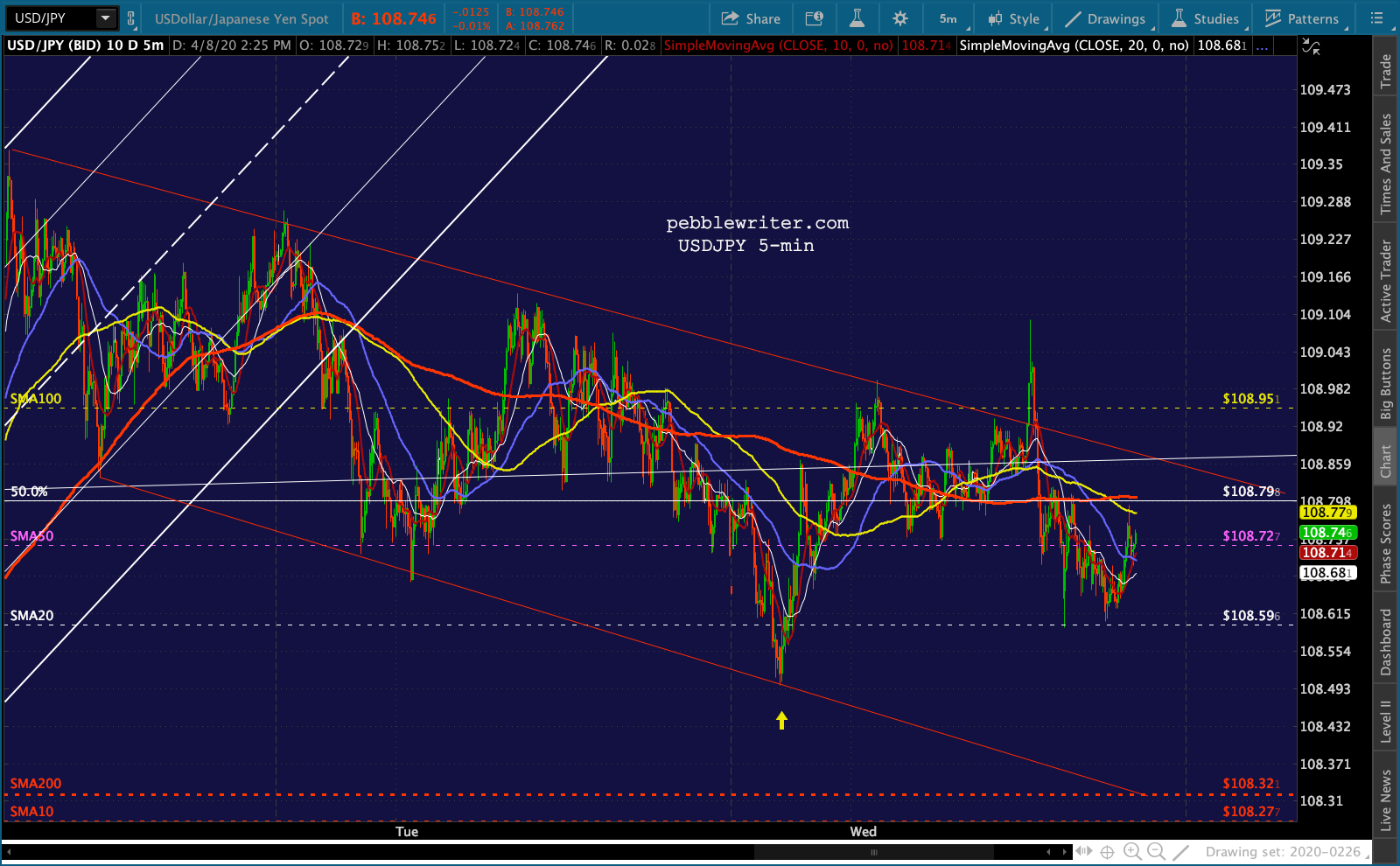

A few days ago, we looked at the outsized influence of oil on algorithms. It’s one of the big three: oil, VIX and USDJPY. This morning, it’s USDJPY’s turn.

Futures, which were down 17 points late last night, are suddenly up 35 points as we approach the opening bell. It happened in the absence of any particular news and without any particular support level having been reached.  It was just USDJPY which, on its way to backtest its SMA200, made a sudden reversal well short of it and went up to test the same overhead TL which has stopped it multiple times since Monday. This time, though, as futures were having a hard time exceeding the overnight highs, it popped through that TL – a breakout that the algos couldn’t ignore.

It was just USDJPY which, on its way to backtest its SMA200, made a sudden reversal well short of it and went up to test the same overhead TL which has stopped it multiple times since Monday. This time, though, as futures were having a hard time exceeding the overnight highs, it popped through that TL – a breakout that the algos couldn’t ignore. Will it be enough to outweigh yesterday’s disappointing reversal of fortune precipitated by oil’s sudden fall from grace?

Will it be enough to outweigh yesterday’s disappointing reversal of fortune precipitated by oil’s sudden fall from grace?

Meanwhile, the “slowdown” in COVID-19 cases and deaths in the US took a turn for the worse yesterday…

Meanwhile, the “slowdown” in COVID-19 cases and deaths in the US took a turn for the worse yesterday…

… as new evidence emerges of the administration’s failure to heed pandemic warnings from Peter Navarro from as early as January 29 even as President Trump and key administration officials were downplaying the risk. Copies of the full memos can be found here.

… as new evidence emerges of the administration’s failure to heed pandemic warnings from Peter Navarro from as early as January 29 even as President Trump and key administration officials were downplaying the risk. Copies of the full memos can be found here.

January 29 memo to the National Security Council, chaired by President Trump:

The February 23 memo addressed directly to the President:

The February 23 memo addressed directly to the President:

ABC reports that US Intelligence officials’ warnings about the virus were first aired in November 2019 and began appearing in the President’s daily briefings in early January.

I suspect this won’t play well in Peoria.

continued for members…

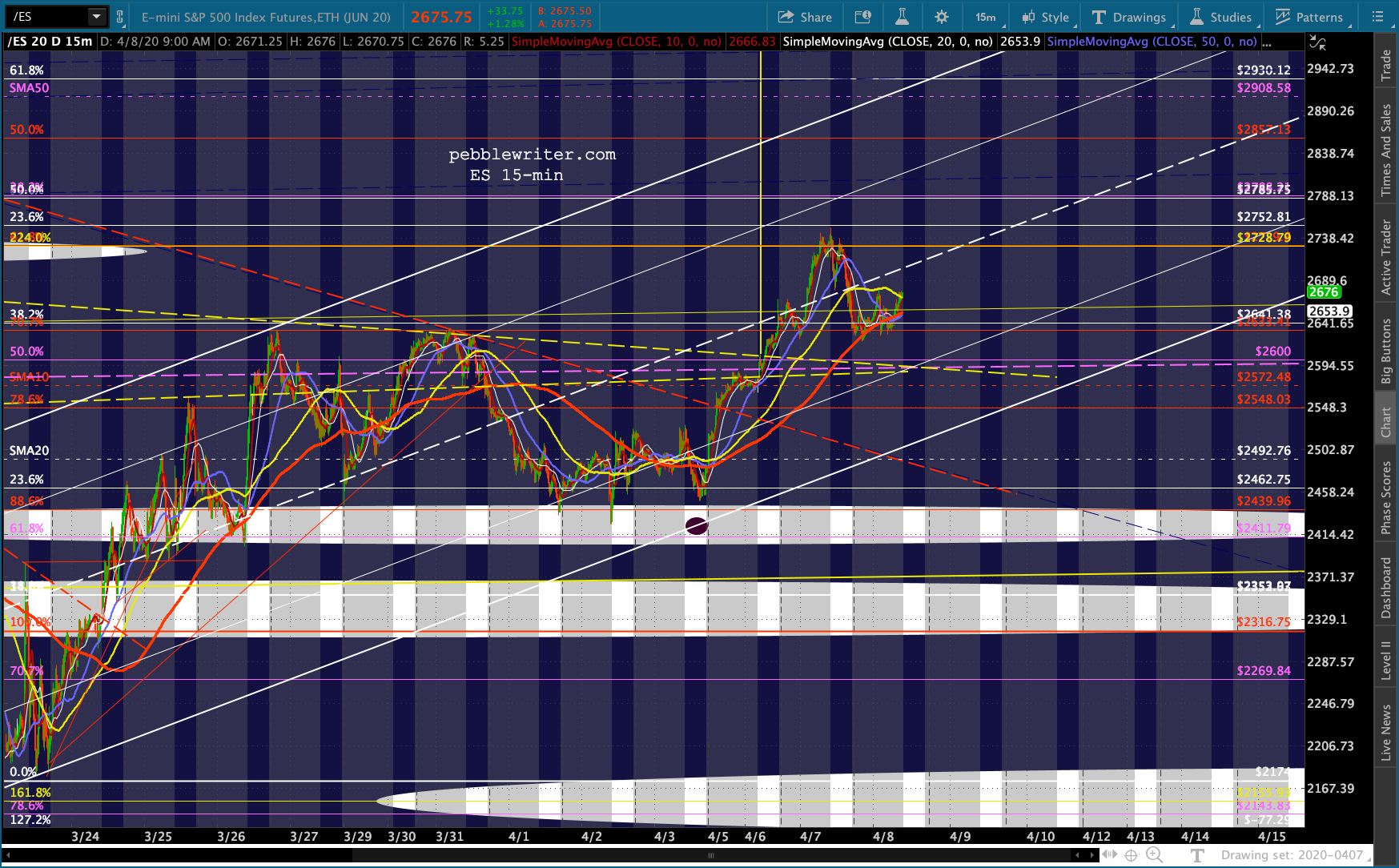

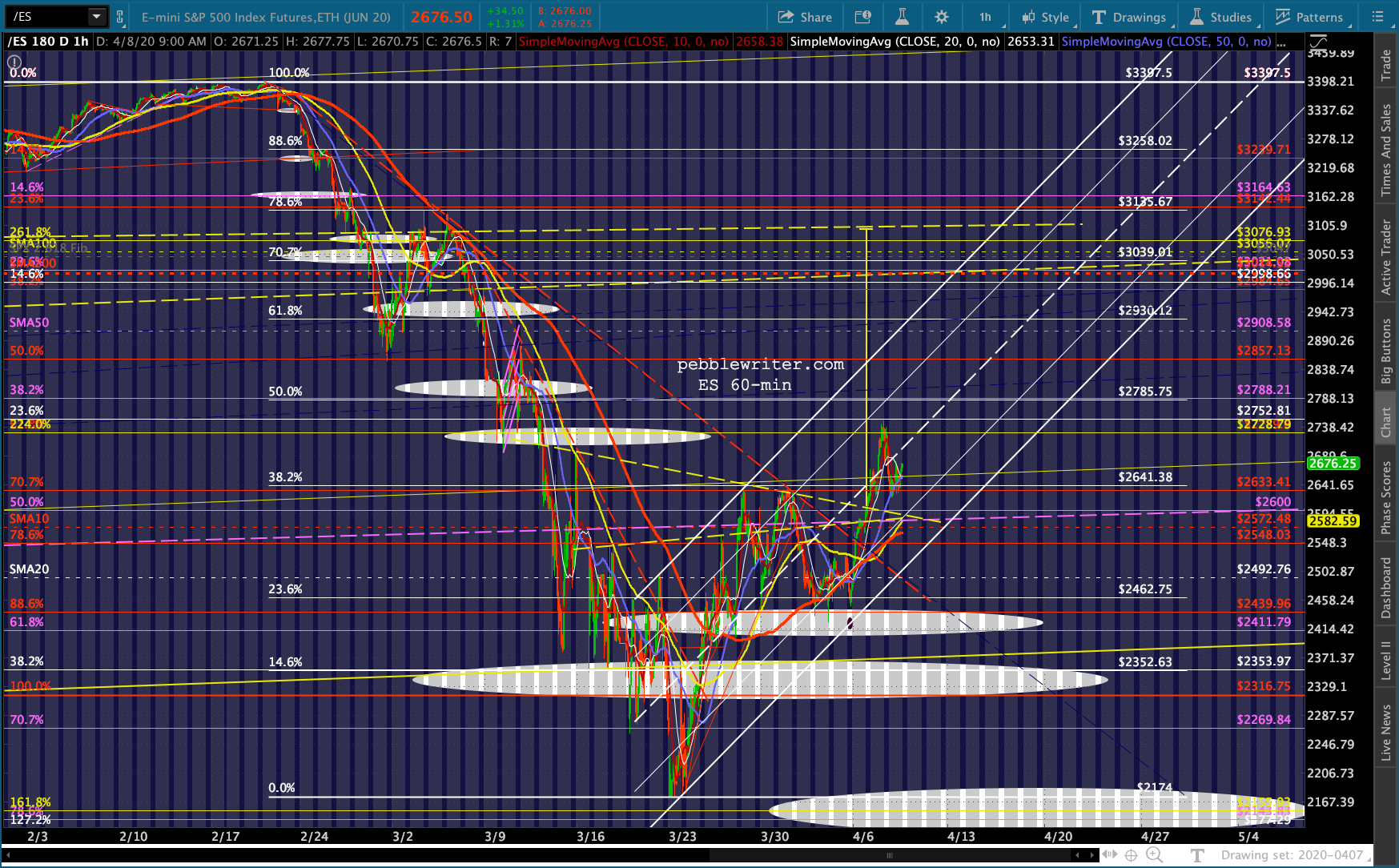

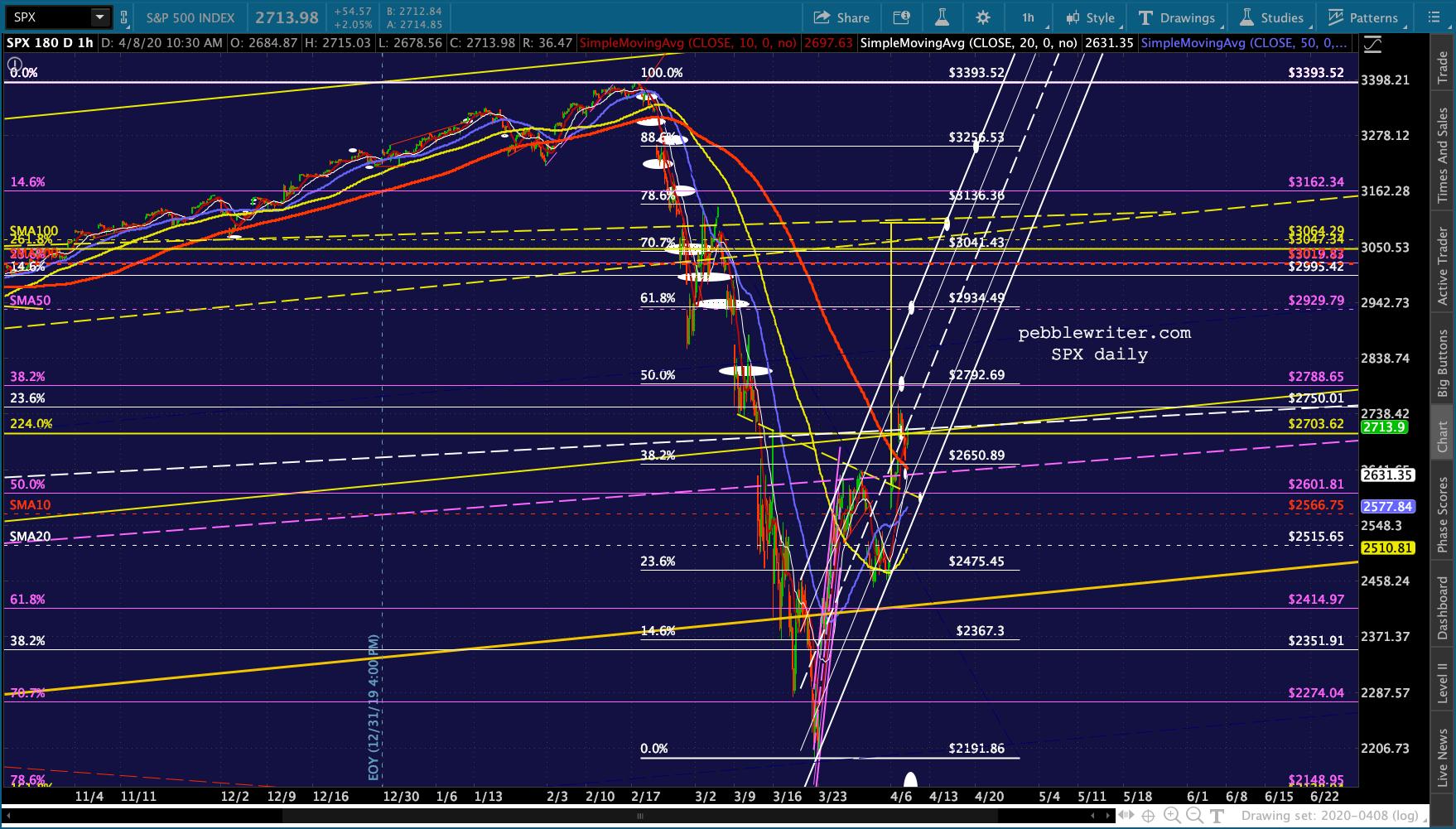

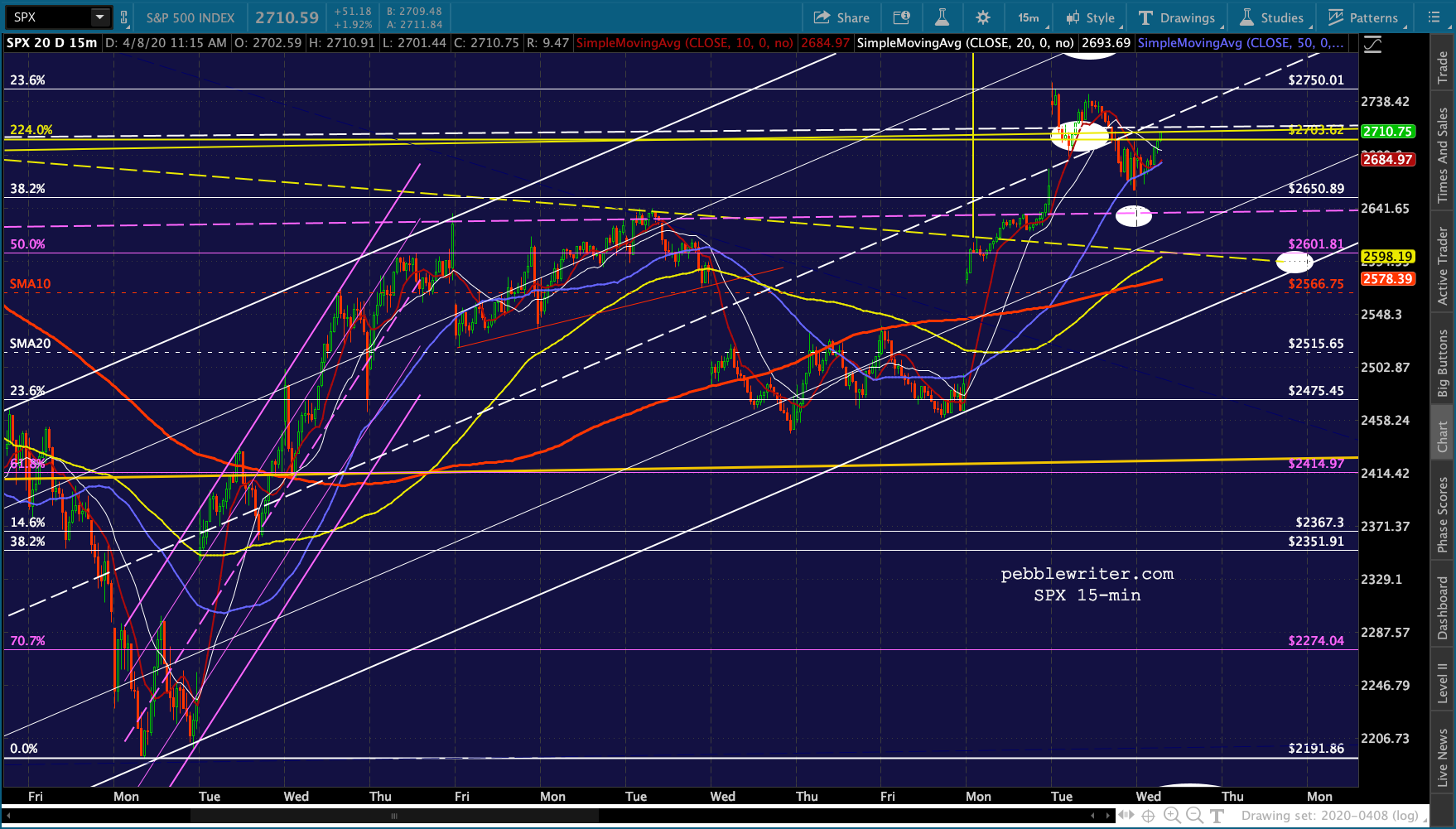

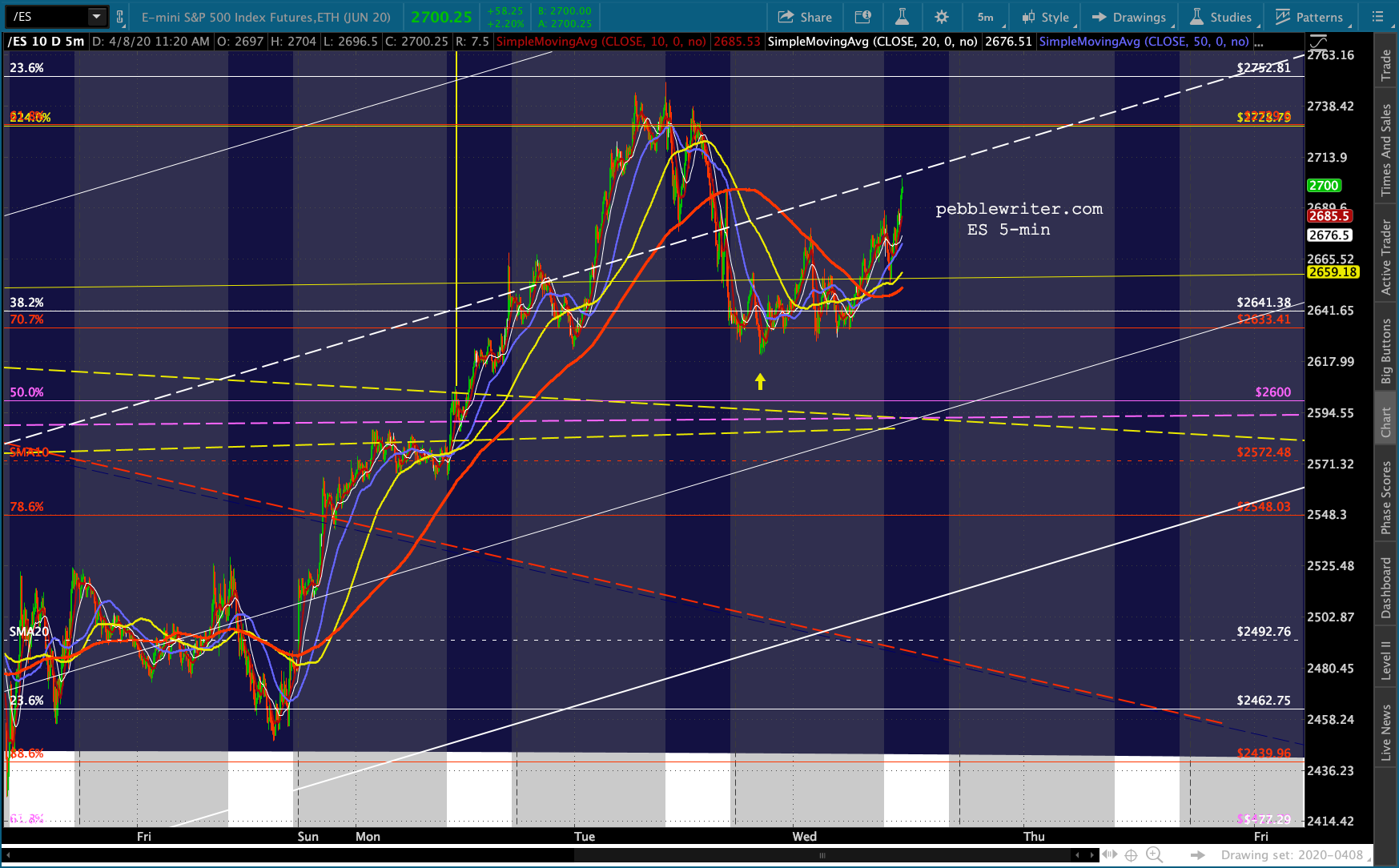

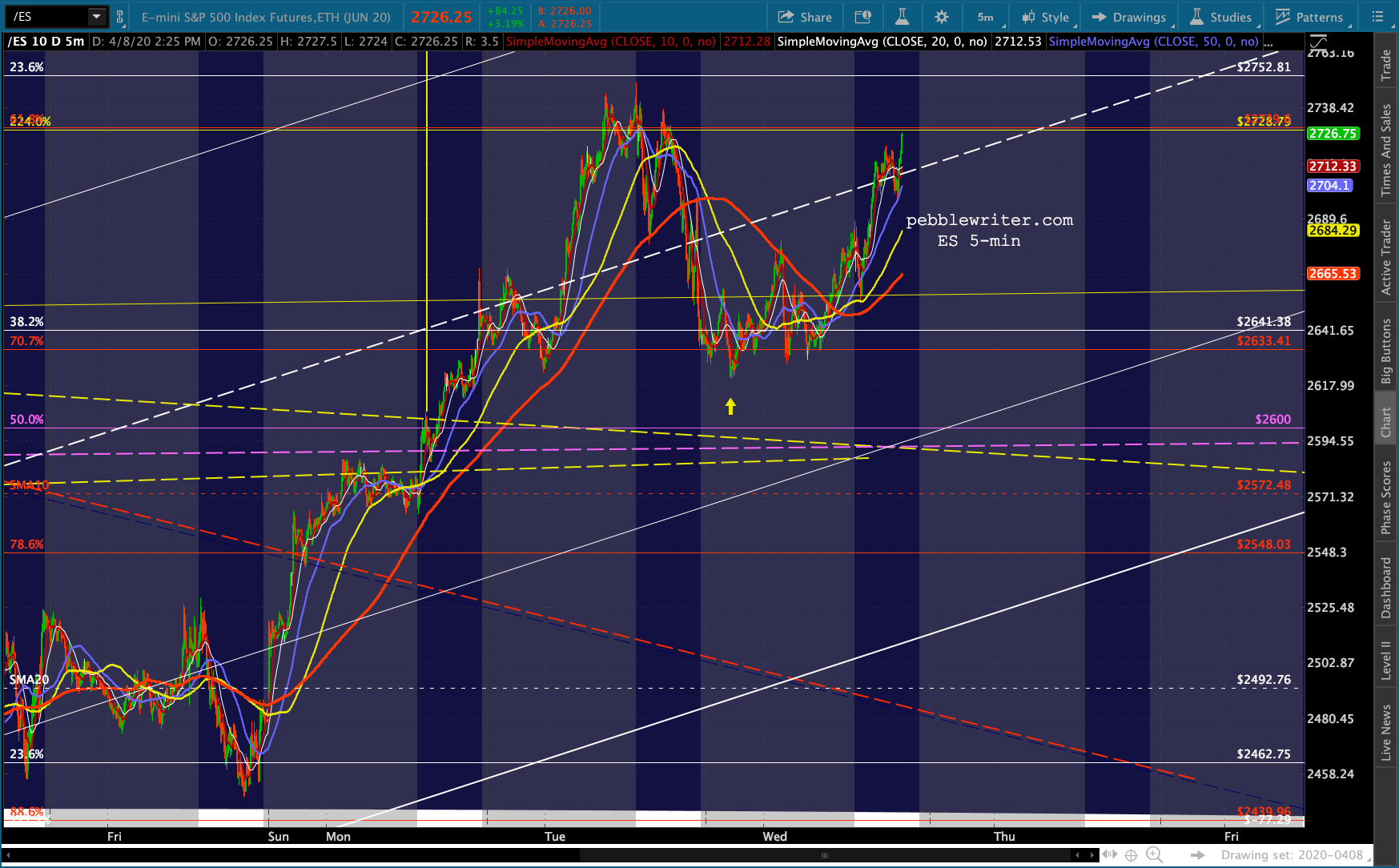

ES still needs a backtest of the yellow neckline and purple TL at about 2595. Depending on when it happens, it might include the SMA10 for the hat trick. Any lower and we’re looking at a channel bottom, currently around 2500. The SMA20 is just below there and rising.

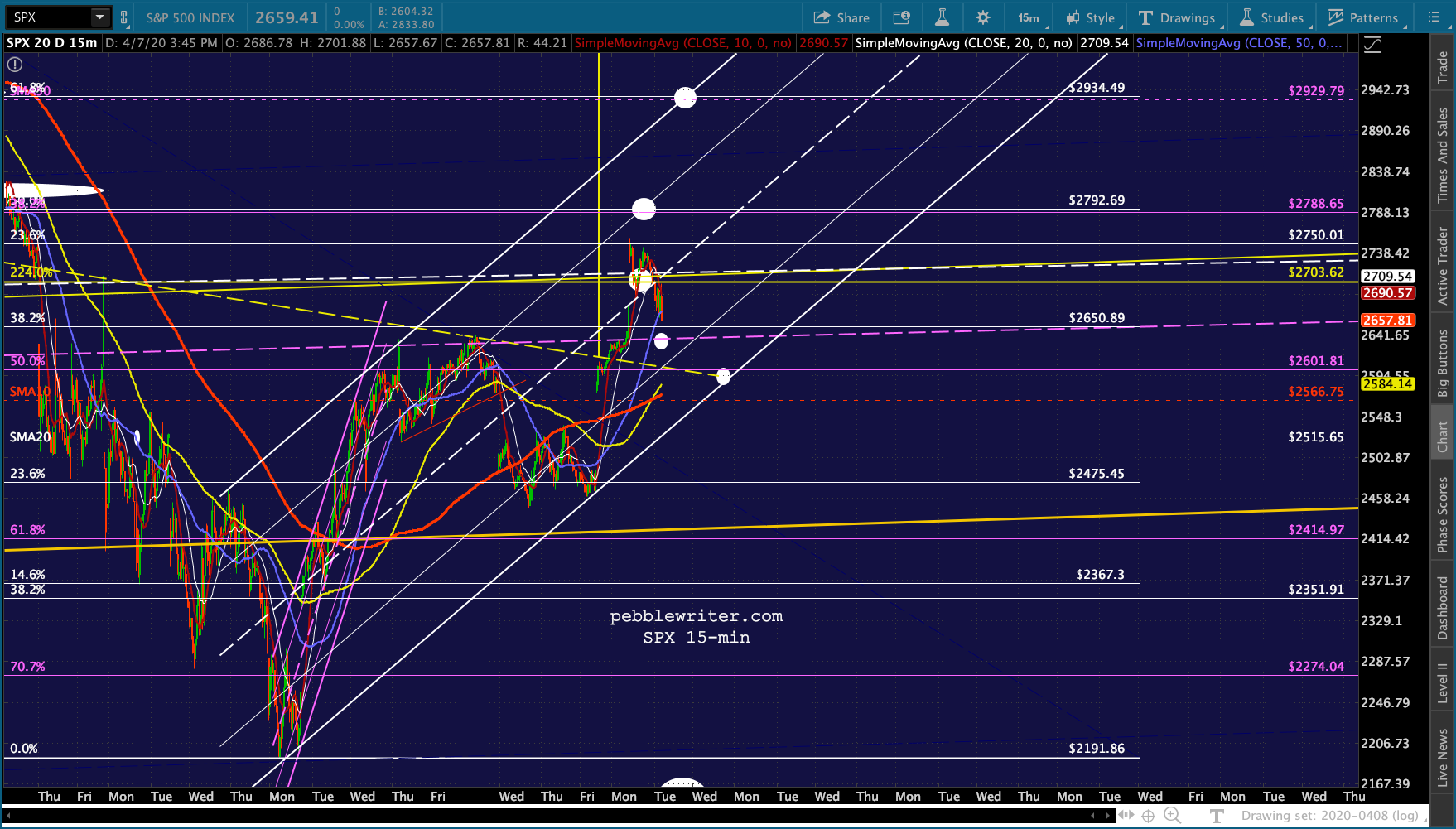

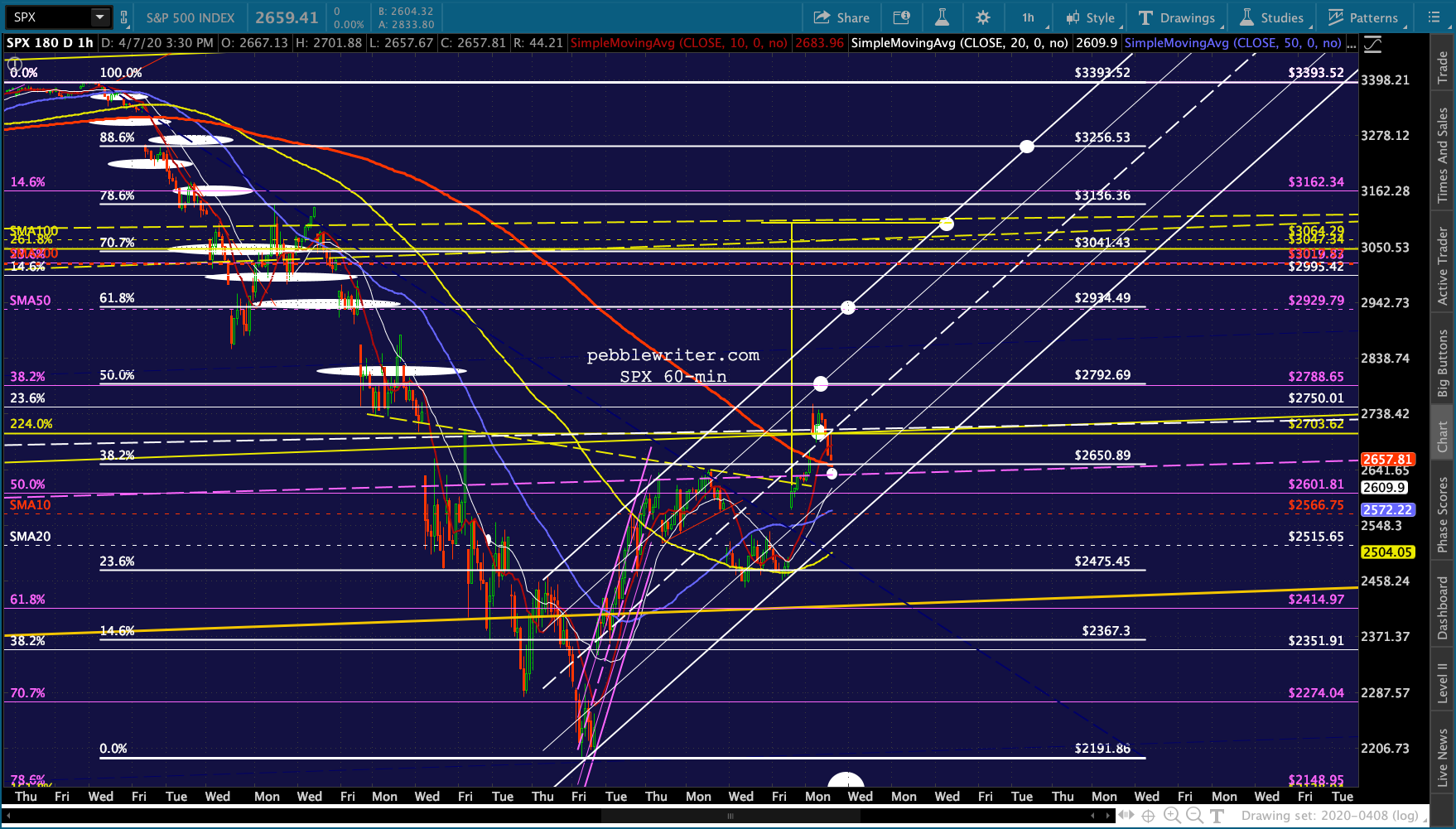

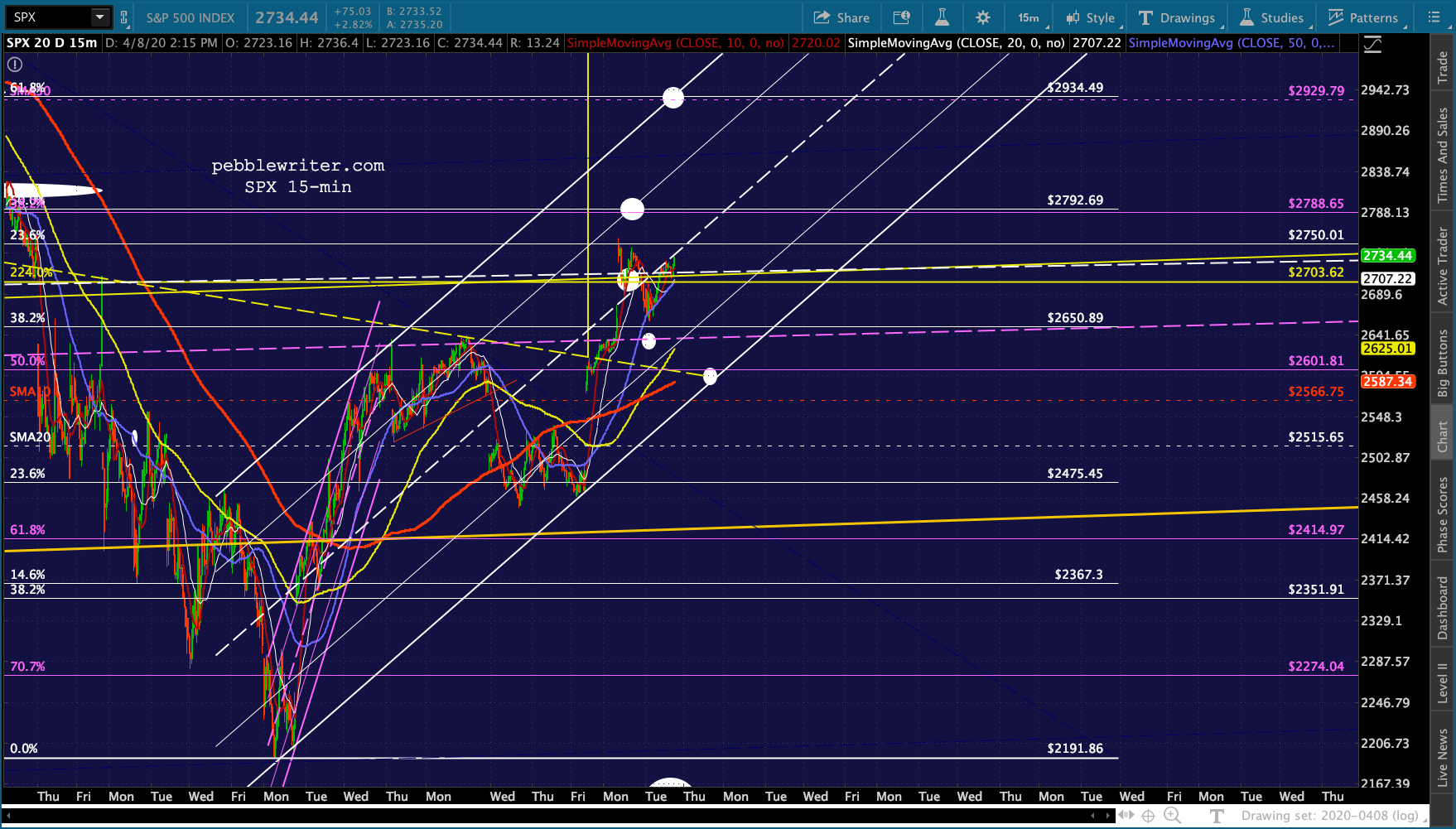

Any lower and we’re looking at a channel bottom, currently around 2500. The SMA20 is just below there and rising.  The SPX version:

The SPX version:

Given how pretty much everything is doing just enough to keep stocks from falling, this continues to feel like a stall rather than a bonafide attempt to push stocks to higher highs.

Given how pretty much everything is doing just enough to keep stocks from falling, this continues to feel like a stall rather than a bonafide attempt to push stocks to higher highs.

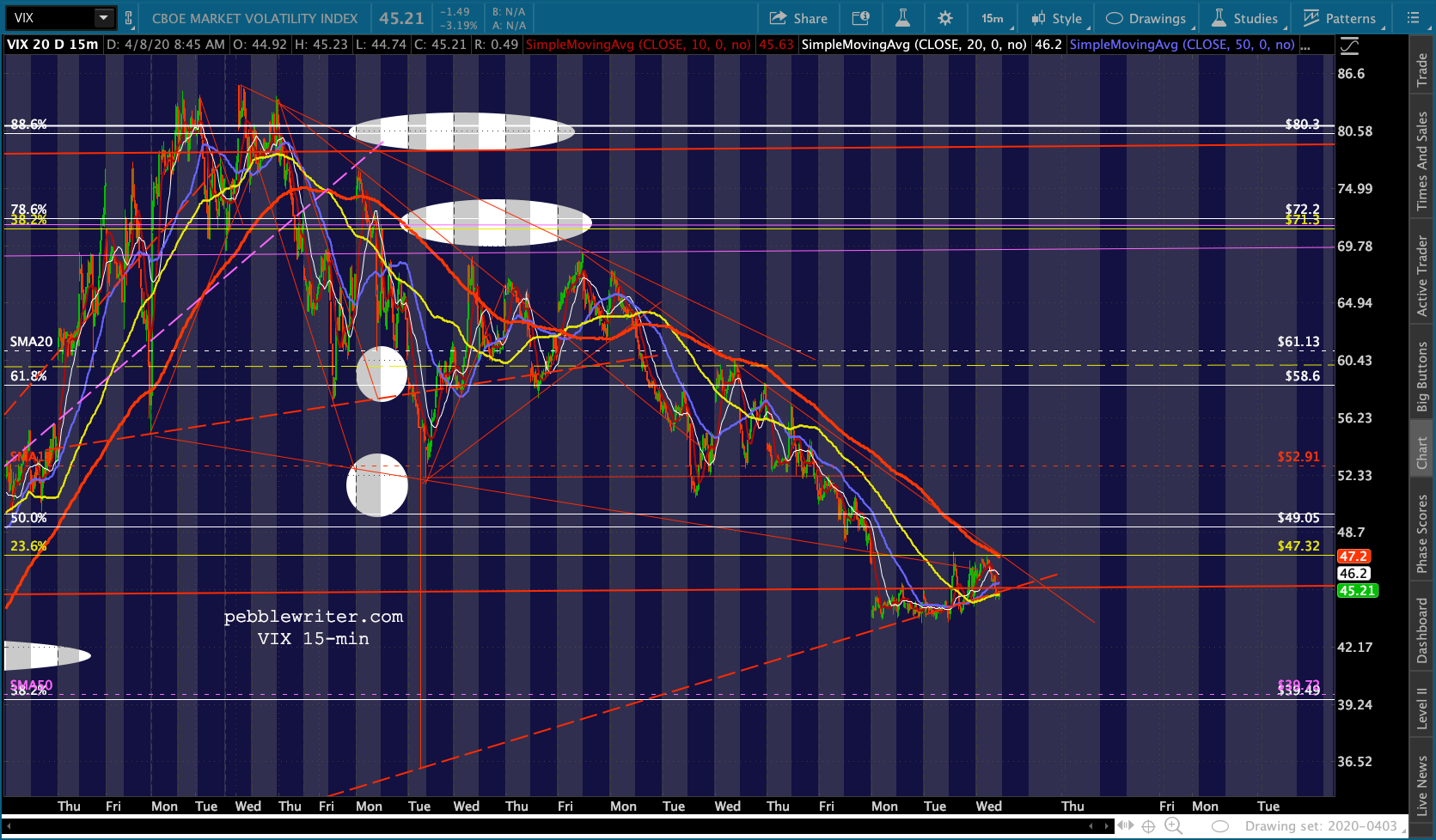

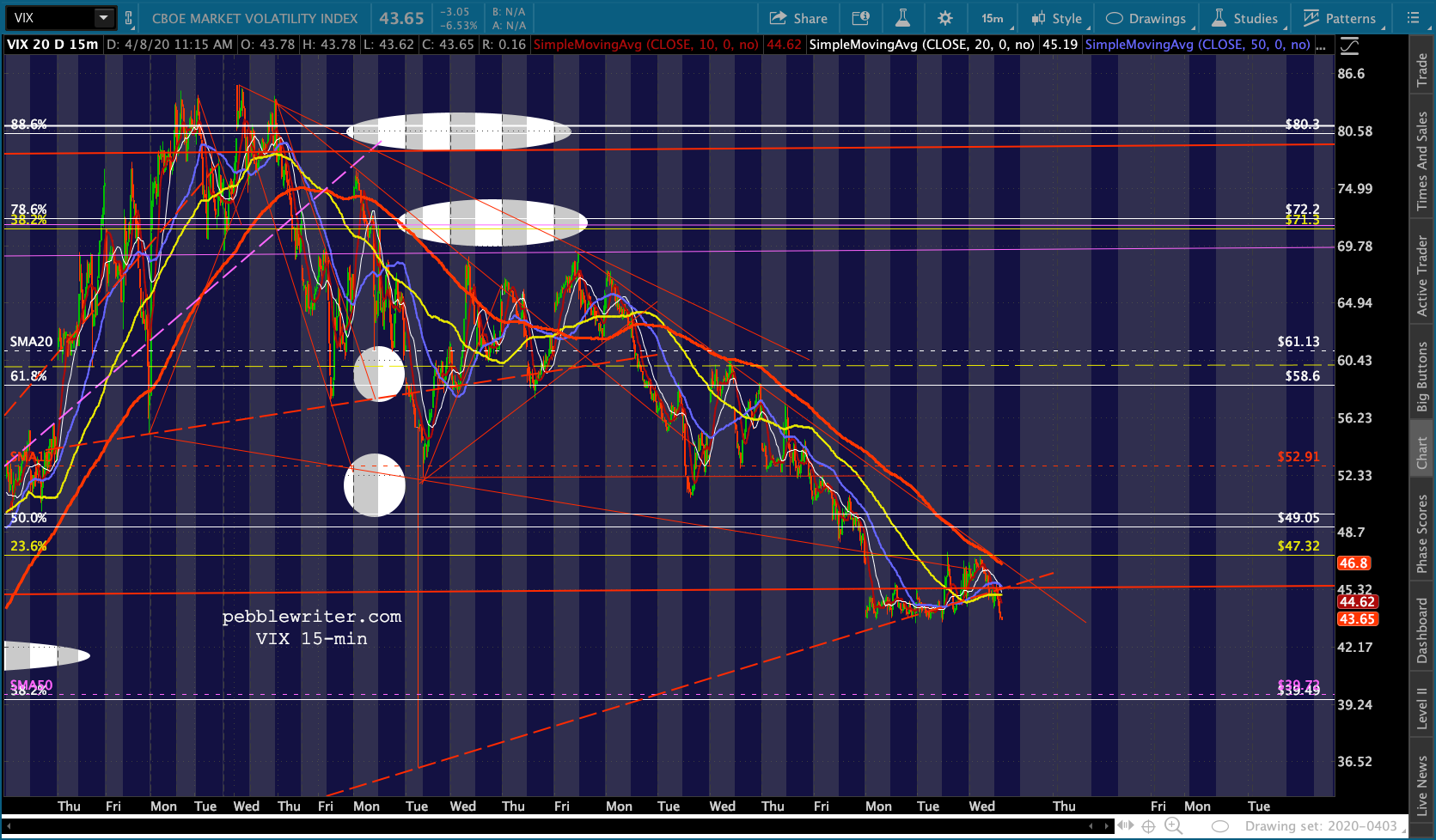

VIX, for instance, has yet to break down – though it has come as close as possible for the past three days.

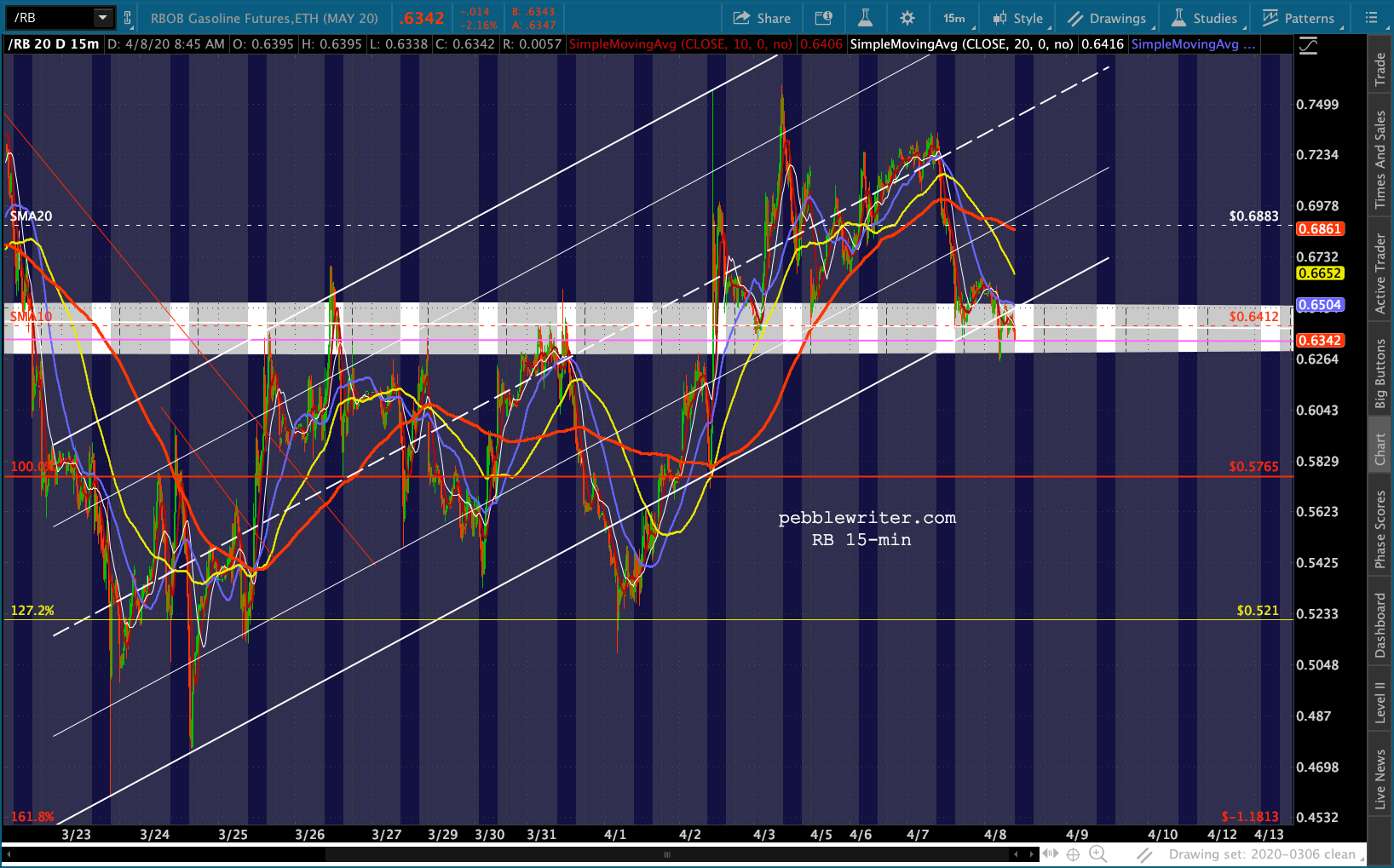

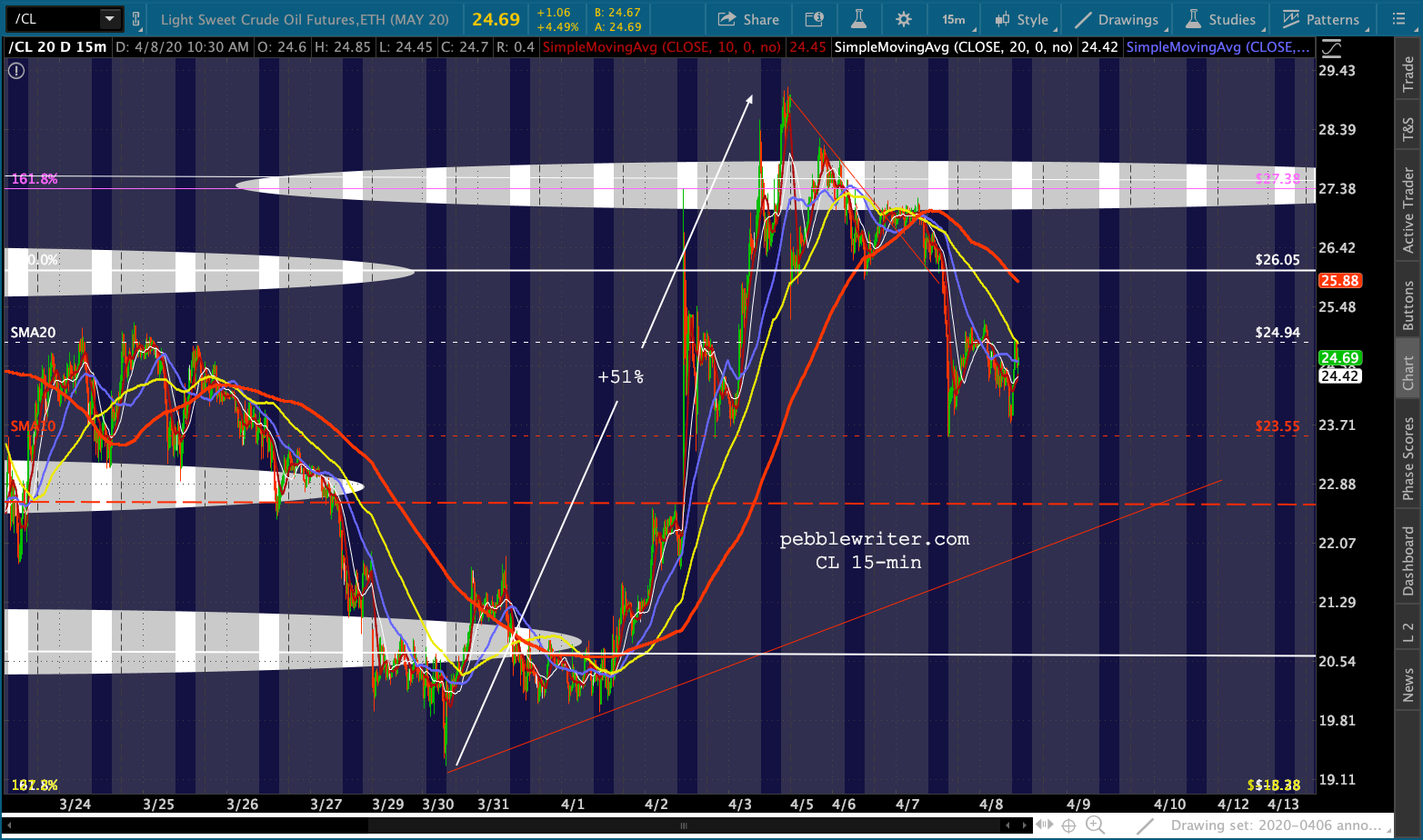

And, like CL, RB looks very weak but is barely managing not to break trend.

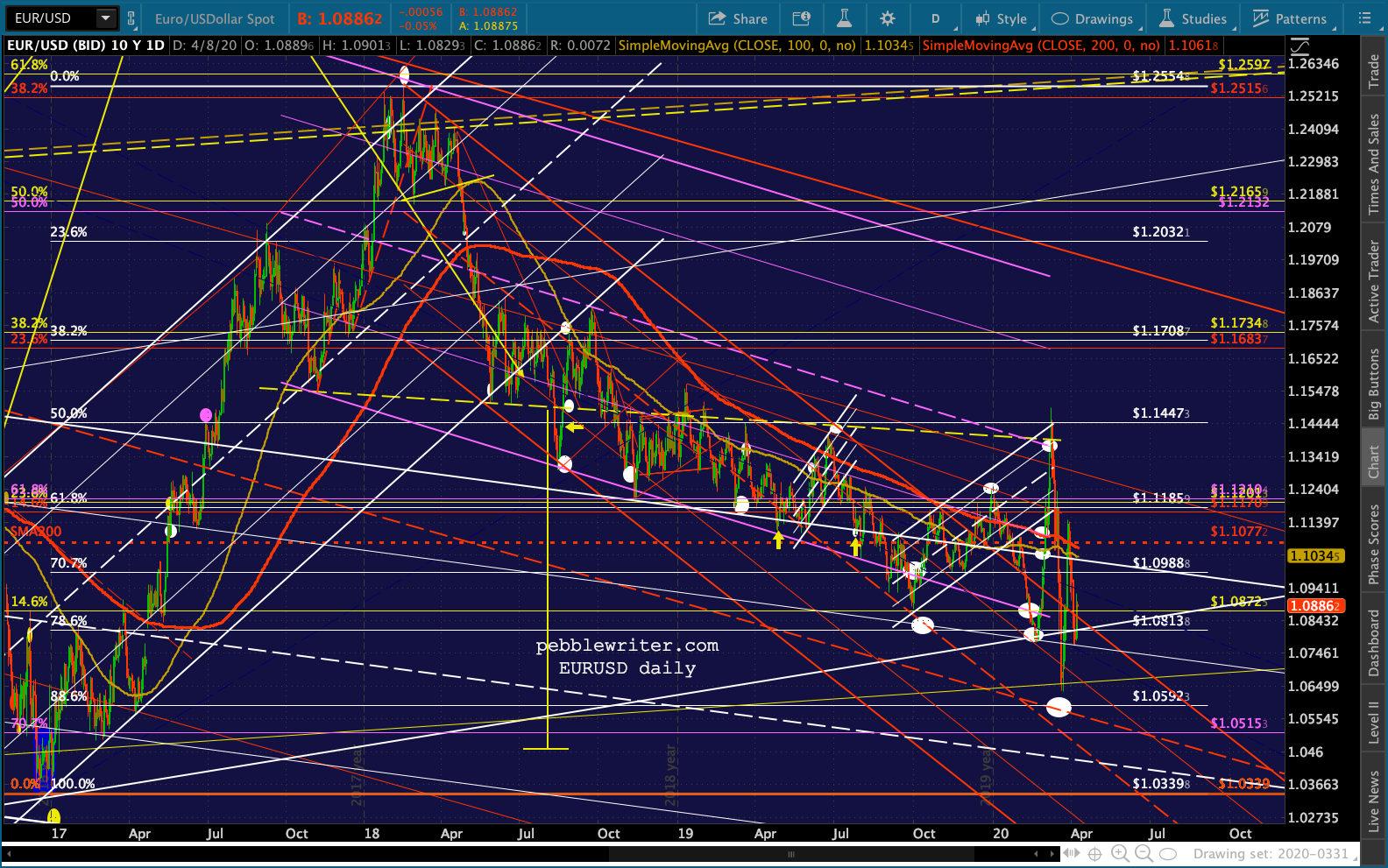

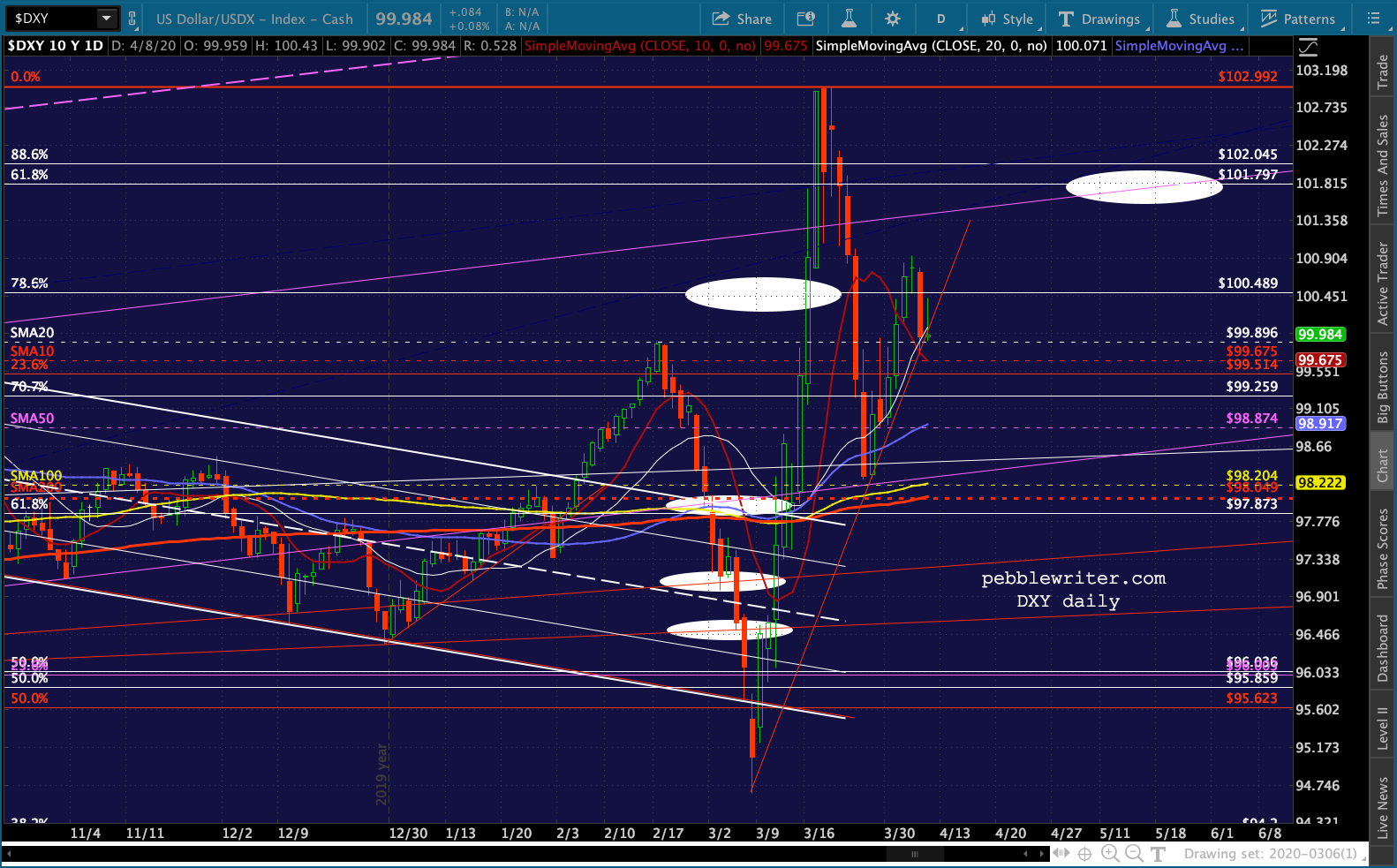

And, like CL, RB looks very weak but is barely managing not to break trend. EURUSD is going nowhere, which leaves DXY still on the brink.

EURUSD is going nowhere, which leaves DXY still on the brink.

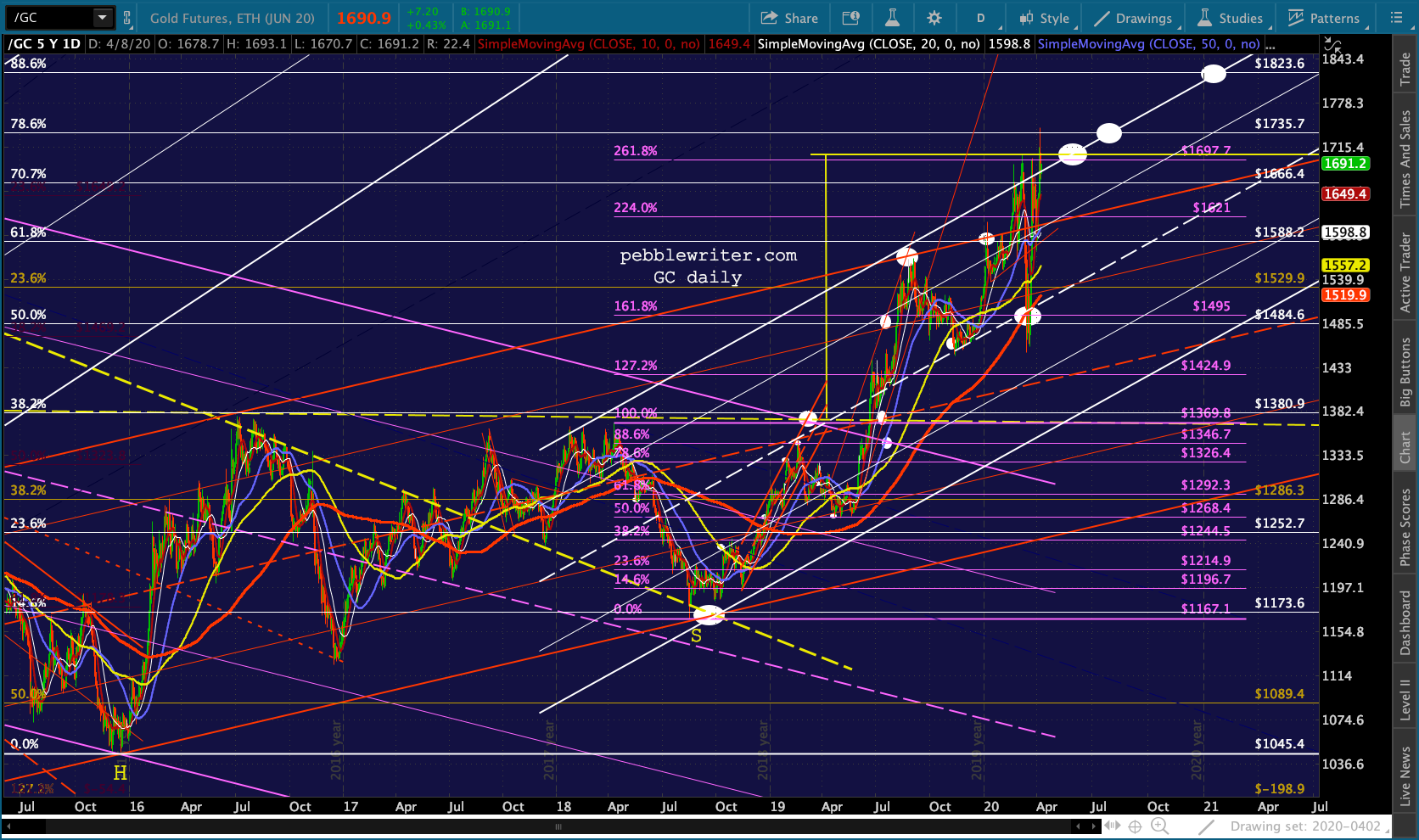

..which resulted in GC making a retreat after tagging our 1735.70 target yesterday (update coming shortly.)

..which resulted in GC making a retreat after tagging our 1735.70 target yesterday (update coming shortly.)

While stalls can take on many forms for many reasons, the two most prominent are because: (a) support in the form of a moving average or other chart feature is arriving on the scene and (b) bad news is coming and a ramp job ahead of that news will allow stocks to fall from a higher level.

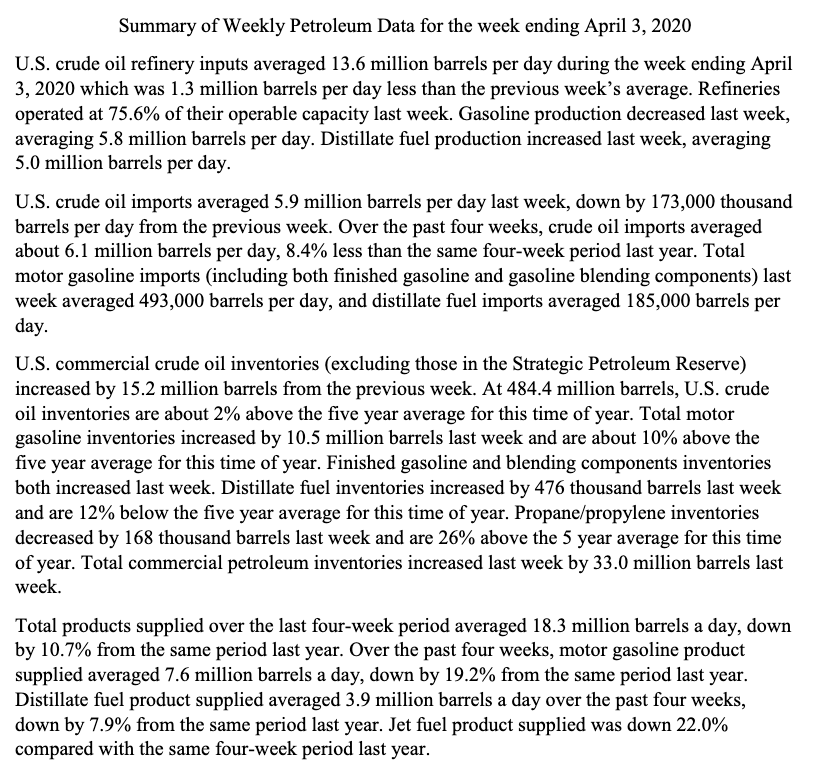

In this case, we have EIA’s inventory report coming out at 10:30 and Fed minutes at 2:00. Both could have consequences. Tomorrow we’ll see PPI, Initial Claims, U of Michigan Consumer Sentiment, and Wholesale Inventories. Again, pretty important stuff under the circumstances.

More later.

UPDATE: 10:31 AM

Massive builds in both oil and gas.

But, expectations were all over the map, so CL and RB aren’t reacting that badly…yet.

But, expectations were all over the map, so CL and RB aren’t reacting that badly…yet.

UPDATE: 11:15 AM

UPDATE: 11:15 AM

Stocks reacted for all of 10-15 seconds… as VIX’s “breakdown” completely offset the underwhelming oil and gas reaction and USDJPY’s reversal of its earlier breakout. Now, as SPX backtests its 2.24 again, we can see that ES is backtesting its channel midline. In other words, it’s VIX against pretty much everything else.

I’ll check back in after the Fed minutes.

Stay tuned.

UPDATE: 2:25 PM

Just read through the minutes – no surprises. Lots of talk about deteriorating economics, frozen markets, etc. We all know what their response was: MMT, or as they call it, a “forceful” policy response.

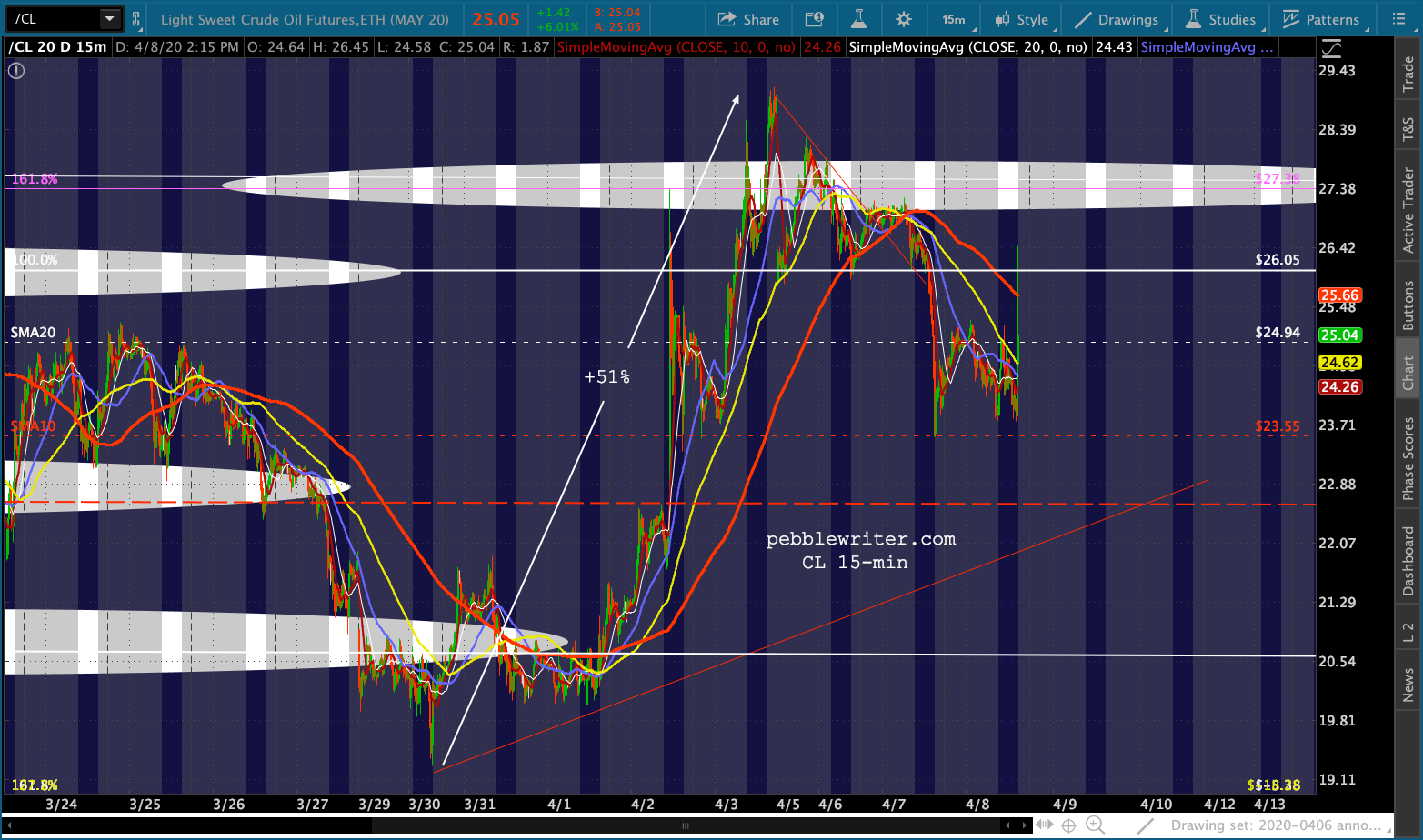

Meanwhile, ES is closing in on its 2.24 as SPX approaches its midline while CL tries out another price spike in advance of tomorrow’s Vienna OPEC talks and USDJPY finds its footing at the SMA20 – at least for now.

If stocks are going to reverse to ES 2590/SPX 2600, this would be the obvious place.

I’ll repeat what I said the other day: a Russia-Saudi deal to cut production by 10-15 million bpd would do very little to address the 25-30 million bpd oversupply.

I’ll repeat what I said the other day: a Russia-Saudi deal to cut production by 10-15 million bpd would do very little to address the 25-30 million bpd oversupply.