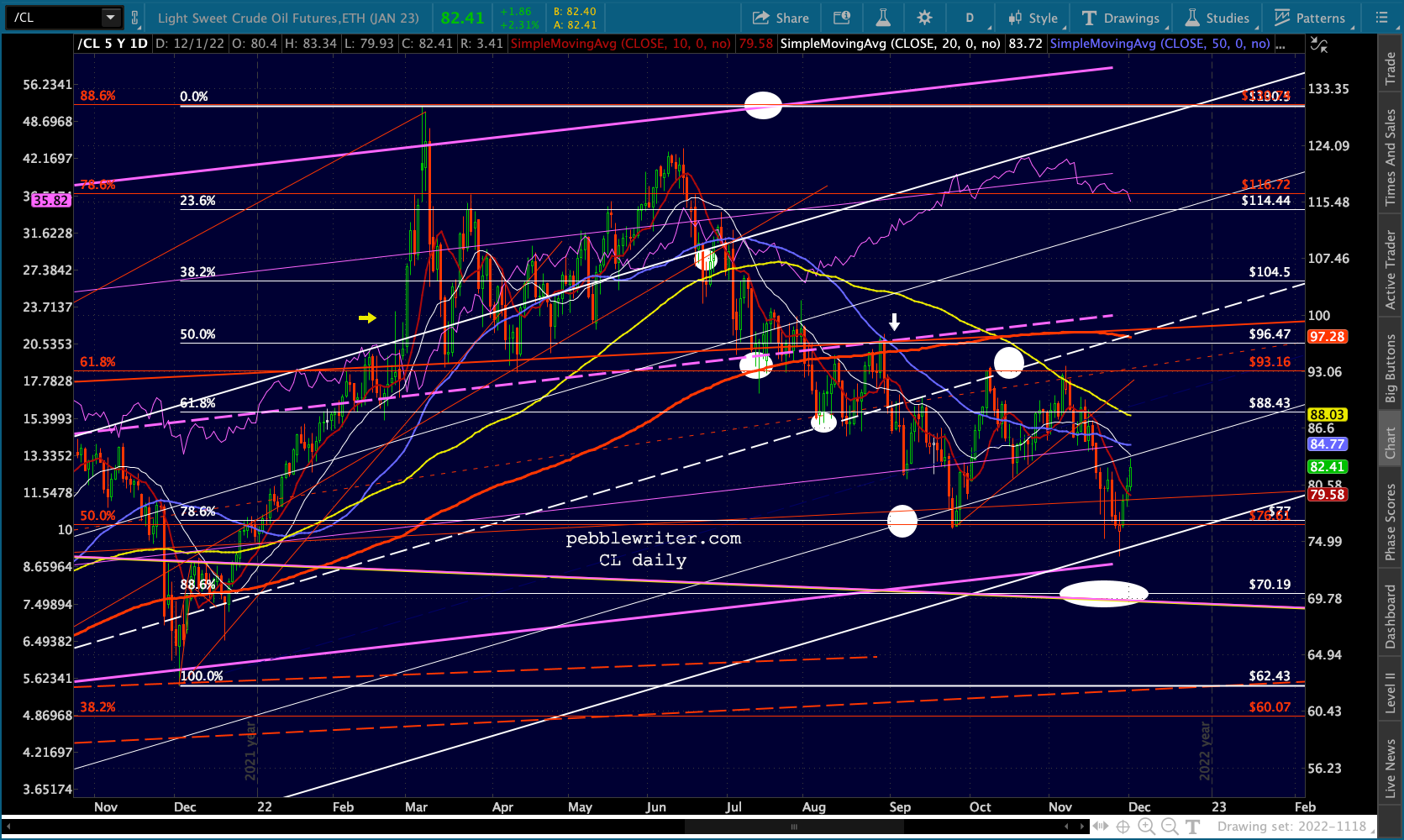

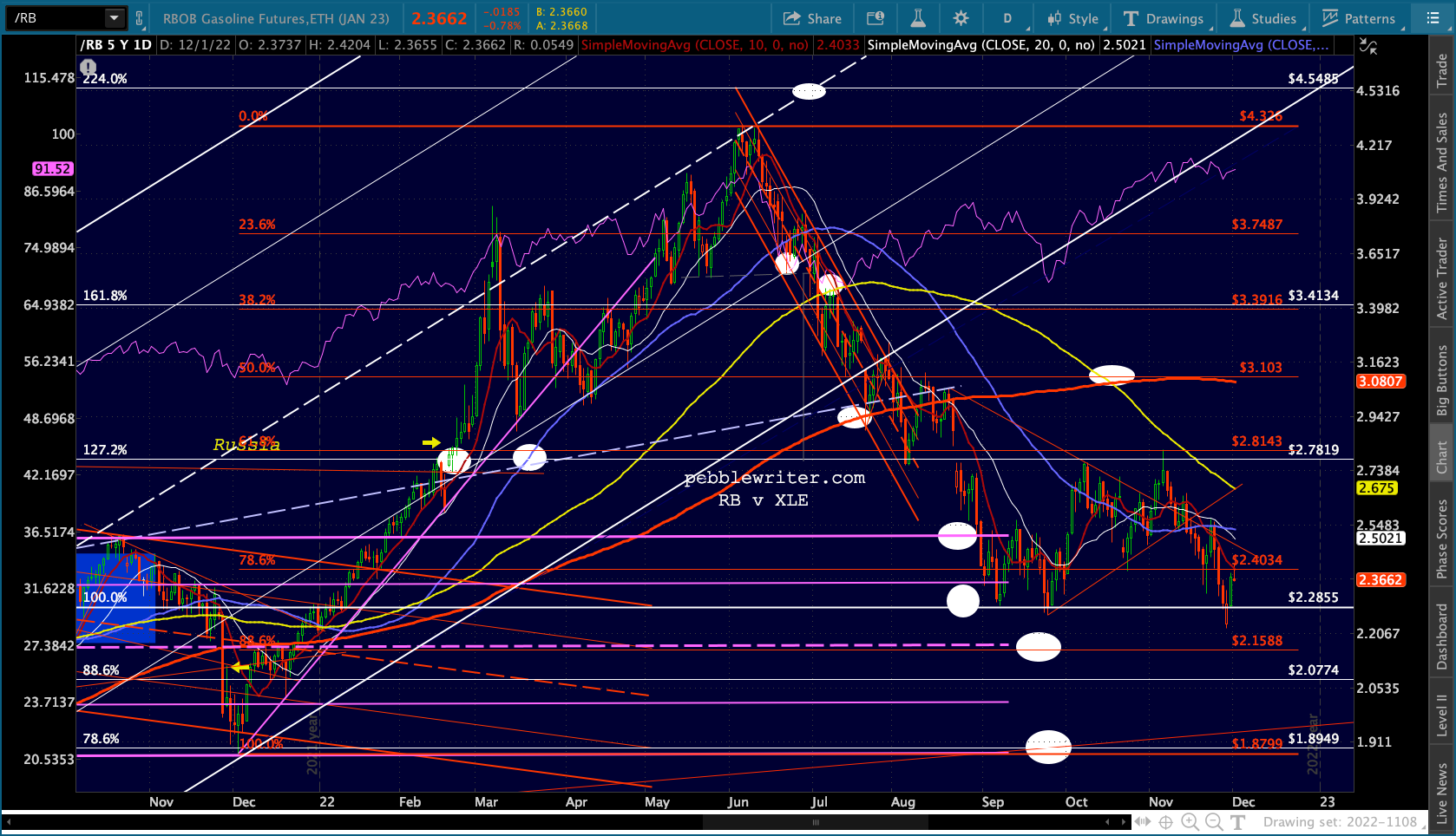

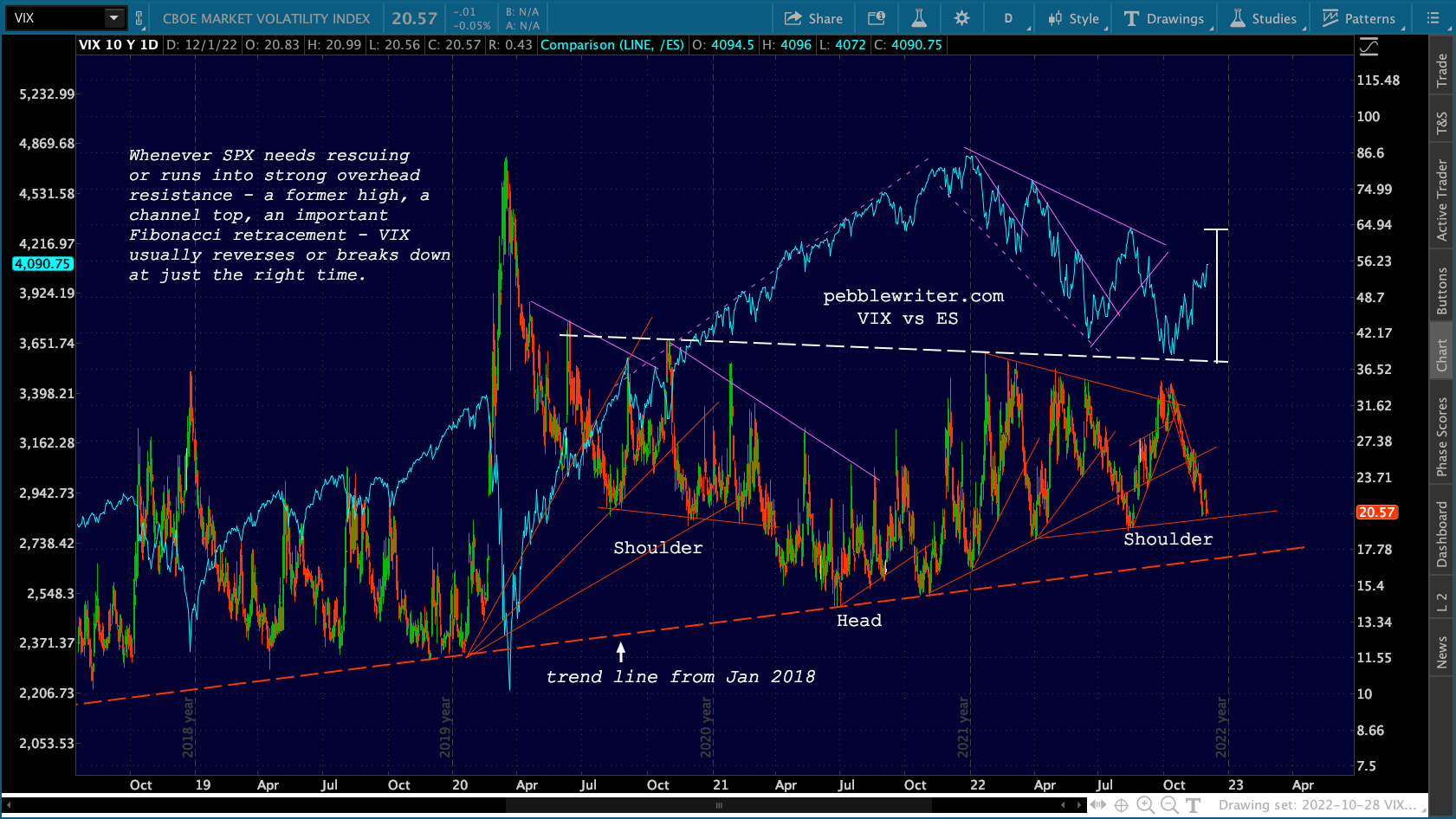

One would expect the exuberance being displayed in currencies and energy to also dissipate intraday if we get a pop and drop. EURUSD remains the most important chart to watch here – with two weeks, now, of backtesting the SMA200.

One would expect the exuberance being displayed in currencies and energy to also dissipate intraday if we get a pop and drop. EURUSD remains the most important chart to watch here – with two weeks, now, of backtesting the SMA200.