Japan’s inflation hit a 40-year high in October, driven by a policy of placing stock market gains above all else.

When Japan first adopted negative interest rates, the argument was that it would help end the country’s deflationary spiral and return inflation to a 2% goal. Now that inflation is nearly twice as high as the goal, one might expect rates to move at least a little higher.

When Japan first adopted negative interest rates, the argument was that it would help end the country’s deflationary spiral and return inflation to a 2% goal. Now that inflation is nearly twice as high as the goal, one might expect rates to move at least a little higher.

Although the BoJ has allowed the 10Y to rise to 0.24%… …they have held short-term rates at -0.1% since 2016.

…they have held short-term rates at -0.1% since 2016. The BoJ’s utter lack of candor is nothing new. Forget about FTX. Japan’s markets are the biggest Ponzi scheme on Earth. Since the Fukushima disaster in 2011, Japan’s stock market has been driven principally by the yen carry trade which relies on an ever-cheaper yen to attract capital into the stock market.

The BoJ’s utter lack of candor is nothing new. Forget about FTX. Japan’s markets are the biggest Ponzi scheme on Earth. Since the Fukushima disaster in 2011, Japan’s stock market has been driven principally by the yen carry trade which relies on an ever-cheaper yen to attract capital into the stock market. The obvious limit to this scheme is that as the yen depreciates, imports become more expensive. And, since Japan imports all of its oil and most of its food, it was simply a matter of time before inflation bit Japan in the お尻.

The obvious limit to this scheme is that as the yen depreciates, imports become more expensive. And, since Japan imports all of its oil and most of its food, it was simply a matter of time before inflation bit Japan in the お尻.

Luckily for Japan, they have no bond market per se. The entirety of Japan’s borrowings are purchased by the BoJ. This monetization of debt has gone on for years without repercussions – until now.

The Nikkei was locked in a falling price channel between Feb 2021 and Mar 2022, when the decline finally reached -20.7%. At that point, it was less than 1% away from its pre-pandemic highs of 24,140. It was no coincidence, then, that USDJPY picked that specific moment to break above both the midline of a channel and a trend line at least 50 years old.

It was no coincidence, then, that USDJPY picked that specific moment to break above both the midline of a channel and a trend line at least 50 years old. Subsequent rises in the USDJPY (declines in the yen) have acted to lift NKD above its SMA200 and out of its falling channel. Everything’s going great – unless you consider rising taxes and plunging consumer confidence problematic.

Subsequent rises in the USDJPY (declines in the yen) have acted to lift NKD above its SMA200 and out of its falling channel. Everything’s going great – unless you consider rising taxes and plunging consumer confidence problematic.

Come to think of it, the US faces similar problems.

* * *

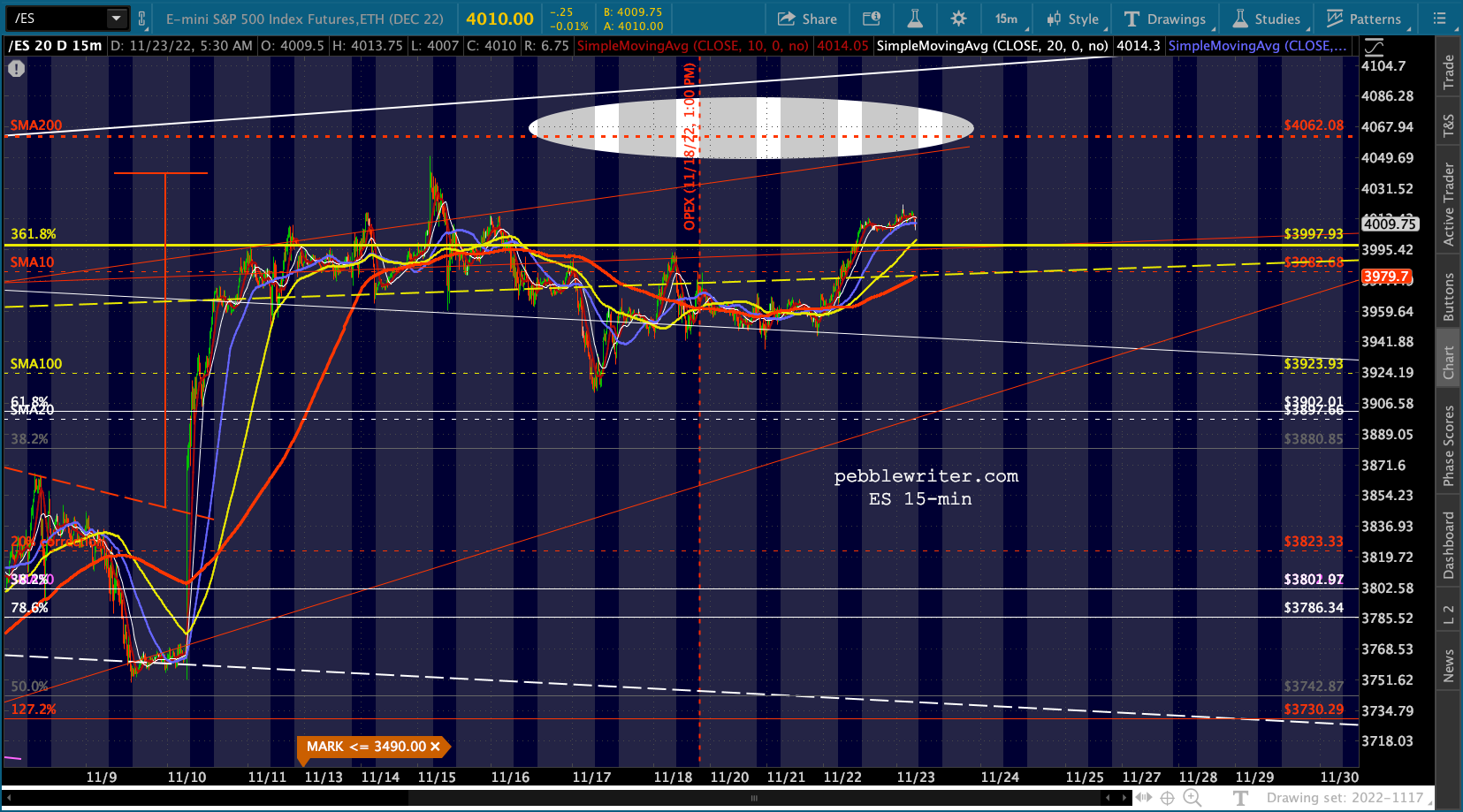

In other news, VIX has sent the all-clear to algos to rally at least a little further – this being OPEX and all. continued for members… (more…)

continued for members… (more…)

Futures are flat after completing the backtest of the trend line from October we had been expecting.

Futures are flat after completing the backtest of the trend line from October we had been expecting.